- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Global Flow Cytometry Market Size

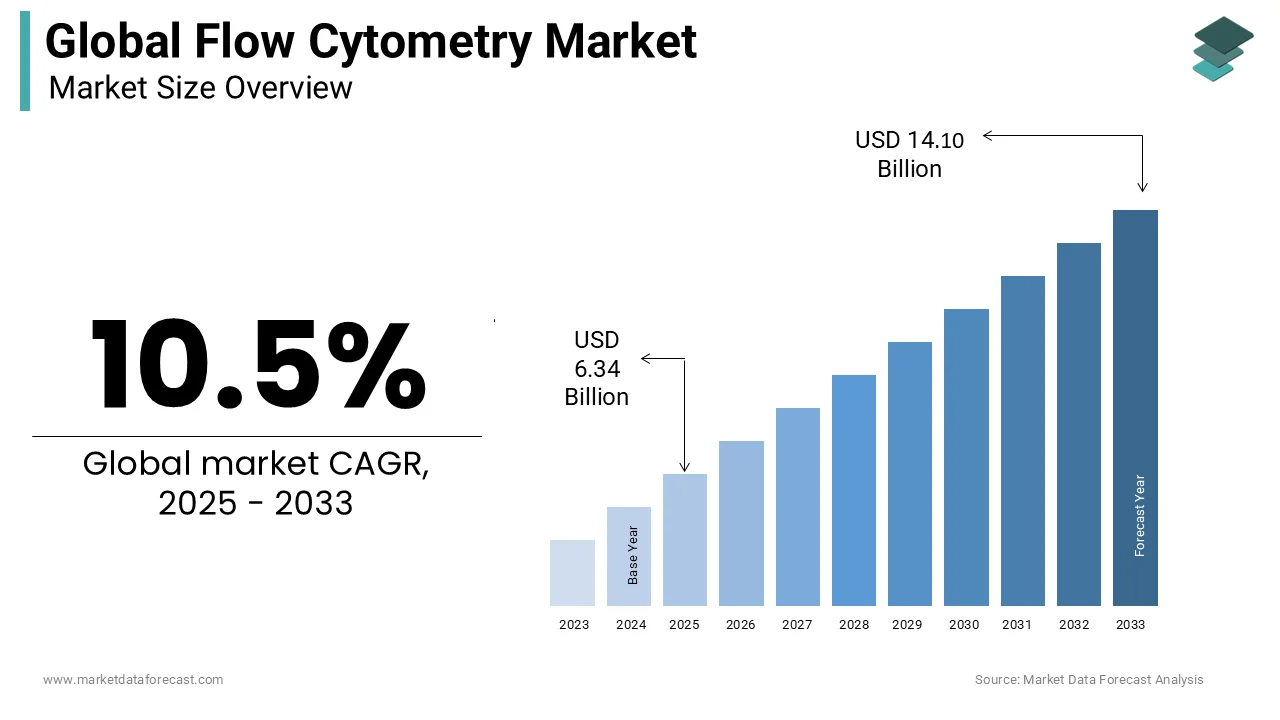

The size of the global low cytometry market was worth USD 5.75 billion in 2024. The global market is anticipated to grow at a CAGR of 10.5% from 2025 to 2033 and be worth USD 14.10 billion by 2033 from USD 6.34 billion in 2025.

Flow cytometry is a laser-based biophysical technology employed to analyze the physicochemical characteristics of cells or particles in a fluid as they pass through a light source, enabling high-throughput, multiparametric analysis at the single-cell level. This technique is extensively utilized in immunology, oncology, and stem cell research due to its precision in cell population identification and functional assessment. The growing integration of flow cytometry in clinical diagnostics and personalized medicine has elevated its relevance in modern biomedical research.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases and Cancer

The escalating global burden of cancer and chronic inflammatory diseases has significantly amplified the demand for advanced diagnostic tools, with flow cytometry emerging as a cornerstone in disease characterization and monitoring. Flow cytometry enables rapid detection of aberrant cell populations in hematological malignancies such as leukemia and lymphoma, where it is considered the gold standard. Furthermore, the increasing adoption of minimal residual disease (MRD) testing has solidified its role in post-treatment surveillance, directly fueling instrument and reagent demand across academic and clinical laboratories.

