Europe Smart Wearables Market Size, Share, Trends & Growth Forecast Report By Product, End User and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, From (2026 to 2034)

Market Size, 2025

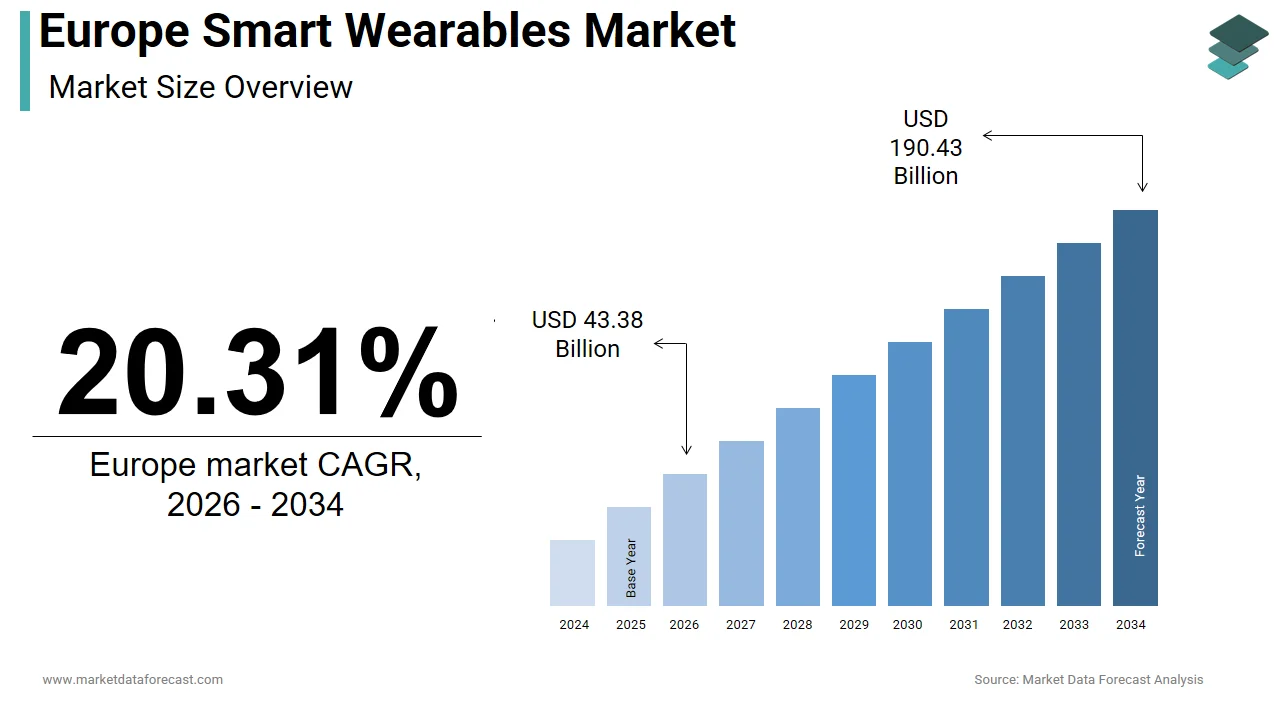

$36.06 BnMarket Estimate, 2026

$43.38 BnMarket Forecast, 2034

$190.43 BnCAGR, 2026–2034

20.31%Europe Smart Wearables Market Summary

The Europe smart wearables market is witnessing rapid expansion, driven by the accelerating adoption of connected health devices, growing integration of biometric data into national preventive care and remote monitoring programs, and the increasing convergence of consumer wellness wearables with regulated medical technologies.

Market Snapshot (2026 to 2034)

- Current Market Value (2026): USD 43.38 billion

- Projected Market Value (2034): USD 190.43 billion

- Growth Velocity (CAGR): 20.31%

- Base Year Value (2025): USD 36.06 billion

- Primary Product Segment: Smartwatches (42.3% share)

- Fastest-Growing Segment: Medical-Grade Wearable Devices

- Top Regional Hub: Germany (23.3% share)

Strategic Market Segments

- Dominant Product (Smartwatches): Smartwatches remain the leading revenue contributor, driven by their evolution from fitness accessories into multifunctional health and lifestyle ecosystems integrating ECG, sleep analytics, blood oxygen monitoring, and stress tracking within secure smartphone platforms.

