Europe Vinyl Flooring Market Size, Share, Trends & Growth Forecast Report, Segmented By Type (Luxury Vinyl Tiles, Vinyl Sheets, Vinyl Tiles), End Use, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis From (2026 To 2034)

Europe Vinyl Flooring Market Report Summary

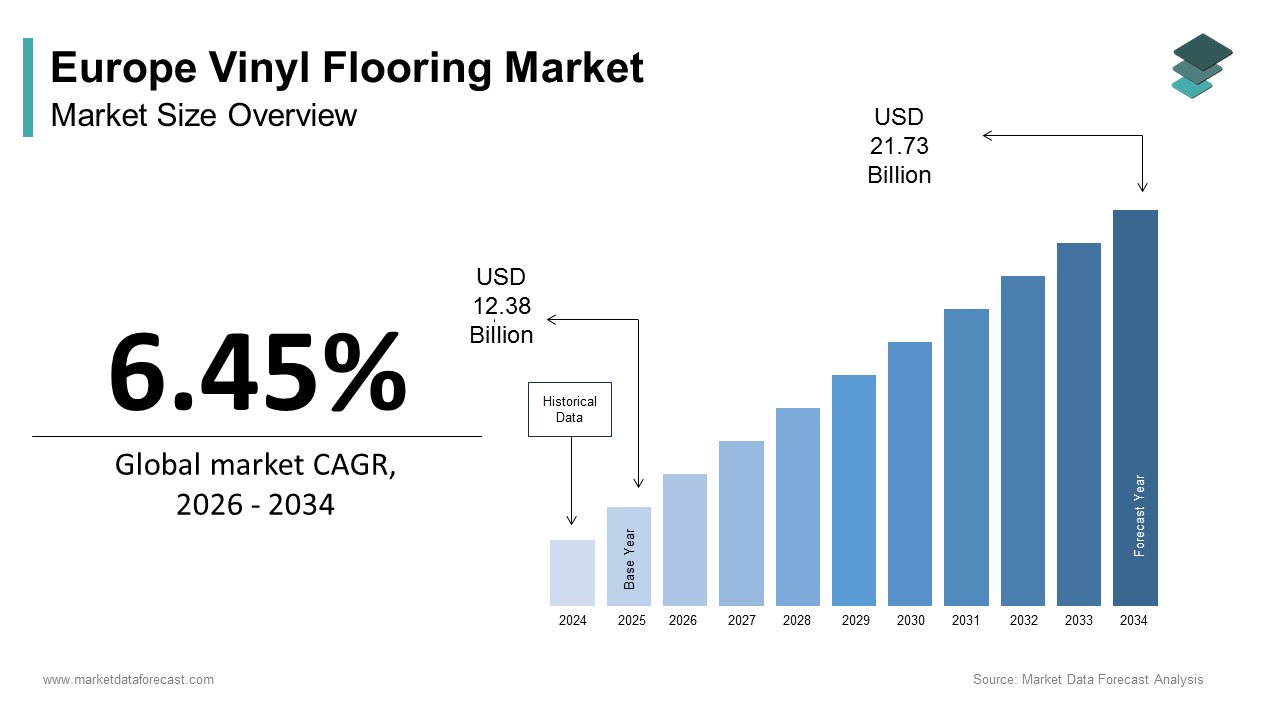

The Europe vinyl flooring market was valued at USD 12.38 billion in 2025 and is projected to reach USD 21.73 billion by 2034, growing from USD 13.18 billion in 2026 at a CAGR of 6.45% during the forecast period. Market growth is driven by rising renovation activities, increasing demand for durable and low-maintenance flooring solutions, and strong adoption across commercial and institutional buildings. The growing popularity of luxury vinyl tiles, supported by advancements in design realism and ease of installation, is further accelerating market expansion. Sustainability initiatives, improved recyclability, and compliance with green building standards are also positively influencing demand across Europe.

Key Market Trends

- Increasing adoption of luxury vinyl tiles due to design flexibility, durability, and cost efficiency

- Strong demand from non-residential spaces such as healthcare facilities, offices, retail, and hospitality

- Rising renovation and retrofit activities across aging building stock in Europe

- Growing focus on sustainable, low-VOC, and recyclable vinyl flooring solutions

- Expansion of modular and click-lock vinyl flooring systems supporting faster installation

Segmental Insights

- Based on type, the luxury vinyl tiles segment dominated the Europe vinyl flooring market in 2024 by capturing 48.2% of the total market share, driven by superior aesthetics, durability, and suitability for high-traffic areas

- Based on end use, the non-residential segment led the market in 2024 by holding 56.3% of the market share, supported by strong demand from commercial, healthcare, education, and hospitality sectors

Regional Insights

- Germany led the Europe vinyl flooring market by capturing 24.3% of the total market share in 2024, supported by strong construction activity, renovation demand, and commercial infrastructure

- France ranked second by accounting for 11.2% of the market share in 2024, driven by public infrastructure upgrades and commercial construction

- United Kingdom is expected to witness steady growth, supported by rising demand in healthcare facilities, private rental housing, and retrofit projects

- Italy is experiencing growth due to its dense network of small and medium-sized flooring manufacturers and strong demand from hospitality and historic renovation projects

- Netherlands is expanding steadily, supported by progressive green building policies, high urban density, and strong adoption of circular economy construction models

Competitive Landscape

The Europe vinyl flooring market is moderately competitive, with leading players focusing on product innovation, sustainable materials, and design differentiation. Companies are expanding their portfolios with eco-friendly vinyl flooring, enhancing digital printing technologies, and strengthening distribution networks across residential and commercial channels.

Prominent players in the Europe vinyl flooring market include Tarkett, Forbo Flooring Systems, Gerflor, Interface, IVC Group, Polyflor, Amtico, BerryAlloc, Balta Group, and Karndean Design Flooring.

Europe Vinyl Flooring Market Size

The Europe vinyl flooring market size was calculated to be USD 12.38 billion in 2025 and is anticipated to be worth USD 21.73 billion by 2034, growing from USD 13.18 billion in 2026 at a CAGR of 6.45% during the forecast period.

Vinyl flooring of polyvinyl chloride (PVC), combined with plasticizers, stabilizers, and fillers, is engineered for durability, water resistance, and aesthetic versatility across residential, commercial, and institutional settings. According to Eurostat, over 2.1 million new residential dwellings were completed across the European Union in 2023, creating consistent demand for cost-effective and low-maintenance flooring solutions. As per the European Environment Agency, more than 180000 public buildings, including schools, hospitals, and administrative offices, underwent renovation under the EU’s Renovation Wave Strategy in 2023, a program mandating improved indoor environmental quality and accessibility, where slip-resistant and easy-to-clean surfaces like vinyl are preferred. Furthermore, the European Committee for Standardization enforces EN 649 and EN 650 classifications governing wear resistance, indentation, and fire behavior, ensuring performance consistency.

MARKET DRIVERS

EU Renovation Wave and Public Infrastructure Upgrades Drive Institutional Demand

The ambitious building renovation agenda for vinyl flooring adoption in public and commercial sectors is majorly propelling the growth of Europe vinyl flooring market. According to the European Commission, over 35 million buildings across the EU are targeted for energy and accessibility upgrades by 2030 under the Renovation Wave Strategy, with public facilities prioritized in the first phase. Vinyl flooring is frequently specified in these projects due to its compliance with EN 14041 standards for accessibility by offering smooth transitions, low rolling resistance for wheelchairs, and slip resistance under EN 13893. The French Ministry of Education mandated resilient flooring in all 12000 primary school renovations in 2023, citing acoustic comfort and impact absorption for child safety. Similarly, Germany’s Technical Relief Agency installed over 1.2 million square meters of antimicrobial vinyl in temporary refugee housing facilities to support hygiene and rapid deployment. These publicly funded projects create stable, non-cyclical demand insulated from consumer sentiment fluctuations.

Rising Preference for Sustainable and Phthalate-Free Vinyl Formulations in Residential Projects

The consumer demand for healthier indoor environments has accelerated the adoption of eco-certified is also boosting the growth of Europe vinyl flooring market. According to the European Consumer Organisation, over 68% of homeowners in Germany, France, and the Netherlands consider indoor air quality a top factor when selecting flooring, with a shift driven by heightened health awareness post pandemic. This has propelled demand for phthalate-free formulations using alternative plasticizers like DINCH and TOTM, which now constitute 82% of residential vinyl production in Western Europe, as confirmed by the European Council of Vinyl Manufacturers in its 2023 sustainability review. Major retailers such as IKEA and Leroy Merlin require all vinyl flooring sold in their EU stores to carry the EU Ecolabel or Blue Angel certification, which restricts volatile organic compound emissions to below 50 micrograms per cubic meter. In Sweden, over 90% of new multi-family housing developments specified certified low-emission vinyl in 2023, as per the study.

MARKET RESTRAINTS

Stringent Chemical Regulations Under REACH Restrict Raw Material Availability

The European Chemicals Agency’s ongoing restrictions on substances of very great concern under the REACH regulation are limiting the growth of Europe vinyl flooring market. In 2023, the agency added two widely used ortho-phthalate plasticizers, such as DINP and DIDP, to the authorization list, requiring companies to seek explicit permission for continued use after sunset dates. Although the industry had largely transitioned to non-phthalate alternatives, these regulatory actions created supply chain uncertainty and increased raw material costs by 12 to 15%, as per the study. Furthermore, the 2024 restriction proposal on lead stabilizers still used in some recycled content formulations threatens to disrupt circular economy models. According to the European Resilient Flooring Manufacturers Institute, over 40% of vinyl flooring producers reported reformulation delays in 2023 due to insufficient safety data on substitute additives. Europe’s precautionary principle approach means regulatory decisions often precede scientific consensus, creating compliance burdens that stifle innovation and increase time to market for new products.

Perception of Vinyl as Non-Renewable Despite Advances in Recycled Content

The persistent perception of vinyl flooring as environmentally unsustainable continues to limit its specification in green building projects. This factor is additionally hampering the growth of Europe vinyl flooring market. In reality, the VinylPlus voluntary program reported that 860000 metric tons of post-consumer and post-industrial vinyl flooring were collected and recycled in Europe in 202 equivalent to 34% of total production. This knowledge gap is exacerbated by greenwashing from competing material sectors and the absence of harmonized environmental product declarations. Until lifecycle data is widely communicated and trusted, this reputational barrier will constrain market penetration in sustainability-driven segments.

MARKET OPPORTUNITIES

Growth in Healthcare and Elderly Care Infrastructure Creates Premium Demand for Hygienic Flooring

The aging population and post pandemic healthcare investment are driving specialized demand for antimicrobial and easy-to-disinfect vinyl flooring in clinical and residential care settings, which is accelerating new opportunities for the growth of Europe vinyl flooring market. According to Eurostat, 21.3% of the EU population was aged 65 or older in 2023, a figure projected to reach 29% by 2050, necessitating expansion of elderly housing and assisted living facilities. The European Centre for Disease Prevention and Control mandates non-porous seamless flooring in all new healthcare construction to minimize pathogen harborage, a requirement met effectively by heterogeneous vinyl with welded seams. Germany’s Federal Ministry of Health funded the renovation of 210 nursing homes with flooring that meets DIN 51130 R10 slip resistance and ISO 22196 antimicrobial standards. Similarly, France’s Agence Nationale de l’Habitat allocated 450 million euros for senior housing upgrades specifying vinyl with acoustic underlays to reduce fall impact noise. Leading manufacturers like Tarkett and Gerflor now offer flooring with silver ion or zinc pyrithione additives validated under EN 14476 for enveloped virus resistance.

Expansion of Modular and Click Vinyl Systems in DIY and Rental Markets

The rise of urban rental housing and do-it-yourself renovation trends is fueling demand for loose lay and rigid core click vinyl flooring that requires no adhesive and can be installed over existing substrates. This factor is swiftly leveraging the growth of Europe vinyl flooring market. According to Eurostat, 32% of Europeans lived in rented accommodation in 2023, with rates exceeding 50% in Germany, Denmark, and the Netherlands. Tenants increasingly seek temporary non-damaging solutions that comply with landlord restrictions, by creating ideal conditions for floating vinyl planks. Similarly, IKEA’s VINDSTYRKA line, made with 80% recycled content, sold over 1.2 million square meters in 2023, primarily to urban renters in Stockholm, Berlin, and Amsterdam. The European Committee for Standardization recently updated EN 16511 to include performance criteria for modular systems, enhancing consumer confidence. This shift toward user-friendly temporary and reversible flooring solutions aligns with Europe’s dynamic urban housing landscape and circular design principles.

MARKET CHALLENGES

Volatility in PVC Resin Prices Linked to Energy and Chlor Alkali Markets

The fluctuations in PVC resin pricing driven by energy costs and chlorine supply dynamics in the chlor-alkali industry are posing a major challenge for the growth of Europe vinyl flooring market. According to ICIS, the European PVC spot price increased by 22% in 2023 due to reduced chlorine demand from the water treatment sector and high natural gas prices affecting electrolysis operations. Since PVC constitutes 40 to 60% of vinyl flooring’s material cost, these swings directly impact manufacturer margins and retail pricing. In 2023, three mid-sized flooring producers in Italy and Spain suspended production for 6 weeks due to unprofitable input costs as reported by the European Resilient Flooring Manufacturers Institute. Europe lacks integrated PVC producers with dedicated flooring grades, forcing converters to compete with pipe and cable sectors for resin allocation. The European Commission’s Carbon Border Adjustment Mechanism further adds cost uncertainty as upstream chemical producers pass on compliance expenses. This raw material fragility undermines price stability and deters long term investment in capacity expansion.

Fragmented Waste Collection Infrastructure Limits Post-Consumer Recycling Rates

The inconsistent and underdeveloped end-of-life collection systems that hinder true closed-loop recycling additionally degrade the growth of Europe vinyl flooring market. According to VinylPlus, only 12% of post-consumer vinyl flooring is currently collected separately from mixed construction waste due to a lack of standardized demolition protocols and economic incentives. In 2023, Germany’s dual system Interseroh reported that 68% of vinyl flooring from residential renovations ended up in incineration because contractors lacked sorting facilities. The EU Construction and Demolition Waste Management Protocol encourages selective demolition, but only six member states have implemented mandatory separation for resilient flooring, as per the European Environment Agency. Without a harmonized take-back scheme,s extended producer responsibility rules, or design for disassembly standards, the industry cannot achieve its 2025 target of 1 million tons recycled annually. This systemic gap contradicts the EU Green Deal’s circular economy vision and exposes the sector to future regulatory risk as waste policies tighten.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.45% |

| Segments Covered | By Type, End Use, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Tarkett, Forbo Flooring Systems, Gerflor, Interface, IVC Group, Polyflor, Amtico, BerryAlloc, Balta Group, Karndean Designflooring |

SEGMENTAL ANALYSIS

By Type Insights

The luxury vinyl tiles segment was the largest by capturing 48.2% of the Europe vinyl flooring market share in 2024 from their ability to replicate natural materials like wood, stone, and concrete with exceptional realism while offering superior durability, water resistance, and acoustic comfort. The segment has become the preferred choice in both high-end residential and commercial projects where aesthetic flexibility and performance are equally valued. In 2023, IKEA reported that 72% of its European flooring sales were LVT due to its compatibility with underfloor heating and scratch resistance tested under EN 660-2. Similarly, the UK’s National House Building Council documented that LVT was specified in 68% of new multi-family housing developments in 2023 for its impact absorption and low maintenance. The technology behind LVT, where rigid core constructions with wear layers exceeding 0.55 millimeters meet the EN 649 classification for heavy commercial use, enabling seamless use across homes, offices, and retail.

The luxury vinyl tiles segment is likely to grow with an expected CAGR of 9.2% from 2025 to 2033, owing to the innovations in rigid core technology and sustainability credentials that align with EU green building mandates. In 2023, Tarkett launched a new line of LVT made with 85% recycled content and bio-based plasticizers certified under the EU Ecolabel, a product that achieved 210000 square meters in public sector contracts within six months. The German Sustainable Building Council now awards extra DGNB certification points for flooring with verified recycled content and low VOC emissions, criteria that LVT increasingly meets. Additionally, the rise of urban micro apartments in cities like Paris, Amsterdam, and Stockholm favors LVT for its dimensional stability over concrete subfloors and compatibility with click installation systems that avoid wet adhesives. As per Eurostat, over 1.2 million new urban dwellings were completed in EU cities in 2023, creating ideal conditions for LVT’s rapid deployment.

By End-Use Insights

The non-residential segment was the largest by holding 56.3% of the Europe vinyl flooring market share in 2024, due to stringent functional requirements in public and commercial buildings, where safety, hygiene, durability, and accessibility are non-negotiable. European building codes, such as DIN 18041 in Germany and NF P 01-013 in France, mandate specific acoustic absorption and slip resistance values for schools, hospitals, and transport hubs, standards consistently met by heterogeneous vinyl sheets and tiles. In 2023, the European Investment Bank funded 840 public infrastructure projects requiring flooring compliant with EN 13893 (slip resistance) and EN ISO 717-2 (impact sound insulation) that exclude many hard surface alternatives. France’s Ministry of Education specified vinyl flooring in all 12000 school renovation projects in 2023, due to its impact absorption and ease of disinfection. Similarly, Germany’s Technical Relief Agency installed over 1.5 million square meters of antimicrobial vinyl in refugee reception centers to support rapid hygiene protocols. These institutional mandates create stable, high-volume demand insulated from consumer sentiment and economic cycles.

The residential segment is projected to expand at a CAGR of 8.7% throughout the forecast period, owing to the rising urbanization, rental housing expansion, and consumer preference for low-maintenance, sustainable flooring in private dwellings. In 2023, 32% of Europeans lived in rented accommodation, with rates exceeding 50% in Germany, Denmark, and the Netherlands, according to Eurostat, creating demand for temporary non-damaging solutions like click LVT. IKEA reported a 39% year on year increase in LVT sales across its European stores in 2023, driven by urban renters seeking reversible installations. Additionally, the EU Renovation Wave Strategy allocated 15 billion euros in 2023 for residential energy efficiency upgrades, where flooring is often replaced alongside insulation and windows. Retailers like Leroy Merlin now require all vinyl flooring sold in their EU stores to carry EU Ecolabel certification, ensuring low VOC emissions with a standard that has reshaped residential product development.

REGIONAL ANALYSIS

Germany Vinyl Flooring Market Analysis

Germany was the top performer of the Europe vinyl flooring market by capturing 24.3% of the share in 2024, with its robust construction sector, stringent building codes, and leadership in sustainable manufacturing. According to the German Federal Statistical Office, over 320000 new residential units were completed in 2023, with 78% specifying resilient flooring for bathrooms and kitchens due to moisture resistance requirements under DIN 18540. The country’s public infrastructure investment under the KfW Energy Efficient Construction program mandated acoustic and slip-resistant flooring in all subsidized multi-family housing, a rule that favored vinyl across 85000 units. Germany is also home to Tarkett’s largest European production facility in Baden-Württemberg, which supplies phthalate-free LVT with Blue Angel certification to public projects. The German Sustainable Building Council’s DGNB certification system awards points for recycled content and low-emission flooring, further incentivizing eco vinyl adoption.

France Vinyl Flooring Market Analysis

France's vinyl flooring market was ranked second by capturing 11.2% of the market share in 2024, with its large-scale public renovation programs and preference for seamless sheet vinyl in institutional settings. The national ANAH agency also subsidized flooring upgrades in 280000 low-income housing units requiring products meeting VOC emission limits under the French A+ label. Gerflor, a French manufacturer, supplies over 60% of public sector vinyl contracts with products validated under ISO 22196 for antimicrobial performance. Additionally, France’s urban renewal agency ANRU, allocated 3.2 billion euros in 2023 for social housing rehabilitation, where durable water-resistant flooring is essential in high-density environments.

United Kingdom Vinyl Flooring Market Analysis

The United Kingdom vinyl flooring market is likely to grow with the strong demand in the healthcare, private rental, and retrofit sectors. According to the UK Health Security Agency, all new NHS hospital builds must use non-porous seamless flooring to minimize infection risk, with a standard met by welded vinyl sheet systems. The National House Building Council reported that LVT was installed in 71% of new residential developments due to its compatibility with underfloor heating and impact sound reduction required under Part E of Building Regulations. The private rental sector also drives adoption, with 45% of landlords replacing carpets with vinyl between tenancies as per the Residential Landlords Association survey. The UK maintains alignment with EU chemical regulations through UK REACH, ensuring the continued use of phthalate-free formulations. Companies like Polyflor and Amtico export 60% of their output to EU markets, maintaining integrated supply chains.

Italy Vinyl Flooring Market Analysis

Italy's vinyl flooring market growth is likely to grow with its dense network of small to medium enterprises in flooring manufacturing and strong demand in hospitality and historic renovation. According to Confindustria, over 450 resilient flooring producers operate in the Emilia Romagna and Veneto regions, many specializing in custom printed LVT for hotels and retail. In 2023, the Ministry of Cultural Heritage approved vinyl flooring for use in 210 protected historical buildings where traditional materials could not meet modern accessibility or fire safety codes, thereby creating a niche for thin-profile adhesive LVT. Additionally, Italy’s National Recovery and Resilience Plan allocated 1.8 billion euros in 2023 for tourism infrastructure upgrades, including hotels and museums, where durable low-maintenance flooring is essential. Italian manufacturers like GranitiFiandre and Ergon have developed LVT that mimics Venetian terrazzo and marble with EN 13501-1 fire class Bfl-s1 certification.

Netherlands Vinyl Flooring Market Analysis

The Netherlands vinyl flooring market growth is likely to grow with its progressive green building policies, high urban density, and in circular-economy models. According to the Dutch Green Building Council, over 90% of new public buildings constructed in 2023 achieved BREEAM NL certification, which awards credits for flooring with verified recycled content and take-back guarantees. Forbo’s facility in Assendelft operates a closed-loop recycling system, where post-consumer vinyl is reprocessed into new flooring, diverting 12000 metric tons from landfill in 2023 alone. The country’s housing shortage has accelerated construction of modular apartment blocks, where click LVT is preferred for rapid installation over concrete slabs. Amsterdam’s Circular Construction Program mandates that all municipal projects use materials with documented end-of-life pathways, a rule that favors certified vinyl systems.

COMPETITION OVERVIEW

Competition in the Europe vinyl flooring market is characterized by a triad of multinational sustainability leaders, regional specialists, and private label producers. Global players like Tarkett, Forbo, and Gerflor dominate public infrastructure and high specification commercial segments through certified eco products, technical compliance, and long-term take-back agreements. These firms benefit from integrated manufacturing R&D centers and deep relationships with government procurement bodies. Meanwhile, mid-sized European manufacturers compete on design customization, rapid lead times, and niche applications such as historical renovation or sports flooring. The market is highly regulated with EN standards for slip resistance wear class, fire behavior, and VOC emissions, creating significant barriers for non-compliant imports. Price competition is moderate in institutional segments but intense in residential DIY channels, where retailers like Leroy Merlin and IKEA exert strong influence. Innovation is increasingly focused on bio-based plasticizers, digital design tools, and circular business models.

KEY MARKET PLAYERS

A few major players of the Europe vinyl flooring market include

- Tarkett

- Forbo Flooring Systems

- Gerflor

- Interface

- IVC Group

- Polyflor

- Amtico

- BerryAlloc

- Balta Group

- Karndean Design flooring

Top Strategies Used by the Key Market Participants

Key players in the Europe vinyl flooring market prioritize sustainability through phthalate-free formulations, high recycled content, and certified take-back programs aligned with VinylPlus and EU Green Public Procurement criteria. They invest in rigid core and click technology to cater to DIY and rental markets seeking adhesive-free installation. Companies obtain environmental product declarations and EPDs to qualify for BREEAM, DGNB, and LEED certifications in public and commercial projects. Strategic partnerships with architects, contractors, and government agencies ensure specification in large-scale renovation programs. Additionally, firms develop antimicrobial and acoustically enhanced products to meet EN standards for healthcare education and urban housing sectors.

Leading Players in the Market

- Tarkett SA is a France-headquartered global leader in sustainable flooring and sports surfaces with a dominant presence across the Europe vinyl flooring market. The company offers a comprehensive portfolio of luxury vinyl tiles, vinyl sheets, and homogeneous flooring compliant with EU Ecolabel, Blue Angel, and Cradle to Cradle certifications. Tarkett operates seven manufacturing facilities in Europe, including its flagship plant in Germany, which produces phthalate-free LVT using 85% recycled content. In 2024, Tarkett expanded its take-back program to cover all 30 EU and EFTA countries, enabling commercial clients to return end-of-life flooring for recycling. It also launched a new rigid core LVT collection with bio-based plasticizers validated under EN 14041 for accessibility and EN ISO 717-2 for acoustic performance. These initiatives reinforce its position as a pioneer in circular and human-centered flooring solutions aligned with Europe’s green building mandates.

- Forbo Holding AG is a Switzerland-based multinational renowned for its Marmoleum linoleum and Allura vinyl flooring brands, with a strong foothold in the European public and healthcare sectors. The company’s Allura Flex and Allura LVT lines are specified in hospitals, schools, and transport hubs across the Netherlands, Germany, and the Nordics due to their antimicrobial properties and acoustic comfort. Forbo’s Assendelft facility in the Netherlands runs a closed-loop recycling system that reprocesses post-consumer vinyl into new products, achieving 95% material recovery. Forbo introduced a digital flooring configurator integrated with BIM libraries to support architects in specifying compliant solutions under BREEAM and DGNB frameworks. It also achieved certification under the EU Construction Products Regulation with full EPD documentation for its entire vinyl range. These actions demonstrate its commitment to transparency, sustainability, and design integration in regulated environments.

- Gerflor Group is a French manufacturer specializing in high-performance vinyl flooring for sports, healthcare, and education sectors with deep integration into Europe’s public procurement ecosystem. Its Creation and Mipolam collections are widely used in French hospitals, Belgian schools, and Swedish gyms due to compliance with ISO 22196 antimicrobial standards and DIN 51130 slip resistance requirements. Gerflor operates a vertically integrated production chain from calendering to printing in Nogent-sur-Oise, ensuring consistent quality and rapid customization. In 202,4 Gerflor launched a new generation of phthalate-free LVT with enhanced sound insulation properties tailored for urban multi-family housing under France’s “Logement d’Abord” housing initiative. It also partnered with the French Ministry of Education to develop flooring with integrated anti-fatigue and impact absorption zones for primary schools. These strategic moves position Gerflor as a mission-oriented supplier serving Europe’s social infrastructure with purpose-built resilient surfaces.

MARKET SEGMENTATION

This research report on the Europe vinyl flooring market has been segmented and sub-segmented based on type, end use, and region.

By Type

- Luxury Vinyl Tiles

- Vinyl Sheets

- Vinyl Tiles

By End Use

- Residential

- Commercial

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving the growth of the Europe vinyl flooring market?

Key drivers include rising construction and renovation activities, demand for cost-effective flooring, durability, ease of maintenance, and growing preference for luxury vinyl tiles (LVT).

2. Which countries dominate the Europe vinyl flooring market?

Major markets include Germany, the UK, France, Italy, Spain, and the Nordic countries due to strong construction activity and high renovation rates.

3. What are the main types of vinyl flooring available in Europe?

The market includes luxury vinyl tiles (LVT), vinyl sheets, vinyl composite tiles (VCT), and rigid core vinyl flooring.

4. Which application segment holds the largest share in Europe?

The residential segment holds a significant share, driven by home renovations, followed by commercial spaces such as offices, healthcare facilities, and retail stores.

5. What role does sustainability play in the Europe vinyl flooring market?

Sustainability is increasingly important, with manufacturers focusing on recyclable materials, low VOC emissions, and eco-friendly production processes.

6. How is the commercial sector influencing market growth?

Growth in commercial construction, especially in healthcare, education, and hospitality sectors, is boosting demand for durable and hygienic vinyl flooring solutions

7. What are the key trends in the Europe vinyl flooring market?

Major trends include rising adoption of LVT, digital printing for realistic designs, waterproof flooring solutions, and increased demand for rigid core vinyl.

8. How does vinyl flooring compare with other flooring materials?

Vinyl flooring is cost-effective, water-resistant, durable, and easier to install compared to hardwood, ceramic tiles, and laminate flooring.

9. What impact does urbanization have on the Europe vinyl flooring market?

Urbanization drives residential and commercial construction, increasing demand for affordable, stylish, and long-lasting flooring options like vinyl.

10. What challenges does the Europe vinyl flooring market face?

Challenges include environmental concerns related to PVC usage, price volatility of raw materials, and competition from alternative flooring materials.

11. What distribution channels are common in the Europe vinyl flooring market?

Common channels include specialty flooring stores, home improvement retailers, distributors, and online sales platforms.

12. What is the future outlook for the Europe vinyl flooring market?

The market is expected to grow steadily, supported by innovation in sustainable products, increasing renovation projects, and continued demand for LVT flooring.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com