Global Fluid Additives Market Size, Share, Trends & Growth Forecast Report – Segmented By Type (Synthetically Modified Natural Additives, Synthetic Additives, Natural Additives), Application, Region (North America, Europe, Asia Pacific, Latin America, And Middle East & Africa) - Industry Analysis (2025 to 2033)

Global Fluid Additives Market Size

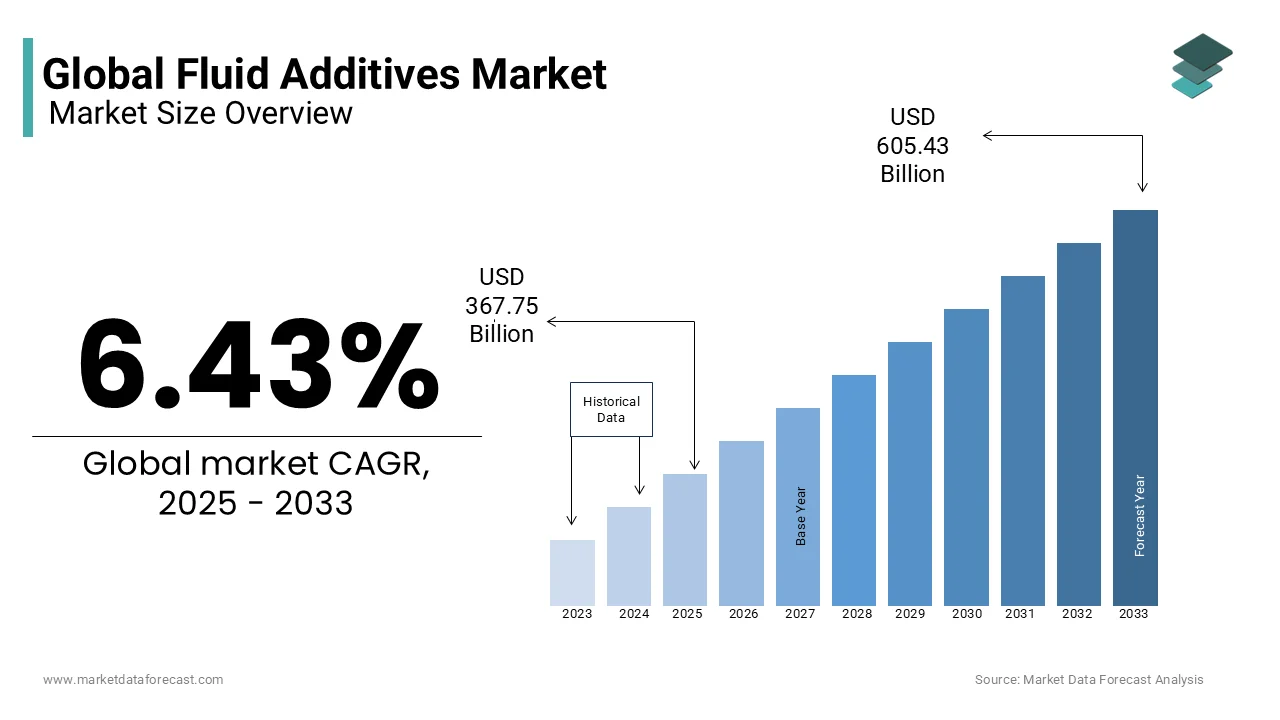

The global fluid additives market size was valued at USD 345.53 million in 2024 and is expected to reach USD 605.43 million by 2033 from USD 367.75 million in 2025. The market is projected to grow at a CAGR of 6.43%.

Fluid additives are chemical substances blended into base fluids to enhance their performance, stability, and longevity across a wide range of industrial applications. These additives are extensively used in lubricants, fuels, metalworking fluids, hydraulic oils, and process fluids to improve viscosity, reduce friction, prevent corrosion, and optimize combustion efficiency. The Fluid Additives Market covers products such as anti-wear agents, dispersants, detergents, antioxidants, pour point depressants, and viscosity modifiers.

