Europe Laboratory Centrifuge Market Research Report By Product, Rotor Design, Intended Use, Application, End User & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) - Industry Analysis Size, Share, Growth, Trends & Forecast 2025 to 2033

Europe Laboratory Centrifuge Market Report Summary

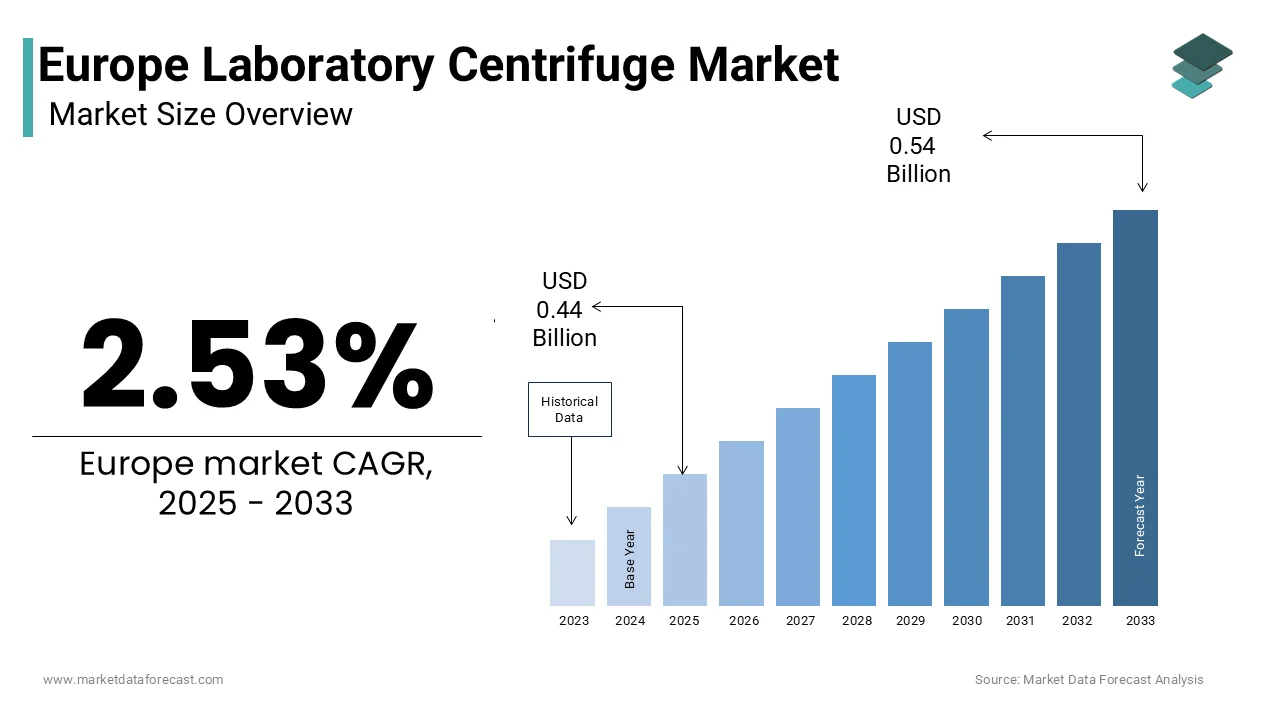

The Europe Laboratory Centrifuge Market was valued at USD 0.43 billion in 2024, is expected to grow at a CAGR of 2.53% from 2025 to 2033, and is projected to reach USD 0.54 billion by 2033, up from USD 0.44 billion in 2025. Market growth is primarily driven by the rising demand for advanced laboratory equipment, increasing adoption of centrifugation in clinical diagnostics, and expanding applications in biotechnology and pharmaceutical research. Additionally, growing investments in precision medicine, biobanking, and academic life science research across Europe are accelerating centrifuge technology adoption. The integration of automated and high-speed centrifuges and enhanced rotor designs continues to improve operational efficiency and reliability in laboratory workflows.

Key Market Trends

- Technological Advancements in Centrifuges: The Development of high-speed and ultra-centrifuge systems with automated imbalance detection and digital monitoring features is enhancing accuracy and productivity.

- Rising Clinical Diagnostic Demand: Increased need for blood separation, plasma analysis, and biomarker testing is expanding centrifuge usage in clinical laboratories and hospitals.

- Growth of Precision Medicine and Biobanking: National initiatives promoting personalized healthcare and genetic research are creating strong demand for advanced centrifugation systems.

- Automation and Safety Enhancements: Integration of touchscreen interfaces, programmable controls, and automated lid-lock systems is improving laboratory workflow safety and efficiency.

- Sustainability in Laboratory Equipment: Manufacturers are focusing on energy-efficient centrifuges and eco-friendly materials to align with Europe’s environmental and regulatory goals.

- Expanding Use in Academic and Pharmaceutical Research: Research institutes and pharma companies are increasing the use of centrifuges for DNA/RNA extraction, cell separation, and sample purification.

Segmental Analysis

By Product Insights

- The equipment segment held a dominant position in the European laboratory centrifuge market in 2024.

- The segment’s leadership is driven by high replacement rates, technological advancements, and rising adoption of benchtop and floor-standing centrifuges in research and diagnostic laboratories.

- Increasing demand for automated centrifuge systems and user-friendly interfaces is further supporting market growth.

By Rotor Design Insights

- The fixed-angle rotor segment accounted for 54.3% of the European laboratory centrifuge market share in 2024, emerging as the leading category.

- Fixed-angle rotors are preferred due to their high-speed capability, compact design, and efficient sedimentation performance in molecular biology and clinical applications.

- Growing use in microbiology, cell culture, and pharmaceutical testing laboratories continues to boost this segment’s adoption.

By Intended Use Insights

- The clinical centrifuges segment held a prominent share of the European laboratory centrifuge market in 2024.

- Widespread use of centrifuges in diagnostic testing, hematology, and biochemical analysis has reinforced the dominance of this segment.

- The trend toward point-of-care diagnostics and integrated laboratory automation further enhances clinical centrifuge utilization.

By End User Insights

- The hospital segment held the second-largest share at 48.3% of the European laboratory centrifuge market in 2024.

- Hospitals are increasingly adopting centrifugation technologies for blood separation, plasma collection, and genetic testing, particularly in emergency and specialized departments.

- The shift toward centralized testing facilities and hospital laboratory automation is supporting steady growth in this segment.

Regional Analysis

- Germany led the European laboratory centrifuge market in 2024, accounting for a 28.3% share. The country’s dominance is supported by advanced laboratory infrastructure, strong biotechnology and pharmaceutical sectors, and heavy investment in medical diagnostics. Germany’s commitment to precision medicine research and automation in clinical labs continues to drive equipment demand.

- The United Kingdom held 17.3% of the market share in 2024, propelled by growth in biopharmaceutical manufacturing, academic collaborations, and public health laboratory modernization initiatives. The increasing focus on molecular diagnostics and cell-based research supports ongoing market expansion in the UK.

- France is witnessing robust growth, driven by its centralized public health system and strategic investments in genomic medicine and precision healthcare. Government-backed initiatives in medical research and biotechnology innovation are fostering the adoption of next-generation centrifugation systems.

Competitive Landscape

The Europe Laboratory Centrifuge Market is moderately consolidated, with leading global manufacturers competing through product innovation, automation integration, and regional distribution expansion.

Companies are focusing on developing energy-efficient centrifuges, enhanced rotor systems, and AI-enabled maintenance diagnostics to improve laboratory performance. Strategic collaborations with research institutions and clinical networks are further strengthening product adoption and brand visibility. Some of the companies that are playing a dominating role in the global Europe Laboratory Centrifuge Market include Thermo Fisher Scientific, Inc., QIAGEN, Becton, Dickinson and Company, Danaher Corporation, Bio-Rad Laboratories, Inc., Agilent Technologies, Inc., Sigma Laborzentrifugen GmbH, Neuation, Hitachi Koki Co., Ltd., and Harvard Bioscience, Inc.

Europe Laboratory Centrifuge Market Size

The europe laboratory centrifuge market size was valued at USD 0.43 billion in 2024, is expected to have a 2.53% CAGR from 2025 to 2033, and be worth USD 0.54 billion by 2033 from USD 0.44 billion in 2025.

The laboratory centrifuge comprises precision-engineered instruments used to separate components of biological, chemical, and clinical samples based on density through high-speed rotational force. These devices are indispensable in diagnostic, biopharmaceutical, research, and academic laboratories and public health institutions across the continent. Furthermore, more than 2800 public and private research institutions in Europe conduct life science experiments annually, necessitating reliable separation technologies.

MARKET DRIVERS

Expansion of Genomic and Precision Medicine Research Fuels Demand for High-Performance Centrifuges

The acceleration of genomic sequencing and personalized therapeutic development has significantly increased reliance on high-speed and ultracentrifuges for nucleic acid and organelle isolation, which is propelling the growth of the European laboratory centrifuge market. As per the European Society of Human Genetics, over 150large-scalee genomic initiatives were active in EU member states in 2024, including national programs in the UK, France, and Germany, aiming to sequence more than 1 million patient genomes by 2028. These efforts require ultra-pure DNA and RNA extraction, where differential centrifugation remains a critical upstream step. For instance, isolating exosomes ' key biomarkers in liquid biopsy requires ultracentrifugation at 100000 g or higher, a capability only advanced models provide. Additionally, the European Organisation for Research and Treatment of Cancer reports that over 70% of clinical trials for targeted oncology therapies in 2024 incorporated centrifugation-based sample preparation for circulating tumor cell analysis.

Strengthening of EU Regulatory Frameworks for In Vitro Diagnostics Elevates Equipment Standards

The implementation of the In Vitro Diagnostic Regulation (IVDR) 2017/746 has fundamentally reshaped laboratory equipment requirements across Europe by imposing stricter performance and traceability mandates. This factor is likely to leverage the growth of the European laboratory centrifuge market. As per the European Commission, the IVDR transition deadline of May 2022 extended full enforcement to 2028, with over 80 % of diagnostic manufacturers now required to validate every step of sample processing, including centrifugation parameters. This regulatory shift compels clinical labs to upgrade from legacy centrifuges to models with digital audit trails, rotor identification sensors, and temperature logging capabilities to ensure compliance. Moreover, under the EU’s Good Laboratory Practice directive, centrifuge calibration records must now be retained for a minimum of 10 years, necessitating integration with laboratory information management systems. These compliance imperatives are accelerating the retirement of analog devices and stimulating demand for smart centrifuges that automatically document run conditions, speed, duration, and temperature by transforming a once passive instrument into an active component of quality assurance ecosystems.

MARKET RESTRAINTS

High Acquisition and Maintenance Costs Limit Adoption in Smaller and Publicly Funded Laboratories

The significant capital outlay and operational complexity of advanced centrifuges constrain accessibility for smaller diagnostic centers and publicly funded institutions is hampering the growth of the European laboratory centrifuge market. Annual maintenance contracts further add 8 to 12 % of the purchase price, creating a recurring financial burden. Furthermore, specialized rotors and biosafety-certified accessories often carry lead times of 8 to 12 weeks and require trained personnel for installation and validation. This cost barrier not only delays technological adoption but also creates disparities in diagnostic accuracy and research reproducibility between well-funded and resource-limited institutions.

Supply Chain Volatility for Precision Components Disrupts Equipment Availability

The persistent disruptions due to dependencies on global supply chains for high-precision mechanical and electronic components are another attribute hampering the growth of the European laboratory centrifuge market. Critical parts such as brushless motors, vacuum-sealed rotors, and microprocessor-based control boards are predominantly sourced from specialized manufacturers in Asia and North America. The war in Ukraine further exacerbated shortages of rare earth magnets used in high torque motors, which are essential for ultracentrifuge stability. Consequently, manufacturers like Eppendorf and Thermo Fisher have reported production slowdowns and selective order prioritization. These constraints delay laboratory expansions and force institutions to postpone critical upgrades, particularly in emerging fields like extracellular vesicle research that require timely access to tnext-generationon equipment.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and IoT Enables Predictive Diagnostics Workflows

The integration of laboratory centrifuges with artificial intelligence and Internet of Things technologies is substantially to create new opportunities for the growth of the European laboratory centrifuge market. Modern centrifuges now embed sensors that monitor vibration, temperature, rotor imbalance, and usage patterns in real time, transmitting data to cloud platforms for predictive maintenance and quality control. These intelligent systems can auto-adjust spin parameters based on sample viscosity or flag deviations that may compromise downstream analysis, such as PCR or mass spectrometry. The European Institute of Innovation and Technology has funded three pilot projects linking centrifuge data streams to digital twin models of diagnostic workflow, enabling real-time protocol optimization. Furthermore, integration with laboratory information systems allows automatic annotation of centrifugation metadata in electronic lab notebooks, enhancing reproducibility with a key priority under the EU’s Open Science agenda.

Rising Incidence of Chronic and Infectious Diseases Drives Diagnostic Infrastructure Investment

The growing burden of non-communicable and re-emerging infectious diseases across Europe is prompting public and private investment in diagnostic laboratory capacity, including centrifugation systems. This factor is likely to create new opportunities for the growth othe f the European laboratory centrifuge market. According to the World Health Organization, Europe's cardiovascular diseases account for 1.8 million deaths annually, while diabetes affects over 61 million adults in the region. Both conditions require routine serum and plasma separation for biomarker testing, such as troponin or HbA1c,1c which depend on reliable centrifugation. In response, the EU’s HERA Incubator has allocated 120 million euros to strengthen national reference laboratories with modern sample processing equipment. Countries like Poland and Romania are upgrading regional hospital labs under the EU4Health program am specifically targeting centrifuge replacements to meet ISO 15189 accreditation standards.

MARKET CHALLENGES

Shortage of Skilled Laboratory Personnel Hinders Optimal Equipment Utilization

The effective deployment of advanced centrifuges is increasingly limited by a critical shortage of trained laboratory professionals. Therefore, the shortage of skilled laboratory personnel is a huge challenge for the growth of the European laboratory centrifuge market. According to the European Federation of Clinical Chemistry and Laboratory Medicine, an estimated 25000 medical laboratory scientist positions remained unfilled across the EU in 2024 due to aging workforces and insufficient vocational training pipelines. Complex centrifuges with programmable protocols, rotor recognition, and biosafety interlocks require certified training for safe and accurate operation. Misuse can result in rotor failure, sample contamination, or data invalidation outcomes that compromise both patient care and research integrity.

Fragmented Reimbursement and Procurement Policies Across Member States

The lack of harmonized healthcare procurement and reimbursement mechanisms across European countries creates inconsistent demand signals and delays equipment modernization. This attribute is additionally used to limit the growth of the European laboratory centrifuge market. While Germany and the Netherlands maintain centralized frameworks for laboratory technology assessment, France and Italy delegate purchasing decisions to individual hospitals, often with rigid budget cycles. Moreover, reimbursement codes for diagnostic tests rarely account for the underlying equipment cost, incentivizing labs to extend the life of outdated centrifuges rather than invest in higher-performance models. The European Commission’s Joint Procurement Agreement for in vitro diagnostics covers reagents but not instrumentation, leaving centrifuges excluded from bulk purchasing benefits. This policy fragmentation not only increases the total cost of ownership but also impedes the adoption of innovative features such as reduced aerosol generation or energy-efficient operation that could enhance biosafety and sustainability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product, Rotor Design, Intended Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Thermo Fisher Scientific, Inc., QIAGEN, Becton, Dickinson and Company, Danaher Corporation, Bio-Rad Laboratories, Inc., Agilent Technologies, Inc., Sigma Laborzentrifugen GmbH, Neuation, Hitachi Koki Co., Ltd., Harvard Bioscience, Inc. |

SEGMENTAL ANALYSIS

By Product Insights

The equipment segment accounted in holding a dominant share of the European laboratory centrifuge market in 2024. Public and private institutions across Europe are actively replacing aging centrifugation systems to meet evolving regulatory and operational standards. The In Vitro Diagnostic Regulation mandates traceable and temperature-controlled sample processing, which legacy analog models cannot support. Consequently, hospitals and reference labs are procuring new benchtop and high-speed centrifuges equipped with digital logging and rotor identification. These regulatory and quality imperatives ensure sustained demand for primary equipment over ancillary components.

The accessories segment is projected to witness a CAGR of 9.6% from 2025 to 2033. Emerging research in extracellular vesicles, viral vector purification, and single-cell isolation requires application-specific rotors that optimize separation efficiency and sample integrity. For instance, fixed-angle rotors with k factors below 50 are essential for rapid pelleting in gene therapy workflows. Manufacturers now offer sealed rotors, biocontainment lids, and anaerosol-proof buckets to meet EN 61010 safety standards. The European Medicines Agency mandates that all advanced therapy medicinal product facilities use validated containment accessories during centrifugation, with a rule driving accessory replacement even when the base unit remains functional.

By Rotor Design Insights

The fixed-angle rotor segment held 54.3% of the European laboratory centrifuge market share in 2024. Fixed-angle rotors position tubes at 25 to 45 degrees, enabling faster sedimentation by reducing the distance particles travel during centrifugation. According to the European Society of Laboratory Medicine, a standard blood separation that takes 15 minutes in a swinging bucket rotor requires only 8 to 10 minutes in a fixed-angle configuration. Fixed-angle rotors also generate denser, more compact pellets, reducing resuspension errors in DNA extraction and immunoassays. Their robust metal construction supports higher g forces, making them ideal for high-speed applications in virology and protein purification.

The vertical rotors segment is likely to register the fastest CAGR of 12.3% throughout the forecast period. Vertical rotors orient tubes horizontally during operation, minimizing path length and enabling rapid equilibrium in density gradient centrifugation. This is indispensable for separating subcellular organelles, lipoproteins, and viral particles, where resolution is paramount. The rise of lipid nanoparticle-based therapeutics has further amplified demand, as quality control requires precise separation of empty and filled nanoparticles with a task where vertical rotors outperform alternatives by reducing run time from 16 to 4 hours.

By Intended Use Insights

The clinical centrifuges segment accounted in holding a prominent share of the European laboratory centrifuge market in 2024. Clinical centrifuges are essential for separating serum, plasma, and cellular components in over 70% of all in vitro diagnostic tests. These instruments are standardized for 4 15-minute runs at 1500 to 4000 rpm, making them ideal for high-volume hospital labs. The In Vitro Diagnostic Regulation requires that all IVD tests maintain sample integrity from collection to analysis, and clinical centrifuges with temperature control and timed braking are mandated for hormone coagulation and infectious disease panels.

The preparative ultracentrifuges segment is anticipated to grow with a CAGR of 11.8% during the forecast period. Preparative ultracentrifuges operating above 100000 g are indispensable for purifying adenoviruses, lentiviruses,,l and AAV vectors used in gene therapies. These systems enable large-scale pelleting or gradient separation of viral particles with high recovery rates essential for commercial viability. The rise of mRNA vaccines has further increased demand as lipid nanoparticle purification relies on density gradient ultracentrifugation to remove impurities. BioNTech’s facilities in Germany use preparative ultracentrifuges to support GMP-compliant production, validating their industrial relevance.

By End User Insights

hospital segment was positioned second in the European laboratory centrifuge market with 48.3% of share in 2024. Hospitals process the vast majority of clinical specimens in Europe, with over 6000 acute care facilities performing daily hematology, chemistry, and microbiology testing. Each European hospital averages 1.2 million laboratory tests annually, necessitating multiple clinical centrifuges per site. Emergency departments rely on rapid centrifugation for troponin lactate and blood gas analysis, where results must be delivered within 30 minutes. The European Society of Emergency Medicine mandates that all level 1 trauma centers maintain at least two dedicated centrifuges to avoid bottlenecks. This operational indispensability ensures consistent procurement and replacement cycles across public and private hospitals.

The biotechend-user segment is expected to witness the fastest CAGR of 13.2% throughout the forecast period. These agile companies require flexible centrifugation solutions for R&D and small-scale GMP production. Preparative ultracentrifuges and high-speed models are critical for plasmid purification, viral vector concentration, and exosome isolation. The United Kingdom alone added 210 biotech startups in 2,024, many co-located in innovation hubs like the Francis Crick Institute that provide shared centrifugation infrastructure. This ecosystem accelerates technology transfer and instrument adoption.

COUNTRY LEVEL ANALYSIS

Germany Laboratory Centrifuge Market Analysis

Germany was the top performer of the European laboratory centrifuge market with a 28.3% share in 2024, with its dense network of clinical laboratories, pharmaceutical headquarters, and public research institutions. Germany’s strong biotech corridor from Munich to Berlin hosts firms like CureVac and BioNTech that rely on ultracentrifuges for mRNA and viral vector production. Additionally, the German Accreditation Body enforces strict compliance with DIN EN ISO 15189, mandating regular equipment validation, which drives consistent replacement demand.

United Kingdom Laboratory Centrifuge Market Analysis

The United Kingdom laboratory centrifuge market held 17.3%the share in 2024, with its world-class academic medical centers and thriving biotech ecosystem. Simultaneously, the UK is home to Europe’s highest concentration of cell and gene therapy companies with over 150 active in 2024. Institutions like the Francis Crick Institute and Oxford Biomedica utilize preparative ultracentrifuges for viral vector purification under MHRA regulatory oversight.

France Laboratory Centrifuge Market Analysis

The French laboratory centrifuge market growth is driven by the centralized public health system and strategic investments in precision medicine. The French National Public Health Agency oversees 1800 hospital laboratories that follow standardized equipment protocols issued by the Haute Autorité de Santé. France’s Genomic Medicine Plan 2025 aims to sequence 230000 genomes annually,, high-throughput centrifugation for DNA extraction. The Pasteur Institute network and biotech clusters in Lyon and Paris utilize advanced centrifuges for infectious disease research, including tuberculosis and dengue diagnostics.

COMPETITIVE LANDSCAPE

The European laboratory centrifuge market features a mix of global instrumentation giants and specialized European manufacturers competing on precision, regulatory alignment, and service responsiveness. Thermo Fisher, Eppendorf, and Beckman Coulter lead in technological innovation, while regional players like Hettich and Sigma Laborzentrifugen maintain strongholds in niche academic and clinical segments. Competition is less price-driven and more focused on compliance with EU regulations, such as IVDR, ISO 15189, and Machinery Directive safety requirements. Differentiation arises through rotor versatility, noise reduction, energy efficiency, and digital features like remote diagnostics and usage analytics. The market is moderately consolidated with established brands benefiting from brand trust, extensive service network, works an,d integration capabilities with broader laboratory workflows. However, rising demand from biotech startups and upgraded public labs is creating openings for agile entrants offering modular application-specific solutions.

KEY MARKET PLAYERS

Promising Companies dominating the europe laboratory centrifuge market profiled are

- Thermo Fisher Scientific, Inc.

- QIAGEN, Becton

- Dickinson and Company

- Danaher Corporation

- Bio-Rad Laboratories, Inc.

- Agilent Technologies, Inc.

- Sigma Laborzentrifugen GmbH

- Neuation

- Hitachi Koki Co., Ltd.

- Harvard Bioscience, Inc.

TOP LEADING PLAYERS IN THE MARKET

- Thermo Fisher Scientific is a global leader in laboratory instrumentation with a significant presence in the European laboratory centrifuge market. The company offers a comprehensive portfolio including high-speed microcentrifuges and ultracentrifuges designed for clinical diagnostics, biopharmaceutical research, and academic applications. Its Sorvall and Heraeus brands are widely recognized for reliability and innovation. The company launched a new generation of refrigerated benchtop centrifuges with touchscreen interfaces and cloud connectivity to support IVDR compliance and digital lab workflows, strengthening its position in regulated European environments.

- Eppendorf AG, headquartered in Germany, is a key European manufacturer specializing in precision laboratory equipment, including centrifuges for life science and clinical use. The company’s Microcentrifuge 5430 and Centrifuge 5910 R models are widely adopted in academic and hospital labs for their ergonomic design, quiet operation,n, and biosafety features. The company partnered with major university hospitals in France and Sweden to co-develop centrifugation protocols for extracellular vesicle isolation, supporting emerging diagnostic research and reinforcing its role as a solutions provider beyond hardware supply.

- Danaher’s Beckman Coulter Life Sciences division is a major contributor to the European laboratory centrifuge market with a focus on high-performance ultracentrifuges and preparative systems for biopharma and advanced research. Its Optima series is integral to viral vector and mRNA vaccine development across European biotech hubs. The company also integrated its centrifuges with laboratory data management platforms to meet the European Medicines Agency’s requirements for data integrity in GMP environments, thereby strengthening its foothold in regulated therapeutic development sectors.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European laboratory centrifuge market prioritize regulatory compliance by embedding digital audit trails, rotor usage tracking, and temperature monitoring to align with IVDR and ISO standards. They invest heavily in application-specific product development, such as rotors for exosome isolation or viral purification, to serve emerging biotech needs. Companies expand service and training networks across Eastern and Southern Europe to reduce downtime and build user competency. Strategic collaborations with academic hospitals and reference labs enable co-creation of validated protocols that enhance product adoption. Additionally, firms integrate centrifuges into digital laboratory ecosystems through cloud connectivity and LIMS compatibility to support Europe’s shift toward smart and automated diagnostics infrastructure.

MARKET SEGMENTATION

This research report on the European laboratory centrifuge market has been segmented and sub-segmented into the following categories.

By Product

- Equipment

- Microcentrifuge

- Ultracentrifuge

- Accessories

By Rotor Design

- Swinging Bucket Rotors

- Fixed Angle Rotors

- Vertical Rotors

By Intended Use

- General-purpose Centrifuges

- Clinical Centrifuges

- Preclinical Centrifuges

- Preparative Ultracentrifuges

By Application

- Diagnostic

- Microbiology

- Proteomics

- Genomics

By End User

- Hospital

- Biotech

- Pharmaceutical

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving the growth of the Europe Laboratory Centrifuge Market?

Growth is driven by increased research activities in life sciences, biotechnology, adoption of automated diagnostic techniques, and rising healthcare investment in the region.

2. Which types of centrifuges are most demanded in the Europe Laboratory Centrifuge Market?

Microcentrifuges, ultracentrifuges, multi-purpose centrifuges, and benchtop centrifuges are highly demanded for clinical, diagnostic, and research applications in Europe.

3. How does technological advancement impact the Europe Laboratory Centrifuge Market?

Technological advances such as digital interfaces, rotor recognition, and cold-chain compatibility enhance product performance, expanding the Europe Laboratory Centrifuge Market.

4. What challenges does the Europe Laboratory Centrifuge Market face?

High equipment and maintenance costs, potential mechanical failure, and concerns about toxic aerosol emissions restrict market growth.

5. What are the key applications of centrifuges in the Europe Laboratory Centrifuge Market?

Applications include molecular diagnostics, hematology, blood component separation, proteomics, genomics, and microbiology.

6. Who are the major end users in the Europe Laboratory Centrifuge Market?

Hospitals, clinical laboratories, biotechnology and pharmaceutical companies, and academic research institutes are main end users.

7. Which countries dominate the Europe Laboratory Centrifuge Market?

Germany, the UK, France, and Italy hold significant shares due to strong biopharmaceutical industries and high research investments.

8. How is the regulatory environment influencing the Europe Laboratory Centrifuge Market?

Regulatory bodies like EMA and MHRA ensure equipment compliance with biosafety and quality standards, creating stable conditions for market growth.

9. What role does research and development play in the Europe Laboratory Centrifuge Market?

R&D investments promote product innovation and increase demand for advanced centrifuge systems in Europe’s life sciences sectors.

10. How is the demand for laboratory centrifuges expected to evolve in Europe?

The European Laboratory Centrifuge Market is expected to grow steadily due to rising infectious diseases prevalence and growing healthcare infrastructure.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com