Europe Neurological Monitoring Devices Market Research Report By Type, Procedure, Therapeutic Application, Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe) - Size, Share, Trends and Growth Forecast (2026 to 2034)

Market Size, 2025

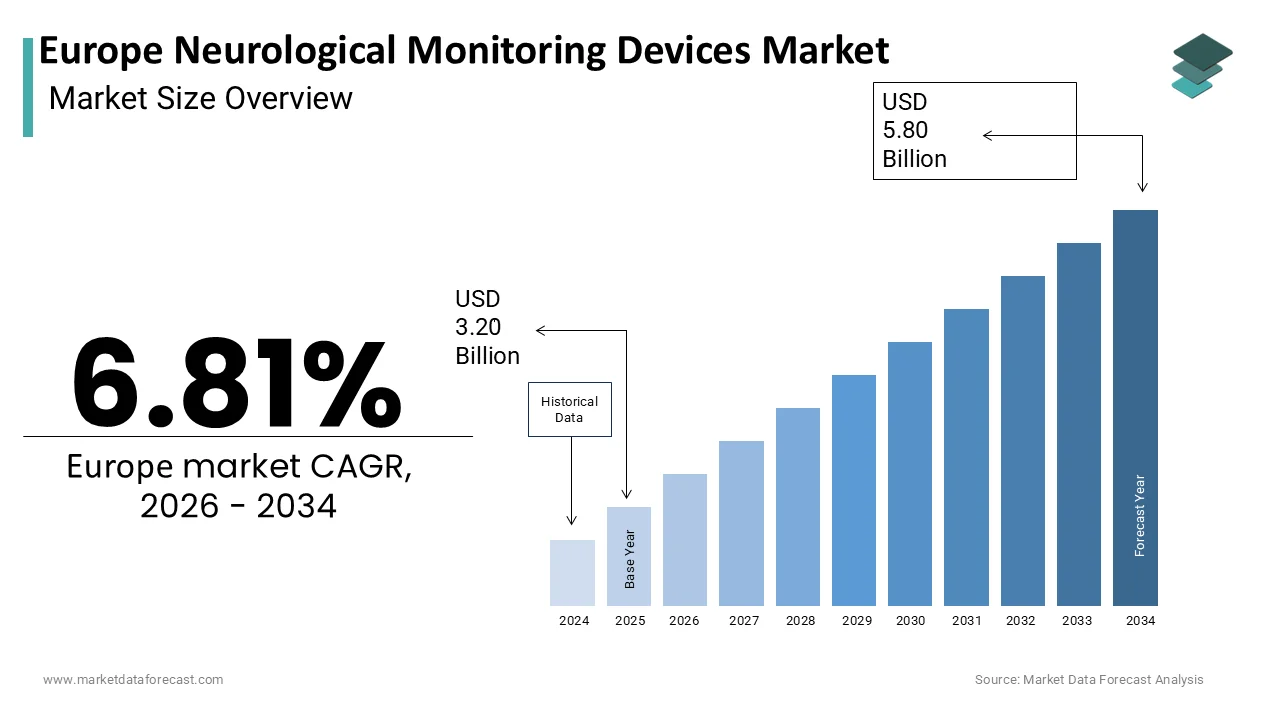

$3.2 BnMarket Estimate, 2026

$3.42 BnMarket Forecast, 2034

$5.8 BnCAGR, 2026–2034

6.81%Europe Neurological Monitoring Devices Market Summary

Europe neurological monitoring devices market was valued at USD 3.0B in 2024, estimated at USD 3.20B in 2025, and forecast to reach USD 5.43B by 2033 (CAGR 6.81%, 2025–2033), powered by rising neurodegenerative disease burden, ERAS-driven intraoperative monitoring, and rapid adoption of AI-enabled predictive neurology.

Market snapshot

- 2024 value: USD 3.00 billion

- 2025 (est): USD 3.20 billion

- 2033 forecast: USD 5.43 billion

- CAGR (2025–2033): 6.81%

Quick growth drivers

- Rising prevalence of dementia, epilepsy, stroke, and post-cardiac arrest encephalopathy.

- Hospitals integrating multimodal monitoring into neurocritical care & ERAS protocols.

- Higher adoption of continuous EEG for detecting non-convulsive seizure activity.

- Technological miniaturization enabling portable, wearable, & home-based neuromonitoring.

- Expansion of guideline-driven monitoring (ESO, ERAS, national neurovascular programs).

Principal restraints

- Fragmented and stringent EU MDR + UK MHRA regulatory pathways → long certification cycles.

- Shortage of neurologists, neurophysiology technicians & neurointensivists limits device utilization.

