Europe Sewing Machine Market Size, Share, Trends & Growth Forecast Report, Segmented By Type (Electric, Computerized, Manual), Use Case, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis From (2025 To 2033)

Europe Sewing Machine Market Size

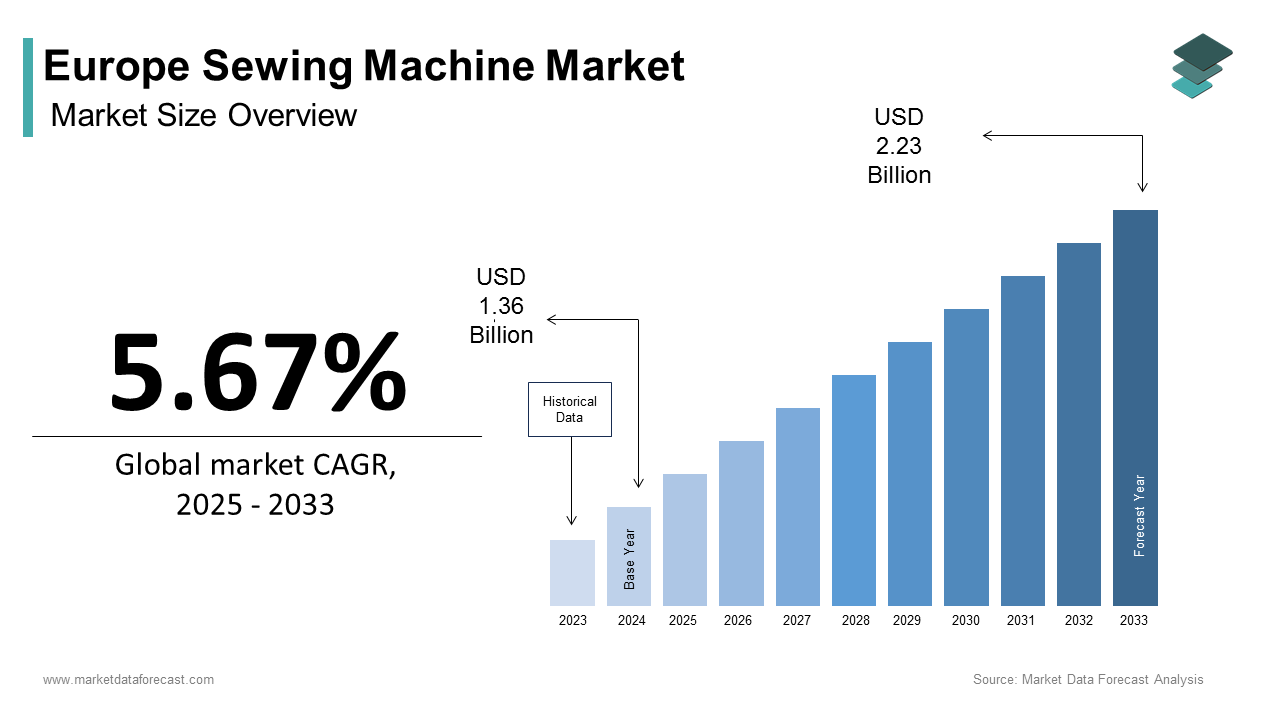

The Europe sewing machine market size was calculated to be USD 1.36 billion in 2024 and is anticipated to be worth USD 2.23 billion by 2033, growing from USD 1.43 billion in 2025 at a CAGR of 5.67% during the forecast period.

Sewing machines are mechanical and computerized devices intended for stitching fabric and other materials in both domestic and professional settings. This market serves a diverse user base ranging from hobbyists and home tailors to industrial garment manufacturers and technical textile producers. In recent years, the sector has experienced renewed relevance driven by cultural shifts toward sustainable consumption, craft revival, and localized production. According to Eurostat, textile-related household craft participation is widespread across Europe, with sewing, knitting, and embroidery activities documented in EU textile industry reports. As per the European Commission’s Circular Economy Action Plan, a majority of EU citizens actively attempt to extend the life of their clothing through repair or alteration, whichreflectsg the growing repair culture highlighted in circular economy studies. Furthermore, vocational education systems across countries like Germany, Italy, and Poland continue to integrate technical sewing skills into curricula, with thousands of students enrolled in textile and garment technology programs as recorded by the European Centre for the Development of Vocational Training. These socio-educational and sustainability-oriented dynamics position the sewing machine not merely as a legacy appliance but as a functional instrument in Europe’s evolving relationship with fashion consumption and material stewardship.

