- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

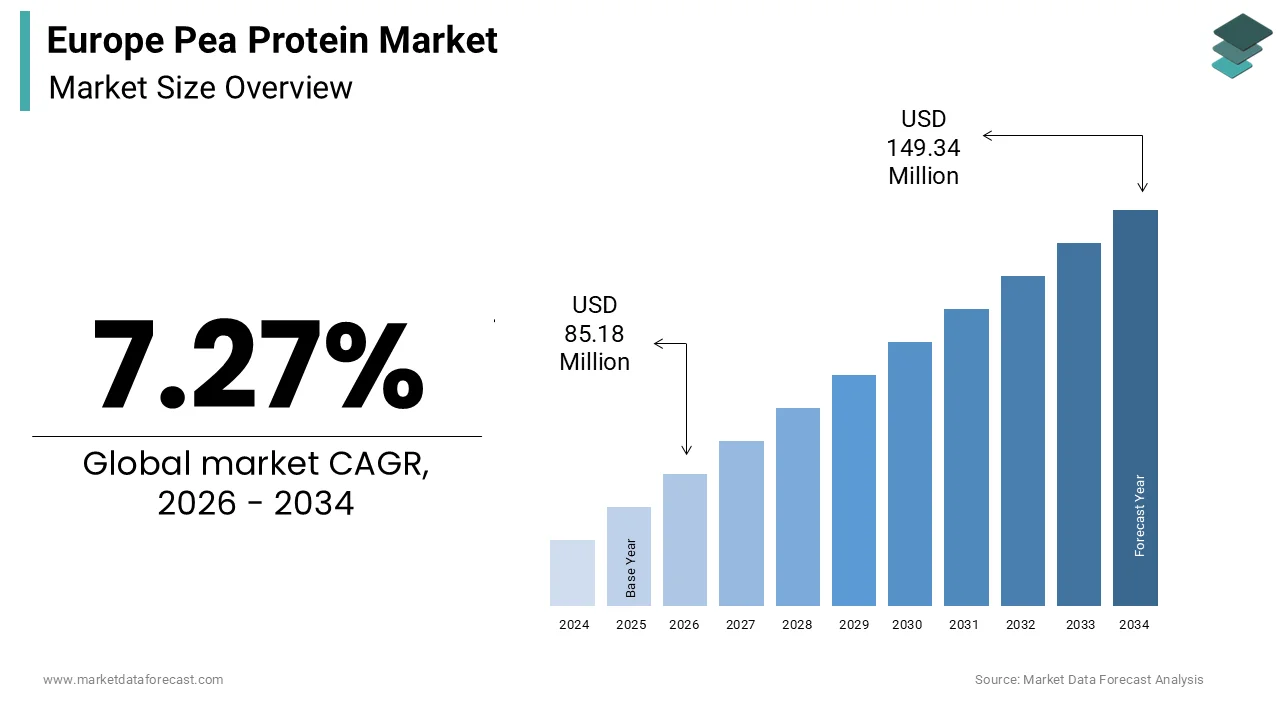

Market Size, 2025

$79.41 MnMarket Estimate, 2026

$85.18 MnMarket Forecast, 2034

$149.34 MnCAGR, 2026–2034

7.27%Europe Pea Protein Market Size

The Europe Pea Protein Market size was calculated to be USD 79.41 million in 2025 and is anticipated to be worth USD 149.34 million by 2034, from USD 85.18 million in 2026, growing at a CAGR of 7.27% during the forecast period.

Pea protein, derived primarily from yellow split peas (Pisum sativum), is a plant-based protein isolate or concentrate widely used in food, beverage, and nutritional formulations across Europe due to its high digestibility, neutral flavor, and allergen-free profile. Unlike soy or dairy proteins, pea protein is non-GMO compliant by default and suitable for vegan, vegetarian, and clean label products, aligning with evolving European consumer preferences. The European Union’s Farm to Fork Strategy actively encourages the cultivation of legumes like peas to reduce synthetic nitrogen dependency and enhance protein self-sufficiency. There has been a noticeable expansion in the land area dedicated to the cultivation of peas across the region. The shift toward increasing pea production reflects an evolving landscape in agricultural land use, influenced by regional policy frameworks that encourage environmentally conscious farming practices. The European Food Safety Authority recognizes pea protein as a safe novel food ingredient, and its inclusion in meat analogs, sports nutrition, and clinical diets continues to grow. As sustainability, health consciousness, and protein diversification converge, pea protein has emerged as a cornerstone of Europe’s alternative protein transition.

MARKET DRIVERS

Rising Consumer Shift Toward Plant-Based and Clean Label Diets

European consumers are increasingly rejecting animal-derived ingredients in favor of transparent, sustainable, and plant-based alternatives, which directly accelerates the growth of the Europe pea protein market. Consumers are increasingly seeking protein from plant-based sources. Specific plant-based options, like pea protein, are viewed positively due to simple processing and perceived non-GMO status. There is a growing preference for foods with short, recognizable ingredient lists. This shift in consumer preference is evident across multiple markets, contributing to significant growth in sales of plant-based meat and dairy alternatives. Major food brands, including Nestlé, Unilever, and Oatly, have reformulated products to feature pea protein as a primary ingredient to meet clean label and vegan certification standards. Additionally, as per sources, millions of Europeans now identify as flexitarian, creating sustained demand for versatile, neutral-tasting proteins that integrate seamlessly into mainstream food formats without allergen or ethical concerns.

EU Policy Support for Legume Cultivation and Protein Autonomy

The European Union’s strategic push for agricultural diversification and reduced soy import dependency has created a favorable policy ecosystem for domestic pea protein production. This further boosts the expansion of the Europe pea protein market. A region relies significantly on external sources for its protein feed, introducing potential vulnerabilities in both sourcing and environmental considerations. A strategic initiative encourages local farmers to incorporate specific protein-rich crops into their regular planting schedules. Cultivating these crops enriches the soil naturally, which can lead to a decrease in the application of manufactured soil nutrients in subsequent plantings. Several individual nations within the region have created their own initiatives aimed at fostering local protein crop production and processing infrastructure. Projections suggest a potential substantial increase in the processing volume of domestically grown protein crops if current supportive measures continue. This institutional backing not only secures raw material supply but also positions pea protein as a strategic asset in Europe’s food sovereignty agenda.

MARKET RESTRAINTS

Limited Domestic Processing Infrastructure Constrains Supply Scalability

The region lacks sufficient dedicated protein extraction facilities, despite growing pea cultivation, which creates a barrier between farm output and market-ready ingredients, and thereby negatively impacts the growth of the Europe pea protein market. Large-scale processing facilities for pea protein are limited in number and geographically concentrated within a few specific nations. A significant portion of locally grown raw materials is shipped abroad for refinement and subsequently returned as finished isolates, creating a trade loop that contrasts with regional sustainability objectives. The high financial requirements and lengthy administrative timelines necessary for establishing new infrastructure act as barriers to entry for potential investors. The ability to transform raw legumes into functional ingredients is currently not aligned with the total volume of crops produced within the region. Europe's dependence on third-country processors will persist, exposing the pea protein supply chain to logistical inefficiencies and carbon footprint penalties that violate Green Deal principles, until public-private partnerships accelerate infrastructure development.

Sensory and Functional Limitations in Complex Food Matrices

Pea protein, while versatile, presents formulation challenges in applications requiring neutral taste, smooth texture, or high solubility, which limits its use in premium food and beverage categories. This restrains the expansion of the Europe pea protein market. The inherent beany or earthy notes, caused by lipoxygenase enzymes and phenolic compounds, often require costly deodorization or masking agents. Consumer perception studies indicate that pea-based dairy alternative products often face challenges with undesirable aftertaste and texture, which can lead to consumer dissatisfaction. Additionally, pea protein exhibits poor foaming stability and limited gelling capacity compared to egg or whey, complicating its use in baked goods and aerated desserts. Food manufacturers perceive the development of highly suitable, ready-to-drink beverages using pea protein as challenging due to current processing and formulation difficulties. Enzymatic and fermentation technologies are being developed for better functionality, but their high expense and limited scalability are hurdles to widespread adoption. These technical barriers restrict pea protein to simpler applications, slowing its penetration into high-margin segments where consumer expectations for sensory performance are stringent.