The market plays a critical role in sectors including automotive, energy, manufacturing, aerospace, and marine, where fluid efficiency directly impacts equipment performance and operational costs. As industries strive for greater energy efficiency and longer equipment life cycles, demand for high-performance fluid additives has surged globally. According to the International Energy Agency (IEA), industrial energy consumption accounts for nearly 37% of global final energy use, making additive-enhanced fluids essential for reducing wear and improving fuel economy.

In addition, regulatory agencies such as the European Chemicals Agency (ECHA) and the U.S. Environmental Protection Agency (EPA) have been instrumental in shaping formulation standards, pushing manufacturers toward environmentally compatible additives that minimize toxicity and emissions.

MARKET DRIVERS

MARKET DRIVERS

Rising Demand from the Automotive Industry

One of the primary drivers of the Fluid Additives Market is the growing demand from the automotive industry, particularly for engine oils, transmission fluids, and fuel additives that enhance performance and prolong vehicle lifespan. As automakers continue to develop more efficient engines with tighter tolerances, the need for high-performance fluid additives to manage heat, reduce wear, and maintain cleanliness has become increasingly crucial.

According to the International Organization of Motor Vehicle Manufacturers (OICA) , global vehicle production reached over 85 million units in 2024 , with a significant portion comprising advanced internal combustion engines and hybrid vehicles that rely on specialized lubricants and fuel treatments. Fluid additives such as dispersants and detergents play a vital role in preventing sludge formation and maintaining optimal engine function under extreme operating conditions.

Also, governments worldwide are implementing stringent emission norms, compelling automakers and oil formulators to adopt low SAPS (sulfated ash, phosphorus, sulfur) additives that are compatible with after-treatment systems like diesel particulate filters and catalytic converters. As per the U.S. Department of Energy , the adoption of high-performance additives in motor oils can lead to a key improvement in fuel efficiency , reinforcing their importance in achieving sustainability targets and enhancing overall engine performance.

Expansion of Renewable and Alternative Fuels

Another major driver influencing the Fluid Additives Market is the rapid expansion of renewable and alternative fuels, which require specialized additives to ensure compatibility, stability, and optimal combustion characteristics. With increasing pressure to reduce carbon emissions and dependence on fossil fuels, biofuels such as biodiesel and ethanol blends are gaining traction across transportation sectors.

As per the Renewable Fuels Association , the United States alone produced over 17 billion gallons of ethanol in 2024 , while biodiesel output exceeded 1.8 billion gallons , necessitating the use of additives that mitigate oxidative degradation, water contamination, and microbial growth. Fluid additives such as antioxidants, corrosion inhibitors, and cold flow improvers are essential for maintaining fuel integrity and engine performance in biofuel blends.

Moreover, the aviation and maritime sectors are exploring synthetic and drop-in biofuels that require tailored additive packages to meet performance and safety standards. According to the International Air Transport Association (IATA) , sustainable aviation fuel (SAF) usage increased significantly between 2022 and 2024 , driving demand for high-purity additives that ensure seamless integration into existing fuel infrastructure without compromising engine reliability or emissions compliance.

MARKET RESTRAINTS

Stringent Environmental Regulations and Chemical Compliance Standards

A key restraint affecting the Fluid Additives Market is the imposition of stringent environmental regulations and chemical compliance standards that limit the use of certain additive chemistries. Regulatory bodies such as the European Chemicals Agency (ECHA) and the U.S. Environmental Protection Agency (EPA) have introduced restrictions on hazardous substances commonly found in older additive formulations, including heavy metals, polyaromatic hydrocarbons, and certain phosphorus-based compounds.

Like, several legacy additives containing zinc dialkyl dithiophosphates (ZDDPs), once widely used for anti-wear protection, are now being phased out due to their adverse impact on catalytic converters and aquatic life. This shift has forced additive manufacturers to reformulate products using safer alternatives, often at higher development and production costs.

In addition, the REACH Regulation in the European Union mandates extensive testing and registration of chemical substances, significantly increasing the time and investment required to bring new additives to market. While these regulations promote environmental safety, they also pose challenges in terms of product innovation, cost management, and market access for traditional additive chemistries.

