Europe Sleep Apnea Devices Market Research Report By Diagnostic Devices, Therapeutic Devices and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis on Size, Share, Trends, COVID-19 Impact & Growth Forecast (2026 to 2034)

Europe Sleep Apnea Devices Market Size

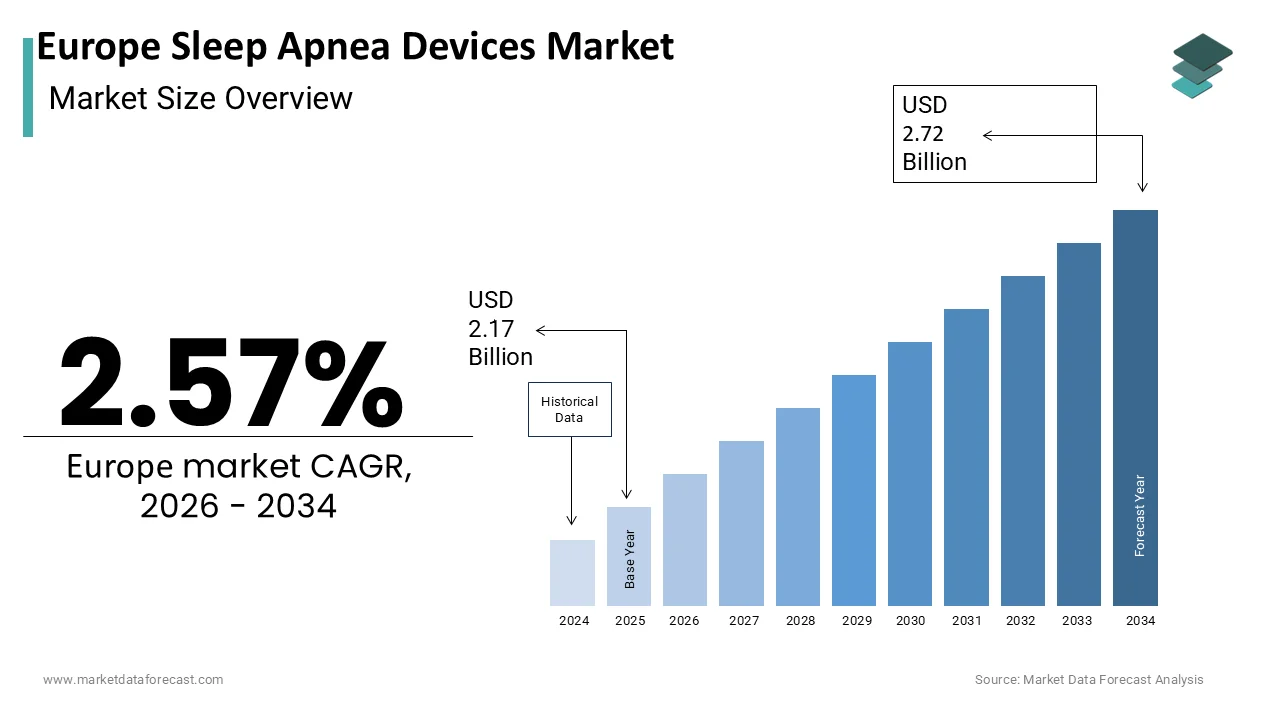

The europe sleep apnea devices market was valued at USD 2.17 billion in 2025, is expected to have a 2.57% CAGR from 2026 to 2034, and be worth USD 2.72 billion by 2033 from USD 2.22 billion in 2025.

The Sleep Apnea Devices are medical technologies designed to diagnose, manage, and treat sleep disordered breathing, which is primarily obstructive sleep apnea (OSA). These include continuous positive airway pressure (CPAP) machines, automatic positive airway pressure (APAP) systems, bilevel positive airway pressure (BiPAP) devices, oral appliances, and diagnostic home sleep testing kits. Sleep apnea affects an estimated 175 million adults across Europe, with prevalence rates exceeding 30 % in individuals over 60 years of age, according to the European Respiratory Society.

MARKET DRIVERS

Rising Prevalence of Obesity and Associated Comorbidities

The increasing prevalence of obesity cases is expected to substantially elevate the growth of the Europe sleep apnea market. Adipose tissue accumulation in the upper airway increases pharyngeal collapsibility during sleep, which is significantly elevating OSA risk. Individuals with a body mass index above 30 are seven times more likely to develop moderate to severe sleep apnea. This epidemiological link is particularly acute in Southern and Eastern Europe, where obesity rates have risen fastest over the past decade. According to the source, 68% of patients diagnosed with OSA also have obesity related comorbidities such as hypertension or type 2 diabetes. The clinicians routinely prescribe CPAP therapy not only to improve sleep but also to mitigate cardiovascular strain. This clinical integration transforms sleep apnea devices from symptomatic aids into essential components of chronic disease intervention, which is broadening their therapeutic mandate and accelerating adoption across primary and secondary care settings.

Strengthening Reimbursement Frameworks in Public Healthcare Systems

The public reimbursement policies are progressively recognizing sleep apnea therapy as a cost-effective intervention, thereby removing financial barriers to device access, which is driving the growth of the Europe sleep apnea devices market. The statutory health insurers have covered CPAP devices for moderate to severe OSA since the early 2000s, and in 2023, the Federal Joint Committee expanded coverage to include home sleep apnea testing as a first-line diagnostic tool. Similarly, France’s National Health Insurance Fund reimburses up to 60 % of CPAP equipment costs upon confirmed diagnosis, with full coverage for low-income beneficiaries.

MARKET RESTRAINTS

Low Diagnosis Rates Due to Limited Sleep Specialist Capacity

The low diagnosis rates stemming from a shortage of sleep medicine specialists and diagnostic infrastructure are a major factor limiting the growth of Europe's sleep apnea devices market. According to the European Sleep Research Society, fewer than 5,000 certified sleep physicians serve the entire EU population by resulting in average wait times of 6 to 14 months for in-lab polysomnography in countries like Italy, Spain, and Poland. The delay in confirmation of OSA postpones device prescription by leaving millions untreated. In rural regions in France and Romania often no dedicated sleep clinics within a 100-kilometer radius. Although home sleep tests offer a scalable alternative, regulatory fragmentation hinders their adoption, where Germany requires physician supervision for test interpretation, while Belgium restricts reimbursement to hospital-based diagnostics.

Patient Non-Adherence Due to Device Discomfort and Stigma

The therapeutic efficacy of sleep apnea devices is frequently undermined by poor long-term patient adherence, which is another factor degrading the growth of the Europe sleep apnea devices market. Clinical studies indicate that up to 30 % of CPAP users discontinue therapy within the first year, with mask leakage, skin irritation, and noise cited as primary reasons. The psychological burden is equally significant, where many patients perceive CPAP use as a marker of frailty or aging by leading to concealment or avoidance among working-age adults. A 2023 survey by the European Lung Foundation found that 42 % of diagnosed individuals under 50 reported skipping therapy during travel or social events due to embarrassment. While newer devices feature quieter motors, lighter masks, and smart pressure adjustment, these innovations often come at a premium not fully covered by public reimbursement schemes.

MARKET OPPORTUNITIES

Integration of Telemedicine and Remote Monitoring Platforms

Telemedicine is unlocking new pathways for sleep apnea diagnosis and therapy management by creating significant opportunities for the growth of the Europe sleep apnea devices market. As per the European Commission’s 2023 Digital Health Action Plan explicitly endorses remote sleep monitoring as a strategy to alleviate specialist shortages. ResMed and Philips have partnered with national health services to embed their devices with secure data transmission capabilities compliant with the EU’s General Data Protection Regulation. A 2025 evaluation by the Danish Health Authority showed that telemonitored CPAP users had 22% higher adherence rates at six months compared to standard care. These digital ecosystems generate longitudinal patient data that can inform personalized therapy adjustments and predictive maintenance alerts.

Expansion of Oral Appliance Therapy in Mild to Moderate OSA

The oral appliance therapy is emerging as a viable and increasingly reimbursed alternative to CPAP for patients with mild to moderate obstructive sleep apnea, which is attributed to the growth of the Europe sleep apnea devices market. In 2025, the European Academy of Dental Sleep Medicine updated its clinical guidelines to recommend oral appliances as a first-line treatment for mild OSA and for CPAP-intolerant patients with moderate disease. This shift is reflected in policy; Germany’s statutory health insurers began partial reimbursement of custom-fitted oral devices in 2023, and France added them to its national list of covered medical devices in early 2025. As per a multicenter trial published in the European Respiratory Journal, 68 % of mild OSA patients using oral appliances achieved a 50 % reduction in apnea hypopnea index after three months.

