- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

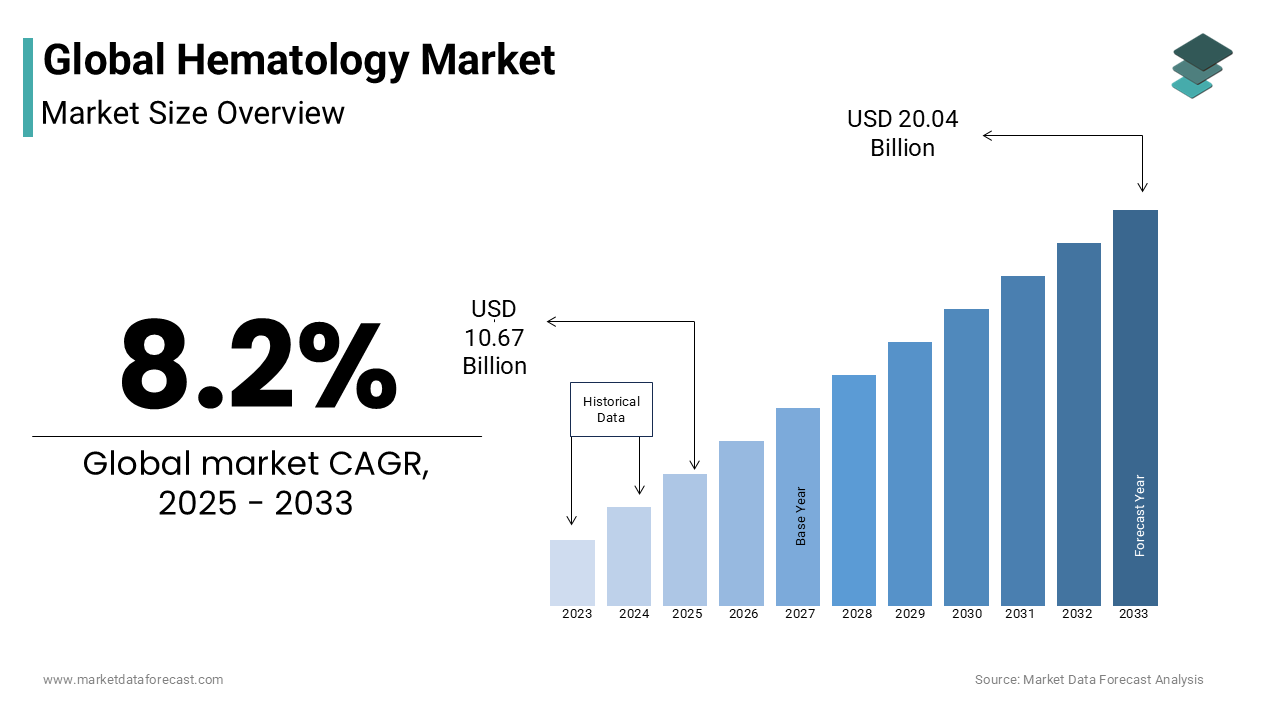

Market Size, 2025

$10.67 BnMarket Estimate, 2026

$11.54 BnMarket Forecast, 2034

$21.68 BnCAGR, 2026–2034

8.2%Global Hematology Market Size

The global hematology market size was valued at USD 10.67 billion in 2025 and is anticipated to reach USD 11.54 billion in 2026 from USD 21.68 billion by 2034, growing at a CAGR of 8.2% during the forecast period from 2026 to 2034.

Hematology refers to the diagnostic and therapeutic technologies used to study blood, blood-forming tissues, and disorders affecting hematopoiesis, coagulation, and immune function. This includes automated hematology analyzers, flow cytometers, molecular diagnostic platforms, reagents, and specialized assays for conditions such as anemia, leukemia, hemophilia, and thrombocytopenia. Blood remains one of the most critical diagnostic fluids in clinical medicine, with a single complete blood count (CBC) offering insights into infection, inflammation, nutritional deficiencies, and malignancy. As per the World Health Organization, an estimated 1.6 billion people worldwide suffer from anemia, primarily due to iron deficiency, making hematology testing a cornerstone of public health screening. In sub-Saharan Africa, where infectious diseases like malaria and HIV disproportionately impact hematological parameters, routine blood analysis is integral to disease management. The U.S. Centers for Disease Control and Prevention reports that over 480 million CBC tests are performed annually in the United States alone, underscoring the test’s ubiquity in both primary and specialized care. Furthermore, the integration of hematology with oncology—particularly in the monitoring of hematologic malignancies—has elevated the demand for high-precision instrumentation and longitudinal patient tracking. The emergence of point-of-care hemoglobinometers and automated differentials in low-resource settings reflects a broader trend toward decentralizing blood diagnostics, improving early detection, and reducing treatment delays.

