Europe Solvents Market Size, Share, Trends & Growth Forecast Report – Segmented By Product Type (Alcohols, Ketones, Esters, and Others), Application, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Solvents Market Size

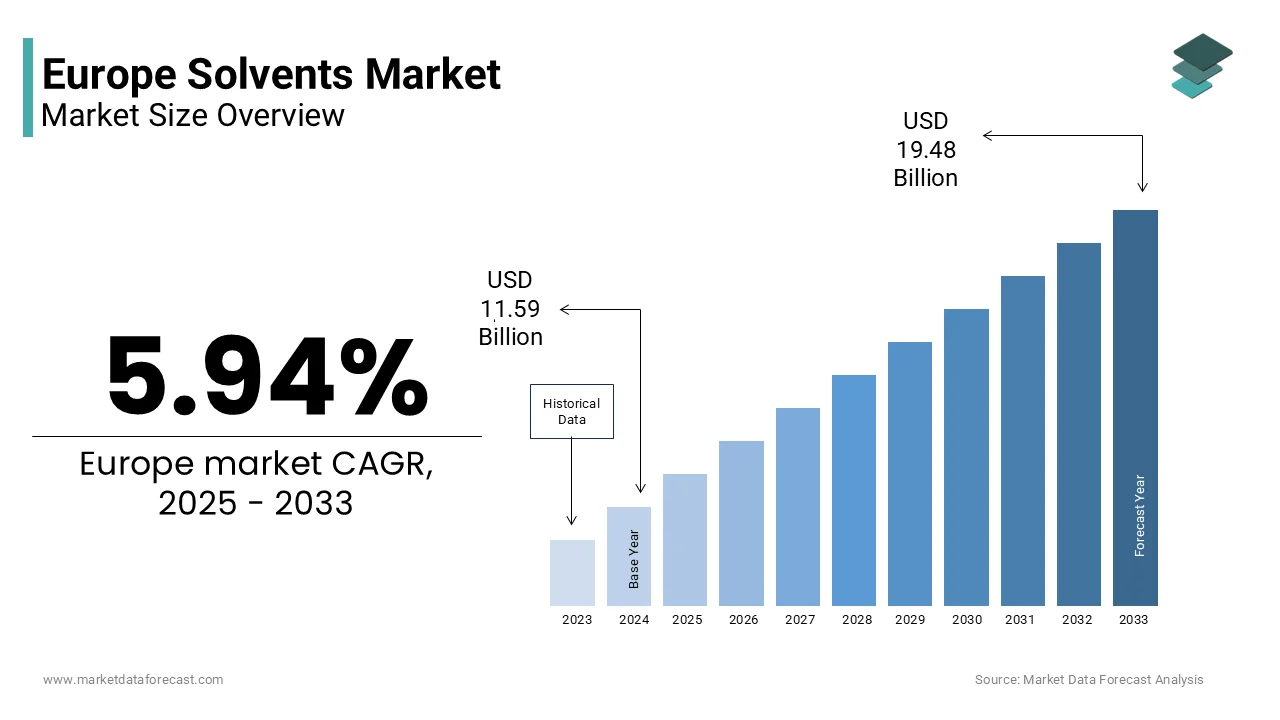

The Europe solvents market size was valued at USD 11.59 billion in 2024 and is projected to reach USD 19.48 billion by 2033 from USD 12.28 billion in 2025, growing at a CAGR of 5.94%.

Solvents are volatile organic compounds used to dissolve or suspend other substances without chemical change, serving as essential process enablers across coatings adhesives pharmaceuticals printing and cleaning industries. In Europe, the solvents market operates under one of the world’s most stringent regulatory frameworks governing chemical safety environmental emissions and occupational exposure. The European Environment Agency reports that solvent related emissions contributed to 18% of total volatile organic compound releases in the EU that year primarily from surface coating and printing activities. Meanwhile, the European Commission’s REACH regulation has restricted or phased out over 35 high concern solvents including trichloroethylene and certain glycol ethers due to reproductive toxicity or persistence.

MARKET DRIVERS

Stringent VOC Emission Regulations Driving Shift to Low VOC Formulations

The regulatory compulsion to reduce volatile organic compound emissions under the EU Industrial Emissions Directive and National Emission Ceilings Directive is majorly propelling the growth of the Europe solvents market. These rules mandate that all surface coating printing and adhesive operations implement best available techniques to minimize solvent release, effectively phasing out high VOC solvents in favor of water based or low VOC alternatives. According to the European Environment Agency, member states reported a 41% reduction in industrial VOC emissions between 2005 and 2023 largely attributable to solvent substitution. In Germany, the Technical Instructions on Air Quality Control require coating lines to achieve VOC abatement efficiencies of at least 90% or use formulations with less than 30 grams of VOC per liter, as per the sources. This has accelerated demand for exempt solvents like acetone and tertiary alcohols which are not classified as VOCs under EU law. Similarly, the EU Ecolabel for paints and varnishes caps VOC content at 5 to 30 grams per liter depending on product type pushing formulators toward bio based esters and glycol ether derivatives.

