Europe Thermal Energy Storage Market Size, Share, Trends & Growth Forecast Report By Technology, Material, End User, and By Country (Germany, Denmark, Sweden, Italy, Netherlands & Rest of Europe) – Industry Analysis and Forecast, 2025 to 2033

Europe Thermal Energy Storage Market Summary

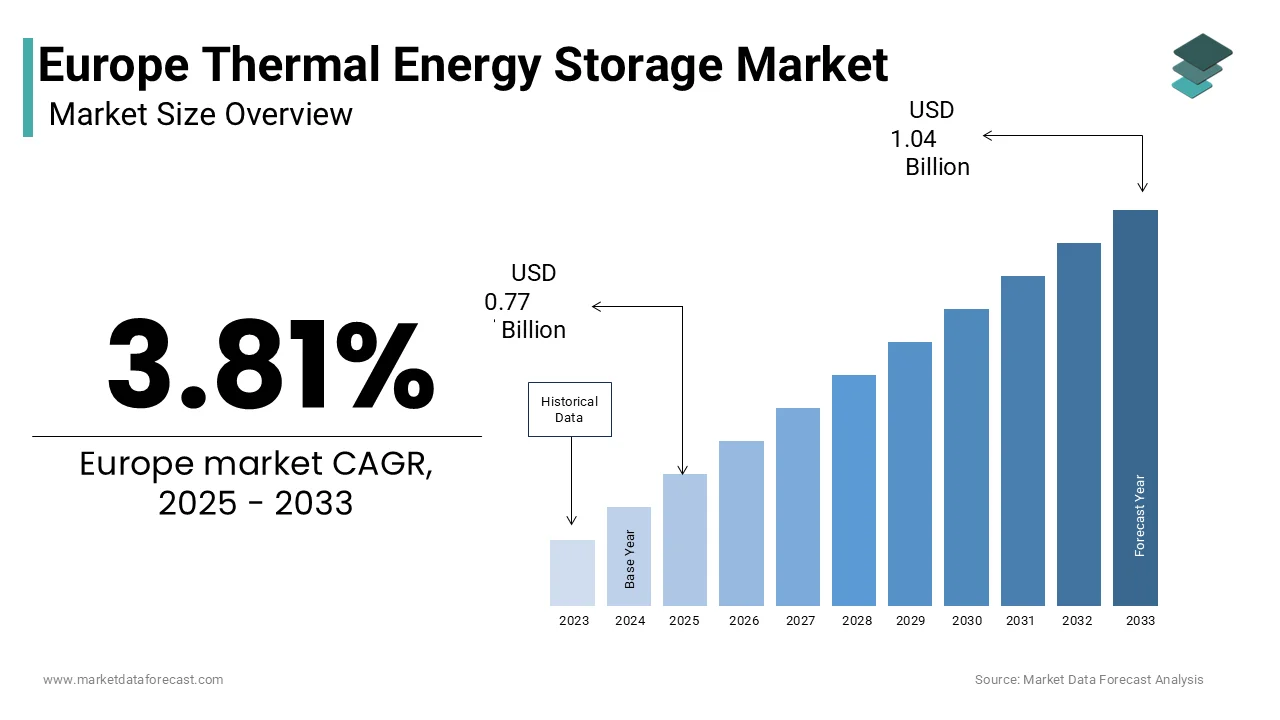

Europe thermal energy storage market was valued at USD 0.74 billion in 2024, is estimated to reach USD 0.77 billion in 2025, and is projected to grow to USD 1.04 billion by 2033, registering a CAGR of 3.81% from 2025 to 2033, driven by district heating modernization, industrial process heat decarbonization, and renewable energy integration.

Key Market Insights

- 2024 value: USD 0.74 billion

- 2025 (est): USD 0.77 billion

- 2033 (forecast): USD 1.04 billion

- CAGR (2025–2033): 3.81%

Quick Growth Drivers

- Large-scale district heating modernization across Northern and Central Europe

- Rising need for seasonal heat balancing in renewable-heavy energy systems

- Industrial decarbonization mandates targeting low- and medium-temperature process heat

- Expansion of solar thermal, electric boilers, and power-to-heat systems

- EU funding support via Energy Efficiency Directive, Innovation Fund, and Horizon Europe

Principal Restraints

- High upfront capital costs for utility-scale and industrial installations

- Long payback periods exceeding 10 years in many markets

- Limited access to capacity markets and flexibility revenues

- Fragmented permitting and regulatory treatment across EU member states

High-Value Opportunities

- Integration of thermal storage within renewable energy communities

- Waste heat recovery from data centers, metro systems, and industrial clusters

- Growth of seasonal storage for solar thermal surplus

- Coupling thermal storage with electricity grid congestion relief strategies

- Expansion into Southern and Eastern Europe through public funding programs

Key Market Challenges

- Material supply constraints for molten salts, PCMs, and corrosion-resistant alloys

- Lack of standardized performance and efficiency certification frameworks

- Inconsistent lifecycle carbon accounting methodologies

- Limited investor confidence due to non-uniform technical validation

Fastest-Growing Segments

- Thermochemical storage: 18.4% CAGR — ultra-high energy density, seasonal use

- Phase change materials (PCMs): 16.7% CAGR — compact, precision temperature control

- Residential thermal storage: 15.2% CAGR — heat pumps, rooftop solar pairing

- Industrial high-temperature storage: driven by ETS carbon pricing pressure

Regional Leadership & Dynamics

- Germany (22.3%) — strong regulation, solar thermal leadership, sector coupling pilots

- Denmark — world leader in seasonal pit thermal storage and district heating

- Sweden — fastest growth, strong industrial electrification and grid resilience focus

- Italy — renovation incentives, solar thermal growth, community storage initiatives

- Netherlands — ATES dominance, urban waste heat integration, zero-gas mandates

What Wins Commercially (Competitive Edge)

- Proven integration with district heating and industrial systems

- Low-maintenance, long-lifetime storage media

- Compatibility with power-to-heat and renewable surplus capture

- Ability to support seasonal and long-duration storage

- Alignment with EU decarbonization and efficiency regulations

Top Strategic Ask for Executives

- Prioritize district heating and industrial partnerships

- Invest in advanced materials to improve energy density and lifespan

- Engage early with regulators to secure thermal storage recognition as flexibility assets

- Leverage EU funding mechanisms for scale-up and replication

- Standardize performance reporting to improve bankability and adoption

Leading Players

Some of the companies that are playing a dominating role in the Europe thermal energy storage market include:

- Siemens Energy AG

- Viessmann Group

- ENGIE SA

- Bosch Thermotechnology GmbH

- EnergyNest AS

- Sunamp Ltd.

- Abengoa Solar

- Absolicon Solar Collector AB

- Hotbridge GmbH

- Calmac Manufacturing Corporation

Europe Thermal Energy Storage Market Size

The europe thermal energy storage market was valued at USD 0.74 billion in 2024, is estimated to reach USD 0.77 billion in 2025, and is projected to grow to USD 1.04 billion by 2033, registering a CAGR of 3.81% from 2025 to 2033.

Thermal energy storage is a strategic enabler of decarbonization and grid flexibility, allowing surplus heat or cold to be stored and dispatched when needed across residential, industrial, and district heating applications. Europe’s seasonal heating demand accounts for over 50% of final energy consumption across the region, according to Eurostat, underscoring the importance of efficient thermal load management. The continent’s aging district heating networks, which serve more than 90 million people with an infrastructure base for integrating large-scale thermal storage solutions, as per recent studies. Additionally, the European Environment Agency notes that buildings contribute to the EU’s total energy-related carbon emissions by creating pressure to modernize thermal systems through storage-enabled efficiency. Thermal energy storage emerges not as a supplementary technology but as a foundational pillar in the transition toward resilient and renewable thermal systems across Europe.

MARKET DRIVERS

Accelerated Deployment of District Heating Modernization Programs

Europe’s push to decarbonize urban thermal networks has significant investment in retrofitting legacy district heating infrastructure with thermal energy storage capabilities, which is attributed to propelling the growth of Europe's thermal energy storage market. District heating already supplies approximately 12% of the EU’s total heat demand, with countries like Denmark and Sweden achieving coverage rates exceeding 60% of households. These systems increasingly incorporatelarge-scalee hot water tanks and pit thermal storage to absorb excess renewable generation during off-peak periods. In Denmark alone, over 300 thermal storage units larger than 1000 cubic meters were operational by 2023, as per Danish Energy Agency data, enabling seasonal shifting of heat from summer solar thermal surplus to winter demand peaks. The EU’s Energy Efficiency Directive mandates that member states assess the potential for expanding district heating in urban areas every five years, compelling utilities to incorporate storage to enhance system responsiveness. Furthermore, the European Investment Bank committed over 5 billion euros between 2020 and 2024 to modernize district energy networks, with thermal storage often embedded as a core component. This policy-driven infrastructure renewal not only enhances grid stability but also unlocks higher penetration of solar thermal and waste heat sources, directly fueling demand for scalable thermal storage technologies across Central and Northern Europe.