MARKET DRIVERS

Rising Global Burden of Hematologic Malignancies and Chronic Blood Disorders

The increasing incidence of hematologic cancers and chronic blood diseases is a pivotal force driving demand for advanced hematology diagnostics and monitoring systems. In the United States, the American Cancer Society estimates that 1.5% individuals will be diagnosed with leukemia during their lifetime, necessitating frequent blood testing for diagnosis, treatment response, and relapse surveillance. Similarly, chronic anemias such as thalassemia and sickle cell disease have high prevalence in South Asia, the Middle East, and Sub-Saharan Africa. This growing disease burden has intensified the need for high-throughput, accurate hematology analyzers capable of detecting subtle morphological and immunophenotypic changes. In India, a high number of new cases of thalassemia are diagnosed annually, prompting government-backed screening programs that rely on automated CBC and HPLC (high-performance liquid chromatography) systems. Additionally, patients with myelodysplastic syndromes require monthly blood monitoring, generating sustained demand for reagents and consumables. With aging populations in high-income countries increasing susceptibility to clonal hematopoiesis and myeloid malignancies, the clinical imperative for robust hematology infrastructure continues to expand, reinforcing the market’s growth trajectory.

Integration of Artificial Intelligence and Digital Pathology in Blood Cell Analysis

The incorporation of artificial intelligence (AI) and digital imaging into hematology workflows is revolutionizing the accuracy, speed, and scalability of blood cell analysis. Traditional manual microscopy, which requires skilled technologists to classify white blood cells from stained smears, is time-consuming and subject to inter-observer variability. AI-powered digital morphology systems enable automated cell classification with high accuracy. These systems utilize deep learning algorithms trained on millions of annotated cell images, allowing for rapid detection of blast cells, dysplastic forms, and rare populations indicative of malignancy. In clinical settings, companies like CellaVision and Scopio Labs have introduced FDA-cleared platforms that digitize peripheral blood smears and provide AI-assisted interpretations, reducing turnaround time from hours to minutes. Furthermore, tele-hematology networks are emerging in rural India and Sub-Saharan Africa, where digitized slides are transmitted to centralized labs for expert review, overcoming local shortages of hematopathologists. The integration of AI not only enhances diagnostic precision but also supports standardization across laboratories, making it a transformative driver in both resource-rich and constrained environments.

MARKET RESTRAINTS

High Cost and Limited Accessibility of Advanced Hematology Instruments in Low-Income Regions

A significant barrier to the expansion of the hematology market is the prohibitive cost of advanced diagnostic equipment, which remains out of reach for many healthcare facilities in low- and middle-income countries. In Nigeria, only y few public hospitals in rural areas possess functional automated analyzers, forcing reliance on manual counting methods prone to error. Additionally, the supply chain for reagents and calibration materials is fragile in regions with poor cold chain infrastructure, resulting in frequent stockouts. Sub-Saharan Africa faces a shortfall in essential diagnostic reagents annually due to import dependencies and customs delays. Even when equipment is donated, a lack of technical training and service support leads to rapid obsolescence. Without sustainable financing models and localized service networks, the disparity in hematology diagnostics will persist, constraining market penetration despite high clinical need.

Shortage of Skilled Hematology Technologists and Diagnostic Personnel

The global deficit of trained professionals capable of operating and interpreting hematology instruments severely limits the effective utilization of advanced diagnostic systems. Moreover, there is a notable shortfall of laboratory technicians worldwide, with the most acute shortages in South Asia and Sub-Saharan Africa. This scarcity is particularly critical in hematology, where expertise in peripheral smear review, flow cytometry, and molecular testing is essential for diagnosing complex disorders like leukemia and myelodysplasia. Even in high-income countries, the aging workforce and declining enrollment in medical laboratory science programs are creating bottlenecks. Furthermore, the complexity of next-generation platforms—such as mass cytometry and NGS-based profiling requires continuous upskilling, yet structured continuing education remains inconsistent. Without coordinated investment in education, certification, and career development, the full potential of advanced hematology technologies will remain unrealized, especially in settings where diagnostic accuracy directly impacts patient survival.