Expansion of Immunotherapy and Precision Medicine

The rapid evolution of immunotherapies, including CAR-T cell treatments and immune checkpoint inhibitors, has created an indispensable need for high-resolution immune cell profiling, a capability uniquely offered by flow cytometry. The therapy manufacturing process demands rigorous characterization of T-cell subsets, activation markers, and exhaustion phenotypes, parameters optimally assessed via multicolor flow panels. Moreover, institutions like the Parker Institute for Cancer Immunotherapy utilize flow cytometry in 90% of their translational immunology studies, highlighting its embedded role in advancing personalized therapeutic strategies and driving instrumentation adoption in biopharma R&D.

MARKET RESTRAINTS

High Instrumentation and Operational Costs

Despite its analytical superiority, the widespread adoption of flow cytometry is impeded by substantial capital and maintenance expenditures associated with high-end instruments. A single advanced flow cytometer capable of 20+ parameter analysis can cost between $300,000 and $500,000, placing it beyond the financial reach of many regional hospitals and developing research institutions. Additionally, operational costs, including trained personnel, specialized reagents, and calibration standards, further strain institutional budgets.

Technical Complexity and Skilled Personnel Shortage

Flow cytometry requires sophisticated expertise in experimental design, panel optimization, data acquisition, and multidimensional analysis, creating a bottleneck in its effective deployment. The complexity of multicolor panel design, where spectral overlap and compensation errors can compromise data integrity, demands continuous training and quality assurance. Moreover, the absence of standardized protocols across institutions leads to inter-laboratory variability, undermining reproducibility. These challenges are exacerbated in emerging economies, where formal training programs in cytometry remain scarce, as per the African Society for Laboratory Medicine, thereby constraining the technology’s full utilization.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence in Data Analysis

The convergence of artificial intelligence (AI) with flow cytometry data interpretation presents a transformative opportunity to overcome analytical bottlenecks and enhance diagnostic accuracy. Traditional manual gating is time-consuming and subjective, whereas AI-driven platforms can automate cell population identification with reproducibility and speed. Companies like Beckman Coulter and Sony Biotechnology have already introduced AI-integrated software suites for automated clustering and anomaly detection. This technological synergy not only improves throughput but also democratizes access for labs with limited cytometry expertise, unlocking scalable applications in clinical diagnostics and population-level studies.

Point-of-Care and Compact Flow Cytometry Devices

The development of portable, miniaturized flow cytometers is poised to revolutionize decentralized testing in resource-limited and clinical settings. Unlike traditional benchtop systems, these compact devices offer rapid, on-site analysis for applications such as CD4+ T-cell counting in HIV management or sepsis biomarker detection. As per the World Health Organization, over 37 million people globally live with HIV, and in sub-Saharan Africa, timely CD4 monitoring remains a challenge due to centralized lab dependence. This shift toward decentralization not only enhances patient outcomes but also expands market penetration into primary care and mobile health units.

MARKET CHALLENGES

Standardization and Interoperability Across Platforms

A persistent challenge in the flow cytometry landscape is the lack of universal standardization in instrument calibration, reagent labeling, and data formats, leading to inconsistent results across laboratories and hindering multi-center studies. As per the Flow Cytometry Standards (FCS) file format consortium, over 30 different instrument manufacturers use proprietary software that often fails to seamlessly exchange data, complicating collaborative research. Moreover, fluorescence compensation and voltage settings are frequently user-dependent, introducing subjectivity. Achieving harmonization remains a critical hurdle for regulatory acceptance and clinical scalability.

Regulatory and Reimbursement Hurdles in Clinical Adoption

While flow cytometry is well-established in research, its transition into routine clinical diagnostics is constrained by evolving regulatory frameworks and inconsistent reimbursement policies. In the United States, the Centers for Medicare & Medicaid Services reimburse only a limited number of flow cytometry-based assays, with many advanced immunophenotyping panels classified as non-covered or investigational. Additionally, the U.S. Food and Drug Administration’s stringent requirements for assay validation and instrument clearance delay the commercialization of novel panels. These regulatory complexities impede innovation and market expansion, particularly for small and mid-sized developers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 10.5% |

| Segments Covered | By Technology, Product, Application, End-User, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key Market Players | Becton, Dickinson, and Company., Beckman Coulter, Inc., Thermo Fisher Scientific, Inc., Merck KGaA, Sysmex Partec GmbH, Luminex Corporation, Miltenyi Biotec GmbH, Bio-Rad Laboratories, Inc.. |

SEGMENTAL ANALYSIS

By Technology Insights

The bead-based technology segment had the largest share of the global market in 2024, and its domination is expected to continue during the forecast period. The segment's growth is driven by the advantages of bead-based flow cytometry technology, such as higher throughput, better sensitivity, and the ability to analyze multiple parameters simultaneously. The bead-based technology performs qualitative and quantitative analyses, and due to this, it is widely adopted by researchers. The growing number of applications of bead-based flow cytometry technology, such as cell sorting, cell counting, and protein analysis, is further propelling segmental growth. In addition, the rising adoption of advanced bead-based flow cytometry technologies, such as magnetic bead-based cell sorting and multiplexed bead assays, contributes to the segment’s growth.