MARKET OPPORTUNITIES

Expansion into Clinical and Medical Nutrition Applications

Pea protein is gaining traction in European clinical nutrition due to its high digestibility, hypoallergenic nature, and favorable amino acid profile, particularly its richness in branched chain amino acids, which is expected to drive the growth of the Europe pea protein market. There is a considerable and ongoing need for medical nutrition support for patients across European healthcare settings, a concern frequently highlighted by clinical nutrition experts and societies like ESPEN. Pea protein’s low purine and phosphorus content makes it suitable for kidney disease diets, while its absence of dairy and soy allergens benefits patients with multiple food sensitivities. The use of plant-based protein sources, such as pea protein, is a growing trend in the development of specialized nutritional products, including those for an aging population. A significant portion of the elderly population in Europe is affected by malnutrition, a recognized public health issue across the continent. Leading clinical nutrition companies are seeing increased interest and procurement of plant-based enteral formulas as demand for alternative nutritional support options grows within healthcare facilities. The expanding elderly demographic in Europe, combined with progress in personalized nutrition, suggests that pea protein's clinical applications present a high-value, regulated opportunity beyond the general food market.

Integration with Cellular Agriculture and Hybrid Meat Platforms

Pea protein is emerging as a critical structural and nutritional component in next-generation alternative proteins, particularly hybrid and cultivated meat products developed across the regional innovation hubs, which provides fresh prospects for the expansion of the Europe pea protein market. The alternative protein industry is seeing significant interest in plant-based ingredients like pea protein for various applications in both plant-based and hybrid cultivated meat product development. In hybrid meat, combining plant protein with cultivated or fermented animal cells, pea protein provides fibrous texture and moisture retention unattainable with soy alone. The Swiss start-up Mirai Foods and Germany’s Formo use pea protein matrices to enhance the mouthfeel of dairy and meat analogs. The European Institute of Innovation and Technology (EIT) actively provides substantial funding through EIT Food to support research and development initiatives in the alternative protein sector, fostering innovation across Europe. Pea protein, vital for next-gen protein products, aligns perfectly with the EU's new novel food framework, bridging sustainability, food security, and food tech advancements.

MARKET CHALLENGES

Price Volatility Due to Competition with Animal Feed Demand

A significant portion of the region’s yellow pea harvest is diverted to animal feed markets, which creates direct competition that inflates prices and destabilizes supply for human food-grade protein, and thereby impedes the growth of the Europe pea protein market. A significant volume of field peas is utilized within the animal feed production sector, particularly for poultry and swine diets. The primary appeal of field peas as a feed ingredient relates to their nutritional composition and their ready local supply. Sudden spikes in demand for feed ingredients result in competitive bidding among various processors, which rapidly increases the cost of raw materials. This intensified market competition can elevate raw material costs for processors by a substantial percentage within a very short timeframe. Instances of drought in major agricultural regions tighten the global supply of key commodities and coincide with notable price increases for alternative protein sources, such as peas, used by food processors. Unlike soy, which has segregated supply chains for food and feed, Europe lacks identity-preserved pea streams, forcing food ingredient makers to compete on open commodity markets. This structural flaw undermines price predictability and deters long term contracts with food manufacturers seeking stable input costs, ultimately slowing product innovation and consumer adoption in price-sensitive categories.

Lack of Standardized Quality and Purity Metrics Across Suppliers

The absence of harmonized specifications for pea protein content, solubility, and anti-nutritional factors across European suppliers creates formulation inconsistency and quality control risks for food manufacturers. This further obstructs the expansion of the Europe pea protein market. Pea protein products show a wide variation in protein concentrations, ranging from lower levels in some products to higher levels in others. Across different products, there are inconsistent levels of compounds such as trypsin inhibitors, phytic acid, and residual starch. A significant portion of pea protein product batches has failed to meet specific quality control benchmarks. These quality control issues have led to operational impacts within manufacturing processes, resulting in production line stoppages or delays in reformulation efforts. Unlike dairy or soy proteins, pea protein lacks EU-wide reference methods for key functional properties. This variability forces brands to conduct extensive batch testing, increasing lead times and costs. The lack of mandatory quality parameters set by the European Committee for Standardization will lead to a fragmented market that obstructs the development of trust and scalability for industrial food applications.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.27% |

| Segments Covered | By Type, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | A&B Ingredients, Roquette Freres, Shandong Jianyuan Foods Co., Ltd, Axiom Foods Inc, Farbest Brands, The Scoular Company, Nutri-Pea Ltd, Consucra-Groupe Warcoing, Sotexpro, Tai Shuang Ta Food Co, AGT Foods, Burcon NutraScience Ltd, ET-Chem, Kerry Inc, and Batory Foods |

SEGMENTAL ANALYSIS

By Type Insights

The pea protein isolate segment held the largest share of 47.6% of the Europe Pea Protein Market in 2025. The supremacy of the pea protein isolate segment is attributed to its superior protein concentration, making it ideal for high protein formulations where purity and functionality are critical. Isolates undergo additional purification steps to remove starch and fiber, resulting in a neutral flavor and improved solubility compared to concentrates. There is a pattern of widespread adoption of a specific plant-based protein in the sports nutrition sector across several European regions. This ingredient is frequently used as a primary component in new product formulations in certain markets, and its selection is influenced by digestibility scores, with preferences shown for those comparable to traditional animal-based proteins. Product development trends indicate a strong preference for ingredients that offer a complete amino acid profile, and on-pack messaging regarding protein content is aligned with established regulatory criteria, influencing how products are marketed to consumers. Food manufacturers also favor isolates for clean label compliance, as they avoid the beany off notes and grittiness associated with lower-grade concentrates. This combination of nutritional efficacy, regulatory validation, and sensory performance solidifies isolate as the preferred form for premium food, beverage, and clinical applications across Europe.

The textured pea protein segment is expected to exhibit a noteworthy CAGR of 12.3% from 2026 to 2034 due toits unique fibrous structure that closely mimics the chew and mouthfeel of meat, making it indispensable in next-generation meat analogs. Unlike isolates and concentrates, textured pea protein undergoes extrusion cooking that aligns protein strands into a meat-like matrix, enabling use in whole cut alternatives such as chicken breasts and steak strips. The plant-based sector is showing a preference for using legume-based proteins in new products. This trend indicates a move away from traditional grain and legume bases toward options addressing dietary sensitivities and cultivation issues. Large food producers are working with processing specialists to improve manufacturing methods for meat alternatives, specifically utilizing advancements in extrusion to enhance product consistency and moisture retention. Regulatory updates have also eased the process for certain plant proteins to reach the market, contributing to a more efficient transition from development to availability. Textured pea protein is emerging as the foundational element for Europe's growing alternative meat sector, meeting rising consumer demand for meat-like products and clearer regulatory frameworks.

By Application Insights

The meat substitutes dominated the Europe Pea Protein Market by capturing a 38.1% share in 2025. The leading position of the meat substitutes segment is fueled by the rapid expansion of plant-based meat products across retail and food service channels, driven by climate-conscious consumers and policy support for protein diversification. The European Commission’s Farm to Fork Strategy encourages reduced meat consumption, and national dietary guidelines recommend plant-based proteins as daily staples. Consumer purchases of alternative meat products have shown a consistent upward trend. A specific plant-derived protein has become a primary ingredient in a significant majority of recently developed items due to its allergen-free status and binding properties. Producers incorporate this ingredient into various products to mimic traditional animal-based taste and consistency, which also enables manufacturers to list simpler, more transparent components, addressing growing consumer preferences for products free of common allergens. This convergence of public health, environmental, and sensory drivers ensures that meat substitutes remain the primary growth engine for pea protein in Europe.

The Food and Beverages segment is predicted to witness the highest CAGR of 11.8% during the forecast period, owing to the integration of pea protein into mainstream categories beyond niche health products, including ready-to-drink shakes, dairy alternatives, breakfast cereals, and even alcoholic beverages. There has been a noticeable rise in the sales of yogurt alternatives made from plants. Manufacturers are combining various plant-based elements to enhance the nutritional value and texture of these goods. Besides, prominent beverage firms have begun testing the inclusion of plant-based protein in select lower-alcohol drink varieties, seemingly targeting consumers focused on wellness. Crucially, advances in enzymatic debittering and microfluidization have significantly improved solubility and reduced sedimentation, key barriers in liquid applications. European food manufacturers, focusing on functional nutrition and clean labels, are increasingly adopting pea protein for mass market products due to its versatility.

REGIONAL ANALYSIS

Germany Pea Protein Market Analysis

Germany led the Europe Pea Protein Market by holding a 21.4% share in 2025. The dominance of the German market is driven by a mature alternative protein ecosystem, strong consumer adoption, and a dense network of food tech manufacturers. A substantial portion of the German population has integrated plant-based alternatives into their routine shopping habits. Consumer interest in these products is often influenced by considerations regarding the environment and the treatment of animals. The domestic market is supported by established food producers and a developing infrastructure for ingredient processing. National policy initiatives are directed toward increasing the capacity for processing locally grown legumes. The expansion of regional extraction facilities suggests a shift toward enhancing the supply chain for plant-derived proteins. Additionally, Germany’s strict clean label standards, prohibiting artificial additives in many categories, favor natural ingredients like pea protein. This blend of consumer demand, industrial capacity, and policy support makes Germany the undisputed innovation and volume hub for pea protein in Europe.

France Pea Protein Market Analysis

France was the next prominent player in the Europe pea protein market by capturing a 18.7% share in 2025. The growth of the French market is credited to its role as the EU’s largest pea producer and the driving force behind Europe’s protein autonomy agenda. France has a significant area dedicated to field pea cultivation and is a major producer within the European Union. The French government has a national strategy in place to boost the country's plant protein production and reduce import dependency, which includes a range of financial support measures and aid for various stages of the supply chain, from farmers to processing industries. Companies like Roquette and Tereos operate world-class pea protein facilities in Picardy and Champagne, supplying both domestic and export markets. French public institutions are legally required to offer at least one vegetarian meal option per week in their canteens. Furthermore, France’s consumer base is highly receptive. This alignment of agricultural output, industrial processing, public procurement, and cultural shift establishes France as Europe’s most vertically integrated pea protein market.

United Kingdom Pea Protein Market Analysis

The United Kingdom witnessed consistent growth in the Europe Pea Protein Market. Its influence arises from a dynamic retail landscape, strong flexitarian trends, and aggressive product reformulation by major brands. Most major UK grocery retailers have established significant floor space for meat alternatives, reflecting a permanent shift in how supermarkets organize their protein categories to accommodate changing consumer habits. Pea protein has become a staple ingredient in a vast array of new food products, from convenient ready-to-eat meals to portable snacks, as manufacturers favor its nutritional profile and versatility. Leading food technology firms are increasingly incorporating plant-derived proteins into their recipes to create "clean label" products that satisfy consumer preferences for simple, allergen-friendly ingredients. Influential national dietary recommendations and sustainability reports are encouraging a transition toward plant-heavy diets, prompting top-tier supermarkets to publicly commit to broadening their selection of animal-free protein sources. Additionally, the UK’s post Brexit regulatory flexibility has enabled faster novel food approvals for textured pea proteins. The UK's blend of informed consumers and pioneering retail strategies positions it as a key market for validating and rolling out new pea protein innovations throughout Europe.

Netherlands Pea Protein Market Analysis

The Netherlands is also a key player in the Europe Pea Protein Market due to its concentration of food tech startups, research institutions, and export-oriented processing infrastructure. The Netherlands is home to The Vegetarian Butcher (owned by Unilever) and numerous alternative protein incubators like ProVeg and the Brightlands Campus, which pilot next-generation pea protein applications. The country imports yellow peas from across the EU but adds high value through extrusion and fermentation technologies before exporting finished ingredients globally. The Netherlands also leads in hybrid meat development, with companies using pea protein as a scaffold for cultivated meat. Supported by the national roadmap and world-class logistics via the Port of Rotterdam, the Netherlands functions as Europe’s innovation gateway and distribution nexus for advanced pea protein solutions.

Sweden Pea Protein Market Analysis

Sweden is likely to expand in the Europe Pea Protein Market from 2026 to 2034 owing to stringent climate policies, public sector leadership, and high consumer environmental consciousness. Sweden’s National Food Agency mandates that all public institutions, including schools and hospitals, follow climate-labeled meal guidelines that prioritize plant-based proteins, generating steady institutional demand. A majority of people in the country observe flexible dietary habits that incorporate elements of both plant-based and conventional eating. One type of plant-based protein ingredient is widely used in both liquid beverages and solid food alternatives offered by various companies. Financial support has been allocated to multiple initial projects focused on creating sustainable processing facilities for this specific plant protein. These facility projects aim to reuse waste materials generated during processing for energy production purposes. Additionally, Sweden’s carbon tax, among the highest globally, makes animal protein comparatively expensive, further incentivizing plant-based alternatives. This policy-driven, sustainability-centered ecosystem positions Sweden as a highly influential, early adopter market that shapes normative standards for pea protein use across Northern Europe.

