Europe Serum Market Size, Share, Trends & Growth Forecast Report – Segmented By Type, Inactivation Technique, Application, End User, Sales Channel, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Serum Market Report Summary

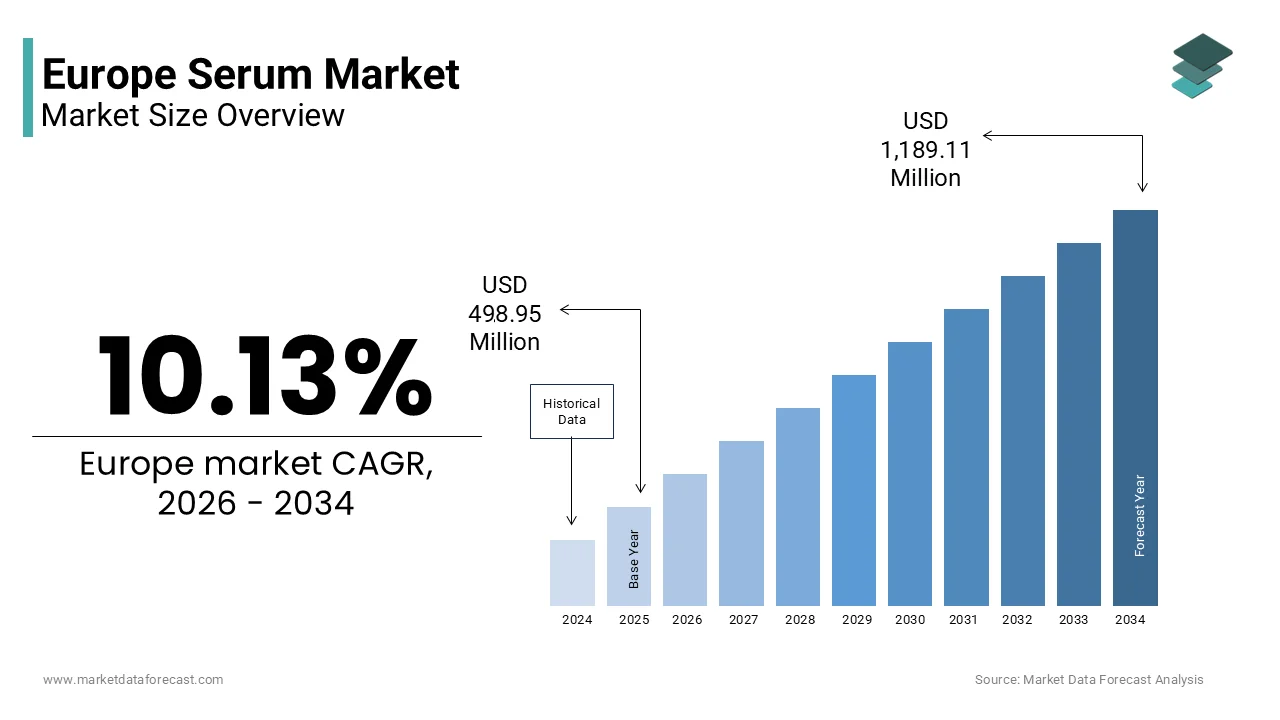

The Europe serum market was valued at USD 498.95 million in 2025, is estimated to reach USD 549.52 million in 2026, and is projected to reach USD 1,189.11 million by 2034, growing at a CAGR of 10.13% during the forecast period. Market growth is driven by increasing demand across biopharmaceutical research, biotechnology applications, and skincare formulations. The rising focus on biologics development, vaccine production, and advanced cell culture technologies is significantly boosting demand for serum products. In addition, the growing popularity of premium skincare and anti aging solutions is further supporting market expansion. Continuous advancements in life sciences research and cosmetic innovations are contributing to strong market growth across Europe.

Key Market Trends

- Rising demand for biologics and vaccine development is increasing the adoption of serum in research and production processes.

- Growing investments in biotechnology and life sciences research are driving market expansion.

- Increasing use of serum in cell culture and regenerative medicine applications is supporting demand growth.

- Rising consumer preference for premium skincare and anti aging products is boosting cosmetic serum adoption.

- Technological advancements in serum processing and quality control are improving product consistency and safety.

Segmental Insights

- Based on type, the fetal bovine serum segment was the largest and held a dominant share of the Europe serum market in 2025. This dominance is attributed to its widespread use in cell culture, high nutrient content, and effectiveness in supporting cell growth in research and biopharmaceutical applications.

- Based on inactivation technique, the heat inactivated serum segment accounted for the largest share of the Europe serum market. This segment is driven by its ability to deactivate complement proteins, improving suitability for sensitive cell culture applications.

- Based on application, the biopharmaceutical drugs segment held 45.3% of the Europe serum market share in 2025. The segment’s growth is fueled by increasing production of biologics, vaccines, and advanced therapeutic products.

- Based on end user, the biopharmaceutical and biotechnology industry segment dominated with 55.4% of the Europe serum market share in 2025, supported by rising research activities and large scale manufacturing of biologics.

Regional Insights

- The Europe serum market is witnessing strong growth across major countries, supported by advanced healthcare infrastructure and increasing R and D investments.

- Germany was the largest contributor, accounting for 28.4% of the Europe serum market share in 2025, driven by a well established biotechnology sector, strong pharmaceutical industry presence, and continuous innovation in life sciences.

Competitive Landscape

The Europe serum market is highly competitive, with key players focusing on product innovation, research collaborations, and expansion of production capabilities. Companies are investing in advanced serum formulations, quality assurance, and sustainable sourcing practices to strengthen their market position. Prominent players in the Europe serum market include L'Oréal S A, Estée Lauder Companies Inc, Unilever plc, Thermo Fisher Scientific, Beiersdorf AG, Shiseido Company Limited, Procter and Gamble Co, Merck KGaA, Clarins Group, Bio Techne, Galderma S A, Amorepacific Group Inc, KOSÉ Corporation, and Revlon Inc.

Europe Serum Market Size

The Europe serum market size was valued at USD 498.95 million in 2025 and is projected to reach USD 1,189.11 million by 2034 from USD 549.52 million in 2026, growing at a CAGR of 10.13%.

The serum is primarily fetal bovine serum, horse serum, and human AB serum, which serve as critical growth supplements for cell culture media in biopharmaceutical manufacturing and academic research. These biological fluids provide essential hormones, growth factors, and attachment proteins required for the proliferation of mammalian cells in-vitro. The operational landscape in Europe is defined by a stringent regulatory environment and a strategic shift towards supply chain security following global disruptions. As per Eurostat, the European Union biotechnology sector employed over 900,000 individuals in 2024, creating a massive foundational demand for cell culture reagents including serum. Furthermore, the European Medicines Agency authorized more than 100 new advanced therapy medicinal products and vaccines in the last year alone, each requiring extensive cell line development phases dependent on high-quality serum. The region also hosts over 6,000 biotechnology companies as noted by EuropaBio, many of which rely on serum for upstream processing.

MARKET DRIVERS

Escalating Production of Biologics and Monoclonal Antibodies

The exponential expansion of biopharmaceutical manufacturing, specifically the production of monoclonal antibodies and recombinant proteins, which require robust cell lines for upstream processing is propelling the growth of Europe serum market. Fetal bovine serum remains the gold standard supplement for cultivating Chinese Hamster Ovary cells and other mammalian lines used to produce these complex therapeutics. As per the European Federation of Pharmaceutical Industries and Associations, the biopharmaceutical sector in Europe accounted for 45% of the global production capacity for biologics in 2024, necessitating vast quantities of culture media supplements. The approval rate for biosimilars in the European Union has surged, with over 30 new biosimilar medicines receiving marketing authorization in the last year, intensifying the competition among manufacturers to optimize cell yields. Each manufacturing batch requires significant volumes of serum during the cell line development and seed train expansion phases before potentially switching to serum-free conditions for final production. According to data from the European Medicines Agency, the pipeline of cell and gene therapies currently under clinical investigation in Europe includes over 1,200 active trials, many of which rely on serum-containing media for initial cell isolation and expansion. This relentless growth in the biologics pipeline ensures a sustained and critical demand for high-grade serum products across the region.

