Europe Social Commerce Market Size, Share, Trends & Growth Forecast Report, Segmented By Business Model (B2B, B2C, C2C), Product Type And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis From (2025 To 2033)

Europe Social Commerce Market Size

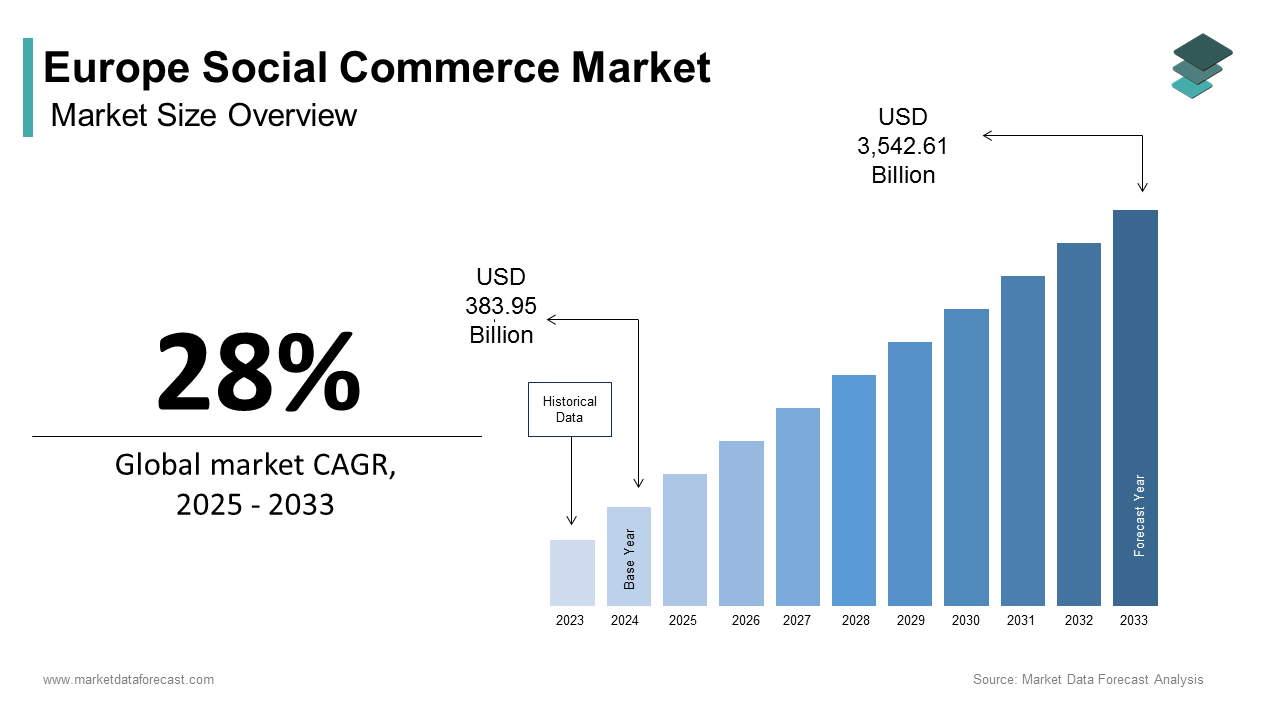

The Europe social commerce market size was calculated at USD 383.95 billion in 2024 and is anticipated to reach USD 3,542.61 billion by 2033, from USD 491.49 billion in 2025, growing at a CAGR of 28% during the forecast period.

Social commerce in Europe refers to the integration of social media platforms with e-commerce functionalities, enabling consumers to discover, purchase, and share products within a social environment. Unlike conventional online retail, this model leverages user-generated content, peer recommendation, and interactive live shopping to drive engagement and conversion. The European digital landscape is uniquely positioned for social commerce growth due to high internet penetration and widespread social media adoption across diverse age groups. According to Eurostat data for 2023, approximately 86 percent of individuals aged 16 to 74 in the European Union used the internet on a daily basis, while around 59 percent of EU citizens actively engaged with social media platforms. Furthermore, a significant cultural shift towards mobile-first digital experiences has redefined consumer expectations, with real-time interactions and community validation becoming central to purchasing decisions. Countries have emerged as early adopters where platforms like Instagram, TikTok, and Pinterest increasingly serve as storefronts rather than mere communication channels. This behavioral transformation, supported by evolving digital infrastructure and regulatory clarity around digital services, sets the foundation for social commerce to mature beyond its nascent phase in the region.