The cell-based segment accounted for a substantial share of the worldwide market in 2024 and is expected to grow considerably during the forecast period, owing to the increasing usage of cell-based flow cytometry technologies in research and diagnostic applications such as immunophenotyping and cell cycle analysis.

The bead-based flow cytometry segment is experiencing the fastest growth and is projected to expand at a CAGR of 11.3% from 2025 to 2033. This acceleration is largely attributed to its utility in high-throughput multiplexed cytokine and biomarker profiling, particularly in vaccine development and autoimmune disease research. Bead-based assays enable simultaneous quantification of up to 50 analytes from a single sample, drastically improving efficiency compared to ELISA. Furthermore, its compatibility with limited sample volumes makes it ideal for pediatric and longitudinal studies.

By Product Insights

The reagents and consumables segment constituted the largest product by accounting for 62.6% of the global flow cytometry market revenue in 2024, according to Evaluate Pharma’s Life Science Diagnostics Report. This dominance is sustained by the recurring nature of reagent purchases, which are consumed in every assay cycle, unlike capital-intensive instruments that are procured infrequently. Monoclonal antibodies conjugated to fluorochromes represent the highest-selling reagent category. The expansion of multicolor panels, now routinely employing 15–30 markers, has exponentially increased per-assay reagent consumption. Additionally, the growing emphasis on standardized antibody panels, such as those recommended by the Human Immunology Project Consortium, has institutionalized reagent procurement across research networks.

The flow cytometry instruments segment is the fastest-growing product and is anticipated to grow at a CAGR of 9.8% through 2033. This surge is propelled by technological advancements such as spectral cytometry and imaging flow cytometers, which offer enhanced resolution and data depth, attracting investment from both academic and clinical sectors. The launch of high-parameter systems like the Cytek Aurora and BD FACSymphony A5 has driven replacement cycles in well-funded research institutions. Moreover, the integration of automation and AI-assisted acquisition software has reduced operational complexity, broadening instrument adoption beyond specialized labs.

By Application Insights

The research application segment led the flow cytometry market by representing 65.2% of total revenue in 2024. This position is underpinned by the indispensable role of flow cytometry in basic and translational life sciences, particularly in immunology, stem cell biology, and drug discovery. The Human Cell Atlas initiative, involving over 1,200 scientists across 75 countries, relies on flow cytometry for single-cell phenotyping, generating massive demand for high-dimensional analysis tools. Besides, the rise of systems immunology has necessitated large-scale immune monitoring. The technology’s ability to dissect heterogeneous cell populations with high precision makes it a cornerstone in functional genomics and CRISPR screening workflows.

The clinical application segment is expanding at the fastest pace, with a projected CAGR of 12.1% from 2025 to 2033. This rapid growth is fueled by the increasing incorporation of flow cytometry into routine diagnostic pathways, particularly in oncology and infectious disease management. The WHO recommends flow cytometry for minimal residual disease (MRD) detection in acute lymphoblastic leukemia. Additionally, the advent of companion diagnostics for immunotherapies has created new clinical use cases. These expanding clinical validations are accelerating regulatory approvals and insurance reimbursements, driving institutional adoption.

By End-users Insights

The research institutes segment represented the prominent end-user by contributing 42.6% of the global flow cytometry market revenue in 2024. This growth is due to the concentration of high-complexity research programs in immunology, oncology, and regenerative medicine that depend on advanced cytometry platforms. Major research hubs such as the Broad Institute and the Max Planck Institutes operate centralized flow cytometry cores that serve hundreds of labs, generating sustained demand for instruments and reagents. Moreover, large-scale collaborative projects like the Human Tumor Atlas Network mandate flow cytometry for spatial and phenotypic mapping, further entrenching its role.

