Global Food Pathogen Testing Market Size, Share, Trends & Growth Forecast Report By Type, Food Type, Technology and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Market Size, 2025

$14.29 BnMarket Estimate, 2026

$15.40 BnMarket Forecast, 2034

$28.09 BnCAGR, 2026–2034

7.8%Global Food Pathogen Testing Market Report Summary

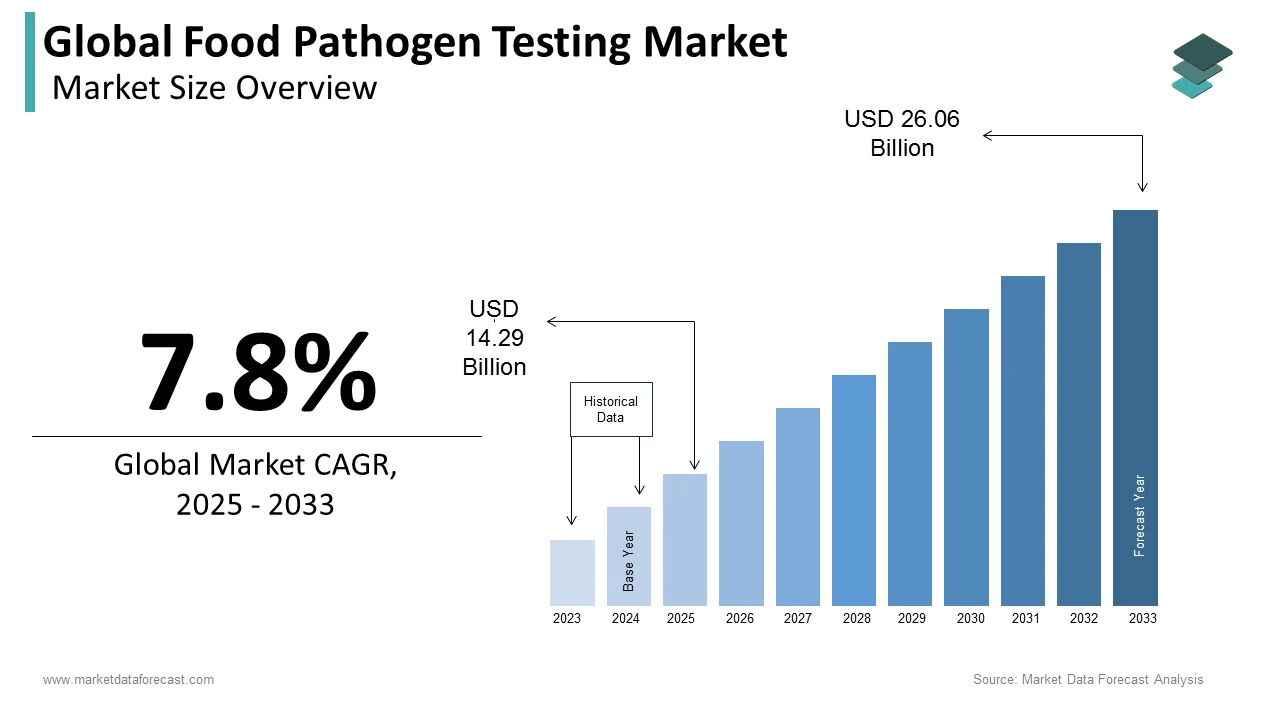

The global food pathogen testing market was valued at USD 14.29 billion in 2025, is estimated to reach USD 15.40 billion in 2026, and is projected to reach USD 28.09 billion by 2034, growing at a CAGR of 7.8% from 2026 to 2034. Market growth is driven by increasing concerns over food safety, rising incidences of foodborne illnesses, and stringent regulatory standards imposed by governments worldwide. The expansion of the global food supply chain, coupled with growing consumer awareness regarding food quality, is further accelerating demand for advanced pathogen testing solutions. Additionally, technological advancements in rapid testing methods are enhancing detection accuracy and efficiency.

Key Market Trends

- Rising concerns regarding food safety and contamination risks.

- Increasing prevalence of foodborne diseases globally.

- Stringent government regulations and quality standards.

- Growing demand for rapid and accurate testing technologies.

- Expansion of global food trade and supply chains.

Segmental Insights

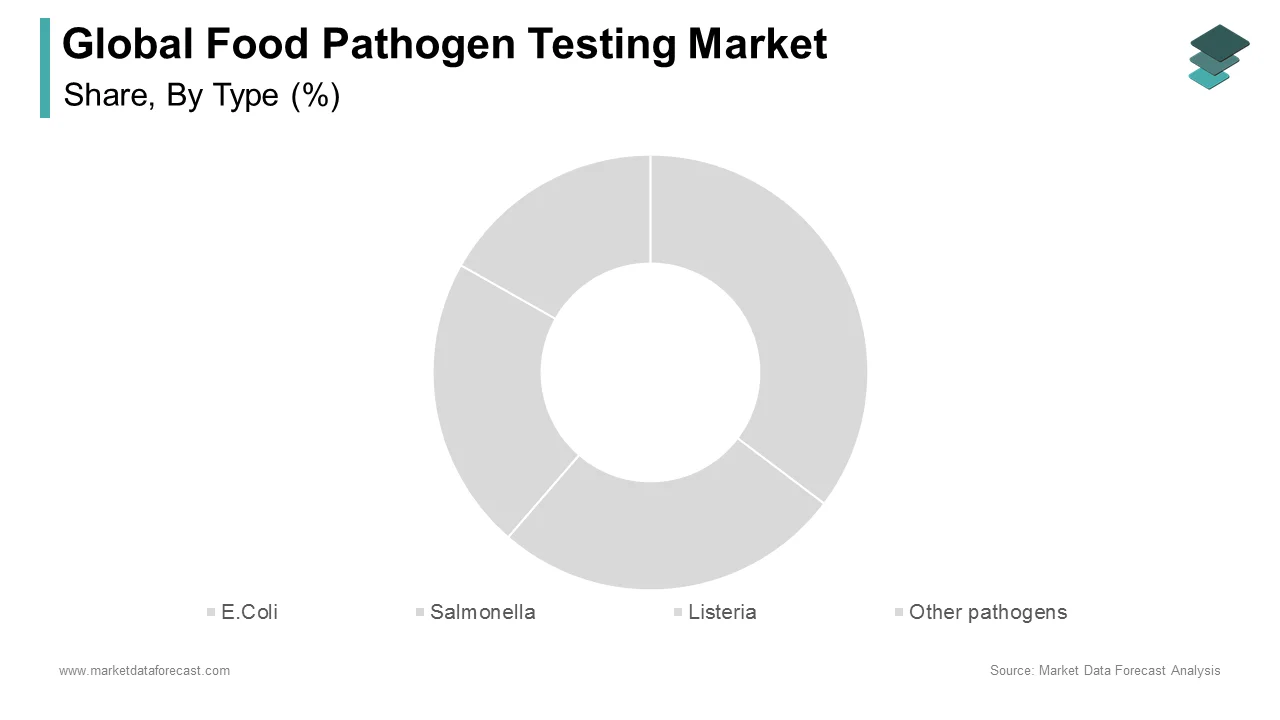

- Based on type, the Salmonella segment dominated the global food pathogen testing market by capturing 32.8% share in 2025, due to its high prevalence in foodborne outbreaks.

- Based on food type, the meat & poultry segment led the market with 38.1% share in 2025, driven by high susceptibility to contamination and strict safety regulations.

- Based on technology, the traditional technology segment held the largest share of 45.8% in 2025, owing to its widespread adoption and cost-effectiveness.

Regional Insights

The global food pathogen testing market is expanding across regions due to growing food safety concerns and regulatory enforcement.

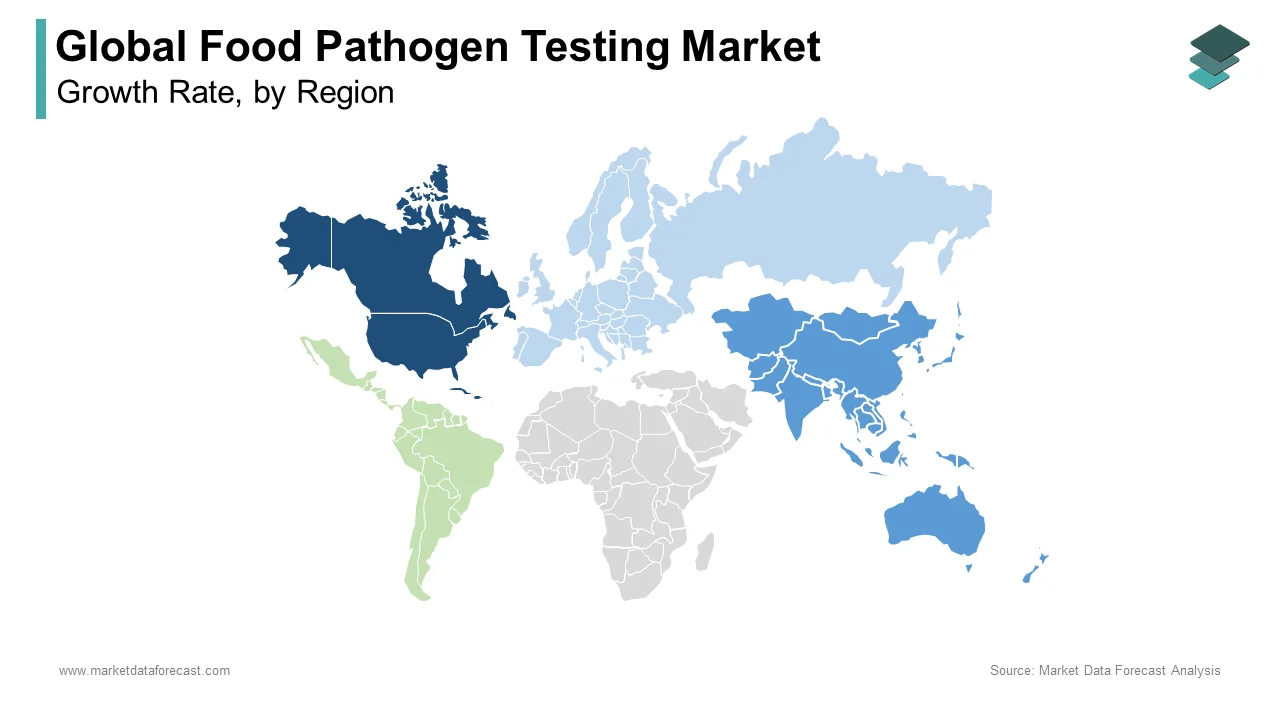

- North America led the market in 2025 with 36.5% share, supported by strict food safety regulations and advanced testing infrastructure.

- Europe followed with 28.6% share, driven by strong regulatory frameworks and high consumer awareness.

- Asia-Pacific is the fastest-growing region due to rapid industrialization of the food sector and increasing export-oriented production.

Competitive Landscape

The global food pathogen testing market is highly competitive, with companies focusing on technological innovation, expanding laboratory networks, and offering comprehensive testing solutions. Strategic partnerships and acquisitions are also shaping the competitive environment.