Volatility in Raw Material Prices and Supply Chain Disruptions

Another major constraint impacting the Fluid Additives Market is the volatility in raw material prices and supply chain disruptions that affect production timelines and cost structures. Many fluid additives are derived from petrochemical feedstocks such as olefins, benzene derivatives, and fatty acids, all of which are subject to fluctuating crude oil prices and geopolitical instability.

According to the U.S. Energy Information Administration (EIA) , crude oil prices experienced a year-over-year variation of more than 20% in 2024, driven by geopolitical tensions and shifts in OPEC+ production strategies. This volatility directly influences the cost of base chemicals used in additive synthesis, including ethylene, propylene, and long-chain alcohols, thereby squeezing profit margins for manufacturers.

Furthermore, global logistics bottlenecks, including port congestion, container shortages, and rising freight costs, have disrupted the timely availability of key ingredients. Until more stable sourcing channels and pricing mechanisms are established, the Fluid Additives Market will remain vulnerable to external economic shocks, limiting its ability to scale efficiently in response to growing industrial demand.

MARKET OPPORTUNITIES

Growth in Electric Vehicles and Hybrid Systems

One of the most promising opportunities for the Fluid Additives Market lies in the rapid growth of electric vehicles (EVs) and hybrid powertrains, which require specialized thermal management fluids and dielectric coolants to ensure optimal battery and motor performance. While EVs eliminate the need for traditional engine oils, they introduce new fluid requirements for battery cooling, gearboxes, and power electronics, all of which depend on high-performance additives to maintain efficiency and longevity.

According to the International Energy Agency (IEA) , global electric car sales surpassed 14 million units in 2024 , representing an annual growth rate of over 25%, indicating a fundamental shift in automotive design and fluid needs. Unlike conventional vehicles, EVs rely on coolant formulations that must balance electrical insulation with high thermal conductivity, necessitating the inclusion of unique additive packages to prevent corrosion, oxidation, and system degradation.

In addition, companies such as BASF, Lubrizol, and Evonik have begun developing proprietary additive blends specifically designed for EV transmission fluids and battery cooling systems. With continued advancements in electrified mobility, the Fluid Additives Market is poised to expand beyond traditional lubricant applications into novel domains that support next-generation transportation technologies.

Adoption of Biodegradable and Eco-Friendly Additives

Another emerging opportunity for the Fluid Additives Market is the growing adoption of biodegradable and eco-friendly additives designed to reduce environmental impact and comply with evolving sustainability mandates. As industries face mounting pressure to transition toward greener operations, there is increasing demand for additives derived from renewable sources such as plant-based esters, bio-lubricants, and enzymatic modifiers that offer performance comparable to conventional chemistries while minimizing ecological harm.

According to the European Environment Agency (EEA), industrial lubricants and process fluids contribute to significant levels of soil and water contamination , prompting regulators and end-users to seek biodegradable alternatives that break down safely in natural environments. In response, additive manufacturers are investing heavily in research and development to create ester-based dispersants, non-toxic corrosion inhibitors, and green friction modifiers that align with circular economy principles.

Also, certification programs such as the U.S. EPA’s Safer Choice initiative and the EU Ecolabel scheme have encouraged companies to reformulate their products using environmentally preferred ingredients. This shift not only supports corporate sustainability goals but also opens new revenue streams for additive producers willing to invest in green chemistry innovations.

MARKET CHALLENGES

Complexity in Formulating Multi-Functional Additive Packages

A major challenge confronting the Fluid Additives Market is the complexity involved in formulating multi-functional additive packages that deliver consistent performance across diverse operating conditions. Modern industrial and automotive applications demand additives that simultaneously address multiple performance criteria—such as anti-wear protection, oxidation resistance, detergency, and viscosity control—without compromising stability or compatibility with other components.

According to the Society of Tribologists and Lubrication Engineers (STLE), additive interactions can lead to unexpected side effects, including deposit formation, additive depletion, or reduced effectiveness when combined in complex blends. As per technical studies published by Shell and ExxonMobil, even minor imbalances in additive composition can result in reduced engine efficiency or accelerated component wear , highlighting the need for precise formulation science.

