Europe Non-Invasive Prenatal Testing Market Research Report By Instruments, Method, Application, End User and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) – Analysis on Market Size, Share, Trends and Growth Forecast (2026 to 2034)

Market Size, 2025

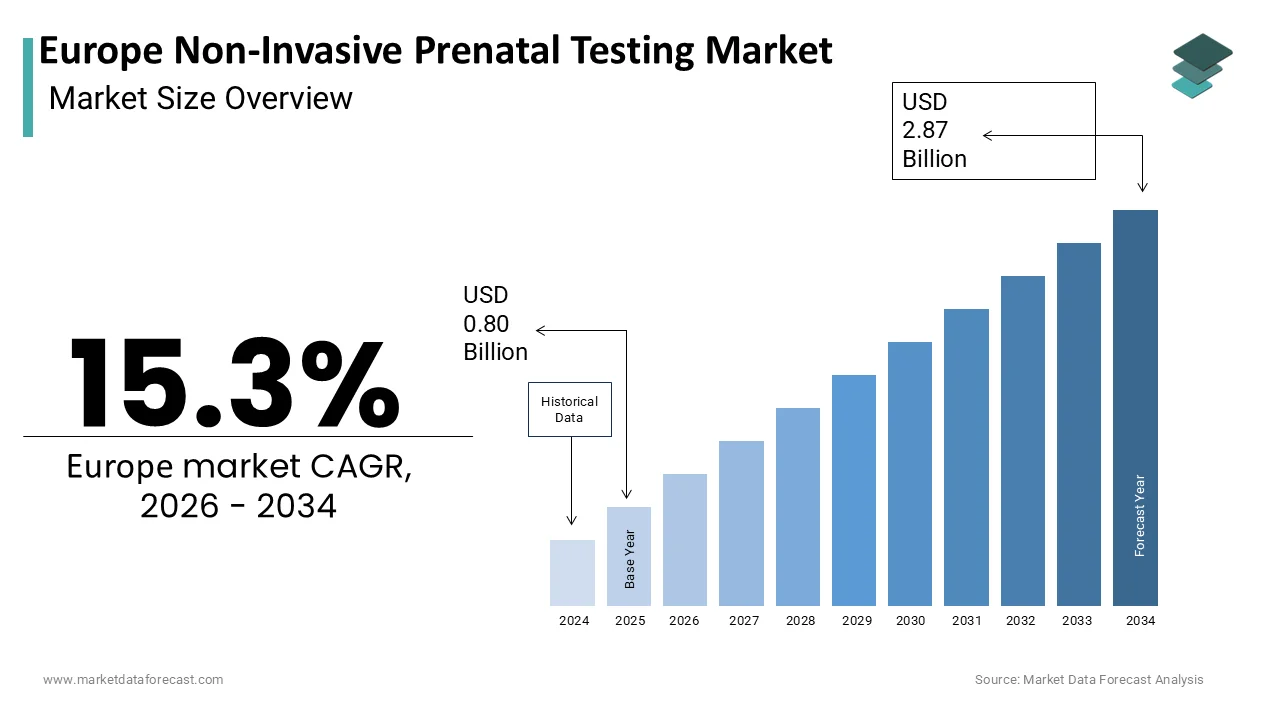

$0.80 BnMarket Estimate, 2026

$0.92 BnMarket Forecast, 2034

$2.87 BnCAGR, 2026–2034

15.3%Europe Non-Invasive Prenatal Testing Market Summary

Europe non-invasive prenatal testing market was valued at USD 0.69 billion in 2024, estimated at USD 0.80 billion in 2025, and is projected to reach USD 2.48 billion by 2033 (CAGR 15.3%, 2025–2033), driven by rising maternal age, public screening program adoption, and growing preference for risk-free prenatal diagnostics.

Market Highlights

- 2024 (actual): USD 0.69 billion

- 2025 (est): USD 0.80 billion

- 2033 (forecast): USD 2.48 billion

- CAGR (2025–2033): 15.3%

Quick growth drivers

- Rising maternal age across Europe, increasing aneuploidy risk, and screening demand.

- High clinical accuracy of NIPT for trisomy 21 with minimal false positives.