MARKET OPPORTUNITIES

Expansion of Point-of-Care and Portable Hematology Devices in Resource-Limited Settings

The development and deployment of portable, battery-operated hematology devices present a transformative opportunity to bridge diagnostic gaps in remote and underserved regions. Traditional hematology analyzers require stable power, climate control, and trained operators, making them impractical in rural clinics and mobile health units. However, innovations such as handheld hemoglobinometers, microfluidic CBC devices, and smartphone-integrated analyzers are overcoming these barriers. Also, devices like the HemoCue Hb 301 can deliver hemoglobin results in seconds using a single drop of blood, enabling mass screening for anemia in community health campaigns. The U.S. Food and Drug Administration has cleared several compact analyzers, including the Orison CBC System, which performs full blood counts from capillary blood without reagents. Hence, these devices are poised to revolutionize access to life-saving blood diagnostics.

Advancements in Liquid Biopsy and Circulating Tumor Cell (CTC) Analysis for Hematologic Monitoring

Liquid biopsy technologies, particularly those focused on circulating tumor cells (CTCs) and cell-free DNA (cfDNA) in blood, are unlocking new frontiers in non-invasive monitoring of hematologic malignancies. Unlike solid tumors, hematologic cancers are inherently accessible through peripheral blood, making them ideal candidates for serial liquid biopsies to track clonal evolution, minimal residual disease (MRD), and treatment resistance. Moreover, CTC enumeration in multiple myeloma patients demonstrated a high correlation with bone marrow biopsy results, enabling less invasive disease assessment. Companies like Menarini Silicon Biosystems and Bio-Rad have developed platforms such as the DEPArray and ddPCR systems that isolate and characterize rare CTCs with single-cell resolution, facilitating personalized therapy adjustments. In chronic lymphocytic leukemia (CLL), the German Chronic Lymphocytic Leukemia Study Group found that cfDNA analysis detected MRD with high concordance, outperforming flow cytometry in some cases. The U.S. Food and Drug Administration has granted breakthrough designation to several liquid biopsy assays for hematologic cancers, accelerating clinical adoption. Additionally, integration with next-generation sequencing allows for real-time mutation tracking, such as in TP53 or FLT3 genes, guiding targeted therapy decisions. With clinical trials increasingly incorporating liquid biopsy endpoints, and reimbursement pathways expanding in the EU and U.S., this technology is transitioning from research to routine care, creating a high-growth avenue within the hematology market.

MARKET CHALLENGES

Regulatory Complexity and Variability in Diagnostic Test Approval Processes

The hematology diagnostics market faces substantial operational challenges due to fragmented and evolving regulatory frameworks governing test validation, instrument clearance, and laboratory-developed tests (LDTs). In the European Union, the In Vitro Diagnostic Regulation (IVDR) implemented in 2022 has significantly increased the burden of clinical evidence and post-market surveillance, delaying the commercialization of new hematology assays. Also, many Class C and D IVDs, including leukemia profiling panels, faced approval delays several months post-IVDR. Emerging markets present additional hurdles. Brazil’s ANVISA enforces stringent biocompatibility and performance testing, while China’s National Medical Products Administration requires data localization and on-site audits. These divergent requirements compel manufacturers to maintain multiple regulatory dossiers and quality systems, inflating R&D and compliance expenditures. Without global alignment, companies—especially small innovators—face sustained barriers to scalability and market access, impeding the timely delivery of life-saving diagnostics.