COMPETITION OVERVIEW

Competition in the Europe Pea Protein Market is characterized by a mix of large agroindustrial cooperatives, specialized ingredient suppliers, and multinational food ingredient companies. The market is highly innovation-driven, with players differentiating through protein functionality, purity, and sustainability credentials rather than price alone. Regulatory alignment with the EU’s protein autonomy and Farm to Fork strategies creates advantages for companies with domestic sourcing and processing capabilities. While French and Belgian firms dominate current capacity competition is intensifying from German, Dutch, and Nordic entrants leveraging food tech expertise. Sensory performance remains a key battleground as brands seek neutral-tasting, highly soluble proteins for mainstream beverages and snacks. The lack of standardized quality metrics allows premium players to command higher margins through verified purity and clinical validation. Overall, the market rewards those who combine agricultural integration, technical innovation, and strong ESG narratives to meet the dual demands of industry and eco-conscious consumers.

KEY MARKET PLAYERS

A few major players of the Europe Pea Protein Market include

- A&B Ingredients

- Roquette Freres

- Shandong Jianyuan Foods Co., Ltd

- Axiom Foods Inc

- Farbest Brands

- The Scoular Company

- Nutri-Pea Ltd

- Consucra-Groupe Warcoing

- Sotexpro

- Tai Shuang Ta Food Co

- AGT Foods

- Burcon NutraScience Ltd

- ET-Chem

- Kerry Inc

- Batory Foods

Top strategies used by the key market participants

Key players in the Europe Pea Protein Market focus on vertical integration by securing direct contracts with pea farmers to ensure non-GMO and traceable raw material supply. They invest in proprietary processing technologies such as enzymatic debittering, high moisture extrusion, and microfluidization to improve solubility, texture, and sensory profile. Companies actively collaborate with food manufacturers to co-develop clean-label and allergen-free formulations for meat analogs and beverages. Strategic expansion of production capacity through new extraction and texturization facilities addresses growing demand and reduces import dependency. Additionally, firms emphasize sustainability certification,s circular water use, and carbon footprint reduction to align with EU Green Deal principles and retailer procurement standards.

Leading Players in the Market

- Roquette Frères is a French global leader in plant-based ingredients with a pioneering role in the Europe Pea Protein Market through its NUTRALYS® pea protein portfolio. The company operates one of the world’s largest pea protein production facilities in France, supplying isolates, concentrates, and textured formats to food and beverage, and nutrition companies across numerous countries. Roquette has strengthened its position by investing in proprietary enzymatic and texturization technologies that enhance solubility and meat like fiber structure. Its commitment to sustainable agriculture and traceable supply chains aligns with European regulatory and consumer expectations, reinforcing its leadership in both regional and global plant protein markets.

- Tereos is a major European agroindustrial cooperative with significant pea protein production capacity across France and Germany. The company leverages its integrated farm-to-factory model to secure a non-GMO yellow pea supply and produce food-grade protein isolates and concentrates for meat analogs, sports nutrition, and dairy alternatives. Tereos has reinforced its market presence by expanding its extrusion capabilities to develop textured pea protein with improved sensory properties. Tereos combines its broad agricultural reach with specialized knowledge to develop European plant proteins, aiding EU self-sufficiency and satisfying international demand for local sources.

- Cosucra Groupe Warcoing is a Belgian-based specialist in legume and chicory processing with a long-standing footprint in the Europe Pea Protein Market under its WILD-branded ingredients. The company produces non-GMO pea protein isolates and flours known for neutral taste and high digestibility, primarily used in clinical nutrition,n bakery, and plant-based meat applications. Cosucra has enhanced its competitiveness by implementing water recycling and zero-waste biorefinery processes at its Warcoing facility, reducing its environmental footprint per kilogram of protein. Its focus on nutritional science, sustainability, and premium quality enables Cosucra to serve high-value segments across Europe and export markets.

MARKET SEGMENTATION

This research report on the Europe pea protein market has been segmented and sub-segmented based on type, application, and region.

By Type

- Concentrated

- Isolated

- Textured

By Application

- Snacks & bakery products

- Meat extenders

- Meat substitute

- Food & beverages

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe