Global Floriculture Market Size, Share, Growth, Trends, And Forecast Report, Segmented By Product Type (Cut Flowers, Foilage Plants, Potted Plants, Bedding Plants And Others), By Application (Personal Use, Cosmetics, Pharmaceuticals And Others) And By Region (North America, Europe, Asia Pacific, Latin America, Middle East And Africa), Industry Analysis From 2026 to 2034

Global Floriculture Market Size

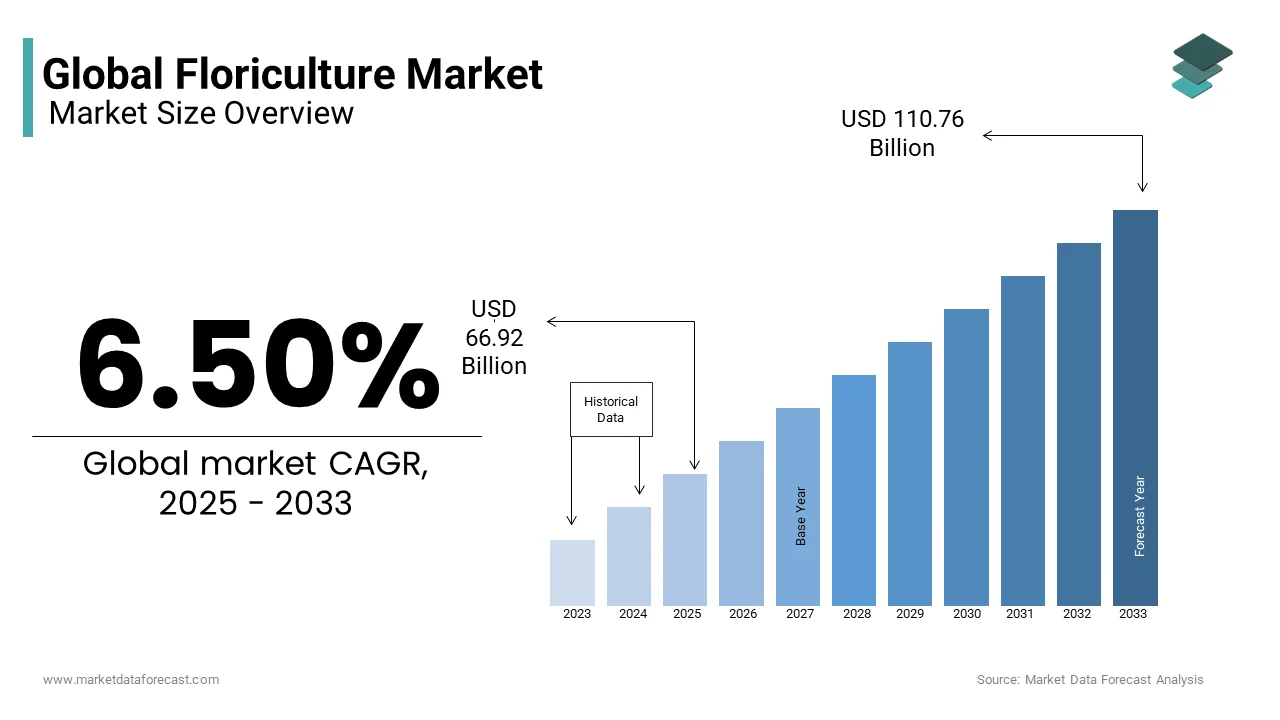

The global floriculture market was valued at USD 66.92 billion in 2025 and is anticipated to reach USD 71.27 billion in 2026 from USD 117.95 billion by 2034, growing at a CAGR of 6.50% from 2026 to 2034.

Floriculture is the cultivation of flowering and ornamental plants, including cut flowers, potted plants, bedding plants, foliage plants, and floral greens for aesthetic, decorative, and ceremonial purposes. The sector operates at the intersection of horticulture design and logistics, with value chains extending from greenhouse nurseries to retail florists and event planners. According to the International Society for Horticultural Science, over 35,000 species of ornamental plants are commercially cultivated worldwide, with breeding programs continuously introducing novel colors, forms, and vase life traits. As per the Food and Agriculture Organization of the United Nations, floriculture occupies more than 2 million hectares globally, with over sixty % grown under protected structures.