Growth in Pharmaceutical and Biotechnology Manufacturing

The expanding pharmaceutical and biotechnology sector for high purity specialty solvents used in synthesis extraction and cleaning processes is another factor prompting the growth of the Europe solvents market. Each kilogram of active pharmaceutical ingredient typically requires 50 to 100 liters of solvents during manufacturing, as noted by the European Medicines Agency. Solvents like ethanol isopropanol dichloromethane and tetrahydrofuran must meet pharmacopeial standards, such as Ph Eur or USP for residual impurities and water content. The rise of biologics and mRNA vaccines further increases demand for aprotic solvents like dimethyl sulfoxide in cryopreservation and purification. Ireland and Belgium have emerged as major pharmaceutical hubs with combined exports exceeding 120 billion euros in 2023 as per national customs data. These facilities operate under strict Good Manufacturing Practice guidelines requiring solvent traceability and batch certification.

MARKET RESTRAINTS

Restrictive REACH and CLP Regulations Limiting Solvent Availability

The European Union’s Registration Evaluation Authorisation and Restriction of Chemicals framework, which continuously evaluates and restricts substances of very high concern that is inhibiting the growth of the Europe solvents market. Under REACH, over 220 solvents have been placed on the Candidate List for authorization including N methyl 2 pyrrolidone certain phthalates and 1 2 dichloroethane, as confirmed by the European Chemicals Agency. For example, the use of NMP in paint stripping was banned in 2020 except for aerospace maintenance. This regulatory attrition forces formulators to reformulate products at significant R&D cost and risk performance trade offs. According to the European Coatings Federation, paint manufacturers reported reformulation delays due to solvent substitution challenges in 2023. Additionally, the Classification Labelling and Packaging regulation mandates hazard communication that discourages downstream use even when legal. This regulatory churn creates uncertainty suppresses investment in solvent dependent processes and increases compliance overhead particularly for small and medium enterprises lacking regulatory expertise.

High Costs and Limited Availability of Bio based and Green Solvents

The barriers in scaling bio-based solvents due to cost and supply constraints is also impeding the growth of the Europe solvents market. Bio-based ethyl lactate or 2 methyltetrahydrofuran can cost two to four times more than their petrochemical counterparts as per data from the European Bioeconomy Network. In 2023, bio based solvent production in the EU totaled only 180000 metric tons representing less than 5% of total solvent consumption. Feedstock competition with food and land use regulations under the Renewable Energy Directive further constrain expansion. For instance, glycerol derived solvents depend on biodiesel production which declined by 12% in the EU in 2023 due to policy shifts as reported by the European Biodiesel Board. Moreover, many green solvents lack the performance profile of traditional solvents in terms of evaporation rate solvency power or stability leading to formulation inefficiencies.

MARKET OPPORTUNITIES

Expansion of Circular Solvent Recovery and Reuse Systems

The adoption of on-site and centralized solvent recovery systems that enable closed loop reuse while complying with waste and chemical regulations is greatly influencing the growth of the Europe solvents market. Under the EU, Waste Framework Directive spent solvents can be reclassified as products rather than waste if purified to original specification. According to the European Solvents Industry Group, industrial solvents in Europe are already recovered through distillation with recovery rates in sectors like pharmaceuticals and metal cleaning. Companies like Solvesso and Veolia operate mobile distillation units that service small manufacturers unable to invest in fixed infrastructure. These systems reduce raw material purchases lower hazardous waste disposal costs and cut carbon footprint key metrics under corporate sustainability reporting mandates like CSRD.

Rise of Electronics and Semiconductor Manufacturing in Europe

The European Chips Act and strategic push for semiconductor sovereignty are creating new high purity solvent demand in wafer fabrication and chip packaging, which is eventually to bolster the growth of Europe solvents market. According to the European Commission, the EU aims to double its global semiconductor production share to 20% by 2030 requiring over 40 billion euros in public and private investment. Solvents like photoresist strippers N methyl 2 pyrrolidone replacements and anhydrous isopropanol must meet SEMI international standards with impurity levels below 10 parts per billion. Germany France and Italy are establishing new fabs with support from Intel Infineon and STMicroelectronics driving localized solvent supply chains. The European Chemicals Agency has introduced fast track compliance pathways for electronics grade solvents to avoid supply disruptions.