Preanalytical Variability and Sample Integrity Issues in Hematology Testing

Preanalytical errors, occurring during sample collection, transport, and handling, represent one of the most persistent challenges in hematology diagnostics, significantly impacting result accuracy and clinical decision-making. Improper mixing, delayed processing, incorrect anticoagulant ratios, and temperature fluctuations can lead to platelet clumping, hemolysis, or cell swelling, distorting CBC parameters. Also, 40.2% of hematology specimens in U.S. hospitals were rejected due to clotting or hemolysis, causing delays in diagnosis and repeat phlebotomy. In low-resource settings, the problem is exacerbated. Additionally, microsampling techniques used in point-of-care devices require strict adherence to volume and mixing procedures, which frontline workers often overlook. These inconsistencies undermine the reliability of hematology results, particularly in critical conditions like sepsis or leukemia, where timely and accurate data are essential. Addressing preanalytical variability requires systemic improvements in training, logistics, and quality control, posing a complex but necessary challenge for the industry.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, End-User, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leader Profiled | Siemens AG Healthcare, Johnson & Johnson, Beckman Coulter, Inc., Abbott Laboratories, Thermo Fisher Scientific, Roche, HORIBA Ltd., Sysmex Corporation, Bio-Rad Laboratories Inc., Boule Diagnostics AB, Mindray Medical International Limited. |