- Capital expenditure pressure in public hospitals → delayed procurement.

- Interoperability challenges between disparate EHR + ICU monitoring platforms.

High-value opportunities

- AI-driven analytics for seizure prediction, DCI alerts, and real-time EEG interpretation.

- Remote & home-based neurological monitoring for epilepsy, neurodegenerative disorders, and chronic care.

- Integrated cloud platforms enabling centralized review of EEG/NIRS/ICP across regions.

- Wearable near-infrared spectroscopy & portable EEG for tele-neuromonitoring expansion.

Key operational challenges

- Need for harmonized data standards for neurophysiology signals across Europe.

- Limited availability of trained clinicians to interpret high-volume waveform data.

- Legacy ICU systems delaying full multimodal integration (EEG + ICP + NIRS + vitals).

- Budget constraints in Southern & Eastern Europe slowing modernization cycles.

Fastest-growing segments

- Near-infrared spectroscopy (NIRS): ~11.3% CAGR — expanding in NICUs, cardiac ORs, stroke transport.

- Epilepsy monitoring: ~10.8% CAGR — fueled by ambulatory EEG + school-based screening pilots.

- Ambulatory / outpatient monitoring: ~9.6% CAGR — supported by telehealth uptake.

Regional leadership & dynamics

- Germany (19.3%) — strongest neurocritical infrastructure; high ICU EEG penetration.

- France (15.7%) — centralized stroke & epilepsy pathways drive uniform device adoption.

- UK — NICE-backed continuous EEG and structured reimbursement → rapid scaling.

- Italy — aging population + rising stroke admissions → demand for multimodal surveillance.

- Spain — tele-neuro monitoring networks in rural regions; EU-funded NIRS innovations.

What wins commercially

MDR-ready platforms with robust clinical validation + postmarket surveillance.

- Seamless integration into hospital EHR/ICU ecosystems (HL7, FHIR, vendor-neutral APIs).

- AI-enhanced dashboards delivering predictive alerts rather than raw signal streams.

- Cloud-connected portable devices enabling hospital-to-home continuity.

- Strong clinical training ecosystems to overcome personnel shortages.

Top strategic

Accelerate development of AI-enabled multimodal monitoring, strengthen regulatory pipelines, expand clinician training networks, and build tele-neuromonitoring ecosystems that integrate hospital, outpatient, and home settings — securing long-term leadership in Europe’s shift toward predictive neurological care.

Leading players

Nihon Kohden · Natus Medical · Philips Healthcare · GE Healthcare · Compumedics · Siemens Healthineers · Medtronic · Integra LifeSciences · Masimo · Electrical Geodesics · Advanced Brain Monitoring · CAS Medical Systems

Europe Neurological Monitoring Devices Market Size

The Europe Neurological Monitoring Devices Market is projected to grow from USD 3.20 billion in 2025 to USD 3.42 billion in 2026 and reach USD 5.80 billion by 2034, registering a CAGR of 6.81% during the forecast period from 2026 to 2034.

Neurological monitoring devices are advanced diagnostic and therapeutic technologies designed to assess and track the electrical and physiological activity of the nervous system, particularly in critical care and perioperative settings. These systems include electroencephalography machines, intracranial pressure monitors, cerebral oximeters, and neuromuscular transmission monitors. The clinical imperative for real-time neurological assessment has intensified as Europe faces a mounting burden of neurological disorders and an aging demographic structure. According to Eurostat, individuals aged sixty-five and above constituted over twenty o the European Union population in two thousand and twenty-three, a segment particularly vulnerable to stroke, dementia, and traumatic brain injuries. Concurrently, the European Brain Council and the European Commission emphasize that a significant portion of the European population lives with a brain disorder, underlining the societal urgency for precise and continuous neurological surveillance. The number of people affected by these conditions is substantial and a major public health challenge. As per the Organisation for Economic Co-operation and Development (OECD), these nations have generally seen improvements in health outcomes related to circulatory diseases, which often translates to a reduction in related mortality rates, rather than a steady increase in hospital admissions for cerebrovascular events. This evolving clinical landscape positions neurological monitoring devices as indispensable tools in safeguarding neurological integrity and guiding therapeutic decisions.

MARKET DRIVERS

Expanding Prevalence of Neurodegenerative and Cerebrovascular Conditions Elevates Clinical Dependency on Continuous Monitoring Solutions

The escalating incidence of neurodegenerative and cerebrovascular diseases across the region has significantly intensified the need for continuous and accurate neurological monitoring, which in turn drives the growth of the Therope neurological monitoring devices market. He prevalence of Alzheimer's disease and other dementias is substantial in the European region, and the number of affected individuals is rising due to demographic changes, placing an increasing burden on healthcare systems. Besides, stroke remains a leading cause of disability and mortality. Stroke represents a significant health challenge, with a considerable number of new cases occurring annually within the European Union. These conditions often necessitate prolonged hospitalization in intensive care units where real-time tracking of cerebral perfusion, oxygenation, and electrical activity becomes critical for preventing secondary neurological deterioration. There has been a noted increase in the use of continuous electroencephalography monitoring in neurocritical care unitpost-cardiacmany in recent years due to rising post-cardiac arrest encephalopathy cases. Moreover, Admissions for acute ischemic stroke that require multimodal neuromonitoring have shown an upward trend in France. Such clinical demands are compelling hospitals to integrate sophisticated monitoring platforms capable of detecting subtle neurological changes before irreversible damage occurs. This trend is further accelerated by updated European Stroke Organisation guidelines that now recommend routine neuromonitoring in high-risk stroke patients, directly stimulating device adoption across tertiary care facilities.

Heightened Integration of Neurological Monitoring in Enhanced Recovery After Surgery Protocols Drives Intraoperative and Postoperative Adoption

The widespread institutionalization of Enhanced Recovery After Surgery protocols across European hospitals has catalyzed the integration of these advanced technologies into perioperative care pathways, which fuels the expansion of the European evidence-based monitoring devices market. These evidence-based frameworks aim to minimize postoperative complications and accelerate patient discharge, with neurological integrity emerging as a pivotal metric in high-risk procedures such as cardiac and major spine surgeries. Many university-affiliated hospitals in several European countries have adopted neuromonitoring as part of their standard intraoperative protocols for certain types of surgery. The use of processed electroencephalography is advised in specific consensus recommendations intended to prevent complications during surgery for elderly patients. Hospitals employing cerebral oximetry during major thoracic procedures have observed improvements in postoperative cognitive outcomes compared to those using only traditional clinical assessment methods. This compelling clinical outcome has prompted national health technology assessment bodies in Belgium and Austria to reimburse neuromonitoring as a bundled service within enhanced recovery packages, which thereby embeds these devices into routine surgical workflows and expands their clinical footprint beyond traditional neurology departments.

MARKET RESTRAINTS

Stringent and Fragmented Medical Device Regulatory Frameworks Across European Jurisdictions Impede Timely Market Access

A complex and nonuniform regulatory ecosystem significantly delays product commercialization and scalability, which impedes the growth of the European neurological monitoring devices market. European Union Medical Device Regulation came into full application in 2021; its interpretation and enforcement vary markedly across member states, creating compliance uncertainty for manufacturers. The European Coordination Committee of the Radiological, Electromedical and Healthcare IT Industry (COCIR) has reported that manufacturers across the medical device sector face significantly extended certification timelines when transitioning to the new European Medical Device Regulation, a trend linked to limited notified body capacity and evolving regulatory guidance. Moreover, the postmarket surveillance obligations under the regulation demand extensive clinical follow-up data, which is particularly burdensome for the follow-up of neuromonitoring technologies lacking long-term usage precedents. Regulatory data from long-term indicates that the process for marketing authorization of medicines within the European Union involves substantial timelines, which some stakeholders note represents a shift in the pace of approvals compared to previous regulatory frameworks. This regulatory friction not only elevates development costs but also discourages small and medium enterprises from entering the market. In addition, the United Kingdom’s departure from the European Union has introduced an entirely separate approval pathway through the Medicines and Healthcare products Regulatory Agency, necessitating duplicate clinical evaluations and technical documentation. Such jurisdictional fragmentation undermines harmonized access and forces companies to adopt country-specific commercialization strategies, slowing the pace at which advanced monitoring solutions reach European clinicians and patients.

Persistent Shortage of Trained Clinical Personnel Limits Optimal Utilization of Advanced Neuromonitoring Systems

A deficit of healthcare professionals skilled in interpreting complex neuromonitoring data hinders the expansion of the European neurological monitoring devices market. According to sources, there is a noticeable gap in the number of practicing neurologists relative to the population's needs in the European Union. This population is sent to specialized neurointensivists and neurophysiology technicians, whose expertise is essential for operating multimodal monitoring platforms and translating waveform data into clinical interventions. A significant number of higher-level intensive care units, particularly in regions outside of Western Europe, do not consistently staff dedicated neurocritical care teams. Many general intensive care physicians have expressed a lack of confidence in independently managing specialized monitoring techniques, such as continuous electroencephalography or intracranial pressure tracking. This human capital gap not only restricts the expansion of monitoring services but also increases the risk of misinterpretation and inappropriate interventions. Simulation-based training initiatives have emerged in Germany and the Netherlands. However, their scalability remains limited by funding constraints and curricular inertia within national medical education systems, perpetuating a bottleneck in the clinical uptake of otherwise available monitoring technologies.

