Global Microbiology Testing Market (Clinical Microbiology Market) Size, Share, Trends & Growth Forecast Report By Product (Instruments and Reagents), Application (Pharmaceutical, Clinical, Food Testing, Energy, Chemical and Material Manufacturing and Environmental), Disease Area and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis From 2025 to 2033

Global Microbiology Testing Market Size

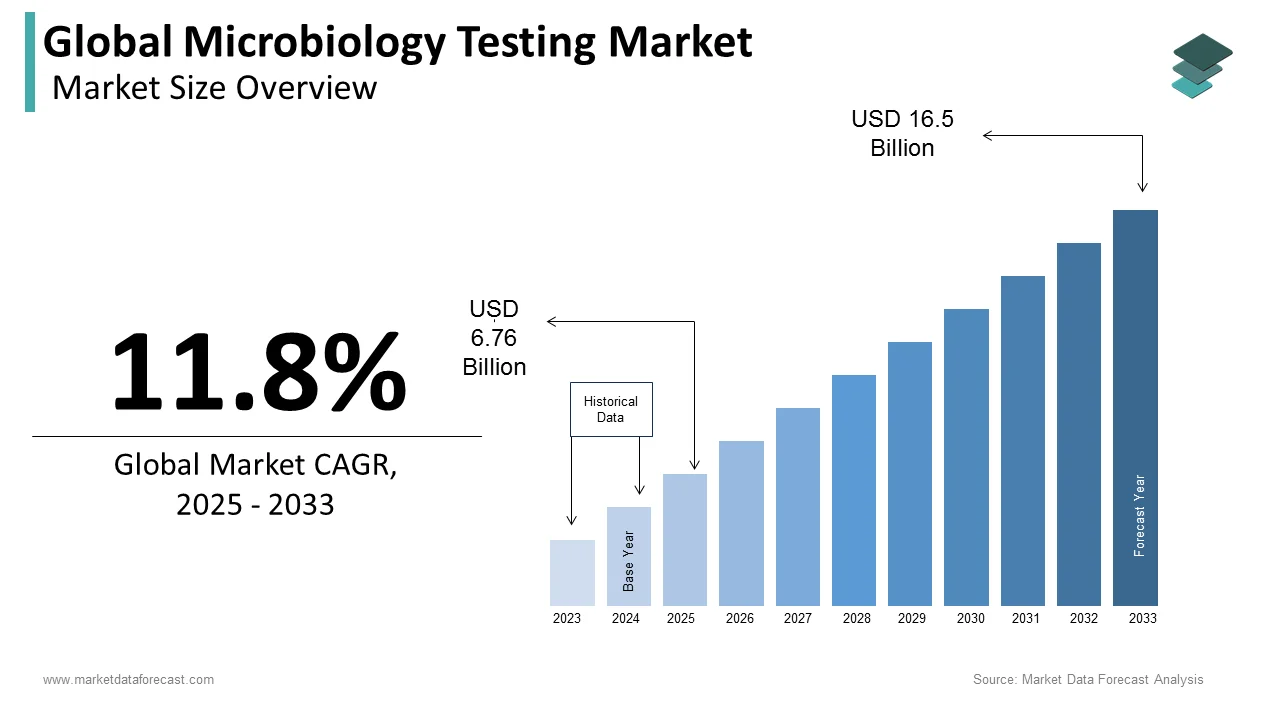

The size of the global microbiology testing market was worth USD 6.05 billion in 2024. The global market is anticipated to grow at a CAGR of 11.80% from 2025 to 2033 and be worth USD 16.5 billion by 2033 from USD 6.76 billion in 2025.