SEGMENTAL ANALYSIS

By Product Insights

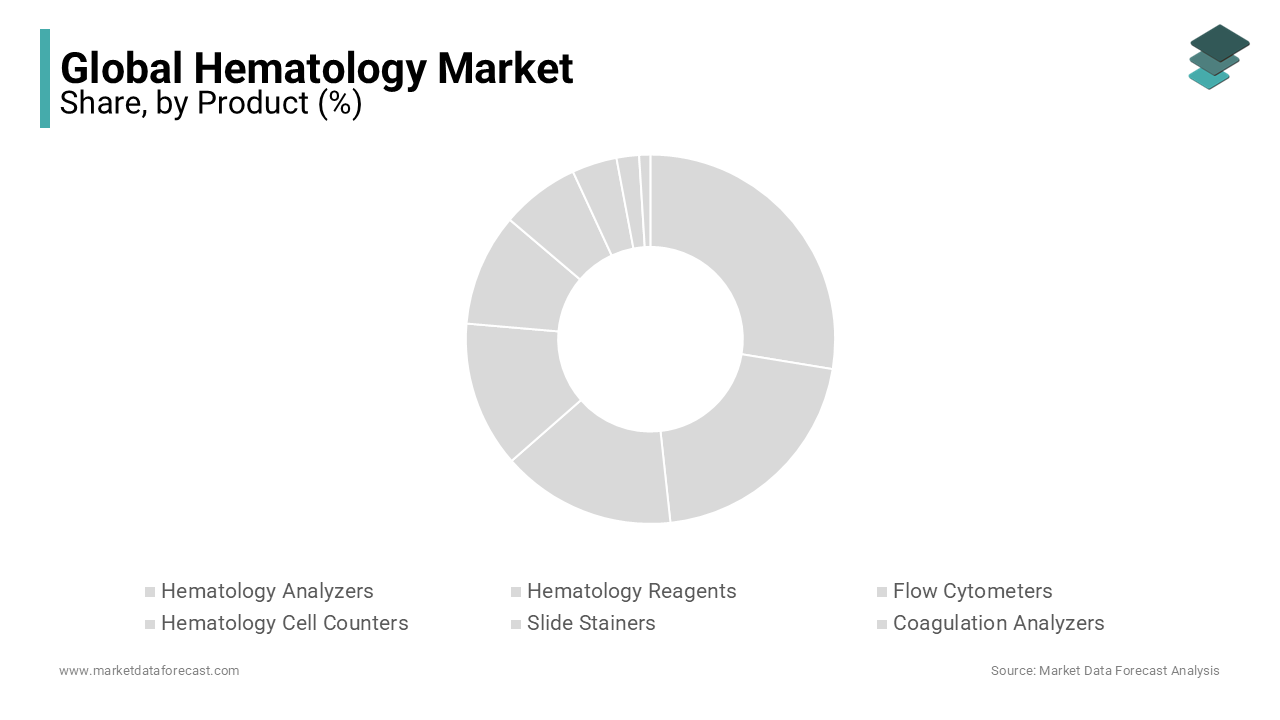

The hematology analyzers segment dominated the global hematology market by accounting for 3.5% of the total share in 2024. This segment’s dominance is credited to the increasing reliance on automated, high-throughput systems for complete blood count (CBC) and differential blood analysis in clinical diagnostics. The escalating global burden of hematological conditions such as anemia, leukemia, and thrombocytopenia is fueling demand for accurate and rapid diagnostic tools. Anemia affects a large percentage of people globally, with many children under five and pregnant women affected. In the United States alone, a significant number of new cases of leukemia, lymphoma, and myeloma were diagnosed, necessitating frequent blood monitoring. These conditions require regular CBC testing, which is primarily conducted using hematology analyzers. The integration of artificial intelligence and advanced algorithms in modern analyzers enables early detection and improved diagnostic precision, further solidifying their indispensability in clinical workflows. The proliferation of diagnostic centers and hospital laboratories, especially in emerging economies, has significantly increased the deployment of hematology analyzers. In addition, India added over 23,000 diagnostic labs by 2022. In high-income countries, a significant share of hospitals and diagnostic labs use fully automated hematology analyzers, driven by regulatory standards and the need for rapid turnaround times. This widespread institutional adoption underscores the segment’s entrenched position in global diagnostics.

The flow cytometers segment is emerging as the fastest-growing product in the hematology market and is projected to expand at a CAGR of 10.4% through 2033. This surge is fueled by their critical role in immunophenotyping, stem cell research, and cancer diagnostics. Flow cytometry has become indispensable in cancer immunophenotyping, particularly in diagnosing leukemias and lymphomas. With the global oncology market expanding, the demand for advanced diagnostic tools like flow cytometers is rising in tandem. The advent of high-parameter flow cytometers capable of analyzing 20+ markers simultaneously has revolutionized minimal residual disease (MRD) detection. The global surge in cell and gene therapy development is a pivotal growth catalyst. As per the Alliance for Regenerative Medicine, global investment in cell therapy reached USD 27.8 billion in 2023, with CAR-T cell therapies leading the charge. Flow cytometry is essential for characterizing T-cell populations pre- and post-infusion. As personalized medicine gains traction, flow cytometers are evolving into multi-laser, high-speed platforms, further accelerating adoption across clinical and research settings.

By Application Insights

The Cancer diagnostics segment stood as the prominent application in the hematology market by capturing 32.5% of the global share in 2024. This position in the market is because of the indispensable role of blood-based diagnostics in hematological malignancies and systemic cancer monitoring. Blood cancers constitute a significant portion of the global cancer burden. In the United States, the American Cancer Society estimates that blood cancers represent nearly 10% of all new cancer diagnoses, with one person diagnosed every three minutes. These conditions require repeated hematological testing, including CBC, peripheral smear analysis, and flow cytometry, to monitor disease progression and treatment response. The integration of hematology into oncology care pathways has made it a cornerstone of cancer management, ensuring sustained market dominance. The emergence of liquid biopsies has expanded the role of hematology in solid tumor monitoring. While traditionally used for blood cancers, hematology platforms now support CTC enumeration and characterization. This convergence of hematology and oncology diagnostics is reinforcing the segment’s leadership in clinical practice.

The infectious diseases application segment is growing at a CAGR of 9.8% and is the highest among all hematology applications. It is driven by the critical role of blood testing in diagnosing and monitoring infections. The COVID-19 pandemic underscored the need for scalable, rapid hematological testing. Countries like Germany and South Korea integrated hematology analyzers into primary care clinics to monitor neutrophil-to-lymphocyte ratios (NLR), a prognostic marker for severe infection. Also, over 1 million deaths in 2021 were directly attributable to drug-resistant infections, necessitating rapid CBC and differential counts to guide antibiotic use. As a result, governments are investing in decentralized testing. Malaria, dengue, HIV, and tuberculosis continue to drive hematology testing demand in tropical and low-income regions. The World Health Organization states that malaria caused 249 million cases and 608,000 deaths in 2022. Similarly, dengue cases have increased 30-fold globally over the past five decades, with thrombocytopenia being a key diagnostic criterion. This sustained focus on infectious disease control is accelerating the adoption of hematology platforms in public health systems worldwide.

By End-User Insights

The hospitals segment commanded the major share of the hematology market at 45.3% of global revenue in 2024. As primary care delivery hubs, hospitals perform the majority of urgent and routine hematological tests, from emergency CBCs to oncology monitoring. Large hospitals process thousands of blood tests daily. Modern hematology analyzers are increasingly integrated with hospital information systems (HIS) and electronic medical records (EMR). This connectivity enhances diagnostic accuracy and supports value-based care models, making hospitals the preferred site for high-complexity hematology testing and driving sustained equipment demand.

The diagnostic laboratories segment is experiencing the fastest growth in the end-user segment and is expanding at a CAGR of 11.2. This surge is driven by the shift toward centralized, high-efficiency testing models. Hospitals are increasingly outsourcing non-urgent testing to specialized labs to reduce costs and improve efficiency. Large reference labs like LabCorp and Quest Diagnostics process a substantial volume of tests annually, with hematology comprising a notable share of their volume. In India, Dr. Lal PathLabs and Metropolis handle millions of tests per year. The global trend toward lab consolidation is evident. This centralization enables faster, cheaper, and more standardized testing, fueling growth. Private investment in diagnostic networks is accelerating in emerging markets. In Africa, South Africa’s Lancet Laboratories serves 14 countries across the continent, leveraging centralized hematology hubs. This infrastructure growth, combined with rising health awareness, is positioning diagnostic labs as the fastest-growing end-users in the hematology ecosystem.

REGIONAL ANALYSIS

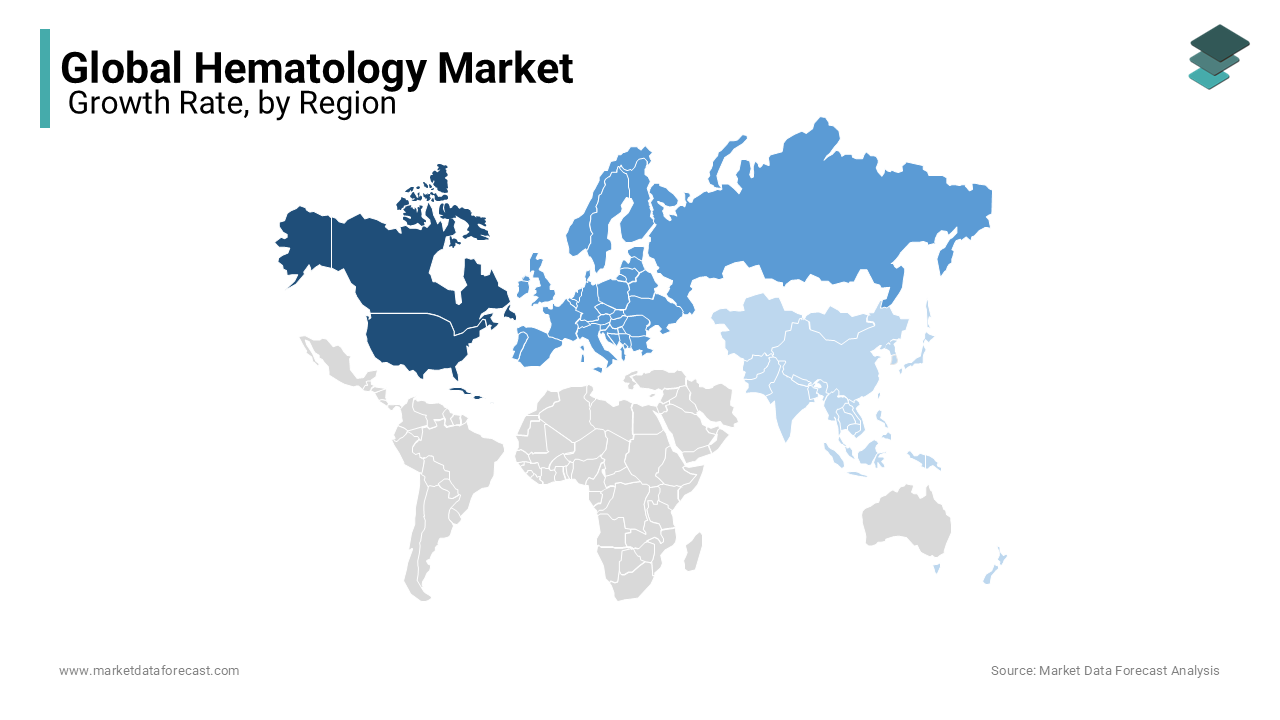

North America Hematology Market Analysis

North America led the global hematology market with a 40.5% share in 2025. The region’s dominance is rooted in its advanced healthcare infrastructure, high diagnostic adoption rates, and robust R&D ecosystem. The U.S. alone accounts for a notable share of the regional market, driven by widespread use of automated hematology systems. The presence of leading manufacturers like Abbott, Beckman Coulter, and Sysmex ensures a steady supply of cutting-edge analyzers. Additionally, the U.S. Food and Drug Administration’s fast-track approvals for AI-integrated hematology devices, such as the CellaVision DM96, have accelerated innovation. Medicare covers over 80% of CBC tests for seniors, ensuring accessibility. With over 6,000 hospitals equipped with advanced hematology labs, North America remains the benchmark for diagnostic excellence and market maturity.