MARKET OPPORTUNITIES

Accelerated Adoption of Artificial Intelligence-Enabled Analytical Platforms Opens New Frontiers in Predictive Neurological Surveillance

The convergence of artificial intelligence with neurological monitoring provides a potential opportunity to shift from reactive observation to predictive intervention across European healthcare settings, which is expected to accelerate the growth of the European neurological monitoring devices market. European algorithms now enable real-time analysis of electroencephalographic areal-timenamic data streams to forecast seizures, cerebral desaturation events, or delayed cerebral ischemia with unprecedented accuracy. Artificial intelligence (AI) driven cerebral oximetry systems may contribute to reducing the time to intervention for cerebral hypoxia compared to standard threshold-based alerts. Deep learning models trained on patient data may improve the ability to predict conditions like nonconvulsive status epilepticus, which can be difficult to detect in routine practice. These innovations are gaining traction as European health systems prioritize value-based care and seek to minimize costly neurological complications. These platforms are poised to redefine the standard of care as they mature and receive CE marking under the new Medical Device Regulation. They achieve this by converting raw physiological signals into actionable clinical intelligence, thereby unlocking new revenue streams and expanding the functional scope of neurological monitoring devices beyond traditional boundaries.

Strategic Expansion of Outpatient and Home-Based Neurological Monitoring Models Unlocks Underpenetrated Care Settings

The growing emphasis on decentralized care delivery in the healthcare sector is creating fertile ground for the development of portable and remote neurological monitoring solutions tailored for outpatient and home use, and thereby offers fresh opportunities for the expansion of the European neurological monitoring devices market. Driven by healthcare cost containment pressures and patient preference for ambulatory management, national health systems are increasingly reimbursing home-based diagnostic services for chronic neurological conditions. There is an increased adoption of home electroencephalography monitoring for epilepsy diagnosis, indicating a shift towards remote patient care in diagnostics. Wearable cerebral oximetry devices are now supported by a dedicated system for reimbursement in France when used for managing patients with sickle cell disease. This shift is further supported by the European Commission’s Digital Europe Programme, which allocated funding to pilot tele-neuro monitoring networks in underserved regions of Portugal and Croatia. These initiatives not only improve access for rural populations but also generate longitudinal data streams that enhance chronic disease management. Companies that develop lightweight, user-friendly, and telehealth-compatible monitoring platforms stand to capture significant market share by aligning with Europe’s strategic pivot toward proactive and community-based neurological care models that reduce hospital dependency and improve patient outcomes.

MARKET CHALLENGES

Interoperability Deficits Among Heterogeneous Healthcare IT Systems Hinder Seamless Data Integration and Clinical Workflow Efficiency

The persistent lack of interoperability between monitoring hardware and existing hospital information ecosystems is among the major challenges for the European neurological monitoring devices market. Despite widespread digitization, European healthcare facilities often operate a mosaic of electronic health record platforms, intensive care information systems, and legacy monitoring equipment from disparate vendors, creating data silos that impede real-time clinical decision making. European healthcare systems generally face ongoing challenges in achieving full interoperability for specialized clinical data, including neurological information, largely due to the variability in the adoption of health information standards across different institutions and vendor systems. This incompatibility is particularly problematic in time-sensitive scenarios such as intracranial hemorrhage management, where delayed access to trended intracranial pressure or brain tissue oxygenation data can compromise outcomes. In many hospital settings, especially in highly specialized units like neurointensive care, clinicians often encounter fragmented data landscapes, requiring the use of multiple disparate software applications to access complete patient information. European efforts to establish seamless health data exchange, such as those under the European Health Data Space initiative, face considerable implementation challenges, including disparities in technical readiness among different member state institutions and ongoing commercial preferences for proprietary systems over fully open architectures. The full clinical and operational potential of advanced neurological monitoring devices cannot be fully realized across much of Europe until seamless integration becomes the norm.

Economic Pressures and Budget Constraints in Public Healthcare Systems Curtail Capital Investment in Advanced Monitoring Infrastructure

Fiscal austerity measures and rising cost containment mandates across the region’s publicly funded healthcare systems are a form of high-end barrier to the acquisition and upkeep of high-end neurological monitoring technology. In turn inhibits the expansion of the European monitoring devices market. Despite clinical benefits, these devices often fall victim to stringent capital expenditure post-pandemically in countries grappling with post-pandemic fiscal deficits. Public health spending as a share of gross domestic product has declined in some European Union member states. In this context, neuromonitoring equipment competes unfavorably against more visible priorities such as bed capacity expansion or pharmaceutical procurement. Certain public hospitals in Southern and Eastern Europe have postponed planned upgrades to their neurocritical monitoring suites. Even in wealthier nations, procurement cycles have lengthened. The average approval timeline for new neurological monitoring systems in Sweden has increased over recent years. Moreover, maintenance and soft long-term costs are frequently excluded from long-term budgeting, leading to premature device obsolescence. The widespread use of next-generation monitoring solutions hinges on creating dedicated funding and value-based procurement mechanisms that account for long-term savings; otherwise, deployment will remain inconsistent and constrained by macroeconomic realities rather than clinical need.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Procedure, Therapeutic Application, End-Users, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | CAS Medical Systems Inc., Compumedics Ltd., Natus Medical Inc., Philips Healthcare, GE Healthcare, AMD Telemedicine, Intel Corporation, Johnson & Johnson, InTouch Health, InTechnology, MEG International Services Ltd., Rimed Inc., Siemens Healthcare, Medtronic Inc., Electrical Geodesics Incorporated, Nihon Kohden Corporation, Advanced Brain Monitoring |

SEGMENTAL ANALYSIS

By Type Insights

The monitors of brain electrical activity segment dominated the European neurological monitoring devices market and accounted for a 34.2% share in 2025. The dominance of the monitors of brain electrical activity segment is attributed to the widespread clinical reliance on electrophysiological diagnostics for conditions ranging from epilepsy to coma assessment. Electroencephalography remains the gold standard for detecting nonconvulsive seizures and monitoring brain function in comatose patients. Many neurointensive care units across Europe routinely employ continuous electroencephalography for patients with altered mental status or following cardiac arrest. Intensive care units in Germany frequently utilize electroencephalography monitoring for neurological admissions. Besides, evoked potentials are indispensable in intraoperative neurophysiological monitoring, especially during spinal and brain tumor surgeries. The use of somatosensory evoked potentials during surgery is noted for helping reduce neurological complication rates in complex spine procedures. These outcomes have solidified electroencephalography and evoked potential systems as foundational tools in both diagnostic and surgical settings. Robust reimbursement frameworks and standardized clinical protocols have accelerated device deployment. Continuous electroencephalography monitoring for suspected nonconvulsive status epilepticus is a widely available and accepted diagnostic approach in some regions. The availability of full reimbursement for this procedure has led to an increase in its utilization. Updated diagnostic frameworks in other regions now include specific reimbursement codes for long-term ambulatory electroencephalography. These updates help to facilitate the adoption of outpatient monitoring methods. These policy enablers ensure consistent funding and institutional uptake across public healthcare systems.

The near infrared spectroscopy segment is anticipated to witness the fastest CAGR of 11.3% from 2025 to 2033, which is fueled by expansion into neonatal and cardiac surgical monitoring, and enabled by technological miniaturization for broader clinical deployment. Near-infrared spectroscopy has gained significance in neonatal intensive care units for monitoring cerebral oxygenation in preterm infants. Many level three neonatal units in several Scandinavian and Dutch regions have integrated cerebral oximetry into standard care practices. In cardiac surgery, its noninvasive real-time assessment of cerebral perfusion has become standard in adult and pediatric centers. The use of cerebral oximetry monitoring has become a required practice in most pediatric cardiac bypass procedures. These validated clinical benefits are driving procurement across high acuity settings. Recent advances have yielded compact, wireless near-infrared spectroscopy devices compatible with near-infrared and emergency settings. A recent service pilot demonstrated that integrating portable cerebral oximeters into mobile stroke units improved the accuracy of patient triage. Funding has been provided to support the development of wearable near-infrared spectroscopy patches designed for the home-based monitoring of various neurodegenerative conditions.

By Therapeutic Application Insights

The stroke led the European neurological devices market and captured a 28.7% share in 2025. The leading position of the stroke segment is credited to Europe’s high cerebrovascular disease burden and standardized monitoring protocols. Stroke cases are observed in the general population. Medical guidelines recommend specific types of patient monitoring, such as multimodal neuromonitoring, for certain post-treatment care scenarios and high-risk conditions. Clinical protocols in various healthcare facilities incorporate consistent monitoring device usage for at-risk cases. The older adult population is expanding, which contributes to an increased demographic susceptible to strokes. Hospital admissions for stroke in certain older age demographics appear to be rising, increasing the need for neurological surveillance in acute care environments.

The epilepsy segment is likely to experience the f, fastest CAGR of 10.8% during the forecast period, owing to the rising ambulatory diagnostics and home monitoring drive volume, and the policy initiatives and early intervention programs that expand screening. Ambulatory electroencephalography has become the cornerstone of epilepsy diagnosis in outpatient pathways. There has been an increase in the adoption and use of remote long-term electroencephalography procedures in healthcare systems. Portable devices now enable multi-day monitoring without hospitalization, improving diagnostic yield and patient compliance. New initiatives in France to improve epilepsy diagnosis have led to an increase in the number of newly diagnosed cases. Besides, school-based seizure detection pilot programs in the Netherlands and Sweden, utilizing wearable electroencephalography headbands, have demonstrated feasibility in identifying undiagnosed pediatric epilepsy, creating new screening channels and reinforcing market growth.

By End Users' Insights

The hospitals, neurological centers, and institutions held the leading share of 61.4% of the European neurological monitoring devices market. The prominence of the hospital's neurological centers and institutions segment is propelled by its role as the primary site for acute neurological care and complex monitoring. European hospitals house nearly all neurointensive and comprehensive stroke units, necessitating multimodal monitoring suites. Intensive care units in Western Europe are commonly equipped with multiple types of neurological monitors, such as intracranial pressure sensors and electroencephalography systems. Certain regions, like Germany, have dedicated neurocritical care beds that utilize integrated monitoring platforms. Public procurement systems in countries like Sweden and France consolidate medical device purchasing at regional hospital networks, which ensures bulk deployment of standardized monitoring systems. Centralized purchasing efforts in some countries cover the majority of public hospital needs for neurological monitoring equipment.

The clinics and ambulatory surgical centers segment is on the rise and is expected to be the fastest-growing segment in the market by witnefastest-growing 9.6%. The rapid expansion of the clinics and ambulatory surgical centers segment is fueled by procedural decentralization and technological adaptation. The volume of minor neurosurgical interventions, such as carpal tunnel releases with intraoperative neuromonitoring, has shifted to ambulatory settings. As per research, there is an observable trend in the Netherlands, as in many other regions, towards shifting healthcare from inpatient hospital settings to more efficient and affordable ambulatory care centers. Ambulatory centers are increasingly leveraging cloud-based electroencephalography platforms that transmit data to central neurology teams. Spain's Ministry of Health is actively pursuing a national digital health strategy to integrate technology into the public health system, which includes the expansion of telemedicine services to improve healthcare access and efficiency. This model is replicating across Southern Europe, accelerating device penetration in non-hospital environments.

COUNTRY LEVEL ANALYSIS

Germany Neurological Monitoring Devices Market Analysis

Germany outperformed other countries in the European neurological monitoring devices market and accounted for a 19.3% share in 2025. The dominance of the German market is primarily driven by its advanced neurocritical infrastructure and robust medtech ecosystem. The country hosts a notable number of neurology specialty hospitals, many integrated with university research centers that pioneer monitoring protocols. Data from German health statistics indicate a long-term increase in the number of surgical procedures related to certain neurodegenerative diseases. Healthcare guidelines in Germany increasingly emphasize the use of neuroprognostication techniques, including EEG monitoring, in post-cardiac arrest patient management. There is growing interest and study in Germany regarding the expanded use of telemedicine for neurointensive care consultations to improve care quality across various intensive care units. Besides, Germany’s strong domestic medtech industry, including companies like Brain Products GmbH, ensures rapid technology transfer from research to clinical deployment, reinforcing its market leadership.

France Neurological Monitoring Devices Market Analysis

France was the second-largest player in the European neurological monitoring devices market by holding a share of 15.7% in 2025 because of its centralized healthcare system and proactive neurological care policies. The French National Authority for Health publishes extensive guidelines on the management of acute stroke cases, emphasizing robust neurological assessment protocols in specialized neurovascular units to improve patient outcomes. Clinical practices related to perioperative neuroprotection in France are evolving, with an increasing emphasis on the use of advanced monitoring techniques in public hospitals. France's national health strategies, including epilepsy action plans, prioritize expanding access to specialized diagnostic facilities and improving the availability of electroencephalography (EEG) systems for outpatient monitoring. These coordinated policy interventions ensure consistent device adoption across both urban and rural care networks.

United Kingdom Neurological Monitoring Devices Market Analysis

The European Kingdom is another major region in the European neurological monitoring devices market due to evidence-based adoption pathways and strong reimbursement support. The National Institute for Health and Care Excellence has issued multiple technology appraisals endorsing continuous electroencephalography for nonconvulsive seizure detection, leading to full National Health Service coverage. Multimodal monitoring is a recognized and growing area of practice within neurocritical care to help prevent secondary brain injury in patients with acute brain injuries, such as traumatic brain injury and subarachnoid hemorrhage. The United Kingdom’s emphasis on data-driven procurement, through bodies like the National Health Service Supply Chain, ensures cost-effective scaling of monitoring technologies across its integrated care system.