MARKET RESTRAINTS

Fragmented Regulatory and Reimbursement Landscapes Across Member States

The regulatory and reimbursement heterogeneity across EU member states is certainly one of the major challenges for the growth of the Europe Sleep Apnea Devices Market. While the European Union Medical Device Regulation (MDR 2017/745) provides a baseline for device approval, national competent authorities retain discretion over clinical evidence requirements, classification nuances, and post-market surveillance expectations. This leads to delays; a CPAP device approved in Germany may require additional clinical data for reimbursement in Italy or Spain, according to the European Coordination Committee of the Radiological, Electromedical, and Healthcare IT Industry. A 2025 analysis by the European Health Management Association found that reimbursement approval timelines ranged from 3 months in the Netherlands to over 18 months in Eastern European countries. Such fragmentation increases market entry costs, discourages SME participation, and creates inequities in patient access.

Cybersecurity and Data Privacy Risks in Connected Devices

The increasing connectivity of sleep apnea devices introduces significant cybersecurity and data governance challenges that threaten patient trust and regulatory compliance, which is also a factor hampering the growth of the Europe Sleep Apnea Devices Market. Modern CPAP and APAP systems routinely collect sensitive health data, including respiratory patterns, usage duration, and mask fit metrics, and transmit it via Wi Fi or Bluetooth to cloud platforms for clinician review. Under the EU’s General Data Protection Regulation, manufacturers are classified as data controllers and bear full liability for breaches. National regulators are responding with stricter conformity assessments. France’s National Agency for Medicines and Health Products Safety now requires penetration testing as part of MDR certification. These requirements increase development costs and time to market, particularly for smaller innovators.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Diagnostic Devices, Therapeutic Devices, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | ResMed, Inc. (U.S.), Philips Healthcare (Netherlands), Fisher & Paykel Healthcare Ltd. (New Zealand), SomnoMed Ltd. (Australia), Compumedics Limited (Australia), Weinmann Medical Devices GmbH (Germany), Whole You, Inc. (U.S.) |

SEGMENTAL ANALYSIS

By Diagnostic Devices Insights

In 2025, the respiratory polygraphs segment was the largest and held 42.3% the share due to their role as the primary tool for home sleep apnea testing, a strategy increasingly adopted to overcome limited access to sleep laboratories. The European Respiratory Society recommends home polygraphy as a first-line diagnostic for suspected moderate to severe obstructive sleep apnea in adults without significant comorbidities. These portable devices measure airflow, respiratory effort, and oxygen saturation with sufficient accuracy for clinical decision making, while reducing costs by up to 60% compared to in-lab polysomnography. National reimbursement policies reinforce this trend. France’s Health Insurance Fund fully covers home polygraphy when prescribed by a physician, and Italy expanded coverage to include rural telemedicine pathways in 2023.

The pulse oximeters segment is lucratively to grow at the fastest CAGR of 11.2% from 2025 to 2033 due to their adoption in primary care settings as a low-cost initial screening tool for nocturnal hypoxemia, with a key indicator of sleep disordered breathing. In 2023, the United Kingdom’s National Institute for Health and Care Excellence updated its OSA referral guidelines to recommend overnight oximetry for patients with high clinical suspicion but limited access to sleep services. Spain’s Ministry of Health launched a pilot program in Andalusia where general practitioners distribute disposable oximeters to at-risk patients, with data automatically transmitted to regional sleep units. These initiatives capitalize on oximetry’s simplicity, affordability, and non-invasiveness.

By Therapeutic Devices Insights

The Positive Airway Pressure (PAP) Devices segment accounted in holding a dominant share of the Europe Sleep Apnea Diagnostic Devices Market in 2025. PAP therapy remains the cornerstone of obstructive sleep apnea management, endorsed as first-line treatment for moderate to severe cases by the European Respiratory Society and national clinical bodies. This efficacy translates into tangible health outcomes, with a 2023 meta-analysis in the European Heart Journal confirming that consistent PAP use lowers the risk of stroke by 38 % and heart failure hospitalization by 32 % in OSA patients with cardiovascular disease.

The oral appliances segment is expected to register the fastest CAGR of 12.8% throughout the forecast period, with updated clinical guidelines that now position mandibular advancement devices as a first-line therapy for mild OSA and for CPAP-intolerant patients with moderate disease. In 2025, Germany’s statutory health insurers began reimbursing custom-fitted oral appliances under a new dental medical code by following positive health technology assessments showing 65% efficacy in reducing respiratory events.

COUNTRY LEVEL ANALYSIS

Germany Sleep Apnea Devices Market Analysis

Germany was the largest contributor in the Europe Sleep Apnea Devices Market by capturing 25.4% of share in 2025 with its comprehensive public healthcare system and early integration of sleep medicine into chronic disease management. Statutory health insurers have covered CPAP therapy since 2001 and expanded reimbursement in 2023 to include home sleep testing and connected PAP devices with remote monitoring. Germany also hosts major device manufacturers like Weinmann Emergency Medical Technology, which supplies both domestic and EU markets.