Europe Hematology Market Analysis

Europe holds a major market share which is driven by strong public healthcare systems and harmonized regulatory standards, according to Statista. Countries like Germany, France, and the UK lead in diagnostic adoption. The European Union’s In Vitro Diagnostic Regulation (IVDR) has raised the bar for device quality, boosting demand for certified hematology analyzers. Germany’s statutory health insurance funds perform lab tests annually, with hematology as the largest category. Additionally, the Horizon Europe program has allocated notable funds to hematology innovation (2021–2027), fostering collaboration across 27 nations. Thus, the region maintains high diagnostic coverage and technological parity.

Asia-Pacific Hematology Market Analysis

The Asia-Pacific region is rapidly ascending. This growth is fueled by rising healthcare spending and expanding diagnostic access. China and India are the primary drivers. China’s National Health Commission reports that millions of CBC tests were conducted in 2022, with the government investing in lab modernization under its 14th Five-Year Plan. India’s diagnostics market is expanding due to insurance penetration and urbanization. Japan, despite a shrinking population, maintains high adoption of advanced analyzers—Sysmex, headquartered in Kobe. With only one hematology analyzer per 50,000 people in rural India, the unmet need is vast, positioning APAC as the future epicenter of market expansion.

Latin America Hematology Market Analysis

Latin American market growth is accelerating, particularly in Brazil and Mexico. Brazil’s Unified Health System (SUS) conducts a substantial volume of hematology tests annually. The country has a large number of private labs, many adopting semi-automated analyzers. Mexico’s healthcare reform has expanded insurance coverage to the population, increasing access to diagnostics. However, challenges remain—only a limited share of rural clinics in Bolivia and Guatemala have functional hematology equipment. Hence, the region is poised for transformation.

Middle East and Africa Hematology Market Analysis

The Middle East and Africa collectively are emerging, particularly in the Gulf and South Africa. The UAE and Saudi Arabia are investing heavily in healthcare. Saudi Vision 2030 includes significant investment for healthcare modernization, with diagnostic labs as a priority. The UAE’s Dubai Health Authority emphasizes CBC for all expatriate visa applicants. However, in sub-Saharan Africa, only a limited people have access to basic diagnostic services, creating a massive unmet need. Initiatives like Africa CDC’s Partnership for African Vaccine Manufacturing include diagnostic infrastructure, signaling a shift. Thus, the region is beginning to close the gap.

COMPETITIVE LANDSCAPE

The hematology market is characterized by intense competition among established global players and emerging regional manufacturers. Innovation in automation, artificial intelligence, and miniaturization defines the competitive landscape, with companies striving to offer faster, more accurate, and integrated diagnostic solutions. Multinational corporations like Sysmex, Abbott, and Beckman Coulter dominate through advanced R&D, extensive distribution networks, and strong brand recognition. However, regional players in India, China, and South Korea are gaining traction by offering cost-effective alternatives tailored to local needs. Competitive differentiation arises from service quality, regulatory compliance, and digital integration capabilities. The race to develop AI-powered analyzers and cloud-connected platforms is accelerating, with firms investing in software ecosystems to enhance lab efficiency. Strategic collaborations with academic institutions and healthcare providers are common to validate new technologies. Mergers and acquisitions are reshaping the market, enabling rapid scaling and technology absorption. Price pressure in low-income regions challenges profitability, prompting tiered pricing and public-private partnerships. Overall, competition is not only about product superiority but also adaptability to diverse healthcare infrastructures, regulatory environments, and patient access models, making the hematology market dynamic and innovation-driven.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the europe space tourism market include

- Siemens AG Healthcare

- Johnson & Johnson

- Beckman Coulter, Inc.

- Abbott Laboratories

- Thermo Fisher Scientific

- Roche

- HORIBA Ltd.

- Sysmex Corporation

- Bio-Rad Laboratories Inc.

- Boule Diagnostics AB

- Mindray Medical International Limited.

