Europe Reusable Water Bottle Market Size, Share, Trends & Growth Forecast Report, By Material (Plastic, Stainless Steel, Glass), Distribution Channel, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis From (2025 To 2033)

Europe Reusable Water Bottle Market Size

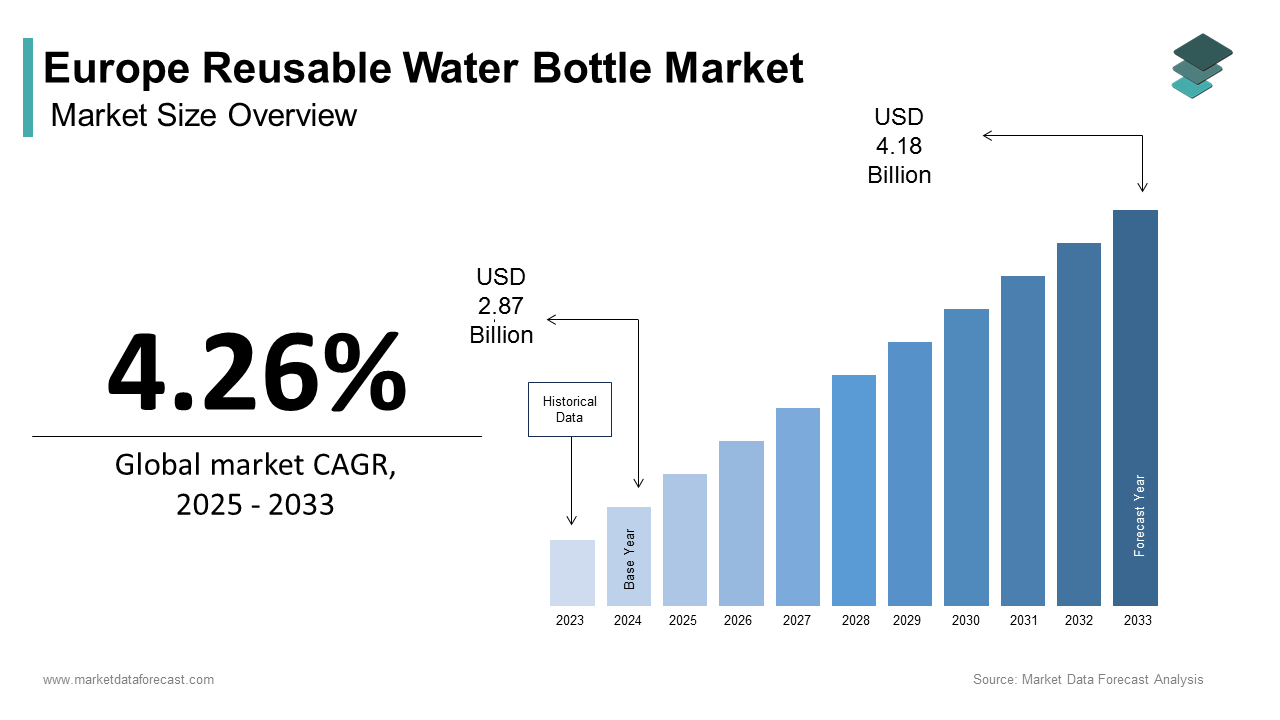

The Europe reusable water bottle market size was calculated to be USD 2.87 billion in 2024 and is anticipated to be worth USD 4.18 billion by 2033, from USD 3 billion in 2025, growing at a CAGR of 4.26% during the forecast period.

A reusable water bottle refers to a refillable container intended for repeated use, primarily constructed from stainless steel, glass, aluminum, and BPA-free plastics. These products serve as environmentally and health-conscious alternatives to single-use plastic bottles, reflecting broader societal shifts toward sustainability and wellness. The market spans diverse user groups, including commuters, students, athletes, and eco-aware households. Europe’s robust regulatory stance against plastic pollution, most notably through the EU Single Use Plastics Directive, has accelerated behavioral and infrastructural changes that favor reusable hydration solutions. According to Eurostat, Europeans generated approximately 16.16 million metric tons of plastic packaging waste in the EU in 2022, with 40.7% effectively recycled. According to the United Nations Environment Program (UNEP) and various global assessments, an estimated 19 to 23 million tonnes of plastic waste leak into aquatic ecosystems (lakes, rivers, and oceans) every year. These systemic waste challenges have caused institutional and individual demand for durable, non-disposable alternatives, which positions reusable water bottles as a cornerstone of Europe’s circular economy ambitions.

MARKET DRIVERS

Rising Environmental Awareness and Anti-Plastic Legislation Are Causing Consumer Shifts

Environmental consciousness among European citizens has become a decisive factor in daily consumption choices, which fuels the growth of the Europe reusable water bottle market. Public sentiment is strongly aligned with waste reduction. According to a 2024 Eurobarometer survey, 87 percent of EU residents are worried about the impact of plastic products on the environment, indicating high public concern. This public mandate is reinforced by binding policy instruments, particularly the EU Single Use Plastics Directive, which requires member states to achieve a 90 percent separate collection rate for plastic bottles by 2029. National implementations have gone further. Germany’s deposit return system has already attained a 98 percent PET bottle return rate, as per the German Environment Agency. Urban infrastructure is also evolving. These coordinated efforts in policy, infrastructure, and civic engagement create a self-reinforcing ecosystem that drives consistent demand for reusable bottles across the region.

Health and Wellness Trends Are Reinforcing Preference for Non-Toxic Hydration Solutions

The shaping of consumer preferences toward inert and non-leaching materials such as stainless steel and borosilicate glass due to health motivations bolsters the expansion of the Europe reusable water bottle market. Growing awareness of endocrine-disrupting chemicals like bisphenol A has led to heightened scrutiny of plastic containers. The European Food Safety Authority continues to flag chemical migration from food contact materials as a public health priority. Concurrently, Europe’s thriving fitness culture amplifies this trend. As per sources, a share of adults in Nordic countries engage in regular physical activity, often carrying reusable bottles during exercise. The European Center for Disease Prevention and Control further emphasizes the role of adequate hydration in immune function, which indirectly promotes consistent water intake through clean, personal vessels. This convergence of preventive health behavior and material safety awareness sustains robust, long-term demand for high-integrity reusable bottles.

MARKET RESTRAINTS

Fragmented Regulatory Standards Across Member States Hinder Product Uniformity

National disparities in regulations governing food contact materials, labeling, and recyclability claims create obstacles for the European reusable water bottle market. France’s Anti Waste Law mandates detailed material traceability, while Germany enforces stringent LFGB standards that restrict certain silicone components permitted elsewhere. This regulatory patchwork increases compliance costs for small and medium enterprises targeting multiple markets. Consumer confusion is equally problematic. A lack of common testing and labeling rules inhibits brands from ensuring consistency across products, results in market entry delays, and jeopardizes consumer trust, which hinders both innovation and the ability to scale operations.

Persistent Consumer Reliance on Convenience and Single-Use Habits Limits Adoption

Convenience remains a restraint to widespread reusable bottle adoption, especially in high mobility contexts such as tourism and commuting, which in turn affects the expansion of the Europe reusable water bottle market. Single-use plastic bottles are ubiquitously available at lower price points in airports, train stations, and convenience stores. According to research, a portion of adults in Southern Europe continue to purchase disposable bottles weekly, citing hygiene and portability as key reasons. As per sources, millions of international tourist arrivals in 2023, many are unfamiliar with local refill options. Even environmentally conscious individuals exhibit situational relapse. Critically, public hydration infrastructure remains underdeveloped. Few European municipalities offer accessible refill points in high traffic zones, as per sources. Market penetration will be constrained by consumer inertia until the new offering is just as convenient as current alternatives.

MARKET OPPORTUNITIES

Integration with Smart Technology Presents a High-Growth Innovation Frontier

The fusion of reusable bottles with digital health technology is creating a premium and high-engagement product segment that drives the growth of the Europe reusable water bottle market. Smart bottles featuring hydration sensors, Bluetooth connectivity, and app integration are gaining traction among health-focused consumers. According to a study, sales of connected hydration devices grew year on year. These products sync with platforms, enabling users to track intake against personalized goals. Brands offer models with LED reminders and temperature monitoring, commanding premium pricing. Corporate wellness programs are further accelerating B2B demand. This intersection of sustainability, personalization, and digital health represents a high-margin growth vector.

Expansion of Refill Infrastructure Through Public-Private Partnerships Fuels Usage Frequency

Strategic investments in public drinking water refill networks are transforming reusable bottles from symbolic gestures into practical daily tools, which opens new opportunities for the Europe reusable water bottle market. Municipalities across Europe are collaborating with NGOs and private sponsors to install hygienic and accessible refill stations. Berlin’s Urban Development Department reported the installation of new stations in 2024. Similarly, expansions are underway in Vienna and Helsinki. The number of cities integrating refill infrastructure into their climate strategies is growing. In addition, the number of refill locations globally is increasing significantly due to the Refill campaign and similar initiatives. Tourist authorities are also engaged. This infrastructure not only encourages initial purchase but also increases reuse frequency, which broadens appeal beyond eco activists to mainstream users who prioritize convenience alongside sustainability.

MARKET CHALLENGES

Material Sourcing Volatility and Supply Chain Fragility Threaten Cost Stability

Mounting burden from volatile input costs and fragile supply chains for critical raw materials impedes the growth of the Europe reusable water bottle market. Stainless steel—used in over 60 percent of premium bottles—has seen significant price swings due to energy costs and reduced European production. According to research, stainless steel, a popular material for reusable bottles, has seen significant price swings due to factors like energy costs and supply chain disruptions, which have impacted European production. Glass manufacturing costs also climbed, driven by natural gas dependency and EU carbon pricing. Apart from these, Europe imports a share of its specialty glass and high-purity metals, exposing the sector to geopolitical and logistical risks. Silicone components, often sourced from Southeast Asia, add another layer of supply vulnerability. These cost pressures force mid-tier brands into difficult pricing decisions, which potentially dampens consumer demand and squeezes margins. Manufacturers face ongoing risks to production and price stability unless they develop local material innovations or secure strategic reserves.

Greenwashing Accusations and Lack of Transparent Certification Erode Consumer Trust

The absence of standardized and verifiable sustainability credentials has led to widespread consumer skepticism, which hinders the expansion of the Europe reusable water bottle market. Many brands use unregulated terms like “eco-friendly” or “recyclable” without third-party validation. Many green claims in the home goods category lacked substantiating evidence. Compounding the issue, multi-material bottles, common in the market, are often not fully recyclable due to composite construction. A lesser share of such bottles can be processed in existing municipal systems. Mandatory transparency mechanisms, such as the forthcoming EU Digital Product Passport under the Ecodesign for Sustainable Products Regulation, are essential for consumers to reliably distinguish ethical products. This trust deficit suppresses conversion, disincentivizes genuine sustainability investment, and allows misleading marketing to dilute the value of authentic eco innovation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.26% |

| Segments Covered | By Material, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | SIGG Switzerland AG, Tupperware Brands Corporation, CamelBak Products LLC, Klean Kanteen Inc., Thermos LLC, Contigo, 24Bottles, Chilly’s Bottles |

SEGMENTAL ANALYSIS

By Material Insights

The stainless-steel segment dominated the Europe reusable water bottle market by accounting for 48.2% share in 2024. Its durability, thermal insulation properties, and perceived safety have significantly propelled the growth of the stainless-steel segment. Consumers increasingly favor stainless steel for its resistance to chemical leaching and compatibility with both hot and cold beverages. A portion of reusable bottle purchasers selected stainless steel as their primary material due to concerns over plastic toxicity and glass fragility, as per studies. The material’s recyclability further aligns with circular economy goals. As per research, a notable share of stainless-steel products in Europe is recovered and recycled at the end of life and far exceeding rates for multi-layer plastics. Apart from these, brands have invested heavily in double-wall vacuum insulation technology, enhancing product performance and justifying premium pricing. Regulatory tailwinds also support adoption. These combined attributes of safety, functionality, and sustainability have cemented stainless steel as the material of choice for mainstream and premium segments alike.

The glass segment is anticipated to witness the fastest CAGR of 9.7% from 2025 to 2033 due to rising demand for chemical-free and aesthetically refined hydration solutions. Health-conscious consumers, particularly in urban centers, are gravitating toward borosilicate glass for its inert nature and transparency, which allows visual verification of cleanliness. According to sources, sales of reusable glass bottles increased, driven by wellness influencers and clean label movements. The material’s compatibility with stringent food safety standards further bolsters its appeal. Moreover, premium lifestyle retailers have dedicated shelf space to designer glass bottles, signaling cultural acceptance beyond functional utility. Startups have leveraged silicone sleeves to address breakage concerns, which improves practicality without compromising purity. The evolving sustainability narrative, which now highlights inherent material integrity as much as recyclability, is driving a faster move to glass packaging among conscious European consumers.

By Distribution Channel Insights

The supermarkets and hypermarkets segment led the Europe reusable water bottle market by capturing 42.5% share in 2024. Factors such as high foot traffic, established consumer trust, and bundled retail strategies are propelling the growth of the supermarkets and hypermarkets segment. Major chains integrate reusable bottles into broader sustainability initiatives, which often place them alongside organic groceries or eco cleaning products to reinforce green shopping behavior. Private label offerings have also expanded. Furthermore, in-store promotions tied to plastic reduction campaigns have boosted visibility and trial. As per research, a notable share of European households shop at hypermarkets at least once weekly by ensuring consistent exposure. This combination of accessibility, affordability, and contextual marketing sustains the channel’s leadership despite digital disruption.

The online retail segment is likely to experience the fastest CAGR of 12.3% during the forecast period, owing to digital adoption, personalized shopping experiences, and direct-to-consumer brand strategies. E-commerce platforms enable niche players to bypass traditional gatekeepers and reach environmentally conscious demographics with targeted messaging. According to sources, online sales of reusable bottles grew, with Germany, the UK, and Sweden accounting for a portion of transactions. Direct-to-consumer brands leverage social media, influencer collaborations, and subscription models to drive repeat purchases and community engagement. Amazon’s Climate Pledge Friendly badge has also increased discoverability. Apart from these, online channels facilitate detailed product storytelling, emphasizing material sourcing, carbon footprint, and design innovation, which resonates with informed buyers. Hence, the digital channel is poised to capture an expanding share of value-driven and convenience-oriented consumers alike.

REGIONAL ANALYSIS

Germany Reusable Water Bottle Market Analysis

Germany outperformed other regions in the Europe reusable water bottle market by occupying 19.5% share in 2024. The domination of Germany is attributed to its strong environmental policy framework, high consumer awareness, and advanced retail infrastructure. The country’s early adoption of the EU Single Use Plastics Directive and nationwide deposit return system for PET bottles has cultivated a culture of reuse. According to research, a share of single-use plastic bottles are returned for recycling, which creates a behavioral foundation for reusable alternatives. Domestic brands benefit from local manufacturing and stringent quality expectations. Urban centers have installed public water refill stations combined. Furthermore, corporate sustainability mandates, driven by Germany’s Supply Chain Due Diligence Act, have led companies to distribute branded reusable bottles to employees. This ecosystem of regulation, infrastructure, and consumer trust solidifies Germany’s leadership position.

United Kingdom Reusable Water Bottle Market

The United Kingdom was the second-largest player in the Europe reusable water bottle market by capturing 16.2% share in 2024. Robust environmental activism, government-backed initiatives, and high digital engagement have contributed to the expansion of the UK. The UK’s Refill campaign, launched by City to Sea, has mapped thousands of public water stations nationwide, as per sources, which makes on-the-go refills widely accessible. According to research, a notable share of British adults report regularly using a reusable bottle, up from that in 2019. Retailers have amplified adoption. Tesco and Sainsbury’s removed single-use bottled water from checkout aisles to discourage impulse plastic purchases. The UK also leads in direct-to-consumer innovation. Brands leverage storytelling around ocean plastic recovery to drive emotional connection. Despite Brexit-related supply chain adjustments, the market remains dynamic due to strong civic environmentalism and agile brand ecosystems.

France Reusable Water Bottle Market Analysis

France is an attractive region in the European reusable water bottle landscape due to aggressive anti-waste legislation and cultural emphasis on quality of life. The country’s Anti Waste and Circular Economy Law, enacted in 2020, bans the destruction of unsold non-food goods and mandates extended producer responsibility, accelerating brand investment in durable products. According to sources, reusable bottle ownership increased, with Paris installing public fountains. French consumers exhibit a strong preference for design-led products. Brands have gained traction through collaborations with fashion and lifestyle retailers such as Merci and Colette. Apart from these, school and university sustainability programs distribute branded bottles to students, embedding reuse habits early. These policies, aesthetic, and educational drivers sustain France’s prominent market position.

Italy Reusable Water Bottle Market Analysis

Italy is growing moderately in the Europe reusable water bottle market, with growing environmental awareness and regional policy divergence. While national legislation lags behind Northern Europe, cities like Milan and Bologna have pioneered local bans on single-use plastics in public events and municipal buildings. According to sources, a share of residents in northern regions reported using reusable bottles weekly in 2024, compared to that in the south, which emphasizes an urban-rural adoption gap. The fashion and design sector plays a unique role. Italian brands partner with luxury houses like Gucci for limited editions, which merge sustainability with style. Furthermore, Italy’s high bottled water consumption creates a natural transition opportunity toward refillable alternatives. National penetration is expected to rise as southern regions modernize their waste infrastructure.

Netherlands Reusable Water Bottle Market Analysis

The Netherlands is predicted to grow in the Europe reusable water bottle market during the forecast period, owing to its integrated sustainability infrastructure and high civic participation. Dutch cities lead in public hydration access. Amsterdam and Rotterdam together operate a number of free refill stations. The country’s strong cycling culture further amplifies demand, as commuters seek lightweight and leak-proof designs compatible with bike bottle cages. Brands have achieved global recognition by donating a share of profits to clean water projects, resonating with socially conscious buyers. This combination of infrastructure, behavioral norms, and ethical branding ensures the Netherlands remains a high-intensity market despite its modest population size.

COMPETITION OVERVIEW

The Europe reusable water bottle market features intense competition among international brands, regional specialists, and mission-driven startups. Established players leverage brand heritage, technological innovation, and extensive distribution networks to maintain relevance, while newer entrants differentiate through sustainability credentials, circular design, and community engagement. The absence of dominant monopolies encourages constant product evolution with companies racing to offer superior insulation, lightweight construction, and eco-friendly materials. Price competition is moderate as consumers often prioritize quality and value over cost alone. Regulatory alignment with EU directives serves as both a barrier and an opportunity, shaping entry strategies. Digital channels amplify brand narrative, allowing even small players to gain visibility through targeted campaigns. Collaborations with cities, NGOs, and retailers further blur the lines between commerce and activism. This multifaceted competitive environment fosters rapid innovation but demands authenticity, transparency, and adaptability from all participants to sustain long-term market presence.

KEY MARKET PLAYERS

A few major key market players of the Europe reusable water bottle market include

- SIGG Switzerland AG

- Tupperware Brands Corporation

- CamelBak Products LLC

- Klean Kanteen Inc

- Thermos LLC

- Contigo

- 24Bottles

- Chilly’s Bottles

Top Strategies Used by the Key Market Participants

Key players in the Europe reusable water bottle market employ product differentiation through material innovation and aesthetic customization to capture diverse consumer segments. They invest heavily in sustainability storytelling by highlighting ethical sourcing, recyclability, and carbon footprint reduction. Strategic retail partnerships with supermarkets, specialty stores, and e-commerce platforms ensure broad market access. Many brands collaborate with public institutions to install refill stations, enhancing usability and brand loyalty. Direct-to-consumer engagement via social media influencer campaigns and digital content drives awareness and repeat purchases. Companies also align with EU environmental regulations to position themselves as policy-compliant and socially responsible. Limited edition launches and co-branding with fashion or wellness entities create exclusivity and premium perception. Continuous R and D in insulation technology leak leak-proof mechanisms, and smart features further strengthen the competitive advantage in this dynamic market landscape.

Leading Players in the Market

S’well

S’well has established itself as a prominent name in the Europe reusable water bottle market through its emphasis on design innovation and sustainability. The company blends fashion-forward aesthetics with high-performance vacuum-insulated stainless steel bottles, appealing to urban professionals and style-conscious consumers. It also launched a refill initiative in collaboration with London’s public transport authority to install branded water stations across key transit hubs. These moves reinforce its brand visibility and align with Europe’s anti-plastic policies while strengthening its global reputation as a lifestyle-driven hydration brand.

Hydro Flask

Hydro Flask is recognized across Europe for its advanced TempShield insulation technology that maintains beverage temperature for extended periods. The brand targets outdoor enthusiasts and health-focused consumers through strategic sponsorships of adventure and wellness events in Germany, France, and the Nordic regions. Hydro Flask introduced limited-edition collections inspired by local landscapes and region-specific color palettes as a strategy to enhance its European foothold. It also enhanced its e-commerce logistics network to ensure faster delivery across the continent. These initiatives reflect its commitment to localized engagement and performance-driven product excellence, which also supports its strong position in the global reusable bottle segment.

Dopper

Dopper is a Netherlands-based social enterprise that has significantly influenced the European market through its mission-driven approach. The company donates a portion of its profits to clean water projects and designs bottles that are fully recyclable and made from certified sustainable materials. Dopper actively collaborates with schools, universities, and municipalities across the Netherlands, Belgium, and Germany to promote tap water usage and reduce plastic waste. Its integration of activism, product design, and circular economy principles has earned it widespread recognition and strengthened its role in both the European and global sustainability movements.

MARKET SEGMENTATION

This research report on the Europe reusable water bottle market has been segmented and sub-segmented based on material, distribution channel, and region.

By Material

- Plastic

- Stainless Steel

- Glass

By Distribution Channel

- Supermarkets & Hypermarkets

- Online

- Specialty Stores

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the demand for reusable water bottles in Europe?

Growing environmental awareness, anti-plastic regulations, increased outdoor and fitness activities, and rising demand for sustainable lifestyle products.

2. Which materials are most commonly used for reusable water bottles?

Stainless steel, BPA-free plastic, glass, aluminum, and silicone.

3. What consumer trends are shaping the market?

Eco-friendly lifestyle adoption, preference for BPA-free and insulated bottles, personalized/ designer bottles, and increasing use of bottles for travel, gyms, and offices.

4. Which type of reusable bottle is most popular in Europe?

Stainless steel insulated bottles are durable and have temperature-control properties.

5. What are the major applications for reusable water bottles?

Outdoor activities, fitness & sports, travel, office and school use, and everyday hydration.

6. What role do sustainability policies play in market growth?

Strict EU regulations on single-use plastics and green initiatives significantly boost reusable bottle adoption.

7. Who are the key target consumer groups?

Health-conscious consumers, eco-friendly users, students, fitness enthusiasts, travelers, and corporate buyers.

8. What challenges does the market face?

Competition from low-cost products, fluctuating material prices, and counterfeit/ low-quality imports.

9. What distribution channels are popular for reusable bottles in Europe?

E-commerce, supermarkets, sporting goods stores, lifestyle stores, and brand-owned outlets.

10. What future trends are expected in the Europe reusable water bottle market?

Smart hydration bottles, eco-certified materials, minimalist designs, collapsible bottles, and increased corporate sustainability programs.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com