Expansion of Academic Research and Regenerative Medicine Initiatives

The vigorous investment in academic research and regenerative medicine programs, which heavily utilize serum for stem cell culture and tissue engineering applications is additionally propelling the growth of Europe serum market. Universities and research institutes require consistent supplies of qualified serum to maintain pluripotent stem cell lines and differentiate them into various tissue types for disease modeling and drug screening. The European Research Council awarded over 2 billion EUR in grants for frontier research in 2024, many of which focus on organoid development and personalized medicine approaches that depend on serum-supplemented media. Furthermore, the rise of contract research organizations in Europe, which support both academic and industrial clients, has amplified the consumption of serum for high-throughput screening assays. According to the European Society for Gene and Cell Therapy, the number of registered clinical trials involving cell-based therapies in Europe increased by 18% in 2024, which is reflecting the growing translation of laboratory research into clinical applications. This deep integration of serum-dependent methodologies in both basic science and translational research sustains a robust market baseline.

MARKET RESTRAINTS

Ethical Concerns and Regulatory Pressure to Reduce Animal-Derived Components

The intensifying ethical scrutiny and regulatory push to eliminate animal-derived ingredients from biopharmaceutical processes, driven by animal welfare advocates and evolving legislation is substantially limiting the growth of Europe serum market. The collection of fetal bovine serum involves the harvesting of blood from bovine fetuses, a practice that has drawn severe criticism from animal rights organizations and prompted stricter oversight from European authorities. As per the European Food Safety Authority, there is increasing pressure to implement the 3Rs principle of Replacement, Reduction, and Refinement in all scientific procedures, compelling laboratories to seek alternatives to traditional serum. The European Union has been a global leader in banning animal testing for cosmetics, and this sentiment is increasingly permeating the research and therapeutic sectors, leading some institutions to voluntarily phase out fetal bovine serum. According to a survey conducted by the European Association for Bioindustries, 35% of European biotech companies have initiated programs to transition to serum-free or xeno-free media formulations to align with corporate sustainability goals and avoid reputational risks. This ethical shift forces manufacturers to invest heavily in alternative media development, thereby slowing the growth trajectory of traditional animal-derived serum products and limiting their long-term market potential.

Supply Chain Volatility and Geographic Concentration of Sourcing

The inherent instability of the global supply chain for serum, which relies heavily on specific geographic regions for sourcing by making vulnerable to external shocks and trade disruptions is additionally hampering the growth of Europe serum market. The majority of fetal bovine serum is sourced from countries in South America and Oceania, and any geopolitical tension, trade embargo, or disease outbreak in these regions can immediately constrict supply to Europe. As per the World Organisation for Animal Health, outbreaks of foot-and-mouth disease in key exporting nations have historically led to immediate import bans by the European Union, causing severe shortages and price spikes. The logistical complexity of maintaining a cold chain for biological products across continents further exacerbates the risk of spoilage and delivery delays. According to the European Centre for Disease Prevention and Control, the reliance on single-source suppliers for critical biological reagents was identified as a major vulnerability in the European health security strategy following recent global crises. This dependency creates uncertainty for European manufacturers who require consistent, high-volume supplies to maintain production schedules, forcing them to hold expensive inventory buffers or face potential production halts.

MARKET OPPORTUNITIES

Development of Defined and Xeno-Free Serum Alternatives

The urgent need to mitigate ethical concerns and ensure supply chain security for the development and commercialization of defined, xeno-free, and human-derived serum alternatives is solely creating new opportunities for the growth of Europe serum market. European regulators and pharmaceutical companies are increasingly seeking replacements that offer consistent composition without the variability and ethical baggage of animal-derived products. As per the European Medicines Agency, there is a growing preference for xeno-free manufacturing processes for cell and gene therapies to minimize the risk of viral contamination and immune reactions in patients. This regulatory tailwind encourages innovation in plant-based hydrolysates, recombinant proteins, and human platelet lysates that can mimic the growth-promoting properties of traditional serum. According to data from the European Biotechnology Association, investment in alternative media technologies in Europe grew by 25% in 2024, signaling strong market confidence in these next-generation solutions. Companies that can validate the performance of these alternatives in complex cell lines stand to capture significant market share as industries transition away from fetal bovine serum. The opportunity extends to providing customization services where media formulations are tailored to specific cell types, offering higher value than commodity serum products.