MARKET DRIVERS

Rising Global Urbanization and Green Space Integration Drive Ornamental Plant Demand

The urban expansion has intensified the human desire for biophilic environments, with flowering and foliage plants serving as accessible conduits to nature in dense built settings. This factor is boosting the growth of the Floriculture Market. According to the reports, 68% of the global population is projected to reside in urban areas by 2050. This shift has spurred municipal and private investment in vertical gardens, rooftop landscapes, and indoor greenery. The urban green space is growing, with new high-rise developments that must incorporate integrated planters or sky terraces often planted with ornamental species like orchids and anthuriums.

Cultural and Ceremonial Significance of Flowers Sustains Recurrent Consumption

The Flowers remain deeply embedded in human rituals across religions and life events, creating non-discretionary demand that transcends economic cycles, which is majorly propelling the growth of the Floriculture Market. In India, the Ministry of Culture estimates that a million tons of marigold, jasmine,ne, and lotus flowers are offered in temples each year, forming an income source for smallholder floriculturists. Similarly, in Jap, the annual Hanami cherry blossom viewing tradition drives seasonal demand for potted sakura and ikebana arrangements.

MARKET RESTRAINTS

High Post-Harvest Losses Due to Perishability Constrain Profitability

The floriculture products are exceptionally perishable, with physiological deterioration beginning immediately after harvesting due to ethylene sensitivity, water loss, and microbial blockage in stems. This factor is majorly limiting the growth of the floriculture market. According to Wageningen University, post-harvest losses in cut flowers globally occur within regions lacking cold chain infrastructure. In India, a study by the Indian Institute of Horticulture Research found that marigold and chrysanthemum losses reach 35% between farm and urban mandis due to the absence of pre-cooling and hydration protocols.

Stringent Phytosanitary and Chemical Residue Regulations Limit Market Access

The international trade in floriculture is heavily governed by phytosanitary protocols, and maximum residue limits are significantly hindering the growth of the floriculture market. According to the International Plant Protection Convention, few countries enforce strict import requirements for pests such as thrips, whitefly, ly and leaf miner, which are endemic in tropical production zones. The European Union’s Regulation EC 396/2005 sets maximum residue limits for pesticide active substances, with non-compliance resulting in immediate consignment rejection. Similarly, the United States Department of Agriculture mandates methyl bromide fumigation or cold treatment for all live plant imports, which increases costs and phytotoxicity risks. These regulatory hurdles disproportionately affect smallholder cooperatives lacking laboratory access or certification capacity, ty thereby concentrating export benefits among large vertically integrated farms with in-house compliance systems.

MARKET OPPORTUNITIES

Expansion of Therapeutic Horticulture and Biophilic Design Creates Institutional Demand

The integration of flowering plants into healthcare education and workplace environments is generating structured institutional procurement channels beyond retail and events, which is expected to bolster the growth of the floriculture market. According to the American Society of Interior Designers, most of the corporate offices renovated since 2020 incorporated permanent floral or foliage installations as part of wellness certifications like WELL Building Standard. In healthcare, the UK’s National Health Service has piloted “green care” wards where patients recovering from surgery are placed in rooms with daily fresh flower arrangements, resulting in a reduction in analgesic use as documented by King’s College London. Similarly, in Japan, over 200 two hundred hospitals participate in the Therapeutic Horticulture Network, which prescribes weekly potted plant interactions for elderly dementia patients.

Growth of EE-Commerceand Direct-to-Consumer Floral Platforms Enhances Market Reach

The digital transformation has reconfigured floriculture distribution by enabling real-time inventory visibility, personalized gift giving, ng afarm-to-consumermer delivery, bypassing traditional wholesale markups, which is an additional factor boosting the growth of the floriculture market. According to the International Floriculture Trade Association, online flower sales are growing annually, with platforms like Bloomon and UrbanStems achieving customer retention rates above 65% through subscription models. In China, over 40% of potted plant sales now occur via livestream commerce on platforms like Douyin, where growers demonstrate care techniques in real time. The Royal FloraHolland’s digital auction system processes daily with AI-driven quality grading and logistics coordination. Moreover, blockchain pilots in Colombia allow consumers to trace a rose from greenhouse to vase, verifying water use and labor conditions. This digitization not only expands market access for niche growers but also builds transparency and emotional connection that premiumize floral purchases in an increasingly experience-driven economy.

MARKET CHALLENGES

Climate Change Induces Production Volatility in Key Export Regions

The floriculture is highly sensitive to microclimatic shifts, with even minor deviin temperatureraturee h o humidity disrupting flowering cycles and quality parameters, which is a primary factor to challenge the growth of the floriculture market. In the Netherlands, the Royal Netherlands Meteorological Institute recorded a 20% increase in summer heatwaves between 2015 and 2024, forcing growers to invest in energy-intensive cooling systems that raise production costs by up to 18%. In Colombia, prolonged droughts in the Bogotá savanna reduced water availability for irrigation, with the National Federation of Flower Growers reporting a fifteen % drop in carnation yields in 2023.

Labor Intensity and Workforce Shortages Threaten Production Scalability

The most labor-dependent agricultural sectors require skilled hands for planting, pruning, ng harvest, and harvesting. According to the International Labour Organization, a single hectare of greenhouse roses employs significantly more people than mechanized field crops. In the European Union, the European Commission’s Farm to Fork Strategy records a decline in agricultural labor availability since 2010, with younger generations avoiding floriculture due to repetitive tasks and seasonal contracts. In the United States, the Department of Agriculture's H-2A visa processing delays caused a 15% reduction in harvest capacity for California’s cut flower farms in 2023. While robotics for harvesting roses or orchids is in development, none have achieved commercial reliability due to flower fragility and morphological diversity.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.5% |

| Segments Covered | By Product Type, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Syngenta Flowers, Karuturi, Rosebud, Beekenkamp, Queens Group, Dutch Flower Group, Washington Bulb, Finlays, Selecta One, Dümmen Orange, and Others. |

SEGMENTAL ANALYSIS

By Product Insights

The cut flowers segment accounted hfor3% of the global floriculture market share in 2024 due to their universal role in gifting ceremonies, religious rituals, and event decoration across cultures, coupled with well-established global cold chain logistics that enable intercontinental trade. Cut flowers remain the primary medium for emotional expression in personal and social milestones, with roses, carnations, nd lilies forming the backbone of global floral gifting. In India, the Ministry of Culture estimates that temples consume huge tons omarigoldsld and jasmine annually for daily rituals, creating year-round demand. The wedding industry further amplifies consumption, with the United States Department of Commerce reporting that the average American wedding spends more than 5000 dollars on floral arrangements. Additionally, the rise of experiential events such as music festivals, corporate galas, and luxury retail activations has institutionalized cut flower use beyond traditional occasions.

The potted plants segment is projected to grow with a significant CAGR of 8.6% throughout the forecast period. The integration of urban densification, wellness awareness, and social media aesthetics has transformed potted plants into essential elements of modern interior design. According to the United Nations Human Settlements Programme, new residential developments in cities like Seo, ul, Tokyo, and Berlin now incorporate mandatory green space quotas often fulfilled through potted ornamentals. In the United States, 72% of millennials own at least three houseplants, with snake plant, poth, os, and peace lilies favored for their air purifying properties validated by NASA’s Clean Air Study. Furthermore, e-commerce platforms like Patch and The Sill offer subscription services with care reminders and stylist consultations, making plant ownership accessible to novice urbanites.

By Application Insights

The personal use segment was the largest and held a significant share of the global floriculture market in 2024. Flowers serve as non-verbal carriers of human emotion and spiritual devotion in ways few other commodities can replicate. According to the Vatican’s Office for Liturgical Celebrations, white lilies and roses are used annually in Catholic masses and processions worldwide. In Japan, the custom of “hanakotoba” or flower language assigns specific meanings to blooms, with chrysanthemums symbolizing longevity and cherry blossoms impermanence, guiding personal gifting choices.

The pharmaceutical segment is likely to register a CAGR of 9.3% throughout the forecast period. Flowers are increasingly recognized as reservoirs of pharmacologically active molecules with documented therapeutic effects. According to the European Medicines Agency, over 30 approved herbal medicines contain active ingredients derived from flowers, including calendula for wound healing and chamomile for gastrointestinal inflammation. In India, the Ministry of AYUSH reports that traditional formulations in Ayurveda rely on floral extracts such as brahmi flower and jasminum for cognitive and dermatological benefits. Similarly, the cytotoxic compounds in Catharanthus roseus that form the basis of vincristine and vinblastine are used in leukemia and Hodgkin’s lymphoma treatment.

REGIONAL ANALYSIS

Europe Floriculture Market Analysis

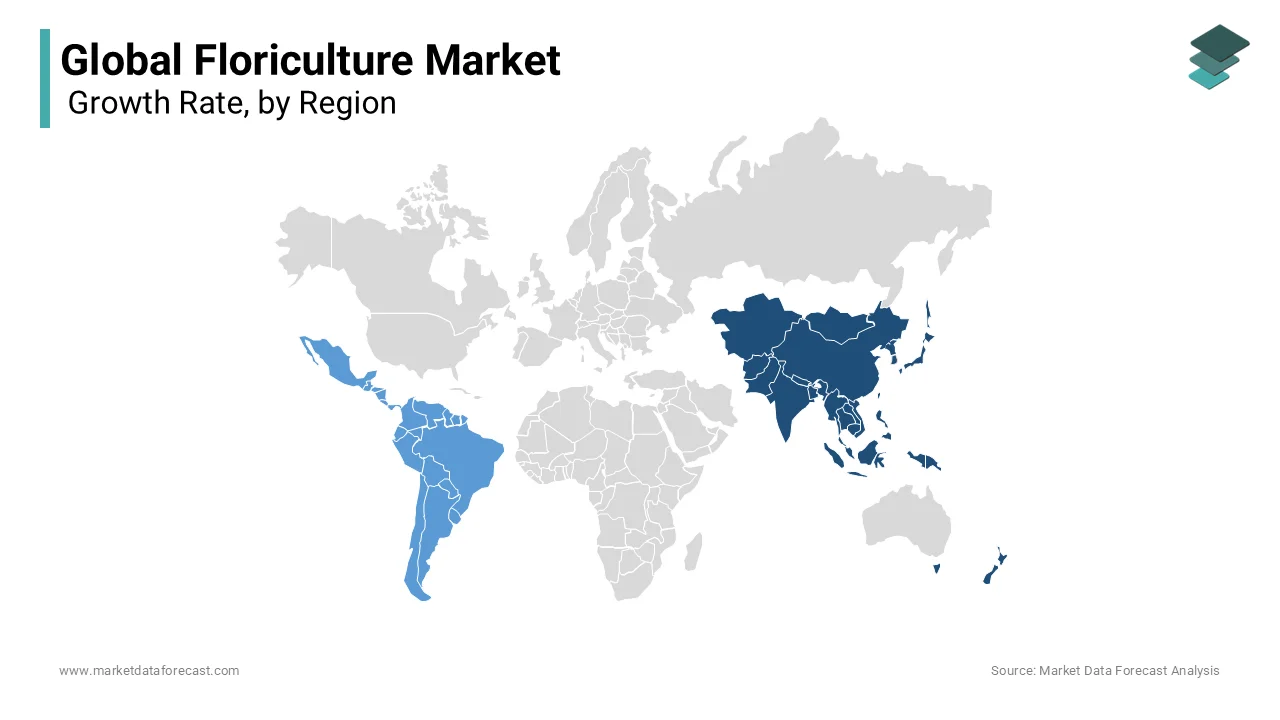

Europe was the largest contributor to the global floriculture market by holding 32.1% of the share in 2024, with its mature consumer base based on strong cultural traditions and advanced production infrastructure. Germany and France are the top consumers of potted plants, with per capita spending exceeding 45 euros yearly. The European Union’s Green Cities initiative mandates floral biodiversity in urban planning, driving municipal procurement of bedding plants. Additionally, the region’s cold chain and phytosanitary compliance systems set global standards, enabling seamless intra-European distribution.

Asia Pacific Floriculture Market Analysis

Asia Pacific floriculture market was positioned second by capturing 28.3% of the share in 2024, with the religious practices rapid urbanization and a burgeoning middle class. China and India are the major contributors to the growth of the market. Japan’s ikebana tradition sustains demand for premium chrysanthemums and camellias while South Korea’s K-beauty industry sources floral extracts for cosmetics. Urban greening policies in Singapore and Thailand further boost bedding plant use in public spaces.

North America Floriculture Market Analysis

North America floriculture market is expected to grow with a prominent growth opportunity throughout the forecast period, with a robust direct-to-consumer e-commerce landscape. California and Florida lead domestic production of potted and bedding plants, supplying national retail chains. Subscription services and same-day delivery platforms have further democratized access, transforming floriculture from an occasional to a habitual purchase. This commercial sophistication and consumer engagement ensure NoAmericarica remains a highly valued,n innovation-led market.

Latin America Floriculture Market Analysis

Latin AAmerica'sfloriculture market growth is anticipated to have significant growth opportunities in the coming years, with a production and export hub rather than a consumption center. Ecuador’s rose farms near Quito leverage equatorial sunlight and volcanic soil to produce extra-long roses prized in luxury markets.

Middle East and Africa Floriculture Market Analysis

The Middle East and Africa floriculture market exhibits high strategic relevance due to religious demand and urban landscaping investments. In Saudi Arabia and the United Arab Emirates, municipal spending on floral displays for events like National Day and Expo exceeds eight hundred million US dollars annually. Kenya is Africa’s largest flower exporter, with roses generating 2 billion US dollars in foreign exchange yearly. Egypt’s Nile Delta supports jasmine and lotus cultivation for both local religious use and essential oil extraction.

COMPETITIVE LANDSCAPE

The floriculture market features a dual competitive structure comprising large-scale export-oriented producers in East Africa, Latin America, and the Netherlands, alongside regional growers and local florists serving domestic demand. Competition among global players centers on vase life consistency, logistics reliability, and sustainability credentials rather than price alone. Dutch cooperatives dominate the auction and distribution, while Colombian and Kenyan farms compete on cost and climatic advantages. In developed markets, boutique growers differentiate through heirloom varieties, organic certification, and storytelling. Simultaneously, stringent phytosanitary regulations and carbon border measures are reshaping competitive dynamics by favoring producers with traceable and low-emission operations. Innovation in post-harvest technologypackaginggg, and plant breeding remains critical to maintaining a competitive edge in this highly perishable and emotionally driven market.

KEY MARKET PLAYERS

A few of the market players in the global floriculture market include

- Syngenta Flowers

- Karuturi

- Oserian Development Company Limited

- Dole Food Company Inc

- Royal FloraHolland

- Rosebud

- Beekenkamp

- Queens Group

- Dutch Flower Group

- Washington Bulb

- Finlays

- Selecta One

- Dümmen Orange

Top Players In The Market

- Royal FloraHolland is the world’s largest floricultural auction and logistics cooperative, facilitating the trade of over twelve billion flowers and plants annually from more than five thousand growers. Headquartered in the Netherlands, it operates advanced cold chain infrastructure, digital auction platforms, and global distribution networks that connect European production with markets across Asia, North America, and the Middle East. Recently, Royal FloraHolland enhanced its sustainability verification system by integrating blockchain technology to track water use, pesticide application, and carbon footprint per batch.

- Dole Food Company Inc. has established a significant presence in the global floriculture market through its Dole Fresh Flowers division, which cultivates and exports premium roses, carnations, and tropical blooms from farms in Colombia and Ecuador. The company leverages its decades of perishable logistics expertise to ensure rapid transit and extended vase life for its floral products. In recent developments, Dole launcheaaa carbon-neutral flower certification program aligned with the Science Based Targets initiative protocols covering energy use, packaging, and transport emissions. It also introduced a line of pesticide-free ornamental bouquets targeting eco-conscious retailers in North America and Europe. These actions underscore Dole’s strategy of applying its global agribusiness discipline to elevate quality, sustainability, and traceability in the floral sector.

- Oserian Development Company Limited is a leading Kenyan floriculture producer renowned for its Lake Naivasha-based rose farms that supply high-quality long-stem varieties to European and Middle Eastern markets. The company integrates sustainable practices, including geothermal energy use, biological pest control, and wastewater recycling, to minimize environmental impact. Recently, Oserian inaugurated a new tissue culture laboratory to propagate disease-resistant and novel rose cultivars in partnership with European breeders.

Top Strategies Used by the Key Market Participants

Key players in the floriculture market prioritize vertical integration from breeding to retail to ensure quality control and reduce post-harvest losses. They invest in cold chain infrastructure and digital auction or e-commerce platforms to enhance supply chain transparency and speed. Sustainability certifications such as MPS and Fair Trade are leveraged to meet retailer and consumer demands for ethical production. Companies also focus on developing novel cultivars with extended vase life, disease resistance, and unique colors through tissue culture and hybridization. Strategic partnwithiairlinesisti airlinesviders aninte expansion into non-traditional channels such as hospitality, wellness, and corporate spaces.

MARKET SEGMENTATION

This research report on the global floriculture market is segmented and sub-segmented into the following categories:

By Product Type

- Cut Flowers

- Foilage Plants

- Potted Plants

- Bedding Plants

- Others

By Application

- Personal Use

- Cosmetics

- Pharmaceuticals

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is driving growth in the Global Floriculture Market?

The Global Floriculture Market is expanding due to rising urban gardening, wellness-driven demand for indoor plants, event-driven flower consumption (weddings, festivals), and e-commerce-enabled gifting across Asia and North America.

How is climate change affecting the Global Floriculture Market?

Extreme weather disrupts traditional growing regions (e.g., Kenya’s roses, Colombia’s carnations), pushing producers toward protected cultivation, resilient varieties, and vertical farming—reshaping supply chains in the Global Floriculture Market.

Which regions dominate production and export in the Global Floriculture Market?

The Netherlands leads in logistics and auction volume (via Royal FloraHolland), while Colombia, Ecuador, Kenya, and Ethiopia dominate cut-flower exports. Meanwhile, India and China are fast-growing domestic markets in the Global Floriculture Market.

Are sustainable certifications becoming essential in the Global Floriculture Market?

Yes—certifications like MPS, Fair Trade, and Rainforest Alliance are now prerequisites for European and North American retailers, pushing growers to adopt water recycling, biocontrol, and ethical labor practices in the Global Floriculture Market.

How is e-commerce transforming flower sales globally?

Direct-to-consumer platforms (e.g., Bloom & Wild, UrbanStems) and marketplace integrations (Amazon Fresh, Flipkart Flowers) are shortening supply chains, reducing waste, and enabling personalized gifting in the Global Floriculture Market.

What role does ornamental foliage play in the Global Floriculture Market?

Beyond cut flowers, demand for indoor foliage (e.g., monstera, snake plants, ZZ plants) is surging—driven by biophilic design in offices and homes, making foliage a high-margin segment in the Global Floriculture Market.

Are lab-grown or preserved flowers gaining commercial traction?

Preserved (stabilized) flowers are growing in luxury decor and long-life arrangements, while lab-grown floral tissue remains experimental—meaning the Global Floriculture Market still relies on traditional cultivation.

How do logistics impact flower quality and pricing?

Flowers are highly perishable; cold chain integrity from farm to vase is critical. Air freight costs and border delays (e.g., post-Brexit, U.S. customs) directly affect freshness and margin in the Global Floriculture Market.

Is there innovation in breeding and genetics?

Yes—CRISPR and marker-assisted selection are creating disease-resistant, longer-vase-life, and novel-color varieties (e.g., blue roses, black callas), differentiating premium offerings in the Global Floriculture Market.

What’s the outlook for the Global Floriculture Market through 2030?

Steady growth (CAGR ~5–6%) is expected, fueled by emotional wellness trends, urban greening policies, and digital retail—though the market remains vulnerable to energy costs, water scarcity, and geopolitical trade shifts in the Global Floriculture Market.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com