Europe Smart Inhalers Market Research Report – Segmented By Product Type, Disorder, End-User, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) – Industry Analysis on Size, Share, Trends, & Growth Forecast (2025 to 2033)

Europe Smart Inhalers Market Size

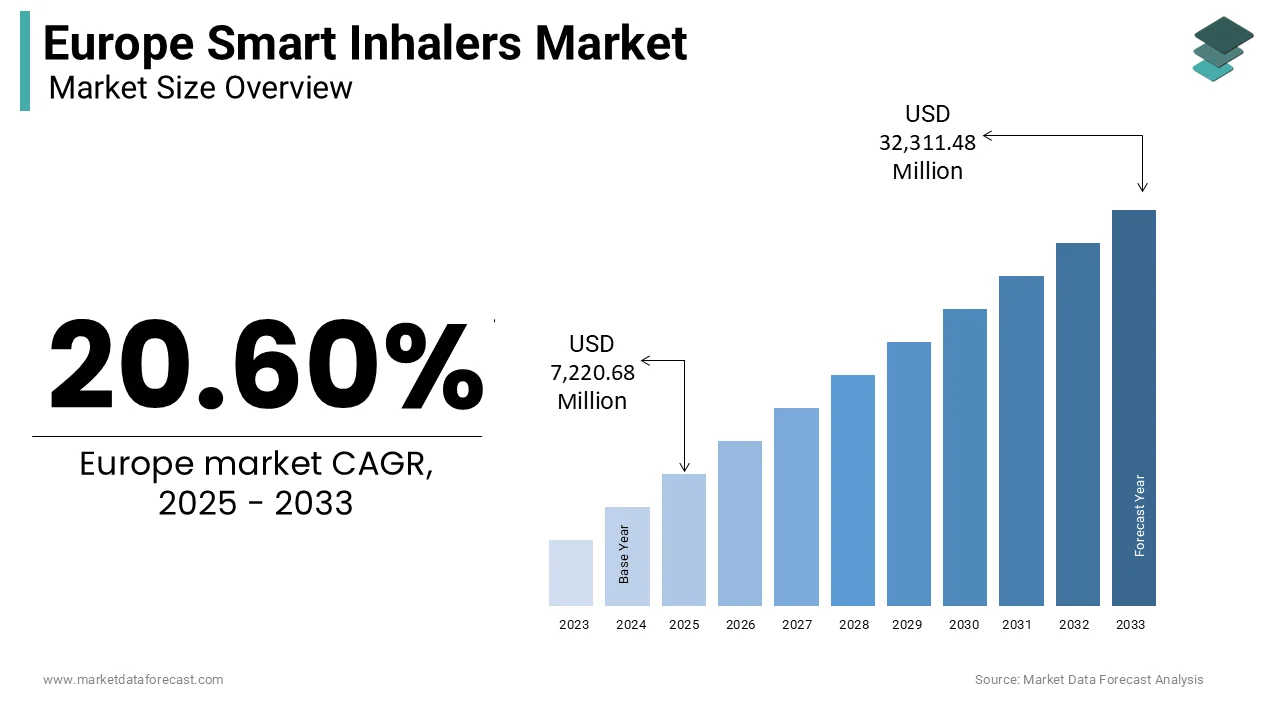

The Europe Smart Inhalers Market was valued at USD 5,987.30 million in 2024, is estimated to reach USD 7,220.68 million in 2025, and is projected to reach USD 32,311.48 million by 2033, growing at a CAGR of 20.6% from 2025 to 2033.

Smart inhalers are advanced medical devices that combine traditional inhaler technology with digital features, such as sensors and Bluetooth connectivity, to help manage respiratory diseases like asthma and COPD more effectively. These systems provide real-time feedback to users and generate actionable data for clinicians, transforming passive drug delivery into an interactive care modality. The market’s evolution is not driven by commercial trends alone but by pressing public health imperatives. According to the European Respiratory Society, over 30 million people in the European Union suffer from asthma, while chronic obstructive pulmonary disease affects millions, collectively contributing to notable annual deaths. Furthermore, the European Commission’s Digital Transformation of Health and Care initiative has prioritized connected medical devices as essential tools for chronic disease management. This clinical urgency, regulatory support, and technological maturity define the strategic foundation of the Europe Smart Inhalers Market.