France Sleep Apnea Devices Market Analysis

France was ranked second by holding 17.2% of the Europe Sleep Apnea Diagnostic Devices Market share in 2025, with its centralized health policy and recent expansion of sleep apnea coverage. The French National Authority for Health updated its OSA management guidelines in 2023 to prioritize home polygraphy and mandate PAP therapy for all patients with an apnea hypopnea index above 15 and daytime sleepiness. According to Santé Publique France, over 4.2 million adults suffer from clinically significant OSA, yet diagnosis rates remain below 12 %, indicating substantial untapped potential. France’s combination of policy ambition, clinical innovation, and reimbursement inclusivity sustains its strong market momentum.

United Kingdom Sleep Apnea Devices Market Analysis

The United Kingdom sleep apnea devices market growth is likely to have a steady growth opportunity during the forecast period. In 2023, NHS England launched the Sleep Apnea Pathway Redesign Program, deploying home oximetry and polygraphy kits across 40 integrated care systems. Over 200,000 home tests were distributed in the first year, reducing wait times from 18 months to under 8 weeks in participating regions. The National Institute for Health and Care Excellence now recommends oral appliances for mild OSA, and NHS Wales began pilot reimbursement in 2025.

Italy Sleep Apnea Devices Market Analysis

Italy's sleep apnea devices market growth is fuelled by the high OSA prevalence and regional innovation in sleep care delivery. Italy also has a growing network of dental sleep clinics in urban centers. Cultural awareness is rising, with public campaigns by the Ministry of Health having increased OSA-related primary care consultations by 34% since 2022.

COMPETITIVE LANDSCAPE

The Europe Sleep Apnea Devices Market features intense competition among multinational corporations and specialized regional innovators, all vying for integration into publicly funded healthcare pathways. Competition is defined less by price and more by clinical validation, regulatory compliance, data security, and user-centric design. Global leaders like ResMed and Philips dominate through comprehensive ecosystems that combine hardware, software, and services, while niche players differentiate via comfort-focused interfaces or dental sleep solutions. The implementation of the EU Medical Device Regulation has raised quality and documentation barriers, favoring established firms with robust quality management systems. However, digital health startups are gaining traction by offering AI-powered diagnostic support or adherence analytics that complement existing devices. National reimbursement policies create fragmented but predictable demand, encouraging companies to tailor strategies by country.

KEY MARKET PLAYERS

A few of the notable companies operating in the europe sleep apnea devices market profiled in this report are

- ResMed, Inc. (U.S.)

- Philips Healthcare (Netherlands)

- Fisher & Paykel Healthcare Ltd. (New Zealand).

- SomnoMed Ltd. (Australia)

- Compumedics Limited (Australia)

- Weinmann Medical Devices GmbH (Germany)

- Whole You, Inc. (U.S.)

TOP LEADING PLAYERS IN THE MARKET

- ResMed is a global leader in sleep apnea diagnostics and therapy, with a strong footprint across Europe through its advanced PAP devices, cloud-based monitoring platforms, and home sleep testing solutions. The company supplies connected CPAP and APAP systems to national health services in Germany, the UK, and the Nordic countries, integrating therapy into digital care pathways. In 2025, ResMed expanded its European data center in Ireland to ensure full compliance with the EU General Data Protection Regulation while supporting real-time remote patient management. It also launched a new generation of ultra-quiet PAP devices with enhanced leak compensation algorithms, specifically calibrated for European facial anatomies.

- Philips Respironics, a division of Royal Philips, is a major contributor to the global sleep apnea market with a comprehensive portfolio spanning diagnostic polygraphs, PAP therapy systems, and integrated telehealth solutions. In Europe, the company collaborates with public health systems in France, Italy, and Spain to deploy bundled diagnostic and therapeutic programs. Following the 2021 recall, Philips undertook extensive remediation efforts, completing over 90 % of device replacements across the EU by early 2025.

- Fisher & Paykel Healthcare is a key player known for its patient-focused PAP interfaces and humidification technologies, which are widely adopted across European sleep centers. The company’s emphasis on comfort-driven design has made its nasal masks and heated tubing systems preferred accessories in both public and private care settings. In 2025, Fisher & Paykel launched a new adaptive PAP platform with integrated oximetry and automatic pressure adjustment tailored for European reimbursement criteria. It also expanded its clinical education program for respiratory therapists in Central and Eastern Europe, enhancing product adoption through professional training.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Sleep Apnea Devices Market focus on developing connected devices with remote monitoring capabilities to align with national telehealth initiatives. They invest in clinical evidence generation to support reimbursement applications and guideline inclusion across diverse EU health systems. Companies are enhancing user comfort through quieter motors, lighter masks, and personalized pressure algorithms to improve long-term adherence. Strategic partnerships with sleep clinics, primary care networks, and dental sleep practitioners expand access and referral pathways. Additionally, manufacturers prioritize compliance with the EU Medical Device Regulation by upgrading cybersecurity protocols and obtaining country-specific certifications to ensure seamless market entry and sustained trust.

MARKET SEGMENTATION

This research report on the europe sleep apnea devices market has been segmented and sub-segmented into the following categories.

By Diagnostic Devices

-

Polysomnography Devices

-

Ambulatory PSG Devices

- Clinical PSG Devices

-

- Respiratory Polygraphs

- Oximeters

- Single-Channel Screening Devices (Pulse Oximeters)

- Fingertip Pulse Oximeters

- Handheld Pulse Oximeters

- Wrist-Worn Pulse Oximeters

- Tabletop Pulse Oximeters

- Actigraphy Systems

By Therapeutic Devices

-

Positive Airway Pressure (PAP) Devices

-

CPAP Devices

- APAP Devices

- BPAP Devices

-

- Facial Interfaces

- Masks

- Nasal Masks

- Nasal Pillow Masks

- Full-Face Masks

- Masks

- Adaptive Servo-Ventilation Instruments (ASV)

- Airway Clearance Systems

- Oxygen Concentrators

- Stationary Concentrators

- Portable Concentrators

- Accessories

- Pillows

- Chin Restraints

- Mask Cleaning Wipes

- Other Accessories

- Oral Appliances

- Mandibular Advancement Devices

- Tongue Retaining Devices

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. Which device types are popular in the Europe Sleep Apnea Devices Market?

The Europe Sleep Apnea Devices Market is largely dominated by therapeutic devices such as CPAP, BiPAP machines, sleep apnea masks, and diagnostic tools like home sleep tests and polysomnography equipment.

2. What drives growth in the Europe Sleep Apnea Devices Market?

Growth in the Europe Sleep Apnea Devices Market is mainly driven by increased sleep apnea awareness, rising obesity rates,

an aging population, improved healthcare infrastructure, and expanded diagnostic services

across Europe.

3. Who are major players in the Europe Sleep Apnea Devices Market?

Major players in the Europe Sleep Apnea Devices Market include ResMed, Philips Respironics, Fisher & Paykel Healthcare, BMC Medical, SOMNOmedics, and other leading device manufacturers serving Europe.

4. Are home sleep testing devices available in the Europe Sleep Apnea Devices Market?

Yes, the Europe Sleep Apnea Devices Market offers a wide array of home sleep testing devices, which help diagnose sleep apnea remotely and increase patient access to sleep health assessments across Europe

5. What impact do government initiatives have on the Europe Sleep Apnea Devices Market?

Government initiatives in Europe, such as funding for sleep apnea awareness campaigns, subsidies for device purchases,

and regulatory support, have significantly boosted the adoption of sleep apnea devices.

6. Why is sleep apnea diagnosis rising across Europe?

Diagnosis rates in the Europe Sleep Apnea Devices Market are rising due to greater public awareness, emphasis on sleep health, advances in sleep labs,

and the availability of convenient home sleep monitoring solutions.

7. Which countries lead the Europe Sleep Apnea Devices Market?

The UK is recognized as the dominant country in the Europe Sleep Apnea Devices Market, followed by Germany, France, and other Western European states,

owing to advanced healthcare systems and robust device adoption.

8. What technological trends affect the Europe Sleep Apnea Devices Market?

The Europe Sleep Apnea Devices Market is influenced by technology trends such as the rise of wearable monitors, cloud-connected PAP machines,

telemedicine integration, and AI-powered therapy management solutions across Europe.

9. What are common symptoms driving device demand in the Europe Sleep Apnea Devices Market?

Persistent daytime fatigue, loud snoring, pauses in breathing during sleep, morning headaches,

and high blood pressure are common symptoms that drive the need for diagnostic and therapeutic devices in the Europe Sleep Apnea Devices Market.

10. How important is telemedicine in the Europe Sleep Apnea Devices Market?

Telemedicine plays a critical role in the Europe Sleep Apnea Devices Market by enabling remote diagnosis,

ongoing patient management, virtual consultations, and easier access to sleep apnea therapies for European patients.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com