Europe Frozen Desserts Market Research Report Segmented By Product Type (Sherbet, Frozen Yogurt, Frozen Ice Cream, Frozen Tofu, Frozen Cakes, Mousse, Frozen Novelties), Fat Content (Regular Frozen Desserts, Low Fat Desserts) , Consumption ( Home, Hotel And Restaurants And Dessert Parlors), And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis On Size, Share, Trends & Growth Forecast (2026 To 2034)

Europe Frozen Desserts Market Size

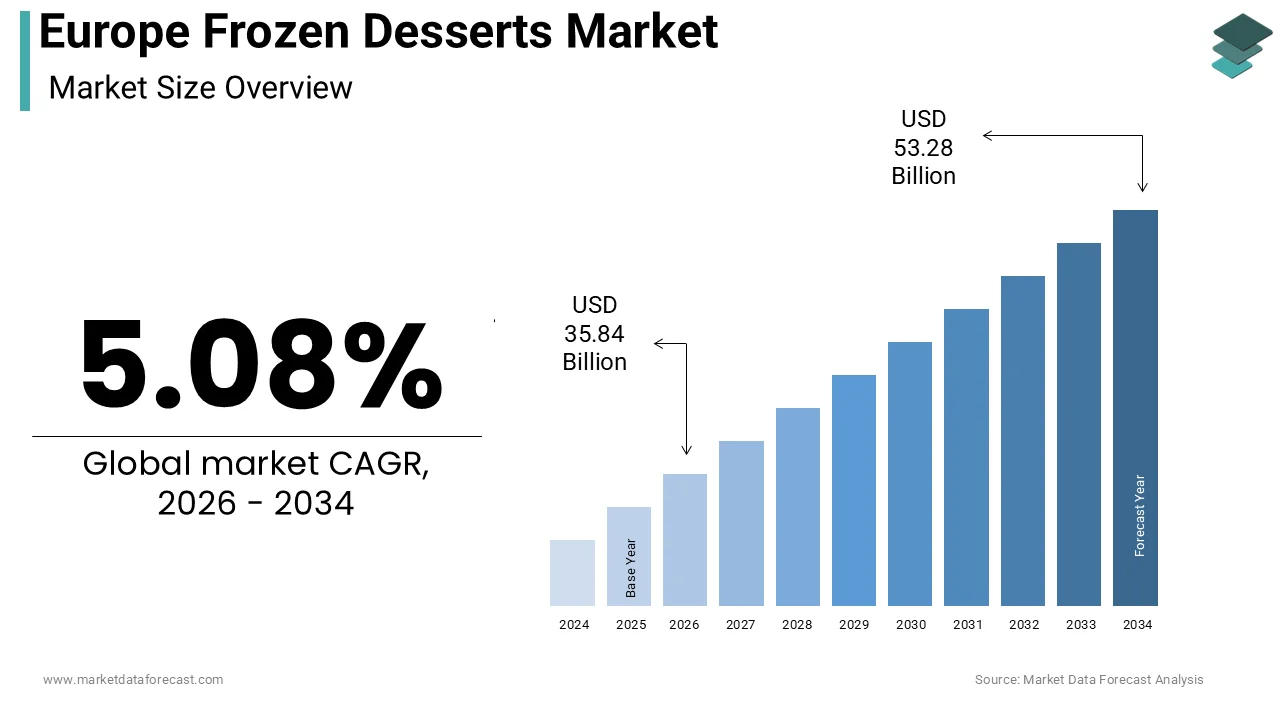

The Europe Frozen Desserts Market size was calculated to be USD 34.11 billion in 2025 and is anticipated to be worth USD 53.28 billion by 2034, from USD 35.84 billion in 2026, growing at a CAGR of 5.08% during the forecast period.

Frozen desserts are a broad category of sweet, chilled treats made by freezing liquids, semi-solids, or solids. These products serve not only as indulgent treats but also as cultural staples during seasonal festivities and social gatherings across the continent. The vast majority of the European Union’s massive and growing number of private households are equipped with domestic cooling appliances that provide dedicated sub-zero storage space suitable for maintaining frozen products. Additionally, consumers across various Western European nations maintain a consistent and significant appetite for frozen dairy products, with some regions emerging as major global leaders in per-capita intake. The production and marketing of frozen desserts in Europe are shaped by broad agricultural market regulations that maintain market stability and transparency for dairy-derived goods. The market is further influenced by evolving dietary preferences, including demand for reduced sugar clean label ingredients and allergen-free alternatives. Escalating summer heat in Southern and Southeastern Europe has made frozen desserts an everyday staple, shifting them from occasional treats to essential comfort food.

MARKET DRIVERS

Rising Demand for Plant-Based and Lactose-Free Alternatives

Consumer shifts toward flexitarian and dairy-sensitive diets have significantly accelerated demand for plant-based frozen desserts across the region, which acts as a major driver of the Europe frozen desserts market. A significant portion of adults in major European markets (Germany, France, and the Netherlands) are actively reducing their dairy consumption due to a combination of health, environmental, and ethical concerns. This behavioral shift has propelled innovation in oat, almond, and pea protein-based formulations that mimic the creamy texture of traditional ice cream without lactose or animal derivatives. Retail sales of plant-based frozen desserts in Sweden continue to rise, driven by brand efforts to improve product texture and reduce added sugar in response to consumer demand for high-quality, plant-based alternatives. The safety confirmation of plant-based emulsifiers, such as sunflower lecithin, by European food regulators has enabled food producers to adopt cleaner, more sustainable, and allergen-free ingredient labels. Moreover, the EU’s Farm to Fork Strategy encourages a reduction in saturated fats, aligning with the inherently lower fat profiles of many plant-based options. As a result, manufacturers are investing heavily in texturizing technologies like high-pressure freezing to overcome iciness, a historical barrier to consumer acceptance, thereby transforming plant-based offerings from niche alternatives into mainstream dessert choices.

Expansion of Premium Artisanal and Regional Gelato Offerings

The proliferation of premium artisanal gelato and locally inspired frozen desserts reflects a broader European consumer preference for authenticity, craftsmanship, and terroir-driven indulgence, which further boosts the expansion of the Europe frozen desserts market. Unlike mass-produced ice cream, Italian-style gelato contains less air and fat yet delivers intense flavor through fresh regional ingredients such as Sicilian pistachios, French lavender, or Greek yogurt. Italy maintains its leadership in the European artisanal gelato market, with a substantial, growing presence and new openings of gelato shops concentrated in Germany and France. This growth is supported by rising disposable incomes, particularly among urban millennials who view premium frozen desserts as experiential purchases rather than mere snacks. Studies indicate that consumers demonstrate a higher willingness to pay for artisanal gelato that carries a recognized Protected Geographical Indication status, recognizing the premium value of authentic, certified products. Furthermore, the European Union’s promotion of culinary heritage through programs like the European Destinations of Excellence initiative has elevated regional desserts as cultural ambassadors. Retail chains such as Eataly and specialty freezer sections in Carrefour now dedicate shelf space to small batch producers, reinforcing the narrative of quality over convenience and fueling sustained demand for differentiated frozen dessert experiences.

MARKET RESTRAINTS

Stringent Regulations on Sugar and Additive Labeling

European regulatory scrutiny on added sugars and artificial ingredients poses a significant restraint on frozen dessert innovation and formulation flexibility, and thereby constrains the growth of the Europe frozen desserts market. Strict European nutrition standards make it difficult for manufacturers to use specific health labels on sweets without negatively impacting the product's physical properties or flavor. Evolving front-of-pack labeling systems in several European nations are pressuring dessert brands to change their recipes to avoid unfavorable ratings caused by high caloric and fat density. In response, manufacturers have turned to alternative sweeteners like stevia and erythritol, but these often introduce off-flavors or cooling effects that detract from the sensory experience. Consumer testing in Germany suggests that many people still find sugar-reduced frozen treats less appealing because they often taste more processed than traditional versions. Moreover, the European Food Safety Authority’s re-evaluation of certain stabilizers like carrageenan has triggered supply chain uncertainty. These regulatory headwinds force companies to balance compliance with palatability, often resulting in higher production costs and delayed product launches that stifle market responsiveness.

High Energy Consumption and Cold Chain Logistics Constraints

Mounting operational constraints, owing to the energy intensity of production and distribution within the region’s tightening climate policy framework, are limiting the expansion of the Europe frozen desserts market. Maintaining an unbroken cold chain integrity from production to final storage significantly increases electrical demand compared to ambient logistics, creating a substantial energy footprint in the food supply sector. The European Union's legislative mandate to heavily reduce greenhouse gas emissions by the end of the decade places significant pressure on frozen food manufacturers to adopt more energy-efficient, costly, and sustainable technologies. High industrial electricity costs, driven by energy dependence, continue to impact small-scale artisanal gelato producers in Italy, challenging the operational viability of traditional batch-freezing methods. Additionally, last-mile delivery via electric refrigerated vans remains limited in rural Eastern Europe, where charging infrastructure is underdeveloped. These systemic inefficiencies not only increase carbon footprints but also restrict market access for artisanal players lacking capital for sustainable cold chain investments, thereby constraining category expansion.

MARKET OPPORTUNITIES

Growth of Functional and Nutrient-Enriched Frozen Desserts

The integration of functional ingredients such as probiotics, protein isolates, and omega three fatty acids into frozen desserts provides a compelling opportunity aligned with the region’s preventive health agenda, which is likely to promote the growth of the Europe frozen desserts market. Consumer demand for foods that support digestive health, immunity, and cognitive function is increasing, providing a strong market for enhanced, functional, and value-added frozen treats across Europe. Companies have launched ice cream variants fortified with Bifidobacterium lactis and vitamin D, responding to EFSA-authorized health claims linking these nutrients to immune modulation. Recent Finnish research indicates that frozen yogurt fortified with probiotics is a stable and effective carrier for promoting improved digestive comfort, highlighting opportunities for healthier, probiotic-rich frozen snacks. The European Union continues to fund research into food innovation through initiatives that focus on developing advanced bioactive delivery systems within frozen products to enhance nutritional value. Plateauing childhood obesity figures in Western Europe are encouraging parents to adopt a more flexible approach toward desserts that incorporate health-conscious ingredients. This convergence of scientific validation regulatoryy endorsement, and consumer wellness consciousness positions functional frozen desserts as a high-margin growth vector beyond traditional indulgence.

Rise of Direct-to-Consumer and Subscription-Based Sales Models

Digital commerce innovations are opening new avenues for the Europe frozen desserts market. This paves the way for brands to bypass traditional retail gatekeepers and build direct consumer relationships. The number of EU households subscribing to online grocery delivery services reached 42 million in 2024, according to Eurostat, with frozen food categories growing twice as fast as ambient counterparts. Startups like Nice Cream Co in the UK and Amorino’s home delivery arm in France leverage insulated packaging and last-mile partnerships with Deliveroo and Gorillas to ensure temperature-controlled doorstep delivery. A 2024 analysis by the European E-Commerce Association revealed that DTC frozen dessert brands achieved customer retention rates of 58 percent compared to 32 percent in conventional retail due to personalized flavor rotations and loyalty rewards. Moreover, cloud kitchen collaborations enable pop-up gelato brands to test markets without brick-and-mortar overhead. The European Investment Bank’s 2024 SME digitalization fund has allocated grants specifically for cold chain e-commerce, enabling small producers to adopt IoT-enabled thermal monitoring. This shift not only reduces dependency on supermarket slotting fees but also generates rich consumption data for agile product development, transforming frozen desserts from impulse buys into curated lifestyle experiences.

MARKET CHALLENGES

Volatility in Dairy and Cocoa Input Costs

Price instability in core raw materials, such as milk powder, cocoa butter, and vanilla, is a major issue for the Europe frozen desserts market. This trend severely impacts the profitability and pricing consistency of traditional frozen desserts across the region. Global skimmed milk powder prices experienced a significant rise during 2024, influenced by reduced milk supply in key European Union producers due to challenging weather conditions. Simultaneously, cocoa bean costs hit historic highs in early 2025, driven by severe production shortages and crop diseases in West Africa, which provides the majority of Europe’s supply. These fluctuations force manufacturers into reactive cost management, including formula simplification or portion downsizing, which risks alienating brand loyalists. A 2024 survey indicated that a majority of mid-sized European ice cream producers chose to absorb rising input costs rather than pass them on to consumers, due to concerns over decreased demand in a high-inflation environment. Unlike private label players, large brands cannot easily switch suppliers due to strict quality and traceability requirements under EU food law. This raw material vulnerability creates asymmetric competitive pressure favoring conglomerates with global procurement networks while marginalizing regional artisans dependent on local dairy cooperatives.