MARKET DRIVERS

Resurgence of Home‑Based Textile Craft and Repair Culture

The widespread revival of home‑based textile crafts, which is fuelled by sustainability awareness, economic pragmatism, and digital community engagement, is one of the major factors propelling the European sewing machine market growth. According to the surveys by the European Consumer Organisation, a majority of younger adults report mending or altering clothing regularly, supported by accessible entry‑level sewing machines. This shift is embedded in broader environmental consciousness. As per the European Environment Agency, most EU respondents view clothing repair as a direct contribution to reducing textile waste. The rise of online learning platforms has democratized skill acquisition, with providers such as Domestika and Skillshare reporting sharp increases in European enrolments for sewing and garment construction courses. Social media further amplifies participation as the European Digital Media Observatory documented billions of views of #sewing and #mending content on TikTok and Instagram in 2024. National initiatives reinforce this trend as Germany’s Reparaturbonus program reimbursed citizens for repair equipment purchases, leading to a notable increase in domestic machine sales. This convergence of policy, digital culture, and eco‑ethics transforms the sewing machine from a niche hobby tool into a mainstream artifact of responsible consumption across Europe.

Integration of Sewing Skills in Vocational and Creative Education

Educational policy across Europe is systematically reinforcing sewing competencies through formal training programs, sustaining long‑term demand for both domestic and semi‑industrial sewing machines, which is further contributing to the European sewing machine market expansion. According to CEDEFOP, hundreds of thousands of students were enrolled in textile, fashion, and garment technology courses in EU member states in 2024, with Germany, Italy, and Poland accounting for the majority. These programs mandate hands‑on machine operation, with institutions procuring units annually for classroom use. In France, the Ministry of National Education introduced a national Savoir Coudre curriculum in 202,3 requiring all middle schools to offer basic sewing instruction by 2025, which is a policy projected to generate significant demand for new machines in the public education sector. Similarly, Sweden’s vocational schools upgraded their sewing equipment in 2024 to include computerized models capable of teaching pattern digitization. Beyond compulsory education, private craft academies are expanding. According to the European Cultural Foundation, a strong increase in registered textile arts schools across Southern Europe between 2022 and 2024. Institutional embedding ensures consistent procurement cycles and cultivates a generation of technically literate users who often transition to home or micro‑enterprise use, anchoring structural demand beyond transient consumer trends.

MARKET RESTRAINTS

Decline of Local Garment Manufacturing and Reduced Industrial Demand

One of the most significant restraints facing the Europe sewing machine market is the continued contraction of small‑ to mid‑scale local garment production, which historically constituted a core segment for industrial and heavy‑duty machines. According to Eurostat data, the number of enterprises in the EU’s apparel manufacturing sector declined sharply between 2018 and 2024, with thousands of small workshops closing permanently. This erosion stems from decades of offshoring. As per the European Apparel and Textile Confederation, most garments sold in the EU are imported, primarily from Asia and North Africa. The loss of these workshops directly reduces demand for professional sewing equipment. In Italy, once a global epicenter of artisanal tailoring, industry associations report a steep drop in registered ateliers. Similarly, Poland’s statistical office recorded a significant reduction in micro‑enterprises offering custom clothing services. While slow fashion and micro‑brands are emerging, the European Fashion Alliance estimates that locally made garments account for less than 5% of total apparel consumption in Europe. This structural hollowing out constrains the industrial segment’s growth potential, which is leaving domestic and educational demand as the primary drivers of the market.

High Initial Cost and Perceived Complexity of Advanced Machines

Despite growing interest in sewing, the high acquisition cost and perceived technical complexity of modern computerized machines deter widespread adoption, particularly among casual users and younger demographics, which is further hindering the sewing machine market growth in Europe. According to the European Consumer Organisation, most Europeans interested in sewing cite price as the primary barrier, with entry‑level computerized models costing several times more than mechanical alternatives. Inflation compounds this issue. According to Eurostat, a double‑digit increase in consumer electronics pricing in 2024, including home sewing equipment. Complexity further discourages uptake. As per the surveys by the European Digital Inclusion Observatory, many adults feel intimidated by the digital interfaces of modern sewing machines, which often include touchscreens, USB connectivity, and automated stitch libraries. In rural regions, digital literacy gaps are pronounced. As per the Joint Research Centre, fewer than half of residents in non‑urban EU areas possess intermediate digital skills necessary to operate connected sewing devices. Retailers confirm this hesitation, reporting high return rates due to user frustration with setup or functionality. Until manufacturers simplify interfaces, reduce entry costs, or offer scalable learning pathways, this dual barrier of affordability and usability will continue to limit market penetration beyond committed enthusiasts.