Industrial Sector’s Pursuit of Process Heat Decarbonization

Europe’s industrial sector is responsible for roughly 25% of the region’s final energy consumption according to the International Energy Agency, which is undergoing a fundamental shift toward low-carbon process heat with a transition heavily reliant on thermal energy storage. The industrial sector’s pursuit of process heat decarbonization is additionally fuelling the growth of Europe's thermal energy storage market. Industries such as cement, glass, and food processing require consistent high temperatures, traditionally supplied by fossil fuels. The European Green Deal’s Industrial Emissions Directive now compels facilities emitting more than 20 megawatts of thermal energy to evaluate renewable alternatives, including thermal storage integrated with concentrated solar power or electric boilers powered by wind and solar. Germany’s Federal Ministry for Economic Affairs and Climate Action reported that over 60% of industrial heat demand falls within the 100 to 400 degree Celsius range, a segment increasingly targeted by novel storage materials like molten salts and thermochemical systems. In 2023, the EU’s Innovation Fund allocated 140 million euros to the H2Heat project in Belgium, which combines green hydrogen and thermal storage to supply carbon-free process heat to a chemical cluster. Similarly, Sweden’s SSAB steel plant, in collaboration with Vattenfall, is piloting a 20-megawatt electric boiler paired with a 5000 cubic meter hot water accumulator to store renewable electricity as heat. These initiatives demonstrate how regulatory pressure and access to clean electricity are converging to make thermal storage indispensable for industrial decarbonization across Europe.

MARKET RESTRAINTS

High Upfront Capital Expenditure for Large-Scale Installations

The thermal energy storage faces significant adoption barriers due to substantial initial investment requirements for large-scale systems integrated into district heating or industrial facilities. The high upfront capital expenditure for large-scale installations is majorly restricting the growth of Europe thermal energy storage market. A typical 10 megawatt-hour hot water tank installation can cost between 2 and 4 million euros, according to analyses by the European Bank for Reconstruction and Development, with additional expenses for civil works, insulation, and control systems inflating total project costs. These capital demands become especially prohibitive in Southern and Eastern European countrie,,s where access to low-cost financing remains constrained. Moreover, thermal storage projects often compete with more mature energy efficiency measures for limited public subsidies under the EU’s Modernisation Fund, which allocated just 12% of its 2021–2023 disbursements to thermal infrastructure, as per the European Commission’s implementation review. This financial asymmetry discouragrisk-averserse stakeholders from pursuing storage despite long term savings. Even with falling component costs, the payback period for utility-scale thermal storage often exceeds 10 years, deterring private investors seeking shorter horizons. Until innovative financing instruments like green bonds or storage-specific grants become more widespread, high upfront costs will continue to suppress deployment velocity, particularly in economically heterogeneous European markets.

Regulatory and Grid Access Ambiguities for Non-Electric Storage Assets

Thermal energy storage systems encounter systemic disadvantages due to the lack of explicit recognition in frameworks, which remain overwhelmingly tailored to electricity storage and generation, which is limiting the growth of Europe's thermal energy storage market. Unlike batteries, thermal storage assets are rarely eligible for capacity markets, ancillary service remuneration, or grid balancing contracts because they do not directly inject electricity into the grid. According to the Clean Energy for All Europeans package, only five EU member states as of 2024, Denmark, Germany, Sweden, Finland, and Austria, have established regulatory mechanisms that formally classify thermal storage as a dispatchable flexibility resource. The European Network of Transmission System Operators for Electricity acknowledged in its 20-Year Network Development Plan that thermal storage could defer up to 15% of projected grid reinforcement costs in heating dense regions, yet current tariff structures fail to monetize this deferral value. Furthermore, district heating operators face fragmented permitting processes. In France, obtaining environmental approval for underground thermal pits can take over 18 months, as per data from the study. This regulatory fragmentation and absence of standardized valuation methodologies for thermal flexibility stifle investor confidence and impede cross-border replication of successful business models.

MARKET OPPORTUNITIES

Integration of Thermal Storage in Renewable Energy Communities

The emergence of citizen-led renewable energy communities for distributed thermal energy storage, particularly in conjunction with solar thermal and heat pump systems, icertainly to create new opportunities for the growth of Europe's thermal energy storage market. Under the EU’s Renewable Energy Directive, member states must facilitate local energy sharing, and by mid 2024, over 3000 registered energy communities existed across the bloc, according to the European Federation of Renewable Energy Cooperatives. These communities, often comprising 50 to 500 households, increasingly deploy communal buffer tanks to store excess solar thermal energy generated in summer for use during shoulder seasons. In the Netherlands, the Stad van de Zon neighborhood in Heerhugowaard operates a 2000 cubic meter seasonal storage system linked to 1400 solar collectors, meeting 80% of annual heating demand as documented by the Dutch Ministry of Economic Affairs. Italy’s PNRR recovery plan allocates 180 million euros specifically for community-scale thermal storage under its “Thermal Communities” initiative by targeting 200 projects by 2026. The decentralized nature of these models reduces transmission losses and enhances social acceptance of renewables, while also qualifying for local subsidies that individual households might not access.