Prominent companies operating in the global food pathogen testing market include SGS S.A., Bureau Veritas S.A., Thermo Fisher Scientific, Merck KGaA, Intertek Group PLC, Eurofins Scientific, Silliker, Inc., IFP Institut Für Produktqualität GmbH, ALS Limited, Asurequality, Microbac Laboratories, Inc., bioMérieux, and Genetic ID NA Inc.

Global Food Pathogen Testing Market Size

The size of the global food pathogen testing market was worth USD 14.29 billion in 2025. The global market is anticipated to grow at a CAGR of 7.8% from 2026 to 2034 and be worth USD 28.09 billion by 2034 from USD 15.40 billion in 2026.

Food pathogen testing is the process of detecting and identifying harmful microorganisms, such as bacteria, viruses, parasites, and fungi, in raw materials, finished food products, and the production environment. This market serves as the primary defense mechanism against foodborne illnesses, ensuring that products ranging from raw agricultural commodities to processed ready-to-eat meals meet stringent safety standards before reaching consumers. The urgency of this market is underscored by the persistent global burden of foodborne diseases, which threaten public health and economic stability. According to the World Health Organization, contaminated food causes approximately 600 million cases of illness annually worldwide, resulting in 420000 deaths each year. In the European Union, the European Food Safety Authority (EFSA) reported a rising trend in food safety incidents, with 6,558 confirmed foodborne outbreaks in 2024 (an increase from 5,691 in 2023). While Salmonella and Campylobacter remained the predominant culprits for outbreak frequency, Listeria monocytogenes continued to be the most severe pathogen, causing the highest proportion of hospitalizations and deaths despite a lower number of outbreaks. These alarming figures drive regulatory bodies and food manufacturers to adopt rigorous testing protocols. The market extends beyond simple detection to include rapid screening methods and confirmatory assays that integrate into production lines. As global trade expands and supply chains become more complex, the necessity for accurate and timely pathogen identification intensifies. This sector functions not merely as a compliance requirement but as an essential pillar of consumer trust and brand integrity, preventing costly recalls and protecting vulnerable populations from severe health outcomes associated with microbial contamination.

MARKET DRIVERS

Escalating Incidence of Foodborne Disease Outbreaks

The rising frequency and severity of foodborne disease outbreaks act as a paramount driver for the food pathogen testing market. Consequently, this is compelling the adoption of advanced pathogen testing solutions. Each outbreak event triggers immediate regulatory scrutiny and necessitates comprehensive testing to identify contamination sources and prevent further spread. According to the Centers for Disease Control and Prevention, foodborne diseases affect one in six Americans annually, illustrating the pervasive nature of the threat that mirrors global trends. The European Centre for Disease Prevention and Control indicates that zoonotic infections transmitted through food remain a primary cause of gastrointestinal illness across the continent. Campylobacteriosis continues to be the most frequently reported foodborne bacterial disease, affecting a vast number of European citizens each year. These statistics create immense pressure on food producers to implement robust testing regimes at every stage of production. High-profile recalls often result in millions of dollars in losses and irreparable brand damage, forcing companies to invest proactively in sensitive detection technologies. The increasing complexity of global supply chains means that a single contaminated ingredient can affect products across multiple countries, amplifying the need for standardized and reliable testing methods. Furthermore, consumer awareness regarding food safety has reached unprecedented levels, with shoppers demanding transparency and proof of safety. This heightened vigilance ensures that testing is not viewed as an optional expense but as a mandatory operational imperative, driving continuous demand for both traditional culture-based methods and rapid molecular diagnostics to mitigate the risks associated with microbial contamination.

Stringent Global Regulatory Frameworks and Compliance Mandates

The implementation of rigorous global regulatory frameworks and mandatory compliance standards further boosts the expansion of the food pathogen testing market. Governments and international bodies have enacted strict laws that require food manufacturers to validate the safety of their products through verified testing protocols before market release. As per the Food Safety Modernization Act in the United States, the focus has shifted from reacting to contamination to preventing it, mandating that facilities establish science-based preventive controls that include regular pathogen testing. Similarly, the European Union maintains some of the world's toughest food safety regulations under the General Food Law, which requires traceability and immediate withdrawal of unsafe products, necessitating frequent and accurate testing. The International Organization for Standardization has published numerous standards, such as ISO 16140, that validate alternative testing methods, encouraging the adoption of rapid technologies. Regulatory agencies conduct routine inspections and impose severe penalties, including facility closures and criminal charges for non-compliance. Data from the Food and Drug Administration highlights that microbial contamination remains a priority for border enforcement. Import refusals for pathogens continue to be a critical tool for preventing unsafe food from entering the domestic supply chain, reflecting strict adherence to safety standards at ports of entry. These legal obligations force food processors, regardless of size, to integrate systematic testing into their quality assurance programs. The harmonization of these standards across trade blocs further ensures that testing becomes a universal requirement for market access, thereby sustaining robust demand for compliant testing services and kits globally.

