Europe Smart Building Market Size, Share, Trends, & Growth Forecast Report Segmented By Solution (Security System, Safety System, and Others (Fire Door Control Systems, Others Parts, and Accessories)), Application (Residential and Commercial), Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) Industry Analysis From 2026 to 2034

Market Size, 2025

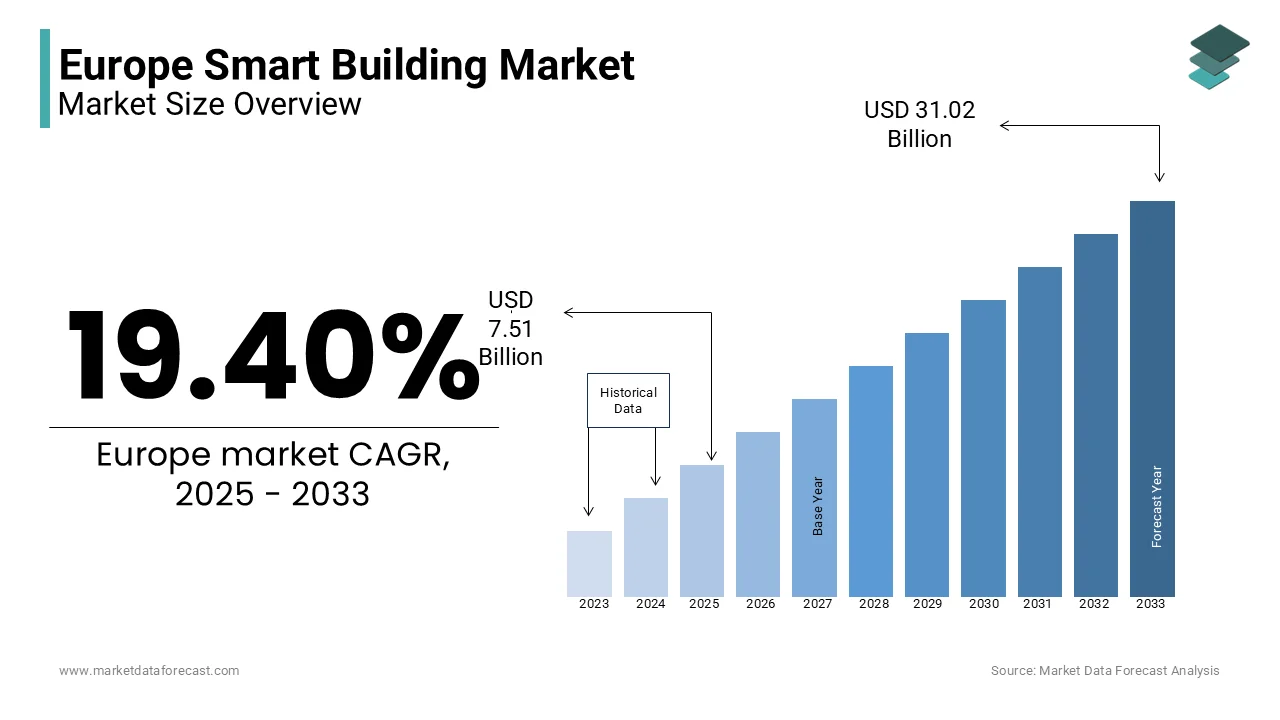

$7.51 BnMarket Estimate, 2026

$8.97 BnMarket Forecast, 2034

$37.04 BnCAGR, 2026–2034

19.40%Europe Smart Building Market Size

The Europe smart building market was worth USD 7.51 billion in 2025. The European market is estimated to reach USD 37.04 billion by 2034 from USD 8.97 billion in 2026, growing at a CAGR of 19.40% from 2026 to 2034.

Smart buildings are an integrated system that leverages Internet of Things sensors, artificial intelligence, and building management platforms to optimize energy use, occupant comfort, security, and operational efficiency across residential, commercial, and public infrastructure. These systems autonomously control lighting, heating, ventilation, access, and air quality based on real-time data and predictive analytics. The Energy Performance of Buildings Directive mandates that all new constructions be nearly zero energy by 2021 and requires member states to renovate 3% of public buildings annually. As per the European Environment Agency, over 35% of Europe’s building stock was constructed before 1970, lacking basic thermal or digital infrastructure. Simultaneously, the European Commission’s Digital Europe Programme has allocated 1.1 billion euros to deploy smart building technologies in cities through the Intelligent Cities Challenge.

MARKET DRIVERS

Stringent EU Energy Efficiency and Building Renovation Mandates

The European Union’s binding legislative framework for building energy performance for smart building adoption is driving the growth of the Europe smart buildings market. The revised Energy Performance of Buildings Directive requires all residential and commercial buildings to achieve at least energy class E by 2030 and class D by 2033, with non-compliance risking fines or rental restrictions. According to the European Commission, over 220 million buildings in the EU fail to meet current efficiency standards, necessitating deep retrofits. Smart building technologies such as adaptive HVAC controls, occupancy-based lighting, and real-time energy dashboards are essential to achieving these targets without a full structural overhaul. The Renovation Wave Strategy aims to double annual renovation rates from 1 to 2% enabling 35 million buildings to be upgraded by 2030. France’s Loi Climat et Résilience prohibits renting poorly insulated homes, while Germany’s Building Energy Act mandates digital energy monitoring in all new constructions. These regulations transform smart systems from optional enhancements into legal prerequisites, driving systematic deployment across public and private portfolios.

Rising Urbanization and Demand for Intelligent Public Infrastructure

Europe’s high urban density and growing city populations intensify demand for intelligent building solutions that enhance space efficiency, resource management, and citizen services is additionally fuelling the growth of Europe's smart buildings market. According to Eurostat, 75% of Europeans lived in urban areas in 2023, with metropolitan regions like Paris, Berlin, and Madrid exceeding 5 million residents. The European Commission’s 100 Climate Neutral Cities by 2030 mission mandates that selected cities deploy smart building technologies in municipal facilities, including schools, hospitals, and administrative offices. In Barcelona, for instance, all new public buildings since 2022 incorporate integrated building management systems that reduce energy use by 30% as verified by the city’s sustainability office. Similarly, Vienna’s Smart City Framework uses building-level data to optimize district heating loads across 300000 apartments.

MARKET RESTRAINTS

High Upfront Investment and Fragmented Retrofit Economics

The significant capital expenditure required for smart building retrofits to widespread adoption, especially in Europe’s vast portfolio of privately owned and heritage structures, is restraining the growth of Europe's small buildings market. Installing a comprehensive building management system in a mid-sized office can cost between 150000 and 400000 euros, according to the European Construction Technology Platform, with payback periods exceeding seven years in regions with low energy prices. In Southern and Eastern Europe, where household disposable income is lower, the return on investment appears even less compelling. Moreover, fragmented ownership in multi-unit residential buildings complicates consensus on shared investments.

Lack of Interoperability and Unified Data Standards

The absence of universal communication protocols and data interoperability standards across devices and platforms is also impeding the growth of the Europe smart buildings market. A typical smart building may integrate products from 10 or more vendors using incompatible systems such as BACnet, KNX, Modbus, and proprietary cloud APIs, preventing seamless integration. This fragmentation increases engineering costs, delays deployment, and locks owners into single vendor ecosystems. The European Telecommunications Standards Institute acknowledges that without common data models, buildings cannot participate in grid flexibility services or city-wide energy optimization. Although the EU’s Digital Twin initiative aims to create unified building information models, implementation remains voluntary and uneven.

MARKET OPPORTUNITIES

Integration with District Energy Systems and Grid Flexibility Services

Smart buildings in Europe are increasingly positioned as active participants in decentralized energy networks offering demand response and storage services to stabilize the grid, which is an opportunity for the growth of the Europe smart buildings market. As per the European Network of Transmission System Operators for Electricity, many commercial buildings across Germany, France, and the Netherlands are enrolled in demand side response programs that adjust HVAC and lighting loads during peak hours. The European Commission’s Clean Energy Package mandates that all new smart meters support remote load control, enabling buildings to provide frequency regulation and renewable energy balancing. In Helsinki, a pilot project aggregates 50 smart buildings into a virtual power plant that delivers 8 megawatts of flexible capacity to the national grid.

Public Procurement and Green Building Certification Incentives

Europe’s robust public procurement policies and green certification frameworks create powerful incentives for smart building deployment in institutional and commercial sectors, which is additionally prompting the growth of Europe's smart buildings market. National programs amplify this effect, where Sweden’s Green Building Council offers tax deductions for smart energy management, while the Netherlands provides accelerated depreciation for IoT-enabled HVAC systems. Additionally, the EU Taxonomy for Sustainable Activities classifies smart building retrofits as eligible economic activities attracting green bond financing. These policy levers de risk to private investment by guaranteeing compliance with future regulations and enhancing asset value through certified sustainability performance, making smart systems a strategic rather than operational decision.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Connected Building Infrastructure

The proliferation of Internet of Things devices in smart buildings introduces significant cybersecurity risks that undermine trust and regulatory compliance, which is a challenge for the growth of the Europe smart buildings market. According to the European Union Agency for Cybersecurity, 72% of smart building systems audited in 2023 had critical vulnerabilities allowing lateral movement into corporate networks. The EU’s Cyber Resilience Act, which takes full effect in 2025, will mandate secure by design principles and vulnerability disclosure for all connected products, yet compliance costs for small integrators remain high.

Shortage of Skilled Workforce for Design Integration and Maintenance

The lack of professionals trained in the multidisciplinary skills required to design, integrate, and maintain smart building systems combining HVAC, electrical, IT, and data analytics expertise is also one of the challenges for the growth of Europe's smart buildings market. According to the European Commission’s Pact for Skills, over 400000 building automation technicians will be needed by 2027, yet current vocational curricula remain siloed in traditional trades. In Eastern Europe, the gap is more acute, with fewer than 500 certified KNX professionals serving the entire region. The complexity of integrating legacy infrastructure with modern platforms further compounds the challenge; retrofitting a 1970s office building requires hybrid expertise few possess.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Solution, Application, and County. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Novoferm GmbH, Siemens AG, Bosch GmbH, GEZE GmbH, Johnson Controls, Hormann, Schüco International, ZKTeco Europe, S.L., Dormakaba, SALTO, SimonsVoss, Schneider Electric, ABB, Honeywell International Inc.,and Others. |

SEGMENTAL ANALYSIS

By Solution Insights

The security systems segment was the largest by occupying 47.4% of the Europe smart buildings market share in 2024, with the rising concerns over physical safety, regulatory mandates for access control, and integration with digital identity frameworks. European cities have seen a 22% increase in commercial property crime since 2020, according to the European Institute for Crime Prevention and Control, prompting businesses to invest in intelligent access management, video analytics, and perimeter intrusion detection. The European Union’s General Data Protection Regulation indirectly fuels adoption by requiring auditable access logs for sensitive facilities, which smart security platforms automate through biometric or credential-based entry systems. In Germany and France, national building codes now mandate electronic access control in all new public and multi-tenant commercial buildings. As per the European Construction Sector Observatory, over 80% of office developments completed in 2023 included facial recognition or mobile credential systems. Additionally, insurance providers like Allianz and AXA offer premium discounts of up to 15% for buildings with certified smart security infrastructure.

The safety systems segment is projected to grow with an anticipated CAGR of 18.2% throughout the forecast period, from stricter occupational health regulations and the integration of real-time environmental monitoring in post-pandemic workplace standards. The European Agency for Safety and Health at Work mandates continuous air quality and occupancy tracking in all workplaces exceeding 50 employees, driving deployment of CO2, particulate, and volatile organic compound sensors linked to HVAC automation. Companies like Siemens and Schneider Electric have responded with AI-powered systems that simulate fire or gas leak scenarios to optimize evacuation routes dynamically. A pilot in Stockholm’s Karolinska Hospital reduced emergency response time by 34% using integrated safety dashboards.

By Application Insights

The commercial applications segment was the largest by accounting for 68.3% of the Europe smart buildings market share in 2024 due to regulatory pressure, economic incentives, and the scale of operational savings achievable in offices, retail spaces, and public institutions. The Energy Performance of Buildings Directive requires all new commercial constructions to incorporate energy monitoring and automated controls, with retrofits mandated for existing stock by 2030. As per the study, commercial buildings consume 45% more energy per square meter than residential units, making them prime targets for efficiency upgrades. In cities like Amsterdam and Copenhagen, municipal regulations prohibit leasing office space below energy class C without smart metering and adaptive lighting. Corporate sustainability reporting under the EU Corporate Sustainability Reporting Directive further compels multinational tenants to demand intelligent infrastructure from landlords.

The residential segment is likely to grow with an anticipated CAGR of 19.4% throughout the forecast period, with national renovation subsidies, digitalization of housing, and rising consumer demand for comfort and energy autonomy. The European Commission’s Renovation Wave Strategy allocates 37 billion euros to support smart retrofits in private homes, with countries like Italy and Spain offering grants covering up to 110% of costs for energy-efficient upgrades, including smart thermostats and lighting. In France, the MaPrimeRénov scheme processed over 1.2 million applications in 2023, with 42% including smart home components. Additionally, rising electricity prices have driven consumer interest in self-optimization using smart heating controls reduced winter bills by 23% on average. The proliferation of interoperable platforms like Matter and Apple HomeKit has also simplified installation, reducing reliance on professional integrators.

COUNTRY LEVEL ANALYSIS

Germany Smart Buildings Market Analysis

Germany was the largest contributor in the Europe smart buildings market with 24.3% of share in 2024, with the stringent energy regulations, advanced industrial integration, and high public investment in building digitalization. The German Building Energy Act mandates that all new constructions incorporate smart metering and automated climate control, while the Federal Ministry for Economic Affairs and Climate Action has allocated 4.2 billion euros under the Building Efficiency Program to subsidize retrofits. German engineering firms like Siemens, Bosch, and RWE lead in developing interoperable platforms that link building data to district heating and grid flexibility services. This regulatory rigor, technological capability, and financial backing position Germany as the continent’s smart building innovation and implementation leader.

France Smart Buildings Market Analysis

France smart buildings market was accounted in holding second position by capturing 18.2% of the market share in 2024, with its ambitious energy renovation policies and centralized public procurement framework. The Loi Climat et Résilience prohibits renting residential or commercial properties below energy class E from 2023 and class D from 2028, driving mass adoption of smart thermostats and energy dashboards. As per France’s Ministry of Ecological Transition, over 850000 MaPrimeRénov grants included smart home components in 2023 alone. The French government also mandates that all new public buildings integrate Building Information Modeling and real-time monitoring under the E+C certification scheme. Paris leads in urban deployment with 100% of new social housing since 2022, featuring centralized smart systems for lighting, heating, and security. Companies like Legrand and Schneider Electric leverage domestic policy to export standardized platforms across Southern Europe. France’s blend of regulatory enforcement, financial incentives, and public sector leadership sustains its position as a high-volume smart building market with strong social equity dimensions.

United Kingdom Smart Buildings Market Analysis

The United Kingdom smart buildings market growth is likely to be driven by the post-Brexit regulatory autonomy, high commercial real estate standards, and consumer-driven smart home adoption. The UK’s Future Buildings Standard requires all new non-domestic buildings from 2025 to produce 80% lower carbon emissions, mandating advanced automation and on-site monitoring. As per the UK Green Building Council, over 70% of London’s Grade A office stock now features AI-powered building management systems that optimize energy use based on occupancy patterns. Companies like BG Group and Honeywell have launched retrofit packages compliant with the Smart Export Guarantee, enabling homes to participate in demand response.

COMPETITIVE LANDSCAPE

Competition in the Europe smart buildings market is characterized by a mix of industrial automation giants, building technology specialists, and agile software startups vying for influence across fragmented national markets. Established players like Siemens, Schneider Electric, and Honeywell dominate large-scale commercial and public projects through integrated hardware and software ecosystems and deep regulatory expertise. Meanwhile, specialized firms such as ABB, Legrand and Johnson Controls compete on niche strengths in lighting, access control, or HVAC optimization. Startups focus on AI analytics, cybersecurity, and user experience ,often partnering with incumbents to scale. The market lacks price-based rivalry; instead, differentiation hinges on complianc,e interoperabilit,y and sustainability credentials. National policies create uneven landscapes, with Germany and France favoring domestic champions, while Nordic countries emphasize open data and citizen well-being.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe smart building market include

- Novoferm GmbH

- Siemens AG

- Bosch GmbH

- GEZE GmbH

- Johnson Controls

- Hormann

- Schüco International

- ZKTeco Europe, S.L.

- Dormakaba

- SALTO

- SimonsVoss

- Schneider Electric

- ABB

- Honeywell International Inc.

TOP PLAYERS IN THE MARKET

- Siemens AG is a foundational force in the Europe smart buildings market through its comprehensive Desigo CC building management platform that integrates HVAC, lightin,g security, and energy systems into a unified operational interface. The company leverages its deep industrial automation expertise to deliver interoperable solutions compliant with European standards such as BACnet and KNX. In 2024, Siemens launched its AI-powered Desigo PX controller with edge computing capabilities enabling predictive maintenance and real-time grid interaction across commercial portfolios. It also partnered with the City of Vienna to retrofit 200 public buildings with carbon tracking dashboards aligned with the EU Taxonomy. These initiatives reinforce Siemens’s global leadership in sustainable building infrastructure while accelerating Europe’s transition to climate-neutral and human-centric built environments.

- Schneider Electric SE significantly shapes the Europe smart buildings market via its EcoStruxure Building solution, which connects IoT devices, cloud analytics, and energy management into a scalable digital ecosystem. The company focuses on both commercial retrofits and residential smart home integration with strong alignment to EU energy efficiency directives. In early 2024, Schneider Electric collaborated with ENGIE to deploy its Building Advisor AI across 500 French public schools, enablinga 25% energy reduction through occupancy-based climate control. It also enhanced its Wiser home platform with Matter protocol support, ensuring cross-brand compatibility for European consumers.

- Honeywell International Inc. plays a pivotal role in the Europe smart buildings market through its Enterprise Buildings Integrator platform that unifies securit,y safety and energy systems with advanced cybersecurity and compliance features. The company emphasizes interoperability and future proofing, particularly in high-value sectors such as healthcare, finance and airports. In 2024, Honeywell introduced its Smart Building Sustainability Suite in partnership with British Land, enabling real-time carbon accounting and EU CSRD-compliant reporting across London office portfolios. It also expanded its European cybersecurity certification portfolio under the EU Cyber Resilience Act, ensuring all connected devices meet secure by design requirements. These actions position Honeywell as a trusted partner for mission-critical facilities seeking resilient, intelligent, and regulation-ready building operations across Europe and globally.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe smart buildings market prioritize interoperability by adopting open protocols such as KNX, BACnet, and Matter to overcome vendor lock-in and enable seamless system integration. They embed artificial intelligence at the edge to deliver predictive maintenance, occupancy-based optimization, and grid flexibility services without compromising data privacy. Companies actively align their platforms with European regulatory framework,s including the Energy Performance of Buildings Directive, EU Taxonomy, and Cyber Resilience Act, to ensure compliance and market access. Strategic partnerships with utilities public agencies, and real estate owners facilitate large-scale deployment and co-funded retrofits.

MARKET SEGMENTATION

This research report on the Europe smart building market is segmented and sub-segmented into the following categories.

By Solution

- Security System

- Access Control System

- Smart Door Lock

- Biometric Door Locks

- Smart Card Door Locks

- Electric Strike Door Locks

- Others (Keypad Door Lock)

- Safety System

- Others (Fire Door Control Systems, Other Parts, and Accessories)

By Application

- Residential

- Commercial

- Hotel

- Healthcare

- Retail

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. Which countries lead the europe smart building market?

Countries like Germany, the UK, France, Italy, and the Netherlands dominate the europe smart building market with advanced infrastructure

2. What are key drivers of growth in the europe smart building market?

Energy efficiency, sustainability initiatives, urbanization, and increasing IoT adoption drive growth in the europe smart building market

3. How does technology impact the europe smart building market?

Advanced technologies such as AI, IoT, and big data analytics enable smart automation and operational efficiency in the europe smart building market

4. What role does sustainability play in the europe smart building market?

Sustainability is a major focus in the europe smart building market, with solutions geared toward reducing energy consumption and carbon footprints

5. What are the main segments of the europe smart building market?

Main segments include energy management, building security, lighting control, HVAC automation, and facility management within the europe smart building market

6. How important is building automation in the europe smart building market?

Building automation is a critical component of the europe smart building market, enabling real-time monitoring and control for improved efficiency

7. What is the impact of urbanization on the europe smart building market?

Rapid urbanization boosts demand for smart infrastructure solutions, strongly influencing the growth of the europe smart building market

8. How does the europe smart building market address security concerns?

Integrated security systems including surveillance, access control, and fire detection are vital parts of the europe smart building market

9. What trends are shaping the europe smart building market?

Key trends include AI-driven automation, IoT device integration, predictive maintenance, and occupant-centric building management

10. How does the residential sector contribute to the europe smart building market?

Smart home technologies for lighting, security, and climate control significantly contribute to the europe smart building market growth

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com