MARKET DRIVERS

Rising Mobile Internet Penetration Fuels Impulse Buying Behavior

The proliferation of mobile internet access in the region has fundamentally reshaped consumer shopping habits, a change that accelerates the growth of the Europe social commerce market and creates fertile ground for social commerce adoption. Mobile devices now serve as the primary gateway for digital engagement, with consumers spending notable hours and minutes daily on mobile apps. This sustained screen time often occurs on visually driven platforms such as Instagram and TikTok, where shoppable posts and in-app checkout options minimize friction between discovery and purchase. Crucially, the immediacy afforded by mobile connectivity heightens susceptibility to impulse buying, especially among younger demographics. The behavioral shift is further amplified by the seamless integration of digital wallets and buy-now-pay-later services native to mobile ecosystems. Consequently, social platforms are evolving into closed-loop commerce environments where browsing, recommendation, and payment occur within a single mobile session, thereby accelerating conversion rates and reinforcing the centrality of mobile infrastructure in scaling social commerce across Europe.

Influencer Marketing Builds Trust and Drives Product Discovery

Authentic influencer engagement has emerged as a cornerstone of consumer trust in the region’s social commerce ecosystem and directly influences purchasing intent through perceived credibility and relatability, which further drives the expansion of the Europe social commerce market. Unlike traditional advertising, influencer-driven content fosters peer-like interactions that resonate particularly with digitally native audiences. This trust stems from the perception of authenticity. Moreover, platforms are increasingly optimizing discovery algorithms to prioritize content from trusted creators, thereby amplifying organic reach. TikTok’s algorithm, for example, favors engagement depth over follower count, which elevates niche influencers whose audiences exhibit high intent and loyalty. This dynamic enables brands to access hyper-targeted communities without relying on broad-based ad campaigns. The resulting alignment between influencer credibility and consumer values not only accelerates product discovery but also cultivates long-term brand affinity within Europe’s fragmented and culturally diverse markets.

MARKET RESTRAINTS

Fragmented Data Privacy Regulations Impede Platform Integration

The region’s stringent and heterogeneous data protection landscape is a significant operational barrier to the seamless integration required for effective social commerce, and this restricts the growth of the Europe social commerce market. While the General Data Protection Regulation establishes a baseline framework for consumer data rights, its interpretation and enforcement vary across member states, creating compliance uncertainty for platforms and sellers alike. This environment discourages social platforms from embedding deep commerce functionalities such as cross-platform user tracking, personalized retargeting, or shared customer profiles, which are essential for optimizing conversion funnels. For example, Meta has publicly acknowledged limitations in its ability to synchronize shopping data between Instagram and Facebook within the EU due to divergent national supervisory authority rulings. Similarly, payment processors integrated into social apps must navigate country-specific consent requirements for transaction data storage, further complicating checkout experiences. These regulatory frictions not only increase development costs but also fragment the user journey, reducing the fluidity that defines successful social commerce ecosystems in less regulated regions. Consequently, European merchants often operate with reduced analytical capabilities, hindering their ability to refine targeting and personalize offers at scale.

Cultural and Linguistic Diversity Limits Content Scalability

The absence of a unified cultural and linguistic framework in the region constrains the expansion of the Europe social commerce market. This affects the scalability of social commerce campaigns that rely heavily on localized content and contextual relevance. The EU's 24 official languages and nationally shaped consumer preferences mean that a viral campaign that succeeds in Sweden could fall flat in Portugal, which emphasizes the variations in humor, aesthetic sensibilities, and product expectations across the continent. The fragmentation is particularly acute for live shopping and influencer collaborations, where real-time interaction demands linguistic fluency and cultural nuance. For instance, a beauty brand leveraging TikTok Live in France must engage French-speaking hosts who understand local beauty standards and regulatory disclosures around cosmetic claims, unlike those in Poland or Greece. Moreover, algorithmic recommendation engines struggle to curate relevant content across language borders, reducing organic reach for multinational sellers. Unlike homogenous markets where a single creative asset can achieve continent-wide impact, European players must deploy decentralized content strategies, multiplying production costs and operational complexity. This barrier disproportionately affects small and medium enterprises lacking the resources for multilingual creative teams, thereby stifling inclusive participation in the social commerce boom.

MARKET OPPORTUNITIES

Integration of Augmented Reality Enhances Virtual Try-On Experiences

The incorporation of augmented reality into social platforms is opening major opportunities for the growth of the Europe social commerce market. This creates the pathway for immersive product interaction, particularly in fashion, beauty, and home decor sectors across Europe. AR-powered virtual try-on features allow consumers to visualize products in real time through their smartphone cameras, significantly reducing purchase hesitation and return rates. Platforms like Instagram and Snapchat have accelerated this trend by offering open AR development tools enabling brands to create custom try-on lenses without requiring native app development. Similarly, beauty retailers have seen conversion rates double on AR-enabled product pages. The appeal of AR lies not only in utility but also in shareability, as users often post their virtual try-on experiences, generating organic peer exposure. The continued refinement of social platforms' augmented reality (AR) software development kits (SDKs) presents an opportunity to transform passive users into active participants within a visual commerce ecosystem that connects digital and physical retail.

Emergence of Social Audio Commerce in Niche Communities

The rise of social audio platforms and voice-based engagement is creating fresh prospects for the expansion of the Europe social commerce market. While visual platforms dominate mainstream social commerce, audio channels such as Clubhouse X Spaces and audio-enabled Discord servers foster intimate conversations where expertise and authenticity drive purchasing decisions. This format is particularly effective in knowledge-intensive categories like organic food, premium supplements, and sustainable fashion, where consumers seek detailed product narratives and ethical validation. Moreover, in the Netherlands, vegan skincare brands have leveraged Dutch language audio sessions to address ingredient transparency concerns, building loyalty among ethically driven buyers. Unlike algorithm-driven feeds, audio commerce thrives on scheduled, real-time interaction, which cultivates anticipation and exclusivity.

MARKET CHALLENGES

Logistical Fragmentation Undermines Cross-Border Fulfillment

The absence of a harmonized last-mile delivery framework in the region poses a persistent challenge to the Europe social commerce market. This affects the scaling of social commerce beyond national borders. Social platforms often facilitate spontaneous cross-border purchases, yet fulfillment remains hampered by disparate carrier networks, customs protocols, and return policies that erode consumer confidence. As per sources, only a share of European online shoppers expressed willingness to buy from a seller in another EU country, primarily due to concerns over delivery delays and return complexity. This fragmentation is particularly acute for social commerce, where impulse buys lack the deliberation typical of traditional e-commerce, leading to higher return expectations. Even within Western Europe, carriers apply inconsistent dimensional pricing and packaging requirements, complicating integration with automated checkout systems. Platforms like TikTok Shop have struggled to implement unified delivery tracking across markets due to incompatible national postal codes and customs declaration formats. This logistical disarray not only inflates operational costs but also diminishes the seamlessness that defines successful social commerce experiences, thereby constraining market expansion and consumer reach.

Platform Algorithm Volatility Disrupts Merchant Visibility

Frequent and opaque changes to social media algorithms significantly affect the predictability of merchant visibility and customer acquisition in the Europe social commerce market. Platforms routinely adjust their ranking systems to prioritize certain content types or user behaviors, often without advance notice or clear documentation, leaving sellers vulnerable to sudden drops in organic reach. Instagram’s shift toward prioritizing Reels over static image posts, for instance, caused fashion microbrands to lose up to a share of their follower interaction. This volatility forces merchants to constantly reallocate budgets toward paid promotion to maintain visibility, eroding the cost advantage that initially made social commerce attractive to small enterprises. Moreover, the lack of transparency in algorithmic criteria prevents sellers from optimizing content effectively since best practices become obsolete overnight. This environment fosters dependency on platform whims rather than sustainable audience building, ultimately stifling innovation and discouraging long-term investment in social selling channels across the region.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 28% |

| Segments Covered | By Business Model, Product Type, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Meta Platforms, Inc., ByteDance Ltd., Pinterest, Inc., Alibaba Group Holding Limited, Tencent Holdings Ltd., Pinduoduo Inc., Snap, Inc., Google LLC, Shopify Inc., Amazon.com, Inc. |