MARKET RESTRAINTS

High Operational Costs and Resource Intensity of Advanced Methods

Significant financial barriers related to the high operational costs and resource intensity of advanced pathogen testing methods act as a major restraint to the overall food pathogen testing market. This is particularly true for small and medium-sized enterprises. Rapid molecular techniques like polymerase chain reaction offer speed and sensitivity. However, they require substantial capital investment in specialized equipment, reagents, and highly trained personnel. According to research, the cost of implementing a comprehensive food safety management system aligned with Global Food Safety Initiative standards can be a significant portion of a smaller company's earnings. This expense can create a disproportionate burden that favors larger corporations over smaller producers. The recurring expenses for proprietary consumables and maintenance contracts further strain operating budgets, making it difficult for smaller players to compete with larger corporations that benefit from economies of scale. Additionally, the need for certified laboratory environments with strict contamination control measures adds to the infrastructure costs. Data from the World Bank indicates that compliance costs for food safety standards are a significant barrier to market entry for businesses in developing regions, limiting the widespread adoption of state-of-the-art testing. Many firms are forced to rely on less sensitive or slower traditional methods to cut costs, which may compromise safety outcomes. The shortage of skilled microbiologists capable of operating complex diagnostic instruments exacerbates the issue, driving up labor costs. This economic reality restricts the universal deployment of the most effective testing technologies, creating a disparity in food safety capabilities across the industry and slowing overall market penetration for high-end solutions.

Complexity of Sample Matrices and Interference Issues

The inherent complexity of diverse food sample matrices and the potential for interference during analysis are significant technical constraints for the food pathogen testing market. This hampers the accuracy and efficiency of pathogen testing. Food products vary widely in composition, containing fats, proteins, carbohydrates, and natural inhibitors that can obstruct detection processes and lead to false negative or false positive results. As per the Journal of Food Protection, certain compounds found in spices, chocolate, and fresh produce can inhibit polymerase chain reaction amplification, requiring extensive sample preparation steps that negate the speed advantages of rapid tests. This necessity for complex pre-enrichment and purification protocols increases turnaround time and labor requirements, reducing the throughput of testing laboratories. The presence of background microflora in fermented foods or raw meats can also outcompete target pathogens during culture-based enrichment, masking their detection. Studies by the International Association for Food Protection highlight that matrix effects remain a leading cause of test failure, necessitating method validation for every new product type. This technical challenge forces manufacturers to develop matrix-specific protocols, increasing the cost and complexity of testing operations. The inability to apply a universal testing method across all food types creates logistical bottlenecks and limits the scalability of testing programs, particularly for companies with diverse product portfolios that must manage multiple validation processes to ensure reliable safety data.

MARKET OPPORTUNITIES

Integration of Whole Genome Sequencing Technologies

The integration of Whole Genome Sequencing technologies provides a transformative opportunity for the food pathogen testing market. It allows for unprecedented precision in outbreak investigation and source tracking. Unlike traditional methods that identify pathogens only to the species level, whole genome sequencing provides detailed genetic fingerprints that allow regulators and manufacturers to link specific contamination events to their exact origins with high confidence. As per sources, the implementation of whole genome sequencing in food safety surveillance has improved the ability to detect outbreaks compared to previous methods, enabling faster and more targeted recalls. This technology facilitates the identification of virulence factors and antibiotic resistance genes, offering critical insights into the public health risk posed by specific strains. Food companies can leverage this data to pinpoint weaknesses in their supply chains and implement corrective actions more effectively. The decreasing cost of sequencing and the development of portable sequencers are making this technology increasingly accessible for routine use in industrial settings. Adopting whole genome sequencing allows the industry to shift from reactive testing to predictive risk management. Consequently, this enhances consumer protection and brand reputation while creating new revenue streams for advanced genomic analysis service providers.

Adoption of Rapid Point of Need Testing Solutions

The widespread adoption of rapid point-of-need testing solutions opens a pathway to decentralize food safety monitoring and accelerate decision-making processes within the supply chain, which is likely to promote the expansion of the food pathogen testing market. These portable and user-friendly devices enable testing directly at production sites, farms, or distribution centers without the need to send samples to external laboratories, drastically reducing turnaround times from days to minutes. Recent advancements in biosensor technology and lateral flow assays have improved the sensitivity and specificity of these rapid tests, making them viable alternatives for screening high-risk batches before they enter the market. A study notes that rapid testing capabilities allow for immediate corrective actions, preventing contaminated products from progressing further down the supply chain and minimizing waste. This shift empowers frontline workers to perform critical safety checks, fostering a culture of proactive quality control. The scalability of point-of-need solutions makes them ideal for small-scale producers and remote locations where laboratory access is limited. Technology is continuing to miniaturize, and connectivity features now allow for instant data transmission to cloud platforms. Consequently, these solutions will become integral to smart food safety ecosystems and drive significant growth in on-site diagnostics.

MARKET CHALLENGES

Emergence of Novel and Resistant Pathogen Strains

The continuous emergence of novel pathogen strains and the increasing prevalence of antimicrobial resistance pose a formidable challenge to the efficacy of existing testing methodologies in the food pathogen testing market. Microorganisms constantly evolve, developing new virulence factors or mutating genetic sequences that may escape detection by standard assays designed for known targets. As per research, antimicrobial resistance is one of the top ten global public health threats, with resistant bacteria like Salmonella and Campylobacter becoming increasingly common in the food supply. This evolution renders some conventional antibodies and primers used in immunoassays and molecular tests less effective, leading to potential false negatives that compromise food safety. The discovery of new serotypes requires constant updates to testing kits and validation protocols, creating a lag between the appearance of a threat and the availability of a reliable detection method. Research indicates that the rate of microbial evolution often outpaces the development of commercial diagnostic tools. Furthermore, the presence of viable but non-culturable states in certain bacteria complicates detection using culture-based methods, which remain the gold standard for many regulations. This biological arms race demands continuous investment in research and development to ensure testing methods remain robust, placing pressure on manufacturers to constantly innovate while maintaining regulatory compliance and cost-effectiveness in a dynamic microbial landscape.