MARKET OPPORTUNITIES

Expansion of Micro Fashion Enterprises and On‑Demand Tailoring Services

An emerging opportunity in the Europe sewing machine market lies in the proliferation of micro fashion businesses and hyper‑local tailoring services enabled by digital platforms and shifting consumer preferences. According to the European Commission’s Digital Innovation Scoreboard, tens of thousands of micro enterprises offering made‑to‑order or customized apparel launched across the EU in 2024, marking strong growth compared to 2022. These ventures typically operate from home or shared studios and rely on mid‑range computerized sewing machines capable of handling diverse fabrics and complex patterns. Platforms such as Etsy, Depop, and Vinted have catalyzed this trend, with the European E‑Commerce Association reporting double‑digit growth in handmade and altered garment sales on EU marketplaces in 2024. In response, specialized sewing machine vendors are introducing compact professional‑grade models that saw notable sales increases in urban centers like Berlin, Lisbon, and Copenhagen. Moreover, city governments are supporting this ecosystem. Paris allocated millions of euros in 2024 to subsidize sewing equipment for certified micro‑tailors as part of its Urban Craft Revival initiative. This fusion of digital commerce, policy support, and consumer demand for uniqueness creates a fertile niche for machines that bridge domestic affordability and professional capability.

Adoption of Smart and Connected Sewing Technologies

The integration of digital design software, Internet of Things connectivity, and augmented reality guidance is unlocking new functionality in sewing machines, which is a significant opportunity for the European sewing machine market. According to the European Institute of Innovation and Technology, smart sewing units equipped with Wi‑Fi pattern libraries and automatic tension control saw strong sales growth in 2024 compared to 2022. These machines sync with design platforms like CLO3D, allowing users to import digital patterns directly and eliminate manual transcription errors. Educational institutions are driving early adoption. As pee Sweden’s National Agency for Education, most vocational fashion schools upgraded to connected sewing systems in 2024 to teach digital garment construction workflows. Consumer interest is also rising. According to the European Digital Media Observatory, a growing share of sewing‑related tutorials in 2024 focused on smart machine features such as stitch simulation and error detection. Manufacturers like Brother and Janome have responded by launching Europe‑specific models with multilingual voice assistance and GDPR‑compliant data handling. As Europe’s digital textile ecosystem matures from design to production, intelligent machines are positioned to become central hubs in a new generation of tech‑enabled making.

MARKET CHALLENGES

Intense Competition from Low‑Cost Asian Imports

The Europe sewing machine market faces persistent pressure from inexpensive imports, primarily from China and Vietnam, which capture significant volume in the entry‑level segment through aggressive pricing and online distribution. According to the European Commission’s Directorate‑General for Trade, machines priced below €100 accounted for the majority of entry‑level units sold in Europe in 2024, with most originating from Asian manufacturers. While European brands emphasize durability, precision, and service, these low‑cost alternatives often lack standardized safety certifications yet evade scrutiny due to e‑commerce loopholes. According to the European Consumer Safety Network, thousands of non‑compliant sewing machines were flagged in 2024 for lacking CE marking or using uncertified electrical components, yet remained available online. This influx erodes brand loyalty and compresses margins for European and Japanese producers. According to the German Electrical and Electronic Manufacturers Association, average selling prices for basic mechanical machines fell significantly between 2021 and 2024 due to import competition. Enforcement remains fragmented. According to the European Free Trade Association, only a minority of EU member states conduct routine physical inspections of small appliance imports. Until harmonized digital gatekeeping mechanisms are implemented, substandard yet affordable alternatives will continue to distort market dynamics and challenge quality‑oriented players.