SEGMENTAL ANALYSIS

By Business Model Insights

The business-to-consumer segment held the largest share of the Europe social commerce market in 2024. The dominance of the business-to-consumer segment is propelled by direct brand engagement through visually driven platforms where immediacy, personalization, and influencer collaboration converge to drive conversion. Consumers across Europe increasingly bypass traditional e-commerce sites in favor of seamless in-app purchasing experiences offered by Instagram, TikTok, and Pinterest. A further factor supporting B2C dominance is the rise of shoppablivestreamsam, where real-time demonstrations and limited-time offers create urgency. Furthermore, major retailers such as Zalando and H&M have embedded native checkout within social platforms, reducing friction and improving basket completion rates. The segment also benefits from robust digital payment adoption. These dynamics position B2C not merely as a sales channel but as an integrated brand storytelling medium that aligns with evolving consumer expectations for authenticity, immediacy, and interactivity.

The consumer-to-consumer segment is expected to exhibit a noteworthy CAGR of 28.4% between 2025 and 2033. The swift expansion of the consumer-to-consumer segment is fuelled by the proliferation of peer-led resale and secondhand marketplaces embedded within social ecosystems where users list, sell, and negotiate directly without intermediary retailers. Platforms like Vinted, Depop, and Facebook Marketplace have become central to circular consumption patterns, particularly among sustainability-conscious youth. The model thrives on trust-based interactions enabled by user ratings, verified profiles, and integrated escrow payment systems that reduce fraud risk. Additionally, the cost-of-living pressures across Europe have intensified demand for affordable alternatives. These behavioral and economic forces are transforming C2C from a niche activity into a mainstream commerce engine.

By Product Type Insights

The apparel segment was the largest segment in the Europe social commerce market by holding a 38.5% share in 2024. The prominence of the apparel segment is attributed to the visual and trend-driven nature of fashion, which aligns seamlessly with the content formats favored by social platforms such as short-form video lookbooks and influencer styling reels. Consumers increasingly rely on peer-generated visuals rather than static product pages. Fast fashion brands have capitalized on this by deploying real-time trend algorithms that convert TikTok hashtags into inventory decisions within hours by enabling hyper-responsive supply chains. Furthermore, the integration of size recommendation tools and virtual try-on features has significantly reduced return rates, which historically plagued online apparel sales. The segment also benefits from high engagement during seasonal transitions. These synergies between visual storytelling, rapid trend cycles, and technology-enhanced decision making solidify apparel’s central role in Europe’s social commerce evolution.

The personal and beauty care segment is predicted to witness the highest CAGR of 26.1% from 2025 to 2033 due to the experiential nature of beauty products, which thrive in interactive formats such as live tutorials, skin tone matching filters, and user-generated before and after content. Platforms like Instagram and TikTok have become de facto beauty consultation spaces where consumers seek real-time advice on formulations, shades, and routines. The rise of clean and personalized beauty has further amplified this trend as consumers demand transparency about ingredients and ethical sourcing. In addition, brands have built cult followings by fostering community-led discussions around ingredient efficacy directly on social channels. Additionally, regulatory clarity under the EU Cosmetic Products Regulation enables confidence in platform claims, reducing legal risk for creators. These factors converge to position beauty not just as a product category but as a participatory social experience uniquely suited to platform native commerce.

REGIONAL ANALYSIS

United Kingdom Social Commerce Market Analysis

The United Kingdom dominated the Europe social commerce market and accounted for 22.7% in 2024. The UK's domination of the regional market is primarily driven by high digital literacy, early adoption of mobile payments, and a culture of influencer engagement that permeates mainstream shopping behaviour. Most UK internet users access social media daily, with platforms serving as primary discovery engines for fashion, beauty, and lifestyle products. The country benefits from a dense ecosystem of digital native brands such as Gymshark and Charlotte Tilbury that pioneered direct-to-consumer social selling models long before the trend spread continent-wide. Additionally, the UK’s regulatory openness to live shopping trials has enabled rapid experimentation. This fertile environment of tech adoption, brand innovation, and consumer trust solidifies the UK’s position as Europe’s social commerce vanguard.

Germany Social Commerce Market Analysis

Germany was the second-largest player in the Europe social commerce landscape and captured a 19.4% share in 2024. The growth of the German market is propelled by disciplined digital infrastructure, high purchasing power, and a growing appetite for convenience-driven retail. Despite historically cautious attitudes toward data sharing, German consumers are increasingly embracing platform-based shopping, particularly in categories like home goods and beauty, ty where product authenticity and reviews carry significant weight. The country’s strong SME sector has also adapted swiftly. Trust is further reinforced by stringent consumer rights under the German Civil Code, which mandates clear return policies and transparent pricing even within social platforms. Notably, brands have pioneered hybrid models combining physical store inventory with Instagram checkout, reducing delivery times to under 24 hours in urban centers.

France Social Commerce Market Analysis

France is an attractive country in the European social commerce market because of its influential fashion and beauty culture and strong mobile internet adoption. The French consumer base exhibits high receptivity to visual storytelling. Paris remains a global trendsetter,ter, and this cultural capital translates into social commerce dominance as luxury and indie brands alike leverage Instagram Reels and TikTok to showcase seasonal collections directly to consumers. The government’s France Relance digital initiative has further accelerated adoption by subsidizing social selling tools for small fashion and cosmetics businesses. Additionally, French consumers place exceptional value on peer validation. Platforms have integrated live shopping into their social strategies, yielding conversion rates higher than standard display ads. These dynamics position France not only as a volume leader but as a stylistic trendsetter shaping aesthetic norms across the continent.

Italy Social Commerce Market Analysis

Italy is moderately growing in the Europe social commerce market due to a digitally engaged youth population and a heritage of design-centric consumerism. Italian shoppers, particularly in urban centers like Milan and Rome, demonstrate a strong preference for discovering apparel accessories and artisanal home goods through Instagram and Pinterest, where visual appeal outweighs textual descriptions. The country’s dense network of small fashion ateliers and family-run beauty brands has embraced social selling as a low-cost route to global audiences, bypassing traditional wholesale structures. Cultural pride in craftsmanship also enhances trust. The integration of WhatsApp Business for order confirmation and after-sales service further differentiates Italy’s approach, creating a hybrid social messaging commerce model rarely seen elsewhere in Europe.

Spain Social Commerce Market Analysis

Spain is predicted to grow in the European social commerce market from 2025 to 2033, owing to mobile-first consumer behavior and a vibrant creator economy. Spanish users spend notable hours and minutes daily on mobile apps, with social platforms accounting for a share of that time. This engagement translates directly into commerce with categories like summer apparel, footwear, and beauty, seeing peak conversions during live shopping events hosted by local influencers. Platforms like TikTok have localized aggressively in Spain, launching Spanish-language shopping dashboards and partnering with regional banks to simplify payment integration. This combination of cultural receptivity, policy support, and mobile readiness positions Spain as a dynamic and rapidly expanding node in Europe’s social commerce network.

COMPETITION OVERVIEW

Competition in the Europe social commerce market is intensifying as global tech giants, regional platforms, and agile startups vie for consumer attention and merchant loyalty. The landscape is characterized by rapid innovation in interactive features such as live shopping, augmented reality try-ons ons and AI-powered personalization, all tailored to Europe’s diverse linguistic and regulatory environments. Unlike more consolidated markets, Europe’s fragmentation demands localized strategies, forcing players to balance scale with customization. Established social networks leverage their user bases and advertising ecosystems while newer entrants differentiate through niche communities, circular economy models audio-based commerce. Regulatory scrutiny, particularly around data usage and platform accountability, adds complexity requiring continuous compliance investment. Despite these challenges, the market remains highly dynamic with frequent feature rollouts, strategic alliances cross-border expansion initiatives. This competitive tension accelerates consumer adoption and pushes the boundaries of how social interaction translates into commercial transactions across the region.

KEY MARKET PLAYERS

A few major players of the Europe social commerce market include

- Meta Platforms, Inc

- ByteDance Ltd

- Pinterest, Inc

- Alibaba Group Holding Limited

- Tencent Holdings Ltd

- Pinduoduo Inc

- Snap, Inc

- Google LLC

- Shopify Inc

- Amazon.com Inc

Top Strategies Used by the Key Market Participants

Key players in the Europe social commerce market employ several strategic approaches to strengthen their foothold. They prioritize localized platform experiences by adapting language, payment methmethodand regulatory compliance to each European country. Strategic partnerships with regional logistics firms, payment gateways, and digital marketing agencies enhance operational efficiency. Investment in augmented reality and live streaming technologies improves product visualization and engagement. Companies also focus on empowering small and medium enterprises through simplified onboarding, educational resources, and creator monetization tools. Additionally, continuous refinement of AI-driven recommendation engines ensures personalized product discovery while adhering to Europe’s strict data privacy standards. These strategies collectively foster trust, usability, and scalability in a fragmented high-potential market.

Leading Players in the Europe Social Commerce Market

Meta Platforms Inc

Meta Platforms plays a pivotal role in shaping the Europe social commerce ecosystem through its integrated shopping features on Instagram and Facebook. The company enables businesses to create digital storefronts, tag products in posts, and host live shopping events directly within its apps. In recent years, Meta has prioritized commerce infrastructure in Europe by launching localized checkout options compliant with GDPR and partnering with European payment processors to support regional financial regulations. It has also invested in AI-driven recommendation engines that surface relevant products to users based on behavior and preferences. Most recently, the company enhanced its Shops product to support multilingual cataloging, pricing specifically for EU merchants, ts reinforcing its commitment to a seamless, cross-border social commerce experience tailored to European consumer expectations and regulatory frameworks.

TikTok Ltd

TikTok Ltd has rapidly emerged as a major force in Europe’s social commerce landscape by leveraging its short-form video format to drive viral product discovery and impulse purchases. The platform introduced TikTok Shop in select European markets, enabling creators and brands to sell directly through livestreams and in-feed videos. To strengthen its position, TikTok has forged partnerships with European logistics providers to ensure faster delivery and established local seller onboarding hubs in countries like France and the United Kingdom. The company has also rolled out creator monetization programs that incentivize authentic product reviews and tutorials.

Amazon.com Inc

Amazon.com, Inc. contributes to the Europe social commerce market by bridging its vast e-commerce infrastructure with social engagement through integrations and pilot programs that connect influencer content to its product catalog. While not a traditional social platform, Amazon has enabled select European influencers to tag items in Instagram and YouTube content that link directly to Amazon product pages through its Amazon Influencer Program. The company has recently enhanced this initiative by introducing real-time performance dashboards for creators and expanding eligibility to micro influencers across Germany, France, and Italy. Additionally, Amazon launched a pilot in the United Kingdom, testing shoppable livestreams featuring third-party sellers showcasing European-made goods. These actions reflect Amazon’s strategy to embed its marketplace into social discovery journeys without owning the social layer, thereby leveraging existing user behaviors while reinforcing its logistics and fulfillment dominance in the region.

MARKET SEGMENTATION

This research report on the Europe social commerce market has been segmented and sub-segmented based on business model, product type, and region.

By Business Model

- B2B

- B2C

- C2C

By Product Type

- Personal & Beauty Care

- Apparel

- Accessories

- Home Products

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the growth of social commerce in Europe?

Key drivers include rising social media adoption, influencer marketing, mobile-first shopping behavior, integrated checkout features, and the growth of short-form video platforms like TikTok.

2. Which social media platforms dominate social commerce in Europe?

Instagram, Facebook, TikTok, Pinterest, and Snapchat are the leading platforms offering strong commerce and advertising capabilities.

3. Who are the key market players in the Europe Social Commerce Market?

Meta Platforms, Inc., ByteDance Ltd., Pinterest, Inc., Alibaba Group Holding Limited, Tencent Holdings Ltd., Pinduoduo Inc., Snap, Inc., Google LLC, Shopify Inc., Amazon.com, Inc.

4. What are the main opportunities in this market?

Personalized shopping experiences, live-commerce adoption, AI-driven product recommendations, international brand expansion, and user-generated content (UGC) marketing.

5. What challenges does social commerce face in Europe?

Data privacy regulations (GDPR), consumer trust issues, payment fragmentation, and cultural differences in shopping behavior across regions.

6. How important is influencer marketing in driving sales?

Very important micro and macro influencers significantly impact purchase decisions, helping brands increase trust and engagement.

7. Which countries lead the Europe Social Commerce Market?

Germany, the U.K., France, and Italy are the leading markets due to high digital adoption and strong e-commerce ecosystems.

8. How does social commerce impact small businesses?

Social commerce allows SMEs to reach wider audiences, reduce marketing costs, use integrated storefronts, and convert followers into buyers.

9. What technologies are enhancing social commerce growth?

AI/ML for recommendations, AR try-ons, chatbots, seamless payment integrations, and advanced analytics tools.

10. What is the future outlook for the Europe Social Commerce Market?

The market is expected to grow steadily, driven by mobile usage, improved shopping tools, live commerce, and expanded social platform features to support direct sales.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com