The clinical testing laboratories segment is emerging as the fastest-growing end-user and is projected to grow at a CAGR of 13.4% through 2033. This acceleration is driven by the formal integration of flow cytometry into standardized diagnostic algorithms for hematologic malignancies and immunodeficiency disorders. The College of American Pathologists mandates flow cytometry for all suspected leukemia cases, leading to widespread adoption in hospital-based labs. Furthermore, the expansion of reference laboratories such as LabCorp and Quest Diagnostics, both of which have invested in high-throughput cytometry automation, has enhanced testing scalability. These systemic shifts are transforming clinical labs into high-volume, technology-driven hubs, fueling instrument procurement and service contracts.

REGIONAL ANALYSIS

North America Flow Cytometry Market Insights

North America led the global flow cytometry market with a 41.8% share in 2024. The region’s supremacy is anchored in its robust biomedical research infrastructure and high healthcare expenditure, particularly in the United States. The National Institutes of Health allocated $48.3 billion to biomedical research in fiscal year 2023, a significant portion of which funded flow cytometry-based immunology and oncology projects. Leading academic institutions such as Harvard Medical School and MD Anderson Cancer Center operate advanced cytometry cores equipped with spectral and imaging systems. Additionally, the U.S. Food and Drug Administration’s accelerated approval pathway for cell and gene therapies has intensified demand for flow-based quality control.

Europe Flow Cytometry Market Insights

Europe holds a significant market share and reflects its strong legacy in immunological research and centralized healthcare systems. Countries like Germany, the UK, and France have integrated flow cytometry into national diagnostic guidelines for hematologic cancers, ensuring standardized clinical deployment. The European Hematology Association’s 2022 guidelines recommend flow cytometry for MRD assessment in multiple blood cancers, driving adoption across public hospitals. The presence of key instrument manufacturers such as BD Biosciences (UK) and Sysmex (Germany) further strengthens the regional ecosystem.

Asia Pacific Flow Cytometry Market Insights

Asia Pacific is witnessing the most dynamic expansion, driven by rising research funding and healthcare modernization in countries like China, Japan, and South Korea. The region’s growing biopharma sector, particularly in CAR-T development, is further accelerating demand.

Latin America Flow Cytometry Market Insights

Latin America is reflecting a gradual but uneven adoption across the region. Brazil and Mexico are the primary contributors, with government-backed initiatives improving access to advanced diagnostics. Brazil’s Unified Health System has incorporated flow cytometry into its national leukemia diagnosis protocol, resulting in an increase in test volume between 2020 and 2023. However, disparities persist; only a few public hospitals in Andean countries have access to functional cytometers. Nonetheless, partnerships with international organizations such as the IAEA’s Technical Cooperation Program have facilitated equipment donations and training, laying the foundation for future growth. The expansion of private diagnostic chains like Grupo Fleury in Brazil is also driving commercial adoption, particularly in oncology testing.

Middle East and Africa Flow Cytometry Market Insights

The Middle East and Africa collectively represent a small share of the global market, with limited but strategic development concentrated in South Africa, Saudi Arabia, and the UAE. South Africa remains the regional leader in flow cytometry utilization, supported by the South African Medical Research Council’s investment in HIV and TB research programs. In the Gulf, Saudi Arabia’s Vision 2030 health transformation plan includes the establishment of advanced diagnostics hubs, with King Abdullah International Medical Research Center acquiring high-end cytometers for cancer research. The UAE’s Dubai Health Authority has integrated flow cytometry into its genetic screening program for thalassemia.

KEY MARKET PLAYERS

Noteworthy companies operating in the global flow cytometry market profiled in this report are Becton, Dickinson, and Company., Beckman Coulter, Inc., Thermo Fisher Scientific, Inc., Merck KGaA, Sysmex Partec GmbH, Luminex Corporation, Miltenyi Biotec GmbH, Bio-Rad Laboratories, Inc., Sony Biotechnology, Life Technologies Corporation Inc., EMD Millipore Corporation, Miltenyi Biotec, Agilent Technologies, Inc., and Affymetrixx Inc.

TOP LEADING PLAYERS IN THE MARKET

BD (Becton, Dickinson and Company)

BD maintains a dominant presence in the Asia Pacific flow cytometry landscape through deep integration with clinical and research ecosystems. The company has expanded its footprint by launching region-specific training programs in countries like India and Indonesia, enhancing user proficiency in multicolor panel design. The facility supports biopharma collaborations, particularly in immuno-oncology and vaccine development. BD has also partnered with leading hospitals in Japan and South Korea to standardize minimal residual disease testing protocols using its reagents and instruments. Through continuous investment in localized technical support and regulatory compliance, BD has strengthened its reputation as a trusted partner in both academic and clinical laboratories across the region.