Microbiology Testing Market refers to the analytical procedures designed to detect, identify, and quantify microorganisms such as bacteria, viruses, fungi, and parasites in clinical, food, pharmaceutical, and environmental samples. These tests are important for diagnosing infectious diseases, ensuring product safety, and monitoring public health threats. According to the World Health Organization (WHO), around 600 million people globally suffer from foodborne illnesses annually, with microbiological contamination being a leading cause, emphasizing the indispensable role of testing in safeguarding health. In clinical settings, as per the study, rapid microbiological diagnostics reduce hospital stays when bloodstream infections are promptly identified. Furthermore, according to the research, a large number of cases of antimicrobial-resistant infections in EU hospitals, strengthening the necessity for accurate microbial identification. Hence, microbiology testing has evolved into a foundational component of risk mitigation and clinical decision-making.

MARKET DRIVERS

Escalating Global Burden of Infectious Diseases

The escalating global burden of infectious diseases drives the growth of the microbiology testing market. The prevalence of such diseases continues to strain healthcare systems and necessitate rapid and accurate diagnostic interventions. According to the study, lower respiratory infections remain one of the leading causes of death worldwide, responsible for a notable number of fatalities. The resurgence of vaccine-preventable diseases such as measles has further amplified demand for microbial surveillance. Apart from these, the ongoing threat of zoonotic spillovers, exemplified by the detection of avian influenza in mammalian populations, has prompted national health agencies to expand routine pathogen screening. In low- and middle-income countries, according to the research, diarrheal diseases caused by E. coli, Shigella, and Vibrio cholerae account for a portion of deaths annually, driving investment in point-of-care microbiological assays. This persistent disease burden compels governments and healthcare providers to prioritize robust diagnostic infrastructure.

Tightening Regulatory Standards in Food and Pharmaceuticals

The tightening of regulatory standards across the food and pharmaceutical industries, mandating comprehensive microbial quality control, propels the growth of the microbiology testing market. As per the study, food recalls were initiated due to microbiological contamination, with Listeria monocytogenes and Salmonella being the most frequently cited pathogens. In response, manufacturers are adopting advanced testing protocols such as PCR and next-generation sequencing (NGS) to meet compliance requirements under the Food Safety Modernization Act (FSMA). Similarly, the European Medicines Agency (EMA) mandates sterility testing for all injectable pharmaceuticals, requiring the detection of viable microorganisms in batches before release. These stringent protocols are not only reactive but preventive, which emphasizes environmental monitoring and contamination control. AS a result, this institutionalizes microbiology testing as a non-negotiable component of operational integrity.

MARKET RESTRAINTS

High Cost and Complexity of Advanced Testing Technologies

The high cost and complexity associated with advanced testing technologies, which limit accessibility in resource-constrained settings, restrain the growth of the microbiology testing market. According to the research, a portion of laboratories in sub-Saharan Africa lack the infrastructure to perform molecular microbiological assays such as real-time PCR, relying instead on conventional culture methods that can take hours for results. The equipment required for automated microbial identification systems. Apart from these, trained personnel are scarce. These barriers delay diagnosis and outbreak response, particularly in rural areas. Even in developed nations, smaller clinical labs face budgetary constraints in upgrading to digital or AI-integrated platforms. This slows the adoption of next-generation testing solutions despite their superior accuracy and speed.

Prolonged Turnaround Time for Culture-Based Methods

The prolonged turnaround time for culture-based microbiological methods, which weakens clinical and industrial decision-making, degrades the growth of the microbiology testing market. According to a 2023 study published in Clinical Microbiology and Infection, conventional blood culture techniques require an average of 48 to 72 hours to detect pathogens, with additional time needed for antibiotic susceptibility testing. This delay contributes to empirical antibiotic use, which the Centers for Disease Control and Prevention (CDC) identifies as a key factor in the rise of antimicrobial resistance. In the food industry, as per research, extended testing timelines forced a portion of dairy producers to hold shipments for days, increasing spoilage risks and operational costs. Rapid tests are available. But, many still lack the sensitivity or regulatory validation for important applications. The persistence of legacy workflows, particularly in public health laboratories with limited funding, perpetuates inefficiencies and reduces the responsiveness of microbial surveillance systems. This impedes timely interventions during outbreaks.

MARKET OPPORTUNITIES

Integration of AI and Machine Learning in Microbiological Diagnostics

The integration of artificial intelligence (AI) and machine learning with microbiological diagnostics to enhance accuracy, speed, and predictive analytics is setting up new opportunities for the growth of the microbiology testing market. As per the study, AI algorithms trained on microbial growth patterns in digital imaging systems can achieve an accuracy in identifying Staphylococcus aureus and Pseudomonas aeruginosa from culture plates, reducing manual interpretation errors. Companies are incorporating AI into automated platforms to predict antibiotic resistance profiles within hours rather than days. These advancements not only improve diagnostic precision but also enable proactive public health responses, which transform microbiology testing from reactive to anticipatory, particularly in urban and high-risk environments.

Expansion of Microbiome-Based Testing in Clinical and Wellness Applications

The expansion of microbiome-based testing in clinical and wellness applications, moving beyond pathogen detection to personalized health insights, is likely to promote new opportunities for the microbiology testing market. According to the Human Microbiome Project, microbial communities in the gut influence immune function, mental health, and metabolic regulation, prompting interest in microbiome profiling for chronic disease management. As per a study, dysbiosis in gut microbiota is associated with an increased risk of developing inflammatory bowel disease (IBD). Companies offer consumer-facing microbiome tests that analyze stool samples to recommend dietary and lifestyle modifications. In oncology, patients with diverse gut microbiomes responded better to immunotherapy, accelerating clinical adoption of microbiome screening. This shift positions microbiology testing as a gateway to precision medicine by opening new revenue streams in preventive healthcare, nutraceuticals, and digital therapeutics.

MARKET CHALLENGES

Lack of Standardization in Testing Methodologies and Reporting

The lack of standardization in testing methodologies and reporting protocols across regions and institutions challenges the growth of the microbiology testing market. According to the study, different culture media and incubation conditions are used globally for Salmonella detection, leading to inconsistent sensitivity and false-negative rates. This variability complicates cross-border data comparison and outbreak tracking, particularly during pandemics. As per research, only a few member states submit fully harmonized microbiological data to the Global Antimicrobial Resistance and Use Surveillance System (GLASS). In clinical labs, discrepancies in antibiotic susceptibility testing methods can result in inappropriate treatment regimens. The absence of universal reference standards for emerging technologies like metagenomic sequencing further hampers regulatory approval and clinical adoption, which affects confidence in test reliability and limits scalability.

Rising Antimicrobial Resistance (AMR)

The rising prevalence of antimicrobial resistance (AMR), which diminishes the effectiveness of traditional microbiological testing that relies on phenotypic response to antibiotics, is set to pose a new challenge for the growth of the microbiology testing market. According to the study, numerous deaths were directly attributed to drug-resistant infections. The CDC warns that a portion of AMR cases originate in healthcare settings where outdated testing methods fail to identify resistance genes early. Molecular tests capable of detecting resistance markers, such as PCR for mecA or NDM-1, remain underutilized due to cost and complexity. As per research, only a portion of EU hospitals routinely use genotypic testing for AMR screening. This gap between microbial evolution and diagnostic capability threatens patient outcomes and public health security, which demands urgent innovation and investment in next-generation microbiological tools.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product, Application, Disease Area, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Market Leaders Profiled | Danaher Corporation (U.S.), Becton, Dickinson, and Company (U.S.), Cepheid (U.S.) Abbott Laboratories Inc. (U.S.), Bio-Rad Laboratories Inc. (U.S.), F. Hoffman-La Roche Ltd. (Switzerland), Alere Inc. (U.S.), Bruker Corporation (U.S.), Hologic, Inc. (U.S.), and Others. |

SEGMENTAL ANALYSIS

By Product Insights

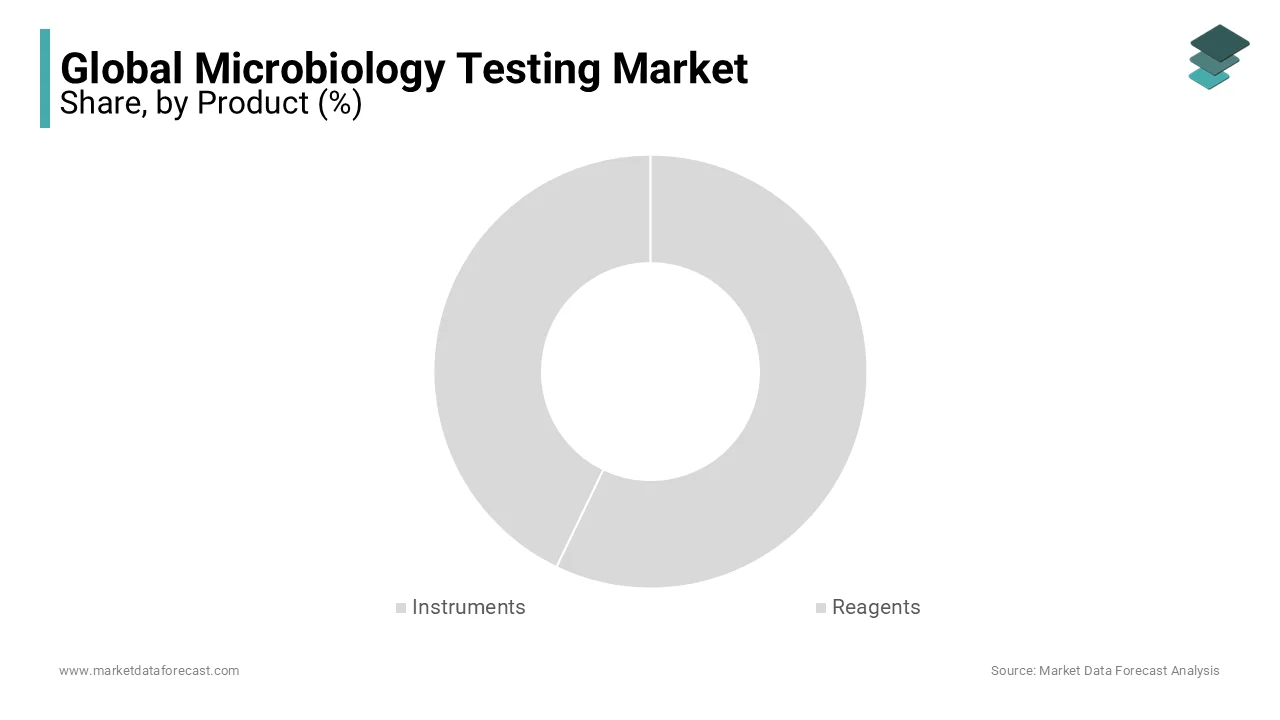

The reagents segment was the dominant product category in the microbiology testing market with a 58.3% share in 2024. The growth of the reagents segment is attributed to the recurring nature of reagent consumption, which necessitates continuous procurement across clinical, pharmaceutical, and food safety laboratories. Unlike capital-intensive instruments, reagents are consumed in every testing cycle, which creates a stable and high-volume demand stream. Apart from these, the shift toward molecular diagnostics, such as PCR and nucleic acid amplification tests (NAATs), has increased reliance on specialized reagents, including primers, probes, and polymerases. As per a study, reagent supply chain disruptions were the primary cause of testing delays, which emphasizes their operational centrality and sustained demand.

The instruments segment is predicted to see the highest CAGR of 9.6% from 2025 to 2033. The rapid adoption of automated and high-throughput microbiological platforms can be attributed to the growth of the instruments segment. Modern laboratories are increasingly investing in systems such as MALDI-TOF mass spectrometers, automated culture analyzers, and next-generation sequencing (NGS) platforms to enhance speed, accuracy, and scalability. According to a study, automated identification systems reduced pathogen detection time compared to conventional methods, significantly improving clinical outcomes. Apart from these, government initiatives such as India’s National Digital Health Mission are funding instrument procurement for public labs by accelerating modernization. These technological advancements, coupled with labor shortages and rising test volumes, are driving sustained investment in instrumentation.

By Application Insights

The clinical diagnostics segment held the leading share of 44.1% of the global microbiology testing market in 2024. The domination of the clinical diagnostics segment is mainly due to the important role microbiology testing plays in diagnosing infectious diseases, guiding antimicrobial therapy, and managing hospital-acquired infections. In acute care settings, timely identification of pathogens such as Staphylococcus aureus, Klebsiella pneumoniae, and Mycobacterium tuberculosis is essential for patient survival. As per the study, healthcare-associated infections (HAIs) affect a portion of hospitalized patients daily, which necessitates routine microbiological surveillance. Apart from these, the integration of rapid diagnostic tests into emergency departments has reduced sepsis. Hence, clinical microbiology remains a cornerstone of modern medicine as millions of blood cultures are performed globally each year, ensuring continuous demand for robust and reliable testing solutions.

The food testing application segment is on the rise and is expected to be the fastest-growing segment in the global market by witnessing a CAGR of 10.2% between 2025 and 2033. Factors like the escalating food safety regulations and rising consumer awareness of contamination risks are contributing to the growth of the food testing application segment. According to the study, millions of people fall ill annually due to contaminated food, with microbiological hazards such as Salmonella, Listeria, and E. coli responsible for a portion of cases. In response, regulatory bodies have mandated routine pathogen testing across supply chains, particularly for ready-to-eat and dairy products. Apart from these, the U.S. Food Safety Modernization Act (FSMA) requires preventive controls, including environmental monitoring in food facilities. With global food trade expanding, the need for standardized and rapid microbiological screening has become imperative because of the expanding global trade in food, which accelerates investment in on-site and lab-based testing infrastructure.

By Disease Area Insights

The respiratory diseases segment accounts for the highest share of the microbiology testing market. Factors like the increasing patient population suffering from respiratory diseases and the growing number of COVID-19 cases are surging the market's growth rate.

REGIONAL ANALYSIS

North America Microbiology Testing Market Analysis

North America was the largest region in the microbiology testing market and captured 36.6% of the global market share in 2024. The dominant position of North America is majorly propelled by advanced healthcare infrastructure, stringent regulatory frameworks, and high adoption of diagnostic technologies. The United States, in particular, drives demand through its extensive network of clinical laboratories and robust public health surveillance systems. According to the research, millions of microbiological tests are conducted annually in clinical labs, including blood cultures, urine analyses, and respiratory panels. The presence of major diagnostic companies such as BD, Thermo Fisher Scientific, and bioMérieux fosters innovation and rapid commercialization of new platforms. Apart from these, the FDA’s accelerated approval pathways for microbiological assays have reduced time-to-market for advanced diagnostics. Thus, North America continues to set the benchmark for diagnostic rigor and technological integration as antimicrobial resistance and hospital-acquired infections remain important concerns.

Europe Microbiology Testing Market Analysis

Europe is closely following in the microbiology testing market by accounting for a 31.3% share in 2024. A well-established regulatory environment and strong public health systems are driving the growth of Europe in the global market. The European Union’s In Vitro Diagnostic Regulation (IVDR) has elevated the performance and traceability requirements for microbiological tests, driving demand for compliant products. According to the research, millions of microbiological tests were conducted in EU hospitals to monitor antimicrobial resistance and nosocomial infections. Countries like Germany and the UK operate centralized public health labs with high testing throughput, while Nordic nations have pioneered digital pathology and AI-assisted diagnostics. Therefore, Europe remains a key hub for innovation and regulatory prominence in microbiological testing due to a strong emphasis on food safety, environmental monitoring, and clinical accuracy.

Asia Pacific Microbiology Testing Market Analysis

Asia Pacific is predicted to be the rapidly expanding region in the microbiology testing market. The rise of Asia Pasic in the global market can be attributed to rapid industrialization, growing healthcare expenditure, and increasing awareness of infectious disease threats. China and India are the primary growth engines, with both governments investing heavily in diagnostic infrastructure. According to the study, China’s healthcare spending rose annually, which enables the expansion of microbiology labs in tier-2 and tier-3 cities. India’s Ayushman Bharat initiative has established numerous health and wellness centers, many equipped with basic microbiological testing capabilities. The region also faces high burdens of tuberculosis and foodborne illnesses, driving demand for accurate diagnostics. Apart from these, the expansion of contract research organizations (CROs) and pharmaceutical manufacturing in India and South Korea has intensified the need for sterility and environmental monitoring. This further boosts market growth.

Latin America Microbiology Testing Market Analysis

Latin America rose gradually in the microbiology testing market, with Brazil and Mexico emerging as key contributors due to expanding healthcare access and food safety modernization. According to the research, Brazil reporteda number of cases of foodborne illness, prompting stricter enforcement of microbial testing in the dairy and meat sectors. Mexico’s food industry, one of the key exporters of fresh produce to the U.S., adheres to FSMA requirements, necessitating rigorous pathogen screening. As per a study, only a portion of hospitals in the region had access to automated identification systems, indicating a significant unmet need. Thus, Latin America is poised for steady market expansion, particularly in clinical and food testing applications because of increasing foreign investment in biopharma and diagnostics.

Middle East and Africa Microbiology Testing Market Analysis

The Middle East and Africa are expected to grow in the microbiology testing market, with growth concentrated in the Gulf Cooperation Council (GCC) countries and select African economies. According to the study, a portion of clinical microbiology labs in sub-Saharan Africa lack the capacity to perform basic antibiotic susceptibility testing, emphasizing vast infrastructure gaps. However, countries like Saudi Arabia and the UAE are investing heavily in healthcare modernization. Hence, the region is gradually strengthening its testing ecosystem due to rising urbanization and food import regulations, which is supported by international partnerships and donor-funded diagnostic programs.

COMPETITIVE LANDSCAPE

The competition in the Microbiology Testing Market is intense and multifaceted, characterized by the dominance of multinational corporations and the rising influence of regional innovators and public-sector initiatives. Global leaders leverage extensive R&D capabilities, regulatory expertise, and integrated product portfolios to maintain technological superiority. However, local manufacturers in Asia and Latin America are gaining traction by offering cost-effective, region-specific solutions that meet basic diagnostic needs. The market is also witnessing increased collaboration between private firms and public health agencies, particularly in low-resource settings, where affordability and scalability are paramount. Innovation cycles are accelerating, with AI-driven diagnostics, point-of-care devices, and next-generation sequencing reshaping expectations. Regulatory harmonization remains a challenge, creating both barriers and opportunities for differentiation. Antimicrobial resistance and pandemic preparedness remain global priorities. The competitive landscape is evolving toward ecosystem-based solutions that combine hardware, software, and data intelligence to deliver actionable insights.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global microbiology testing market include

- Danaher Corporation

- Becton, Dickinson, and Company

- Cepheid

- Abbott Laboratories Inc.

- Bio-Rad Laboratories Inc.

- Hoffman-La Roche Ltd

- Alere Inc.

- Bruker Corporation

- Hologic, Inc.

TOP PLAYERS IN THE MARKET

- Thermo Fisher Scientific is a pivotal force in the Microbiology Testing Market, with a strong and expanding footprint across the Asia Pacific region. The company has intensified its presence through localized manufacturing in Singapore and India, ensuring faster supply chain responsiveness and regulatory alignment with national health standards. Apart from these, Thermo Fisher established a regional innovation hub in Shanghai to co-develop rapid testing solutions with local research institutions. Its integration of cloud-based data analytics enables seamless monitoring of test outcomes across hospital networks, which strengthens its role as a technology leader in the region.

- BioMérieux plays a transformative role in advancing microbiological diagnostics throughout the Asia Pacific, leveraging its expertise in automated identification and antimicrobial susceptibility testing. The company has deepened its engagement in Southeast Asia by collaborating with public health agencies in Thailand, Vietnam, and Indonesia to strengthen infectious disease surveillance. Furthermore, the company initiated training programs for lab technicians in ASEAN nations through its LabExpert initiative, which enhances technical capacity and trust in its diagnostic ecosystem.

- BD (Becton, Dickinson and Company) has significantly influenced the Microbiology Testing Market in the Asia Pacific by expanding access to standardized, high-performance diagnostic platforms. The company strengthened its regional presence by inaugurating a new distribution center, which enables faster delivery to many countries. In India, BD collaborated with the Indian Council of Medical Research (ICMR) to support antimicrobial resistance (AMR) surveillance, supplying automated culture and identification systems to designated sentinel labs.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Microbiology Testing Market are deploying a combination of technological innovation, geographic expansion, strategic partnerships, and capacity-building initiatives to consolidate their dominance. Companies are investing heavily in automated, rapid, and molecular diagnostic platforms to meet the demand for faster, more accurate results. Expansion into emerging markets is being accelerated through localized manufacturing, regulatory alignment, and collaborations with public health institutions. Strategic alliances with governments and global health organizations enable large-scale deployment of testing systems in national programs. Firms are also prioritizing digital integration by linking instruments to laboratory information systems for real-time data analytics and outbreak tracking. Apart from these, workforce training and technical support programs are being scaled to ensure proper implementation and sustained adoption. The focus on end-to-end solutions, from instruments and reagents to software and services, is redefining competitive advantage in a market increasingly driven by system compatibility and operational efficiency.

MARKET SEGMENTATION

This research report on the global microbiology testing market has been segmented based on the product, application, disease area, and region.

By Product

- Instruments

- Reagents

By Application

- Pharmaceutical

- Clinical

- Food Testing

- Energy

- Chemical and Material Manufacturing

- Environmental

By Disease Area

- Respiratory Diseases

- Bloodstream Infections

- Gastrointestinal Diseases

- Sexually Transmitted Diseases

- Urinary Tract Infections

- Periodontal Diseases

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What is the Microbiology Testing Market and what are its key growth drivers?

The Microbiology Testing Market involves diagnostic testing to detect microorganisms causing infections and contamination. Growth is driven by infectious disease prevalence, technological advancements, and stringent food and healthcare regulations

2. What are the major product segments in the Microbiology Testing Market?

Key segments include microbial identification systems, reagents and kits, instruments, and testing services

3. How does the Microbiology Testing Market contribute to infectious disease diagnosis?

It provides rapid, accurate detection of bacterial, viral, fungal, and parasitic infections enabling timely treatment and better patient outcomes

4. What role does microbiology testing play in food safety within the market?

Microbiology testing ensures food products are free from harmful pathogens like Salmonella and E. coli, helping manufacturers meet safety regulations and prevent outbreaks

5. Which technologies are commonly used in the Microbiology Testing Market?

Common technologies include polymerase chain reaction (PCR), next-generation sequencing (NGS), culture-based methods, and mass spectrometry

6. What applications drive demand in the Microbiology Testing Market?

Applications include clinical diagnostics, food and beverage safety, pharmaceutical manufacturing, and environmental testing

7. Which regions lead the Microbiology Testing Market?

North America is the largest market due to advanced healthcare infrastructure, followed by Europe and Asia-Pacific regions

8. How is automation impacting the Microbiology Testing Market?

Automation improves testing speed, accuracy, and throughput, reducing human errors and operational costs within clinical and industrial microbiology labs

9. Who are the leading companies in the Microbiology Testing Market?

Key players include Abbott Laboratories, Thermo Fisher Scientific, Danaher, Bio-Rad Laboratories, Merck KGaA, and Becton Dickinson

10. How does antimicrobial resistance influence the Microbiology Testing Market?

The rise of antimicrobial resistance increases the need for advanced microbial susceptibility testing within the market to guide effective treatments

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com