MARKET DRIVERS

High Prevalence of Chronic Respiratory Diseases Fuels Clinical Need for Adherence Monitoring

The escalating burden of asthma and chronic obstructive pulmonary disease across regions surges the growth rate of the Europe smart inhalers market. A pivotal factor driving smart inhaler use is the documented gap between prescribed and actual medication use. As per the European Lung Foundation, a portion of patients with chronic respiratory conditions demonstrate incorrect inhaler technique, while non-adherence rates range from 30 to 70 percent depending on the region and patient demographics. These behavioral shortcomings directly contribute to avoidable emergency visits. Smart inhalers address this by capturing objective usage data and delivering personalized coaching via smartphone applications. National health systems in countries like the United Kingdom and Sweden have begun integrating these devices into integrated care pathways, which recognize their potential to reduce system strain and improve long-term outcomes.

EU Digital Health Policies Accelerate Integration of Connected Inhalers into Care Pathways

The European Union’s strategic push toward digital health infrastructure is creating a favorable ecosystem, which further fuels the expansion of the Europe smart inhalers market. Smart inhalers align directly with this vision by generating standardized, real-time adherence data that can be integrated into electronic health records under the EU’s Electronic Health Record Exchange Format initiative. Furthermore, the Medical Device Regulation 2017 745 provides a clear classification framework for software as a medical device, enabling companies to obtain CE marking for companion apps that analyze inhaler use patterns. Also, France’s Health Data Hub now accepts anonymized smart inhaler data for real-world evidence generation. These policy enablers reduce market access barriers and incentivize healthcare providers to adopt digital respiratory solutions as part of value-based care models.

MARKET RESTRAINTS

Reimbursement Limitations Across European Countries Restrict Widespread Adoption

Reimbursement hurdles impede patient access, which restricts the growth of the Europe smart inhalers market. In the United Kingdom, the National Institute for Health and Care Excellence has not issued formal guidance on smart inhalers, leaving local clinical commissioning groups to make fragmented funding decisions. This financial barrier is especially important given that respiratory diseases disproportionately affect lower-income populations. The market for smart inhalers is significantly hindered by the lack of harmonized reimbursement and national formulary policies, which keep them from moving beyond a niche, premium product to a standard of care.

Data Privacy and Cybersecurity Concerns Affect Patient and Provider Trust

The collection and transmission of sensitive health data by smart inhalers raises legitimate concerns regarding privacy and security under Europe’s stringent regulatory regime, and this also affects the expansion of the smart inhalers market. According to sources, respiratory data collected through connected medical devices can expose sensitive personal details such as activity patterns, location, and health condition, making it subject to strict privacy protection requirements under European regulations. As per research, recent assessments in France revealed that many smart inhaler applications still fall short in ensuring complete data security or obtaining clear user consent for sharing information with external partners. These vulnerabilities deter both patients and clinicians. Moreover, the lack of standardized cybersecurity certification for medical IoT devices creates uncertainty for manufacturers and healthcare institutions. The scalability of smart inhaler solutions across the region will remain limited until robust, transparent, and auditable data governance frameworks are universally adopted.

MARKET OPPORTUNITIES

Integration with National Telehealth Platforms Enables Scalable Remote Monitoring

Region’s rapid expansion of telehealth infrastructure creates a new opportunity for the growth of the Europe smart inhalers market. According to sources, many EU countries have established national telemedicine strategies since 2020, with remote chronic disease management as a core pillar. In Denmark, while the national health portal Sundhed.dk serves as a hub for general health information, patient medical records, and prescriptions, the integration of smart inhaler data into primary care dashboards for general practitioners is handled through specific, project-based initiatives rather than a standardized feature of the national platform. The European Commission’s Cross-Border Healthcare Directive further facilitates data portability, enabling patients to maintain continuity of care while traveling. Smart inhalers provide an easy, scalable way for healthcare providers to digitize respiratory care and engage with patients continuously, which aligns with the shift toward proactive and preventive health models.

Partnerships with Pharmaceutical Companies Drive CCo-Development and Co-Commercialization

Strategic alliances between digital health firms and pharmaceutical manufacturers are unlocking new commercial and clinical pathways, which in turn provide potential prospects for the expansion of the Europe smart inhalers market. These collaborations leverage the pharma companies’ distribution networks, regulatory expertise, and patient access programs to accelerate adoption. The rise of value-based pricing in Europe is pushing drug manufacturers to form partnerships. This allows them to demonstrate real-world outcomes and encourages co-innovation and market growth.

MARKET CHALLENGES

Interoperability Gaps Between Health Systems Hinder Seamless Data Exchange

The absence of universal technical standards prevents smart inhaler data from flowing seamlessly across fragmented healthcare ecosystems, which challenges the growth of the Europe smart inhalers market. According to sources, a smaller percentage of national electronic health record systems in the EU support Fast Healthcare Interoperability Resources or other common data models required for device integration. In practice, this means that a patient using a smart inhaler in Italy may generate data that cannot be accessed by a specialist in Belgium due to incompatible formats or authentication protocols. This technical burden increases development costs and delays time to market, which ultimately slows the realization of connected respiratory care at scale.

Limited Health Literacy and Digital Skills Among Elderly Patients Reduce Effective Utilization

The primary user base for smart inhalers includes older adults with chronic obstructive pulmonary disease, many of whom face significant barriers to digital engagement, and this hampers the expansion of the Europe smart inhalers market. The digital divide is particularly acute in rural regions of countries like Romania, Bulgaria, and Greece, where broadband access and smartphone ownership remain low. Even when devices are provided, a lack of ongoing support leads to suboptimal utilization. The clinical and equitable benefits of smart inhalers will not be realized for the most vulnerable populations unless targeted interventions, such as simplified user interfaces, voice guidance, and community-based digital literacy programs, are implemented.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product Type, Disorder, End-user and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe |

| Market Leaders Profiled | Vectura Group plc, Teva Pharmaceutical Industries Ltd., GlaxoSmithKline plc, Boehringer Ingelheim GmbH, AstraZeneca plc, Adherium Limited, Cohero Health, LLC, Propeller Health, GlaxoSmithKline plc, OPKO Health, Inc. |

SEGMENTAL ANALYSIS

By Product Type Insights

In 2024, the inhalers segment led the Europe Smart Inhalers Market by capturing a substantial share 2024. Their portability, ease of use, and alignment with outpatient management of chronic respiratory diseases drive the growth of the inhalers segment in the regional market. Unlike nebulizers, which require electricity, compressors, and longer administration times, inhalers, particularly pressurized metered dose and dry powder variants, are designed for daily self-administration by patients in home or community settings. The integration of digital sensors into existing inhaler platforms has been seamless, leveraging established user habits without requiring behavioral retraining. This pharmaceutical preference strengthens the centrality of inhalers in treatment protocols. Focus on the benefits of smart inhalers. Given that smart inhalers are built on a familiar delivery system, their rapid adoption is driven by user convenience, clinical ease of use, and compatibility with real-world adherence tracking, which cements their status as a foundational element of the digital respiratory ecosystem.

The nebulizers segment is predicted to witness the highest CAGR of 14.2% from 2025 to 2033. The rapid expansion of the nebulizers segment is driven by niche clinical applications and technological modernization. Traditionally used in hospitals and for pediatric or elderly patients with limited coordination, nebulizers are now being re-engineered with smart capabilities for home use. According to studies, a large number of children in the EU suffer from severe asthma requiring nebulized therapy, and adherence in this group is particularly challenging to monitor. Smart nebulizers equipped with usage sensors and cloud connectivity now enable caregivers and clinicians to track treatment completion remotely. These innovations are transforming nebulizers from passive devices into intelligent care tools by unlocking growth in vulnerable populations previously underserved by standard smart inhalers.

By Disorder Insights

The asthma segment was the largest share of the Europe Smart Inhalers Market by occupying 58.1% share in 2024. Its high prevalence among younger and tech-literate populations who readily adopt digital health tools has significantly contributed to the dominance of the asthma segment. The demographic is inherently more comfortable with smartphone applications and digital feedback by facilitating sustained engagement with smart inhaler platforms. National asthma management guidelines in countries explicitly recommend adherence monitoring for patients with uncontrolled symptoms by creating a clinical mandate for digital solutions. Furthermore, school-based asthma programs have begun incorporating smart inhaler data into care coordination, enabling teachers and nurses to identify at-risk students. The combination of early disease onset, behavioral malleability, and policy support ensures asthma remains the primary driver of smart inhaler utilization across Europe.

The chronic obstructive pulmonary disease segment is estimated to register the fastest CAGR of 16.8% from 2025 to 2033. The swift expansion of the chronic obstructive pulmonary disease segment is fueled by aging demographics, hospital avoidance strategies, and value-based healthcare reforms. Health systems are under intense pressure to reduce costly exacerbations. Smart inhalers offer a scalable solution by detecting usage lapses and poor technique that often precede crises. The transition to outcome-based contracts is accelerating the adoption of these devices in high-cost, high-burden patient groups, specifically because the devices can demonstrate reduced exacerbation rates.

By End User Insights

The patients segment dominated the Europe Smart Inhalers Market and accounted for a substantial share in 2024. The dominance of the patients segment is due to direct engagement, with patients using companion apps to track doses, receive reminders, and review inhalation technique feedback. National digital health strategies further strengthen this trend. Real-world evidence from Sweden shows that patient-led use of smart inhalers correlates with a reduction in rescue medication use over one year. Moreover, direct-to-consumer marketing by manufacturers, compliant with EU medical device regulations, has raised awareness among tech-savvy patient communities. This user-centric design philosophy, combined with policy support for patient empowerment, ensures that individuals remain the primary adopters and beneficiaries of smart inhaler technology.

The R and D segment is anticipated to witness the fastest CAGR of 18.3% during the forecast period. The demand for real-world evidence and regulatory science has largely fuelled the growth of the R and D segment. Pharmaceutical companies and academic institutions are increasingly utilizing smart inhalers as data collection platforms in clinical trials and post-marketing surveillance. The shift responds to regulatory expectations for objective usage data, which traditional patient diaries fail to provide reliably. Besides, regulatory bodies like Germany’s Paul Ehrlich Institute now accept smart inhaler data for pharmacovigilance assessments. The EU's reinforced Medical Device Regulation, which requires real-world performance evidence, will cause the R&D applications market segment to expand, making it more vital and valuable than ever.

COUNTRY LEVEL ANALYSIS

Germany Market Analysis

Germany was the top performer in the Europe smart inhalers market and accounted for a 22.6% share in 2024. The domination of Germany in the regional market is due to its advanced healthcare infrastructure, strong regulatory framework, and proactive digital health policies. The country’s statutory health insurance system covers a portion of the population and has begun piloting reimbursement for digital therapeutics, including connected inhalers, under the Digital Health Applications Ordinance. Furthermore, Germany hosts key European headquarters for both pharmaceutical and digital health companies, fostering co-innovation. The combination of payer openness, clinical need, and industrial ecosystem supports Germany’s role as the region’s innovation and adoption leader.

United Kingdom Market Analysis

The United Kingdom was the second largest in the European smart inhalers landscape and captured a 19.6% share in 2024. The growth of the United Kingdom is led by centralized healthcare procurement and early integration of digital tools into national pathways. As per research, a large number of people across the United Kingdom are currently treated for asthma, and early trials in major cities have shown that connected inhaler technology can help reduce emergency visits and improve overall disease management. The Medicines and Healthcare products Regulatory Agency maintains a streamlined approval process for Class IIa digital medical devices, enabling rapid market entry. The UK presents a key opportunity for the development and testing of scalable smart inhaler technology for the European market, thanks to its strong academic ties and digitally-enabled patient base.

France Market Analysis

France is another key player in the smart inhalers market, with its universal healthcare coverage and national digital health transformation agenda. The French National Authority for Health has issued guidance supporting the use of connected devices for chronic disease management, and the Health Data Hub now facilitates anonymized smart inhaler data sharing for research. The policy has spurred adoption in both urban and rural regions, where telemedicine is expanding. Furthermore, France’s robust medtech innovation ecosystem, supported by Bpifrance funding, has nurtured several homegrown smart inhaler start-ups. These structural and policy enablers ensure France’s continued influence in shaping digital respiratory care standards.

Sweden Market Analysis

Sweden is growing gradually in the European smart inhalers market due to its digitized healthcare system, high public trust in e-health, and focus on preventive care. The country’s national e-health strategy mandates interoperability across all digital health tools, and smart inhaler data can be seamlessly integrated into the national patient portal 1177.se. Sweden’s commitment to sustainability also favours reusable sensor-based inhalers over single-use alternatives. Sweden's advanced digital infrastructure, from near-universal smartphone adoption to its robust public health system, provides a powerful case study for rapid and large-scale smart inhaler adoption.

Netherlands Market Analysis

The Netherlands is predicted to expand in the European smart inhalers market during the forecast period due to its integrated care models and dominance in health data innovation. The Dutch healthcare system emphasizes disease management programs for chronic conditions, and since 2022, several insurers, including Menzis and CZ, have included smart inhalers in their chronic care packages for asthma and chronic obstructive pulmonary disease. The country’s Personal Health Train initiative enables secure analysis of smart inhaler data without centralizing sensitive information by addressing privacy concerns. Academic medical centers in Utrecht and Leiden are actively involved in validating digital endpoints for regulatory use. This blend of payer innovation, technical infrastructure, and clinical research cements the Netherlands as a key hub for smart inhaler development and deployment in Europe.

COMPETITIVE LANDSCAPE

The Europe Smart Inhalers Market features a dynamic competitive landscape shaped by digital health innovators, pharmaceutical technology firms, and medtech specialists vying for integration into increasingly value-based healthcare systems. Competition is not primarily price-driven but centers on clinical validation, regulatorycompliancece data security, t, and interoperability with national digital health infrastructures. Leading companies differentiate through robust evidence partnerships with payers and seamless electronic health record integration. The market is further characterized by high entry barriers due to stringent EU Medical Device Regulation requirements and the need for extensive clinical validation. While large players leverage global scale and pharmaceutical alliances, smaller firms compete through niche innovations such as environmental sensing or orpedpediatric-focusedgn. National variations in reimbursement, digital mmatumaturity respiratory disease burden create a fragmented,opportunity-rich environment where localized strategies and policy alignment determine long-term success.

KEY MARKET PLAYERS

A few of the notable companies operating in the europe smart inhalers market profiled in this report are

- Vectura Group plc

- Teva Pharmaceutical Industries Ltd.

- GlaxoSmithKline plc

- Boehringer Ingelheim GmbH

- AstraZeneca plc

- Adherium Limited

- Cohero Health, LLC

- Propeller Health

- GlaxoSmithKline plc

- OPKO Health, Inc.

TOP LEADING PLAYERS IN THE MARKET

- Propeller Health is a pioneering force in the Europe Smart Inhalers Market with a globally recognized platform that combines sensor-enabled inhalers and data analytics to improve respiratory care. The company’s solutions are integrated into national health systems across the United Kingdom, Germany, and France, where they support remote patient monitoring and clinical decision making. Propeller Health has collaborated with major European healthcare providers and insurers to demonstrate cost savings through reduced exacerbations and hospitalizations. These innovations support its prominence in delivering evidence-based digital respiratory therapeutics aligned with European value-based care objectives.

- Vectura Group plays an important role in the Europe Smart Inhalers Market through its deep expertise in inhaled drug delivery and strategic focus on connected devices. As a UK-based pharmaceutical technology company, Vectura develops both proprietary smart inhaler platforms and partnerships with global drug manufacturers to embed digital capabilities into existing therapies. The company’s Smart Respiratory Portfolio includes sensor-integrated dry powder and pressurized metered dose inhalers designed for seamless patient use. This initiative exemplifies its commitment to bridging pharmaceutical innovation with digital health to improve outcomes across Europe’s respiratory disease landscape.

- Adherium Limited contributes significantly to the Europe Smart Inhalers Market through its clinically validated Smartinhaler platform, which is widely used in research and routine care settings across Sweden,n the Netherlands, and Italy. The company specializes in low-power sensor technology that attaches to standard inhalers without altering drug formulation or regulatory status. Adherium has established partnerships with academic institutions and public health agencies to generate real-world evidence on adherence and inhalation technique. Most recently, the company integrated its platform with national electronic health record systems in Denmark, allowing clinicians to access adherence reports during virtual consultations. This interoperability focus strengthens its position as a trusted enabler of data-driven respiratory care in highly digitized European healthcare environments.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Smart Inhalers Market prioritize strategic collaborations with national health systems and pharmaceutical companies to embed their solutions into standard care pathways. They invest heavily in generating real-world clinical evidence to demonstrate cost-effectiveness and health outcomes for reimbursement negotiations. Regulatory preparedness is central for firms ensuring full compliance with the EU Medical Device Regulation and General Data Protection Regulation through robust cybersecurity and data governance frameworks. Companies also focus on user-centric design by developing simplified interfaces, voice guidance,a nd multilingual support to enhance accessibility for elderly and pediatric populations. Apart from these, they leverage cloud-based analytics and artificial intelligence to transform raw inhaler data into actionable clinical insights, enabling proactive intervention and personalized therapy adjustments across diverse European healthcare settings.

MARKET SEGMENTATION

This research report on the europe smart inhalers market has been segmented and sub-segmented into the following categories.

By Product Type

- Nebulizers

- Inhalers

By Disorder

- Chronic Obstructive Pulmonary Disease

- Asthma

- Others

By End-user

- Patients

- R&D

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving the growth of the Europe Smart Inhalers Market?

The Europe Smart Inhalers Market growth is driven by increasing asthma and COPD prevalence, rising air pollution, and the shift toward digital healthcare monitoring. Technological innovation and better medication adherence systems further boost its adoption.

2. What are the major segments in the Europe Smart Inhalers Market?

The Europe Smart Inhalers Market is segmented by product (metered-dose inhalers, dry powder inhalers), by indication (asthma and COPD), and by distribution channel (hospitals, pharmacies, online).

Each segment shows strong growth due to AI and IoT integration in devices

3. Which countries lead the Europe Smart Inhalers Market?

Germany, the UK, and France dominate the Europe Smart Inhalers Market due to advanced healthcare infrastructure and strong digital health policies. The Nordic region is also showing high adoption of connected inhalers.

4. Who are the key players in the Europe Smart Inhalers Market?

Prominent companies in the Europe Smart Inhalers Market include Teva Pharmaceutical, AstraZeneca, Philips Respironics, Vectura Group, and FindAir. These firms focus on R&D and strategic partnerships to enhance connectivity features

5. How is technology influencing the Europe Smart Inhalers Market?

AI, IoT, and Bluetooth integration in inhalers have revolutionized patient adherence tracking and data collection.

These innovations transform inhalers into real-time health monitoring tools across European markets.

6. What challenges are limiting the Europe Smart Inhalers Market?

The Europe Smart Inhalers Market faces challenges such as high device costs, data privacy concerns related to GDPR, and limited awareness in some regions.

However, compliance-driven innovation is steadily overcoming these barriers

7. How does air pollution affect the Europe Smart Inhalers Market?

Increasing air pollution in Europe is directly contributing to a higher incidence of respiratory diseases, driving smart inhaler adoption.

Governments and hospitals promote connected inhaler devices to combat pollution-linked illnesses.

8. What role does digital health play in the Europe Smart Inhalers Market?

Digital health initiatives across Europe support integration of respiratory monitoring apps with smart inhalers.

This convergence improves remote care, medication adherence, and reduces hospital visits.

9. What are the trends shaping the future of the Europe Smart Inhalers Market?

Rising R&D investment, AI data analytics, and partnerships between pharmaceutical and tech firms define the future trends. Cloud integration for patient management and predictive healthcare analytics lead the innovation wave.

10. How are COPD patients benefiting from the Europe Smart Inhalers Market?

Smart inhalers help COPD patients track inhalation frequency, receive dosage reminders, and transmit data to healthcare providers for real-time monitoring.

This enhances disease management and reduces hospitalization rates.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com