MARKET CHALLENGES

Inconsistent National Implementation of EU Chemical Legislation

The divergent transposition and enforcement of EU chemical regulations across member states creating legal uncertainty and operational friction is one of the challenging factors for the growth of Europe solvents market. Although REACH and CLP are directly applicable national authorities retain discretion in inspection frequency classification interpretation and enforcement penalties. According to the European Court of Auditors in 2023, only 14 of 27 member states fully complied with REACH evaluation timelines while others exhibited significant delays. Similarly, Germany’s stricter workplace exposure limits for toluene compared to EU averages force formulators to maintain multiple product variants. These discrepancies increase compliance costs for multinational companies which must adapt formulations regionally. The European Chemicals Agency acknowledges this fragmentation but lacks enforcement authority over national bodies.

Dependence on Imported Feedstock and Energy Volatility

The reliance on imported crude oil natural gas and bio feedstocks for raw material production is additionally to degrade the growth of the Europe solvents market in coming years. BASF reduced its Ludwigshafen solvent output by 18% in 2022 due to unviable energy costs as confirmed by its annual report. Simultaneously, bio based solvent producers depend on imported soy or corn oil with 60% sourced from South America by exposing them to supply chain disruptions and deforestation regulations. The EU’s Carbon Border Adjustment Mechanism adds further cost uncertainty for imported intermediates.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.94% |

| Segments Covered | By Product Type, Application, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | BASF, Dow Chemical, Ashland, ExxonMobil, Huntsman, Arkema, LyondellBasell, BP, INEOS, Honeywell International, Solvay, Eastman Chemical, Chevron Phillips Chemical, Celanese, Top Solvent, BioAmber, Flotek Industries, Invista, and Monument Chemical |

SEGMENTAL ANALYSIS

By Product Type Insights

The alcohols segment held 38.6% of the Europe solvents market share in 2024. Ethanol and isopropanol are exempt from volatile organic compound classification under the EU Solvents Emissions Directive due to their high photochemical reactivity threshold. According to the European Environment Agency this regulatory status makes them preferred substitutes in water reduced paints industrial cleaners and disinfectants. Similarly, in industrial cleaning isopropanol dominates precision degreasing in electronics and aerospace due to its rapid drying and residue free properties.

The esters segment is anticipated to grow at a fastest CAGR of 6.8% throughout the forecast period. Acetates and lactates derived from fermented sugars or vegetable oils are gaining traction as green solvents in architectural and industrial coatings. Ethyl lactate for instance is fully biodegradable has low aquatic toxicity and is REACH registered without classification. The European Bioeconomy Network reports that bio-based ester production in the EU grew by 22% in 2023 reaching 48,000 metric tons primarily for use in eco labeled paints. Companies like AkzoNobel and PPG now formulate premium wood finishes using butyl acetate from renewable feedstocks to meet customer sustainability criteria. Esters like propylene glycol methyl ether acetate offer balanced evaporation rates high solvency power and low residue making them ideal for photoresist stripping and wafer cleaning in semiconductor manufacturing. The German Technical Rules for Hazardous Substances classify many esters as non-sensitizing enabling easier workplace handling.

By Application Insights

The paints & coatings segment was accounted in holding 42.3% of the Europe solvents market share in 2024. The EU Paints Directive and Industrial Emissions Directive compel formulators to reduce volatile organic compound content through solvent substitution or water dilution. This transition has not eliminated solvents but shifted demand toward exempt alcohols and oxygenated solvents like esters that stabilize water borne resins. In industrial coatings high solids formulations still require significant solvent loads up to 30% by volume to ensure application properties. Germany’s Technical Instructions on Air Quality Control mandate VOC abatement or low solvent use driving adoption of acetates and glycol ethers.

The industrial cleaning segment is likely to grow at a fastest CAGR of 7.2% throughout the forecast period. The European Chips Act and medical device regulation are driving demand for ultra pure solvents in precision cleaning. Each semiconductor fab uses over 2 million liters of isopropanol and esters annually for wafer cleaning, as per the reports. Similarly medical device manufacturers require residue free degreasers for implantable components with strict ISO 13485 compliance. The European Medical Devices Coordination Group reports that over 500000 cleaning validation batches were conducted in 2023 alone. Solvents like n propyl bromide replacements and bio based d limonene are gaining ground due to lower occupational hazards.

REGIONAL ANALYSIS

Germany Market Analysis

Germany was the top performer in the Europe solvents market by occupying 24.7% of share in 2024 due to its dominant chemical industry advanced manufacturing base and strict environmental governance. The country hosts global solvent producers like BASF Evonik and Lanxess operating integrated facilities in Ludwigshafen and Marl that supply high purity alcohols ketones and esters across Europe. Germany’s Technical Instructions on Air Quality Control impose some of the EU’s most stringent VOC abatement requirements pushing innovation in low emission formulations. The federal government’s High-Tech Strategy 2030 supports green solvent R&D with 120 million euros allocated to bio-based alternatives in 2023.

France Market Analysis

France commands 16.8% of the Europe solvents market driven by its strong pharmaceutical cosmetics and aerospace industries. The country is home to Sanofi L’Oréal and Safran which collectively consumed over 320000 metric tons of specialty solvents in 2023 as per France’s Ministry of Ecological Transition. The cosmetics sector alone uses ethanol and esters in 90% of fragrances and skincare products with France accounting for 28% of global perfume exports according to Business France. The French Environmental Code mandates solvent recovery in all industrial facilities generating more than 100 kilograms of waste annually accelerating adoption of on site distillation. The national REACH helpdesk provides extensive support for small formulators navigating chemical compliance reducing substitution barriers. Additionally, France’s investment in semiconductor sovereignty through the Chips Act includes solvent supply chain security assessments ensuring stable demand from emerging microelectronics clusters in Grenoble and Crolles.

Italy Market Analysis

Italy solvents market growth is likely to grow with its world leading furniture automotive refinish and fashion industries. Similarly, Italy’s 15000 plus automotive body shops rely on ketones and esters for color matching and fast drying in repair coatings. The Italian Ministry of Environment enforces EU VOC directives through regional agencies with Lombardy and Emilia Romagna requiring real time emission monitoring in coating facilities. Italy, also hosts significant solvent import and blending operations in the Port of Genoa handling over 400000 metric tons annually as per port authority data. This blend of industrial heritage and regulatory adaptation sustains Italy’s position as a major and resilient solvent consumer.

United Kingdom Market Analysis

The United Kingdom solvents market growth is likely to grow with the strong demand despite Brexit through its pharmaceutical aerospace and printing sectors. According to the UK Chemical Industries Association over 300000 metric tons of solvents were used in 2023 primarily in drug synthesis aircraft maintenance and packaging inks. The Medicines and Healthcare products Regulatory Agency requires solvent traceability in all pharmaceutical batches ensuring consistent high purity alcohol and ester consumption. The UK’s retained REACH regime mirrors EU restrictions but offers faster authorization for critical solvents in defense and aerospace applications. Companies like AstraZeneca and Rolls Royce maintain strategic solvent inventories to mitigate supply chain risks. Additionally, the British Coatings Federation reports that heritage building restoration governed by Historic England still permits solvent based paints for authenticity preserving demand in conservation.

Spain Market Analysis

Spain solvents market growth is likely to grow with its automotive manufacturing shipbuilding and construction sectors. The country produces over 2.4 million vehicles annually making it Europe’s second largest car producer. Each assembly line uses solvent-based adhesives and coatings requiring 45000 metric tons of ketones and aromatics yearly. Spain’s shipyards in Cádiz and Vigo consume large volumes of industrial cleaners for hull degreasing with strict MARPOL compliance driving adoption of biodegradable esters. The Spanish Ministry for Ecological Transition enforces EU VOC limits through regional industrial parks where shared solvent recovery units reduce waste costs. Additionally, Spain’s construction boom fueled by EU recovery funds generated 18 billion euros in renovation projects in 2023 as per the Ministry of Transport increasing demand for architectural coatings.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the notable key players in the Europe solvents market are

- BASF

- Dow Chemical

- Ashland

- ExxonMobil

- Huntsman

- Arkema

- LyondellBasell

- BP

- INEOS

- Honeywell International

- Solvay

- Eastma Chemical

- Chevron Phillips Chemical

- Celanese

- Top Solvent

- BioAmber

- Flotek Industries

- Invista

- Monument Chemical

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the Europe solvents market focus on developing bio based and renewable solvent alternatives to meet tightening VOC and sustainability regulations. They invest in molecular recycling and mass balance certification to offer circular solvent solutions with verified environmental credentials. Companies enhance digital tools for regulatory compliance formulation support and solvent selection aligned with REACH and CLP requirements. Strategic integration of solvent recovery and distillation services enables closed loop systems for industrial customers reducing waste and cost. Partnerships with end user industries such as automotive electronics and pharmaceuticals ensure co development of application specific solvent grades that balance performance safety and environmental criteria.

COMPETITION OVERVIEW

The Europe solvents market features a competitive landscape dominated by large integrated chemical producers alongside specialized regional players and niche bio based innovators. Competition is defined less by price and more by regulatory compliance technical support and sustainability credentials. Global giants like BASF and INEOS leverage scale and vertical integration to offer consistent quality and secure supply while smaller firms differentiate through green chemistry expertise or localized recovery services. The stringent and evolving nature of EU chemical legislation creates high barriers to entry favoring incumbents with established regulatory dossiers and compliance infrastructure. At the same time customer demand for transparency under the Corporate Sustainability Reporting Directive pushes suppliers to provide full lifecycle data and carbon footprint metrics. Innovation is increasingly collaborative with formulators solvents producers and end users co developing solutions that meet both performance and environmental targets. This ecosystem fosters dynamic yet consolidated competition where strategic positioning and sustainability leadership outweigh volume alone.

TOP PLAYERS IN THE MARKET

- BASF is a German multinational and one of the world’s largest chemical producers with a comprehensive portfolio of oxygenated solvents including alcohols ketones and esters tailored for European regulatory standards. The company supplies high purity solvents to automotive pharmaceutical and electronics industries across the continent from its integrated Verbund site in Ludwigshafen. BASF plays a pivotal role globally by setting benchmarks for sustainable solvent production through its ChemCycling and biomass balance approaches. The company also enhanced its digital solvent selection tool to help formulators comply with REACH and VOC directives accelerating the adoption of compliant alternatives in complex applications.

- INEOS Solvents is a leading European producer of industrial solvents with manufacturing facilities in the United Kingdom France and Germany specializing in alcohols acetates and glycol ethers. The company serves key sectors including coatings cleaning and pharmaceuticals with a strong focus on solvent recovery and circularity. INEOS contributes globally by operating one of the largest solvent distillation networks enabling customers to reuse purified solvents across multiple cycles. The company also integrated real time emissions monitoring at all its European plants to align with Industrial Emissions Directive requirements reinforcing its position as a responsible and reliable supplier in a highly regulated market.

- Eastman Chemical Company is a US based specialty materials firm with a significant footprint in Europe through its high performance solvents business. The company is renowned for its innovative ester and ketone technologies including bio based and non VOC exempt solvents used in advanced coatings electronics and personal care. Eastman’s molecular recycling technologies enable the production of solvents from plastic waste supporting circular economy goals. The company also strengthened its regulatory compliance support services across Europe to assist customers navigating evolving REACH and CLP classifications ensuring uninterrupted supply of critical solvent solutions.

MARKET SEGMENTATION

This research report on the Europe solvents market has been segmented and sub-segmented based on categories.

By Product Type

- Alcohols

- Ketones

- Esters

- Others

By Application

- Paints & Coatings

- Printing Inks

- Industrial Cleaning

- Adhesives

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe solvents market?

The Europe solvents market covers chemical substances used to dissolve, disperse, or extract materials across industries such as paints, coatings, pharmaceuticals, adhesives, and chemicals.

2. What factors are driving the solvents market in Europe?

Key drivers include growth in construction and automotive sectors, expansion in pharmaceuticals, and rising demand for eco-friendly and bio-based solvents.

3. Which countries dominate the Europe solvents market?

Germany, France, the UK, Italy, and the Netherlands lead due to strong industrial bases and chemical manufacturing activities.

4. What types of solvents are widely used in Europe?

Common types include alcohols, ketones, esters, hydrocarbons, glycols, and emerging bio-based solvents.

5. Which industry uses the largest amount of solvents in Europe?

The paints & coatings industry is the largest consumer, driven by demand from construction, automotive production, and industrial equipment.

6. What are bio-based solvents, and why are they becoming popular?

Bio-based solvents are derived from renewable sources and are gaining importance due to EU regulations promoting low-VOC and sustainable chemicals.

7. What challenges does the Europe solvents market face?

Major challenges include strict environmental regulations, volatile raw material prices, and the shift toward environmentally safer alternatives.

8. How are solvents used in the pharmaceutical sector?

Pharmaceutical companies use solvents for drug formulation, extraction, purification, and various synthesis processes.

9. Who are the key players in the Europe solvents market?

Key players include BASF, Dow Chemical, Ashland, ExxonMobil, Huntsman, Arkema, LyondellBasell, BP, INEOS, Honeywell International, Solvay, Eastman Chemical, Chevron Phillips Chemical, Celanese, Top Solvent, BioAmber, Flotek Industries, Invista, and Monument Chemical.

10. What is the long-term outlook for the Europe solvents market?

The market is expected to grow steadily as industries adopt greener technologies, expand manufacturing activities, and invest in sustainable solvent alternatives.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com