Europe Organic Fertilizers Market Report – Segmented By Source, Crop Type, Form And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) - Industry Analysis Size, Share, Trends, COVID-19 Impact & Growth Forecast From 2024 to 2032

Europe Organic Fertilizers Market Size (2024 to 2032)

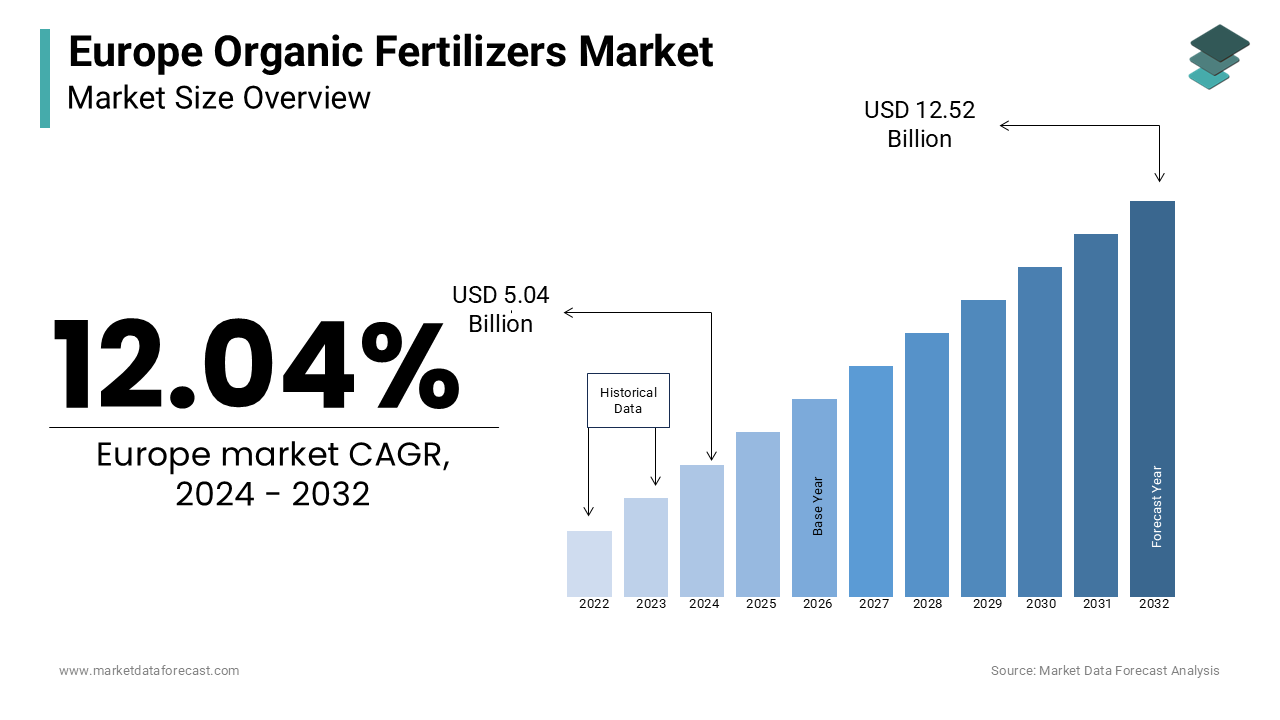

The Europe organic fertilizers market was valued at USD 4.5 billion in 2023 and is anticipated to reach USD 5.04 billion in 2024 from USD 12.52 billion by 2032, growing at a CAGR of 12.04% from 2024 to 2032.

Organic fertilizers are obtained from human or animal waste and vegetable matter. Naturally occurring organic fertilizers contain animal matter from peats, slurries, and various industries. As fertilizers are obtained naturally, there is a low risk of environmental damage. Organic fertilizers also reduce the risk of diseases in humans. The most commonly used organic fertilizers available in the market include blood meal, bone meal, composites, earthworm castings, bat guano, fish emulsion, and rock phosphate.

As people are becoming more conscious about their health, there has been an increase in the demand for organic and green products. There has been a major development in organic agriculture, along with an increase in the demand for organic food products, making it a major driver of this market. The market has been growing at a steady rate because of government support and farmers switching to these fertilizers. Organic fertilizers are more efficient and cheaper than chemical fertilizers. Due to the government’s various policies regarding pollution and non-biodegradable items, there has been a rise in the production of organic fertilizers. However, the market is dependent upon the weather. Hence, weather conditions can hamper the growth of the organic fertilizer market. The majority of organic fertilizers have a lesser nutrient ratio than chemical fertilizers, which can massively impact farm produce.

This market research report on the Europe organic fertilizers market is segmented and sub-segmented into the following categories.

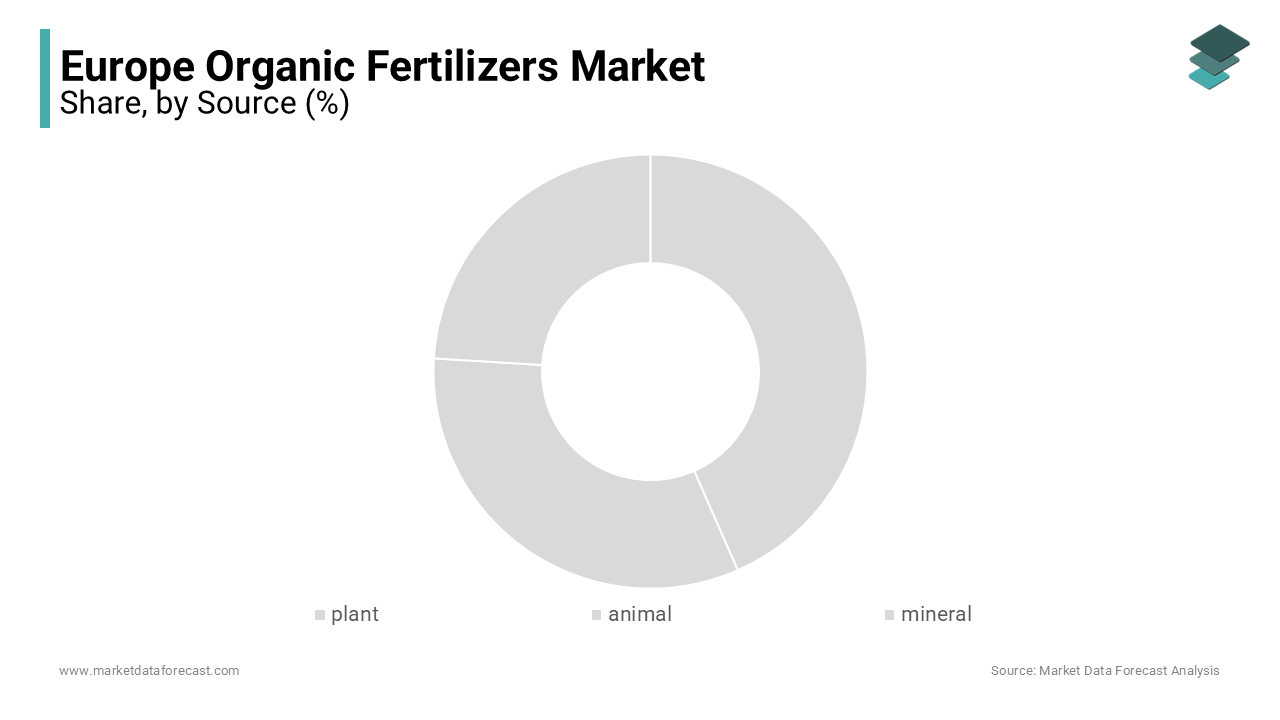

Europe Organic Fertilizers Market Analysis By Source

- plant

- animal

- mineral

The animal based segment accounted for the largest share in the market. Further, the blood meal segment holds a major share in the animal based fertilizer market.

Europe Organic Fertilizers Market Analysis By Crop Type

- cereals and grains

- oilseeds& pulses

- fruits& vegetables

Fruits & Vegetables market is expected to grow at the highest CAGR. This is mainly because of the importance of fruits and vegetables and it being irreplaceable. Moreover they are highly perishable as compared to cereals.

Europe Organic Fertilizers Market Analysis By Form

- dry

- liquid

Liquid fertilizers are projected to dominate the market during the forecast period. They are more effective and economical when compared to the dry fertilizers.

COUNTRY ANALYSIS

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

On the basis of geography, the European market is analyzed under various regions, namely U.K., Italy, Germany, France, and Spain. Europe dominates the global market for organic fertilizers.

KEY PLAYERS IN THE EUROPE ORGANIC FERTILIZERS MARKET

The key players in the market include Tata Chemicals Ltd (India), The Scotts Miracle-Gro Company (U.S.), Coromandel International Limited (India), National Fertilizers Limited (India) and Krishak Bharati Cooperative Limited (India). Other significant players include Midwestern BioAg (U.S.), Italpollina SpA (Italy), and ILSA S.p.A (Italy), Perfect Blend, LLC (U.S.), and Sustane Natural Fertilizer, Inc. (U.S.).

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]