Fragmented Global Supply Chains and Traceability Gaps

The intricate and fragmented nature of global food supply chains creates significant hurdles for maintaining consistent pathogen testing standards and achieving complete traceability from farm to fork, which negatively impacts the food pathogen testing market. Food ingredients often traverse multiple countries and pass through numerous handlers before reaching the final processor, increasing the risk of contamination at various touchpoints and complicating the assignment of testing responsibilities. Disparities in regulatory stringency and laboratory capabilities across different jurisdictions create gaps where contaminated products might evade detection. The lack of standardized data sharing mechanisms hinders the rapid identification of contamination sources during cross-border outbreaks. A study highlights that differing national standards for pathogen limits and testing methods create trade barriers and confusion for multinational food companies. This fragmentation makes it difficult to implement a unified testing strategy, forcing companies to navigate a complex web of requirements that may not align. The opacity of sub-tier supplier networks further exacerbates the issue, as primary manufacturers often lack visibility into the safety practices of raw material providers. These structural weaknesses undermine the effectiveness of testing regimes and complicate efforts to ensure universal food safety across the interconnected global market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Food Type, Technology, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered |

|

| Market Leaders Profiled | SGS S.A., Bureau Veritas S.A., Intertek Group PLC, Eurofins Scientific, Silliker, Inc., IFP Institut für Produktqualität GmbH, ALS Limited, Asurequality, Microbac Laboratories, Inc. und Genetic Id Na Inc.

|

SEGMENTAL ANALYSIS

By Type Insights

The Salmonella segment held the majority share of 32.8% share of the global food pathogen testing market in 2025. This dominance of the segment is driven by the ubiquity of the pathogen across diverse food matrices and the severe regulatory consequences associated with its presence in consumer goods. Apart from these, the main aspect supporting the leadership of the Salmonella segment is its status as one of the most common causes of foodborne illness worldwide, necessitating rigorous and frequent testing across almost all food categories. According to the World Health Organization, non-typhoidal Salmonella infections cause approximately 94 million cases of gastroenteritis globally each year, resulting in a substantial number of deaths. This staggering incidence rate forces food manufacturers to implement comprehensive screening protocols for raw materials and finished products. The ability of the bacteria to survive in dry environments and resist certain sanitizers increases the risk of persistent contamination in processing facilities. Consequently, regulatory bodies like the United States Department of Agriculture enforce zero-tolerance policies for specific Salmonella serotypes in ready-to-eat meats, compelling producers to invest heavily in sensitive detection methods. The sheer volume of samples required to mitigate this widespread threat ensures that Salmonella testing remains the cornerstone of food safety programs, driving consistent demand for both traditional and rapid diagnostic solutions. Strict international regulatory limits and the necessity for export certification further cement the dominance of the Salmonella testing segment. Global trade in food products relies on adherence to stringent microbiological criteria, where the detection of Salmonella can lead to immediate rejection of shipments and severe economic losses. Companies aiming to access lucrative markets in North America and Europe must provide certified test results proving the absence of the pathogen, making testing a mandatory gatekeeping step. This regulatory pressure creates a non-negotiable demand for accurate and validated testing services, ensuring that the Salmonella segment maintains its leading position as a critical compliance requirement for the global food industry.

The listeria segment is estimated to register the fastest CAGR 8.4% during the forecast period due to the increasing consumption of ready-to-eat foods, the unique ability of the pathogen to thrive in cold temperatures, and the severe health implications for vulnerable populations. In addition, the surge in global demand for convenience foods that require no further cooking before consumption is the primary engine driving the rapid expansion of Listeria testing. Unlike many other pathogens, Listeria monocytogenes can grow at refrigeration temperatures, posing a significant risk in chilled ready-to-eat products such as deli meats, soft cheeses, and smoked seafood. Manufacturers of these products must implement environmental monitoring programs and finished product testing to ensure safety throughout the shelf life, as the pathogen can proliferate during storage. The high mortality rate associated with listeriosis, particularly among pregnant women, newborns, and the elderly, drives regulators to impose strict controls. This combination of changing consumer lifestyles favoring convenience and the biological resilience of the pathogen creates an urgent and growing need for specialized testing solutions tailored to detect low levels of Listeria in complex food matrices. The implementation of enhanced surveillance programs and zero-tolerance regulatory policies specifically targeting Listeria is a critical factor propelling the segment's rapid growth. Governments worldwide have recognized the severity of listeriosis outbreaks and have responded by mandating more frequent and sensitive testing protocols for high-risk facilities. The regulatory frameworks force companies to adopt advanced molecular methods capable of detecting the pathogen at very low concentrations to avoid costly recalls and legal liabilities. The shift from reactive testing to proactive environmental monitoring creates a sustained and accelerating demand for Listeria-specific assays, making it the fastest-growing segment in the market.

By Food Type Insights

The meat & poultry segment led the food pathogen testing market and captured a 38.1% share in 2025. This leading position of the segment is supported by the high susceptibility of animal proteins to microbial contamination and the extensive regulatory frameworks governing their production and distribution. The inherent biological characteristics of meat and poultry make them ideal vectors for a wide range of pathogens, necessitating intensive testing protocols that drive the segment's market leadership. Raw meat provides a nutrient-rich environment that supports the rapid growth of bacteria such as Salmonella, Campylobacter, E. coli O157:H7, and Listeria if not properly handled or cooked. The complexity of the slaughter and processing process, which involves multiple steps where cross-contamination can occur, requires testing at critical control points from the farm to the packaging line. Furthermore, the global consumption of meat continues to rise. The severe health consequences of consuming undercooked or contaminated meat ensure that this sector remains the primary focus of food safety efforts, sustaining its dominant share of the testing market. Robust mandatory government inspection and verification programs specifically designed for the meat and poultry industry act as a fundamental driver for the segment's dominance. In many countries, the production of meat and poultry is subject to continuous federal inspection, which includes mandatory pathogen testing as a condition of operation. The European Union enforces similar strictures under Regulation EC No 2073/2005, which sets microbiological criteria for foodstuffs and mandates regular sampling of carcasses and processed meat products. These legal requirements create a consistent and high-volume demand for testing services that is less susceptible to market fluctuations compared to voluntary testing in other sectors. The integration of testing into the legal framework of meat production ensures that the segment remains the largest consumer of pathogen detection technologies and services globally.