Moreover, the trend toward lower viscosity motor oils and extended drain intervals places additional stress on additive systems, requiring enhanced durability and thermal resilience. As per the Chevron Oronite Technical Center , modern low-viscosity engine oils must contain at least six different additive types to maintain protection and cleanliness under high-temperature, high-shear conditions.

Increasing Competition from Synthetic and Customized Lubricant Solutions

Another critical challenge for the Fluid Additives Market is the increasing competition from synthetic and fully customized lubricant solutions that integrate performance-enhancing properties at the base fluid level, potentially reducing reliance on traditional additive packages. As technology advances, formulators are developing tailor-made synthetic oils and ester-based fluids that inherently possess desirable characteristics such as high thermal stability, low volatility, and excellent low-temperature performance.

Also, the use of Group III, IV, and V base oils has grown significantly in recent years, allowing manufacturers to achieve desired performance metrics with fewer additive components. For instance, some synthetic ester-based fluids exhibit intrinsic dispersancy and corrosion resistance, diminishing the need for separate additive treatments.

Additionally, companies like TotalEnergies, BP Castrol, and Fuchs Petrolub have launched pre-blended synthetic lubricants optimized for specific applications, reducing the necessity for aftermarket additive supplementation. As per Kline & Company , the share of fully formulated synthetic lubricants in the industrial and automotive segments rose by over 15% in 2024 , signaling a shift away from traditional additive-dependent formulations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6.43% |

| Segments Covered | By Type, Application, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Halliburton (US), Schlumberger Limited (US), Newpark Resources Inc. (US), Solvay (Belgium), BASF SE (Germany), Clariant (Switzerland), Global Drilling Fluid and Chemicals Limited (India), Tytan Organics (India), Nouryon (US), Kemira OYJ, Schlumberger Limited Chevron Phillips, DoW Chemical, Innospec Inc., and others. |

SEGMENTAL ANALYSIS

By Type Insights

The synthetic additives segment had the biggest share of a 58.6% in the global Fluid Additives Market in 2024, driven by their superior performance characteristics and widespread use across industrial, automotive, and energy sectors. These additives are chemically engineered to provide enhanced thermal stability, oxidation resistance, and compatibility with modern fuel and lubricant formulations.

One key factor behind this dominance is the increasing demand for high-performance lubricants in advanced engine technologies.

Additionally, the aerospace and marine industries rely heavily on synthetic additives such as anti-wear agents and viscosity modifiers to ensure equipment reliability under extreme conditions. As per the International Council on Combustion Engines (CIMAC) , synthetic-based hydraulic fluids and gear oils have become standard in high-load applications due to their ability to maintain performance consistency at elevated temperatures and pressures.

The synthetically modified natural additives segment is projected to grow at the fastest CAGR of 8.6% during the forecast period, fueled by rising environmental awareness and stricter regulations promoting biodegradable and renewable chemical alternatives. These additives combine the benefits of naturally derived compounds with synthetic enhancements to improve functionality while maintaining eco-compatibility.

A major growth driver is the increasing adoption of bio-based lubricants and green process fluids in industrial and agricultural machinery. According to the European Environment Agency (EEA) , the use of environmentally acceptable lubricants increased significantly in 2024 , particularly in sensitive ecosystems where mineral oil-based products pose contamination risks.

Moreover, companies like BASF and Evonik have been investing in R&D to develop ester-modified natural additives that offer improved oxidative stability and load-carrying capacity without compromising sustainability credentials. With continued innovation and expanding regulatory support, this segment is well-positioned to outpace traditional additive categories in the coming years.

By Application Insights

The drilling fluid application segment accounted for approximately 64% of the Fluid Additives Market in 2024, driven by its critical role in oil and gas exploration, geothermal drilling, and deep-sea mining operations. These fluids are commonly referred to as muds which are essential for cooling drill bits, stabilizing boreholes, and carrying rock cuttings to the surface, necessitating the use of specialized additives to enhance performance and safety.

One of the leading drivers behind this segment’s dominance is the continuous expansion of offshore and unconventional hydrocarbon extraction activities. According to the U.S. Energy Information Administration (EIA) , global crude oil production reached over 100 million barrels per day in 2024 , with a significant portion sourced from deepwater and shale formations requiring advanced drilling fluid systems.

In addition, additives such as viscosifiers, emulsifiers, and filtration control agents play a crucial role in optimizing drilling efficiency and minimizing environmental impact. With sustained investment in upstream energy projects and evolving regulatory demands for reduced ecological footprint, the drilling fluid segment remains a cornerstone of the Fluid Additives Market.

The cement slurry application segment is anticipated to exhibit the highest CAGR of 9.3% in the Fluid Additives Market, driven by growing infrastructure development, oil well cementing requirements, and construction industry demand for high-performance grouting materials. Also, these slurries are widely used in oil and gas wells, tunneling, foundation works, and structural reinforcement, where additives enhance flowability, setting time, and compressive strength.

A key growth factor is the increasing need for durable well completion and zonal isolation in oil and gas wells. Furthermore, urbanization trends and government-led infrastructure investments in Asia-Pacific and Africa are boosting cement additive consumption. As per the Global Construction Outlook Report , global cement production grew in 2024 , directly influencing demand for fluid additives that improve workability and reduce water content without compromising strength.

REGIONAL ANALYSIS

North America Market Analysis

North America commanded the global Fluid Additives Market, accounting for 28.1% of total market revenue in 2024, driven by a robust industrial base, mature automotive sector, and extensive oil and gas operations. The United States plays a dominant role due to its large-scale manufacturing facilities and stringent environmental regulations that drive demand for high-performance additives.

Moreover, the Environmental Protection Agency (EPA) has mandated the use of low-emission lubricants and fuels, pushing additive manufacturers toward cleaner, longer-lasting formulations.

In Canada, the oil sands industry represents a major consumer of drilling fluid additives, with Alberta being a focal point for heavy oil extraction. As per the Canadian Association of Petroleum Producers (CAPP) , oil sands production exceeded 3.5 million barrels per day in 2024 , reinforcing the region's reliance on specialized fluid additives for operational efficiency and environmental compliance.

Europe Market Analysis

Europe is distinguished by its emphasis on regulatory leadership and sustainability-driven product development. Countries such as Germany, France, and the Netherlands have established rigorous chemical compliance frameworks, including the REACH Regulation and EU Ecolabel certifications, which influence additive formulation strategies across the continent.

As per the European Chemicals Agency (ECHA) , over 60% of industrial fluid additive producers operating in Europe have reformulated their products to meet stricter toxicity and biodegradability standards, aligning with the European Green Deal’s goals for a circular economy. This shift has spurred innovation in bio-based and low-hazard additives, particularly in the automotive and manufacturing sectors.

Moreover, Germany remains a key hub for additive research, hosting several technical centers operated by Lubrizol, BASF, and Evonik that focus on next-generation lubricant and coolant formulations. With continued regulatory momentum and investment in green chemistry, Europe is positioned to remain a leader in sustainable fluid additive innovation.

Asia Pacific Market Analysis

Asia-Pacific captures a significant share of the global Fluid Additives Market, driven by rapid industrialization, expanding automotive manufacturing, and increasing energy production. China, India, and Japan represent the core markets, with growing demand stemming from metalworking fluids, engine oils, and process lubricants used across diverse manufacturing sectors.

According to the International Organization of Motor Vehicle Manufacturers (OICA), Asia-Pacific countries collectively produced over 45 million vehicles in 2024 , reinforcing the region's position as a global automotive powerhouse. This surge in production has significantly boosted demand for high-performance lubricants and fuel additives that enhance efficiency and comply with tightening emissions norms.

China has seen a rise in domestic additive production, supported by state-backed initiatives aimed at reducing dependence on imported formulations. Besides, India has also witnessed strong growth, particularly in the railway and power generation sectors, where fluid additives are increasingly used to extend maintenance intervals and reduce downtime.

Middle East and Africa Market Analysis

The Middle East and Africa is another key player in the global Fluid Additives Market, primarily driven by the region’s vast oil and gas reserves and ongoing infrastructure development. Countries such as Saudi Arabia, UAE, and Nigeria are major consumers, with drilling fluid additives playing a central role in upstream operations.

In Saudi Arabia, Aramco and other national oil companies have invested in advanced fluid treatment technologies to optimize recovery rates and minimize environmental impact.

In Africa, the discovery of new offshore reserves in Mozambique, Ghana, and Namibia has led to increased exploration activity, further boosting additive consumption. With continued investment in energy infrastructure and regional industrialization, the Middle East and Africa are poised for steady growth in fluid additive demand.

Latin America Market Analysis

Latin America is seeing steady growth in the global Fluid Additives Market, with Brazil and Mexico serving as primary growth engines. The region’s market expansion is largely attributed to increasing oil and gas production, along with rising industrial activity in the automotive and manufacturing sectors.

Petrobras, the national oil company, has implemented advanced fluid management protocols that rely heavily on customized additive packages to enhance operational efficiency.

Mexico, on the other hand, has seen a resurgence in automotive manufacturing, with companies like BMW, Ford, and Stellantis expanding their production capacities. With ongoing investments in energy and manufacturing, Latin America is emerging as a key contributor to the global Fluid Additives Market, offering substantial growth potential for additive suppliers seeking regional expansion opportunities.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the key players in the global fluid additives market are

-

Halliburton (US)

-

Schlumberger Limited (US)

-

Newpark Resources Inc. (US)

-

Solvay (Belgium)

-

BASF SE (Germany)

-

Clariant (Switzerland)

-

Global Drilling Fluid and Chemicals Limited (India)

-

Tytan Organics (India)

-

Nouryon (US)

-

Kemira OYJ

-

Schlumberger Limited

-

Chevron Phillips

-

Dow Chemical

-

Innospec Inc.

-

Tetra Technologies

TOP STRATEGIES USED BY KEY MARKET PLAYERS

One major strategy employed by leading players in the Fluid Additives Market is continuous innovation through advanced R&D initiatives. Companies are investing heavily in developing next-generation additive chemistries that offer superior performance while complying with stringent environmental regulations. These efforts include creating low SAPS (sulfated ash, phosphorus, sulfur) formulations, bio-based additives, and multi-functional packages that enhance fluid efficiency across diverse applications.

Another key approach is strategic partnerships and joint ventures with oil refiners, automotive manufacturers, and technology providers . By collaborating closely with end-users and industry stakeholders, additive suppliers ensure their products meet evolving performance demands and regulatory standards. These alliances also facilitate co-development of customized solutions tailored to specific machinery and operational conditions, strengthening market relevance and customer loyalty.

Lastly, expansion into emerging markets through localized production and distribution networks is a crucial growth strategy. As demand for high-performance fluids rises in Asia-Pacific, Latin America, and Africa, companies are establishing regional footholds to better serve local industries, reduce supply chain bottlenecks, and capture new business opportunities in fast-growing economies.

COMPETITION OVERVIEW

The competition in the Fluid Additives Market is highly dynamic, characterized by the presence of established multinational corporations, specialized chemical firms, and emerging regional players. The market landscape is dominated by a few large-scale producers such as BASF, Lubrizol, and Evonik, which leverage their technological expertise, global reach, and strong R&D capabilities to maintain a competitive edge. However, niche players are increasingly gaining traction by focusing on eco-friendly additives, custom-formulated blends, and application-specific performance enhancements.

Competitive differentiation largely hinges on formulation expertise, regulatory compliance, and the ability to anticipate industry trends such as electrification, renewable fuels, and sustainable manufacturing. Companies are under constant pressure to innovate and adapt to stricter environmental norms while maintaining cost-effectiveness and scalability. Additionally, the growing emphasis on digitalization in additive development—such as AI-driven formulation modeling and predictive analytics—is reshaping how companies design and deploy new products.

With rising demand from automotive, energy, and industrial sectors, the Fluid Additives Market remains an intensely contested space where agility, technical proficiency, and strategic foresight determine long-term success. As market needs evolve, firms must continuously refine their offerings to remain relevant and capture emerging opportunities across global value chains.

TOP MARKET PLAYERS

- BASF is a global leader in the development and production of high-performance fluid additives, offering a wide range of products for lubricants, fuels, and industrial fluids. The company plays a pivotal role in advancing additive technologies that enhance energy efficiency, reduce emissions, and improve equipment longevity. With a strong focus on research and innovation, BASF collaborates with automotive OEMs and energy companies to develop tailored additive solutions that meet evolving industry standards and environmental regulations.

- A subsidiary of Berkshire Hathaway, Lubrizol specializes in additives for engine oils, transmission fluids, and industrial lubricants. The company’s extensive product portfolio supports performance optimization across automotive, marine, and heavy-duty applications. Lubrizol is recognized for its technical expertise and long-standing partnerships with major oil companies and vehicle manufacturers, ensuring that its additive formulations align with next-generation engine requirements and sustainability goals.

- Evonik is a key player in specialty chemical solutions, including fluid additives designed for enhanced lubrication, fuel efficiency, and corrosion protection. The company emphasizes sustainable chemistry and digital formulation tools to deliver advanced additive packages for both conventional and synthetic fluids. Through strategic collaborations and continuous investment in R&D, Evonik contributes significantly to shaping the future of fluid performance in industrial and mobility sectors worldwide.

RECENT HAPPENINGS IN THE MARKET

- In January 2024, BASF launched a new line of low-ash additive concentrates specifically designed for modern diesel engines, aiming to support cleaner combustion and improved after-treatment system compatibility, reinforcing its leadership in environmentally responsible fluid solutions.

- In March 2024, The Lubrizol Corporation expanded its technical service center in Singapore, enhancing its capacity to provide on-site formulation support to Asian customers and accelerating response times for tailored additive development in the region.

- In June 2024, Evonik announced a partnership with a leading European battery manufacturer to develop dielectric cooling fluids for electric vehicles, incorporating proprietary fluid additives that enhance thermal management and prolong battery life.

- In September 2024, Chevron Oronite introduced a novel dispersant technology that significantly reduces sludge formation in high-mileage engines, positioning itself at the forefront of next-generation lubricant additive innovation.

- In November 2024, Afton Chemical opened a state-of-the-art additive blending facility in Brazil, strengthening its presence in Latin America and enabling localized production to meet the growing demand for high-performance engine oils and industrial lubricants.

MARKET SEGMENTATION

This research report on the global fluid additives market has been segmented and sub-segmented based on type, application, and region.

By Type

- Synthetically modified natural additives

- Synthetic additives

- Natural additives

By Application

- Drilling fluid

- Cement flurry

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the market size and CAGR of the global fluid additives market?

The market is projected to grow from USD 367.75 million in 2025 to USD 605.43 million by 2033, at a CAGR of 6.43%.

2. What are the major trends shaping the fluid additives market?

Increased demand for eco-friendly additives and advancements in synthetic formulations are driving market trends.

3. Which industries are primarily driving demand for fluid additives?

Automotive, industrial lubricants, oil & gas, and metalworking fluids are major contributors to market growth.

4. How is the push for sustainability impacting the fluid additives industry?

The market is shifting toward biodegradable and non-toxic additive solutions to align with environmental regulations.

5. What technological advancements are influencing the market?

Nano-additives, performance enhancers, and multi-functional additives are revolutionizing product efficiency.

6. What growth opportunities exist in emerging markets?

Asia-Pacific and Latin America offer strong growth potential due to industrial expansion and rising lubricant demand.

7. What challenges does the fluid additives market face?

Volatile raw material prices and stringent environmental norms may hinder market expansion.

8. What insights are available about end-user behavior and preferences?

End-users seek additives that improve equipment life, reduce maintenance, and perform reliably under diverse conditions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com