Italy Neurological Monitoring Devices Market Analysis

Italy is moving ahead steadfastly in the European neurological monitoring devices market due to its aging population and rising cerebrovascular disease burden. The aging population contributes to a growing need for healthcare services. There is an increasing demand for neurological surveillance due to demographic shifts. Hospitalizations related to stroke have shown an upward trend. Health authorities have taken steps to improve neurocritical care facilities. Neurocritical units are being upgraded with advanced monitoring systems. Moreover, Lombardy and Lazio regions have launched public tenders for portable electroencephalography devices to support epilepsy diagnosis in community clinics, addressing long diagnostic delays that previously exceeded eight weeks.

Spain Neurological Monitoring Devices Market Analysis

Spain is anticipated to expand notably in the European neurological devices market from 2025 to 2033. This growth is attributable to digital health integration and regional healthcare autonomy. Autonomous communities such as Catalonia and Andalusia have independently invested in tele-neuro monitoring networks to overcome neurologist shortages in rural provinces. The number of remote electroencephalography procedures has increased notably in recent years. The growth in these procedures was supported by new reimbursement structures. Additionally, Spain’s inclusion in European Union-funded projects has enabled pilot deployments of AI-enhanced near-infrared spectroscopy in mobile stroke units, positioning the country as an innovator in decentralized neurological care despite moderate overall spending.

TOP LEADING PLAYERS IN THE MARKET

- Nihon Kohden is a prominent contributor to the European neurological monitoring devices market, with a strong emphasis on electroencephalography and evoked potential systems. The company supplies advanced neuromonitoring solutions to neurocritical care units and operating theaters across Germany, France, and the United Kingdom. In recent years, Nihon Kohden has expanded its European service network to ensure faster device deployment and technical support. It has also partnered with academic hospitals to validate AI-enhanced electroencephalography algorithms for AI-enhanced prediction, aligning with Europe’s shift toward predictive neurology. These initiatives reinforce its clinical credibility and deepen integration within European healthcare workflows without relying solely on hardware sales.

- Masimo Corporation plays a pivotal role in Europe through its cerebral oximetry and near-infrared spectroscopy technologies. Its INVOS and O3 systems are widely adopted in cardiac surgery and neonatal intensive care units across Scandinavia and Western Europe. To strengthen its position, Masimo has intensified regulatory engagements with European notified bodies to secure expanded indications for brain oxygenation monitoring in trauma and stroke settings. The company also launched cloud-connected cerebral oximeters compatible with European electronic health record standards, facilitating seamless data integration. These efforts position Masimo as a key enabler of multimodal monitoring in high acuity environments across the region.

- Integra LifeSciences holds significant influence in the European market through its intracranial pressure and brain tissue oxygen monitoring platforms. The company’s Camino and Licox systems are standard in neurotrauma centers in Italy, Spain, and the Netherlands. Integra has recently enhanced its European footprint by establishing a dedicated neuromonitoring training academy in France to address clinician skill gaps. It also completed a strategic collaboration with a major German university hospital to develop real-time analytics for intracranial compliance. Real-time actions demonstrate a commitment to clinical education and innovation, thereby solidifying long-term relationships with European neurocritical institutions.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European neurological monitoring devices market are adopting four strategic approaches to sustain competitiveness. First, they pursue regulatory alignment by proactively engaging with European notified bodies to expedite CE marking under the Medical Device Regulation. Second, they invest in clinical evidence generation through multicenter trials with European academic hospitals to validate device efficacy in local patient populations. Third, they expand service and training infrastructure to address the shortage of skilled personnel and ensure optimal device utilization. Fourth, they integrate artificial intelligence and cloud connectivity to meet Europe’s demand for predictive and interoperable monitoring solutions.

COMPETITIVE LANDSCAPE

The European neurological monitoring devices market presents a moderately consolidated competitive landscape dominated by established multinational medtech firms alongside specialized innovators. Competition centers not on pr, i ce, but on clinical validation, interoperability, nd postmarket support. Leading companies differentiate through robust regulatory compliance tailored to Europe’s fragmented healthcare systems and by embedding their devices into standardized care pathways, such as stroke and enhanced recovery after surgery protocols. Recent years have seen intensified collaboration between device manufacturers and next-generation institutions to co-develop next-generation monitoring algorithms, particularly in AI-driven electroencephalography and cerebral oximetry. Smaller firms compete by focusing on niche applications like ambulatory epilepsy monitoring or portable transcranial Doppler. The entry barriers remain, mainly due to stringent regulatory requirements, long sales cycles, and the necessity for extensive clinical training. Consequently, market participants prioritize long-term partnerships with hospitals rather than transactional sales.

KEY MARKET PLAYERS

Some of the leading companies operating in the europe neurological monitoring devices market profiled in this report are

- CAS Medical Systems Inc.

- Compumedics Ltd.

- Natus Medical Inc.

- Philips Healthcare

- GE Healthcare

- AMD Telemedicine

- Intel Corporation

- Johnson & Johnson

- InTouch Health

- InTechnology

- MEG International Services Ltd.

- Rimed Inc.

- Siemens Healthcare

- Medtronic Inc.

- Electrical Geodesics Incorporated

- Nihon Kohden Corporation

- Advanced Brain Monitoring

MARKET SEGMENTATION

This research report on the europe neurological monitoring devices market is segmented and sub-segmented into the following categories.

By Type

- Monitors of Intracranial Pressure & Blood Flow Dynamics

- Intracranial Pressure Monitor Jugular Venous Oximetry

- Transcranial Doppler (TCD) Ultrasonography

- Near-Infrared Spectroscopy

- Brain Tissue Oxygen Tension Monitor

- Monitors of Brain Electrical Activity

- Electroencephalography & Evoked Potentials

By Procedure

- Non-Invasive & Invasive

By Therapeutic Application

- Traumatic Brain Injuries

- Stroke

- Dementia

- Headache Disorders

- Sleep Disorders

- Epilepsy

- Parkinson’s Disease & Huntington’s Disease.

By End-Users

- Hospitals, Neurological Centers & Institutions

- Clinics & Ambulatory Surgical Centers

- Diagnostic Centers and Ambulances

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic, and the Rest of Europe

Frequently Asked Questions

1. What drives growth in the Europe Neurological Monitoring Devices Market?

Key drivers in the Europe Neurological Monitoring Devices Market include surging incidences of brain disorders, geriatric demographics, and innovations in EEG and cerebral oximeters. Investments in healthcare tech and R&D boost adoption across hospitals in Germany and France.

2. Which products dominate the Europe Neurological Monitoring Devices Market?

EEG devices and MRI systems lead the Europe Neurological Monitoring Devices Market, with intracranial pressure monitors and cerebral oximeters gaining traction for TBI and stroke applications. Multichannel EEGs excel in epilepsy diagnostics

3. What is the role of Germany in the Europe Neurological Monitoring Devices Market?

Germany dominates the Europe Neurological Monitoring Devices Market due to high brain disorder rates, new device launches, and robust healthcare infrastructure. It drives demand for EEG and neuro monitoring innovations.

4. How does stroke impact the Europe Neurological Monitoring Devices Market?

Stroke significantly propels the Europe Neurological Monitoring Devices Market as leading indication, with devices like Doppler ultrasound and EEG enabling real-time monitoring. Rising cases in aging Europe fuel this segment.

5. What are key trends in the Europe Neurological Monitoring Devices Market?

Trends in the Europe Neurological Monitoring Devices Market feature AI integration, wearable EEGs, and wireless systems for remote monitoring of epilepsy and sleep disorders. Minimally invasive tech enhances precision.

6. Who are major players in the Europe Neurological Monitoring Devices Market?

Leading firms in the Europe Neurological Monitoring Devices Market include Medtronic, Philips Healthcare, GE Healthcare, Siemens Healthineers, and Nihon Kohden, focusing on EEG and ICP monitor innovations.

7. What is the forecast for the Europe Neurological Monitoring Devices Market by 2033?

The Europe Neurological Monitoring Devices Market eyes USD 5.43 billion by 2033, driven by neurotech advances and chronic disorder prevalence. EEG and oximeters will expand via telemedicine.

8. How does epilepsy monitoring fit the Europe Neurological Monitoring Devices Market?

Epilepsy monitoring via long-term EEG thrives in the Europe Neurological Monitoring Devices Market, supported by wearable tech and NHS pilots in the UK for remote seizure tracking.

9. What challenges face the Europe Neurological Monitoring Devices Market?

Challenges in the Europe Neurological Monitoring Devices Market involve high costs, CE marking regulations, and reimbursement variances. Yet, AI and portability counter these hurdles.

10. Which diseases key the Europe Neurological Monitoring Devices Market?

TBI, stroke, epilepsy, Parkinson's, and sleep disorders anchor the Europe Neurological Monitoring Devices Market, with devices tailored for early detection in clinical settings.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com