Integration of Advanced Quality Control and Traceability Technologies

The implementation of advanced tracking and quality assurance technologies to enhance the value proposition of serum products is also to create new opportunities for the growth of Europe serum market. Manufacturers can leverage blockchain and digital serialization to provide end-to-end traceability from the abattoir to the end user, ensuring authenticity and compliance with strict European Pharmacopoeia standards. As per the European Commission, the fight against falsified medicines and biological reagents has led to stricter documentation requirements, creating demand for suppliers who can offer immutable proof of origin and testing history. According to the European Directorate for the Quality of Medicines, the adoption of digital quality management systems in the biologicals sector is expected to become mandatory for certain high-risk categories in the near future. Suppliers who proactively adopt these technologies can differentiate themselves as premium partners for large-scale biopharmaceutical production where batch consistency is important.

MARKET CHALLENGES

Risk of Viral Contamination and Pathogen Transmission

The persistent threat of viral contamination and the transmission of exotic pathogens through animal-derived serum that complicates procurement and usage is one of the major challenges for the growth of Europe serum market. Despite rigorous testing protocols, the biological nature of serum means it can potentially harbor unknown viruses or prions that evade standard detection methods, posing a risk to cell cultures and ultimately to patient safety in therapeutic applications. As per the European Centre for Disease Prevention and Control, the emergence of new zoonotic diseases globally has heightened vigilance regarding the importation of biological materials from non-EU countries. The cost and time associated with comprehensive viral safety testing, including PCR assays and in vivo studies, add significant burdens to manufacturers and increase the final price of the product. According to the European Pharmacopoeia, the list of mandatory tests for imported serum continues to expand, requiring suppliers to invest heavily in state-of-the-art screening facilities. Any detection of contaminants can lead to massive product recalls and long-term import bans, disrupting the supply chain for months. This inherent biological risk forces European users to maintain strict qualification processes for suppliers, limiting the pool of eligible vendors and creating a barrier to entry for smaller players who cannot afford extensive safety validation programs.

Extreme Price Volatility and Economic Accessibility Issues

The ongoing challenge of extreme price volatility driven by fluctuating global supply dynamics, which makes budgeting and long-term planning difficult for research institutions and smaller biotech firms is acting as a barrier for the growth of Europe serum market. Prices for fetal bovine serum have historically experienced dramatic swings, sometimes doubling within a single year due to droughts, disease outbreaks, or changes in export policies in sourcing countries. The economic instability disproportionately affects academic laboratories and startups operating on fixed grants or limited venture capital, forcing them to reduce experimental scales or seek lower-quality alternatives that may compromise data integrity. According to the European University Association, many member institutions reported freezing hiring or cutting back on consumable orders in 2024 due to unsustainable cost increases in reagents. The lack of price transparency and the oligopolistic nature of the global supplier base further exacerbate the issue, leaving buyers with little negotiating power. This financial unpredictability threatens to stifle innovation in sectors that rely heavily on affordable access to high-quality cell culture media.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 10.13% |

| Segments Covered | By Type, Inactivation Technique, Application, End User, Sales Channel, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | L'Oréal S.A., Estée Lauder Companies Inc., Unilever plc, Thermo Fisher Scientific, Beiersdorf AG, Shiseido Company Limited, Procter & Gamble Co., Merck KGaA, Clarins Group, Bio Techne, Galderma S.A., Amorepacific Group Inc., KOSÉ Corporation, and Revlon Inc |

SEGMENTAL ANALYSIS

By Type Insights

The fetal bovine serum segment was the largest by holding a dominant share of the Europe serum market in 2025 due to its unparalleled composition of growth factors, hormones, and attachment proteins which are essential for the proliferation of a wide variety of mammalian cell lines used in biopharmaceutical manufacturing and research. The growth of the segment is also driven by its unique biological profile that supports rapid cell division and high viability, making it indispensable for the critical stages of cell line development and seed train expansion. Unlike adult bovine serum or other alternatives, FBS contains low levels of antibodies and inhibitory factors while being rich in embryonic growth promoters like fibroblast growth factor and insulin-like growth factor. As per the European Medicines Agency, over 90% of approved monoclonal antibody therapies in Europe were developed using cell lines adapted to grow in FBS-supplemented media during their initial discovery phases. The consistency required to maintain genetic stability in Chinese Hamster Ovary cells, the workhorse of the biopharma industry, relies heavily on the specific nutrient balance found only in fetal serum. According to data from the European Federation of Pharmaceutical Industries and Associations, the production volume of biologics in Europe reached record highs in 2024, with manufacturers continuing to depend on FBS for upstream processing to ensure maximum yield before transitioning to serum-free conditions.