Expansion of Waste Heat Recovery from Data Centers and Urban Infrastructure

Europe’s growing digital economy is generating vast quantities of low-grade waste heat, much of which can be economically valorized through thermal energy storage integrated into urban heating networks. The expansion of waste heat recovery from data centers and urban infrastructure is expected to fuel the growth of Europe's thermal energy storage market. Data centers alone consumed approximately 156 terawatt hours of electricity in the EU in 2023, with over 90% of that energy ultimately dissipating as heat, according to some reports. In Helsinki, the Yandex data center supplies 8000 megawatt hours of recovered heat annually to the city’s district network via a 1500 cubic meter buffer tank, enough to warm 1000 households with the municipal energy company. Similarly, Paris’s 2023 heat recovery strategy mandates that all new data centers exceeding 1 megawatt of IT load must assess heat reuse feasibility, with thermal storage serving as the critical intermediary to match intermittent server operation with steady heating demand. The EU’s upcoming Energy Efficiency First principle implementation guidelines, expected in 2025, will require municipalities to map waste heat sources above 100 kilowatts, potentially uncovering over 3000 gigawatt hours of recoverable heat annually, according to assessments by the European Heat Pump Association.

MARKET CHALLENGES

Material and Supply Chain Constraints for Advanced Storage Media

The performance and scalability of next-generation thermal energy storage systems depend heavily on specialized materials, such as high-purity salts, phase change compounds, and corrosion-resistant alloys, many of which face supply chain vulnerabilities. The material and supply chain constraints for advanced storage media are one of the primary factors that challenge the growth of Europe's thermal energy storage market. Domestic production capacity for phase change materials based on bio-derived fatty acids remains limited to pilot scale, with only three commercial suppliers operating in the EU as of 2024, as per sources. This dependency not only exposes projects to geopolitical risks but also inflates costs; the price of technical-grade sodium nitrate rose by 42% between 2021 and 2023, as documented by the European Commission’s Raw Materials Information System. Furthermore, high-temperature systems relying on molten chloride salts demand nickel-based alloys resistant to oxidation and thermal stress, yet Europe’s specialty steel sector operates at near full capacity, with lead times exceeding 12 months for large forgings, as reported by Eurofer. These material bottlenecks delay project execution and increase capital risk for demonstration plants aiming to validate novel storage chemistries.

Lack of Standardized Performance Metrics and Verification Protocols

The absence of harmonized standards for measuring and certifying the efficiency, lifetime, and environmental impact of thermal energy storage systems impedes investor confidence and cross-market deployment. The lack of standardized performance metrics and verification protocols. Unlike photovoltaic panels or heat pumps, which benefit from established CE marking and Ecodesign requirements, thermal storage technologies operate in a regulatory gray zone where performance claims often rely on proprietary or non-comparable testing methods. A 2023 review by the Joint Research Centre of the European Commission found that over 60% of commercial thermal storage products lackedthird-partyy validation of round-trip efficiency, with declared values ranging from 70 to 95% for seemingly similar hot water tanks. This opacity complicates procurement decisions for public utilities and discourages integration into building energy performance certificates, which influence over 75% of renovation investments in the EU. Moreover, lifecycle assessment methodologies for thermal storage remain inconsistent, while Sweden applies ISO 14040-compliant protocols to evaluate carbon payback periods, countries like Poland and Romania have no mandatory disclosure rules. The European Committee for Standardization has initiated work on CEN/TS 17958 for thermal storage testing, but final adoption is not expected before 2026.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Technology, Material, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Calmac Manufacturing Corporation, Bridgelux, Inc., Enerstore (VITO NV), Sonnen GmbH, Viessmann Group, Vaillant Group, Bosch Thermotechnology GmbH, ENGIE SA, Siemens AG, GE Renewable Energy, Babcock & Wilcox Enterprises, Inc., Abengoa Solar, BrightSource Energy, Inc., Absolicon Solar Collector AB, Exergonix, Inc., EnergyNest AS, Ice Energy, Inc., Hotbridge GmbH, TES Vsetín a.s., Sunamp Ltd |

SEGMENTAL ANALYSIS

By Technology Insights

The sensible heat storage segment accounted in holding 68.4% of the European thermal energy storage market share in 2024, with its use of water and solid materials like concrete or rocks, which are inexpensive, non-toxic, and technologically mature. The widespread integration of hot water storage tanks in district heating networks across Northern and Central Europe underpins this leadership. Additionally, EU building codes under the Energy Performance of Buildings Directive require new residential and public buildings to include thermal storage capacitywhen connected to district heating, further entrenching sensible heat technology. Germany alone added more than 1200 new sensible storage installations in 2023, primarily in municipal heating networks, according to the German Energy Storage Association. The simplicity of operation, compatibility with existing infrastructure, and low maintenance needs make sensible heat the default choice for both short and medium duration thermal buffering in heheating-dominateduropean climates.

The thermochemical storage segment is projected to expand at a CAGR of 18.4% from 2025 to 2033, with its exceptional energy density up to 5 to 10 times higher than sensible or latent systems and its ability to store heat for months with negligible loss,y making it ideal for seasonal applications. The EU’s Horizon Europe program has allocated over 95 million euros since 2021 to advance thermochemical materials, such as salt hydrates and metal oxides, with flagship projects like STORE4HEAT validating pilot systems in Italy and the Netherlands. In Denmark, the Technical University of Denmark has demonstrated a sorption-based thermochemical unit achieving 92% round trip efficiency in laboratory trials, as reported in its 2023 annual energy technology review. Moreover, the European Green Deal’s Industrial Decarbonisation Strategy identifies thermochemical storage as critical for high temperature industrial processes above 300 degrees Celsius, a sector accounting for 22% of EU industrial emissions according to the European Environment Agency.

By Material Insights

The water segment was the largest by holding a significant share of the European thermal energy storage market in 2024, with its high specific heat capacity, abundance, safety, and seamless compatibility with existing hydronic heating systems across the continent. Over 85% of Europe’s district heating networks operate on water-based circuits, and nearly all residential buffer tanks utilize water as the storage medium, according to Euroheat & Power. Similarly, Finland’s national energy strategy mandates that all new district heating projects include thermal storage with water as the primary medium, resulting in over 400 new installations since 2022, as per the Finnish Energy Authority. Water’s non-flammable nature and zero environmental toxicity further align with the EU’s Chemicals Strategy for Sustainability by making it the preferred choice for densely populated urban areas.

The phase change materials segment is likely to witness the fastest CAGR of 16.7% throughout the forecast period, with the PCM’s ability to store and release large amounts of latent heat at near constant temperatures by enabling precise thermal management in sensitive applications like data centers, pharmaceutical cold chains, and residential retrofitting. The European Commission’s Circular Economy Action Plan has specifically endorsed bio-based PCMs derived from fatty acids and sugar alcohols, with pilot production scaling up in Belgium and the Netherlands. Additionally, the EU-funded INNOVATE project demonstrated that PCM-enhanced concrete in commercial buildings cut peak cooling loads by 35%, as per some reports. The material safety and regulatory clarity are accelerating adoption across building and transport sectors, where compact, high-density thermal buffering is essential.

By End User Insights

The industrial sector segment accounted in holding 54.3% of Europe’s thermal energy storage market share in 2024, with the sector’s immense and consistent need for process heat, which accounts for nearly 70% of all industrial energy use in the EU. Industries such as cement, steel, chemicals, and food processing operate at temperatures ranging from 100 to over 1000 degrees Celsius by creating a strong demand for robust and scalable thermal storage to decouple heat production from consumption. Germany’s Federal Ministry for Economic Affairs and Climate Action reported that industrial facilities installed more than 350 thermal storage systems in 2023 alone, primarily to leverage low-price electricity periods for electric boiler charging. The EU Emissions Trading System has further intensified this trend, with carbon prices exceeding 80 euros per ton in 2024, pushing energy-intensive firms to adopt storage-enabled electrification. Sweden’s SSAB and Norway’s Norsk Hydro have both commissioned industrial thermal storage units exceeding 20 megawatt thermal capacity to support fossil-free production roadmaps, as confirmed by their 2023 sustainability disclosures. Regulatory mandates under the EU Industrial Emissions Directive and access to Innovation Fund grants make industry the cornerstone of thermal storage deployment in Europe.

The residential segment is projected to expand at a CAGR of 15.2% during the forecast period, with the policy driven building renovations, rising heat pump adoption, and consumer demand for energy autonomy amid volatile energy prices. In 2023, heat pump installations in Europe surpassed 3 million units, and over 65% of these were paired with buffer tanks as per the European Heat Pump Association. Italy’s Ecobonus scheme provided 110% tax deductions for thermal storage retrofits in 2022–2023, resulting in more than 220000 residential units installed, according to the study. Similarly, the Netherlands requires all new homes to include at least 50 liters of thermal storage per household under its Building Decree 2024. Rising electricity self-consumption from rooftop solar, now exceeding 45% in German households,t further incentivizes storage to shift surplus daytime generation to evening heating needs.

COUNTRY LEVEL ANALYSIS

Germany Thermal Energy Storage Market Analysis

Germany was the largest contributor to the European thermal energy storage market by capturing 22.3% of the share in 2024, with its comprehensive regulatory ecosystem, including the Renewable Energy Sources Act and the Building Energy Act, which mandate thermal storage integration in new heating systems powered by renewables. Germany operates over 1200 district heating networks, nearly all of which have incorporated thermal storage since 20,20 as documented by the Federal Network Agency. The nation’s 2.1 gigawatt of installed solar thermal capacitywhich isre the highest in Europe according to the European Solar Thermal Industry Federation, relies heavily on buffer tanks for load leveling. Furthermore, Germany’s grid operator, TenneT, has piloted thermal storage as a flexibility resource in its “Sector Coupling” initiative, validating its role in balancing renewable supply and demand.

Denmark Thermal Energy Storage Market Analysis

Denmark's thermal energy storage market growth is likely to grow with its world-leading district heating penetration, and it integrates seasonal pit thermal storage at scale. Denmark hosts more than 300 large thermal storage units exceeding 1000 cubic meters, with the largest, Marstal’s 75000 cubic meter pit, storing solar heat for 6 months annually. The Energy Agreement 2022 committed 4.3 billion Danish kroner to expand thermal storage in urban heating systems through 2027. Moreover, Denmark’s power-to-heat strategy, managed by Energinet, enables electric boilers linked to thermal storage to absorb excess wind power. In 2023, this mechanism consumed 1.8 terawatt hours of surplus electricity, equivalent to 3% of national wind generation. Research institutions like DTU and Aalborg University continue to pioneer advanced materials by ensuring Denmark’s technological edge in long-duration thermal storage.

Sweden Thermal Energy Storage Market Analysis

Sweden's thermal energy storage market growth is likely to grow at the fastest CAGR in the coming years. Its strength lies in the synergy between abundant hydropower, nuclear baseload, and extensive district heating networks that collectively enable cost-effective thermal storage deployment. Over 50% of Sweden’s heating demand is met by district systems, and virtually all incorporate thermal storage tanks ranging from 500 to 10000 cubic meters. The government’s Fossil Free Sweden initiative has driven industrial adoption, with companies like SSAB and Sandvik installing high-temperature thermal buffers to support electrified furnaces. In 2023, Sweden added 850 new thermal storage units in residential buildings, largely due to the ROT tax deduction scheme covering 30% of installation costs. Additionally, the Swedish Energy Markets Inspectorate reported that thermal storage reduced peak heating electricity demand by 11% during the 2022–2023 winter, enhancing grid resilience.

Italy Thermal Energy Storage Market Analysis

Italy's thermal energy storage market growth is expected to grow with the aggressive building renovation incentives and rising solar thermal adoption in the residential and commercial sectors. The Superbonus 110 policy, active until 2023, drove the installation of over 180000 thermal storage tanks paired with heat pumps and solar collectors. Italy now boasts the ssecond-highestsolar thermal capacity in Europe at 4.2 gigawatts, according to the European Solar Thermal Industry Federation, with thermal storage essential for maximizing self-consumption. Industrial clusters in Lombardy and Emilia Romagna are also piloting PCM-based systems to recover waste heat from food and textile processing. In 2024, the Ministry launched the “Thermal Communities” program, allocating 200 million euros to support shared thermal storage in urban energy communities.

Netherlands Thermal Energy Storage Market Analysis

The Netherlands' thermal energy storage market growth is likely to grow with the innovative urban thermal infrastructure, including aquifer thermal energy storage (ATES) systems that serve over 2000 commercial buildings. The Netherlands hosts Europe’s highest density of ATES installations, leveraging its favorable geology to store cold in summer and heat in winter with round-trip efficiencies exceeding 80% as verified by TNO, the Netherlands Organisation for Applied Scientific Research. The National Heat Plan 2021 mandates that all new residential districts include thermal storage as part of zero gas heating systems. In 2023, the Port of Rotterdam launched a 100 megawatt thermal grid linking industrial waste heat sources to storage and distribution networks, supported by 120 million euros from the EU Innovation Fund. The country’s 2024 Building Decree requires minimum thermal storage volumes in all new construction by ensuring sustained market expansion driven by regulatory foresight and geological advantage.

COMPETITIVE LANDSCAPE

The competition in the European thermal energy storage market is characterized by a mix of specialized engineering firms, established energy technology providers, rs and innovative start-ups each targeting distinct segments. Large industrial players focushigh-temperatureture applications for heavy industry, while niche manufacturers dominate residential buffer tank supply. The absence of standardized performance metrics has created a fragmented landscape where differentiation hinges on material innovation,n system integration, and project execution speed. Public funding and regulatory mandates drive much of the procurement, ent creating intense competition government-backedcked tenders. At the same time, cross-border collaboration is increasing with companies forming consortia to access EU grants and scale proven solutions.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global europe thermal energy storage market include

- Calmac Manufacturing Corporation

- Bridgelux, Inc.

- Enerstore (VITO NV)

- Sonnen GmbH

- Viessmann Group

- Vaillant Group

- Bosch Thermotechnology GmbH

- ENGIE SA

- Siemens AG

- GE Renewable Energy

- Babcock & Wilcox Enterprises, Inc.

- Abengoa Solar

- BrightSource Energy, Inc.

- Absolicon Solar Collector AB

- Exergonix, Inc.

- EnergyNest AS

- Ice Energy, Inc.

- Hotbridge GmbH

- TES Vsetín a.s.

- Sunamp Ltd.

TOP LEADING PLAYERS IN THE MARKET

- Siemens Energy AG plays a pivotal role in advancing thermal energy storage across Europe through its integration of power to heat and hybrid storage solutions. The company has developed high-temperature thermal storage systems using solid media for industrial decarbonization, particularly in the steel and cement sectors. In 2023, Siemens partnered with Swedish green steel pioneer H2 Green Steel to supply electric boilers and thermal buffer systems capable of storing up to 100 megawatt hours of heat. It also collaborates with European grid operators to demonstrate thermal storage’s role in grid balancing. These initiatives reinforce Siemens Energy’s position as a technology enabler, leveraging renewable electricity and thermal demand in heavy industry and district heating networks across the continent.

- Baltimore Thermal LLC has established a strong footprint in Europe by deliverlarge-scalecale sensible heat storage solutions for district heating and industrial applications. The company specializes in custom-engineered hot water tanks with capacities exceeding 10000 cubic meters, deployed in countries like DenmarkGermanyan,y and Sweden. In early 20,24 Baltimore Thermal completed a 15000 cubic meter seasonal storage installation in Aarhus, Denmark, enabling the city to store summer solar thermal energy for winter use. The firm also works closely with European engineering procurement and construction firms to integrate storage into decarbonization retrofits. Its focus on ddurabilityy scalabi li, ty and seamless integration with existing thermal infrastructure has solidified its reputation as a reliable partner in Europe’s clean heat transition.

- Steffes Corporation contributes to the European thermal energy storage market through its advanced electric thermal storage systems designed for residential and commercial load shifting. While headquartered in the United States, the company has expanded its presence in Europe by partnering with heat pump and smart grid integrators in the United Kingd Ireland rela, nd and the Nordic region. In 2,023 Steffes launched a new generation of high-density ceramic core storage units compatible with dynamic electricity pricing and virtual power plant platforms. It also collaborated with a major Irish utility to deploy 500 residential thermal storage units as part of a demand response pilot. These efforts position Steffes as a key enabler of distributed thermal flexibility in Europe’s evolving electricity and heating landscape.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in Europeanrope thermal energy storage market primarily pursue strategic partnerships with district heating operators and industrial decarbonization projects to embed their technologies into large-scale infrastructure. They invest heavily in research and development to enhance energy density and reduce material costs, particularly for phase change and thermochemical systems. Companies also align closely with European Union funding mechanisms such as Horizon Europe and the Innovation Fund to co-finance deployments. Geographic expansion into Southern and Eastern Europe is another core tactic targeting regions with growing heating demand and supportive clean energy policies. The firms actively engage in policy advocacy to secure regulatory recognition of thermal storage as a grid flexibility asset, ensuring long term market viability.

MARKET SEGMENTATION

This research report on the europe thermal energy storage market is segmented and sub-segmented into the following categories.

By Technology

- Sensible Heat Storage

- Latent Heat Storage

- Thermochemical Storage

By Material

- Water

- Molten Salt

- Phase Change Materials (PCMs)

- Others

By End User

- Industrial

- Residential

- Commercial

- Utilities

By Country

- Germany

- Denmark

- Sweden

- Italy

- Netherlands

- Rest of Europe

Frequently Asked Questions

1. Which countries dominate the Europe Thermal Energy Storage Market?

Germany leads the Europe Thermal Energy Storage Market, followed by the United Kingdom, France, Italy, Austria, Denmark, Sweden, and Russia as key contributors to market revenue and technological deployment. Germany's dominance stems from its extensive solar district heating programs, robust renewable energy policies, and advanced concentrated solar power installations with integrated thermal storage systems that account for the largest market share in the European region.

2. What are the main technologies used in the Europe Thermal Energy Storage Market?

The Europe Thermal Energy Storage Market utilizes three primary technology segments: sensible heat storage (using water, molten salts, concrete, or sand), latent heat storage (employing phase change materials that absorb/release energy during phase transitions), and thermochemical storage (using reversible chemical reactions). Sensible heat storage currently holds the largest market share due to its cost-effectiveness and proven reliability in large-scale applications like concentrated solar power plants and district heating networks.

3. What applications drive demand in the Europe Thermal Energy Storage Market?

Power generation through concentrated solar power (CSP) plants represents the largest application segment in the Europe Thermal Energy Storage Market, followed by district heating and cooling systems serving urban areas, and HVAC applications in residential and commercial buildings. Europe operates over 200 solar district heating programs, predominantly in Germany, Austria, Denmark, and Sweden, where thermal energy storage enables seasonal energy management and peak load reduction for enhanced grid stability and operational efficiency.

4. How does thermal energy storage benefit concentrated solar power plants in the Europe Thermal Energy Storage Market?

In the Europe Thermal Energy Storage Market, thermal energy storage systems integrated with concentrated solar power (CSP) plants enable continuous electricity generation even when sunlight is unavailable by storing excess solar heat in molten salt systems during peak sunshine hours. This integration increases overall plant efficiency by 15-20%, reduces levelized cost of energy (LCOE), improves reliability, minimizes carbon dioxide emissions, and allows CSP facilities to provide dispatchable renewable power that supports grid stability during periods of high electricity demand.

5. What storage materials are commonly used in the Europe Thermal Energy Storage Market?

The Europe Thermal Energy Storage Market predominantly utilizes molten salts (sodium nitrate and potassium nitrate mixtures), water for sensible heat storage, phase change materials including paraffins and salt hydrates for latent heat storage, and solid materials like concrete blocks, rocks, and sand-like particles for thermal mass applications. Molten salt systems operate at temperatures ranging from 260°C to 565°C and offer superior energy density and long-duration storage capabilities compared to conventional battery storage technologies.

6. How does district heating utilize thermal energy storage in the Europe Thermal Energy Storage Market?

District heating systems in the Europe Thermal Energy Storage Market employ thermal energy storage to separate heat production from consumption times, storing hot water in large-scale tanks during periods of low demand or high renewable energy generation and distributing it when needed. This approach optimizes Combined Heat and Power (CHP) plant operations, enables integration of industrial surplus heat and solar thermal energy, provides seasonal storage capabilities for summer-to-winter energy transfer, and delivers operational cost savings exceeding DKK 6 million annually for major systems like Copenhagen's pit thermal energy storage.

7. What role do government policies play in the Europe Thermal Energy Storage Market growth?

Government policies significantly accelerate the Europe Thermal Energy Storage Market through mandates aligned with net-zero carbon emission targets, Paris Agreement commitments, the European Green Deal, and REPowerEU initiative that prioritize renewable energy infrastructure and sustainable storage solutions. These policies provide financial incentives for thermal storage integration in industrial sectors, residential buildings, and utility-scale renewable energy projects, while addressing energy security concerns and volatile fossil fuel prices that drive demand for cost-effective thermal energy management technologies.

8. What are the key differences between sensible, latent, and thermochemical storage in the Europe Thermal Energy Storage Market?

In the Europe Thermal Energy Storage Market, sensible heat storage increases material temperature proportionally with stored energy using water or molten salts; latent heat storage utilizes phase change materials that absorb/release substantial energy during solid-liquid transitions at constant temperature; and thermochemical storage employs reversible chemical reactions offering highest energy density and negligible long-term energy loss. Thermochemical systems provide superior compactness and scalability advantages with tailored temperature ranges for diverse applications, while sensible storage remains most commercially established for large-scale concentrated solar power and district heating implementations.

9. How does the Europe Thermal Energy Storage Market compete with battery storage solutions?

The Europe Thermal Energy Storage Market differentiates itself from battery storage by offering cost-effective long-duration energy storage (8-16 hours) at significantly lower capital costs per kilowatt-hour, particularly for building heating/cooling applications and utility-scale renewable energy integration where thermal storage excels. While batteries provide superior response times for electrical backup power, elevators, computers, and grid frequency regulation, thermal energy storage systems deliver better economics for managing daily and seasonal heating demands, industrial process heat recovery, and concentrated solar power applications where heat-to-power conversion efficiency and storage duration are critical performance parameters.

10. What is the role of phase change materials in the Europe Thermal Energy Storage Market?

Phase change materials (PCMs) in the Europe Thermal Energy Storage Market provide enhanced energy storage capacity through latent heat absorption/release during phase transitions, offering higher energy density per unit volume compared to sensible heat storage systems while maintaining constant operating temperatures. PCMs include inorganic systems like salt hydrates and metal alloys for medium-temperature applications, and organic compounds like paraffins and fatty acids for building-integrated thermal storage, with molten salt composite PCMs increasingly deployed in concentrated solar power plants to improve heat exchanger efficiency, shape stability, and electrical heating conversion rates by up to 93.8%

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com