Top Players in the Hematology Market

Sysmex Corporation

Headquartered in Japan, Sysmex is a dominant force in the Asia Pacific hematology market, renowned for its automated hematology analyzers and diagnostic solutions. The company maintains a strong footprint across hospitals, laboratories, and research centers in China, India, and Southeast Asia. Sysmex has intensified its focus on AI-integrated platforms, launching the XN-30 series for body fluid analysis in 2023. It expanded its manufacturing capacity in Singapore to meet regional demand and partnered with India’s National Institute of Pathology to support diagnostic standardization. Through continuous R&D investment and localized service networks, Sysmex enhances accessibility and reliability, reinforcing its leadership in high-volume blood testing across the region.

Abbott Laboratories

Abbott plays a pivotal role in advancing point-of-care hematology diagnostics in Asia Pacific, particularly in rural and underserved areas. The company’s hematological offerings include the CELL-DYN series of analyzers and the Pima Hemoglobinometer, widely deployed in India and Indonesia. In 2023, Abbott launched a mobile diagnostic van initiative in partnership with NGOs in the Philippines and Bangladesh to expand anemia screening. It also strengthened its supply chain in Vietnam and Thailand to ensure product availability. By focusing on affordability, portability, and ease of use, Abbott is bridging diagnostic gaps and supporting public health programs, especially in maternal and child health, solidifying its relevance across diverse healthcare settings.

Beckman Coulter (Danaher Corporation)

Beckman Coulter is a key innovator in high-throughput hematology systems across Asia Pacific, serving major hospitals and reference laboratories in South Korea, Australia, and India. The company introduced the DxH 520 hematology analyzer in 2023, designed for mid-sized labs seeking automation and precision. It expanded its collaboration with Australia’s Royal College of Pathologists to support training and standardization. In China, Beckman Coulter opened a new technical support center in Shanghai to accelerate service delivery. By integrating digital workflows and remote diagnostics into its platforms, the company enhances lab efficiency. Its focus on scalable solutions and regulatory compliance positions it as a preferred partner for modernizing clinical laboratories across the region.

Top Strategies Used by Key Market Participants

Key players in the hematology market employ strategies centered on technological innovation, geographic expansion, and strategic partnerships. Companies are investing heavily in AI-driven diagnostics and automation to improve accuracy and throughput. Product diversification, especially in point-of-care and portable devices, targets underserved regions. Mergers and acquisitions are common, enabling access to new technologies and customer bases. Firms are also enhancing service networks and technical support to ensure reliability. Collaborations with governments and NGOs expand reach in public health programs. Regulatory compliance, particularly with IVDR and CE standards, is prioritized for global access. Digital integration with laboratory information systems is another focus, improving workflow efficiency. Training programs for lab technicians strengthen customer relationships. Additionally, companies are tailoring pricing models for emerging markets, balancing affordability with profitability, ensuring sustainable growth in diverse healthcare ecosystems.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Sysmex Corporation launched the XN-30 series hematology analyzer in India, designed for high-precision body fluid analysis, enhancing diagnostic capabilities in oncology and infectious diseases.

- In May 2023, Abbott Laboratories partnered with the Bangladesh Ministry of Health to deploy 500 Pima Hemoglobinometers across rural clinics, expanding anemia screening access for pregnant women and children.

- In September 2023, Beckman Coulter opened a new technical support and training center in Shanghai, China, to accelerate service delivery and strengthen relationships with hospitals and laboratories.

- In February 2024, Danaher Corporation completed the acquisition of Cepheid’s molecular diagnostics division, integrating its technologies with Beckman Coulter’s hematology platforms for comprehensive infectious disease testing.

- In April 2024, Abbott launched a mobile diagnostic van program in the Philippines, equipped with CELL-DYN analyzers, to provide on-site hematology testing in remote and disaster-prone areas.

MARKET SEGMENTATION

The research report on the global hematology market has been segmented and sub-segmented based on the product, application, end-user, and region.

By Product

- Hematology Analyzers

- Hematology Reagents

- Flow Cytometers

- Hematology Cell Counters

- Slide Stainers

- Coagulation Analyzers

- Hematology Testing

- Centrifuges

- Hemoglobinometers

- Others

By Application

- Infectious Diseases

- Cancer

- Cardiovascular Disorders

- Blood Screening

- Diabetes

- HIV

- Auto-Immune Diseases

By End-User

- Hospitals

- Clinics

- Diagnostic Laboratories

- Research and Development Centers

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa