- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

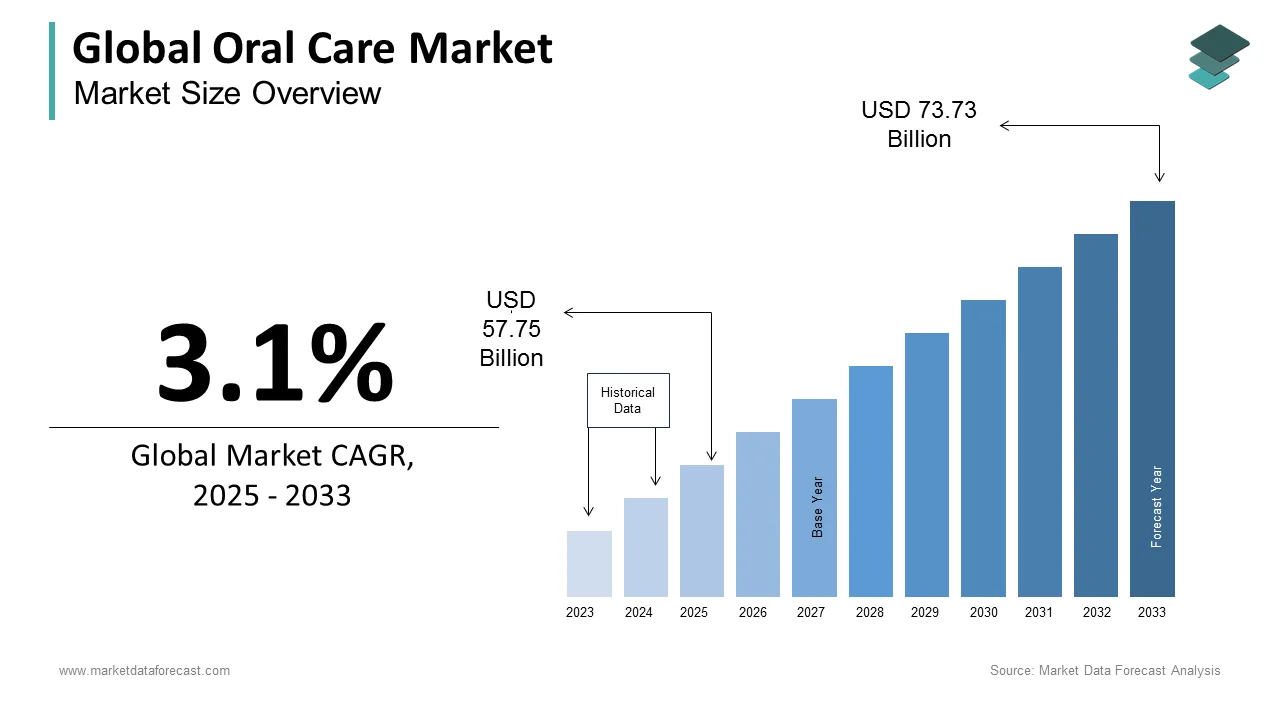

Market Size, 2025

$57.75 BnMarket Estimate, 2026

$59.54 BnMarket Forecast, 2034

$76.01 BnCAGR, 2026–2034

3.1%Global Oral Care Market Report Summary

The global oral care market was valued at USD 57.75 billion in 2025 and is projected to grow from USD 59.54 billion in 2026 to USD 76.01 billion by 2034, registering a CAGR of 3.1% from 2026 to 2034. Market growth is driven by increasing awareness regarding oral hygiene, rising prevalence of dental disorders, and growing consumer spending on personal care products. Oral care products such as toothpaste, toothbrushes, mouthwashes, and whitening solutions are increasingly adopted as part of preventive healthcare routines. Expanding urbanization, growing demand for premium oral care products, and increasing availability of innovative formulations are further supporting market expansion globally.

Key Market Trends

- Rising consumer focus on preventive oral healthcare and hygiene awareness.

- Increasing demand for premium, herbal, and natural oral care products.

- Growing adoption of teeth whitening and cosmetic oral care solutions.

- Expansion of e-commerce and omnichannel retail distribution networks.

- Continuous innovation in sensitive teeth care and advanced oral hygiene formulations.

Segmental Insights

- Based on product type, the toothpaste segment dominated the global oral care market in 2025 by accounting for 40.5% market share, driven by widespread daily usage and increasing demand for specialized formulations.

- Based on application/end user, the adult segment held the majority share of 60.3% in 2025, supported by high oral health awareness, preventive care habits, and growing adoption of premium oral hygiene products.

- Based on distribution channel, the supermarkets and hypermarkets segment led the market by capturing 45.8% share in 2025, driven by extensive product availability, strong consumer accessibility, and promotional retail strategies.

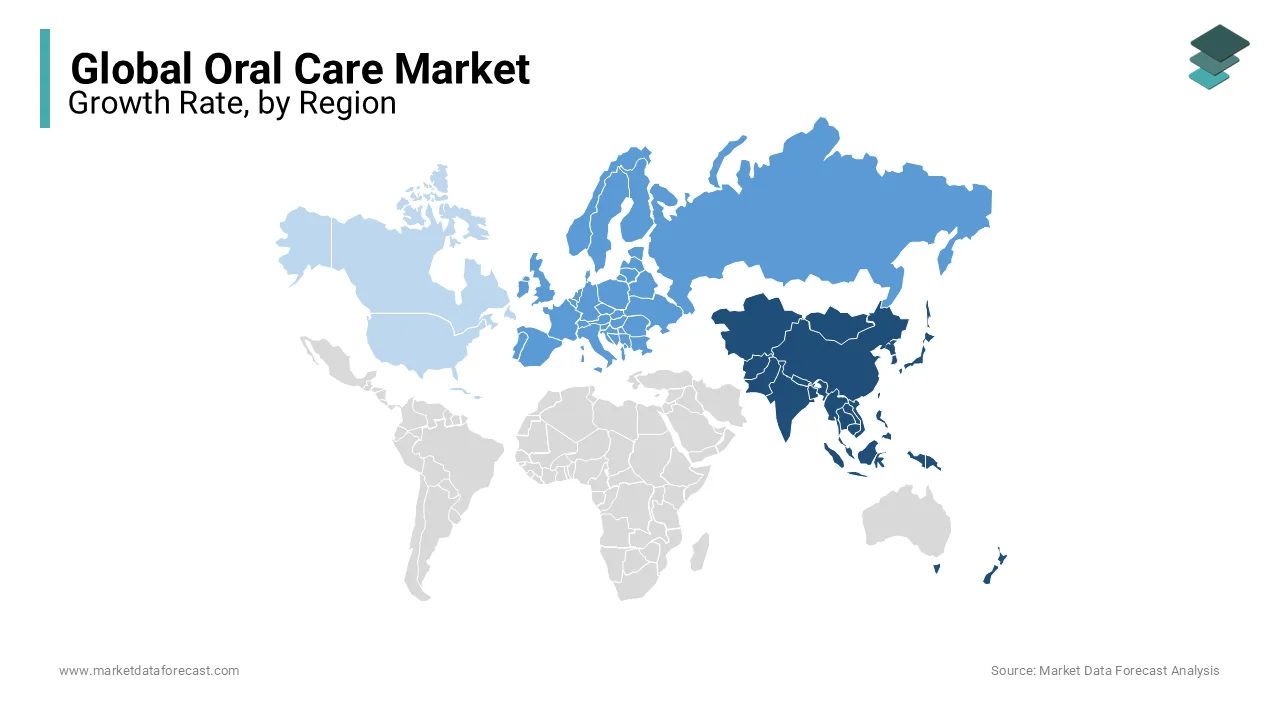

Regional Insights

The global oral care market is witnessing steady growth across major regions, supported by increasing healthcare awareness, rising disposable incomes, and growing emphasis on preventive dental care.

- North America dominated the global market in 2025 with 35.8% share, driven by high consumer awareness, strong spending on personal care products, and advanced retail infrastructure.

- Europe held the second-largest position with 30.7% share in 2025, supported by widespread oral hygiene awareness and strong demand for premium and sustainable oral care products.

- Asia-Pacific is experiencing rapid expansion due to rising incomes, urbanization, and increasing awareness regarding oral health and hygiene practices.

Competitive Landscape

The global oral care market is characterized by strong competition among multinational consumer goods companies and personal healthcare product manufacturers focusing on innovation, brand expansion, and premium product development. Market participants are emphasizing natural ingredient formulations, sustainable packaging, and expansion of digital marketing strategies to strengthen market positioning. Strategic acquisitions, product launches, and investments in research and development are shaping competitive dynamics across the market.

Prominent companies operating in the global oral care market include Sunstar Suisse SA, Henkel AG & Co. KGaA, GlaxoSmithKline PLC, Haleon plc, Unilever PLC, Johnson & Johnson, Procter & Gamble, Colgate-Palmolive Company, and Church & Dwight Co. Inc.

Global Oral Care Market Size

The size of the global oral care market was worth USD 57.75 billion in 2025. The global market is anticipated to grow at a CAGR of 3.1% from 2026 to 2034 and be worth USD 76.01 billion by 2034 from USD 59.54 billion in 2026.

Oral care (or oral hygiene) refers to the practices and habits you follow to keep your mouth, teeth, and gums clean, healthy, and disease-free. It involves much more than a gleaming smile; it prevents tooth decay, gum disease, and bad breath, while protecting your overall health. This market includes daily use items such as toothpaste, toothbrushes, mouthwash, and dental floss, alongside professional treatments like whitening, orthodontics, and restorative procedures. The market is fundamentally driven by the intrinsic link between oral health and systemic well-being. According to the World Health Organization, oral diseases affect nearly 3.5 billion people globally, with untreated caries in permanent teeth being the most common health condition worldwide. As per the Centers for Disease Control and Prevention, approximately 47 percent of adults aged 30 years and older in the United States show signs of gum disease, highlighting the pervasive nature of periodontal issues. The rising prevalence of lifestyle-related conditions such as diabetes further exacerbates oral health risks, creating a continuous demand for preventive and therapeutic solutions. Regulatory bodies strictly monitor ingredient safety and efficacy claims, ensuring consumer protection. The integration of digital technologies in diagnostics and treatment planning has transformed professional care delivery. Consumer awareness regarding the impact of oral hygiene on overall health drives consistent product adoption. The market also reflects shifting aesthetic preferences with increasing demand for cosmetic dentistry and at-home whitening solutions. This dynamic landscape requires manufacturers to balance clinical effectiveness with consumer convenience and sustainability concerns. The sector serves as a critical component of public health infrastructure, influencing quality of life and healthcare costs.

MARKET DRIVERS

Rising Prevalence of Oral Diseases and Systemic Health Links

The rising prevalence of oral diseases and their established links to systemic health conditions are driving the growth of the oral care market. Conditions such as dental caries, periodontitis, and oral cancer are increasingly recognized not merely as localized issues but as indicators of broader health status. According to the Global Burden of Disease Study, oral conditions have remained highly prevalent over the past three decades, affecting billions of individuals despite preventive efforts. As per the American Heart Association, research indicates a significant correlation between periodontal disease and cardiovascular issues, including heart disease and stroke. This scientific evidence prompts healthcare providers to emphasize oral hygiene as a critical component of overall wellness protocols. Patients diagnosed with diabetes are particularly vigilant about oral care since gum disease can complicate blood sugar control. The aging population further amplifies demand as older adults are more susceptible to root decay and tooth loss. Public health campaigns by governments and non-governmental organizations educate communities on the importance of regular brushing, flossing, and professional checkups. These initiatives drive the consumption of therapeutic toothpastes, antimicrobial mouthwashes, and specialized brushes. The economic burden of treating advanced oral diseases encourages early intervention through daily care products. Consequently, the growing awareness of health interconnectivity sustains robust demand for effective oral hygiene solutions. This driver ensures consistent market growth across diverse demographic segments.

Increasing Consumer Awareness and Aesthetic Demands

Increasing consumer awareness and aesthetic demands significantly propel the expansion of the oral care market. As a result, individuals increasingly prioritize their personal appearance and social confidence. The influence of social media and celebrity culture has normalized bright white smiles and straight teeth as standards of beauty and success. According to the American Academy of Cosmetic Dentistry, a majority of adults believe that an attractive smile is an important social asset, and many are willing to invest in improvements. As per Statista, the global interest in teeth whitening products has surged, with millions of consumers seeking both professional treatments and at-home kits. This trend extends beyond whitening to include alignment correction, driving the adoption of clear aligners and invisible braces. Consumers are increasingly educated about the benefits of electric toothbrushes, water flossers, and tongue cleaners in achieving superior hygiene. The availability of information online empowers individuals to make informed choices about ingredients and technologies. Marketing campaigns by major brands emphasize the connection between oral care and self-esteem, reinforcing purchasing behavior. The rise of influencer endorsements and digital tutorials further accelerates product adoption among younger demographics. Premiumization trends lead consumers to trade up from basic manual brushes to high-tech devices with smart features. Thus, the desire for aesthetic perfection and social acceptance drives market vitality. The focus on visual appeal ensures sustained innovation and sales growth.

MARKET RESTRAINTS

High Cost of Advanced Dental Treatments and Devices

The high cost of advanced dental treatments and devices restrains the accessibility and growth of the oral care market. This issue is particularly evident in emerging economies and among lower-income populations. Professional procedures such as implants, orthodontics, and cosmetic surgeries require substantial financial investment, which is often not covered by insurance plans. According to the Kaiser Family Foundation, dental coverage remains separate from medical insurance for many adults in the United States, leading to high out-of-pocket expenses. As per the World Bank, limited healthcare budgets in developing nations restrict access to essential dental services, let alone premium care products. The high price point of electric toothbrushes, water flossers, and professional-grade whitening systems discourages widespread adoption among budget-conscious consumers. Many individuals postpone necessary treatments due to financial constraints, resulting in worsening oral health conditions that could have been prevented. The lack of affordable financing options further limits market penetration for high-value devices. In rural areas, the scarcity of qualified dental professionals exacerbates the issue, making travel and treatment costs prohibitive. This economic barrier creates a disparity in oral health outcomes between socioeconomic groups. Manufacturers face challenges in pricing strategies that balance profitability with accessibility. Therefore, the financial burden acts as a persistent brake on market expansion. The need for cost-effective solutions remains unmet in many segments.

Lack of Awareness in Rural and Underserved Regions

Lack of awareness in rural and underserved regions is a major obstacle to the uniform expansion of the oral care market. Despite global health initiatives, many communities lack basic knowledge about proper oral hygiene practices and the importance of regular dental visits. According to the World Health Organization, oral health education is insufficient in many low and middle-income countries, leading to high rates of preventable diseases. As per the United Nations Children's Fund, children in rural areas often suffer from severe tooth decay due to poor dietary habits and inadequate brushing routines. The absence of structured school-based health programs means that healthy habits are not instilled from a young age. Cultural beliefs and misconceptions about dental care further hinder the adoption of modern oral hygiene products. Limited access to clean water and sanitation facilities also complicates daily hygiene practices. Retail distribution networks for oral care products are often sparse in remote areas, reducing availability. Without targeted educational campaigns and infrastructure improvements, demand remains stagnant in these regions. Governments and nonprofits struggle to allocate sufficient resources for widespread outreach. This knowledge gap limits the potential customer base for manufacturers. Hence, the disparity in health literacy restrains market development. Addressing this issue requires long-term collaborative efforts.

MARKET OPPORTUNITIES

Integration of Digital Technology and Smart Devices

Integration of digital technology and smart devices offers a strong opening for innovation and value addition in the oral care market. The emergence of connected toothbrush apps and artificial intelligence-driven diagnostics transforms routine hygiene into a data-driven health management practice. According to the Consumer Electronics Association, the adoption of smart home health devices is accelerating, with users seeking personalized feedback on their brushing habits. As per Deloitte, digital health solutions enable real-time monitoring of plaque removal, brush pressure, and coverage areas, enhancing user compliance. Smartphone applications provide gamified experiences and progress tracking, which motivate consistent usage, especially among children and teenagers. Teledentistry platforms allow for remote consultations, reducing the need for frequent physical visits and expanding access to professional advice. The collection of longitudinal oral health data enables dentists to offer preventive interventions tailored to individual needs. Manufacturers can leverage this data to develop new products and services that address specific user behaviors. The premium positioning of smart devices attracts tech-savvy consumers willing to pay for advanced features. Partnerships with insurance providers may lead to incentives for maintaining good oral hygiene tracked via devices. Thus, the convergence of technology and oral care drives market modernization. This trend opens new revenue streams and enhances customer engagement.

Expansion of Natural and Organic Product Lines

Expansion of natural and organic product lines provides a promising avenue for growth in the oral care market. Consumers are increasingly prioritizing sustainability and ingredient transparency. There is a growing preference for products free from synthetic chemicals, artificial flavors, and microplastics, reflecting broader wellness trends. As per the Environmental Working Group, consumers are becoming more aware of potentially harmful ingredients such as triclosan and sodium lauryl sulfate, leading to demand for safer alternatives. Brands are responding by formulating toothpastes and mouthwashes with plant-based extracts, essential oils, and mineral ingredients like hydroxyapatite. Eco-friendly packaging solutions, such as biodegradable tubes and bamboo toothbrushes, appeal to environmentally conscious buyers. The rise of zero-waste lifestyles drives innovation in solid toothpaste tablets and reusable floss picks. Certification from recognized organic bodies enhances credibility and trust among discerning customers. Retailers are dedicating more shelf space to natural oral care categories, reflecting shifting consumer preferences. This segment allows for premium pricing and brand differentiation in a crowded market. Therefore, the focus on purity and sustainability supports market expansion. The alignment with ethical values ensures long-term loyalty.

MARKET CHALLENGES

Stringent Regulatory Standards and Compliance Requirements

Stringent regulatory standards and compliance requirements are major challenges to the oral care market. This imposes rigorous testing and approval processes for new products. Oral care items are often classified as cosmetics or over-the-counter drugs, depending on their claims and ingredients, subjecting them to complex legal frameworks. According to the Food and Drug Administration, manufacturers must adhere to strict guidelines regarding labeling, ingredient safety, and good manufacturing practices. As per the European Commission, the prohibition of certain substances and the requirement for extensive safety assessments increase development time and costs. Claims related to whitening sensitivity relief or gum health require clinical substantiation, which involves expensive and time-consuming trials. Variations in regulations across different countries complicate global expansion strategies for multinational companies. Non-compliance can result in product recalls, fines, and reputational damage. The evolving nature of regulatory landscapes requires continuous monitoring and adaptation of formulations. Small and medium-sized enterprises may lack the resources to navigate these complexities effectively. The pressure to innovate while maintaining compliance creates a delicate balance for research and development teams. Consequently, regulatory hurdles act as a significant barrier to entry and speed to market. The need for meticulous documentation increases operational overhead.

Environmental Concerns and Plastic Waste Management

Environmental concerns and plastic waste management are significant impediments to the oral care market. This is driven by intensifying scrutiny on single-use plastics. Traditional oral care products such as toothpaste tubes, toothbrushes, and floss containers contribute substantially to global plastic pollution. According to the United Nations Environment Program, millions of tons of plastic waste enter oceans annually, with personal care items being a notable contributor. As per Greenpeace, activists and consumers are pressuring brands to adopt sustainable packaging and biodegradable materials. The multi-layer structure of toothpaste tubes makes them difficult to recycle, leading to low recovery rates. Bans on microbeads in exfoliating products have already impacted formulation strategies requiring alternative ingredients. Companies face the challenge of redesigning products and supply chains to meet environmental standards without compromising functionality or cost. The transition to aluminum glass or compostable materials involves higher production expenses and logistical complexities. Consumer skepticism regarding greenwashing necessitates transparent and verifiable sustainability claims. Regulatory pressures are increasing with extended producer responsibility laws being implemented in various jurisdictions. Failure to address these issues can lead to boycotts and loss of market share. Thus, environmental sustainability remains a critical operational challenge. The industry must innovate to reduce its ecological footprint.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product Type, Application / End-User, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Sunstar Suisse SA, Henkel AG & Co. KGaA, GlaxoSmithKline PLC, Unilever, Johnson & Johnson, Procter & Gamble, Colgate-Palmolive Company, and Church & Dwight Co. |

SEGMENTAL ANALYSIS

By Product Insights

The toothpaste segment was the largest by occupying a 40.5% share of the global oral care market in 2025. Its dominance is driven by its status as an essential daily hygiene product with universal adoption across all demographics. This segment includes fluoride-based whitening sensitivity relief and herbal variants. Universal daily usage and essential hygiene requirements drive the domination of toothpaste in the oral care market. Brushing teeth twice daily is a globally recommended practice by health organizations, making toothpaste a non-discretionary purchase for billions of consumers. According to the World Health Organization, maintaining oral hygiene through regular brushing is the primary method for preventing dental caries and periodontal disease. According to verified public health datasets compiled by dental groups and matching CDC Oral Health Reports, approximately 69% of adults in the United States brush their teeth twice a day, while roughly 23% of Americans admit to regularly going two consecutive days or longer without brushing at all. The low cost and high frequency of replacement create a stable revenue stream for manufacturers. Unlike other oral care products that may be used intermittently, toothpaste is consumed regularly, requiring frequent repurchasing. The availability of diverse formulations catering to specific needs, such as enamel protection, gum health, and bad breath control, ensures broad appeal. Marketing campaigns emphasize the critical role of toothpaste in overall health, reinforcing habitual use. The integration of toothpaste into morning and evening routines makes it resistant to economic downturns. Consequently, the indispensability of toothpaste sustains its market leadership. The consistent consumption pattern ensures predictable sales volumes.

In addition, innovation in functional formulations and ingredients significantly contributes to the leading status of toothpaste in the oral care market. Manufacturers continuously invest in research and development to introduce advanced ingredients that address specific oral health concerns. According to the American Dental Association, the inclusion of fluoride remains the gold standard for cavity prevention, but newer additives like hydroxyapatite and arginine are gaining traction for enamel repair and sensitivity relief. As per Colgate Palmolive, the launch of probiotic toothpastes and charcoal-based variants has expanded the product portfolio, attracting health-conscious consumers. These innovations allow brands to differentiate themselves in a saturated market and command premium prices. The trend towards natural and organic ingredients has led to the development of fluoride-free options using plant-based extracts. Clinical studies supporting the efficacy of these new formulations build consumer trust and drive adoption. The ability to offer multifunctional benefits such as whitening and breath freshening in a single product enhances the value proposition. Regulatory approvals for new active ingredients enable continuous product evolution. Thus, technological advancement in formulation sustains the dominance of toothpaste. The focus on enhanced efficacy ensures long-term relevance.

On the other hand, the electric toothbrush segment is predicted to witness the highest CAGR of 7.5% over the forecast period. This swift expansion of the segment is fueled by increasing consumer awareness of superior cleaning efficiency, technological advancements, and the rising popularity of smart home health devices. Superior cleaning efficiency and dental professional recommendations drive the rapid growth of the electric toothbrush segment in the oral care market. Clinical studies have consistently demonstrated that electric toothbrushes remove more plaque and reduce gingivitis more effectively than manual brushes. As per the American Dental Association, many dentists actively recommend electric toothbrushes to patients with gum disease or limited dexterity. This professional endorsement builds consumer confidence and drives adoption. The oscillating, rotating, and sonic technologies provide a deeper clean that is difficult to achieve manually. Consumers are increasingly willing to invest in higher-priced devices to improve their oral health outcomes. The perception of electric toothbrushes as a premium health investment supports market expansion. Insurance companies in some regions are beginning to recognize the preventive benefits, potentially leading to subsidies. The tangible health benefits justify the initial cost for many users. Consequently, the clinical superiority of electric brushes sustains rapid growth. The focus on preventive care drives demand.

Moreover, integration of smart technology and connectivity features accelerates the adoption of electric toothbrushes in the oral care market. Modern electric toothbrushes are equipped with sensors, Bluetooth connectivity, and artificial intelligence to provide real-time feedback on brushing habits. As per Philips Sonicare, smart toothbrushes can track brushing duration, pressure, and coverage areas, sending data to smartphone apps for analysis. This gamified approach encourages proper technique and consistency, especially among younger users. The ability to monitor progress and receive personalized coaching enhances user engagement and satisfaction. Tech-savvy consumers view these devices as part of their broader smart home ecosystem. The data collected can be shared with dental professionals for remote monitoring and advice. The novelty and functionality of smart features justify premium pricing and drive upgrades. Manufacturers continue to innovate with features like UV sanitizing bases and multiple brushing modes. Thus, technological integration supports the fast-paced growth of the segment. The focus on digital health ensures sustained interest.

By Application / End-User Insights

In 2025, the adult segment held the majority share of 60.3% of the oral care market. High awareness and preventive care habits are the factors behind the supremacy of this segment. This demographic includes individuals aged 18 to 64 who are the primary decision makers and purchasers of oral care products. Adults are generally more educated about the importance of oral hygiene and its impact on overall health compared to younger demographics. Only about 65% of US adults visit a dentist annually, and NHANES behavioral metrics track that only 31.7% of the adult population cleans interdentally (flosses) on a daily basis, highlighting a severe deficit in ideal hygiene maintenance. As per the World Health Organization, adults are the target audience for most public health campaigns regarding gum disease and tooth decay. This awareness translates into consistent purchasing of toothpaste, mouthwash, and other hygiene products. Adults are also more likely to invest in premium products such as whitening strips and electric toothbrushes to maintain aesthetic appearance. The prevalence of lifestyle factors such as coffee consumption and smoking increases the need for specialized care products. The responsibility for family purchases often rests with adults, further amplifying their market influence. The focus on maintaining social and professional appearance drives demand for cosmetic oral care. Consequently, the established habits of adults sustain their market leadership. The emphasis on prevention ensures steady consumption.

Disposable income and premium product adoption significantly contribute to the leading status of the adult segment in the oral care market. Adults typically have higher financial stability, allowing them to spend on high-quality and specialized oral care solutions. According to the Bureau of Labor Statistics, household spending on personal care products increases with age and income level. The ability to afford regular dental checkups and supplementary home care products enhances overall oral health. Adults are willing to pay for convenience and effectiveness, preferring products that offer multiple benefits. The trend towards self-care and wellness encourages investment in personal grooming. Marketing strategies targeting adults emphasize sophistication and results appealing to their purchasing power. The availability of flexible payment options for expensive dental treatments further supports spending. Thus, financial capacity drives the dominance of the adult segment. The focus on quality ensures high-value transactions.

But the geriatric population segment is estimated to register the fastest CAGR of 6.8% from 2026 to 2034 due to the aging global population, increased prevalence of oral health issues, and the need for specialized care products. An aging global population and increased longevity support the quick surge of the geriatric segment in the oral care market. The number of individuals aged 65 and older is rising significantly worldwide, creating a larger base for oral care consumption. According to the United Nations Department of Economic and Social Affairs, the global population aged 65 years or above is projected to double by 2050. As per the Centers for Disease Control and Prevention, older adults are more susceptible to root caries, gum disease, and tooth loss due to receding gums and medication side effects. This vulnerability necessitates the use of specialized products such as high-fluoride toothpaste, soft-bristle brushes, and antimicrobial mouthwashes. The increasing lifespan means that individuals retain their natural teeth longer, requiring ongoing maintenance. The demand for denture care products also rises with age. Healthcare systems are focusing more on geriatric oral health to improve quality of life. The growing awareness among seniors about oral hygiene drives product adoption. Consequently, the demographic shift sustains the rapid expansion of this segment. The focus on healthy aging ensures long-term demand.

Specific oral health needs and specialized products accelerate the adoption of oral care solutions among the geriatric population. Older adults face unique challenges such as dry mouth, sensitivity, and difficulty with manual dexterity, requiring tailored solutions. According to the American Dental Association, xerostomia or dry mouth is a common condition in seniors often caused by medications, leading to increased risk of decay. As per the National Institute on Aging, specialized toothpastes with moisturizing agents and high fluoride content are essential for managing these conditions. Ergonomic toothbrush handles and water flossers help those with arthritis or limited mobility maintain hygiene. The availability of these targeted products encourages regular use and improves outcomes. Caregivers and family members often assist in purchasing these specialized items, driving market growth. Dental professionals recommend specific regimens for older patients, enhancing compliance. The focus on comfort and ease of use makes these products attractive. Thus, the alignment with specific health needs supports the fast-paced growth of the segment. The emphasis on accessibility ensures sustained adoption.

By Distribution Channel Insights

The supermarkets and hypermarkets segment led the oral care market and accounted for a 45.8% share in 2025. Convenience and a one-stop shopping experience have contributed to the leading position of this segment. This channel offers a wide variety of products under one roof, providing convenience and competitive pricing. Consumers prefer purchasing oral care products alongside groceries and household items to save time and effort. The extensive shelf space allows for prominent display of leading brands and new launches, influencing buying decisions. Promotional offers,, bundle deals, and loyalty programs attract price-sensitive customers. The immediate availability of products eliminates waiting times associated with online delivery or pharmacy visits. Families often stock up on essentials during weekly shopping trips, ensuring consistent sales volume. The familiar environment reduces purchase anxiety for standard items like toothpaste and manual brushes. Consequently, the ease of access sustains the leadership of this channel. The focus on convenience ensures high turnover.

Competitive pricing and promotional activities significantly contribute to the leading status of supermarkets and hypermarkets in the oral care market. These retailers leverage their large-scale purchasing power to offer lower prices and frequent discounts. The ability to compare prices across different brands on the same aisle facilitates informed decision-making. Private label brands offered by supermarkets provide affordable alternatives, attracting budget-conscious shoppers. Seasonal sales and holiday promotions further boost volume. The transparency of pricing builds trust and encourages repeat visits. Retailers collaborate with manufacturers for exclusive launches and displays, enhancing visibility. Thus, the economic advantage supports the dominance of supermarkets. The focus on value ensures customer loyalty.

On the contrary, the online retail segment is anticipated to witness the fastest CAGR of 9.2% during the forecast period owing to the expansion of e-commerce platforms, the convenience of home delivery, and access to a wider product range. Consumers increasingly prefer shopping online for the convenience of having products delivered to their doorstep. The ability to shop 24/7 without geographical constraints expands market reach. Online platforms offer detailed product descriptions, reviews, and comparisons, aiding decision-making. The COVID-19 pandemic accelerated the shift to online shopping, a trend that has persisted. Fast delivery options make online purchases comparable in speed to physical stores. The ease of returning unsatisfactory products builds consumer confidence. Consequently, the convenience of digital shopping sustains rapid growth. The focus on accessibility ensures widespread adoption.

Access to niche and specialty products accelerates the adoption of online retail in the oral care market. Physical stores often have limited shelf space, restricting the variety of available brands and formulations. The ability to find specific products for rare conditions or preferences drives traffic to digital platforms. Online reviews and influencer recommendations guide consumers towards these niche options. The transparency of ingredient lists and sourcing information appeals to informed buyers. Direct-to-consumer brands leverage online channels to build relationships and offer personalized experiences. Thus, the breadth of selection supports the fast-paced growth of the segment. The focus on variety ensures sustained interest.

REGION ANALYSIS

North America Oral Care Market Analysis

North America dominated the global oral care market and accounted for a 35.8% share in 2025. The demand for oral care was supported by high consumer awareness, advanced healthcare infrastructure, and the strong presence of major industry players. The market status is defined by a preference for premium and technologically advanced products. According to the American Dental Association, regular dental visits and adherence to hygiene routines are common among the population. As per the Centers for Disease Control and Prevention, the prevalence of dental insurance coverage supports access to professional and home care products. The United States and Canada are key markets driving innovation in electric toothbrushes and whitening solutions. High disposable income enables consumers to invest in cosmetic oral care. The presence of leading manufacturers facilitates rapid product launches and marketing campaigns. Regulatory standards ensure product safety and efficacy. The trend towards preventive care drives consistent demand. The integration of digital health tools enhances user engagement. These factors ensure North America remains a leader. The focus on innovation maintains competitiveness. The mature market supports steady growth.

Europe Oral Care Market Analysis

Europe was positioned second in the global market and captured a 30.7% share in 2025. The region is known for strict regulatory standards and a strong preference for natural and sustainable products. The European market is propelled by high adoption of eco-friendly packaging and organic formulations. According to the European Commission, regulations on plastic waste drive innovation in sustainable packaging solutions. Studies compiled by the European Federation of Periodontology (EFP) and the Oral Health Foundation indicate that actual consumer awareness remains dangerously low. A multi-country European survey revealed that up to 74.9% of adolescents were completely unaware that brushing prevents gum disease. Furthermore, large portions of the adult population remain uneducated on how periodontitis structurally impacts systemic health concerns like diabetes, heart disease, and strokes. Countries like Germany, France, and the United Kingdom are major contributors to market revenue. The demand for herbal and fluoride-free toothpastes is growing rapidly. Retailers prioritize environmentally responsible brands. Government initiatives promote oral health education in schools. The aging population increases demand for specialized care. The focus on sustainability drives product development. These elements sustain Europe's market position. The emphasis on quality ensures long-term loyalty. The regulatory framework shapes market dynamics.

Asia-Pacific Oral Care Market Analysis

Asia-Pacific is experiencing rapid expansion in the global oral care market due to rising incomes, urbanization, and increasing health awareness. The market status is defined by a large population base and an emerging middle class. According to the World Health Organization, oral disease prevalence is high in the region, driving demand for preventive products. As per the China National Medical Products Administration, regulatory reforms are improving product quality and safety. India and China are key growth engines with increasing adoption of electric toothbrushes and mouthwashes. Urban consumers are shifting towards premium brands. Rural areas present opportunities for basic hygiene products. Government programs aim to improve access to dental care. The influence of Western beauty standards drives demand for whitening products. Local manufacturers are gaining market share. These drivers ensure Asia-Pacific remains a high-growth market. The demographic dividend supports long-term demand. The shift towards modernization accelerates uptake.

Latin America Oral Care Market Analysis

Latin America grew steadily in the global oral care market owing to diverse economic conditions and a growing focus on oral hygiene. The market is evolving as basic care products become more accessible and awareness grows. According to the Pan American Health Organization, efforts to reduce dental caries are driving public health initiatives. As per Euromonitor International, Brazil and Mexico are the largest markets in the region. The popularity of cosmetic dentistry drives demand for whitening products. Economic instability affects purchasing power, but basic oral care remains a priority. Local brands compete with international players on price. The expansion of retail chains improves product availability. The rising middle class adopts premium products. The focus on affordability drives volume. These factors contribute to steady market growth. The potential for expansion remains high. The integration into global trends supports development.

Middle East and Africa Oral Care Market AnalysisThe

Middle East and Africa region is likely to expand notably in the global oral care market during the forecast period due to investments in healthcare and rising awareness. The market status is defined by varying levels of development and access. As per the African Union, initiatives to promote hygiene are encouraging product adoption. South Africa and the United Arab Emirates are key markets. The demand for basic oral care products is rising with urbanization. Cultural factors influence product preferences. The lack of local manufacturing creates reliance on imports. Government efforts to improve public health support market growth. The young population presents future opportunities. The focus on education drives awareness. These dynamics suggest potential for future growth. The market is in the early stages of development. The emphasis on accessibility drives progress.

COMPETITIVE LANDSCAPE

The competition in the global oral care market is characterized by intense rivalry among multinational corporations and specialized niche brands striving to offer superior efficacy and innovation. Major players compete based on brand reputation, technological advancement, and product diversity. The market features a mix of established giants with extensive distribution networks and agile startups focusing on natural or sustainable solutions. Companies differentiate themselves through proprietary ingredients such as stannous fluoride or hydroxyapatite and advanced device technologies like sonic brushing. Strategic acquisitions of emerging brands help larger entities expand their portfolios and capture new demographic segments. Price competitiveness remains a key factor in developing markets where affordability drives purchasing decisions. Innovation in digital health tools and personalized care experiences drives customer acquisition and retention. Intellectual property protection for unique formulations and device designs serves as a competitive barrier. This dynamic environment fosters continuous improvement and marketing creativity, benefiting consumers with diverse and effective options. The ability to adapt to sustainability trends and health consciousness determines long-term success.

KEY MARKET PARTICIPANTS

Some of the companies that are playing a dominating role in the global oral care market include

- Sunstar Suisse SA (Switzerland)

- Henkel AG & Co. KGaA (Germany)

- GlaxoSmithKline PLC (U.K.)

- Haleon plc

- Unilever PLC (U.K./Netherlands)

- Johnson & Johnson (U.S.)

- Procter & Gamble (U.S.)

- Colgate-Palmolive Company (U.S.)

- Church & Dwight Co. Inc. (U.S.)

TOP PLAYERS IN THE MARKET:

- Procter and Gamble Company is a dominant force in the global oral care market, primarily through its Crest and Oral-B brands. The company offers a comprehensive portfolio, including toothpaste, manual and electric toothbrushes, and mouthwash. Recent actions involve the integration of artificial intelligence into Oral-B smart brushes to provide real-time feedback on brushing habits. Procter and Gamble has expanded its direct-to-consumer channels to enhance customer engagement and data collection. The firm focuses on sustainability by introducing recyclable packaging for its product lines. By leveraging advanced research and development, the company continues to innovate in enamel protection and sensitivity relief. These initiatives strengthen its reputation for scientific excellence and consumer trust. The strategic emphasis on digital health tools differentiates its offerings in a competitive landscape. This approach drives brand loyalty and sustained growth in key markets worldwide.

- Colgate Palmolive Company contributes significantly to the global oral care market with its flagship Colgate brand and diverse portfolio of personal care products. The company is renowned for its extensive distribution network reaching consumers in over two hundred countries. Recent developments include the launch of Colgate Keep, a sustainable electric toothbrush designed with replaceable heads to reduce waste. Colgate has invested heavily in professional dental partnerships to promote preventive care education globally. The firm focuses on innovation in natural ingredients and fluoride-free options to meet evolving consumer preferences. By emphasizing holistic oral health, the company addresses gum disease and enamel erosion effectively. These efforts enhance its position as a leader in both mass and premium segments. The commitment to sustainability and accessibility drives long-term value. This strategy ensures continued relevance and strong market presence across diverse demographics.

- Haleon plc plays a vital role in the global oral care market through its Sensodyne and Parodontax brands, which specialize in sensitive teeth and gum health. Spun off from GlaxoSmithKline, Haleon focuses exclusively on consumer health products. Recent actions involve the expansion of its professional endorsement programs with dentists and hygienists to build clinical credibility. The company has introduced new formulations using stannous fluoride for enhanced protection against sensitivity and gingivitis. Haleon invests in digital marketing campaigns to educate consumers about the link between oral and overall health. The firm prioritizes science-backed innovation to address specific oral care needs. By focusing on niche therapeutic segments, Haleon differentiates itself from generalist competitors. These strategies strengthen its leadership in the sensitive care category. The emphasis on clinical efficacy and professional trust drives sustained growth and consumer loyalty in the global market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the global oral care market primarily employ strategies focused on product innovation and sustainability to maintain a competitive advantage. Companies invest heavily in research and development to create advanced formulations for sensitivity whitening and gum health. Strategic partnerships with dental professionals help build clinical credibility and drive consumer trust. Firms prioritize eco-friendly packaging solutions to address environmental concerns and meet regulatory standards. Expansion into emerging markets through localized product offerings and affordable pricing drives volume growth. Providers also focus on digital integration by developing smart toothbrushes and apps for personalized oral hygiene monitoring. Marketing efforts emphasize the connection between oral health and overall well-being to educate consumers. These strategic initiatives enable firms to differentiate their offerings and respond effectively to changing consumer preferences in the dynamic global oral care sector.

MARKET SEGMENTATION

This research report on the global oral care market has been segmented based on the product type, application / end-user, distribution channel, and region.

By Product Type

-

Toothpaste

-

Toothbrush

-

Manual Toothbrush

-

Electric Toothbrush

-

-

Mouthwash

-

Dental Floss

-

Teeth Whitening Products

-

Other Oral Care Products (e.g., gels, powders, etc.)

By Application / End-User

- Adults

- Children

- Geriatric Population

By Distribution Channel

- Supermarkets/Hypermarkets

- Pharmacies/Drug Stores

- Online Retail

- Specialty Stores

- Others (Convenience stores, dental clinics, etc.)

By Region

- Asia Pacific

- Europe

- North America

- Latin America

- The Middle East and Africa