Europe Tuberculin Market Size, Share, Trends & Growth Forecast Report By Product Type, Application & Country, Industry Analysis From 2026 to 2034

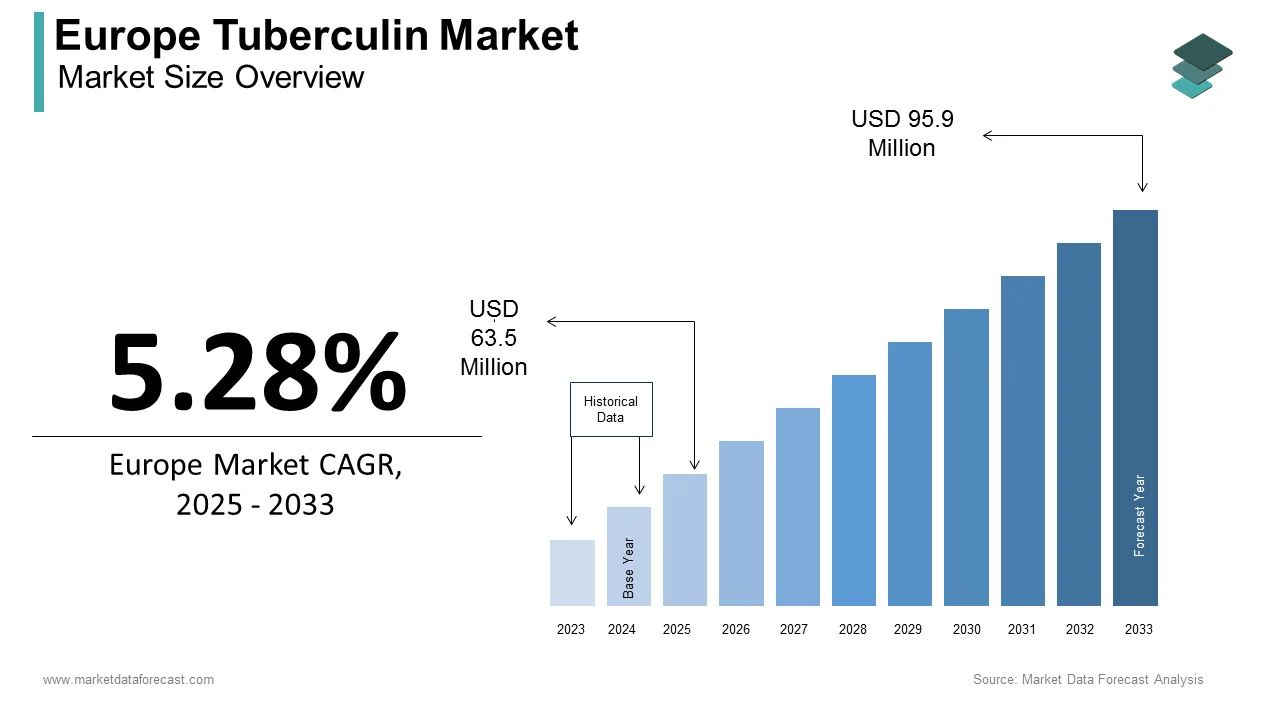

Market Size, 2025

$63.5 MnMarket Estimate, 2026

$66.85 MnMarket Forecast, 2034

$101 MnCAGR, 2026–2034

5.28%Europe Tuberculin Market Report Summary

The Europe tuberculin market was valued at USD 63.5 million in 2025, is anticipated to reach USD 66.85 million in 2026, and is projected to reach USD 101 million by 2034, growing at a CAGR of 5.28% during the forecast period. Market growth is driven by increasing tuberculosis surveillance programs, rising prevalence of bovine tuberculosis, and strong government initiatives for animal and public health management. The expanding use of tuberculin testing in livestock disease control, routine screening in high-risk populations, and cross-border disease monitoring programs is further supporting market expansion. Advancements in diagnostic accuracy, quality assurance standards, and vaccine-related research activities are also contributing to sustained demand across Europe.

Key Market Trends

- Increasing implementation of national tuberculosis eradication and monitoring programs across European countries.

- Rising demand for reliable diagnostic reagents in veterinary and public health applications.

- Growing focus on early disease detection and preventive healthcare in livestock management.

- Expansion of quality control and standardization protocols for tuberculin production and testing.

- Strengthening collaboration between public health agencies and veterinary authorities for integrated disease surveillance.

Segmental Insights

- Based on product type, the PPD RT23 segment dominated the Europe tuberculin market in 2025 by accounting for a substantial share. The segment’s dominance is attributed to its high reliability, standardized potency, and widespread acceptance in tuberculosis screening programs.

- Based on application, the animal use segment was the largest, holding 65.6% market share in 2025, driven by extensive testing requirements in cattle, wildlife, and dairy herds to control and eradicate bovine tuberculosis.

Regional Insights

The Europe tuberculin market is witnessing steady growth across major economies, supported by active disease surveillance systems, rising livestock health investments, and strong regulatory frameworks.

- The United Kingdom led the market by accounting for 21.4% share in 2025, driven by extensive bovine tuberculosis control programs and sustained government funding.

- Germany ranked second with 18.7% share in 2025, supported by advanced veterinary infrastructure and strong disease monitoring networks.

- Spain holds a significant position due to persistent bovine tuberculosis challenges, particularly in Castilla y León and Andalusia, where wild boar act as reservoirs, driving continuous testing demand.

Competitive Landscape

The Europe tuberculin market is characterized by the presence of established pharmaceutical manufacturers, biotechnology firms, and specialized diagnostic reagent providers. Market players are focusing on improving product consistency, enhancing supply chain reliability, and complying with stringent regulatory standards. Strategic collaborations with public health authorities, capacity expansions, and investments in quality assurance systems are strengthening competitive positioning across the region.

Prominent companies operating in the Europe tuberculin market include San Road Biological, Statens Serum Institut (SSI), Par Sterile, Sanofi Pasteur, Zoetis, Thermo Fisher Scientific, China National Biotec Group (CNBG), and CZ Veterinaria.

Europe Tuberculin Market Size

The tuberculin market size in Europe was valued at USD 63.5 million in 2025. The European market is anticipated to be worth USD 66.85 million in 2026 and USD 101 million by 2034, growing at a CAGR of 5.28% during the forecast period.

Tuberculin refers to purified protein derivative (PPD) derived from Mycobacterium tuberculosis, used primarily in the Mantoux skin test to detect latent tuberculosis infection. It is administered intradermally and interpreted based on induration size after 48 to 72 hours, serving as a critical tool in public health screening for high-risk populations, including healthcare workers, migrants, and immunocompromised individuals. Following an earlier decline, tuberculosis notifications in the European Union and European Economic Area have begun to rise, with a significant portion of cases originating from outside the region, particularly among specific migrant populations. Certain Eastern European nations within the broader European region continue to experience high tuberculosis incidence rates and significant challenges with drug-resistant strains. The European Medicines Agency classifies tuberculin as a medical product subject to rigorous regulatory standards and mandated batch release protocols, as defined by European Union legislation. National tuberculosis programs in countries like Germany, Sweden, and the UK mandate routine tuberculin testing for specific occupational and demographic groups, making it a cornerstone of preventive care despite the emergence of interferon gamma release assays. In this context, tuberculin maintains irreplaceable utility due to its low cost, simplicity, and established infrastructure across primary care settings.

MARKET DRIVERS

Mandatory Tuberculosis Screening in High-Risk Occupational and Migrant Populations

Public health policies across Europe enforce systematic tuberculin testing for populations at elevated risk of tuberculosis exposure or progression, which acts as a major driver of the Europe tuberculin market. Many European nations have implemented policies that mandate tuberculosis screening for specific groups, including individuals arriving from regions with higher disease prevalence and personnel working in healthcare or residential care environments. Protocols within these countries, such as those governing asylum procedures and occupational health regulations, establish a consistent, structured approach to screening, which results in ongoing demand for diagnostic tests. These institutionalized testing programs function independently of broader market trends, creating a stable requirement for tuberculin skin tests. National health frameworks frequently incorporate these screenings as a standard part of public health assessments for new residents and as mandatory, periodic occupational health check-ups for employees in care settings. Tuberculin remains a firmly anchored, first-line diagnostic tool driven by consistent migration trends, rising healthcare employment, and epidemiological requirements.

Integration into National Bovine Tuberculosis Eradication Programs

Tuberculin plays a dual role in the region as a veterinary diagnostic essential for controlling bovine tuberculosis, which is further propelling the expansion of the Europe tuberculin market. Bovine tuberculosis is a zoonotic disease with significant agricultural and public health implications. Regulations across the region necessitate mandated monitoring for tuberculosis in cattle herds using a specific skin test procedure. Screening efforts for this condition are extensive, with certain locations conducting more frequent testing to address persistent wildlife reservoirs. Substantial testing initiatives are carried out as part of efforts to reduce the occurrence of the disease in herds. Funding from agricultural policies supports monitoring and compensation programs, which help sustain the procurement of necessary testing materials. This cross-sectoral application ensures steady industrial-scale demand independent of human diagnostic trends. Moreover, the One Health approach endorsed by the World Organisation for Animal Health reinforces the linkage between animal and human tuberculosis control, making veterinary tuberculin not just an agricultural input but a pillar of integrated disease prevention across the continent.

MARKET RESTRAINTS

Limited Reimbursement and Declining Use in Favor of Interferon Gamma Release Assays

Tuberculin faces increasing displacement in human diagnostics by interferon gamma release assays, which offer higher specificity and eliminate cross reactivity with BCG vaccination, and thereby restrict the growth of the Europe tuberculin market. Several European nations are transitioning their diagnostic protocols by limiting the use of traditional skin tests to specific groups, such as children or individuals in areas with fewer medical resources. Multiple countries have shifted their primary testing focus for adults toward blood-based diagnostic methods. Updated clinical guidelines increasingly favor modern assays over older skin-based tests for routine screenings, particularly for staff in medical environments. There is a noticeable trend of decreasing reliance on traditional testing methods within specialized healthcare facilities. While newer blood-based tests carry a higher initial unit price than traditional skin tests, they are often viewed as offering greater diagnostic precision. The transition toward blood-based testing is partly driven by the logistical advantage of requiring fewer patient consultations to complete a single screening. Public hospitals facing budget constraints increasingly adopt this shift despite tuberculin’s lower unit cost due to savings in follow-up visits and false positive management. The increasing preference for precision and efficiency in national health systems is narrowing tuberculin's diagnostic application to niche areas, which is undermining its established market volume.

Stringent Batch-to-Batch Potency Variability and Regulatory Compliance Burdens

The biological nature of tuberculin introduces significant manufacturing challenges related to consistency, potency, and regulatory oversight that constrain supply reliability. Consequently, this limits the expansion of the European tuberculin market. The validation process for tuberculin involves assessing antigenic activity through animal-based testing, which is time-intensive and susceptible to natural, inherent fluctuations in results. Regulatory standards require that the potency of each batch remain within a precise, narrow range, yet variations in the cultivation process often necessitate the rejection of batches. A significant portion of tuberculin batches submitted for official control fails initial potency testing, leading to the necessity for reprocessing or disposal. Regulatory bodies enforce strict, comprehensive traceability and documentation for all raw materials, cell banks, and production parameters. These requirements deter new entrants and limit production flexibility for existing manufacturers who operate under thin margins. Consequently, supply shortages occur periodically, undermining public health program continuity and eroding confidence in tuberculin as a dependable diagnostic tool.

MARKET OPPORTUNITIES

Expansion of Pediatric and School-Based Latent TB Screening Initiatives

Emerging public health strategies targeting childhood tuberculosis offer strong potential for sustained tuberculin use given its safety profile and suitability for young populations, which is expected to fuel the growth of the Europe tuberculin market. Pediatric tuberculosis accounts for a small percentage of reported cases but is challenging to diagnose in children due to atypical symptoms. The incidence in children is considered an indicator of recent transmission within a community. School-based screening programs are being implemented, utilizing non-invasive methods like the tuberculin skin test for their cost-effectiveness and ease of use. Screening programs targeting young students are identifying latent infections, particularly in areas with higher incidence rates. Governmental health organizations are funding the expansion of these screening initiatives in regions with tuberculosis rates above the national average. The European Respiratory Society endorses tuberculin for children under five, as interferon assays show reduced sensitivity in this age group. The EU roadmap for childhood TB prioritizes child-friendly testing, creating a specific niche for tuberculin tests whose practical benefits currently outweigh modern alternatives in pediatric care.

Adoption in Wildlife Surveillance and Cross-Border Animal Health Coordination

The growing recognition of wildlife reservoirs, particularly badgers in the UK and wild boar in Spain, as sources of bovine tuberculosis transmission has expanded tuberculin’s application into ecological surveillance, which is predicted to contribute to the expansion of the Europe tuberculin market. Wildlife surveillance and testing initiatives for detecting specific pathogens are increasingly implemented across multiple European nations. The application of diagnostic agents in wild populations is occurring through both direct capture methods and experimental vaccine trials. Systematic, large-scale testing of badger populations is part of broader disease eradication strategies in specific regions. Cross-border initiatives are being launched to monitor wild boar populations along shared borders. Wildlife disease surveillance is a prioritized area for funding within European health strategies, with a focus on early detection in potential reservoir species. These programs require large volumes of veterinary tuberculin with standardized potency across jurisdictions. Rising human-wildlife-livestock interfaces, driven by climate and land-use changes, are creating a durable demand for expanded surveillance. This shift moves beyond traditional livestock testing, establishing tuberculin as a key tool for managing diseases at an ecosystem level.

MARKET CHALLENGES

Cold Chain and Shelf Life Limitations in Decentralized Healthcare Settings

The requirement for uninterrupted refrigeration and short shelf life complicates distribution in rural and primary care environments. This is a persistent operational challenge to the Europe Tuberculin Market. Strict requirements for maintaining a cold chain and limited post-opening shelf lives often lead to the disposal of unused medical supplies. Maintaining the integrity of temperature-sensitive materials is particularly difficult for outreach programs that operate outside of centralized locations. Unlike lyophilized vaccines, tuberculin is supplied only in liquid form with no thermostable alternative approved under current EU pharmacopoeial standards. This fragility limits deployment in community pharmacies, school health services, and migrant reception centers where cold chain infrastructure is unreliable. Despite universal access policies, the public health impact of tuberculin remains constrained in decentralized settings, awaiting formulation advances that ensure ambient stability.

Lack of Standardization in Interpretation and Training Across Primary Care Providers

Variability in tuberculin test administration and reading introduces diagnostic inconsistency that affects its reliability and fuels skepticism among clinicians, and thereby negatively impacts the expansion of the Europe tuberculin market. Variability exists in measuring skin reaction induration, influenced by subjective visual interpretation and inconsistent environmental conditions. Test accuracy can be affected by staff training levels, with less frequent training correlating with higher rates of missed infections in primary care settings. Discrepancies in diagnostic cutoffs across guidelines may lead to inconsistent interpretations in cross-border regions. Standardized electronic training resources for test interpretation are not uniformly available across all health jurisdictions. In the absence of standardized certification and digital measurement tools, such as caliper apps, the test’s accuracy is compromised by operator variability, which diminishes confidence in results and accelerates the adoption of objective blood-based assays. This human factor represents a systemic vulnerability that cannot be resolved by product improvement alone but requires coordinated educational investment across fragmented healthcare systems.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Application, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | San Road Biological, Statens Serum Institut (SSI), Par Sterile, Sanofi Pasteur, Zoetis, Thermo Fisher Scientific, China National Biotec Group (CNBG), CZ Veterinaria, and Others. |

SEGMENT ANALYSIS

By Product Type Insights

The PPD RT23 segment dominated the Europe Tuberculin Market by accounting for a substantial share in 2025. The dominance of the PPD RT23 segment is driven by its standardized composition and widespread regulatory acceptance across both human and veterinary applications. PPD RT23 is produced using a reference strain of Mycobacterium tuberculosis under strict WHO guidelines, ensuring consistent antigenic profile and batch reproducibility, a critical requirement for national tuberculosis control programs. In human diagnostics, countries like Sweden, Denmark, and the Netherlands specify PPD RT23 in their national protocols due to its well-documented sensitivity in BCG vaccinated populations. The European Pharmacopoeia includes monographs exclusively for PPD RT23, further cementing its status as the gold standard. This harmonized adoption ensures PPD RT23 remains the backbone of tuberculosis surveillance across the continent.

The PPD S segment is predicted to witness the highest CAGR of 5.8% between 2026 and 2034 due to its preferential use in specific national human diagnostic protocols where historical validation and local manufacturing support create entrenched demand. In the United States, PPD S derived from a different M tuberculosis seed lot is standard, but in Europe, it persists primarily in Germany and parts of Eastern Europe due to legacy infrastructure. Additionally, some research institutions favor PPD S for immunological studies due to subtle differences in protein epitopes that may influence T cell response profiles. While not replacing PPD RT23 in mainstream programs, its niche application in specialized clinical settings and continuity requirements in long term cohort studies sustain steady growth. Germany’s top-tier TB monitoring system ensures persistent demand for PPD S, defying broader trends toward standardization.

By Application Insights

The animal use segment was the largest segment by holding a 65.6% share in 2025. The supremacy of the animal use segment is attributed to the mandatory and large-scale nature of bovine tuberculosis eradication programs enforced across all EU member states under the Animal Health Law. Bovine tuberculosis testing involves a high volume of animals across Europe, with increased surveillance and multiple rounds of testing occurring in specific regions known for higher prevalence. Certain locations with identified wildlife reservoirs undergo intensive, frequent testing initiatives aimed at managing infection levels. Significant funding is allocated by European authorities to support these comprehensive surveillance programs, which include efforts to detect, control, and manage infected animals. Unlike human testing, which is targeted and declining in some regions, animal testing is universal, recurrent, and legally binding, creating predictable high-volume demand. Furthermore, the One Health framework endorsed by the World Organisation for Animal Health reinforces the linkage between animal and human tuberculosis control, making veterinary tuberculin not just an agricultural necessity but a pillar of integrated public health strategy across Europe.

The human use segment is estimated to register the fastest CAGR of 4.9% during the forecast period, owing to expanded screening mandates for vulnerable populations and renewed focus on latent tuberculosis elimination. An increased movement of people into Europe has led to enhanced protocols for infectious disease screening within reception facilities in various nations. Regional health strategies increasingly emphasize the early detection of latent infections shortly after arrival in member states. Public health initiatives are focusing more on pediatric screenings to identify and manage infections within school-aged populations. Medical guidelines continue to support the use of specific, established diagnostic tools for assessing infections in young children. Public health imperatives are overriding technological substitution in high-risk cohorts, ensuring sustained and even growing demand for human tuberculin in targeted yet voluminous screening initiatives.

COUNTRY-LEVEL ANALYSIS

United Kingdom Tuberculin Market Analysis

The United Kingdom led the Europe tuberculin market by accounting for a 21.4% share in 2025. The prominence of the UK market is supported by its dual burden of human and bovine tuberculosis, requiring intensive surveillance across both domains. Human health guidelines require tuberculin screening for incoming healthcare staff, arriving asylum seekers, and individuals exposed to active cases, creating a consistent volume of screenings. Wildlife management strategies involve ongoing, localized badger testing initiatives within specific regions. Cattle surveillance programs mandate extensive, widespread herd testing to monitor for infection within the farming industry. The UK also hosts one of Europe’s few licensed tuberculin manufacturers, ensuring domestic supply security. Despite Brexit, the country maintains alignment with EU potency standards through mutual recognition agreements. This combination of high disease burden, rigorous policy enforcement, and localized production cements the UK’s role as Europe’s highest volume and most operationally complex tuberculin market.

Germany Tuberculin Market Analysis

Germany was the second largest country in the Europe tuberculin market by holding a share of 18.7% in 2025. The growth of the German market is fuelled by its systematic occupational health framework and large migrant screening infrastructure. Regular tuberculosis screening is a recurring requirement for healthcare and social care professionals as a measure of workplace safety. Latent tuberculosis screening is also part of the health assessments for individuals seeking asylum. These mandatory testing protocols are designed to cover a broad range of workers in specialized sectors and are integrated into the procedures for processing large groups of new arrivals. The country uniquely maintains dual approval for both PPD RT23 and PPD S, allowing institutional preference based on historical calibration. The Paul Ehrlich Institute enforces stringent batch release protocols, ensuring high quality but also contributing to occasional supply constraints. Germany’s decentralized federal structure means 16 state health authorities independently procure tuberculin, creating fragmented but consistent demand. Germany maintains a stable, high-compliance, and effective human tuberculosis (TB) program, driven by robust funding, low social stigma, and strong legal mandates. This approach facilitates high detection and treatment success rates within the European region.

Spain Tuberculin Market Analysis

Spain captured a noteworthy position in the Europe tuberculin market due to its extensive bovine tuberculosis challenges, particularly in regions like Castilla y León and Andalusia, where wild boar act as persistent reservoirs. Cattle monitoring involves a high volume of annual testing, with more frequent screenings required for herds located in designated high-risk areas. A cross-border initiative has been implemented with a neighboring country to conduct surveillance along shared wildlife corridors using tuberculin. Public health strategies include specific screenings for detainees and newly arrived individuals, with a focus on particular populations. The country also serves as a logistical hub for tuberculin distribution to North Africa under EU health cooperation agreements. Spain’s role as a critical hub in TB management, both in livestock and human health, is driven by endemic transmission and intense livestock density, ensuring a steady requirement for high-quality tuberculin.

Ireland Tuberculin Market Analysis

Ireland grew steadily in the Europe tuberculin market owing to its exceptional per capita usage stems from its intensive bovine tuberculosis eradication program, one of the world’s most aggressive, which tests every cattle herd at least once yearly and high-risk herds up to four times. Tuberculin tests are administered at a frequency that results in the volume of tests exceeding the size of the national herd, which suggests the implementation of repeated testing protocols. Wildlife intervention is incorporated into the disease management program, with tuberculin used in both vaccination trials and standard skin testing. Human testing focuses on specific populations like close contacts and those with compromised immune systems, contributing a smaller portion to the overall testing volume. The state-owned manufacturer ensures an uninterrupted supply aligned with national potency standards. Ireland’s commitment to tuberculin-based surveillance remains unwavering, making it the most veterinary-dependent market in Europe.

France Tuberculin Market Analysis

France is predicted to expand in the Europe tuberculin market from 2026 to 2034 due to balanced demand from the human public health and veterinary sectors. The national tuberculosis program mandates tuberculin screening for healthcare students, asylum seekers, and contacts of active cases, resulting in a substantial number of human tests annually. Agricultural authorities mandate screening for cattle, involving a high volume of animals, particularly in regions with elevated dairy density where disease transmission risks are higher. The national reference laboratory verifies the quality of tuberculin batches to ensure adherence to established European standards. Recent policy shifts include expanded school screening in overseas departments like Guadeloupe, where TB incidence exceeds metropolitan rates. Additionally, France participates in EU-funded research on tuberculin alternatives but continues to rely on PPD RT23 for operational consistency. France bridges human and animal health imperatives to maintain a stable, scientifically grounded tuberculin ecosystem, driven by strong coordination and substantial funding.

COMPETITIVE LANDSCAPE

The Europe Tuberculin Market features limited competition due to high regulatory barriers, stringent biological manufacturing requirements, and low commercial margins, which deter new entrants. The market is primarily served by a few specialized entities, including public health institutes like Statens Serum Institut and established pharmaceutical or animal health companies such as Sanofi and Zoetis. Competition is not price-driven but centered on regulatory compliance, batch reliability, and alignment with national tuberculosis control protocols. Human and veterinary segments operate almost independently with distinct regulatory pathways and customer bases. Public manufacturers dominate due to their non-profit orientation and integration with national health systems, while private players focus on niche or regional mandates. The threat of substitution by interferon gamma release assays exists in human diagnostics but is mitigated in veterinary and pediatric applications, where tuberculin remains irreplaceable. Overall, the market is characterized by stable demand, predictable procurement cycles, and strategic importance outweighing commercial incentives, making it a mission-driven rather than profit-driven sector.

KEY MARKET PLAYERS

The leading companies operating in the Europe tuberculin market include:

- San Road Biological

- Statens Serum Institut (SSI)

- Par Sterile

- Sanofi Pasteur

- Zoetis

- Thermo Fisher Scientific

- China National Biotec Group (CNBG)

- CZ Veterinaria

TOP PLAYERS IN THE MARKET

- Statens Serum Institut is a Danish public health and research institution that serves as a leading global supplier of tuberculin, particularly PPD RT23, used in both human and veterinary diagnostics. SSI is recognized by the World Health Organization as a reference manufacturer and supplies standardized tuberculin to numerous countries, including most EU member states. The institute produces tuberculin under strict Good Manufacturing Practice conditions with full traceability from seed lot to final vial. In recent years, SSI has enhanced its batch release protocols by integrating digital potency tracking and expanding cold chain logistics to reduce wastage in decentralized settings. It also collaborates with the European Centre for Disease Prevention and Control on harmonizing tuberculin interpretation guidelines across member states. SSI supports national TB programs by combining the roles of a public health agency and a commercial supplier, ensuring consistent quality and stable supply.

- Sanofi is a French multinational pharmaceutical company with a legacy in biological reagents, including tuberculin for human diagnostic use. While it has scaled back broader vaccine operations in Europe, Sanofi continues to manufacture and distribute PPD S under regulatory authorization in Germany and select Eastern European markets where historical validation supports its continued use. The company leverages its established distribution network and regulatory expertise to maintain compliance with national pharmacopoeial standards. Recently, Sanofi upgraded its biologics facility in Lyon to align with European Medicines Agency requirements for biological reference products, ensuring ongoing batch consistency. It also provides technical support to public health agencies on storage, handling, and administration protocols. Sanofi’s role, though not high-volume, guarantees supply stability for European institutions relying on PPD S, supporting a diversified diagnostic ecosystem.

- Zoetis is a global animal health leader with significant involvement in the European veterinary tuberculin market. The company supplies PPD RT23 formulations specifically calibrated for bovine and wildlife tuberculosis testing across livestock and surveillance programs. Zoetis works closely with national veterinary authorities in the UK, Ireland, and Spain to meet stringent potency and sterility requirements mandated under the EU Animal Health Law. In recent years, the company has invested in cold chain integrity systems, including temperature-monitored shipping and extended shelf life formulations, to reduce field wastage. It also partners with wildlife agencies on tuberculin-based monitoring of badgers and wild boar populations. Zoetis targets the veterinary sector, supplying critical, reliable solutions that support the EU’s One Health approach to combating tuberculosis.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Tuberculin Market are prioritizing compliance with European Pharmacopoeia and WHO reference standards to ensure batch consistency and regulatory acceptance. They are investing in cold chain optimization and digital batch tracking to minimize wastage in decentralized healthcare and veterinary settings. Companies are strengthening partnerships with national public health and veterinary authorities to align production with mandatory screening programs. Strategic focus on either human or animal segments allows specialization in formulation calibration and distribution logistics. Additionally, firms are supporting training initiatives for healthcare workers and veterinarians to standardize test administration and interpretation, thereby enhancing diagnostic reliability and maintaining trust in tuberculin as a critical public health tool.

EUROPE TUBERCULIN MARKET NEWS

- In May 2024, Statens Serum Institut, a Danish public health institute, implemented a digital batch potency tracking system for its PPD RT23 production, enhancing traceability and reducing variability. This upgrade strengthens its Europe Tuberculin Market presence.

- In November 2023, Zoetis, an American animal health company, launched an extended shelf life formulation of veterinary tuberculin validated for use in wild boar surveillance programs in Spain and Portugal. This innovation reduces field wastage in ecological monitoring.

- In February 2024, Sanofi, a French pharmaceutical company, modernized its biologics facility in Lyon, France, to comply with updated European Medicines Agency standards for biological reference products. This ensuresthe continued supply of PPD S for legacy human diagnostic programs

- In September 2023, Statens Serum Institut partnered with the European Centre for Disease Prevention and Control to develop standardized training modules for tuberculin test interpretation across member states. This initiative improves diagnostic consistency and reinforces clinical trust.t

- In March 2024, Zoetis collaborated with the UK Animal and Plant Health Agency to supply temperature-monitored tuberculin shipments for badger testing in England. This logistics enhancement minimizes cold chain breaches in remote field operations.

MARKET SEGMENTATION

This research report on the Europe tuberculin market is segmented and sub-segmented into the following categories.

By Product Type

- PPD-S

- PPD RT23

By Application

- Human Use

- Animal Use

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe tuberculin market?

The Europe tuberculin market supplies PPD solutions for TB skin testing in humans and cattle. It supports screening programs across healthcare and veterinary sectors.

What drives the Europe tuberculin market?

TB incidence and animal health priorities drive the Europe tuberculin market. Awareness campaigns and healthcare infrastructure expand diagnostic demand.

How is the Europe tuberculin market segmented?

The Europe tuberculin market segments by application into human diagnostics and veterinary testing, plus product forms for skin tests and assays.

Which countries lead the Europe tuberculin market?

Germany and UK lead the Europe tuberculin market with advanced diagnostics. France and Spain follow through TB surveillance programs.

Why human diagnostics dominate the Europe tuberculin market?

Human TB screening programs fuel the Europe tuberculin market detecting latent infections via Mantoux tests in high-risk populations.

What role does veterinary testing play in the Europe tuberculin market?

Veterinary tuberculin tests protect livestock in the Europe tuberculin market preventing zoonotic transmission from cattle herds.

What applications define the Europe tuberculin market?

TB detection in healthcare and agriculture characterizes the Europe tuberculin market using intradermal injections for immune response assessment.

What challenges face the Europe tuberculin market?

IGRA alternatives and BCG vaccination interference challenge the Europe tuberculin market requiring complementary diagnostic strategies.

How does regulation impact the Europe tuberculin market?

EMA approvals standardize the Europe tuberculin market ensuring PPD purity and efficacy for reliable TB screening outcomes.

Why syringes important in the Europe tuberculin market?

Safety-engineered tuberculin syringes enable precise dosing in the Europe tuberculin market reducing needlestick risks during skin testing.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com