- High-Growth Segment (Medical Wearables & Remote Monitoring Devices): Medical-grade wearable biosensors and clinically validated monitoring patches are expanding rapidly, supported by reimbursement inclusion in chronic disease management programs and formal adoption under EU digital health and telemedicine frameworks.

Country-Level Performance

- Germany (23.3%): The regional market leader, Germany’s dominance is supported by strong consumer trust in privacy-compliant platforms, high employer adoption of wellness wearables, deep integration into remote patient monitoring pilots, and strict GDPR-aligned data localization standards.

- United Kingdom: A frontrunner in digital health pilots and hearables adoption, with NHS-backed remote monitoring programs using wearables for cardiac and diabetes care, alongside strong consumer uptake of premium smartwatch ecosystems.

- France: Growth is driven by reimbursement pathways for digital therapeutics, medical-grade ECG wearables, and large-scale state-funded elderly care and fall-detection initiatives under national e-health strategies.

- Netherlands & Sweden: The Netherlands leads in corporate wellness and interoperable health data platforms, while Sweden demonstrates high public trust in medical wearables and strong clinical research adoption in remote cardiac monitoring.

Competitive Landscape & Market Trends

The Europe smart wearables market is transitioning from lifestyle-focused devices toward clinically validated, privacy-secure, and reimbursement-supported digital health ecosystems.

- Healthcare Integration & Remote Monitoring: Wearables are increasingly embedded into national telehealth, chronic care, and preventive health programs.

- Data Protection & Sovereign Cloud Processing: Manufacturers prioritize GDPR compliance, EU-based servers, on-device analytics, and cybersecurity resilience.

- Mental Health & Recovery Analytics: Demand is rising for stress, sleep, and cognitive well-being metrics across corporate wellness and personal care.

- Right-to-Repair & Circular Economy Compliance: Design shifts toward replaceable components, sustainability, and extended software support align with EU policy mandates.

Leading Companies

The market includes a mix of global consumer electronics leaders, specialized health-tech firms, and regulated medical wearable manufacturers:

- Consumer & Multiplatform Ecosystem Leaders: Apple, Samsung, Huawei, Sony, Qualcomm

- Health & Medical Wearable Innovators: Philips • Omron • Withings SAS • LifeWatch AG • Vital Connect

- Sports, Fitness & Performance-Tracking Specialists: Garmin • Polar Electro • Adidas Group

- Legacy & Connected Device Manufacturers: Nokia Technologies • Drägerwerk AG & Co. KGaA

Europe Smart Wearables Market Size

The size of the Europe smart wearables market was valued at USD 36.06 billion in 2025. This market is expected to grow at a CAGR of 20.31% from 2026 to 2034 and be worth USD 190.43 billion by 2034 from USD 43.38 billion in 2026.

Smart wearables are electronic devices worn on the body that integrate sensors, connectivity, and data processing to monitor health, enhance fitness, or deliver contextual information. This category includes smartwatches, fitness trackers, smart rings, hearables, and medical-grade biosensors used for preventive and clinical purposes. The unique regulatory framework, where consumer devices fall under the Radio Equipment Directive, while health monitoring features increasingly intersect with the EU Medical Devices Regulation if they claim diagnostic or therapeutic functionality. According to the European Commission’s Digital Economy and Society Index, 54% of EU citizens used a health or fitness app in 2023, with 38% owning a connected wearable device. As per Eurostat, over 112 million Europeans aged 16 to 74 actively tracked physical activity using digital tools, reflecting deep integration into daily wellness routines. The European Data Protection Board has issued specific guidance on biometric data processing from wearables, requiring explicit consent and data minimization under the General Data Protection Regulation. Additionally, the EU’s Cyber Resilience Act now mandates baseline security standards for all connected devices, influencing firmware design and update protocols. These intersecting forces of digital health adoption, privacy enforcement, and cybersecurity regulation shape the evolving landscape of the Europe smart wearables market.

MARKET DRIVERS

Integration of Wearables into National Digital Health and Preventive Care Strategies

Governments are actively incorporating smart wearables into public health initiatives to reduce chronic disease burden and optimize healthcare spending, which is driving the growth of Europe smart wearables market. According to the European Observatory on Health Systems and Policies, 14 EU member states now include validated wearable data in national preventive care programs, with Finland’s “Active Life” initiative reimbursing fitness trackers for prediabetic citizens who achieve activity targets. The European Commission’s Digital Europe Programme allocated EUR 210 million in 2023 to scale AI-driven remote monitoring ecosystems, many reliant on wearable biosensors.

Rising Consumer Demand for Holistic Wellness and Mental Health Monitoring

The European consumers increasingly seek wearables that offer insights into stress recovery and sleep quality, reflecting a cultural shift toward holistic well-being. The rising consumer demand for holistic wellness and mental health monitoring is additionally fuelling the growth of Europe smar wearables market. In Sweden and the Netherlands, where workplace well-being laws mandate employer attention to mental health, companies like Spotify and Philips provide staff with Oura rings to optimize recovery and reduce burnout. Startups like Finland’s Firstbeat and Germany’s Moodmetric have developed validated algorithms that translate biometric data into actionable well-being scores, increasingly integrated into corporate HR platforms. This expansion from fitness quantification to emotional and cognitive health positions wearables as central to Europe’s broader wellness economy.

MARKET RESTRAINTS

Stringent EU Data Privacy and Biometric Consent Requirements

The General Data Protection Regulation imposes significant compliance burdens on wearable manufacturers handling sensitive biometric data, such as heart rate, electrocardiograms, and sleep patterns. The stringent EU data privacy and biometric consent requirements are restraining the growth of Europe smart wearables market. According to the European Data Protection Board, continuous physiological monitoring qualifies as “special category data” under Article 9 by requiring explicit user consent and purpose limitation. As per the European Consumer Organisation, 61% of wearable privacy policies fail to clearly explain data retention periods or third-party sharing practices by creating legal vulnerability. Additionally, the upcoming European Health Data Space Regulation will require certified health wearables to use standardized data formats and secure gateways, increasing development costs. These regulatory hurdles delay product launches, deter startups, and force global brands to maintain separate EU data architectures, constraining innovation and market entry.

Limited Clinical Validation and Regulatory Ambiguity for Health Claims

Many wearable health features operate in a regulatory gray zone, where diagnostic claims trigger medical device classification but general wellness statements lack clinical proof. The limited clinical validation and regulatory ambiguity for health claims are hampering the growth of Europe smart wearables market. In Germany, health insurers reject reimbursement for unvalidated devices, limiting adoption despite consumer interest. A 2023 study by the Karolinska Institute found that sleep staging algorithms in popular trackers deviated from polysomnography by up to 48 minutes on average, undermining reliability. Until the EU establishes clear conformity assessment pathways for digital biomarkers, manufacturers face uncertainty in marketing health features, stifling investment in clinically meaningful innovation, and eroding consumer trust in wellness claims.

MARKET OPPORTUNITIES

Expansion into Employer-Sponsored Digital Therapeutics and Corporate Wellness Programs

Smart wearables are gaining traction as prescribed tools in employer-funded digital therapeutics, creating a high-value B2B2C opportunity beyond retail. The expansion into employer-sponsored digital therapeutics and corporate wellness programs is creating new opportunities for the growth of Europe's smart wearables market. According to the European Agency for Safety and Health at Work, 58% of large EU companies now offer digital wellness programs, with wearables serving as the primary data capture layer. In the Netherlands, the national health insurer CZ partners with employers to provide Garmin devices to employees enrolled in diabetes prevention programs, with incentives tied to activity milestones. The European Commission’s Horizon Europe funding stream has allocated EUR 150 million to workplace health innovation, prioritizing AI-driven interventions powered by wearable biosensors.

Adoption in Remote Patient Monitoring Under National Reimbursement Schemes

The formal integration of wearables into reimbursed remote patient monitoring, aligned with EU healthcare digitization goals, is expected to elevate the growth of Europe smart wearables market. According to the European Health Telematics Observatory, 9 EU countries now reimburse connected wearables as part of chronic disease management, with Italy’s national health service covering prescription-grade devices for heart failure patients since 2023. In Denmark, the Sundhedsdatastyrelsen approved the use of Apple Watch ECG data in public cardiology clinics, enabling earlier atrial fibrillation detection. The EU’s Digital Europe Programme supports national efforts to build interoperable health data infrastructures by ensuring wearable data can flow securely into electronic health records. As reimbursement frameworks mature and clinical evidence accumulates, wearables will shift from consumer gadgets to regulated medical tools, unlocking institutional budgets and long-term sustainability.

MARKET CHALLENGES

Fragmented Connectivity Standards and Interoperability Barriers

The technical fragmentation in data exchange due to incompatible health platforms and proprietary ecosystems is hindering the growth of Europe smart wearable market. According to the European Institute for Health Records, consumer wearables can seamlessly integrate with national electronic health record systems like Germany’s ePA or France’s DMP. The lack of standardized APIs for digital biomarkers prevents aggregation across devices by limiting AI model training on diverse populations.

Short Product Lifecycles and E-Waste Concerns Under the Right to Repair Framework

Rapid obsolescence and non-replaceable batteries in smart wearables conflict with the EU’s sustainability and circular economy mandates, triggering regulatory and reputational risks. The EU’s Ecodesign for Sustainable Products Regulation, effective from 2025, will require all wearables to offer battery replacement, standardized chargers, and 7-year software support. In 2023, the European Commission’s Right to Repair initiative identified wearables as a priority category, mandating spare part availability and repair manuals. Manufacturers face costly redesigns to comply, while consumers grow wary of disposable electronics.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Apple Inc, Covidien Plc, Philips Electronics, Fitbit Inc., LifeWatch AG, Polar Electro, Jawbone, Sotera Wireless, Pebble Technology Corp., Drägerwerk AG & Co. KGaA, Omron Corp., Samsung Electronics Co Ltd, Huawei, Lifesense Group, Adidas Group, Qualcomm Technologies, Inc, Sony Corporation, Withings SAS, Garmin, Nokia Technologies, Vital Connect, and Everist Genomics. |

SEGMENTAL ANALYSIS

By Product Insights

The smartwatches segment accounted in holding 42.3% of the Europe smart wearables market share in 2024. Smartwatches lead because they have evolved beyond timekeeping into indispensable lifestyle and health hubs that consolidate multiple daily functions. Health integration is equally important, where new smartwatches sold in Germany and France in 2023 included FDA and CE-certified ECG and blood oxygen sensors. Furthermore, seamless integration with iOS and Android ecosystems ensures automatic call message and app notifications by reducing smartphone dependency.

The Medical Devices segment is projected to expand at the fastest CAGR of 24.7% from 2025 to 2033. Medical wearables are accelerating due to inclusion in publicly funded remote patient monitoring programs across Europe. The French National Authority for Health approved 14 new wearable-based digital therapeutics in 2023, each requiring CE Class IIa certification and clinical validation. These reimbursements transform wearables from out-of-pocket purchases into accessible clinical tools, driving volume through physician prescriptions rather than consumer marketing. The Medical Devices Regulation provides a clear conformity assessment pathway that builds trust among clinicians and payers. The regulation mandates clinical evidence, risk management, and post-market surveillance, ensuring reliability that consumer devices lack. Startups like Germany’s Vasomedical and France’s Chronolife have leveraged this framework to secure partnerships with hospital networks and health insurers.

COUNTRY-LEVEL ANALYSIS

Germany Smart Wearables Market Analysis

Germany was the top performer of the Europe smart wearables market by capturing 23.3% of the market share in 2024, functioning as the region’s most mature and regulation-conscious adopter. The high digital literacy, robust healthcare integration, and strong consumer demand for data privacy-compliant devices are attributed to fuelling the growth of the market in this country. The country’s stringent enforcement of the General Data Protection Regulation has made local consumers wary of non-EU data handling, favoring brands like Garmin and Withings that process data within Europe. Germany remains the benchmark for sustainable, regulated wearable adoption in Europe with deep integration into both consumer wellness and clinical pathways.

United Kingdom Smart Wearables Market Analysis

The United Kingdom smart wearables market growth is likely to grow with the rapid adoption of hearables and smartwatches with advanced health features. According to the UK Office for National Statistics, 63% of adults used a connected wearable in 2023, the highest rate in Europe, driven by strong brand presence and NHS digital health pilots. The National Health Service launched 28 remote monitoring programs in 2023 using wearables for diabetes and cardiac rehabilitation, partnering with Apple and Omron. The UK’s post Brexit regulatory autonomy has enabled faster approval of novel digital biomarkers through the Medicines and Healthcare products Regulatory Agency.

France Smart Wearables Market Analysis

France smart wearables market growth is driven by the state-led digital health initiatives and strong demand for medical wearables. According to France’s National Agency for the Safety of Medicines and Health Products, 12 wearable-based digital therapeutics received reimbursement approval in 2023 under the “Digital Health Pass” program. The French Data Protection Authority enforces strict biometric consent rules, pushing manufacturers to adopt on-device processing. Withings and Nokia Health lead with EU-hosted data centers. The government’s “Ma Santé 2022” strategy allocated EUR 180 million to equip 500,000 elderly citizens with fall detection wearables by 2025.

Netherlands Smart Wearables Market Analysis

The Netherlands wearables market growth is likely to grow with the emergence as a leader in corporate wellness and interoperable health data ecosystems. The country’s national health data infrastructure, LSP, enables secure sharing of wearable data with general practitioners used by 1.2 million citizens in 2023, as per the Ministry of Health. Dutch consumers prioritize sustainability; iFixit Europe rated Dutch brands like Fairphone Wear as top for repairability. The government’s Digital Health Action Plan mandates FHIR-based APIs for all health apps by 2025, ensuring seamless integration.

Sweden Smart Wearables Market Analysis

Sweden smart wearables market growth is likely to grow with the early adoption of medical wearables and strong public trust in digital health. According to the Swedish eHealth Agency, 68% of regional healthcare providers use CE-certified wearables for remote patient monitoring, with Karolinska University Hospital running Europe’s largest cardiac patch trial. The country’s national digital ID system, BankID, enables secure authentication for health apps, boosting adoption. Swedish consumers favor privacy by design, brands like Minut and Moodmetric lead with on-device AI that avoids cloud transmission.

COMPETITIVE LANDSCAPE

The Europe Smart Wearables Market features intense competition among global tech giants, specialized health tech firms, and emerging medical device innovators. Differentiation centers on regulatory compliance, clinical validation, data sovereignty, and ecosystem integration, rather than hardware specifications alone. Apple and Samsung dominate the consumer segment through brand loyalty and platform lock-in, while European companies like Withings and Garmin gain traction in health-focused niches by emphasizing medical certification and privacy. Barriers to entry are high due to the need for CE medical device approval, adherence to the Cyber Resilience Act, and investment in local data infrastructure. The market is bifurcating between lifestyle wearables and clinically validated devices, with the latter increasingly funded through public health systems.

KEY MARKET PLAYERS

The leading companies operating in the Europe smart wearables market include:

- Apple Inc

- Covidien Plc

- Philips Electronics

- Fitbit Inc.

- LifeWatch AG

- Polar Electro

- Jawbone

- Sotera Wireless

- Pebble Technology Corp.

- Drägerwerk AG & Co. KGaA

- Omron Corp.

- Samsung Electronics Co. Ltd

- Huawei

- Lifesense Group

- Adidas Group

- Qualcomm Technologies, Inc.

- Sony Corporation

- Withings SAS

- Garmin

- Nokia Technologies

- Vital Connect

- Everist Genomics

TOP PLAYERS IN THE MARKET

- Apple Inc is a dominant global technology company whose Apple Watch has become the benchmark for smartwatches in Europe. The company integrates advanced health sensors, including ECG, blood oxygen, and temperature tracking, with seamless iOS ecosystem functionality. Apple has strengthened its European position by achieving CE certification for medical features, ensuring compliance with the EU Medical Devices Regulation. The company also processes all European health data within EU-based data centers in Ireland and Denmark to align with General Data Protection Regulation requirements. In recent years, Apple expanded clinical partnerships with hospitals in Germany and the UK to validate its atrial fibrillation and sleep apnea detection algorithms, enhancing credibility in the Europe Smart Wearables Market.

- Samsung Electronics Co., Ltd. is a leading global consumer electronics manufacturer with a strong presence in Europe, through its Galaxy Watch series. The company offers comprehensive health monitoring, including body composition analysis, stress tracking, and advanced sleep coaching tailored to European wellness preferences. Samsung has reinforced its market position by ensuring full compliance with the EU Cyber Resilience Act and by integrating its wearables with European health platforms such as Germany’s ePA and France’s DMP through standardized APIs.

- Withings SAS is a French digital health company specializing in clinically validated smart wearables, including hybrid smartwatches and medical-grade trackers. The company’s products are designed to meet stringent EU Medical Devices Regulation standards with features like medical ECG and atrial fibrillation detection. Withings has strengthened its position by securing reimbursement approval from national health authorities in France, Germany, and the Netherlands for its connected health solutions. The company processes all user data exclusively within European servers and emphasizes device repairability and long-term software support, aligning with EU right to repair and circular economy mandates in the Europe Smart Wearables Market.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Smart Wearables Market prioritize compliance with the EU Medical Devices Regulation and General Data Protection Regulation by implementing on-device data processing and EU-based cloud infrastructure. They pursue clinical validation through partnerships with hospitals and national health agencies to secure reimbursement eligibility. Companies integrate wearables with national electronic health record systems using standardized FHIR APIs to enable seamless data flow. Strategic localization includes region-specific health features, wellness programs, and multilingual support. Additionally, they design products for longevity with replaceable batteries, seven-year software updates, and repairable components to meet EU Ecodesign and right to repair requirements.

MARKET SEGMENTATION

This Europe smart wearables market research report is segmented and sub-segmented into the following categories.

By Product

- Smartwatches

- Head-mounted Displays

- Smart Clothing

- Ear Worn

- Fitness Trackers

- Body-worn Camera

- Exoskeleton

- Medical Devices

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the size of the Europe smart wearables market?

The Europe smart wearables market reached USD 43.38 billion in 2026, projected to hit USD 190.43 billion by 2034 at 13.98% CAGR, driven by health features.

What defines the Europe smart wearables market?

The Europe smart wearables market includes wrist devices, eyewear, and patches tracking health metrics through advanced sensors and apps.

How does the Europe smart wearables market evolve?

The Europe smart wearables market advances with AI insights and 5G connectivity enabling real-time wellness coaching features.

What drives growth in the Europe smart wearables market?

Health consciousness and remote monitoring needs propel the Europe smart wearables market across fitness and medical uses.

Who leads the Europe smart wearables market?

Tech giants like Apple and Garmin dominate the Europe smart wearables market with ecosystem integrations.

What role do smartwatches play in the Europe smart wearables market?

Smartwatches lead wrist-wear tracking heart rate in the Europe smart wearables market consumer segment.

How prominent are fitness bands in the Europe smart wearables market?

Bands offer affordable activity monitoring within the Europe smart wearables market entry-level category.

What impact do hospitals have on the Europe smart wearables market?

Hospitals adopt wearables for patient monitoring, boosting the Europe smart wearables market medical applications.

How does AI influence the Europe smart wearables market?

AI provides predictive health alerts expanding the Europe smart wearables market intelligent features.

What is eyewear's place in the Europe smart wearables market?

Smart glasses grow for AR fitness in the Europe smart wearables market emerging form factors.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com