The other sera segment is likely o expand at an anticipated CAGR of 7.8% during the forecast period. The rapid expansion of the other sera segment is fueled by the specific requirement for Horse Serum and other non-bovine sera in the production of certain viral vaccines and antivenoms where bovine components may interfere with viral replication or induce immune reactions. Horse serum, for instance, contains specific inhibitors and growth factors that are optimal for cultivating viruses used in influenza and rabies vaccines, which are seeing renewed investment across Europe. As per the European Centre for Disease Prevention and Control, the strategic stockpiling and production of vaccines against emerging infectious diseases increased by 30% in 2024, driving demand for specialized sera that support unique viral host ranges. Furthermore, in neuroscience research, Horse Serum is often preferred for differentiating neuronal cell lines due to its distinct protein profile that promotes neurite outgrowth more effectively than FBS. The European Society for Neuroscience reports a 25% increase in grants awarded for neurodegenerative disease studies in 2024, directly correlating with higher consumption of these specialized sera. The inability of FBS to replicate these specific biological effects ensures a growing and dedicated market for alternative animal sera.

By Inactivation Technique Insights

The heat inactivated serum segment was the largest by holding a dominant share of the Europe serum market owing to the need to eliminate complement activity, a group of plasma proteins that can cause cell lysis or interfere with antibody-antigen binding in various experimental setups. In applications such as flow cytometry, immunohistochemistry, and the culture of sensitive cell lines like stem cells, active complement can lead to false positives or cell death, rendering experiments invalid. As per the European Journal of Immunology, over 80% of published immunoassay protocols in European laboratories explicitly mandate the use of heat inactivated serum to ensure data reliability and reproducibility. The standard procedure involves heating serum to 56 degrees Celsius for 30 minutes, a process that effectively denatures complement components without significantly degrading essential growth factors. According to the European Committee for Standardization, the adoption of standardized heat inactivation protocols has become a best practice in Good Laboratory Practice guidelines, reinforcing its usage across academic and industrial sectors.

The non-heat inactivated serum segment is anticipated to witness a CAGR of 6.5% from 2025 to 2034. The growth of the non-heat inactivated segment is primarily driven by the increasing use of complex and sensitive cell types, such as induced pluripotent stem cells and primary neurons, which rely on heat-labile growth factors that are partially destroyed during the inactivation process. Studies have shown that heating serum can reduce the activity of critical proteins like fibroblast growth factor and transferrin, leading to suboptimal cell proliferation and differentiation outcomes in these demanding applications. As per the International Society for Stem Cell Research, recent publications from European labs indicate an increase in the use of native serum for maintaining stem cell pluripotency, as researchers seek to maximize the potency of their culture media. The shift towards personalized medicine and organoid technology, which requires highly physiological conditions, further accelerates this trend. As scientists become more aware of the detrimental effects of heat on specific bioactive molecules, the demand for non-heat inactivated serum for high-value research and development is rising sharply.

By Application Insights

The biopharmaceutical drugs application segment was the largest by accounting for 45.3% of the Europe serum market share in 2025 owing to the sheer volume of commercial production activities across Europe, where serum is a critical raw material for generating the initial cell banks and expanding cultures before large-scale fermentation. Europe is a global hub for biopharma, hosting numerous production facilities for top-selling drugs that treat cancer, autoimmune diseases, and chronic conditions. Each new drug launch requires the establishment of robust master and working cell banks, a process that consumes significant quantities of FBS to ensure cell viability and genetic stability. According to the European Medicines Agency, the approval rate for new biologics in Europe has remained steady, with over 20 new molecular entities approved annually, each adding to the cumulative demand for serum in their lifecycle. The industrial scale of these operations dwarfs research-level consumption, ensuring that the biopharmaceutical drugs segment remains the largest consumer of serum in the region.

The vaccine products segment is esteemed to grow at a fastest CAGR of 8.2% from 2026 to 2034 owing to the urgent need for pandemic preparedness and the active development of vaccines against emerging infectious diseases, which heavily rely on serum for viral propagation in cell cultures. Following recent global health crises, European governments and the EU have invested billions in building sovereign vaccine manufacturing capabilities, leading to a surge in production activities that require vast amounts of serum. As per the European Commission, the HERA Incubator initiative has funded over 50 new vaccine development projects in 2024 alone, many of which utilize egg-based or cell-culture methods dependent on high-quality serum for virus amplification. The shift towards mRNA and viral vector vaccines also requires robust cell lines for production, further driving demand. According to the European Centre for Disease Prevention and Control, the stockpiling of vaccines for seasonal influenza and potential future outbreaks has increased by creating a sustained spike in serum consumption.

By End User Insights

The biopharmaceutical and biotechnology industry segment was accounted in holding 55.4% of the Europe serum market share in 2025 with the massive volume of serum required for the commercial manufacturing of biologics, where even small inefficiencies can cost millions, making high-quality serum a critical investment. Large pharmaceutical companies operate multi-thousand-liter bioreactors that require tons of culture media, supplemented with serum during the inoculation and expansion phases, creating a demand scale that far exceeds academic or diagnostic sectors. As per the European Federation of Pharmaceutical Industries and Associations, the biopharma sector in Europe employs over 800,000 people and operates more than 500 large-scale manufacturing sites, all of which are heavy consumers of serum. The trend towards personalized medicine and orphan drugs has also led to the establishment of smaller but highly specialized production lines that still rely on serum for cell line development. According to data from the European Medicines Agency, the pipeline of novel biologics in late-stage clinical trials is at an all-time high, future commercial production needs that will sustain serum demand.

The diagnostics laboratories segment is expected to grow at a fastest CAGR of 7.5% from 2026 to 2034 owing to the sustained high volume of infectious disease testing and the widespread adoption of molecular diagnostic techniques that often utilize serum as a supplement or control material. The aftermath of global pandemics has left a legacy of enhanced surveillance systems and routine screening programs that require reliable reagents for accurate results. As per the European Centre for Disease Prevention and Control, the number of diagnostic tests performed in European labs increased by 35% in 2024 compared to pre-pandemic levels, driving up the consumption of serum-based reagents. The shift towards multiplex assays and high-throughput screening in clinical settings also increases the demand for standardized serum controls to ensure test validity. According to the European Diagnostic Manufacturers Association, the market for in vitro diagnostics in Europe is expanding rapidly, with a particular focus on rapid and point-of-care tests that may still rely on serum components for calibration.

REGIONAL ANALYSIS

Germany Serum Market Analysis

Germany was the top performer in the Europe serum market by holding 28.4% of the share in 2025. Germany is home to global pharmaceutical giants like Bayer, Merck KGaA, and Boehringer Ingelheim, whose extensive manufacturing operations for biologics and vaccines drive immense consumption of high-quality serum. The country boasts the highest number of accredited GMP manufacturing facilities in Europe, each requiring certified serum for production processes. Furthermore, Germany's strong automotive and engineering sectors have facilitated the development of advanced bioprocessing equipment, creating a synergistic ecosystem that supports large-scale serum utilization. The presence of renowned universities and Max Planck institutes ensures a steady stream of cutting-edge research that consumes premium reagents. According to the German Biotechnology Association, the sector employs over 150,000 people, with a significant portion engaged in activities directly dependent on serum.

United Kingdom Serum Market Analysis

The United Kingdom serum market was ranked second by capturing 22.3% of share in 2025 with its pioneering role in genomics, a vibrant biotech cluster, and a strong tradition of biomedical research that drives consistent demand for serum. The UK market is characterized by high innovation rates and a strategic focus on cell and gene therapies.

The UK's leadership in genomics, anchored by institutions like the Sanger Institute and Genomics England, creates a massive demand for serum for DNA sequencing library preparation and cell line maintenance. As per the Office for National Statistics, the life sciences sector contributes over 90 billion GBP to the UK economy, with biotechnology being a key growth engine. The "Golden Triangle" of London, Oxford, and Cambridge hosts a dense concentration of biotech startups and academic labs that are heavy users of serum for drug discovery and development. The country's regulatory body, the MHRA, has been proactive in approving advanced therapies, encouraging companies to set up manufacturing units that require serum for upstream processing. According to the British Biotechnology and Biopharmaceutical Association, the UK accounts for nearly half of all cell and gene therapy trials in Europe, a segment that is particularly serum-intensive. The strong government support through the Life Sciences Vision strategy further boosts R&D activities. This dynamic blend of academic prowess, entrepreneurial spirit, and regulatory agility sustains the UK's strong market position.