The fruits & vegetables segment is anticipated to witness the fastest CAGR of 7.9% from 2026 to 2034, owing to shifting consumer dietary patterns toward fresh produce, increased recognition of produce-related outbreaks, and the challenges of cleaning complex surface structures. Moreover, the global shift in consumer preferences toward fresh, organic, and plant-based diets is a primary catalyst for the rapid growth of pathogen testing in the fruits and vegetables sector. As health consciousness rises, individuals are consuming larger quantities of raw produce, which bypasses the kill-step of cooking and thus retains any present pathogens. This surge in volume directly correlates with an increased frequency of testing to ensure safety. The organic farming trend, which restricts the use of synthetic sanitizers, further complicates pathogen control, necessitating more rigorous testing regimes to validate safety. Retailers and food service providers are responding to consumer demand for transparency by requiring suppliers to provide comprehensive test results for fresh produce. This evolving landscape transforms fruits and vegetables from a low-risk category into a high-priority segment for pathogen detection, fueling its rapid expansion. The unique challenges associated with surface contamination and the reliance on agricultural water sources are significant factors driving the accelerated growth of testing in the fruits and vegetables segment. Unlike homogeneous products, fresh produce often has rough or leafy surfaces that can harbor pathogens in biofilms, making them difficult to remove and detect without specialized methods. The difficulty in decontaminating fresh produce without compromising quality means that prevention through testing is critical. Growers and packers are increasingly adopting rapid testing technologies to screen water and finished products before distribution. This focus on mitigating risks associated with environmental exposure and surface topology is propelling the segment to become the fastest-growing area in the food pathogen testing market.

By Technology Insights

The traditional technology segment dominated the food pathogen testing market and accounted for a share of 45.8% in 2025. This supremacy of the segment is attributed to its status as the regulatory gold standard, its cost-effectiveness for high-volume screening, and its universal acceptance in legal disputes. The enduring leadership of traditional agar culturing is largely due to its recognition by global regulatory bodies as the reference method against which all other tests are validated. When legal disputes arise regarding food safety or when regulatory agencies conduct official inspections, culture-based results are often the only data accepted as definitive proof of contamination or safety. The ability of culture methods to provide viable isolates for further characterization, such as serotyping or whole genome sequencing, adds value that rapid methods cannot always replicate. This regulatory entrenchment and legal defensibility ensure that, despite the rise of faster technologies, traditional methods remain the backbone of food safety testing protocols globally. The cost-effectiveness and broad accessibility of traditional agar culturing make it the preferred choice for routine screening, particularly for small and medium-sized enterprises and laboratories in developing regions. The equipment required for culture-based testing, such as incubators and autoclaves, represents a lower capital investment compared to the sophisticated instrumentation needed for molecular or immunoassay technologies. The reagents and media used in agar culturing are widely available and have long shelf lives, reducing supply chain complexities. The simplicity of the methodology allows technicians with basic microbiological training to perform tests reliably, addressing the global shortage of highly specialized staff. This economic and operational accessibility ensures that traditional technology remains the dominant workhorse of the industry, especially for initial screening, where turnaround time is less critical than cost and reliability.

The PCR technology segment is likely to experience the fastest CAGR of 9.2% over the forecast period. This surge of the segment is propelled by the urgent need for faster turnaround times to reduce inventory holding costs and the superior sensitivity of molecular methods in detecting low-level contamination. The critical need to accelerate decision-making within the food supply chain is the primary driver fueling the rapid adoption of PCR technology. Traditional methods can take days to yield results, forcing manufacturers to hold inventory in quarantine, which ties up capital and risks spoilage of perishable goods. PCR methods can provide definitive results in hours, enabling companies to release products to market much faster and significantly improving supply chain efficiency. The ability to obtain same-day results allows for real-time adjustments in production lines, preventing the mass production of contaminated batches. As just-in-time manufacturing becomes the norm, the speed advantage of PCR transforms it from a niche tool into a strategic necessity. This economic imperative to balance safety with operational velocity is propelling PCR to become the fastest-growing technology segment in the market. The exceptional sensitivity and specificity of PCR technology in detecting trace amounts of pathogen DNA within complex food matrices are key factors driving its accelerated growth. Unlike culture methods that rely on the viability and growth of organisms, PCR can detect genetic material from pathogens even if they are injured or present in very low numbers, reducing the risk of false negatives. The high sensitivity is crucial for testing processed foods where pathogens may be stressed by heat or preservatives. The ability of multiplex PCR to detect multiple pathogens simultaneously in a single reaction further enhances its utility and cost-efficiency for comprehensive screening. The United States Department of Agriculture has increasingly accepted PCR-based methods for regulatory compliance in various commodities, validating their reliability. As food formulations become more complex and global supply chains introduce diverse contamination risks, the precision of PCR offers a level of assurance that is unmatched. This technical superiority, combined with continuous advancements in automation and ease of use, ensures that PCR remains the fastest-evolving and most rapidly adopted technology in the sector.

REGIONAL ANALYSIS

North America Food Pathogen Testing Market Analysis

North America was the top performer in the global food pathogen testing market and captured a 36.5% share in 2025. The prominence of the North American market is supported by a highly litigious environment, stringent federal regulations, and advanced technological adoption. The market features mature infrastructure, with rapid testing widely adopted in corporate quality control. In addition, the strict regulatory framework maintained by agencies such as the FDA and USDA is a primary driving force. These agencies mandate rigorous testing under the Food Safety Modernization Act. The high prevalence of class-action lawsuits related to food safety incidents further compels manufacturers to adopt the most sensitive detection methods available to mitigate legal risks. Additionally, the presence of major technology developers in the region facilitates early access to innovative solutions such as next-generation sequencing and automated PCR systems. The consumer demand for transparency and clean labels also pushes retailers to require extensive testing data from suppliers. This convergence of regulatory pressure, economic stakes, and technological readiness solidifies North America's position as the largest and most sophisticated market for food pathogen testing globally.

Europe Food Pathogen Testing Market Analysis

Europe was the next prominent country in the food pathogen testing market and occupied a 28.6% in 2025. This position of the European market is fuelled by its harmonized regulatory approach and strong emphasis on precautionary principles. The market operates under stringent European Union guidelines, ensuring high consumer protection standards and safe, frictionless cross-border trade. Key drivers include complying with the General Food Law and specific European Commission microbiological criteria. These regulations require comprehensive testing for pathogens like Listeria and Salmonella in a wide range of food products. The "farm to fork" strategy adopted by the EU mandates testing at every stage of the supply chain, increasing the volume of samples analyzed. Furthermore, the high density of intra-European trade necessitates standardized testing protocols to ensure that products moving between member states meet uniform safety standards. Consumer trust in food safety is paramount in Europe, and any breach can lead to significant brand damage across the continent. The region's strong commitment to public health and its well-funded research initiatives into new detection methods sustain its status as a key pillar of the global market.

Asia Pacific Food Pathogen Testing Market Analysis

The Asia Pacific region is quickly growing in the food pathogen testing market owing to the rapid industrialization of the food sector and increasing export orientation. Market conditions are both diverse and fluid, ranging from stringent regulatory regimes in Australia and Japan to rapidly transforming landscapes in India and China. The dominant driving factor is the surging demand for food exports from the region to North America and Europe. This requires local manufacturers to adhere to strict international testing standards to gain market access. Rising disposable incomes and urbanization are also shifting domestic consumption patterns toward processed and packaged foods, prompting local governments to strengthen food safety laws. The Chinese government's revised Food Safety Law has significantly increased penalties for violations, driving a boom in testing services. Additionally, the occurrence of high-profile food safety scandals in the region has heightened public awareness and regulatory scrutiny. These factors combine to create a vibrant growth environment where investment in testing infrastructure is accelerating rapidly, positioning the Asia Pacific as the most promising frontier for market expansion.

Latin America Food Pathogen Testing Market Analysis

Latin America occupies a strategically important position in the global market due to its role as a major agricultural exporter and gradual improvements in domestic food safety regulations. The market is heavily focused on export compliance for meat, soy, and fruit, particularly for shipments to the U.S. and Europe, highlighting strict adherence to international regulations. Surging demand for food exports from the region to North America and Europe is the dominant driving factor. Consequently, local manufacturers must adhere to strict international testing standards to gain market access. Domestic markets are also evolving, with countries like Brazil and Mexico implementing stricter food safety codes following outbreaks of foodborne diseases. The Pan American Health Organization highlights that strengthening national food control systems is a priority for the region, leading to greater investment in laboratory capabilities. While resource constraints and fragmented supply chains pose challenges, the economic imperative of maintaining access to lucrative export markets ensures a steady demand for testing services. This export-led growth model makes Latin America a critical region for global food safety compliance.

Middle East and Africa Food Pathogen Testing Market Analysis

The Middle East and Africa region is likely to grow notably in the Europe food pathogen testing market from 2026 to 2034, owing to increasing food import dependency and government modernization efforts. The market status is heavily influenced by the need to ensure the safety of imported food products, which constitute a significant portion of the diet in many Gulf Cooperation Council countries and African nations. A significant driving factor is the implementation of new food safety regulations by governments aiming to protect public health and reduce the burden of foodborne diseases. In the Gulf region, high per capita income and a focus on luxury food imports drive demand for premium testing services to ensure quality. The Saudi Food and Drug Authority has recently updated its technical regulations to align with international standards, increasing testing requirements for incoming shipments. Furthermore, initiatives to develop local agricultural sectors in countries like Egypt and Nigeria are beginning to incorporate safety testing to support future exports.

COMPETITIVE LANDSCAPE

The competition in the global food pathogen testing market is characterized by intense rivalry among established multinational corporations and specialized biotechnology firms striving for technological superiority. The landscape is moderately consolidated with several key players dominating through extensive product portfolios and strong distribution networks. Competitive dynamics are driven by the constant race to reduce turnaround times while increasing sensitivity and specificity of detection methods. Price competition exists particularly in routine screening segments, but the primary battleground has shifted toward value-added services such as automation integration and data analytics. Regulatory compliance acts as a significant barrier to entry, ensuring that only firms with robust quality systems can sustain operations. Mergers and acquisitions are frequent as larger entities seek to absorb innovative startups and integrate complementary technologies like next-generation sequencing. This dynamic environment fosters continuous improvement in product performance and encourages the adoption of digital solutions that enhance traceability and efficiency across the global food supply chain.

KEY MARKET PLAYERS

A few of the notable companies dominating the global food pathogen testing market profiled in this report are

- SGS S.A.

- Bureau Veritas S.A.

- Thermo Fisher Scientific

- Merck KGaA

- Intertek Group PLC

- Eurofins Scientific

- Silliker, Inc.

- IFP Institut für Produktqualität GmbH

- ALS Limited

- Asurequality

- Microbac Laboratories, Inc.

- bioMérieux

- Genetic ID NA Inc.

TOP PLAYERS IN THE MARKET

- Thermo Fisher Scientific stands as a global leader in the food pathogen testing sector by providing a comprehensive portfolio of molecular diagnostics and traditional culture solutions. The company significantly contributes to the global market through its Invitrogen and Oxoid brands, which offer reliable reagents and instruments for detecting harmful microorganisms. Recently, Thermo Fisher has strengthened its position by launching advanced real-time polymerase chain reaction systems that deliver faster results for multiple pathogens simultaneously. They have also expanded their digital ecosystem to allow seamless data integration for food manufacturers seeking end-to-end traceability. Their continuous investment in research ensures the development of highly sensitive assays capable of identifying low-level contamination in complex food matrices. The company focuses on automation and ease of use. This approach empowers laboratories to increase throughput while maintaining rigorous accuracy standards.

- bioMérieux is a prominent player dedicated to improving public health through innovative diagnostic solutions, including specialized food safety testing kits and automated platforms. The company plays a vital role in the global market by offering the VIDAS system, which utilizes enzyme-linked fluorescent assay technology for rapid pathogen detection. Recent actions to bolster their market presence include the introduction of new single test kits for Listeria and Salmonella that reduce preparation time and minimize human error. bioMérieux has also enhanced its service offerings by providing extensive training programs and technical support to help food producers navigate complex regulatory requirements. Their commitment to sustainability is evident in efforts to reduce waste in testing processes. bioMérieux continues to set industry benchmarks for reliability and speed by leveraging decades of microbiological expertise. In doing so, they ensure that food supply chains remain safe from biological threats.

- Merck KGaA operates as a key contributor to the food pathogen testing market through its MilliporeSigma life science business, which supplies essential culture media and rapid detection tools. The company supports global food safety initiatives by providing high-quality agar plates and molecular reagents that serve as the foundation for accurate microbial analysis. To strengthen its market position, Merck recently launched a series of ready-to-use chromogenic media that simplify the identification of specific bacteria without requiring confirmatory tests. They have also invested in expanding their manufacturing capabilities to ensure consistent supply chains for critical testing materials worldwide. Furthermore, Merck actively collaborates with regulatory bodies and industry groups to validate new methods and establish best practices. Their focus on integrating digital tools with traditional testing workflows enables customers to manage data more effectively, reinforcing their status as a trusted partner in food safety.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the food pathogen testing market primarily focus on product innovation to develop faster and more sensitive detection technologies that meet evolving regulatory demands. Companies heavily invest in research and development to create multiplex assays capable of identifying multiple pathogens simultaneously within complex food matrices. Strategic acquisitions represent another major approach where large corporations purchase smaller niche firms to expand their portfolios and geographic reach. Market participants are increasingly adopting automation strategies to reduce manual labor and minimize human error in high-volume testing environments. Partnerships with regulatory agencies and industry associations help firms stay ahead of compliance changes and validate new methods quickly. Additionally, companies are expanding their service offerings to include comprehensive training and data management solutions that add value beyond simple testing kits. These combined strategies allow leading firms to maintain competitive advantages and drive growth in a dynamic landscape.

MARKET SEGMENTATION

This research report on the global food pathogen testing market has been segmented and sub-segmented based on type, food type, technology, and region.

By Type

- E.Coli

- Salmonella

- Listeria

- Other pathogens

By Food Type

- Meat & Poultry

- Dairy

- Processed Food

- Fruits & Vegetables

- Cereals & Grains

By Technology

- Traditional

- Agar Culturing

- Rapid

- Convenience-Based

- PCR

- Immunoassay

- Other Molecular-Based Tests

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the global food pathogen testing market?

The global food pathogen testing market involves detection of harmful pathogens in food to ensure safety and compliance with regulations for product quality and consumer health

2. What are the key drivers of growth in the global food pathogen testing market?

Growth is driven by rising foodborne illnesses, increased demand for packaged foods, strict food safety standards, and adoption of rapid, reliable testing technologies worldwide

3. Which pathogens are commonly tested in the global food pathogen testing market?

Common pathogens include Salmonella, E. coli, Listeria monocytogenes, and Campylobacter, which are major causes of food contamination and safety risks

4. What technologies are used in the global food pathogen testing market?

Technologies include microbiological, molecular, immunological methods, and rapid testing systems that improve sensitivity, speed, and accuracy of pathogen detection

5. How does the global food pathogen testing market impact food manufacturers?

It helps manufacturers meet regulatory compliance, avoid recalls, and ensure food safety by detecting contaminants throughout production and supply chains

6. What regions lead the global food pathogen testing market growth?

North America, Europe, and Asia-Pacific lead due to stringent regulations, consumer awareness, and high demand for safe and quality food products

7. How important is rapid testing in the global food pathogen testing market?

Rapid testing reduces turnaround times, enabling timely quality checks and faster market releases, boosting demand within the global food pathogen testing market

8. Which food products are covered in the global food pathogen testing market?

Testing spans dairy, meat, seafood, bakery, packaged foods, beverages, and ready-to-eat products to ensure broad safety coverage

9. What role do regulations play in the global food pathogen testing market?

Regulations like HACCP, ISO 22000, and FSMA govern testing to ensure food safety, driving adoption of advanced pathogen testing solutions worldwide

10. Who are the major players in the global food pathogen testing market?

Key players include 3M, PerkinElmer, Thermo Fisher Scientific, bioMérieux, Neogen, and Randox among others innovating in this market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com