Thermo Fisher Scientific

Thermo Fisher Scientific has significantly advanced its position in the Asia Pacific flow cytometry market by leveraging its end-to-end portfolio, spanning instruments, reagents, and software. The company launched Attune NxT Advanced Flow Cytometers tailored for high-throughput research in emerging markets, including Vietnam and Thailand. The company also collaborated with Australia’s Walter and Eliza Hall Institute to co-develop optimized antibody panels for immunology research. Additionally, Thermo Fisher has expanded its e-commerce platform in India and Indonesia, improving accessibility for smaller laboratories. Its acquisition of high-parameter reagent technologies has further solidified its role in supporting complex research applications, making it a preferred provider for both academic and industrial users in the region.

Sony Biotechnology

Sony Biotechnology has carved a niche in the Asia Pacific market by focusing on spectral and imaging flow cytometry innovation. The company’s ID7000 Spectral Cell Analyzer has gained traction in advanced research institutions across Japan and South Korea due to its superior resolution in highly multiplexed experiments. The company also introduced localized service teams in India and Australia to reduce instrument downtime and improve customer retention. Sony’s commitment to open-platform software integration allows seamless data sharing, appealing to collaborative research networks. By actively participating in regional scientific conferences and sponsoring cytometry workshops, Sony has built strong academic relationships, positioning itself as a technology leader in high-dimensional flow cytometry across the Asia Pacific region.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the flow cytometry market employ a combination of product innovation, strategic partnerships, geographic expansion, and digital integration to consolidate their positions. Companies are increasingly investing in high-parameter and spectral flow cytometry platforms to meet the demands of complex research and clinical applications. Strategic collaborations with academic institutions and hospitals enable co-development of standardized assays and clinical protocols. Geographic expansion, particularly in the Asia Pacific and Latin America, is achieved through localized manufacturing, training centers, and regulatory alignment. Additionally, firms are integrating artificial intelligence into data analysis software to enhance accuracy and usability. Acquisition of niche technology developers allows rapid entry into emerging subsegments such as imaging flow cytometry and point-of-care devices. These multifaceted strategies ensure sustained competitiveness and responsiveness to evolving scientific and clinical needs.

COMPETITION OVERVIEW

The flow cytometry market is characterized by intense competition driven by technological differentiation, application-specific innovation, and global reach. Major players compete not only on instrument performance but also on reagent portfolios, software capabilities, and after-sales support. The shift toward high-parameter and spectral systems has intensified R&D investments, with companies striving to offer superior resolution and ease of use. Competitive dynamics are further shaped by the growing demand for standardized workflows in clinical diagnostics and cell therapy manufacturing. Emerging players are challenging incumbents with cost-effective, compact systems tailored for resource-limited settings. At the same time, established firms leverage their global distribution networks and regulatory expertise to maintain dominance. Collaboration with research consortia and participation in large-scale health initiatives enhance brand credibility and market penetration, making the competitive landscape both dynamic and highly specialized.

RECENT MARKET DEVELOPMENTS

- In April 2024, BD launched its next-generation FACSymphony S6 flow cytometer in Japan, featuring 50-parameter detection and integrated AI-powered analysis software, enhancing its leadership in high-dimensional research and clinical immunophenotyping in the Asia Pacific region.

- In January 2023, Thermo Fisher Scientific inaugurated a new flow cytometry reagent manufacturing facility in Shanghai, enabling localized production to meet rising demand in China and reduce supply chain dependencies for research and diagnostic customers.

- In September 2023, Sony Biotechnology partnered with the Indian Institute of Science to establish a spectral flow cytometry center of excellence in Bangalore, supporting advanced immunology and cancer research with cutting-edge instrumentation and training.

- In June 2024, Beckman Coulter introduced the CytoFLEX LX Advanced Flow Cytometer in Australia, designed for high-throughput clinical labs, featuring automated calibration and enhanced sensitivity for minimal residual disease detection.

- In February 2023, Agilent Technologies acquired Luxcel Biosciences, a Cork-based developer of metabolic flux assays, integrating its technologies into flow cytometry workflows to expand functional cell analysis capabilities for pharmaceutical and academic clients globally.

MARKET SEGMENTATION

This market research report on the global flow cytometry market has been segmented and sub-segmented based on technology, product, application, end-user, and region.

By Technology

- Cell-based

- Bead-based

By Product

- Reagents & Consumables

- Flow Cytometry Instruments

By Application

- Research

- Clinical

- Industrial

By End-users

- Commercial Organizations

- Research Institutes

- Clinical Testing Labs

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa