Europe Oral Care Market Size, Share, Trends & Growth Forecast Report By Product Type (Toothpaste, Toothbrush [Manual Toothbrush, Electric Toothbrush], Mouthwash, Dental Floss, Teeth Whitening Products), Application / End-User (Adults, Children, Geriatric Population), Distribution Channel (Supermarkets/Hypermarkets, Pharmacies/Drug Stores, Online Retail, Specialty Stores), and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) Industry Analysis From 2026 to 2034.

Market Size, 2025

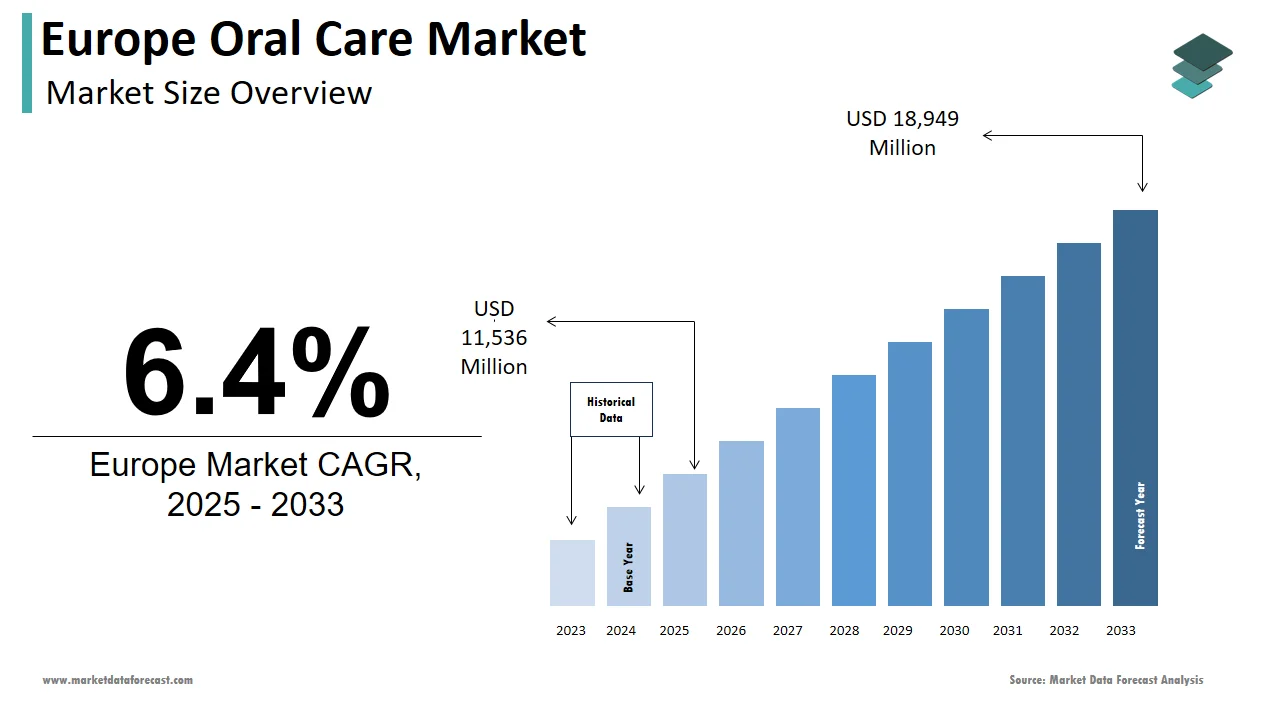

$11,536 MnMarket Estimate, 2026

$12,175 MnMarket Forecast, 2034

$20,162 MnCAGR, 2026–2034

6.4%Europe Oral Care Market Size

The oral care market size in Europe was valued at USD 11,536 million in 2025. The European market is estimated to be worth USD 20,162 million by 2034 from USD 12,175 million in 2026, growing at a CAGR of 6.4% from 2026 to 2034.

The Oral Care products and formulations are designed to maintain dental hygiene, prevent oral diseases, and enhance aesthetic appearance, including toothpastes, mouthwashes, toothbrushes, interdental cleaners, and specialized treatments such as desensitizing agents and enamel strengtheners. As of 2025, over 40% of adults across the European Union exhibit signs of severe periodontitis according to the European Federation of Periodontology, highlighting a persistent public health burden. Furthermore, the European Commission classifies fluoride as a substance of very high concern under REACH, yet permits its use in toothpaste under strict concentration limits by illustrating the region’s cautious yet pragmatic regulatory stance.

MARKET DRIVERS

Rising Scientific Recognition of Oral Systemic Health Linkages Elevates Preventive Care

Growing clinical evidence now establishes strong bidirectional relationships between periodontal disease and systemic conditions, such as type 2 diabetes and cardiovascular disorders is propelling the growth of the Europe oral care market. Similarly, the International Diabetes Federation confirmed that effective periodontal treatment improves glycemic control in diabetic patients by reducing HbA1c levels by 0.4 percentage points on average. These findings have prompted national health agencies to integrate oral health into chronic disease management protocols. In Germany, statutory health insurers now reimburse professional teeth cleaning for diabetic patients twice yearly as per the Federal Joint Committee’s 2023 directive. Public awareness campaigns such as the UK’s “Mouth Healthy” initiative have further reinforced daily brushing and interdental cleaning as non-negotiable health behaviours.

Expansion of E Commerce and Direct-to-Consumer Branding Reshapes Product Accessibility

The digital retail channels have dramatically altered oral care purchasing patterns, with online sales growing every year is also prompting the growth of the Europe oral care market. Consumers now access niche formulations, such as hydroxyapatite toothpaste for enamel regeneration or alcohol free antimicrobial mouth rinses, through curated subscription platforms that bypass traditional pharmacy gatekeeping. Brands like Nucao and Denttabs have leveraged social media influencers and sustainability narratives to build loyal communities, particularly among urban millennials in France and the Netherlands. Regulatory harmonisation under the EU Cosmetic Products Notification Portal further enables agile brand launches across borders. This digital democratization not only accelerates innovation cycles but also empowers consumers to seek personalized solutions beyond mass market offerings, reinforcing proactive oral health management.

MARKET RESTRAINTS

Stringent EU Regulations on Fluoride and Antimicrobial Ingredients Limit Product Innovation

The European Union enforces some of the world’s strictest controls on active ingredients in oral care products under Regulation EC 1223 2009 on cosmetics and the Biocidal Products Regulation EU 528 2012. These stringent EU regulations are hampering the growth of the Europe oral care market. Fluoride concentration in toothpaste is capped at 1500 parts per million with mandatory child safety warnings, while triclosan was banned entirely in 2016 due to endocrine disruption concerns. More recently, the European Chemicals Agency classified chlorhexidine as a substance of very high concern requiring rigorous authorization for use in mouthwashes. This regulatory caution discourages investment in next-generation antimicrobials even as antibiotic resistance rises. Manufacturers must instead rely on less potent alternatives such as essential oils or zinc salts, which offer inferior plaque control.

Persistent Oral Health Inequalities Across Socioeconomic and Geographic Lines Suppress Market Penetration

The access to effective oral care with significant disparities tied to income, education, and regional healthcare infrastructure is additionally impeding the growth of the Europe oral care market. Even in wealthy nations, socioeconomic gradients persist, with UK data from the Office for National Statistics showing that adults in the lowest income quintile are three times more likely to skip brushing twice daily. Public dental services in countries like Spain and Italy focus almost exclusively on children, leaving adults to seek private care, with a barrier for 25% of the EU population lacking supplemental insurance. These structural gaps mean that advanced or premium oral care products primarily serve affluent urban segments, while large portions of the population rely on basic, low-cost alternatives.

MARKET OPPORTUNITIES

Integration of Personalised Oral Care Through AI and At-Home Diagnostics

The emerging digital health technologies are enabling hyper personalised oral care regimens based on individual microbiome profiles and behavioural data, which is setting up new opportunities for the growth of the Europe oral care market. Startups like OraWell in Switzerland and SmileOne in Germany now offer at-home saliva test kits that analyse bacterial load, pH, and inflammation markers, transmitting results to mobile apps that recommend tailored product combinations. These innovations align with the EU’s Digital Health Action Plan, which promotes preventive self-care through validated consumer devices. National health systems are beginning to recognise their value, with Finland’s Kanta Services platform piloting integration of oral health data into national electronic records.

Growth of Sustainable and Waterless Oral Care Formats Aligns with EU Green Consumption Trends

The increasing demand for sustainable and waterless oral care formats with EU green consumption trends is likely to elevate the growth of the Europe oral care market. Toothpaste tablets packaged in glass or metal containers now account for 12% of new product launches in Western Europe, as per the European Cosmetic Association’s 2024 sustainability report. Brands like Bite and Denttabs have eliminated over 200 million plastic tubes from circulation since 2020 by promoting solid formats that require no water during use. Regulatory incentives further support this shift with France’s Anti-Waste Law banning single-use plastic packaging in cosmetics by 2025. Consumers are responding enthusiastically, with 68% of Germans expressing willingness to pay a premium for zero-waste oral care.

MARKET CHALLENGES

Consumer Skepticism Toward “Natural” Claims and Greenwashing Undermines Trust

The proliferation of plant-based and “chemical-free” oral care products has triggered regulatory scrutiny and consumer wariness across Europe. The trend towards greenwashing has a majorly impact on the growth of the Europe oral care market. In response, Germany’s Federal Office of Consumer Protection issued warnings against charcoal toothpaste for enamel abrasion, while the French Directorate General for Competition fined three brands for misleading whitening assertions. This regulatory backlash has eroded consumer confidence, with a 2024 Eurobarometer survey revealing that only 32% of EU citizens trust natural oral care labels without third-party certification.

Shortage of Dental Professionals in Rural and Eastern European Regions Limits Preventive Guidance

A deficit of dentists in non-urban areas and Eastern Europe restricts professional reinforcement of daily oral hygiene practices, which is also degrading the growth of the Europe oral care market. The WHO recommends a dentist-to-population ratio of 1 per 2000, but Romania and Bulgaria report ratios of 1 per 5000 and 1 per 4200, respectively. This scarcity means preventive education, such as proper brushing technique or interdental cleaning, which is rarely delivered outside schools or online. Consequently, even when effective products are available, behavioural adoption remains low. The EU’s Health Workforce Strategy aims to address this imbalance by 2030, but migration of dentists to Western Europe continues apace, with 1800 Romanian dentists registering in Germany in 2024 alone, as per the German Dental Association.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Application / End-User, Distribution Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Procter & Gamble, Unilever, Colgate-Palmolive Company, GSK Consumer Healthcare, Church & Dwight Co., Inc., GlaxoSmithKline PLC, Sunstar Suisse SA, Henkel AG & Co. KGaA, Hawley & Hazel (BVI) Co. Ltd., and Others. |

SEGMENTAL ANALYSIS

By Product Insights

The toothpaste segment was the largest and held 44.3% of the Europe Oral Care Market share in 2024. Fluoride toothpaste remains the cornerstone of caries prevention across European public health policy. The World Health Organization’s European Regional Office recommends twice-daily brushing with fluoride toothpaste as a non-negotiable standard for all age groups. The European Commission permits fluoride concentrations up to 1500 parts per million in adult formulations under Regulation EC 1223 2009, ensuring consistent anti-caries efficacy. Furthermore, toothpaste serves as the primary delivery system for additional actives such as stannous fluoride for gingivitis or potassium nitrate for sensitivity, making it a multi-functional platform.

The electric toothbrushes segment is expected to witness the fastest CAGR of 8.2% during the forecast period, with technological integration and clinical validation. This evidence has led national dental associations in Sweden and the Netherlands to formally recommend electric brushes for patients with periodontal risk. In Germany, statutory health insurers now partially reimburse electric toothbrushes for diabetic and orthodontic patients following Federal Joint Committee guidelines issued in 2024. Modern electric toothbrushes feature Bluetooth connectivity, pressure sensors, and AI-driven brushing feedback transmitted to mobile apps that track coverage duration and technique. Brands like Oral-B and Philips Sonicare partner with dental practices to embed app data into recall systems, enabling personalised hygiene advice.

By Application / End User Insights

The adult segment held a dominant share of the Europe Oral Care Market in 2024, with the income autonomy and rising awareness of oral systemic links. Adults aged 25 to 64 control household purchasing decisions and increasingly view oral care as integral to long-term health. In Germany, 72% of adults use therapeutic toothpastes targeting gum health or sensitivity. Furthermore, workplace dental insurance in countries like France and the Netherlands covers professional cleanings twice yearly, reinforcing daily home care. This combination of financial agency health literacy and clinical need ensures adults remain the primary engine of product demand and innovation. Many European employers and private insurers now integrate oral health into wellness initiatives.

The geriatric segment is anticipated to register the fastest CAGR of 7.6% in next coming years with ageing and geriatric dentistry advancements. This cohort faces elevated risks of root caries, dry mouth, and periodontal disease due to polypharmacy and reduced salivary flow. National health systems are responding with targeted interventions such as Germany’s 2023 Geriatric Dental Care Protocol, which mandates fluoride varnish and high-concentration toothpaste prescriptions for nursing home residents. Age-related dexterity loss and visual impairment necessitate adaptive oral care solutions. Electric toothbrushes with ergonomic grips, large button interfaces, and automatic timers now dominate senior purchases in Switzerland and Denmark, as per national pharmacy sales data. Manufacturers like GSK and Colgate have launched senior-specific lines featuring high contrast packaging, larger text, and simplified routines. These human-centred designs lower usage barriers and align with EU accessibility directives under the European Disability Strategy 2021–2030.

By Distribution Channel Insights

The pharmacies and drug stores segment was the largest by capturing 41.2% of the Europe oral care market share in 2024. Pharmacies in Europe are legally permitted to offer clinical advice on over-the-counter oral health products, creating a high-trust environment. In France and Italy, pharmacists must hold a state diploma and are often the first point of contact for sensitivity gum disease or post-surgical care recommendations. This advisory role is reinforced by regulatory distinctions; prescription-strength fluoride toothpastes (2800–5000 ppm) are exclusively dispensed through pharmacies in Germany and the UK as per national medicines agencies.

The online retail segment is expected to witness the fastest CAGR of 12.4% in next coming years with digital adoption and niche product accessibility. Online channels enable agile brands to bypass traditional gatekeepers and reach eco-conscious or ingredient-literate consumers directly. Brands like Hydrophil and David’s offer plastic-free toothpaste tablets, refillable floss, and compostable brushes primarily through their own websites and Amazon. Subscription models further enhance retention, offering convenience and personalised replenishment. EU harmonisation under the Single Market allows seamless cross-border e-commerce, enabling consumers to access specialised products unavailable locally. Additionally, online retailers use browsing and purchase data to recommend complementary products, suggesting interdental brushes after an electric toothbrush purchase, for example.

COUNTRY LEVEL ANALYSIS

Germany Oral Care Market Analysis

Germany was the largest contributor to the Europe Oral Care Market by holding 23.3% of the share in 2024, with its robust healthcare infrastructure, high health literacy, and regulatory influence. The country enforces strict product classification under the Medical Devices Regulation, enabling a clear distinction between cosmetic and therapeutic oral care. Public health initiatives such as the “Gesund ins Leben” programme promote oral hygiene from infancy, while statutory health insurers reimburse professional cleanings for high-risk groups. The combination of scientific rigour, consumer awareness, and policy integration makes Germany the region’s most mature and influential market.

France Oral Care Market Analysis

The France oral care market growth is driven by its pharmacy-dominated distribution model and strong cultural emphasis on aesthetic oral care. The French National Health Insurance covers annual dental check-ups for children and partial reimbursement for scaling in adults, reinforcing preventive habits. Additionally, France exhibits a high demand for premium and natural formulations, with 65% of adults preferring plant-based or herbal mouthwashes according to the French Institute for Public Opinion. Regulatory bodies like ANSM maintain strict oversight on cosmetic claims, ensuring product credibility.

United Kingdom Oral Care Market Analysis

The UK oral care market growth is propelled by its hybrid public-private dental system and strong digital adoption. The UK also leads in e-commerce with 52% of oral care sales occurring online according to the Office for National Statistics, driven by subscription models and direct-to-consumer brands. Post Brexit, the UKCA marking maintains alignment with EU safety standards, ensuring continued product availability.

Italy Oral Care Market Analysis

The Italy oral care market growth is driven by family-centric oral care traditions and rising geriatric needs. The country maintains one of Europe’s highest dentist-to-population ratios with over 55,000 practitioners. Family pharmacies play a central role, with 80% of households purchasing children’s and senior toothpastes through local drug stores. Italy also shows high consumption of herbal and essential oil-based mouthwashes rooted in Mediterranean wellness practices.

COMPETITIVE LANDSCAPE

The Europe oral care market features intense competition among global consumer health giants, regional pharmaceutical players, and agile direct-to-consumer startups. The top tier, dominated by Haleon, Colgate Palmolive, and Procter and Gamble, competes on scientific credibility, brand heritage, and professional endorsement rather than price. These firms leverage clinical data to secure placement in pharmacy recommendations and national prevention guidelines. Mid-tier competitors, including Pierre Fabre and Laboratoires Filorga, focus on natural formulations and dermo cosmetic positioning targeting premium niches. Meanwhile, digital natives like Bite and David’s disrupt through sustainability storytelling, subscription models, and social media marketing, bypassing traditional retail. Regulatory complexity under EU cosmetic and medical device frameworks acts as a significant barrier protecting established players but also incentivising continuous reformulation. Competition is increasingly defined by the ability to blend therapeutic efficacy, environmental responsibility, and digital interactivity into cohesive consumer health ecosystems.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe oral care market include

- Procter & Gamble

- Unilever

- Colgate-Palmolive Company

- GSK Consumer Healthcare

- Church & Dwight Co., Inc.

- GlaxoSmithKline PLC

- Sunstar Suisse SA

- Henkel AG & Co. KGaA

- Hawley & Hazel (BVI) Co. Ltd.

TOP PLAYERS IN THE MARKET

- GSK Consumer Healthcare, now operating as Haleon, is a dominant force in the Europe Oral Care Market with globally recognised brands such as Sensodyne and Parodontax that address sensitivity and gum health. The company leverages extensive clinical research to substantiate product efficacy, aligning with Europe’s evidence-driven consumer and regulatory landscape. Furthermore, Haleon enhanced its sustainability profile by transitioning Sensodyne tubes to recyclable aluminium in Western Europe.

- Colgate Palmolive maintains a strong presence in the Europe Oral Care Market through its comprehensive portfolio, including Colgate Total and Elmex, which cater to caries sensitivity and enamel protection needs. The company invests heavily in public health initiatives, collaborating with ministries of health across France, Italy, and the Nordic countries to deliver school-based oral hygiene education.

- Procter and Gamble plays a pivotal role in the Europe Oral Care Market through its Oral-B and Crest brands, which lead in electric toothbrushes and whitening solutions. The company integrates advanced technology with oral health science, offering AI-powered brushing feedback and enamel-safe whitening systems. Additionally, P and G deepened collaborations with dental clinics in the UK and the Netherlands to provide in-practice demonstrations of its smart devices. These initiatives position P and G at the intersection of digital health sustainability and professional validation, driving sustained engagement in a competitive marketplace.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Oral Care Market pursue integrated strategies centred on clinical validation, sustainability, and digital engagement. Companies invest in robust clinical trials to substantiate therapeutic claims, ensuring alignment with EU regulatory expectations and dentists recommendations. They reformulate products to meet tightening restrictions on fluorides, antimicrobials, and plastics while advancing recyclable and waterless formats. Strategic partnerships with national dental associations, public health bodies, and pharmacies enhance professional credibility and distribution access. Digital transformation is prioritised through smart devices, mobile apps, and AI-driven brushing analytics that promote adherence and personalisation. Additionally, sfirms accelerate eco innovation by adopting refillable packaging mono mono-material tubes, and bio-based ingredients in response to the EU Green Deal and consumer demand for ethical consumption.

MARKET SEGMENTATION

This Europe sporting goods market research report is segmented and sub-segmented into the following categories.

By Product Type

-

Toothpaste

-

Toothbrush

-

Manual Toothbrush

-

Electric Toothbrush

-

-

Mouthwash

-

Dental Floss

-

Teeth Whitening Products

-

Other Oral Care Products (e.g., gels, powders, etc.)

By Application / End-User

- Adults

- Children

- Geriatric Population

By Distribution Channel

- Supermarkets/Hypermarkets

- Pharmacies/Drug Stores

- Online Retail

- Specialty Stores

- Others (Convenience stores, dental clinics, etc.)

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the europe oral care market?

The europe oral care market includes oral hygiene products, dental accessories, and preventive solutions for healthy teeth and gums across european countries

2. Which countries lead the europe oral care market?

Germany leads the europe oral care market, followed by the UK, France, Italy, and Spain, thanks to high awareness and advanced dental infrastructure

3. What drives growth in the europe oral care market?

Growth in the europe oral care market is driven by preventive healthcare, cosmetic dentistry trends, e-commerce, and rising disposable incomes

4. What are the top product segments in the europe oral care market?

Toothpaste, toothbrushes, dental floss, mouthwash, whitening products, and smart toothbrushes dominate the europe oral care market

5. How do cosmetic dental products affect the europe oral care market?

Cosmetic dental products like whitening strips and enamel repair kits boost demand, shaping the europe oral care market by meeting aesthetic needs

6. What role does preventive care play in the europe oral care market?

Preventive care drives growth in the europe oral care market through consumer education, dental visits, and products like floss and mouthwash

7. How is sustainability influencing the europe oral care market?

Eco-friendly products and sustainable dental practices are crucial trends, transforming the europe oral care market across nations like Germany

8. What impact does e-commerce have on the europe oral care market?

Online retail is the fastest-growing channel, allowing consumers to buy europe oral care market products conveniently with expanded product info

9. Who are leading companies in the europe oral care market?

Major players in the europe oral care market include Colgate-Palmolive, Procter & Gamble, GlaxoSmithKline, and Johnson & Johnson

10. What challenges face the europe oral care market?

Competition, regulatory changes, evolving consumer habits, and sustainability requirements challenge the europe oral care market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com