France Serum Market Analysis

France serum market is likely to expand at a fastest CAGR in coming years with its strong national research organizations, a growing biopharmaceutical industry, and significant government investments in health sovereignty and vaccine production. Institutions like INSERM and the Pasteur Institute form the backbone of French life science research, conducting large-scale projects in virology and immunology that drive consistent demand for serum. As per the French Ministry of Higher Education and Research, the "France 2030" investment plan has allocated billions to revitalizing the domestic vaccine industry, leading to the construction of new production facilities that will increase serum consumption. France is a major producer of vaccines in Europe, with companies like Sanofi playing a pivotal role in global supply, necessitating large volumes of serum for viral propagation. The country's strong agricultural sector also supports a robust veterinary vaccine market, adding to the demand. The government's push for health independence has led to increased funding for domestic production of critical reagents and therapies.

Switzerland Serum Market Analysis

Switzerland serum market growth is likely to grow with its concentration of global pharmaceutical headquarters, top-tier research institutes, and a focus on high-value biopharmaceuticals. Home to giants like Roche and Novartis, Switzerland is a global epicenter for biopharmaceutical innovation, particularly in oncology and immunology, where precise cell culture conditions are critical for producing complex biologics. The presence of ETH Zurich and other elite universities fosters cutting-edge research in structural biology and chemical biology, driving demand for advanced specialty sera. The Swiss regulatory environment, closely aligned with EMA standards but often more stringent, necessitates the use of the highest quality serum for regulatory submissions. The country's strong focus on personalized medicine and cell therapy also creates a niche demand for specialized molecular tools and reagents.

Netherlands Serum Market Analysis

The Netherlands serum market growth is anticipated to grow with its strategic location as a logistics hub, a strong agricultural biotechnology sector, and a collaborative approach to life science research. As per the Netherlands Organisation for Scientific Research, the country invests heavily in interdisciplinary research, particularly in areas like agri-food tech and medical devices, which utilize serum extensively for cell culture applications. The Port of Rotterdam and Schiphol Airport facilitate the rapid import and distribution of temperature-sensitive biological reagents, making the Netherlands a key entry point for serum into the European market. The country's strong biotech sector, centered around hubs like Leiden and Groningen, focuses on enzyme engineering and synthetic biology, driving demand for both standard and specialty markers. The Dutch government's "Top Sector Life Sciences and Health" initiative fosters public-private partnerships that accelerate innovation and market uptake.

COMPETITIVE LANDSCAPE

The competition in the Europe serum market is intense and characterized by a handful of dominant global corporations vying for supremacy through superior quality assurance, supply chain reliability, and regulatory compliance. Rivalry centers heavily on the ability to provide documented viral safety and ethical sourcing credentials as European regulators and consumers demand greater transparency and animal welfare adherence. Price competition exists but is often secondary to quality and reliability given the critical nature of serum in biopharmaceutical production where batch failure can result in massive financial losses. Companies differentiate themselves by offering value added services such as custom fractionation, dedicated logistics, and technical support to foster long term loyalty among large pharmaceutical clients. The emergence of alternative media technologies adds pressure on traditional serum providers to innovate and demonstrate the irreplaceable value of their natural products while simultaneously developing next generation solutions to future proof their portfolios against shifting market preferences.

KEY MARKET PLAYERS

Some of the notable key players in the Europe serum market are

- L'Oréal S.A.

- Estée Lauder Companies Inc.

- Unilever plc

- Thermo Fisher Scientific

- Beiersdorf AG

- Shiseido Company Limited

- Procter & Gamble Co.

- Merck KGaA

- Clarins Group

- Bio-Techne

- Galderma S.A.

- Amorepacific Group Inc.

- KOSÉ Corporation

- Revlon Inc.

