- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

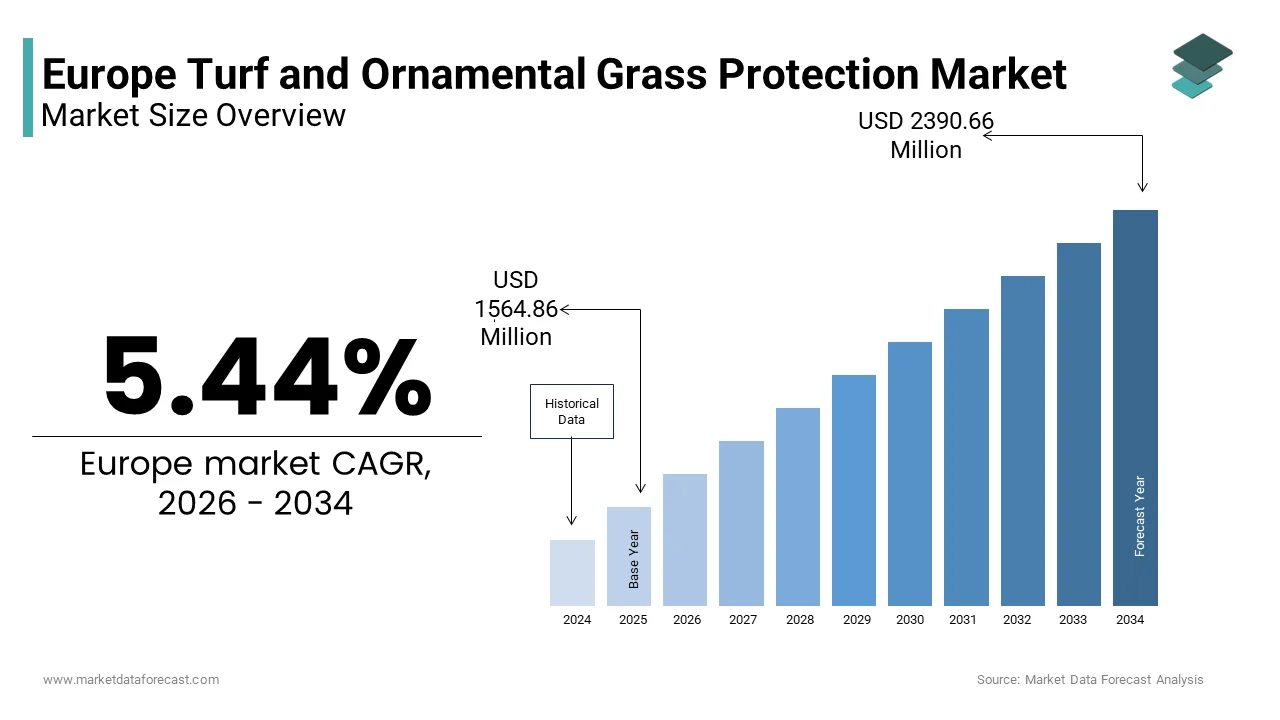

Market Size, 2025

$1484 MnMarket Estimate, 2026

$1564 MnMarket Forecast, 2034

$2390 MnCAGR, 2026–2034

5.44%Europe Turf and Ornamental Grass Protection Market Size

The Europe turf and ornamental grass protection market was valued at USD 1484.12 million in 2025 and is anticipated to reach USD 1564.86 million in 2026 and 2390.66 million by 2034, growing at a CAGR of 5.44% during the forecast period from 2026 to 2034.

Turf and ornamental grass protection includes a specialised range of chemical and biological solutions, including fungicides, herbicide,s insecticid, es plant growth regulat,,ors and bio stimulants that are designed to preserve the aesthetic quality,, health,, and functional performance of managed grassed areas such as golf courses, sports stadiums,, public park,,s and residential lawns. Unlike agricultural crop protection products, these formulations prioritise visual uniformity, disease resistance, and wear tolerance over yield. The market operates within a tightly regulated environmental framework that increasingly restricts synthetic active ingredients. According to the European Environment Agency, over 80 million hectares of land in the EU are classified as agricultural and managed green areas, requiring routine maintenance. As per Eurostat, a majority of European cities with populations exceeding 100,000 implement municipal green space management plans that mandate pest and disease control protocols. The European Green Deal’s Farm to Fork Strategy targets a 50% reduction in chemical pesticide use by 2030, which is intensifying pressure to innovate with bio-based alternatives. This intersection of urban greening mandates, ecological regulation, and visual expectation defines the unique contours of the Europe turf and ornamental grass protection market.

MARKET DRIVERS

Stringent Urban Green Space Management Regulations Driving Preventive Care

Municipal and institutional mandates for maintaining high-quality public green spaces are one of the key factors driving the European turf and ornamental grass protection market. According to the European Urban Green Space Observatory, a majority of EU cities with more than 50,000 residents enforce aesthetic and safety standards for parks, sports fields, and roadside verges requiring proactive disease and weed control. In Germany, the Federal Nature Conservation Act obliges local authorities to ensure green spaces remain “visually intact and functionally safe” year-round. This translates into scheduled applications of fungicides and growth regulators even in the absence of visible infestation. As per the European Turfgrass Society, municipal groundskeepers in France and the Netherlands frequently apply preventive fungicide programs during humid spring months to avoid outbreaks of Microdochium patch that could trigger public complaints. Additionally, major sporting venues such as Wembley Stadium and Camp Nou operate under UEFA and FIFA pitch quality guidelines that mandate uniform grass cover and traction, as these standards are unattainable without integrated protection regimes. This institutionalised expectation of perfection sustains consistent demand for professional turf care solutions.

Expansion of High Value Sports and Leisure Infrastructure

The growth of premium sports stadiums, golf courses, and recreational complexes across Europe directly fuels demand for advanced turf protection technologies, which is further boosting the regional market expansion. According to the European Golf Association, over 6,800 golf courses operate in the EU, hosting millions of rounds annually, with a significant share classified as championship or resort grade requiring intensive agronomic management. Similarly, UEFA’s stadium infrastructure reports indicate that numerous new or renovated football venues have been completed since 2022, many featuring hybrid turf systems that demand specialised fungicides and wetting agents to prevent root rot and compaction. These high-traffic surfaces experience extreme wear and microclimate stress, making them vulnerable to diseases like Fusarium and anthracnose. As per the All England Lawn Tennis Club, Wimbledon’s grass courts receive more than 15 targeted protection treatments per year to maintain quality. Private leisure operators also invest heavily as Scandinavian wellness resorts now feature year-round ornamental lawns using cold-tolerant grass blends protected by bio-stimulants that enhance frost resilience. This concentration of high-value managed turf creates a premium segment where performance justifies cost and innovation thrives.

MARKET RESTRAINTS

Progressive EU Pesticide Restrictions Limiting Active Ingredient Availability

The Europe turf and ornamental grass protection market faces significant constraints from the European Union’s aggressive chemical reduction agenda under the Sustainable Use of Pesticides Regulation and the Farm to Fork Strategy. As per the European Commission, more than 40 synthetic active substances previously used in amenity turf care have been withdrawn since 2020, including key fungicides such as iprodione and chlorothalonil. The approval process for new chemistries has slowed dramatically; according to the European Food Safety Authority, only a limited number of novel turf-specific actives gained EU authorisation between 2021 and 2024. National bans compound this pressure—France’s “Loi Labbé” prohibits all non-professional pesticide use in public spaces, while Germany’s Plant Protection Act restricts applications within 50 metres of water bodies. These measures force grounds managers to rely on fewer, less effective tools, increasing the risk of turf failure. For instance, municipal parks across Europe have reported increased disease incidence following the loss of legacy fungicides. Without timely access to robust alternatives, the market risks declining turf quality and rising maintenance costs.

Public Opposition to Chemical Use in Urban Environments

Growing societal resistance to pesticide application in public green spaces presents a persistent social and operational barrier to the turf protection market in Europe. According to the European Consumer Organisation, a majority of EU citizens support restrictions or bans on synthetic pesticides in parks and playgrounds, which reflects heightened environmental health awareness. This sentiment translates into local policy action as over 300 municipalities in Italy, Spain, and Belgium have adopted “pesticide-free park” ordinances since 2022. In Sweden and Denmark, chemical applications in municipal green spaces now require prior public notification and justification. Such scrutiny discourages groundskeepers from using even approved products due to fear of complaints or media backlash. As per the European Environment Agency, professional pesticide usage in urban amenity areas declined significantly between 2021 and 2024 despite rising disease pressure. This social license deficit forces a rapid shift toward biologicals and cultural controls, which is creating a performance gap that threatens the viability of high-quality managed turf in public settings.

MARKET OPPORTUNITIES

Rising Adoption of Bio-based and Microbial Turf Protection Solutions

The regulatory and social pressure against synthetics has catalysed significant innovation in bio-based turf protection, which is creating a high growth opportunity for the European turf and ornamental grass protection market. According to the European Biocontrol Manufacturers Association, registrations of biologically active substances for amenity turf increased in the EU between 2021 and 2024. Products containing Bacillus subtilis, Trichoderma harzianum, and seaweed extracts now offer measurable suppression of dollar spot and red thread diseases. As per independent trials conducted by leading turf research institutes in the UK in 2024, a microbial and humic acid blend demonstrated meaningful disease reduction in sports turf. As per Horizon Europe, funding was allocated in 2024 to develop next-generation biostimulants that enhance grass resilience through root microbiome modulation. As per industry reports, golf courses in the Netherlands and Switzerland are leading adoption, with many now integrating biologicals into seasonal programs. This concentration of high-value managed turf creates a premium segment where performance justifies cost and innovation thrives, justified by growing biological registrations, supported efficacy evidence, and targeted public R&D investment.

Integration of Precision Application Technologies and Digital Agronomy

The convergence of digital tools and precision delivery systems is a promising opportunity for the European turf and ornamental grass protection market. According to the European Agricultural Machinery Association, robotic mowers equipped with spray modules are increasingly being deployed on European golf courses and municipal lawns, enabling targeted micro applications that reduce chemical use significantly. Platforms like Syngenta’s “TurfCloud” use satellite imagery and soil moisture sensors to generate variable rate treatment maps, identifying only those zones requiring intervention. As per the European Committee for Standardisation, EN 17895 is being finalised to certify AI-driven disease prediction models for professional turf use. In Germany, municipal parks in Munich and Hamburg now employ drone-based multispectral scanning to detect early stress signatures before visible symptoms appear, allowing preemptive bio-stimulant deployment. This data-driven approach not only complies with EU chemical reduction targets but also lowers operational costs and enhances turf performance consistency. As digital infrastructure matures, precision agronomy is becoming the new standard for high-accountability turf management.

MARKET CHALLENGES

Limited Efficacy and Inconsistent Performance of Biological Alternatives

Despite growing investment, biological turf protection products often fail to deliver the reliability and speed of action required in high-stakes managed environments, which is one of the major challenges to the European turf and ornamental grass protection market. According to independent multi-site trials in Europe, microbial fungicides achieved only 40 to 55% control of Microdochium nivale under cold, wet conditions, significantly below the 80–85% control offered by legacy synthetics. This performance gap is exacerbated by environmental sensitivity as the viability of live bacteria and fungi in formulations declines rapidly under UV exposure or temperature fluctuations during storage. As per surveys of professional turf managers, many groundskeepers at UEFA stadium venues still rely on synthetic fungicides for critical match-day preparation due to unpredictable bio-efficacy. Furthermore, the lack of standardised testing protocols for biologicals under EU regulations means product claims are often based on non-comparable trial data. Without robust field validation and shelf-life stability improvements, many biologicals remain relegated to supplementary roles, which is undermining the sector’s transition to sustainable protection.

Fragmented Regulatory Approval Processes Across Member States

The Europe turf and ornamental grass protection market contends with a highly inconsistent national implementation of EU pesticide regulations, creating commercial and compliance uncertainty. While Regulation EC 1107/2009 governs active substance approval at the EU level, product authorisation remains the responsibility of individual member states. According to the European Commission’s 2024 Pesticide Monitoring Report, approval timelines for turf fungicides vary significantly across member states, with Germany completing reviews in under a year while Italy may take up to two years due to differing risk assessment interpretations. This fragmentation forces manufacturers to maintain multiple dossier versions and delays pan-European launches. In 2024, a leading biostimulant was approved in France and the Netherlands but rejected in Spain over unstandardised ecotoxicity data requirements. The lack of mutual recognition undermines economies of scale and discourages SMEs from entering the market. Until the EU harmonises national evaluation criteria and establishes a centralised authorisation pathway for non-food use products, the market will remain inefficient, and innovation will be stifled by administrative duplication.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.44% |

| Segments Covered | By Type, Product, and Country |

| VaProductnalyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | Germany, France, Italy, UK, Spain, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Rest of Europe |

| Market Leaders Profiled | Adama Agricultural Solutions LTD, American Vanguard Corporation, AMVAC Chemical Corporation, Arysta Lifescience, Bayer CropScience AG, Bio-Works Inc., Cheminova A/S, Chemtura Agro Solutions, DuPont, FMC Corporation, Syngenta International AG, and Valent Biosciences Corp. |

SEGMENTAL ANALYSIS

By Type Insights

The turf segment led the market by holding 60.8% of the European turf and ornamental grass protection market share in 2024. The dominance of the turf segment in the European market is driven by the high maintenance demands of intensively managed sports and recreational surfaces. Golf courses, football stadiums, and municipal playing fields require year-round disease and wear resistance that necessitates regular protective treatments. For instance, extensive areas of sports turf are actively maintained across the EU, and a large share receive scheduled fungicide and growth regulator applications. According to UEFA Pitch Quality Guidelines, Champions League venues are required to maintain high-quality, uniform grass cover and consistent shear strength, as these standards are nattainable without integrated chemical and biological protection. As per Deloitte’s 2024 Annual Review of Football Finance, a single match postponement due to turf failure can lead to significant revenue losses for clubs. As per Germany’s Federal Institute for Sports Science, public sports fields commonly undergo preventive disease control to ensure year-round usability. This performance imperative sustains consistent demand for advanced turf protection solutions across professional and public sectors.

The ornamental grass protection segment is the fastest growing segment in the Europe turf and ornamental grass protection market and is predicted to witness a CAGR of 8.2% over the forecast period, owing to the rising investment in urban landscaping, public realm aesthetics, cs and luxury residential developments that prioritise visual perfection. According to Eurostat, new urban development projects in the EU in 2024 frequently included dedicated ornamental lawns and decorative grass beds as part of sustainability and wellbeing mandates. High-end residential complexes in Spain and Italy now feature curated native grass blends requiring specialised herbicides to suppress invasive species without harming delicate cultivars. According to Entente Florale Europe, the competition awarded multiple cities in 2024 for ornamental horticulture excellence, which is driving municipal investment in precision protection tools. Furthermore, ornamental grasses are increasingly used in green infrastructure such as bioswales and green roofs, where root rot from waterlogging demands targeted fungicide use. This fusion of urban design policy and aesthetic expectation fuels sustained innovation in ornamental grass care.

By Product Insights

The synthetic fungicides segment held 33.1% of the European market share in 2024. The growth of the synthetic fungicides segment in this regional market can be credited to their unmatched efficacy against high-impact diseases like Microdochium patch, Fusarium, um and dollar spot. Despite regulatory pressure, these chemistries remain indispensable in high-value settings where turf failure is not an option. For instance, groundskeepers in the UK, Germany, and the Netherlands continue to use synthetic fungicides at least once per season to meet performance standards. As per UEFA pitch management practices, stadium venues apply timely curative fungicide treatments to avoid match disruptions. Compounds like azoxystrobin and propiconazole continue to be authorised for amenity use under strict stewardship protocols. According to the European Food Safety Authority, these actives pose negligible risk to bystanders when applied according to label instructions on non-food sites in 2024. This risk-managed authorisation, combined with performance reliability, ty ensures synthetic fungicides remain the backbone of professional turf disease control despite the rise of biologicals.

The bio-fungicides segment is the fastest expanding product category in the Europe turf and ornamental grass protection market and is anticipated to record a CAGR of 13.2% over the forecast period, owing to the tightening EU restrictions on synthetic actives and growing institutional demand for sustainable alternatives. According to the International Biocontrol Manufacturers Association, biocontrol registrations and market activity in Europe have increased in recent years as the sector expands. As per peer‑reviewed and technical sources, products containing Bacillus subtilis and Trichoderma harzianum offer measurable suppression of turf diseases such as Fusarium and red threadTaylor & Francis Online. As per the Sports Turf Research Institute and Golf Course 2030 guidance, adoption of integrated turf management has grown across European golf courses, with greater incorporation of biological tools alongside cultural practices. As per green public procurement practices in Sweden and the Netherlands, municipalities promote lower‑impact inputs and increasingly specify environmental criteria that favour biologicals in public park management. For instance, formulation innovations and improved microbial strains are enhancing the field performance of biological fungicides. This regulatory tailwind, institutional adoption, and technological maturation position bio‑fungicides as the highest growth vector.

COUNTRY ANALYSIS

Germany Turf And Ornamental Grass Protection Market Analysis

Germany led the turf and ornamental grass protection market in Europe in 2024 by holding 23.2% of the regional market share. The dense network of professional sports venues, municipal green spaces, and advanced agronomic research is fuelling the domination of Germany in the European market. According to national sports associations, Germany maintains regulated football pitches and numerous golf courses, all adhering to strict national turf quality standards set by the German Football Association and German Golf Association. As per the Federal Ministry for the Environment, many German municipalities implement integrated pest management plans for public parks that include both synthetic and biological protection tools. According to Germany’s Federal Institute for Risk Assessment, restricted use of key fungicides on non-food sites is permitted, which ensures continuity of care. According to the Julius Kühn Institute, leading research institutions validate new turf protection products under EU guidelines. This ecosystem of regulatory clarity, professional demand, and scientific validation solidifies Germany’s position as Europe’s most sophisticated and highest value turf protection market.

United Kingdom Turf And Ornamental Grass Protection Market Analysis

The United Kingdom held a promising share of the Europe turf and ornamental grass protection market in 2024. The growth of the UK in the European market is driven by its globally renowned sports culture and historic commitment to landscape aesthetics. According to the Sports Turf Research Institute, a large majority of Premier League stadiums use hybrid turf systems requiring intensive protection against wear and disease. According to industry golf data, the UK has one of the highest densities of golf courses in Europe, with thousands of facilities maintaining championship-grade playing surfaces. As per the Department for Environment, Food and Rural Affairs, municipal councils manage extensive areas of public green space under the Good Practice Guide for Urban Greening, which endorses targeted pesticide use where non-chemical methods fail. Despite post-Brexit regulatory autonomy, the UK maintains alignment with EU pesticide standards, ensuring product continuity. The rise of ornamental lawns in luxury housing developments in the South East further boosts demand. This blend of sporting excellence, civic landscaping, and regulatory pragmatism sustains the UK’s leadership role.

France Turf And Ornamental Grass Protection Market Analysis

France is projected to account for a promising share of the Europe turf and ornamental grass protection market during the forecast period. The strong municipal landscaping culture and complex regulatory landscape are propelling the French market growth. France manages public parks under the “Ville Fleurie” programme, which awards communes for floral and turf excellence, driving investment in ornamental grass protection. However, France enforces some of Europe’s strictest pesticide laws; the Loi Labbé prohibits all non-professional synthetic pesticide use in public spaces since 2022. This paradox creates high demand for authorised professional products and advanced biocontrol solutions. As per recent reports, France has over 960 communes participating in the Ville Fleurie programme, with regions such as Grand Est and Auvergne-Rhône-Alpes leading in the number of awarded municipalities. As per the French Golf Federation, France has more than 400 golf courses, all of which are encouraged to adopt integrated protection plans to ensure consistent product use. This dual pressure of aesthetic expectation and chemical restriction fosters a dynamic market where innovation in biologicals and precision application thrives.

Italy Turf And Ornamental Grass Protection Market Analysis

Italy is expected to exhibit a prominent CAGR in the Europe turf and ornamental grass protection market over the forecast period due to its luxury residential landscaping and historic garden preservation. High-end developments in Tuscany, Lombardy, and the Amalfi Coast feature ornamental native grasses requiring selective herbicides to suppress invasive species without harming delicate cultivars. According to Coldiretti, Italy’s floriculture sector reached a record value of €3.3 billion in 2024, with production spread across 30,000 hectares of ornamental plants and flowers, driven by premium real estate and export demand. Italy maintains around 233 golf courses, with several internationally recognized venues such as Marco Simone Golf & Country Club hosting championship events. However, the country faces regulatory fragmentation; regional authorities in Tuscany and Emilia Romagna enforce stricter pesticide bans than national guidelines, creating compliance complexity. As per Italy’s CAP Strategic Plan, the Ministry of Agricultural Policies promotes biologicals and sustainable practices, with targeted funding allocated to urban green management initiatives. This mix of luxury demand, agronomic challenge, and policy variance defines Italy’s unique market trajectory.

Netherlands Turf And Ornamental Grass Protection Market Analysis

The Netherlands is estimated to account for a notable share of the Europe turf and ornamental grass protection market over the forecast period. The Netherlands is emerging as a leader in sustainable turf innovation and horticultural expertise. The country’s 292 golf courses and over 40 professional football stadiums operate under the Green Deal Sports Infrastructure, which is part of the Netherlands’ broader sustainability agenda, aiming to phase out synthetic pesticide use in sports and public spaces. As per Wageningen University initiatives, soil microbiome research is increasingly applied to urban and agricultural systems, supporting targeted bio-stimulant applications. The Netherlands is also a hub for biocontrol development; as per Koppert Biological Systems, the company supplies microbial fungicides and biological crop protection solutions across Europe. As per the Dutch Ministry of Agriculture’s Circular Agriculture Vision, urban green spaces are included in strategies promoting closed-loop nutrient and protection systems. Additionally, ornamental grasses remain integral to Dutch water management landscapes such as retention basins, which require disease-resistant cultivars to sustain ecological resilience. This fusion of policy leadership, scientific research, and ecological design positions the Netherlands as a benchmark for next-generation turf protection in Europe.

COMPETITIVE LANDSCAPE

The Europe turf and ornamental grass protection market features intense competition among three multinational agrochemical leaders—Bayer, Syngenta, and BASF—who dominate through integrated portfolios, regulatory expertise, and professional service networks. These firms compete on product efficacy, environmental profile, and digital enablement rather than price due to the specialised nature of professional turf care. New entrants face high barriers, including stringent EU pesticide authorisation requirements, limited access to field trial networks, and the need for agronomic credibility. Differentiation arises through innovations in biological formulation science and data-driven application tools. Regional players exist but lack the scale to offer full seasonal programs or comply with fragmented national regulations. Competition is further shaped by institutional procurement policies, sports federation guidelines, and municipal green space mandates. The market rewards companies that combine scientific rigor, sustainability commitment, and on-the-ground support in this highly regulated and expectation-driven sector.

KEY MARKET PLAYERS

The main companies that are dominating the Europe market for turf and ornamental grass protection are

- Adama Agricultural Solutions LTD

- American Vanguard Corporation

- AMVAC Chemical Corporation

- Arysta Lifescience

- BASF SE

- Bayer CropScience AG

- Bio-works Inc

- Cheminova A/S

- Chemtura Agro Solutions

- DuPont

- FMC Corporation

- Syngenta International AG

- Valent Biosciences Corp.

Top Players in the Market

- Bayer AG is a global leader in crop protection with a dedicated turf and ornamental solutions portfolio serving professional groundskeepers across Europe. Through its Environmental Science division, Bayer offers integrated programs combining synthetic fungicides like Serata and bio-based innovations such as Trianum bio fungicide. The company supports golf courses, stadiums, and municipalities with agronomic advisory services and digital tools like the GreenTrust app for usage documentation. In 20,24, Bayer launched a new microbial seed treatment for ornamental grasses that enhances root resilience against soil-borne pathogens. It also expanded its stewardship training for professional applicators in alignment with the EU Sustainable Use Regulation requirements. These initiatives reinforce Bayer’s role as a science-driven partner in sustainable professional turf management worldwide.

- Syngenta Group maintains a strong presence in the Europe turf and ornamental grass protection market through its Professional Solutions business, focusing on high-performance disease and weed control. The company provides products such as Heritage fungicide and Primo growth regulator, widely used on UEFA stadiums and championship golf courses. Syngenta invests heavily in field validation, working with the Sports Turf Research Institgenerate EU-specific efficacy data. In early 2025, Syngenta introduced an advanced-generation bio-fungicide formulated with improved UV stability for consistent field performance. It also enhanced its TurfCloud digital platform, enabling variable rate applications on real-time disease risk mapping. These actions strengthen Syngenta’s reputation for innovation, prisio,n, and r, regulatory compliance in Europe and globally.

- BASF SE plays a pivotal role in the Europe turf and ornamental grass protection market through its Performance Products division,n offering differentiated chemistries and biologicals for professional use. The company’s portfolio includes Medallion fungicide and Legacy herbicide, known for selectivity on ornamental grasses. BASF collaborates with European green space managers to develop integrated protection plans that balance efficacy with environmental stewardship. In 202, BASF launched a nneonicotinoid-containing productcontaining seaweed extracts and humic acids that improves drought tolerance in amenity turf. It also partnered with German municipalities to pilot pesticide reduction programs using precision sprayers and drone monitoring. These efforts position BASF as a solutions provider committed to sustainable urban green space management across Europe and international markets.

Top Strategies Used by the Key Market Participants

Key players in the Europe turf and ornamental grass protection market are accelerating the development of bio-based and hybrid formulations to comply with EU chemical reduction targets. They invest in digital agronomy platforms enabling precision application and usage documentation for regulatory compliance. Companies provide agronomic advisory services and stewardship training to professional applicators to ensure proper product use. Strategic partnerships with sports federations, golf associations, a nd municipal networks enhance field validation and adoption. Innovation in formulation technology improves stability, itself, and rainfastness of biologicals. Ultimately, all firms engage in policy dialogue to shape national implementation of pesticide regulations. These strategies collectively aare regulatorylat ory, so,cietal and performance demands in a rapidly evolving market.

MARKET SEGMENTATION

This research report on the European turf and ornamental grass protection market has been segmented and sub-segmented into the following regions.

By Type

- Turf

- Ornamental

By Product

- Synthetic Pesticides

- Synthetic Herbicides

- Synthetic Insecticides

- Synthetic Fungicides

- Other Synthetic Pesticides

- Bio-pesticides

- Bio-herbicides

- Bio-insecticides

- Bio-fungicides

- Other Bio-pesticides

- Other crop protection products

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe