Europe Nuts Market Size, Share, Trends & Growth Forecast Report By Mode Type, Product Type, and By Country (Germany, United Kingdom, France, Spain, Italy & Rest of Europe) – Industry Analysis and Forecast, 2025 to 2033

Europe Nuts Market Summary

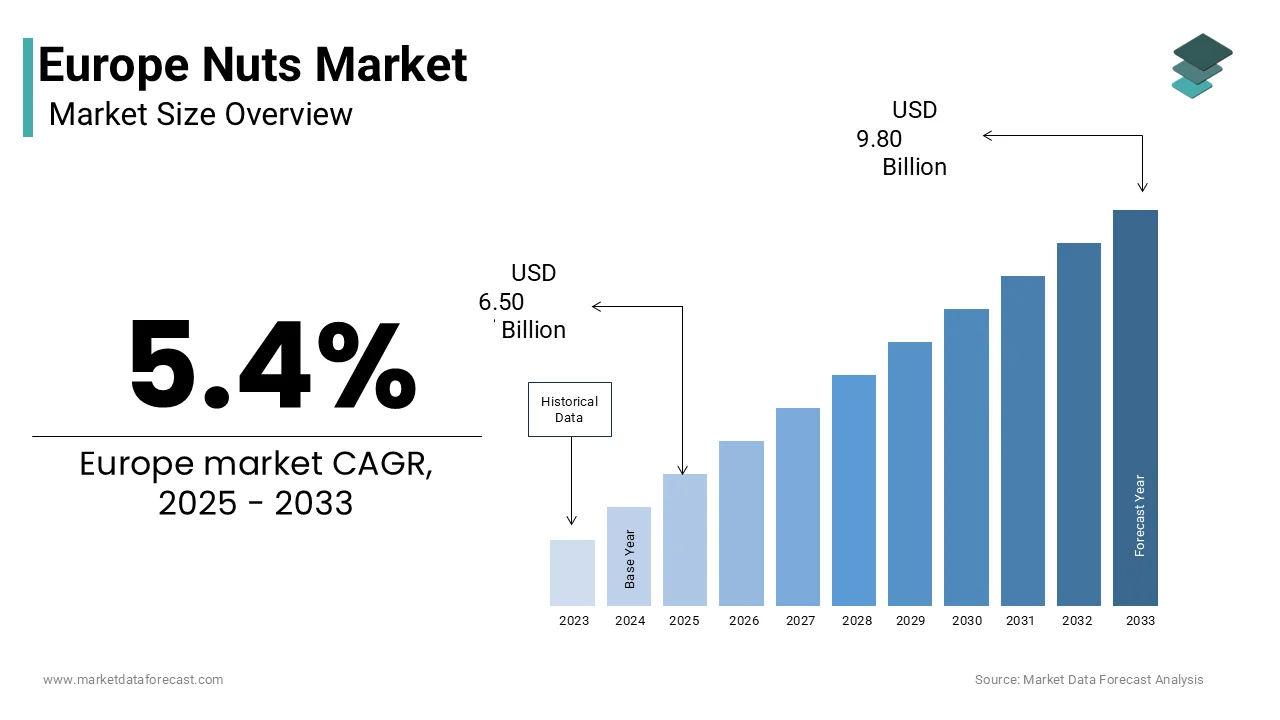

The Europe nuts market was valued at USD 6.17 billion in 2024, is estimated to reach USD 6.50 billion in 2025, and is projected to reach USD 9.80 billion by 2033, growing at a CAGR of 5.4% during the forecast period, driven by rising health consciousness, expanding plant-based food formulations, premium snacking trends, and increasing incorporation of nuts into functional and clinical nutrition across Europe.

Market Highlights

- 2024 value: USD 6.17 billion

- 2025 (est): USD 6.50 billion

- 2033 (forecast): USD 9.80 billion

- CAGR (2025–2033): 5.4%

Quick growth drivers

- Rising integration of nuts into plant-based dairy alternatives, protein bars, and functional foods.

- Increasing consumer preference for premium, nutrient-dense snacking and on-the-go nutrition.

- Formal recognition of nut consumption benefits by European food safety and public health authorities.

- Strong demand from bakery, confectionery, and foodservice sectors across Western Europe.

- Expanding retail shelf space for organic, flavored, and portion-controlled nut products.

Principal restraints

- Stringent EU food safety and allergen labeling regulations increasing compliance costs.

- High exposure to climate-induced supply volatility due to reliance on imported almonds and hazelnuts.

- Price sensitivity among value-focused consumers during periods of raw material inflation.

High-value opportunities

- Expansion of certified organic and regenerative nut sourcing partnerships aligned with EU sustainability goals.

- Growing use of nut-derived proteins and lipids in clinical, elderly, and sports nutrition formulations.

- Direct-to-consumer and subscription-based models enabling premiumization and personalization.

- Development of traceable, deforestation-free nut supply chains under EU regulatory frameworks.

Key operational challenges

- Persistent labor shortages in southern European nut-producing regions limiting domestic output.

- Rising costs and performance trade-offs associated with sustainable packaging compliance.

- Managing allergen cross-contamination risks across complex multi-product food manufacturing lines.

Fastest-growing segments

- Online distribution: 11.4% CAGR driven by e-grocery adoption and curated wellness assortments.

- Walnuts: 9.7% CAGR supported by cardiovascular and cognitive health positioning.

- Functional nut ingredients: accelerated uptake in clinical and fortified nutrition products.

Regional leadership & dynamics

- Germany: Market leader supported by health-conscious consumers, strong organic retail penetration, and bakery demand.

- United Kingdom: High growth fueled by plant-based diets, premium snacking culture, and e-commerce adoption.

- France: Strong demand driven by gastronomic tradition, PGI-certified nuts, and preventive health policies.

- Spain & Italy: Strategic importance as key EU nut producers and major confectionery hubs.

What wins commercially

- Secure, diversified sourcing with traceability and sustainability certification.

- Premium positioning through health claims, clean labels, and functional benefits.

- Strong offline retail presence combined with fast-growing digital channels.

- Compliance excellence in allergen management and EU food safety regulations.

Top strategic ask for executives

- Invest in long-term sustainable sourcing agreements to mitigate climate and price volatility.

- Expand functional and clinical nutrition portfolios using nut-derived proteins and lipids.

- Optimize packaging innovation to balance shelf life, sustainability, and cost efficiency.

- Leverage digital channels and data transparency to drive premiumization and consumer trust.

Leading players

Intersnack Group · Ferrero · Olam International · Kerry Group · John B. Sanfilippo & Son · The Wonderful Company

Europe Nuts Market Size

The europe nuts market was valued at USD 6.17 billion in 2024, is estimated to reach USD 6.50 billion in 2025, and is projected to reach USD 9.80 billion by 2033, growing at a CAGR of 5.4% during the forecast period.

Nuts serve as essential components in both direct human consumption and processed food applications, ranging from bakery confectionery to plant-based dairy alternatives. Europe’s position as a major nut consumer is underpinned by evolving dietary patterns, health consciousness,, ss and the integration of nuts into mainstream culinary traditions. According to Eplant-based average per-capita consumption of nuts in the European Union reached 2.1 kilograms in 2023, reflecting a steady upward trajectorydriven by nutritional awareness. The European Food Safety Authority has formally acknowledged the benefits of daily nut intake in reducing cardiovascular disease risk, which has further legitimized their inclusion in public health dietary guidance. This normalization of nuts as a daily dietary staple, combined with strong retail and food service demand, defines the contemporary structure of the European nuts market.

MARKET DRIVERS

Growing Integration of Nuts into Plant-Based and Health-Focused Food Formulations

The a,,ccelerating incorporation of nuts into plant based a, nd functional food products is a major driving factor for the growth of Europe nuts market. As conPlant-BasedeasingHealth-Focusedlabel, high protein and allergen-conscious alternatives to dairy and meat nuts have emerged as foundationalue to their nutritional density and versatile functionality. According to the European Commission, some of the new food and beallergen-conscious the European Union in 2024 featured nuts as a core component, with almond and cashew bases dominating plant-based milk and yogurt categories. Major food manufacturers, such as Nestlé and Oatly, have expanded their nut-based product portfolios with almonds alone featured in over 200 new SKUs launched across Western Europlant-based This ingredient shift is further reinforced by scientific validation, as the World Health Organization in 2023 stated that regular nut consumption correlates with a lower incidence of coronary heart disease among adults.

Rising Consumer Preference for Premium Snacking and On-the-Go Nutrition

Europeans are increasingly substituting traditional processed snacks with nutrient-dense portable alternatives, and nuts have become a cornerstone of this behavioral shift. The rising consumer preference for premium snacking and on thIncreasinglyon is escalating the growth of Europe nuts markenutrient-densen time scarcity and he,ightened health literacy have converged to elevate demand for convenient yet wholesome snacking options. Germany, France, and the Netherlands lead this trend with urban consumers reporting daily or weekly nut c,,onsumption as a midday snack, according to national dietary surveys compiled by the European Food Information Council in 2024. Retailers such as Edeka and Carrefour have responded by dedicating expanded shelf space to portion-controlled roasted and flavored nut varieties, often positioned alongside fitness and wellness products. This alignment with modern nutritional priorities positions nuts as a default choice in the evolving Europeportion-controlledape.

MARKET RESTRAINTS

Stringent Food Safety and Allergen Labeling Regulations

The region’s rigorous allergen control and labeling mandates, which impose operational and financial burdens on producers and retailers alike. The stringent food safety and allergen labelling regulatio ares restricting the growth of Europe nuts market. Tree nuts are classifiedthe 14 major allergens under EU Regulation 1169 2011, requiring explicit declaration on all prepacked and non-prepacked food items. Accord areareto the European Commission, over 90% of food recalls in the European Union related to undeclared allergens in 2023 involved cross-contaminationwith nuts during processing or packaging. Compliance necessitates segregated production lines,s dedicated storage facilities, and extensive staff training with small and medium enterprises that often lcross-contaminationfor such infrastructure. Furthermore, Europeans suffer from tree nut allergies, making regulator,y enforcement both a legaland a, nd public health imperative.

Vulnerability to Climate-Induced Supply Volatility

Europe’s heavy reliance on imported nuts, particularly almonds from California and hazelnuts from Turkey, exposes tit o climate driven supply shocks that disrupt availability and escalateClimate-Inducedlnerability to climate induced supply volatility, also degrading the growth of Europe's nut market. According to the Food an,,d Agricit ulit turclimate-driven of the United Nations, prolonged droughts in California reduced the 2024 almond harvest by 16% compared to the five-year average,e directly impacting European import volumes. Sine, Europe sources its hazelnuts and almonds from these two regions, and climate instability is impeding the growth of the market. The European Commission’s Agricultural Market Observatory documented a year-on-year increase inholesale almond prices in the EU during the first half of 2024, attributable to supply contraction. Such volatility complicates long term procurement planning for food manufacturers and retaileyear-on-yearoding consumer purchasing power, particularly in value-sensitive segments ther, thereby constraining overall market fluidity.

MARKET OPPORTUNITIES

Expansion of Organic and Regenerative Nut Farming Partnerships

The growing alignment between European retailer,s and overseas nvalue-sensitivemmitted to, certified organic and regenerative agricultural practices is creating new opportunities for the growth of Europe's nut market. Consumer demand for traceable, environmentally responsible ingredients has prompted major chains, such as Aldi and Lidl, to establish direct sourcing agreements with farms adhering to EU organic standards. According to IFOAM Organics, Europe certifiedorganic nut imports into the European Union increased in 202,4 with almonds and walnuts leading the category. The European Commission’s Farm to Fork Strategy further incentivizes such partnerships by providing funding for supply chains that demonstrate carbon sequestration, soil health improvement, and biodiversity preservation. These initiatives not only satisfeco-consciousus consumers but also mitigate future regulatory risks as the EU prepares mandatory deforestation-free product regulations. Consequently, s,ustainability driven sourcing is transforming from a niche prefereeco-consciousrategic procurement imperative.

Development of Nut-Based Functional Ingredients for Clinical Nutrition

The rising application of nuts in medical and clinical nutrition is expected to further elevate the growth of Europe nuts market. Innovations in lipid extraction proteNut-Basedion and micronutrient concentration have enabled the formulation of nut-derived ingredients tailored for elderly maexpectedfurther s recovery and metabolic health management. As per the European Society for Clinical Nutrition and Metabolism, specialized nutritional products launched in nut-derivedand pharmacies in 2024 incorporated walnut or almond protein, isolates due to their high arginine and omega-3 content. Clinical studies published by the Karolinska Institute in 2023 demonstrated that daily supplementation with almond-based protein blends improved muscle synthesis rates in adults over 65. In response, omega-3s such as DSM and Kerry Group have developed standardized nut ingredient platforms compatible with fortified beverages almond-basedical foods. This emergence of clinical validation, regulatory support,t and ingredient innovation positions nuts as critical components in Europe’s expanding functional nutrition ecosystem.

MARKET CHALLENGES

Persistent Labor Shortages in Key European Nut Harvesting Regio, ns

The constraining, domestic nut production in Europe relates to acute agricultural labor shortages, particularly in southern regions, where manual harvesting remains essential. The persistent labor shortages in key European nut harvesting are one of the challenges for the growth of Europe nuts market. Countries, such as Spain and Italy, which account for nearly aEU-producedced almonds and hazelnuts, rely heavily on seasonal migrant workers yet face declining availability due to demographic shifts and regulatory barriers. According to Spain’s Ministry of Agriculture, athe lmond orchard experienced delayed or incomplete harvesting in 2024 due to insufficient labor. These bottlenecks not only reduce domestic output butalso increase post-harvest losses and elevate production costs, thereby undermining Europe’s potential for import substitution and supply chain resilience.

Escalating Costs of Sustainable Packaging Compliance

The transition to eco-friendly packaging mandated under the EU Packaging and Packaging Waste Directive is a significant financial and logistical challenge for nut processors and retailers. This factor is attributed in degrading the growth of Europe nuts market. Nuts require barrier protection against moisture and oxygen, yesingle-use plastic formats are being phased out in favor of recyclable or compostable alternatives that often underperform or cost significantly more. According to the European Packaging Federation, the average cost of single-usecompostable nut packaging rose by 37% in 2024 compared to conventional laminates. Moreover, commercially available bioplastics currently meet industrial composting infrastructure requirements in Europe, leading to consumer confusion and contamination in waste streams. These expenditures strain margins,s particularly for small roasters and private label suppliers, rs while failing to guarantee equivalent shelf life. Conseque,,ntly, the packaging transition imposes a dual burden of elevated costs and technical compromise tthere thereby affecting product quality and market competitiveness.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Mode Type, Product Type, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Olam International Ltd (deforestation-free), The Wonderful Company, Intersnack Group GmbH & Co. KG, John B. Sanfilippo & Son, Inc. (Famous Amos, Fisher Nuts), Hormel Foods Corporation, Kerry Group plc, American Pistachio Growers, Setton Farms, Inc., SNC Lavalin (nut processing & supply partners), Bali Nut Company, Alesto (Lidl private-label nut products), Nicholas Food Company, Deutsche See GmbH (nut & seafood divisions), Vitacost (nut & health brands), Trader Joe’s (private-label nuts), Markal Organic Foods, Squirrel Brand Nuts |

SEGMENTAL ANALYSIS

By Mode Type

The offline segment was the largest by holding a dominant share of tEuropeanope nuts market in 2024, which is primarily anchored in consumer preference for tactile product evaluation, bulk purchasing,g and immediate consumption, particularly for fresh roasted and premium varieties. According to Europeanstat, over 82% of European households routinely purchase groceries in physical stores with nuts frequently bought alongs, ide staples due to their shelf-stable nature and snack versatility. Retailers such as Carrefour in France and Edeka in Germany have expanded refrigerated and ambient nut sections featuring regional blends, organic options, and allergen segregatedshelf-sableshelf-stableo meet evolving demand. These behavioral and logistical advantages sustain offline channels as the backbone of European nut distribution despite digital proliferation.

The online distribution segment is likely to witness the fastest CAGR of 11.4% throughout the forecast period, from the emergence of e-grocery adoption,n digital health engagement, and demand for curated specialty products unavailable locally. Ocado and Amazon Fresh reported athe29% year on year increase in nut bundle sales in 2024, among urban professionals seeking keto, paleo, or vegan aligned asso,rtments. The rise of direct-to-consumer brands, such as Joe & Seph’s in the UK and KoRo in Germany, has further fueled growth through subscription models and personalized nutrition kits featu, ring,sinvegan-alignedstachios or activated almonds. Additionally, the European Consumer Organisation noted that online nut bbuyersvalue detailed nutritional dashboards and sustainability certifications more readily accessible on e-commerce platforms. This digital enablement transforms nuts from commodity purchases into experiential wellness choices,s driving disproportionate online penetration.

Product Type Insights

The almonds segment was the largest by capturing 32.1% of the European nuts market share in 2024 with their unparalleled versatility across food manufacturing,tu turningetail, and plant-based nutrition. Their dominance is reinforced by widespread use in dairy alternatives, bakery fillings, coEuropeanonery, and ready-to-eat snacking formats. According to the European Commission, almonds feature, ured i,,n oveplant-based food product launches across the EU in 202,3 making them, the most incorporated nut in innovation pipelines. The European Food Safety Authority’s 2022 scientific opinion, confirming that almond consumption contributes to maintaining normal blood cholesterol levels h, has been instrumental in mainstreaming their health positioning. Additionally, Spain is the EU’s sole commercial almond producer,ducer harvested 330000 metric tons in 2023, as per the Ministry of Agriculture providing region,, al supply stability that enhances commercial confidence.

The walnuts segment is projected to witness the fastest CAGR of 9.7% throughout the forecast period, owing to the mounting scientific validation of their cognitive and cardiovascular benefits. Rich in alpha linolenic acid and polyphenols, walnuts have become focal points in preventive nutrition strategies targeting aging populations. As per the European Society of Cardiology, a 2023 meta-analysis of 14 clinical trials concluded that daily walnut intake reducedLDL cholesterol and improved endothelial function in adults over 50. This evidence has been integrated into national dietary guidelines with France’s Programme National Nutrition Santé explicitly recommending three weekly servings of walnuts for heart health. Furthermore, the International Nut and Dried Fruit Council reported that European walnut imports from the United States and Chile are being increased to meet surging demand.

COUNTRY LEVEL ANALYSIS

Germany Nuts Market Analysis

Germany was the top performer in the European nuts market share in 2024, with strong health consciousness, high disposable income, and a mature organic food sector that prioritizes premium nut products. The country’s robust bakery and confectionery industryEuropeananto global players like Bah,lsen atorck drives consistent industrial demand for haze,lnuts and almonds. Additionally, Germany’s Bio seal certification system has accelerated organic nut sales, as reported by the Federal Ministry of Food and Agriculture. Discount retailers such as Aldi and Lidl have also expanded private label nut ranges featuring Fairtrade and climate-neutral claims, aligning with evolving consumer ethics.

United Kingdom Nuts Market Analysis

The United Kingdom nuts market was ranked second by holding a snacking culture, plant-based diet adoption, and a strong e-commerce culture. A,ccording to the UK Food Standards Agency, nut consumption among adults aged 25 to 45 increased between 2021 and 2024, with almonds and cashews leading due plant-basedse in vegan cheese and protein bars. Furthermore, the UK’s departure from the EU has prompted import diversification with increased sourcing from South Africa and Australia, enhancing supply resilience. Innovators like Graze and Joe & Seph’s have leveraged direct-to-consumer models to introduce exotic blends, such as wasabi cashews and dark chocolate pistachios, capturing premium urban dema,, nd.

France Nuts Market Analysis

France's nuts market growth is likely to grow with direct-to-consumerin gastronomic tradition,n preventive healthcare policies, es and bakery applications. According to FranceAgriMer, the national agricultural board, France's production of walnuts and hazelnuts rose by 16% in 2024, supported by regional specialties su,, ch as Noix de Grenoble and Périgord walnuts, which carry Protected Geographical Indication status. Retailers like Mon, Oprixx have integrated nuts into “Bien Manger” healthy eating zones,s with traceability QR codes detailing origin and carbon footprint. Additionally, France’s artisanal chocolate sector, led by Valrhona and Michel Cluiz, el drives consistent demand for premium hazelnuts and almonds. This unique blend of culinary heritage, age, public health advocacy,cacy, and premiumization ensures France’s enduring relevance.

Spain Nuts Market Analysis

Spain'ss nuts market growth is driven by its status as the only EU producer of commercial-scale almonds and significant domestic consumpti, on. According to Spain’s Ministry of Agriculture, the country harvested 330,000 metric tons of almonds in 2023, making it the world’s second largest producer afcommercial-scaletates. This domestic supply enables stable pricing and strong local brand loyalty, with brands like El Coto and Hacendado dominating retail shelves. Moreover, traditional consumption patterns, such as almonds in turrón and marzipan during the festive season, sustain year-round demand. Recent investmen inn water-efficient irrigation have also enhanced sustainability credentials, attracting EU green procurement contracts. Spain’s dual role as producer and consumer creates aresilieyear-roundinsulated from import volatility.

Italy Nuts Market Analysis

Italy's nut market growth is likely to grow w,, ith its iconic hazelnut-based confectionery industry and growing health-oriented retail segment. According to Coldiretti Italy’sagricultural confederatio the the country produces over 100000 metric tons of hazelnuts annually primarilhazelnut-basedand Lazio supplies iconic brands likehealth-orientedtella and Kinder products. The Italian Ministry of Health’s 2023 dietary guidelines explicitly endorsedaily nut intake for metabolic health, further normalizing consumption.

COMPETITIVE LANDSCAPE

Competition in the European nuts market is characterized by a dual dynamic between global food conglomerates and agile regional specialty brands. Large players leverage scale vertical integration and branded product portfolios to dominate shelf space while smaller organic and direct to consumer brands compete through premiumization, traceability, and innovative forActivach as,acactivae,d or sprouted nuts. Differentiation hinges on sustainability credentials nutritiona, nutritional storytelling, and direct-to-consumer rather than price alone. The market fea,,ture tiers riers in allergen control packaging compliance and supply chain certification, yet remains open to niche entrants via e-commerce channels. Regulatory alignment with EU food safety allergen labeling and deforestation-free sourcing rules is non-negotiable and shapes competitive viability.

KEY MARKET PLAYERS

Some of the companies that aree-commerce dominating role in the europe nuts market include

- Olam International Ltd deforestation-freeers

- The Wonderful Cnon-negotiableA Group

- Intersnack Group GmbH & Co. KG

- John B. Sanfilippo & Son, Inc. (Famous Amos, Fisher Nuts)

- Hormel Foods Corporation)

- Kerry Group plc

- American Pistachio Growers

- Setton Farms, Inc.

- SNC Lavalin (Nut processing & supply partners)

- Bali Nut Company

- Alesto (Lidl brand, nut products)

- Nicholas Food Company

- Deutsche See GmbH (nut & seafood divisions)

- Vitacost (nut & health brands)

- Trader Joe’s (private label nuts)

- Markal Organic Foods

- Squirrel Brand Nuts

TOP LEADING PLAYERS IN THE MARKET

- Intersnack Group is a leading European snack manufacturer with a significant footprint in the nuts segment across Germany, France, the Netherlands, and Scandinavia. The company integrates nuts into a wide portfolio of branded snack products, includingFunny Frischh and Chio, offering roasted salted and flavored nut variants tailored to local taste preferences. Intersnack launched a new line ofof protein-focusedut mixes under its premium brand LEIBNIZ NussEck, targeting FuFunnyrischscious urb, an consumers. The company has also invested in sustainable sourcing by partnering with almond growers in Spain, certified under the protein-focused Board of California’s sustainability protocol. These initiatives reinforce Intersnack’s commitment to nutritional innovation and environmental responsibility, while deepening its retail and food service integration across Europe.

- Ferrero International is a global confectionery leader whose European operations are deeply intertwined with the nuts market primarily through its extensive use of hazelnuts, aalmondss and peanuts in iconic products such as Nutella, Kinder,r and Ferrero Rocher. Headquartered in Luxembourg, the company sources over 25% of the world’s hazelnut supply and maintains long term contracts with growers i,,n Italy, Turkey, and Spain. Ferrero expanded its hazelnut,, sustai,nability program, Ferrero Farming Values t to includeinclu, de regenerative agriculture practices across 80000 hectares in Southern Europe. The company also introduced a new traceability platform allowing European consumers to scan packaging and view origin data.

- Kerry Group is a multinational taste and nutrition company that plays a strategic role in the European nuts market by supplying nut-based ingredients to food manufacturers developing plant-based dairy alternatives, bakery fillings, and functional beverages. Its European innovation centers in Irelan Germanyany, and the Europeanlands focus on clean labelnut-basedein isolates and lipid systems that enhanceplant-based stabilityy. In 2024 K,erry launched N,,utraFusion,, a proprietary almond and walnut protein blend designed for,,c linical and sports nutrition applications approved under the EU Novel Foods Regulation. The company also partnered with major retailers to develop private-label nut butter ranges featuring reduced sugar and no palm oil formulations. Through ingredient science and collaborative product development, Kerry strengthens the technical backbone of Europe’snut-drivenn food innovation.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European nuts market focus on sustainable and traceable sourcing to m,eet stringent EU environmental and deforestation regunut-drivenhey invest heavily in product diversification by launching functional nut blends targeting European heart health and cognitive wellness claims backed by scientific validation. Companies enhance digital transparency through QR code-enabled origin and carbon footprint tracking to build consumer trust. Strategic partnerships with local farmers and cooperatives ensure supply stability while advancing regenerative agriculture practices. Additionacode-enabledioritize clean label clean packaging innovation using recyclable materials and eliminating additives to align with European clean eating trends and regulatory expectations.

MARKET SEGMENTATION

This research report on the europe nuts market is segmented and sub-segmented into the following categories.

By Mode Type

- Offline

- Online

By Product Type

- Almonds

- Walnuts

- Cashews

- Hazelnuts

- Pistachios

- Others

By Country

- Germany

- United Kingdom

- France

- SEuropeantaly

- Rest of Europe

Frequently Asked Questions

1. What are the main product types driving growth in the Europe Nuts Market?

Almonds dominate the Europe Nuts Market with approximately 30% market share in 2025, followed by cashews, walnuts, pistachios, and hazelnuts as key product categories. Almonds and cashews are the fastest-growing segments within the Europe Nuts Market due to their exceptional versatility, superior nutritional profile featuring high vitamin E content, and widespread use across snacking, bakery, and food processing applications.

2. What health benefits are driving consumer demand in the Europe Nuts Market?

Health benefits fueling the Europe Nuts Market include reduced risk of heart disease and diabetes, lower cholesterol and triglycerides levels, weight management support, and provision of essential nutrients like fiber, healthy fats, vitamins, minerals, and antioxidants. These nutritional advantages position the Europe Nuts Market as a key component of Mediterranean and plant-based dietary patterns increasingly adopted by health-conscious European consumers.

3. What distribution channels are most important in the Europe Nuts Market?

The B2B segment dominates the Europe Nuts Market with 53.76% market share in 2025, while B2C channels including supermarkets/hypermarkets, convenience stores, health food stores, specialty stores, HoReCa, and online e-commerce platforms account for the remaining share. Within the Europe Nuts Market, household retail consumption represents 60% of total demand in 2025, with consumers purchasing nuts for home snacking, cooking ingredients, and baking applications.

4. How is the organic segment performing in the Europe Nuts Market?

The organic segment in the Europe Nuts Market is experiencing rapid growth, driven by increasing consumer awareness and demand for healthier, environmentally friendly food options with minimal processing and additives. The Europe Nuts Market's organic subsector was valued with nuts accounting for 75.1% of organic edible nuts and seeds revenue in 2023, reflecting strong consumer preference for certified organic products particularly in Nordic countries and Germany.

5. What are the major challenges facing the Europe Nuts Market?

Price volatility represents a major constraint in the Europe Nuts Market, with fluctuating prices driven by unpredictable weather events such as droughts, floods, and frost disrupting supply chains in key growing regions. These adverse conditions in the Europe Nuts Market lead to reduced yields and sharp price increases, making it difficult for manufacturers to maintain stable product costs and creating uncertainty for both producers and buyers.

6. How are sustainability trends impacting the Europe Nuts Market?

Sustainability is becoming a critical differentiator in the Europe Nuts Market, with European consumers increasingly prioritizing organic, locally-sourced, fair-trade, and ethically sourced nuts as part of broader environmental commitments. The Europe Nuts Market is witnessing retailer pressure for sustainable products, with EU-wide regulations and green directives shaping product design, sourcing practices, and reporting requirements across the supply chain.

7. What role do plant-based diets play in the Europe Nuts Market?

Plant-based dietary trends are significantly propelling the Europe Nuts Market, as consumers shift towards sustainable and environmentally friendly dietary choices, with nuts serving as preferred alternatives to animal-derived protein sources. The Europe Nuts Market benefits from nuts being naturally plant-based and versatile protein sources, appealing particularly to millennials and Gen Z consumers who prioritize health, sustainability, and diverse nutritional benefits.

8. Which regions within Europe show the strongest growth potential in the Europe Nuts Market?

Western Europe dominates the Europe Nuts Market with over 60% of sales, exhibiting mature demand with focus on sustainability and quality, while Eastern Europe shows strong expansion potential driven by increasing retail penetration and rising consumer awareness. The Netherlands demonstrates the strongest growth trajectory in the Europe Nuts Market with 6.8% CAGR, followed by Spain at 6.3% CAGR, supported by innovative food technology sectors and expanding nut production capabilities.

9. What are the key application segments in the Europe Nuts Market?

Primary applications in the Europe Nuts Market include direct consumption snacks, bakery products, breakfast cereals, smoothies, cooking ingredients, nut-based spreads, and food processing components. The Europe Nuts Market shows rising demand for premium and flavored varieties, with nuts increasingly incorporated into daily meals across multiple formats from whole natural to blanched, sliced, and flour alternatives for modern dietary needs.

10. How is e-commerce impacting the Europe Nuts Market?

Online sales channels are gaining importance in the Europe Nuts Market through e-commerce marketplaces and brand-owned websites, offering consumers convenient access to diverse nut varieties, premium products, and specialty items. The Europe Nuts Market's digital transformation enables direct-to-consumer engagement, subscription models, and personalized product offerings, particularly appealing to younger demographics and urban consumers seeking convenience.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com