Top Players in the Market

- Thermo Fisher Scientific is a global supplier of life science solutions with a profound impact on the Europe serum market through its extensive portfolio of high quality fetal bovine serum and specialty media. The company leverages its vast global supply chain to ensure consistent availability of certified serum products that meet stringent European regulatory standards for biopharmaceutical manufacturing. Recently Thermo Fisher Scientific expanded its cold chain logistics capabilities across key European hubs to guarantee the integrity of temperature sensitive biological reagents during transit. Their commitment to quality is demonstrated by rigorous testing protocols that exceed standard pharmacopoeial requirements, providing customers with unmatched confidence in product safety.

- Merck KGaA operates as a leading science and technology company with a significant presence in the Europe serum market via its Life Science business sector which provides premium biological reagents. The company distinguishes itself through advanced traceability systems that document the origin and testing history of every serum batch, addressing critical transparency needs in the European pharmaceutical industry. Merck KGaA recently invested in new processing facilities within Germany to enhance local production capacity and reduce reliance on imported raw materials, thereby strengthening supply security for regional clients. Their focus on sustainability has led to the development of ethically sourced serum options that align with evolving animal welfare regulations in the European Union.

- Bio-Techne is a prominent developer and manufacturer of high purity biological products including a specialized range of characterized sera for demanding research and clinical applications across Europe. The company contributes to the global market by setting rigorous standards for serum performance particularly in stem cell research and regenerative medicine where consistency is paramount. Bio-Techne recently strengthened its European footprint by establishing strategic partnerships with local distributors to improve market access and provide faster delivery times to academic and industrial customers. Their dedication to innovation is evident in their launch of defined serum alternatives that mimic the benefits of traditional fetal bovine serum while eliminating variability and ethical concerns.

Top Strategies Used by the Key Market Participants

Key players in the Europe serum market primarily focus on securing robust and diversified supply chains to mitigate risks associated with geographic concentration and potential disease outbreaks in sourcing regions. Companies frequently invest in state of the art testing laboratories to ensure complete compliance with European Pharmacopoeia standards and to guarantee viral safety for all batches. Strategic acquisitions of regional distributors allow major firms to enhance their logistical networks and provide faster delivery of temperature sensitive products to end users. Product differentiation through the development of certified ethically sourced or xeno free alternatives serves as a crucial tactic to address growing animal welfare concerns and regulatory pressures. Partnerships with biopharmaceutical manufacturers enable suppliers to co develop customized media formulations that optimize cell growth and yield for specific therapeutic applications. Additionally, firms emphasize digital traceability solutions to provide transparent documentation of product origin and handling, building trust with highly regulated European clients.

MARKET SEGMENTATION

This research report on the European serum market has been segmented and sub-segmented based on categories.

By Type

- Bovine Serum

- FBS

- Others

By Inactivation Technique

- Heat Inactivated

- Non Heat Inactivated

By Application

- Biological Products

- Research

- Cell Culture

- Biopharmaceutical Drugs

- Vaccine Products

- Diagnostic Products

- Others

By End User

- Biopharmaceutical and Biotechnology Industry

- Diagnostics Laboratories

- Research Laboratories

- Academic Research

By Sales Channel

- Direct Channel

- Distribution Channel

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1.What are the key drivers of the Europe serum market?

The market growth is driven by increasing skincare awareness, rising demand for anti aging products, and higher disposable incomes.

2.Which product type dominates the Europe serum market?

Anti aging serums dominate the market due to strong demand from the aging population.

3.Which segment is the fastest growing in the Europe serum market?

Skin brightening and vitamin C based serums are among the fastest growing segments due to demand for radiant skin.

4.What are the common ingredients used in serums?

Common ingredients include hyaluronic acid, vitamin C, retinol, niacinamide, and peptides.

5.Which countries are leading in the Europe serum market?

Germany, France, and the United Kingdom are leading markets due to strong consumer demand and established beauty industries.

6.What are the major trends in the Europe serum market?

Key trends include natural and organic formulations, sustainable packaging, and personalized skincare solutions.

7.How is e commerce influencing the serum market in Europe?

E commerce is expanding rapidly, making serums more accessible and boosting direct to consumer sales.

8.What challenges does the Europe serum market face?

The market faces challenges such as high product costs, regulatory compliance, and the presence of counterfeit products.

9.What role does innovation play in the serum market?

Innovation plays a major role through advanced formulations, targeted treatments, and multifunctional products.

10.What is the future outlook of the Europe serum market?

The market is expected to grow steadily with increasing demand for premium and specialized skincare products.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com