Global Point of Care Diagnostics Market (POC Testing Market) Size, Share, Trends and Growth Forecast Report – Segmented By Product (Infectious Diseases, Cardiac Markers, Oncology Markers, OTC Diagnostic Tests, Drugs Of Abuse, Blood Gas Testing, Fertility Testing, Urinalysis, Coagulation, Hematology, Glucose Monitoring, Ambulatory Chemistry and Decentralized Clinical Chemistry) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis From 2024 to 2033

Global Point of Care Diagnostics Market Size

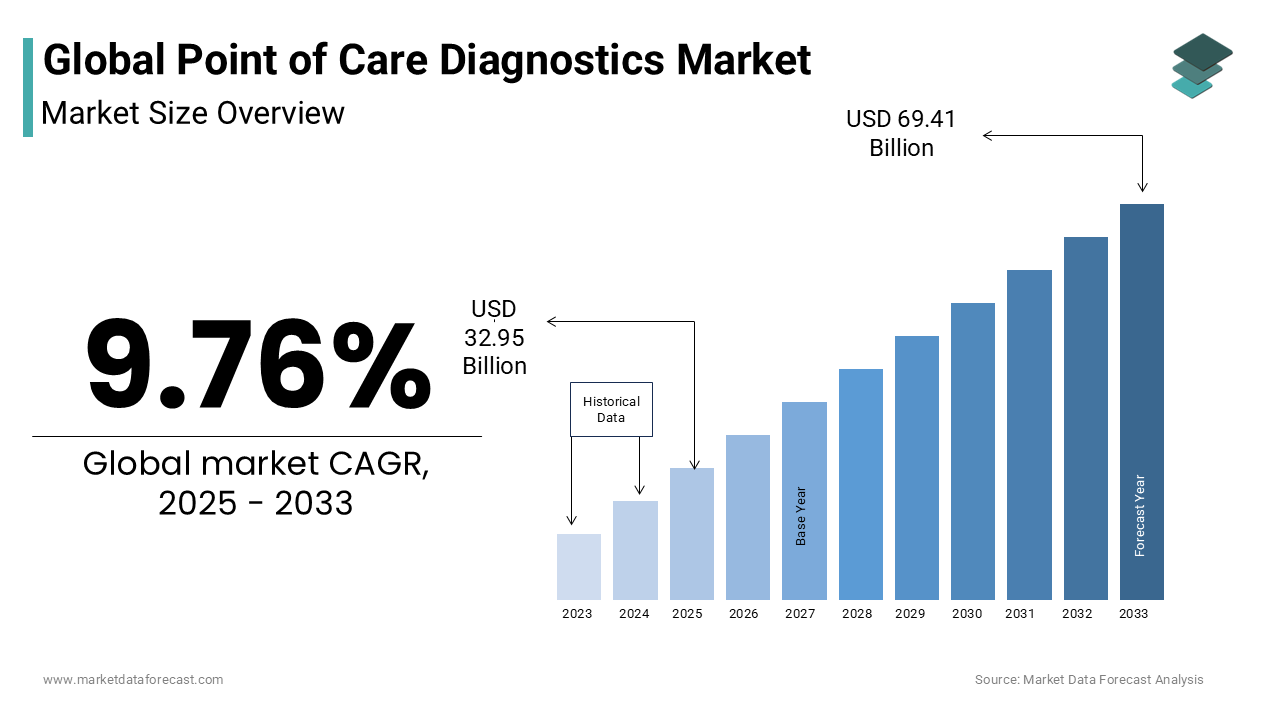

The global point of care (POC) diagnostics market is estimated to grow from USD 30.02 billion in 2024 to USD 69.41 billion in 2033, representing a CAGR of 9.76%.

The Point of Care Diagnostics (POCD) is a medical test conducted at or near the site of patient care, enabling rapid clinical decision-making outside traditional laboratory settings. These diagnostic tools are deployed in diverse environments, including clinics, ambulances, pharmacies, and home settings, delivering immediate results for conditions such as infectious diseases, diabetes, cardiovascular disorders, and pregnancy. The integration of microfluidics, biosensors, and digital connectivity has significantly advanced the accuracy and usability of these devices. As per the World Health Organization, over 50% of essential diagnostic tests in low-resource settings remain inaccessible, intensifying the need for decentralized testing solutions.

MARKET DRIVERS

Rising Burden of Chronic Diseases Driving Demand for Immediate Diagnostic Tools

The escalating global prevalence of chronic diseases, particularly diabetes and cardiovascular conditions, is a pivotal driver for the expansion of the point of care diagnostics market. As per the International Diabetes Federation, approximately 537 million adults were living with diabetes in 2021, a figure projected to rise to 643 million by 2030, with over half of these cases undiagnosed or poorly managed. This growing burden necessitates frequent monitoring and immediate intervention, which POCD devices facilitate through real-time glucose, HbA1c, and lipid profiling. In primary care settings, handheld HbA1c analyzers enable clinicians to assess long-term glycemic control during a single visit, improving patient adherence and reducing hospitalization rates. According to the American Heart Association, cardiovascular diseases account for nearly 18 million deaths annually worldwide, with delayed diagnosis contributing significantly to mortality. POCD platforms for cardiac biomarkers such as troponin and BNP allow emergency departments and rural clinics to triage high-risk patients within minutes.

Expansion of Healthcare Access in Underserved and Remote Regions

The urgent need to bridge healthcare disparities in rural and low-resource settings is additionally propelling the growth of the point of care diagnostics (POCD) market. In countries like Indonesia and Nigeria, over 60% of the population resides in remote regions where transportation to urban medical centers can take days. The World Health Organization’s 2023 Essential Diagnostics List explicitly advocates for decentralized testing to improve access to health services. According to Médecins Sans Frontières, 50% reduction in tuberculosis diagnosis time after introducing molecular POCD platforms in mobile clinics. The U.S. National Institutes of Health emphasizes that rapid diagnostic tests for HIV and syphilis in antenatal clinics in sub-Saharan Africa have increased treatment coverage by over 40%, which is directly impacting maternal and neonatal outcomes.

MARKET RESTRAINTS

Regulatory Heterogeneity and Lack of Standardization Across Regions

The fragmented and inconsistent regulatory landscape across countries, which impedes device approval, commercialization, and clinical adoption is solely hampering the growth of the point of care diagnostics market. As per the Global Fund, over 70 low- and middle-income countries lack a functional national regulatory authority for medical devices, which is leading to delayed market entry and inconsistent quality control. The U.S. Food and Drug Administration requires rigorous analytical and clinical performance data for CLIA-waived status, which many POCD devices fail to achieve, limiting their use in non-laboratory settings.

Limited Accuracy and Reliability Compared to Centralized Laboratory Testing

The analytical performance of the testing devices may vary in real time procedures which is also hindering the growth of the point of care diagnostics market. As per the Foundation for Innovative New Diagnostics (FIND), rapid antigen tests for infectious diseases exhibit sensitivity rates as low as 60–70% compared to PCR-based laboratory methods, which leads to potential false negatives and misdiagnosis. The College of American Pathologists, variability in operator skill, environmental conditions, and sample handling at the point of care can further compromise test accuracy.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Digital Health Platforms

The integration of artificial intelligence (AI) and digital health infrastructure is to create opportunities for the growth of the point of care diagnostics market. AI-powered algorithms can enhance diagnostic accuracy by analyzing test results in conjunction with patient history, symptoms, and epidemiological data. Companies like DarioHealth and Abbott are embedding machine learning into glucose monitoring systems to predict hypoglycemic events up to 30 minutes in advance. Furthermore, integration with electronic health records (EHRs) and telemedicine platforms enables seamless data transmission by allowing remote clinicians to make timely decisions.

Growing Adoption in Home-Based and Self-Testing Scenarios

The shift toward patient-centric care and self-management in home environments is additionally to amplify the growth of the point of care diagnostics market. As per the U.S. Census Bureau, 77% of American adults now own a smartphone by enabling widespread use of connected diagnostic devices such as smart glucometers, at-home STI test kits, and portable ECG monitors.

MARKET CHALLENGES

Ensuring Data Security and Privacy in Connected Diagnostic Devices

The risk of data breaches and cyber threats escalates is escalating, driving up the growth of the point of care diagnostics market. Many POCD platforms now transmit sensitive health information via Bluetooth or cloud-based systems, which is making them vulnerable to hacking. According to the U.S. Department of Health and Human Services, healthcare data breaches affected over 49 million individuals in 2023 alone, with medical devices identified as emerging attack vectors. The FDA issued a safety communication in 2023 warning of cybersecurity vulnerabilities in certain wireless glucose monitors that could allow unauthorized access to patient data. In Europe, according to the European Union Agency for Cybersecurity, 38% of connected medical devices lack adequate encryption protocols. In India, the Digital Information Security in Healthcare Act (DISHA) is still pending, which is leaving patient data from POCD systems in a regulatory grey zone.

Maintaining Supply Chain Resilience for Diagnostic Components

The global supply chain for point of care diagnostics faces persistent vulnerabilities in the sourcing of biosensors, microfluidic chips, and rare reagents. As per the World Trade Organization, disruptions during the pandemic caused a 30% decline in the global shipment of diagnostic components in 2021, affecting availability in over 100 countries. In 2022, the U.S. Food and Drug Administration listed over 20 diagnostic products under shortage due to semiconductor and plastic resin shortages. Additionally, cold chain requirements for certain assays limit distribution in tropical regions. These supply constraints delay deployment, inflate costs, and undermine public health responses, particularly during outbreaks. Building regional manufacturing capacity and diversifying suppliers are essential to ensuring uninterrupted access to life-saving POCD tools.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2024 to 2033 |

| Segments Covered | By Product, End-User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key Market Players | Abbott Laboratories, Inc., Danaher Corporation, Roche Diagnostics Limited, BioMerieux, Siemens Healthcare, Beckman Coulter, Inc., Becton, Dickinson and Company, Johnson & Johnson, Alere Inc., and PTS Diagnostics. |

SEGMENTAL ANALYSIS

By Product Insights

The glucose monitoring segment accounted in holding 28.3% of the global point of care diagnostics market share in 2024 owing to the prevalence of diabetes worldwide is the cornerstone of this segment’s dominance. Type 2 diabetes, which constitutes over 90% of cases require daily glucose monitoring to prevent complications such as neuropathy, retinopathy, and cardiovascular events. Additionally, the integration of continuous glucose monitoring (CGM) systems such as Abbott’s FreeStyle Libre and Dexcom G7 into routine care has accelerated adoption. These devices now offer real-time alerts, smartphone connectivity, and AI-driven trend analysis by enhancing patient compliance and clinical outcomes.

The oncology markers segment is expected to grow with an expected CAGR of 12.4% in the next coming years with the rising global cancer burden and the urgent need for early detection. As per the International Agency for Research on Cancer, cancer incidence reached 20 million new cases in 2022, with projections indicating a 47% increase by 2040 in low- and middle-income countries. Point-of-care tests for tumor markers such as PSA, CA-125, and CEA are increasingly being deployed in primary care clinics and mobile screening units to enable rapid triage. Furthermore, advancements in liquid biopsy technologies and microfluidic platforms are enabling non-invasive, real-time cancer monitoring at the bedside.

REGIONAL ANALYSIS

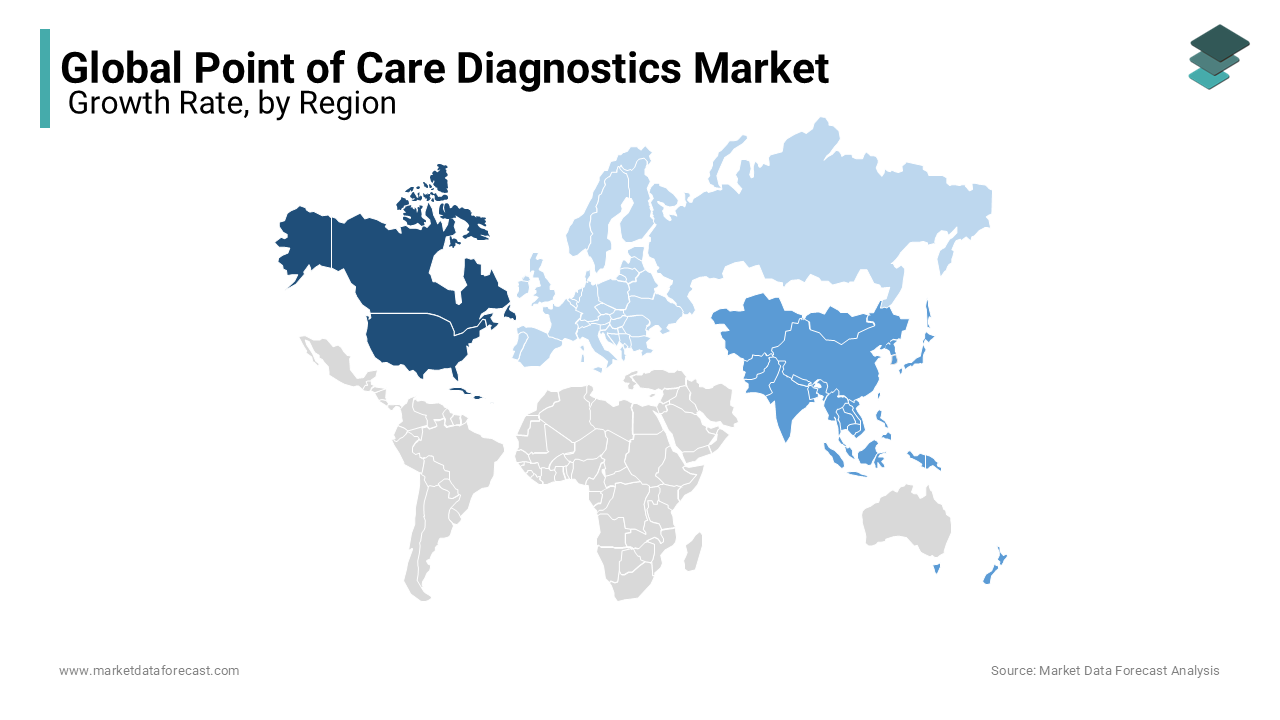

North America Point of Care Diagnostics (POCD) Market Insights

North America was the top performer in the global point of care diagnostics market by capturing 38.3% of share in 2024 with its advanced healthcare infrastructure, high healthcare expenditure, and strong regulatory framework that fosters innovation. According to the Centers for Medicare & Medicaid Services, national health spending reached $4.5 trillion in 2022, with diagnostics representing a growing segment. The FDA’s expedited clearance pathways, such as the Breakthrough Devices Program, have accelerated the approval of novel POCD platforms, including AI-integrated glucose monitors and rapid sepsis panels.

Europe Point of Care Diagnostics (POCD) Market Insights

Europe was positioned second with 29.3% of the point of care diagnostics market share in 2024 owing to the well-established healthcare systems, high physician adoption of decentralized testing, and a growing emphasis on preventive care. Additionally, the EU4Health program has allocated €500 million for digital health integration, including point-of-care platforms for cardiovascular and infectious diseases. These systemic investments are coupled with aging populations and rising chronic disease rates that sustain Europe’s strong market position.

Asia Pacific Point of Care Diagnostics (POCD) Market Insights

The Asia-Pacific point of care diagnostics market growth is likely to grow with dominant CAGR during the forecast period. Countries like China, India, and Japan are driving expansion through aggressive healthcare reforms, rising medical tourism, and increasing investment in diagnostic infrastructure. In India, the National Health Mission has deployed over 150,000 point-of-care devices across rural health centers by enabling rapid testing for anemia, HIV, and tuberculosis, as confirmed by the Ministry of Health and Family Welfare. China’s “Healthy China 2030” initiative includes a $120 billion investment in primary care modernization, with a focus on decentralized diagnostics in tier-2 and tier-3 cities.

Latin America Point of Care Diagnostics (POCD) Market Insights

Latin America point of care diagnostics market is likely to grow steadily in the coming years. Brazil’s Unified Health System (SUS) has integrated rapid molecular tests for tuberculosis and HIV into over 5,000 primary care units, reducing diagnosis time from weeks to hours, as reported by the Brazilian Ministry of Health. The country has expanded its diabetes screening programs using POCD in community health centers, reaching over 2 million patients annually. Argentina has implemented national point-of-care syphilis testing in prenatal clinics, contributing to a 33% decline in congenital syphilis cases between 2018 and 2022, as cited by the National Directorate of Epidemiology. However, challenges such as import dependency and uneven reimbursement persist.

Middle East and Africa Point of Care Diagnostics (POCD) Market Insights

The Middle East and Africa point of care diagnostics market growth is expected to grow with the high strategic importance due with its vast unmet diagnostic needs and growing public health investments. The UAE has emerged as a regional hub for medical innovation by launching the “Weqaya” national screening program that uses POCD for diabetes and cardiovascular risk in over 300,000 citizens annually, as reported by the Dubai Health Authority.

KEY MARKET PLAYERS

Notable market participants in the Global Point of Care Diagnostics Market profiled Abbott Laboratories, Inc., Danaher Corporation, Roche Diagnostics Limited, BioMerieux, Siemens Healthcare, Beckman Coulter, Inc., Becton, Dickinson and Company, Johnson & Johnson, Alere Inc., and PTS Diagnostics. Key market players are investing more in R&D to develop innovative products and expand revenues through collaborations with other companies, research universities, and private research organizations.

The point of care diagnostics market is marked by intense competition driven by technological differentiation, speed of innovation, and strategic positioning in high-growth regions. Established players like Abbott, Roche, and Danaher compete not only on device accuracy and speed but also on ecosystem integration, including digital connectivity, data management, and remote monitoring capabilities. The race to miniaturize molecular diagnostics while maintaining sensitivity has intensified, particularly in infectious disease and oncology applications. Furthermore, public health mandates, pandemic preparedness funding, and national screening programs influence procurement dynamics. As healthcare systems increasingly prioritize early diagnosis and decentralized care, the competitive landscape is evolving toward integrated, scalable, and interoperable diagnostic solutions that deliver actionable insights at the bedside, pharmacy, or home.

Top Players in the Market

Abbott Laboratories

Abbott is a dominant force in the point of care diagnostics market, particularly across the Asia-Pacific region, where its rapid, portable testing platforms have become essential in both urban clinics and remote health centers. The company’s i-STAT handheld blood analyzer delivers results for blood gases, electrolytes, and cardiac markers within minutes, supporting emergency and intensive care settings. In India and Southeast Asia, Abbott’s Panbio™ rapid antigen tests have been widely deployed for infectious disease screening, including dengue, malaria, and COVID-19, in alignment with national public health programs. In 2023, Abbott expanded its manufacturing footprint in Malaysia to enhance regional supply resilience. It also partnered with governments in Indonesia and the Philippines to strengthen decentralized testing infrastructure.

Roche Diagnostics

Roche Diagnostics plays a pivotal role in advancing point of care testing in the Asia-Pacific region through its high-precision, scalable diagnostic platforms. The company’s cobas® Liat system, a fully automated molecular POCT platform, enables rapid detection of respiratory pathogens, including influenza and SARS-CoV-2, within 20 minutes, making it ideal for clinics and hospitals with limited lab access. In Japan, Roche collaborated with local health authorities to deploy the cobas® Liat in outpatient facilities, improving early intervention rates. In Australia, the Therapeutic Goods Administration approved Roche’s cobas HIV-1 qualitative test for near-patient use by enhancing maternal screening in rural areas. Roche has also strengthened its presence through training programs for healthcare providers in India and Vietnam by ensuring proper device utilization.

Danaher Corporation (via Cepheid)

Danaher, through its subsidiary Cepheid, is a key innovator in molecular point of care diagnostics, with significant influence across the Asia-Pacific region. The GeneXpert platform, which is renowned for its rapid, cartridge-based testing, is widely used for tuberculosis, HIV, and antimicrobial resistance detection in high-burden countries like India, Indonesia, and South Africa. In India, over 2,500 GeneXpert machines have been installed under the National TB Elimination Program, enabling same-day diagnosis and treatment initiation. Cepheid has localized service and supply chains to reduce turnaround times and improve uptime. In 2023, Danaher launched the Xpert Xpress CoV-2/Flu/RSV test in Japan and South Korea, supporting winter respiratory disease management. The company also partnered with public health agencies to expand access in rural and underserved areas.

Top Strategies Used by the Key Market Participants

Key players in the point-of-care diagnostics market employ strategic initiatives centered on technological innovation, regulatory expansion, and public-private collaboration. Companies prioritize the development of multiplexed, automated platforms that deliver lab-quality results in minutes. Expansion into emerging markets is achieved through localized manufacturing, which simplifies device interfaces, and ruggedized designs for challenging environments. Strategic partnerships with governments and global health organizations facilitate large-scale deployment in infectious disease control programs. Regulatory approvals across diverse geographies, including CE marking, FDA clearance, and WHO prequalification, are pursued to enable global market access. Additionally, companies are acquiring niche technology firms to accelerate R&D in microfluidics and biosensors. These strategies collectively strengthen product portfolios, improve accessibility, and reinforce competitive positioning in the rapidly evolving point of care diagnostics landscape.

RECENT MARKET HAPPENINGS

- In January 2022, Abbott launched the ID NOW Omni, a portable molecular diagnostic device, in Australia and South Korea by enabling the rapid detection of respiratory viruses in clinics and pharmacies, thereby expanding its decentralized testing footprint.

- In June 2022, Roche received the CE mark for the cobas Liat SARS-CoV-2 & Flu A/B test, allowing European and APAC markets to deploy the platform for multiplexed respiratory testing in near-patient settings.

- In March 2023, Danaher’s Cepheid announced a partnership with the Indian government to deploy 500 additional GeneXpert systems in rural districts for TB and drug-resistant TB screening by enhancing diagnostic equity.

- In September 2023, Abbott received FDA clearance for the FreeStyle Libre 3 Integrated CGM System and subsequently launched it in Japan, which is marking a significant expansion of its glucose monitoring dominance in the Asia-Pacific region.

- In February 2024, Roche launched the cobas HIV-1 Qualitative test on the cobas® Liat platform in South Africa, which is supporting early infant diagnosis and strengthening its presence in public health-driven POCT programs.

MARKET SEGMENTATION

This market research report on the global point-of-care diagnostics market (POC testing market) has been segmented and sub-segmented based on the product, end-user, and region.

By Product

- Infectious Diseases

- Cardiac Markers

- Oncology Markers

- OTC Diagnostic Tests

- Drugs Of Abuse

- Blood Gas Testing

- Fertility Testing

- Urinalysis

- Coagulation

- Hematology

- Glucose Monitoring

- Ambulatory Chemistry

- Decentralized Clinical Chemistry

By End-User

- Clinics

- Hospitals

- Home Healthcare

- Ambulatory Care Settings

- Laboratories

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

Which factors contribute to the growth of point of care diagnostics in Europe?

Factors such as the increasing prevalence of chronic diseases and the demand for rapid diagnostics contribute to the growth of point-of-care diagnostics market in Europe.

What are the emerging trends in Point of Care diagnostics in the Middle East and Africa?

The Middle East and Africa are witnessing a trend towards decentralized healthcare, driving the adoption of Point of Care diagnostics for quicker and more accessible medical results.

What are the challenges faced by Point of Care diagnostics companies in South America?

Challenges include navigating complex regulatory landscapes and addressing affordability concerns, which impact market penetration in South America.

How is the Point of Care diagnostics market in the Asia-Pacific region adapting to the increasing demand for personalized medicine?

The market is witnessing a shift towards the development of Point of Care diagnostics tailored for personalized medicine, reflecting the growing demand for individualized healthcare in the Asia-Pacific region.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com