Limited After‑Sales Support and Spare Parts Availability

A critical challenge undermining consumer confidence in the Europe sewing machine market is the inconsistent availability of repair services and genuine spare parts, particularly for mid‑range and computerized models. As per the European Consumer Organisation, nearly half of sewing machine owners who experienced a malfunction in 2024 either abandoned repair attempts or switched brands due to service unavailability. In Southern and Eastern Europe, the problem is acute. As per the European Repair Coalition, fewer than one‑third of municipalities in Romania, Bulgaria, and Greece host certified sewing machine technicians. Manufacturers often restrict access to diagnostic software and proprietary components, limiting third‑party repairs. The European Right to Repair Initiative documented that most sewing machine brands require proprietary tools or software resets to replace common parts like bobbin cases or feed dogs. This contrasts with the EU’s broader repairability mandates for electronics, which are creating a regulatory gap. Consequently, the average machine lifespan is declining. As per the estimations of the Joint Research Centre, nearly 40% of sewing machines purchased in Europe in 2024 were discarded within five years due to unrepaired faults, compared to about one‑quarter in 2015. Without standardized service networks, accessible parts catalogs, and technician training programs, post‑purchase fragmentation will continue to deter long‑term investment and dampen repeat purchasing behavior across the market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.67% |

| Segments Covered | By Type, Use Case, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Brother Industries, Bernina International AG, Janome Sewing Machine Co., JUKI Corporation, Singer Corporation, Pfaff Industrial, Husqvarna Viking, Elna International Corp., Toyota Industries Corporation, Jaguar Sewing Machines, Necchi, Durkopp Adler, Jack Sewing Machine, Pegasus Sewing Machine Manufacturing Co., SEIKO Sewing Machine |

SEGMENTAL ANALYSIS

By Type Insights

The electric sewing machines segment held 57.5% of the European market share in 2024. The dominance of the electric segment in this regional market is attributed to its optimal balance of affordability, reliability, and ease of use for both hobbyists and semi-professional users. Unlike manual models, which require physical effort and offer limited stitch variety, electric machines provide consistent stitch quality with minimal user fatigue, which is making them ideal for regular home use. A key factor driving this segment is accessibility in vocational and adult education. According to the European Centre for the Development of Vocational Training, 74% of publicly funded sewing and textile courses across EU member states in 2024 utilized electric machines as the standard teaching tool due to their durability and straightforward mechanical interface. Additionally, price sensitivity among casual users favours electric models, which average 140 euros compared to 320 euros for computerized variants as per data from the European Consumer Organisation. In Southern and Eastern Europe, where disposable income for hobby equipment remains constrained, the German Electrical and Electronic Manufacturers Association reported that electric machines represented over 70% of all sewing equipment sold in Poland, Romania, and Greece in 2024. Their plug-and-play functionality without software dependencies also ensures usability across all age groups, with Eurostat noting that 61% of Europeans aged 55 and above who sew prefer electric models for their intuitive operation. This combination of pedagogical, institutional, and demographic alignment secures the electric segment’s market leadership.

The computerized segment is the fastest-growing segment in the Europe sewing machine market and is estimated to witness a CAGR of 12.2% over the forecast period, owing to the rising demand for precision customization, integration with digital design ecosystems, and growing interest in complex textile crafts among digitally native consumers. A primary driver is the convergence of sewing with digital fashion creation. As per the European Institute of Innovation and Technology, over 12,000 European users adopted computerized machines in 2024 specifically to execute patterns generated by software like CLO3D and Valentina, enabling seamless transition from virtual design to physical garment. Educational institutions are also accelerating adoption. As per the Swedish National Agency for Education, 82% of upper secondary fashion programs upgraded to computerized units in 2024 to teach automated embroidery and multi-step stitching sequences. Moreover, urban micro entrepreneurs are leveraging these machines for small batch production. According to the European Commission’s Digital Europe Programme, a 45% increase in sole proprietor fashion businesses using computerized sewing equipment in cities like Berlin, Lisbon, and Amsterdam during 2024. Features such as touchscreen interfaces, USB pattern loading, and automatic thread trimming reduce skill barriers while enhancing creative output. As Europe’s maker culture deepens and digital literacy rises, computerized machines are transitioning from niche professional tools to mainstream creative instruments.

By Use Case Insights

The apparel segment commanded the highest share of 60.5% of the European market in 2024. The dominating position of the apparel segment in the European market can be credited to the enduring centrality of garment construction in both domestic and professional sewing contexts. The segment is anchored by a combination of household garment maintenance, rising slow fashion participation, and structured vocational training in dressmaking. Consumer behavior is a major contributor. According to the European Consumer Organisation, 63% of European households engaged in clothing alteration or creation in 2024, with 89% of those activities focused exclusively on apparel such as dresses, shirts, and trousers. As per the European Environment Agency, 58% of citizens who repaired textiles in 2024 did so to extend the life of worn garments rather than accessories. Institutional demand reinforces this dominance. According to the European Centre for the Development of Vocational Training, 91% of sewing machine usage in EU educational settings is dedicated to apparel construction curricula. Even microenterprises prioritize apparel. According to the European Fashion Alliance, 76% of EEU-basedmicro fashion brands launched in 2024 specialize in ready-to-wear or made-to-measure clothing rather than footwear or leather goods. The universality of apparel as both a practical necessity and creative canvas ensures its unrivaled position across all user tiers.

The bags segment is the fastest-growing use case in the Europe sewing machine market and is projected to register a CAGR of 14.4% over the forecast period, owing to the artisanal leather goods revival, urban craftsmanship movements, and increasing consumer preference for durable handcrafted accessoriesover mass-producedd alternatives. The rise of sustainable luxury is a critical enabler. As per the European Leather Working Group, sales of hand-sewn vegan and vegetable-tanned leather bags by independent European makers grew by 48% in 2024, with creators relying on heavy-duty and computerized machines capable of stitching thick, layered materials. Cities like Florence, Milan, and Copenhagen have become hubs for micro bag ateliers. According to the Italian Artisans Confederation, over 1,800 new bag-making micro businesses registered in Italy alone in 2024, each requiring industrial-grade or robust domestic machines. Online platforms amplify visibility. As per the European E-Commerce Association, handmade bag listings on Etsy and Vinted from EU sellers increased by 61% year on year in 2024. Additionally, vocational schools are diversifying curricula. The Danish Design School introduced a dedicated bag construction module in 2024, requiring specialized sewing equipment for leather and synthetic composites. This fusion of heritage craftsmanship, digital commerce, and eco-conscious consumption positions bag-making as the most dynamic frontier in Europe’s sewing ecosystem.

REGIONAL ANALYSIS

Germany Sewing Machine Market Analysis

Germany captured the leading share of 20.8% of the European sewing machine market in 2024. The dominance of Germany in the European market is attributed to its vocational education, technical craftsmanship, and strong manufacturing heritage. According to the Federal Institute for Vocational Education, 42,000 students enrolled in garment and textile technology programs in 2024, showing how education sustains skilled demand. German brands like Pfaff and Bernina maintain reputations that drive loyalty and exports. According to the German Electrical and Electronic Manufacturers Association, 68% of sewing machines sold in Germany in 2024 were produced by EU‑based companies, proving how domestic and regional production reinforces quality preference. The Federal Environment Agency found that 72% of German households engaged in clothing repair in 2024, the highest rate in Europe, showing how a sustainability culture boosts machine usage. Government initiatives like the “Reparaturbonus” subsidy program further incentivize purchases. Germany’s combination of education, manufacturing excellence, and eco‑conscious consumer behavior anchors its leadership in Europe’s sewing machine ecosystem.

Italy Sewing Machine Market Analysis

Italy occupied a substantial share of the European sewing machine market in 2024. The growth of Italy in the European market is propelled by fashion heritage, artisanal ateliers, and specialized textile education. According to the Italian National Confederation of Artisans, over 24,000 tailoring and bag‑making workshops in 2024, showing how artisanal density sustains demand. Fashion schools such as Polimoda and Istituto Marangoni train thousands annually, with the Ministry of Education noting that 88% of fashion design programs mandate hands‑on machine training, proving how education drives equipment adoption. The Italian National Institute of Statistics reported that 65% of Italians aged 30–60 own a sewing machine, showing how consumer culture values craftsmanship. Regional clusters like Prato and Biella sustain localized supply chains, reinforcing mid‑range machine demand. Italy’s haute couture tradition and micro‑manufacturing culture ensure consistent demand across professional and semi‑professional segments.

United Kingdom Sewing Machine Market Analysis

The United Kingdom is anticipated to account for a prominent share of the European sewing machine market over the forecast period. The growth of the UK in the European market is likely to be driven by the vibrant maker movement, online craft communities, and creative industry support. The Office for National Statistics reported 8.2 million adults engaged in textile crafts in 2024, a 22% increase since 2020, showing how cultural revival drives demand. The British Craft Council documented that 71% of new sewers in 2024 learned through YouTube, Instagram, or apps, proving how digital onboarding sustains entry‑level machine sales. Retailers John Lewis and Hobbycraft reported a 35% year‑on‑year increase in sewing machine sales in 2024, showing how retail accessibility supports growth. The Department for Education expanded creative arts funding in 2023, leading to sewing machine procurement in over 1,200 secondary schools by early 2025, proving how policy investment strengthens adoption. The UK’s blend of digital engagement, retail accessibility, and cultural celebration of making sustains broad‑based market participation.

France Sewing Machine Market Analysis

France is a prominent regional segment in the European sewing machine market. The elite fashion schools, circular economy policies, and grassroots repair culture are expected to boost the sewing machine market in France during the forecast period. Institutions such as ESMOD and IFM produce thousands of graduates annually, requiring advanced equipment for prototyping. The French Ministry of Ecological Transition allocated €18 million in 2024 to “Repair and Reuse” centers across 300 municipalities, showing how policy directly funds infrastructure. The French Agency for Environmental and Energy Management reported that 59% of citizens repaired clothing in 2024, up from 41% in 2021, proving how consumer behavior aligns with sustainability. France’s “Anti‑Waste Law” mandates extended producer responsibility, encouraging brands to support repair infrastructure, indirectly boosting machine demand. France’s alignment of fashion education, sustainability policy, and consumer repair culture positions it as a sophisticated, policy‑driven market.

Sweden Sewing Machine Market Analysis

Sweden is likely to grow at a healthy CAGR in the European sewing machine market over the forecast period. Sweden is notable for sustainability integration, gender inclusivity, and digital learning. The Swedish Environmental Protection Agency includes home sewing in “Climate Smart Living” guidelines, showing how policy embeds sewing into carbon reduction strategies. The National Agency for Education mandates textile craft in compulsory schooling, with every student using machines by age 14, proving how education ensures universal exposure. According to Statistics Sweden, 52% of sewing machine owners are male, showing how gender inclusivity broadens participation. Digital platforms like Hemslöjd and Formexperten provide multilingual tutorials, driving informed purchases. In 2024, the Swedish Innovation Agency funded 15 maker spaces equipped with computerized sewing units, showing how community infrastructure sustains adoption. Sweden’s environmental policy, educational equity, and inclusive culture create a future‑oriented sewing market that outperforms its population size.

COMPETITION OVERVIEW

Competition in the Europe sewing machine market is shaped by a blend of legacy craftsmanship, modern technological integration, and sustainability mandates that favor established brands with proven durability and service infrastructure. While global manufacturers dominate the premium and mid-range segment,s local online-only brands from Asia exert pressure in the entry-level tier through aggressive pricing, though often lacking certification or repair support. Differentiation increasingly hinges on user experience with features like automatic threading noise reduction and digital pattern compatibility becoming decisive factors. Regulatory alignment, particularly with CEmarkingng RoHS compliance and GDPR for connected devices, creates barriers for non-compliant entrants. Educational institutions act as influential gatekeepers with procurement decisions favoring brands that offer training materials, technician certification, and curriculum integration. Meanwhile, rising consumer awareness of planned obsolescence has shifted preference toward repairable, long-lasting machines, intensifying scrutiny on build quality. These dynamic fosters a competitive environment where trust, heritage anpost-purchasese support are as critical as initial functionality.

KEY MARKET PLAYERS

A few major players of the Europe sewing machine market include

- Brother Industries

- Bernina International AG

- Janome Sewing Machine Co

- JUKI Corporation

- Singer Corporation

- Pfaff Industrial

- Husqvarna Viking

- Elna International Corp

- Toyota Industries Corporation

- Jaguar Sewing Machines

- Necchi

- Durkopp Adler

- Jack Sewing Machine

- Pegasus Sewing Machine Manufacturing Co

- SEIKO Sewing Machine

Top Strategies Used by the Key Market Participants

Key players in the Europe sewing machine market pursue differentiated strategies centred on product innovation, educational collaboration, sustainability integration, and digital enablement. Companies invest in developing quieter, more energy-efficient motors and intuitive interfaces to lower entry barriers for new users. Strategic partnerships with fashion schools, vocational institutes, and municipal repair centers embed their machines into the institutional ecosystem,s ensuring long term adoption. Sustainability is prioritized through modular designs, extended warranty programs, and transparent spare parts access in response to Europe’s right to repair movement. Digital strategies include multilingual video tutor,ials mobile app connectivity, and cloud-based pattern libraries that enhance post purchase engagement. Geographic customization, such as region-specific stitch libraries and compliance with local electrical safety standards, further strengthens local relevance. These multifaceted approaches position leading brands not merely as equipment providers but as enablers of Europe’s evolving textile culture.

Leading Players in the Europe Sewing Machine Market

- Bernina International AG is a Switzerland-based manufacturer renowned for its precision-engineered sewing and embroidery machines, widely used by professionals and serious hobbyists across Europe. The company contributes significantly to the global market through its commitment to mechanical excellence, longevity, and modular design that supports decades of use. In 2,024 Bernina launched its upgraded B 800 series featuring enhanced thread tension control and quieter motor technology specifically tailored for European vocational schools and boutique ateliers. It also expanded its training partnerships with fashion academies in Milan and Stockholm to embed its machines into curriculum workflows. These initiatives reinforce its reputation as a premium durable solution aligned with Europe’s emphasis on quality craftsmanship and education.

- Janome Sewing Machine Co Ltd maintains a strong presence in the Europe sewing machine market through its diverse portfolio that includes entry-level electric models and advanced computerized units. The company supports global sewing communities via multilingual user interfaces and accessible digital learning content. In 2024, Janome introduced its Skyline S9 Special Edition with integrated European language support,t including Scandinavian and Eastern European scripts, enhancing usability across diverse regions. It also partnered with online crafting platforms in France and the Netherlands to offer bundled machine and tutorial packages. These actions reflect a strategy focused on user empowerment, digital engagement,t and regional customization, which resonate with Europe’s expanding base of new sewers.

- Brother Industries Ltd plays a pivotal role in the Europe sewing machine market by offerireliablelia,ble affordable, and feature-rich machines that cater to both domestic users and micro entrepreneurs. The company contributes to the global market through scalable manufacturing and strong after-sales networks. In late 2024, Brother rolled out its Innov-is V7 LED series across Germany andItalyly featuring USB pattern import and automatic needle threading designed to simplify complex projects for beginners. It also launched a pan-European “Sew Sustainably” campaign providing free repair guides and spare parts access to extend product life. These efforts align with Europe’s circular economy values and strengthen long-term consumer trust beyond initial purchase.

MARKET SEGMENTATION

This research report on the Europe sewing machine market has been segmented and sub-segmented based on type, use case, and region.

By Type

- Electric

- Computerized

- Manual

By Use Case

- Apparel

- Shoes

- Bags

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the current market scenario of the Europe Sewing Machine Market?

The market is mature and stable, supported by consistent demand from the textile, apparel, home furnishing, and DIY sewing segments.

2. What are the key drivers of the Europe Sewing Machine Market?

Key drivers include growth in the apparel industry, increasing DIY and craft activities, demand for automated machines, and rising focus on sustainable fashion.

3. What are the major restraints in the Europe Sewing Machine Market?

High product costs, availability of low-cost alternatives, and declining traditional tailoring practices in some regions are major restraints.

4. Which product types dominate the Europe Sewing Machine Market?

Industrial sewing machines dominate the market due to high demand from garment and textile manufacturing, followed by household and computerized machines.

5. What applications drive demand in the Europe Sewing Machine Market?

Major applications include apparel manufacturing, home textiles, upholstery, leather goods, and personal or hobby sewing.

6. Which countries lead the Europe Sewing Machine Market?

Germany, the United Kingdom, France, Italy, and Spain are leading markets due to strong textile industries and consumer demand.

7. How is technology impacting the Europe Sewing Machine Market?

Technological advancements such as computerized controls, automation, and smart features are improving productivity, precision, and ease of use.

8. What role does e-commerce play in this market?

E-commerce has expanded product accessibility, enabled price comparison, and increased sales, especially in the household sewing machine segment.

9. What are the key trends in the Europe Sewing Machine Market?

Key trends include smart and automated sewing machines, energy-efficient models, and increased adoption of computerized sewing systems.

10. Who are the major end users in the Europe Sewing Machine Market?

Major end users include garment manufacturers, tailoring shops, upholstery manufacturers, fashion designers, and home users.

11. What challenges does the Europe Sewing Machine Market face?

Challenges include intense competition, pricing pressure, rapid technological changes, and supply chain disruptions.

12. What future opportunities exist in the Europe Sewing Machine Market?

Future opportunities include growth in customized clothing, expansion of smart sewing machines, and rising demand from sustainable and slow fashion movements.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com