Consumer Skepticism Toward “Healthy” Indulgence Claims

Consumer skepticism affects the credibility of functional and reduced-calorie claims and slows down the expansion of the Europe frozen desserts market. This is despite industry efforts to position frozen desserts as guilt-free treats. European consumers are increasingly skeptical of functional claims on frozen desserts, such as enhanced protein or reduced sugar, often associating these products with disappointing taste profiles and deceptive marketing. This cynicism is amplified by media coverage highlighting discrepancies between marketing narratives and actual nutritional profiles. German food safety authorities are tightening oversight of "probiotic" frozen desserts, targeting brands that falsely claim live probiotic cultures remain active after the freezing process. Moreover, the psychological association of ice cream with indulgence makes health positioning inherently contradictory for many consumers, particularly older demographics. French consumers often perceive the concept of healthy ice cream as contradictory, showing a stronger preference for ingredient transparency and acknowledging such products as occasional treats rather than "virtue-signaling" health foods. This perceptual barrier limits the scalability of functional variants and forces brands into costly education campaigns that yield uncertain returns, creating a strategic dilemma between authenticity and innovation in a category defined by pleasure rather than utility.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.08% |

| Segments Covered | By Product Type, Fat Content, Consumption Channel, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Conagra Brands, General Mills, Inc., Sara Lee Desserts, Kellogg Company, Mrs. Smith’s, Van’s Foods, Lantmannen Unibake USA, Inc., Nestle USA, Inc., and Campbell Soup Company. |

SEGMENTAL ANALYSIS

By Product Type Insights

The frozen ice cream segment led the Europe frozen desserts market by capturing a 48.5% share in 2025. The leading position of the ice cream segment is attributed to deep cultural integration, year-round availability, and versatile consumption occasions across age groups. Research suggests that Italian households frequently consume ice cream, indicating its popularity as a year-round, staple indulgence rather than just a seasonal item. The segment benefits from robust industrial infrastructure. The European Union hosts a vast network of dedicated ice cream production facilities, with significant output coming from nations like Germany, France, and Italy, according to European statistical data. Specific EU agricultural regulations, alongside compositional rules, help define standards for dairy-based frozen desserts, promoting consistent quality and consumer confidence in the market. Additionally, major brands like Unilever’s Magnum and Nestlé’s Movenpick have invested heavily in premiumization through single-origin cocoa, Belgian chocolate coatings, and ethically sourced vanilla, aligning with experiential consumption trends. Unlike niche alternatives, ice cream enjoys universal distribution across supermarkets, convenience stores, and food service channels, creating unmatched accessibility that sustains its market leadership.

The frozen yogurt segment is predicted to witness the highest CAGR of 9.7% between 2026 and 2034 due to rising demand forgut-health-supportingg desserts among health-conscious urban consumers, particularly in Germany, France, and the Nordic countries. Retailers in Sweden are experiencing a rise in demand for functional frozen yogurt, particularly those featuring live cultures and reduced sugar content, driven by consumer interest in healthier dessert alternatives. Despite scientific support for certain probiotic strains, EU regulatory frameworks mandate stringent, strain-specific, and substantiated claims for yogurt labeling, limiting the generic use of the term 'probiotic'. Frozen yogurt is gaining popularity as a lighter alternative to traditional, high-fat ice cream, fitting into broader nutritional recommendations that favor reduced saturated fat consumption. Retailers like REWE and Tesco have responded by expanding dedicated freezer sections for functional desserts, while dessert chains such as Yorica have introduced customizable toppings bars that enhance perceived control over nutritional content. This convergence of science-backed wellness positioning and experiential retail is transforming frozen yogurt from a diet alternative into a mainstream lifestyle choice.

By Fat Content Insights

The regular frozen desserts segment dominated the Europe frozen desserts market by accounting for a substantial share in 2025. The dominance of the regular frozen desserts segment is driven by enduring consumer preference for full-fat sensory profiles, particularly in premium and artisanal offerings, where richness and mouthfeel are central to the experience. The psychological association of indulgence with full-fat formulations remains strong, especially among adults aged 35 and above who view frozen desserts as occasional treats rather than daily staples. Furthermore, regulatory frameworks require clear labeling of fat content but do not penalize higher levels, enabling brands to prioritize taste over reduction. Major manufacturers continue to invest in fat structuring technologies like partial coalescence control to enhance creaminess without increasing total fat, demonstrating that the market values perceived quality over calorie minimization. Regular frozen desserts will maintain their market lead through emotional and sensory attachment until low-fat alternatives reach full parity.

The low-fat frozen desserts segment is estimated to register the fastest CAGR of 8.3% during the forecast period, owing to shifting dietary norms among younger Europeans who increasingly integrate desserts into daily routines without compromising health goals. In the Netherlands, younger adults are increasingly driving demand for "clean label" frozen desserts that emphasize natural ingredients and are free from artificial sweeteners, favoring better-for-you alternatives. Innovations in texturizing systems, such as microparticulated whey protein and resistant starch, have enabled manufacturers to mimic fat mouthfeel while reducing total fat. Scientific research indicates that novel structural designs in reduced-fat foods can mimic the satiety effects of higher-fat alternatives, reducing the tendency to overeat later. Additionally, retailer private labels, including organic and premium lines, are expanding, with affordable low-fat product ranges, providing cost-effective, healthier options for consumers. Driven by European health initiatives targeting reduced adult obesity, the market for low-fat frozen desserts is expanding, framing these products as permissible indulgences within a healthier lifestyle.

By Consumption Channel Insights

The home consumption segment held the majority share of the Europe frozen desserts market in 2025. The supremacy of the home consumption segment is credited to widespread household freezer penetration, which was a significant share in Western and Northern Europe, enabling convenient storage and on-demand enjoyment. The rise of multi-serve tub formats and family packs further reinforces home use as a shared ritual during television viewing or weekend gatherings. Retail innovations such as dedicated freezer aisles with temperature-controlled lighting and QR code-enabled ingredient transparency have enhanced in-store discovery. Moreover, the post pandemic normalization of at-home entertainment has sustained elevated baseline demand even as out-of-home activities rebounded. Private label offerings from retailers like Edeka and Sainsbury’s provide cost-effective variety, encouraging trial and repeat purchase. Unlike food service channels, home consumption is less vulnerable to labor shortages or energy cost spikes, making it a stable and scalable revenue stream for manufacturers prioritizing volume and distribution reach over premium pricing.

The dessert parlors segment is likely to experience the fastest CAGR of 11.2% between 2026 and 2034. The rapid expansion of the dessert parlors segment is fueled by the experiential economy, where consumers, particularly Gen Z and millennials, prioritize Instagrammable moments and artisanal craftsmanship over convenience. Driven by the recovery of tourism and urban improvements in cities such as Barcelona and Valencia, the specialized ice cream and gelato industry in Spain is experiencing a surge in popularity and premiumization. These establishments differentiate through house-made bases using local ingredients such as Andalusian olive oil-infused sorbet or Basque cheesecake swirls, creating regional identity and limited edition appeal. The European Investment Bank is offering financial support to small culinary enterprises for the adoption of sustainable packaging and digital systems to enhance their environmental impact and operational efficiency. Moreover, dessert parlors serve as innovation test beds for new textures like aerated mousse or layered semifreddo that later inspire retail product development. The shift toward experiential spending is turning seasonal dessert kiosks into permanent, year-round cultural hotspots.

COMPETITION OVERVIEW

The Europe frozen desserts market features intense rivalry among multinational corporations, regional dairy cooperatives, and artisanal startups, each vying for consumer attention through differentiation in taste, sustainability, and experience. Global giants like Unilever and Nestlé dominate through scale, brand recognition, and distribution reach, while local players such as Italy’s Grom or Sweden’s Almnäs compete on terroir authenticity and small batch craftsmanship. Competition extends beyond flavor innovation to include ethical sourcing, carbon footprint transparency, and packaging recyclability as mandated by tightening EU regulations. Private label offerings from retailers like Carrefour and Aldi exert significant price pressure, particularly in the mid-tier segment, forcing branded players to justify premiums through provenance or functionality. The entry of plant-based specialists like Oatly has further fragmented the landscape, compelling traditional manufacturers to accelerate dairy-free development. With low barriers to entry in dessert parlors but high capital requirements for industrial freezing infrastructure, the market exhibits a dual structure where mass market and premium niches evolve along parallel yet intersecting trajectories shaped by cultural preference and policy.

KEY MARKET PLAYERS

A few major players of the Europe frozen desserts market include

- Conagra Brands

- General Mills, Inc

- Sara Lee Desserts

- Kellogg Company

- Mrs. Smith’s

- Van’s Foods

- Lantmannen Unibake USA, Inc.

- Nestle USA, Inc

- Campbell Soup Company

Top Strategies Used by the Key Market Participants

Key players in the Europe frozen desserts market employ five core strategies to sustain competitive advantage. First, they invest in clean label reformulation, reducing added sugars and eliminating artificial stabilizers to meet EU nutritional guidelines. Second, they expand plant-based and functional offerings fortified with protein probiotics or vitamins to capture wellness-oriented consumers. Third, they leverage digital technologies, including AI-driven demand forecasting and IoT-enabled freezer monitoring, to optimize inventory and reduce waste. Fourth, they pursue sustainable packaging innovations such as mono-material recyclable tubs and paper-based sticks aligned with EU circular economy mandates. Fifth, they strengthen direct-to-consumer channels through e-commerce partnerships and subscription models to build brand loyalty beyond traditional retail. These strategies collectively address evolving regulatory, environmental, and experiential demands shaping the future of frozen indulgence in Europe.

Leading Players in the Europe Frozen Desserts Market

- Unilever PLC is a dominant force in the Europe frozen desserts market through its iconic Ben & Jerry’s and Magnum brands, which combine ethical sourcing with premium indulgence. The company leverages its global R&D network to introduce region-specific flavors such as olive oil swirl in Spain and lavender honey in France while maintaining consistent quality across markets. It also upgraded freezer cabinets in over 15000 retail outlets with energy-efficient models compliant with EU Ecodesign regulations. These initiatives reinforce its leadership in both sustainability and sensory innovation, aligning with evolving European consumer expectations for responsible yet luxurious frozen treats.

- Nestlé SA contributes significantly to the Europe frozen desserts market through its Movenpick and Nestlé Ice Cream lines, which emphasize Swiss craftsmanship and nutritional balance. The company integrates its global nutrition science expertise to develop reduced sugar formulations using natural sweeteners like monk fruit extract without compromising texture. It also partnered with major retailers to implement dynamic pricing algorithms that optimize frozen dessert promotions based on weather and seasonal demand. These actions position Nestlé at the intersection of health-conscious indulgence and operational agility within the European chilled confectionery landscape.

- Froneri International Ltd plays a pivotal role in the Europe frozen desserts market as a joint venture between Nestlé and PAI Partners, managing brands like Häagen-Dazs and Nuii alongside private label manufacturing. The company operates numerous production facilities across Europe, enabling rapid response to local taste preferences and regulatory requirements. It also rolled out a direct-to-consumer subscription service for limited edition flavors in Sweden and Belgium, leveraging insulated last-mile delivery networks. These innovations enhance product quality and customer engagement while strengthening Froneri’s dual identity as both a premium brand owner and agile contract manufacturer.

MARKET SEGMENTATION

This research report on the Europe frozen desserts market has been segmented and sub-segmented based on product type, fat content, consumption channel, and region.

By Product Type

- Sherbet

- Frozen Yogurt

- Frozen Ice Cream

- Rozen Tofu

- Frozen Cakes

- Mousse

- Frozen Novelties

By Fat Content

- Regular Frozen Desserts

- Low-Fat Desserts

By Consumption Channel

- Home

- Hotel And Restaurants

- Dessert Parlors

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving market growth?

Key drivers include rising demand for premium desserts, increasing preference for convenience foods, and growing interest in plant-based and low-sugar products.

2. Which products are included in frozen desserts?

Major products include ice cream, gelato, frozen yogurt, sorbet, and frozen bakery desserts.

3. Which segment dominates the market by product type?

Ice cream holds the largest share due to its widespread popularity and extensive availability.

4. Which segment is the fastest growing?

Frozen yogurt and plant-based desserts are among the fastest-growing segments due to health-conscious consumer trends.

5. What are the key trends in the market?

Trends include premiumization, artisanal products, vegan desserts, and functional ingredients like probiotics.

6. What are the main distribution channels?

Supermarkets/hypermarkets, convenience stores, specialty stores, and online retail dominate distribution.

7. How is consumer behavior changing in this market?

Consumers are shifting toward healthier, low-calorie, and plant-based frozen desserts, while still seeking indulgent premium options.

8. What challenges does the market face?

Challenges include rising raw material costs, strict food regulations, and health concerns over sugar and fat content.

9. What opportunities exist in this market?

Opportunities include innovation in flavors, expansion of vegan products, and growth in e-commerce channels.

10. What is the future outlook of the Europe frozen desserts market?

The market is expected to witness steady growth, driven by innovation, health-focused offerings, and increasing demand for convenient indulgent foods.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com