- Shift away from invasive diagnostics (amniocentesis, CVS) due to miscarriage risk.

- Integration into national prenatal screening programs in countries such as the Netherlands, Denmark, and Belgium.

- EU cross-border healthcare access, enabling wider availability of advanced diagnostics.

Principal restraints

- Fragmented reimbursement policies across EU member states are limiting universal access.

- Out-of-pocket cost burden in countries with private-pay dominant models.

- Insufficient genetic counseling infrastructure in several markets.

- Ethical and regulatory caution restricts broader test scope expansion.

High-value opportunities

- Expansion beyond common trisomies into microdeletions and monogenic disorders.

- Laboratory-developed NIPT services enabling localized, faster turnaround testing.

- Regional genomics hubs supporting public health screening equity.

- Precision medicine alignment, positioning NIPT as a genomic risk-stratification tool.

Key operational challenges

- Regulatory ambiguity under EU IVDR for laboratory-developed tests.

- Inconsistent test scope and marketing claims across private providers.

- Psychosocial impact management for ambiguous or incidental findings.

- Scaling counseling services alongside test volume growth.

Fastest-growing segments

- Fetal cells in maternal blood (FCMB): 19.4% CAGR — potential shift toward true non-invasive diagnostics.

- Digital PCR platforms: 13.2% CAGR — decentralized and rapid testing adoption.

- Hospital-based testing: 11.8% CAGR — integrated prenatal care pathways.

- Expanded genomic screening panels: high future upside pending reimbursement clarity.

Regional leadership & dynamics

Netherlands (lead, 22.4%)

- State-funded NIPT under the national screening program.

- Centralized labs, mandatory counseling, and high uptake.

Denmark (17.4%)

- Universal NIPT access within public healthcare.

- Fully digitized, population-wide screening model.

United Kingdom

- Hybrid public-private model with accelerating NHS adoption.

- Strong lab infrastructure serving Europe.

Germany & France

- High demand driven by maternal age trends.

- Gradual reimbursement expansion under strict bioethical governance.

What wins commercially (competitive edge)

- CE-IVD compliant platforms aligned with EU IVDR.

- High analytical validity (NGS-based) with robust quality assurance.

- Integrated genetic counseling support.

- Localized laboratory networks ensuring fast turnaround and data sovereignty.

- Alignment with national screening pathways rather than DTC-only models.

Top strategic ask for executives

- Prioritize public reimbursement integration over pure private-pay expansion.

- Invest in expanded but clinically validated panels.

- Strengthen ethical governance and counseling ecosystems.

- Build country-specific market access strategies reflecting EU fragmentation.

Leading players

Roche Diagnostics · Illumina · Thermo Fisher Scientific · QIAGEN · Agilent Technologies · PerkinElmer · Pacific Biosciences · BGI · Philips Healthcare · GE Healthcare

Europe Non-Invasive Prenatal Testing Market Size

The Europe Non-Invasive Prenatal Testing Market is projected to grow from USD 0.80 billion in 2025 to USD 0.92 billion in 2026 and reach USD 2.87 billion by 2034, registering a CAGR of 15.3% during the forecast period from 2026 to 2034.

Non-invasive prenatal testing (NIPT) is a molecular screening method that analyzes cell-free fetal DNA circulating in maternal blood to assess the risk of chromosomal abnormalities, most commonly trisomies 21 (Down syndrome), 18 (Edwards syndrome), and 13 (Patau syndrome). In Europe, non-invasive prenatal testing (NIPT) is typically available from the tenth week of gestation, providing a highly effective screening method for trisomy 21 with a consistently high detection rate and a significantly lower false-positive rate compared to traditional screening methods. NIPT is a non-invasive screening test that carries no procedural risk to the fetus, which is a key difference when compared with invasive diagnostic procedures like amniocentesis and chorionic villus sampling, which inherently carry a small risk of pregnancy loss. According to Eurostat data, the annual number of live births across the European Union has been on a general downward trend in recent years, falling below four million. Concurrently, there has been a steady increase in the average maternal age at first childbirth across the EU member states. Furthermore, the European Commission’s Cross-Border Healthcare Directive facilitates patient access to advanced diagnostics, enabling cross-national NIPT adoption. In an era of advancing genomics and increased emphasis on patient safety, NIPT has grown into a central pillar of modern prenatal care across Europe.

MARKET DRIVERS

Rising Maternal Age and Associated Aneuploidy Risk Drive Screening Demand

The continuous increase in the average maternal age across the region is a key driver of the European non-invasive prenatal testing market. This directly elevates the clinical need for accurate early screening. The mean age of women at childbirth in the European Union has shown a consistent upward trend over the past several years, with countries in Southern Europe generally reporting the highest average maternal ages. This trend is clinically significant because the risk of fetal trisomy rises exponentially with maternal age. The risk of carrying a fetus with Down syndrome increases notably as maternal age advances, a trend consistently tracked by public health surveillance systems. National health systems increasingly recognize NIPT as a cost-effective triage tool to reduce unnecessary invasive procedures. Following the integration of NIPT into the national prenatal screening program in the Netherlands, a substantial majority of women at increased risk now choose NIPT as their initial screening method, consequently decreasing the frequency of invasive diagnostic procedures. This risk stratification not only enhances patient safety but also optimizes healthcare resource allocation, reinforcing NIPT’s role as a standard of care in aging obstetric populations.

Integration into National Public Health Screening Programs Enhances Accessibility

The formal incorporation of NIPT into publicly funded prenatal pathways across multiple European countries has dramatically expanded its accessibility and normalized its use, which propels the expansion of the European non-invasive prenatal testing market. Unlike regions where NIPT remains a private pay service, countries like Belgium, the Netherlands, and Denmark offer state-reimbursed NIPT to women identified as high risk through first-trimester combined screening. The number of publicly funded NIPT tests performed has been substantial, covering nearly all eligible pregnancies in the region. This institutional endorsement reduces socioeconomic disparities in access and increases uptake among broader patient groups. Following the introduction of universal reimbursement in Belgium, there was a significant decrease in the false positive rate for trisomy 21 screening. Moreover, national programs mandate quality assurance through accredited laboratories, ensuring analytical reliability and standardized counseling protocols. These public health frameworks transform NIPT from a premium add-on into an essential component of equitable, evidence-based prenatal care across Europe.

MARKET RESTRAINTS

Fragmented Reimbursement Policies Limit Universal Patient Access

Inconsistent public funding for non-invasive prenatal testing across European nations remains a critical restraint despite clinical validation, creating stark disparities in patient access based on geography and income, and thereby restraining the growth of the European non-invasive prenatal testing market. While countries like the Netherlands and Denmark offer full reimbursement within national screening programs, others, such as Germany, France, and Italy, restrict coverage to high-risk cases or provide no public funding at all. NIPT is now an established benefit of the statutory health insurance system, specifically for detecting trisomies 21, 18, and 13, when deemed medically necessary in the individual's situation. Medical necessity is not exclusively tied to a prior high-risk screening result; personal reasons, such as significant anxiety about potential trisomy, can also justify coverage. Coverage for the NIPT has increased, meaning fewer individuals must pay for the test entirely out of pocket compared to the period before the 2022 policy update. Costs for other screenings, such as the combined first-trimester screening (which can provide an initial risk assessment), are often not covered by statutory insurance and typically remain an out-of-pocket expense. This financial barrier disproportionately affects low-income and rural populations, exacerbating health inequities. The absence of EU-wide harmonization means a woman in Lisbon may access NIPT for free while her counterpart in Warsaw must navigate private clinics with variable quality standards, which affects the principle of equitable genomic medicine across the region.

Ethical and Counseling Infrastructure Gaps Undermine Informed Decision Making

The rapid technological adoption of NIPT has outpaced the development of robust genetic counseling and ethical safeguards in many European healthcare systems, which constrains the expansion of the European non-invasive prenatal testing market. This poses a significant restraint on responsible implementation. NIPT’s high accuracy can create a false perception of diagnostic certainty among patients, yet it remains a screening tool that requires confirmatory invasive testing for positive results. In countries like Poland and Greece, NIPT is increasingly marketed directly to consumers. This knowledge gap can lead to psychological distress, inappropriate clinical decisions, or ethical dilemmas, particularly as NIPT expands to screen for microdeletions and sex chromosome aneuploidies with lower predictive values. Failing to provide adequate counseling alongside NIPT risks diminishing its positive impact, potentially leading to poorly informed patient decisions and a compromise of their autonomy.

MARKET OPPORTUNITIES

Expansion into Broader Genomic Screening Unlocks New Clinical Utility

The progressive extension of NIPT beyond common trisomies into subchromosomal anomalies and monogenic disorders is a major opportunity to enhance prenatal diagnostics across the region, which is expected to fuel the growth of the European non-invasive prenatal testing market. Advanced NIPT platforms now detect microdeletion syndromes with clinically relevant sensitivity. Pilot programs are testing the cost-effectiveness of expanded panels for high-risk pregnancies, though they aren't routinely reimbursed yet. Furthermore, research institutions are developing NIPT assays for single-gene disorders such as skeletal dysplasias and Noonan syndrome, leveraging whole-genome sequencing and bioinformatic refinement. Enhanced analytical validity and the evolution of health technology assessments may allow these advanced applications to convert NIPT into a comprehensive fetal genomic assessment, in line with Europe’s precision medicine goals.

Growth of Laboratory Developed Tests and Regional Diagnostic Hubs

The proliferation of laboratory-developed NIPT services within European academic medical centers and private diagnostics networks creates a potential opportunity to localize testing, reduce turnaround times, and tailor offerings to regional needs, which in turn provides fresh prospects for the European non-invasive prenatal testing market. In Spain, the publicly funded network integrates regional laboratories to offer standardized NIPT with uniform quality control, increasing equity of access across autonomous communities. Besides, local platforms facilitate adaptation to national guidelines. This decentralization not only strengthens data sovereignty and clinical responsiveness but also fosters innovation through region-specific validation studies, which positions Europe to lead in ethically governed, locally embedded genomic prenatal care.

MARKET CHALLENGES

Regulatory Ambiguity Around Test Scope and Marketing Claims

The evolving and inconsistent regulatory classification of NIPT across European jurisdictions poses a persistent challenge to the European non-invasive prenatal testing market. This negatively impacts market standardization and consumer protection. While NIPT kits marketed as in vitro diagnostic medical devices fall under the EU In Vitro Diagnostic Regulation, many laboratory-developed tests operate under national derogations with variable oversight. The implementation of national guidelines governing the scope of conditions reportable via NIPT varies. This leads to a lack of uniformity in clinical practice. Also, the range of conditions screened for by some private health services can be extensive. Concerns have been raised that some screening practices lack sufficient clinical validation. One national health authority has indicated that certain related advertising practices could be seen as potentially misleading. This regulatory gray zone enables aggressive direct-to-consumer marketing that may overstate test capabilities, eroding trust in legitimate services. Moreover, the lack of harmonized performance standards complicates cross-border recognition of results, hindering the EU’s goal of integrated digital health. The market faces potential fragmentation and consumer confusion in the absence of a unified framework for test validation, permissible indications, and advertising.

Psychosocial and Societal Implications of Expanded Fetal Information

The increasing capacity of NIPT to reveal extensive fetal genomic information introduces complex psychosocial and societal challenges that European healthcare systems are unprepared to manage, and thereby hinders the expansion of the European non-invasive prenatal testing market. The expansion of NIPT to cover sex chromosome conditions and variants of uncertain significance means expectant parents are increasingly likely to encounter ambiguous or incidental test results that lack clear clinical guidance. Furthermore, the routine availability of fetal sex and genetic traits raises concerns about non-medical sex selection and the potential reinforcement of ableist attitudes toward disability. National counseling services remain under-resourced to address these nuanced conversations. Expanding NIPT (non-invasive prenatal testing) without dedicated investment in essential supporting systems, like counseling, ethics, and inclusive education, jeopardizes the balance, favoring a technology-first approach over holistic patient autonomy and equitable outcomes.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Instruments, Method, Setup Type, Application, End-User Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | GE Healthcare (U.S.), Koninklijke Philips N.V. (Netherlands), Illumina, Inc. (U.S.), Thermo Fisher Scientific, Inc. (U.S.), F. Hoffmann-La Roche Ltd. (Switzerland), Pacific Biosciences of California, Inc. (U.S.), PerkinElmer, Inc. (U.S.), QIAGEN N.V. (Germany), Agilent Technologies, Inc. (U.S.), and Beijing Genomics Institute (China) |

SEGMENTAL ANALYSIS

By Instruments Insights

The next-generation sequencing (NGS) segment held the largest share of 58.4% of the European non-invasive Prenatal Testing Market in 2025. The prominence of the NGS segment is credited to its unparalleled accuracy, scalability, and capacity to detect a broad spectrum of chromosomal anomalies. A different factor behind this dominance is its superior analytical performance. Unlike targeted methods, NGS enables genome-wide analysis, allowing detection of sex chromosome aneuploidies and select microdeletions without a significant cost increase per sample. A further driver is institutional adoption; national screening programs in the Netherlands, Denmark, and Sweden exclusively use NGS platforms due to their reproducibility and compatibility with centralized laboratory workflows. Additionally, declining sequencing costs have made NGS economically viable even for mid-volume labs, cementing its position as the technological backbone of European prenatal genomics.

The digital PCR segment is expected to exhibit a noteworthy CAGR of 13.2% from 2025 to 2033. The rapid expansion of the digital PCR segment is fuelled by demand for rapid, targeted, and instrument lean testing in decentralized settings. An additional driver is its operational simplicity. Digital PCR provides timely results, often within two days, using small benchtop systems. The technology requires minimal bioinformatics support, making it suitable for standard hospital laboratories. Digital PCR offers reliable performance in key applications, showing strong alignment with results from next-generation sequencing (NGS) methods. This reliability has been observed across various tests, supporting its use for core indications. An additional accelerator is cost efficiency in low-throughput environments. Countries where centralized genomics hubs are limited are increasingly adopting digital PCR to bring NIPT closer to the point of care, which supports equitable access while maintaining clinical rigor.

By Method Insights

The cell-free DNA analysis segment led the European in-vitro prenatal testing market by accounting for a substantial share in 2025. It serves as the universal methodological foundation due to its non-invasive nature, early gestational applicability, and robust clinical validation. The foremost factor driving its dominance is biological feasibility. These DNA fragments appear in the first trimester of pregnancy. The quantity present is typically sufficient for reliable analysis. This method is considered more practical than relying on intact fetal cells found in the maternal blood. The isolation of these circulating DNA fragments can be managed using standard blood draw volumes and automated laboratory processes. A further driver of this segment is regulatory endorsement. All publicly funded NIPT programs in the EU, from the Dutch TRIDENT initiative to Denmark’s national screening, specify cfDNA as the required analyte. This methodological standardization ensures consistency in performance, interpretation, and quality control across diverse healthcare settings.

The Fetal Cells in Maternal Blood (FCMB) segment is predicted to witness the highest CAGR of 19.4% between 2025 and 2033. The swift growth of the FCMB segment is propelled by breakthroughs in rare cell capture and whole genome amplification that overcome historical technical barriers. Unlike cf DNA, which reflects placental genetics and may yield confined placental mosaicism, fetal nucleated red blood cells and trophoblasts provide direct access to the complete fetal genome, enabling diagnosis, not just screening, of monogenic disorders. A microfluidic enrichment platform has shown effectiveness in isolating intact fetal cells from samples. The platform demonstrated success in processing second-trimester samples with a high degree of purity. Funding has been provided to a project focused on developing advanced non-invasive prenatal testing (NIPT). This NIPT development is aimed at conditions such as cystic fibrosis and spinal muscular atrophy. These breakthroughs mark FCMB as a potential paradigm shift for truly non-invasive diagnostics, drawing crucial investment from academic and venture sources across Germany, Switzerland, and the UK, even as clinical deployment awaits.

By End User Insights

The diagnostic laboratories segment dominated the European non-invasive prenatal testing market by capturing a significant share in 2025. Factors such as centralized testing models, regulatory requirements for accredited facilities, and economies of scale in high-volume processing mainly contribute to the supremacy of the diagnostic laboratories segment. National screening programs in countries mandate that all NIPT samples be analyzed in ISO 115189-accredited laboratories to ensure analytical validity and data traceability. An additional growth factor is technological complexity. NGS-based NIPT requires specialized instrumentation, bioinformatics pipelines, and quality control frameworks that are cost-prohibitive for most hospitals. Furthermore, cross-border sample referral under the EU Cross-Border Healthcare Directive has consolidated testing into regional reference centers, enhancing efficiency. This centralized model ensures standardized performance, reduces inter-laboratory variability, and supports large-scale data collection for continuous improvement, which makes diagnostic labs the operational cornerstone of European NIPT delivery.

The hospitals segment is estimated to register the fastest CAGR of 11.8 from 2025 to 2030, owing to the integration of point-of-care genomics into obstetric care pathways and the deployment of simplified testing platforms like digital PCR. In countries with decentralized healthcare systems such as Italy and Spain, regional hospitals are establishing in-house NIPT services to reduce turnaround time and retain patients within their networks. A further growth driver is enhanced patient navigation; when testing occurs within the prenatal clinic, counseling, blood draw, and result discussion happen in a single care continuum, improving compliance and psychological support. Hospitals are evolving into active diagnostic hubs rather than just sample collection points, thanks to more compact and automated instrumentation.

COUNTRY LEVEL ANALYSIS

Netherlands Non-Invasive Prenatal Testing Market Analysis

The Netherlands was the top performer in the European non-invasive prenatal testing market by accounting for a share of 22.4% in 2025 because of its world-leading national screening program that integrates NIPT as a second-tier test for all pregnant women. Public funding for non-invasive prenatal testing is available under specific criteria. The testing is offered to women with an elevated risk identified through initial screening. Widespread adoption of the test is evident among the eligible population. The program mandates centralized analysis through four accredited laboratories, ensuring uniform quality and data collection. High public awareness drives exceptional uptake. Moreover, the Dutch system includes mandatory pre- and post-test counseling, setting a global benchmark for ethical implementation. This combination of universal access, rigorous quality control, and patient education solidifies the Netherlands as the most mature and equitable NIPT market in Europe.

Denmark Non-Invasive Prenatal Testing Market Analysis

Denmark followed closely in the European non-invasive prenatal testing market by holding a 17.4% share in 2025. This growth is credited to its seamless integration of NIPT into the national free healthcare system without risk stratification. In Denmark, NIPT is offered as a screening option for trisomies 21, 18, and 13 to all pregnant women. The test is widely utilized across pregnancies in the country. The entire workflow, from blood draw at local clinics to analysis at the Statens Serum Institut, is digitized and linked to the national electronic health record, enabling real-time monitoring and outcome tracking. This universal approach has reduced invasive procedures since program inception. Denmark’s success lies in its centralized public health infrastructure, strong genomic expertise, and societal consensus on equitable access to advanced diagnostics.

United Kingdom Non-Invasive Prenatal Testing Market Analysis

The United Kingdom grew steadily in the European non-invasive prenatal testing market due to a hybrid model where private pay dominates, but NHS adoption is accelerating. Non-invasive prenatal testing (NIPT) is not yet funded for everyone. The national health system provides NIPT to women considered to have a higher risk after initial screening. A significant number of publicly funded tests are performed annually. Separately, private healthcare providers conduct many additional tests each year. Demand in the private sector is likely influenced by personal patient preference and a general upward trend in maternal age at the time of childbirth. The UK also hosts major NIPT laboratories, which serve both domestic and European clients. Recent NHS England evaluations confirm NIPT’s cost-effectiveness, paving the way for broader reimbursement. This dual pathway reflects the UK’s pragmatic and evidence-led transition toward mainstream genomic prenatal care.

Germany Non-Invasive Prenatal Testing Market Analysis

Germany expanded moderately in the European non-invasive prenatal testing market owing to its federal healthcare structure and predominantly private pay model. Statutory health insurers generally provide coverage for NIPT primarily in cases identified as high-risk, subject to a prior approval process. A significant volume of these tests is accessed by individuals outside the scope of statutory insurance coverage. These tests typically involve patients paying for the service themselves. The personal cost associated with obtaining the test varies within a certain range. Utilization of NIPT is notable across the population. Several federal states, including Bavaria and BBaden-Württemberg, have launched pilot programs to evaluate public funding, reflecting growing clinical recognition. Germany also hosts leading diagnostic laboratories and research centers, which contribute to European NIPT validation studies. High health literacy and strong patient advocacy further drive demand. Despite reimbursement barriers, Germany’s large population and medical innovation ecosystem sustain robust market activity.

France Non-Invasive Prenatal Testing Market Analysis

France is likely to grow in the European non-invasive prenatal testing market from 2025 to 2033 due to its cautious yet progressive incorporation of NIPT under strict bioethical governance. France also mandates pre-test counselling through certified genetic centers, with numerous such units nationwide. The country’s high birth rate and aging maternal profile create substantial demand. Ongoing parliamentary debates aim to expand reimbursement, reflecting a careful balance between technological advancement, ethical safeguards, and equitable access, which positions France as a model of regulated innovation in prenatal genomics.

COMPETITIVE LANDSCAPE

Competition in the European Non-Invasive Prenatal Testing Market is characterized by a mix of global diagnostics leaders and specialized genomics firms, all operating within a highly regulated and ethically sensitive environment. The market is not driven by price but by analytical validity, regulatory compliance, and integration into national healthcare pathways. Leading companies leverage next-generation sequencing or proprietary molecular methods to achieve high sensitivity while navigating strict EU rules on permissible test indications and data handling. Differentiation occurs through test scope, such as inclusion of microdeletions or twin zygosity determination, counseling support, and digital health integration. National disparities in reimbursement and public program inclusion create fragmented commercial landscapes, requiring localized strategies. New entrants face high barriers due to the need for CE IVD certification, accredited laboratory partnerships, and clinical evidence generation. As European countries progressively adopt NIPT into routine care, competition increasingly centers on service reliability, ethical governance, and alignment with public health priorities rather than technological novelty alone.

KEY MARKET PLAYERS

Companies playing a dominant role in the europe non-invasive prenatal testing market profiled in this report are

- GE Healthcare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Illumina, Inc. (U.S.)

- Thermo Fisher Scientific, Inc. (U.S.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Pacific Biosciences of California, Inc. (U.S.)

- PerkinElmer, Inc. (U.S.)

- QIAGEN N.V. (Germany)

- Agilent Technologies, Inc. (U.S.)

- Beijing Genomics Institute (China)

TOP LEADING PLAYERS IN THE MARKET

- Roche Diagnostics is a global leader in molecular diagnostics and a pivotal contributor to the advancement of non-invasive prenatal testing in Europe. The company offers its Harmony Prenatal Test through a network of certified laboratories and maintains strong partnerships with public health systems in countries like the UK and Switzerland. Roche actively supports clinical validation studies and provides comprehensive educational resources for healthcare professionals on test interpretation and ethical considerations. Roche also collaborates with European regulatory bodies to align its offerings with evolving in vitro diagnostic regulations, ensuring sustained compliance and trust across diverse national frameworks.

- Illumina Inc. plays a foundational role in the European Non-Invasive Prenatal Testing Market by supplying next-generation sequencing platforms and bioinformatics solutions that power the majority of high-throughput NIPT services. Although it does not offer a branded test directly to consumers, Illumina’s sequencing instruments and VeriSeq NIPT software are integral to accredited laboratories in the Netherlands, Germany, and Sweden. The company invests heavily in analytical validation and data standardization to support regulatory submissions across the EU. It also partnered with European university hospitals to establish training programs on genomic data interpretation, reinforcing its position as an enabling technology provider in Europe’s precision prenatal care ecosystem.

- Natera Inc. has established a significant footprint in the European Non-Invasive Prenatal Testing Market through its Panorama test, which utilizes single-nucleotide polymorphism-based technology to distinguish maternal from fetal DNA and detect conditions like triploidy and vanishing twins. The company works with a network of distributors and reference laboratories across France, Spain, and the Nordic countries to facilitate sample processing and reporting. Natera emphasizes clinical differentiation through expanded screening panels and proprietary algorithms. The company also launched a digital physician portal in Germany to streamline test ordering and result delivery, strengthening integration into European clinical workflows.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European Non-Invasive Prenatal Testing Market focus on regulatory compliance and CE IVD certification to ensure product legality under the EU In Vitro Diagnostic Regulation. They invest in clinical validation studies with European institutions to demonstrate performance in local populations and support national reimbursement applications. Companies expand laboratory networks or partner with accredited local labs to reduce turnaround time and comply with data sovereignty requirements under the General Data Protection Regulation. Strategic emphasis is placed on healthcare professional education through workshops and digital platforms to improve test ordering accuracy and result interpretation. Additionally, firms differentiate offerings through expanded screening panels, proprietary bioinformatics, and integration with electronic health records, enhancing clinical utility while adhering to ethical guidelines on permissible reporting.

MARKET SEGMENTATION

This research report on the europe non-invasive prenatal testing market has been segmented and sub-segmented into the following categories.

By Instruments

- Ultrasound

- NGS

- PCR

- Microarray

By Method

- FCMB

- Cf-DNA

By Application

- Trisomy

- Microdeletion

- Genetics and Rh Factor

By End User

- Hospitals

- Diagnostic Labs

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic and the Rest of Europe

Frequently Asked Questions

1. What drives growth in the Europe Non-Invasive Prenatal Testing Market?

Key drivers include advanced genomic technologies, increasing late pregnancies (over 33 years), high Down syndrome incidence, and reimbursement expansions in countries like Germany and the UK, boosting accessibility and adoption across the Europe Non-Invasive Prenatal Testing Market.

2. Which countries lead the Europe Non-Invasive Prenatal Testing Market?

Germany holds the largest share in the Europe Non-Invasive Prenatal Testing Market due to high uptake over 50%, followed by the UK, France, and Italy, supported by favorable regulations and healthcare infrastructure promoting NIPT integration.

3. Who are the major players in the Europe Non-Invasive Prenatal Testing Market?

Leading companies in the Europe Non-Invasive Prenatal Testing Market include F. Hoffmann-La Roche, Eurofins Scientific, Centogene, and Yourgene Health, focusing on product launches, partnerships, and NGS advancements to capture market share.

4. How does regulation impact the Europe Non-Invasive Prenatal Testing Market?

Strict regulations in the Europe Non-Invasive Prenatal Testing Market ensure test accuracy but slow innovation; liberal policies in France and Germany for aneuploidy screening drive growth, while challenges persist in standardization across EU countries.

5. What technologies dominate the Europe Non-Invasive Prenatal Testing Market?

NGS and cell-free DNA analysis lead the Europe Non-Invasive Prenatal Testing Market, with NIFTY tests prominent for high accuracy in detecting trisomies; machine learning enhancements further improve personalized risk assessments.

6. What challenges face the Europe Non-Invasive Prenatal Testing Market?

High costs, reimbursement variations, and ethical concerns over expanded screening slow the Europe Non-Invasive Prenatal Testing Market, though medical tourism and cross-border access in nations like Spain aid expansion.

7. What is NIPT's accuracy in the Europe Non-Invasive Prenatal Testing Market?

NIPT offers over 99% accuracy for trisomy 21 in the Europe Non-Invasive Prenatal Testing Market, outperforming traditional screening and minimizing miscarriage risks associated with invasive diagnostics.

8. When is NIPT performed in the Europe Non-Invasive Prenatal Testing Market context?

Typically from week 10 in the Europe Non-Invasive Prenatal Testing Market, NIPT analyzes maternal blood for fetal DNA, ideal post-first trimester combined screening in high-risk cases across Europe.

9. What does NIPT screen for in the Europe Non-Invasive Prenatal Testing Market?

In the Europe Non-Invasive Prenatal Testing Market, NIPT screens for trisomies 21, 18, 13, sex chromosome issues, and microdeletions, with expanding panels gaining validation for broader chromosomal abnormalities.

10. Is NIPT reimbursable in the Europe Non-Invasive Prenatal Testing Market?

Reimbursement varies; Germany and UK offer broad coverage in the Europe Non-Invasive Prenatal Testing Market for high-risk women, while France limits to trisomy 21, influencing uptake rates continent-wide.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com