Europe Microbiology Testing Market Size, Share, Trends & Growth Forecast By Microbiology Application, Clinical Application, Product and Country (Germany, UK, France, Italy, Rest of Europe) – Industry Analysis From 2026 to 2034.

Market Size, 2025

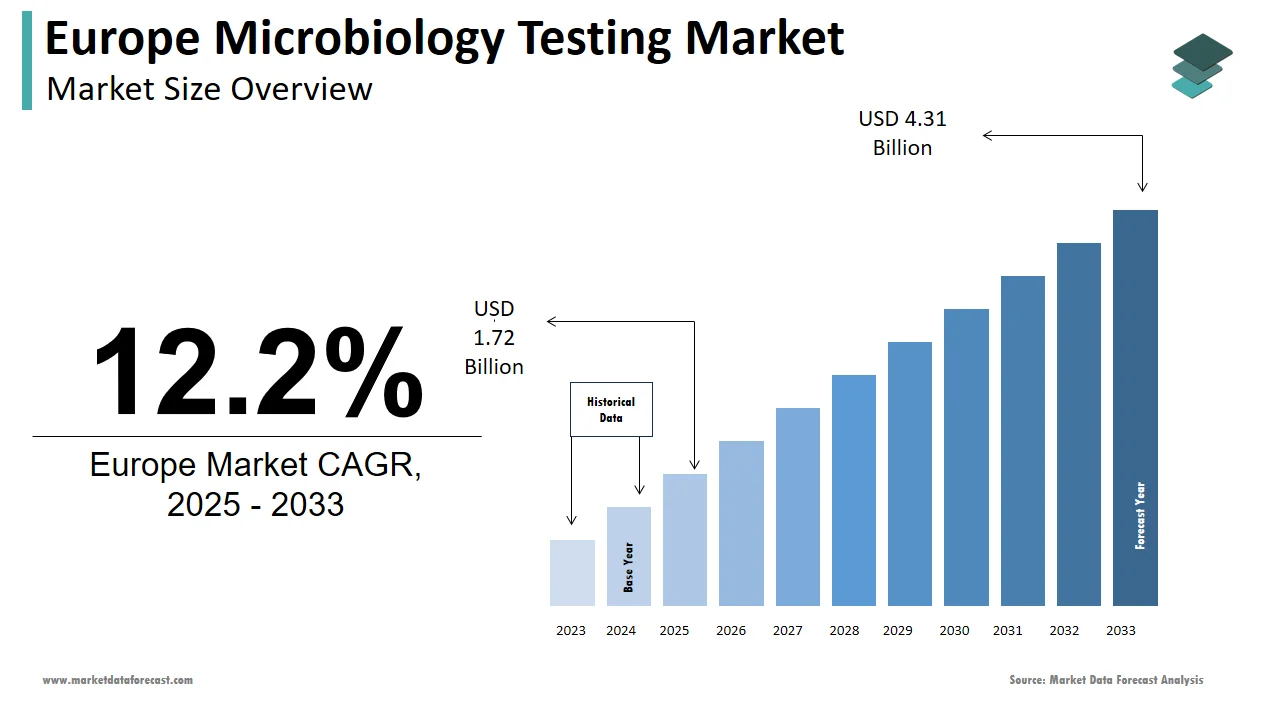

$1.72 BnMarket Estimate, 2026

$1.93 BnMarket Forecast, 2034

$4.85 BnCAGR, 2026–2034

12.2%Europe Microbiology Testing Market Size

The size of the Europe microbiology testing market was valued at USD 1.72 billion in 2025. This market is expected to grow at a CAGR of 12.2% from 2026 to 2034 and be worth USD 4.85 billion by 2034 from USD 1.93 billion in 2026.

Microbiology Testing refers to the analytical methodologies deployed to detect, identify, and quantify microorganisms in clinical, pharmaceutical, food, and environmental matrices. These tests serve as foundational tools for safeguarding public health, ensuring regulatory compliance, and maintaining product safety across multiple sectors. In recent years, the region has experienced a paradigm shift toward rapid, automated, and molecular-based diagnostic platforms, spurred by escalating infectious disease threats and evolving regulatory expectations. According to the European Centre for Disease Prevention and Control, antimicrobial-resistant infections now claim more than 35,000 lives annually in the European Union and European Economic Area. Concurrently, As per the EU Drinking Water Directive, public water systems relied on by the vast majority of EU citizens are legally mandated to undergo regular microbiological monitoring. This confluence of public health imperatives and statutory obligations emphasizes the structural growth and technological transformation of microbiology testing across Europe.

MARKET DRIVERS

Escalating Burden of Healthcare-Associated Infections Fuels Demand for Clinical Microbiology Testing

Healthcare-associated infections remain a formidable challenge within European healthcare systems, which directly intensifies the reliance on advanced clinical microbiology diagnostics and drives the growth of the Europe microbiology market. These infections impose a financial burden annually on healthcare budgets. In this context, rapid microbiological diagnostics have become indispensable for timely pathogen identification and precision antimicrobial therapy. As per the European Society of Clinical Microbiology and Infectious Diseases, molecular assays can reduce diagnostic turnaround time by up to 48 hours compared to traditional culture methods. This acceleration is particularly vital in critical care settings, where sepsis mortality increases when appropriate antibiotics are delayed. Consequently, hospitals across Europe are prioritizing the integration of rapid testing platforms to enhance infection control, improve patient outcomes, and support antimicrobial stewardship initiatives.

Stringent Regulatory Frameworks in the Food and Beverage Sector Mandate Routine Microbial Surveillance

The European Union enforces some of the most comprehensive food safety regulations globally by compelling continuous microbiological monitoring throughout the food supply chain that boosts the expansion of the Europe microbiology testing market. As per the European Food Safety Authority and the European Centre for Disease Prevention and Control, 48,605 individuals were affected by documented foodborne outbreaks in the EU in 2022. Regulation EC No 2073 2005 establishes binding microbiological criteria for food products, which requires manufacturers to conduct regular testing for both pathogens and indicator organisms. Apart from these, the European Commission mandates that all food business operators validate their hazard analysis and critical control point systems through microbial verification. In 2023, the Rapid Alert System for Food and Feed (RASFF) logged 856 notifications concerning pathogenic microorganisms in food, which emphasizes the complexity and vigilance inherent in the sector. Robust demand for microbiology testing services is being sustained by food producers, who are increasingly adopting rapid detection technologies like real-time polymerase chain reaction and enzyme-linked immunosorbent assays to meet compliance deadlines and mitigate recall risks.

MARKET RESTRAINTS

High Capital and Operational Expenditure Constrain Adoption in Small and Mid-Sized Laboratories

The financial burden associated with deploying advanced microbiology testing systems is a significant restraint for the growth of the Europe microbiology testing market. Beyond acquisition costs, recurring expenses for reagents, service contracts, and specialized personnel further inflate the total cost of ownership. As a result, many continue to rely on manual, culture-based techniques that are slower and less sensitive. This technological disparity not only compromises diagnostic reliability but also impedes the harmonization of testing standards across the region, which ultimately limits market penetration despite rising clinical demand.

Fragmented Regulatory Landscape Across European Countries Complicates Standardization

National regulatory divergence continues to hinder the standardization of microbiology testing protocols across member states, which in turn hampers the expansion of the Europe microbiology testing market. According to research, countries such as Germany, France, and Italy maintain distinct validation requirements for microbiological methods used in pharmaceutical quality control, leading to redundant testing and extended product release cycles. Similarly, while Regulation EC No 852 2004 outlines general hygiene rules for food businesses, individual member states apply varying interpretations of microbial limits and sampling frequencies. Inconsistent application of standards is a known cause of discrepancies in interlaboratory test results for microbiological analysis, as per studies. This regulatory fragmentation forces testing providers to maintain multiple compliance frameworks, increasing administrative overhead and operational complexity. Greater alignment among European national authorities is necessary to address the inefficiencies that currently hinder scalability and innovation in the microbiology testing market.

MARKET OPPORTUNITIES

Expansion of Point of Care and Decentralized Testing Platforms Creates New Market Avenues

The proliferation of decentralized diagnostic models is reshaping the accessibility and application of microbiology testing across Europe, which opens potential opportunities for the growth of the Europe microbiology testing market. According to the World Health Organization Regional Office for Europe, the number of point-of-care testing sites in primary care clinics and community pharmacies has grown since 2020, driven by the need for rapid infectious disease screening. Under the EU In Vitro Diagnostic Regulation, molecular point-of-care devices capable of detecting influenza, respiratory syncytial virus, and group A streptococcus within 30 minutes are gaining market authorization. Furthermore, the European Commission has committed a substantial amount to integrating diagnostic data from decentralized platforms into national electronic health records. This convergence of regulatory support, clinical validation, and digital infrastructure is enabling microbiology testing to expand beyond centralized laboratories into ambulatory care, long-term care facilities, and even home-based settings.

Integration of Artificial Intelligence and Predictive Analytics Enhances Test Interpretation and Workflow Efficiency

Artificial intelligence is emerging as a key opportunity for the expansion of the Europe microbiology testing market. This is likely to help in microbiology diagnostics, enhancing data interpretation, resistance prediction, and laboratory automation. According to sources, AI-powered image analysis systems have demonstrated the potential to improve the consistency and accuracy of Gram stain interpretation compared to manual assessment. Advanced diagnostic technologies like MALDI-TOF mass spectrometry have dramatically shortened the time needed for microbial identification, which reduces the time for certain analyses to a matter of hours, and complements or replaces traditional phenotypic confirmation methods. Public repositories like those managed by the European Bioinformatics Institute (EBI) receive large and continuous additions of bacterial genome sequences. For example, a 2024 update to the AllTheBacteria dataset added over 1.2 million bacterial genomes, demonstrating the massive and rapid growth of genomic data available to researchers. Besides, AI-enabled laboratory information systems are optimizing sample routing and instrument utilization. AI-enabled laboratory information systems and AI-assisted workflows are being explored and tested in pilot programs across Europe, including in the Netherlands and Finland, to improve efficiency and increase test throughput. The integration of intelligent analytics presents a high-potential solution for improving diagnostic accuracy and streamlining workflows within European healthcare, which is facing severe workforce shortages and rising test volumes.

MARKET CHALLENGES

Persistent Shortage of Skilled Microbiology Professionals Impedes Test Accuracy and Turnaround

Deficit of qualified microbiology personnel is affecting the growth of the Europe microbiology testing market. According to sources, the EU faces a shortfall of laboratory professionals specializing in infectious disease diagnostics, with vacancies in several Southern and Eastern European countries. The resulting staffing gaps lead to increased workloads, reliance on outdated methods, and elevated error rates. So, this human capital crisis will continue to constrain the effective implementation of advanced testing technologies and compromise public health responses without coordinated investment in education, training pipelines, and retention incentives.

Complexity of Emerging Multidrug-Resistant Pathogens Demands Continuous Test Method Evolution

The rapid evolution of multidrug-resistant microorganisms is outpacing the capabilities of conventional microbiology testing platforms, which challenges the growth of the Europe microbiology market. This necessitates relentless methodological innovation. According to the European Antimicrobial Resistance Surveillance Network, a portion of invasive Klebsiella pneumoniae isolates in 2022 exhibited resistance to third-generation cephalosporins, while carbapenem resistance in Pseudomonas aeruginosa surged in parts of Southern Europe. These resistance mechanisms, often mediated by novel enzymes such as extended-spectrum beta-lactamases and carbapenemases, are frequently undetected by standard phenotypic assays. Consequently, laboratories must continuously update test panels, validate new genetic markers, and recalibrate instruments, placing immense strain on quality assurance resources. This dynamic microbial threat landscape ensures that microbiology testing providers must operate in a state of perpetual adaptation by offering a persistent scientific and operational challenge to maintaining diagnostic accuracy and public health readiness.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Microbiology Application, Clinical Application, Product, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Danaher Corporation, Becton, Dickinson, and Company, Cepheid Abbott Laboratories Inc., Bio-Rad Laboratories Inc., F. Hoffman-La Roche Ltd. (Switzerland), Alere Inc., Bruker Corporation, and Hologic, Inc. |

SEGMENTAL ANALYSIS

By Microbiology Application Insights

In 2024, the clinical segment led the Europe microbiology testing market and occupied 42.5% share of the clinical segment. The growth of the clinical segment is driven primarily by the high volume of diagnostic testing in hospitals and reference laboratories. The persistent burden of infectious diseases across the region is also a key factor supporting this dominance. Furthermore, the European Union’s cross-border health threats initiative has strengthened laboratory networks for pathogen surveillance, further embedding microbiology testing into national healthcare infrastructures. The integration of rapid molecular diagnostics into clinical workflows is another driver of this segment. This shift not only improves antimicrobial stewardship but also aligns with EU antimicrobial resistance action plans that prioritize timely and accurate diagnostics. The clinical segment’s entrenched role in public health response and hospital operations strengthens its dominance in the market.

The pharmaceutical segment is expected to exhibit a noteworthy CAGR of 9.3% from 2025 to 2033. Stringent regulatory mandates and the growth of biologics manufacturing boost the expansion of the pharmaceutical segment in the regional market. According to studies, a portion of new marketing authorization applications for biopharmaceuticals required comprehensive sterility and bioburden testing as part of quality control protocols. The EU Good Manufacturing Practice guidelines explicitly require environmental monitoring and microbial testing at every stage of drug production, especially for aseptic products. Furthermore, the rise in contract development and manufacturing organizations across Ireland, Switzerland, and Germany has intensified demand for outsourced microbiological validation services. These converging regulatory and industrial dynamics are accelerating the adoption of microbiology testing in the pharmaceutical sector.

By Clinical Application Insights

The urinary tract infections segment was the largest in the Europe microbiology testing market and accounted for 38.1% share in 2024. The prominence of the urinary tract infections segment is largely attributed to their high incidence and recurrent nature across all age groups. In primary care settings across Germany, France, and the United Kingdom, UTIs account for a portion of all antimicrobial prescriptions, which necessitates confirmatory culture and susceptibility testing to guide therapy. According to studies, inappropriate empiric treatment of UTIs contributes to rising resistance in Escherichia coli, with resistance to fluoroquinolones exceeding that in several Southern European countries. This resistance trend has intensified the reliance on urine culture and antimicrobial susceptibility testing to avoid treatment failure. Moreover, national guidelines in countries like Sweden and the Netherlands now mandate microbiological confirmation before initiating second-line antibiotics for uncomplicated UTIs. These clinical and antimicrobial stewardship imperatives ensure sustained and high-volume demand for UTI-related microbiology testing across European healthcare systems.

The STD testing segment is predicted to witness the highest CAGR of 10.1% during the forecast period. The rapid expansion of the STD testing segment is fuelled by rising infection rates, expanded screening programs, and the adoption of nucleic acid amplification technologies. According to sources, reported cases of chlamydia, gonorrhea, and syphilis increased. National screening initiatives have significantly contributed to this growth. Furthermore, the European Union’s Joint Action on HIV and STI Prevention has promoted the integration of molecular diagnostics into routine sexual health services. These tests offer superior sensitivity compared to traditional culture methods, particularly for fastidious organisms like Neisseria gonorrhoeae. The convergence of public health policy, technological advancement, and behavioral factors is driving the STD segment.

By Product Insights

The consumables segment captured the largest share of 58.2% of the Europe microbiology testing market. The dominance of the consumables segment is because of the high-throughput nature of diagnostic and quality control testing across clinical, pharmaceutical, and food sectors. Moreover, in the pharmaceutical industry, environmental monitoring programs mandated under EU GMP guidelines necessitate thousands of contact plates, swabs, and broth media units per facility each month. Moreover, the shift toward rapid methods such as chromogenic media and MALDI TOF target plates has increased the value per test, further boosting consumables revenue. The market's economic structure is built on consumables, which provide a steady revenue stream through repetitive use, unlike the capital-intensive and long-lived nature of instruments.

The analyzers segment is estimated to register the fastest CAGR of 11.3% from 2025 to 2033 and is driven by automation, integration, and the need for high-throughput diagnostics. These analyzers, such as VITEK 2 and BD Phoenix, reduce manual labor, minimize human error, and deliver results in half the time of conventional methods. The European Commission’s Digital Europe Programme has further accelerated adoption by funding laboratory digitization projects that link analyzers to electronic health records and antimicrobial stewardship platforms. Besides, the integration of artificial intelligence for pattern recognition in microbial growth curves is enhancing the predictive capabilities of these systems. The market for intelligent, connected analyzers is expanding rapidly, driven by European healthcare systems' struggle with workforce shortages and increasing test volumes.

COUNTRY LEVEL ANALYSIS

Germany Market Analysis

Germany was the top performer in the Europe microbiology testing market and accounted for 22.5% from 2025 to 2033. The domination of Germany in the regional market is attributed to a robust healthcare infrastructure, a dense network of reference laboratories, and a strong pharmaceutical manufacturing base. The country hosts clinical microbiology laboratories, including university-affiliated centers that serve as hubs for infectious disease surveillance. The nation’s prominence in biopharmaceutical production further amplifies demand, with companies requiring stringent microbial testing under EU GMP Annex 1. Furthermore, Germany’s National Antimicrobial Resistance Strategy mandates routine susceptibility testing for all clinically relevant isolates, supporting laboratory testing volumes. Public investment in laboratory modernization. This confluence of clinical, industrial, and policy factors cements Germany’s dominance in the regional market.

United Kingdom Market Analysis

The United Kingdom is moderately expanding in the European microbiology testing landscape, with a centralized public health system and proactive infectious disease surveillance mechanisms. Public Health England, now part of the UK Health Security Agency, operates one of Europe’s most extensive microbiological reference networks, processing a large number of diagnostic samples annually. The National Health Service mandates culture confirmation for all urinary and bloodstream infections before initiating targeted therapy by ensuring consistent test volumes. The integration of microbiology data into the national digital health strategy also enhances test utilization across primary and secondary care. These systemic and strategic initiatives sustain the UK’s strong market position.

France Market Analysis

France is the second-largest and fastest-growing market in the European microbiology testing market. The growth of France is driven by a high burden of infectious diseases and a well-structured public health laboratory system. The French National Reference Centre for Infectious Diseases oversees a network of specialized laboratories that perform over 8 million microbiological analyses each year. The country’s pharmaceutical sector, home to global players like Sanofi, also contributes significantly, with manufacturing facilities adhering to strict EU microbial quality standards. Apart from these, France leads in antimicrobial stewardship, with mandatory susceptibility testing required for all hospital-acquired infections under national guidelines. These clinical, industrial, and policy drivers ensure France’s continued prominence in the market.

Italy Market Analysis

Italy is gradually in the European microbiology testing market owing to regional disparities in healthcare access and a high prevalence of antimicrobial-resistant infections. According to studies, Southern regions report carbapenem-resistant Klebsiella pneumoniae rates exceeding, among the highest in Europe, driving intensive diagnostic efforts. The country operates hospital-based microbiology labs, though modernization levels vary significantly between the North and South. Nevertheless, national initiatives have standardized testing protocols and expanded rapid diagnostics for bloodstream and urinary infections. Italy’s pharmaceutical industry, with many manufacturing sites, also mandates routine environmental and sterility testing under EU regulations. These efforts to bridge regional gaps and combat resistance are strengthening Italy’s market relevance.

Switzerland Market Analysis

Switzerland is predicted to grow in the European microbiology testing market during the forecast period due to its concentration of global pharmaceutical and diagnostics companies. Home to Roche Diagnostics and Novartis, the country serves as a hub for both test development and high-end manufacturing quality control. The Swiss Federal Office of Public Health mandates comprehensive microbial monitoring in all hospitals. Switzerland also leads in adopting next-generation diagnostics. Besides, the country’s high per capita healthcare expenditure supports investment in premium testing platforms. This unique blend of industrial dominance, regulatory rigor, and healthcare sophistication emphasizes Switzerland’s outsized market influence.

COMPETITIVE LANDSCAPE

The Europe Microbiology Testing Market features intense competition among global leaders and specialized regional players striving to address diverse sectoral demands. Companies differentiate themselves through technological sophistication, regulatory compliance, and service depth rather than price alone. Clinical diagnostics is dominated by firms offering integrated identification and susceptibility platforms, while the pharmaceutical segment favors providers with GMP-certified consumables and rapid methods. The implementation of the EU In Vitro Diagnostic Regulation has raised entry barriers, compelling smaller entities to seek partnerships or exit. Simultaneously, large corporations are acquiring niche innovators to broaden their portfolios in molecular and point-of-care testing. National health policie,s antimicrobial resistance initiatives, and manufacturing quality mandates further shape competitive dynamics.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe microbiology testing market include

- Danaher Corporation

- Becton, Dickinson and Company

- Cepheid

- Abbott Laboratories Inc.

- Bio-Rad Laboratories Inc.

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Alere Inc.

- Bruker Corporation

- Hologic, Inc.

Top Players in the Market

- Thermo Fisher Scientific is a pivotal contributor to the Europe Microbiology Testing Market through its comprehensive portfolio of culture media, rapid detection systems, and molecular diagnostic platforms. The company supplies clinical and pharmaceutical laboratories across the region with advanced solutions such as the BacT Alert blood culture system and chromogenic agar formulations. These initiatives support its commitment to regulatory compliance and timely delivery, aligning with EU Good Manufacturing Practice and In Vitro Diagnostic Regulation requirements to better serve regional customers.

- BioMérieux holds a distinguished position in European clinical microbiology by delivering innovative diagnostic solutions focused on infectious disease management and antimicrobial resistance. The company’s VITEK and BioFire platforms are widely adopted in hospitals for rapid pathogen identification and syndromic testing. These strategic moves enhance its capacity to meet rising demand for fast and accurate diagnostics across European healthcare systems.

- Merck KGaA plays a vital role in the Europe Microbiology Testing Market by providing high-quality culture media, sterility testing kits, and environmental monitoring solutions primarily for the pharmaceutical and biotechnology sectors. Merck recently upgraded its manufacturing site in Darmstadt, Germany, to increase production of certified consumables and launched a digital platform enabling real-time tracking of media sterility validation. These actions demonstrate its focus on quality assurance and digital integration to meet evolving regulatory and operational needs in European manufacturing environments.

Top Strategies Used by the Key Market Participants

Key players in the Europe Microbiology Testing Market employ several strategic approaches to support their competitive standing. Product innovation remains central, with companies consistently launching advanced rapid detection systems and automated platforms aligned with EU regulatory standards. Strategic partnerships with public health agencies and academic institutions facilitate co-development of diagnostic assays and real-world validation. Geographic expansion through localized manufacturing and distribution hubs ensures supply chain resilience and faster customer response. Companies also invest heavily in digital integration by linking analyzers to laboratory information systems and antimicrobial stewardship platforms. Furthermore, regulatory preparedness is prioritized through proactive compliance with the EU In Vitro Diagnostic Regulation and Good Manufacturing Practice guidelines to maintain uninterrupted market access and customer trust.

MARKET SEGMENTATION

This Europe microbiology testing market research report is segmented and sub-segmented into the following categories.

By Microbiology Application

- Pharmaceutical

- Clinical

- Manufacturing

- Energy

By Clinical Application

- Respiratory Diseases

- STD

- UTI

By Product

- instruments

- Analyzers

- Consumables

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe Microbiology Testing Market and what drives its growth?

The Europe Microbiology Testing Market involves diagnostic testing for microorganisms causing disease, including advanced molecular techniques like PCR and NGS. Growth is driven by rising infectious diseases, antimicrobial resistance concerns, and demand for rapid, precise testing

2. Which technological advancements are impacting the Europe Microbiology Testing Market?

Advanced molecular diagnostics, real-time PCR, next-generation sequencing, and automated instrumentation improve detection specificity and speed

3. What are the key microbiology test types used in Europe?

Bacterial, viral, fungal identification tests, antimicrobial susceptibility testing, and molecular screening dominate the market

4. Which clinical applications drive demand in the Europe Microbiology Testing Market?

Applications include respiratory diseases, bloodstream infections, gastrointestinal illnesses, sexually transmitted infections, and urinary tract infections

5. What are the main end users of microbiology testing services in Europe?

Hospitals, diagnostic centers, research institutes, and pharmaceutical companies are major end users

6. Which countries lead the Europe Microbiology Testing Market?

Germany, the UK, France, Italy, and Spain hold major market shares, backed by developed healthcare infrastructure and strong R&D

7. How does antimicrobial resistance (AMR) affect the Europe Microbiology Testing Market?

AMR accelerates demand for rapid susceptibility testing to guide effective antimicrobial therapies and control resistant infections

8. How important is automated microbiology testing in Europe?

Automation enhances accuracy, reduces turnaround times, and increases lab productivity, boosting adoption

9. What role do diagnostics reagent and kit manufacturers play?

They supply targeted kits and reagents critical for detecting specific pathogens with high sensitivity and fast processing

10. What challenges impact the Europe Microbiology Testing Market?

Regulatory complexity, cost constraints, and the need for specialized technical skills pose challenges

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com