Global Fluoroscopy Market Size, Share, Trends & Growth Analysis Report – Segmented By Surgery Type, End User and Region - Industry Forecast (2024 to 2033)

Global Fluoroscopy Market Summary

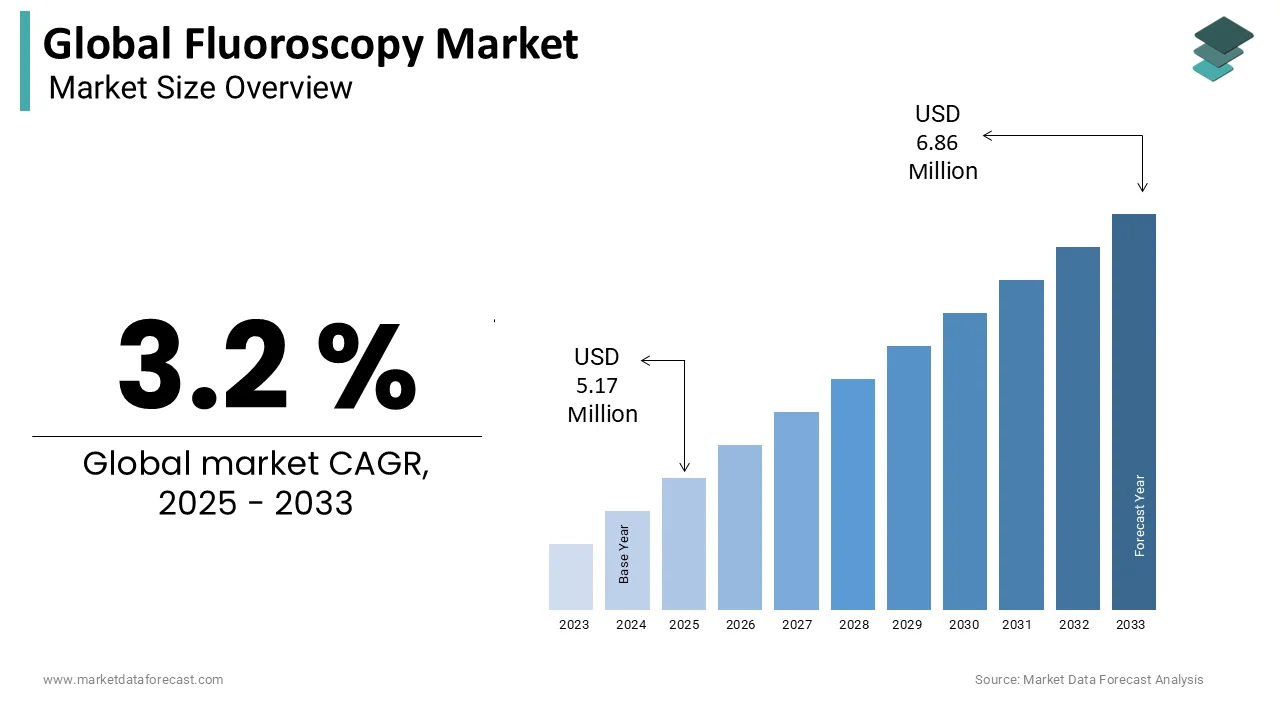

The Global Fluoroscopy Market size was valued at USD 5.17 million in 2024 and is anticipated to reach USD 6.86 million by 2033, growing at a CAGR of 3.20% from 2024 to 2033. The market is gaining momentum due to the rising demand for remote cardiac care, the growing burden of cardiovascular diseases, and technological advancements in AI-powered diagnostics and wearable cardiac monitoring devices.

Key Market Trends & Insights

- Global dominated the global market with a largest share in 2024.

- Global is projected to grow at the fastest rate between 2024 and 2033.

- Based on technology, the IT services segment is the fastest-growing with a projected CAGR of 3.20%.

- AI and wearable tech adoption are key trends driving innovation in the market.

Market Size & Forecast

- 2024 Market Size: USD 5.17 million

- 2033 Projected Market Size: USD 6.86 million

- CAGR (2024–2033): 3.20%

- Global: Largest market in 2024

- Global: Fastest-growing region

Global Fluoroscopy Market Size

In 2024, the global surgical sutures market was valued at USD 5.17 million and it is expected to reach USD 6.86 million by 2033 , growing at a CAGR of 3.2 % during the forecast period.

The fluoroscopy enable real-time visualization of internal body structures using continuous X-ray beams. Widely used in diagnostic and interventional procedures across cardiology, gastroenterology, orthopedics, and urology, fluoroscopy plays an important role in guiding minimally invasive surgeries, detecting abnormalities, and monitoring therapeutic interventions. Modern fluoroscopic systems incorporate digital imaging, flat-panel detectors, and radiation dose optimization features to enhance image quality while minimizing patient exposure.

According to the World Health Organization (WHO), the global demand for advanced medical imaging technologies has surged due to rising prevalence of chronic diseases, growing geriatric populations, and increasing preference for less invasive treatment modalities. As per the International Atomic Energy Agency (IAEA), over 3.6 billion diagnostic radiology exams are conducted annually worldwide, with fluoroscopy accounting for a significant share in complex surgical and interventional settings. Additionally, technological advancements such as artificial intelligence integration, machine learning-based image enhancement, and portable fluoroscopic devices have expanded clinical applications beyond traditional hospital environments. Academic research institutions and healthcare providers are increasingly adopting these innovations to improve procedural accuracy, reduce complications, and streamline workflow efficiency.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases Requiring Image-Guided Interventions

The escalating incidence of chronic diseases that necessitate image-guided diagnostic and therapeutic interventions is propelling the growth of the fluoroscopy market. According to the World Health Organization (WHO), non-communicable diseases (NCDs) such as cardiovascular disorders, cancer, gastrointestinal conditions, and musculoskeletal ailments account for nearly 71% of global deaths annually. Many of these conditions require fluoroscopic guidance for accurate diagnosis and treatment planning. As noted by the Global Burden of Disease Study, cardiovascular diseases alone affect over 520 million people globally, with millions undergoing catheter-based interventions each year procedures that heavily rely on fluoroscopic imaging. Additionally, the International Diabetes Federation (IDF) reports that over 537 million adults suffer from diabetes, many of whom develop complications requiring vascular imaging and foot ulcer assessments guided by fluoroscopy.

Expansion of Minimally Invasive Surgical Procedures

The growing adoption of minimally invasive surgical (MIS) procedures, which rely heavily on real-time imaging for precision and safety is additionally to boost the growth of the fluoroscopy market. According to the Society of Interventional Radiology (SIR), over 10 million interventional procedures were performed in the U.S. alone in 2023, many of which utilized fluoroscopic guidance for catheter placement, stent deployment, and embolization techniques. Furthermore, the rise in outpatient surgical centers equipped with advanced imaging capabilities has facilitated broader access to fluoroscopy-based interventions. As per the Ambulatory Surgery Center Association (ASCA), over 6,000 ambulatory surgery centers operate in the U.S. by offering cost-effective and efficient alternatives to hospital-based procedures.

MARKET RESTRAINTS

Radiation Exposure Concerns and Regulatory Scrutiny

The growing concern over radiation exposure associated with prolonged use of fluoroscopic imaging during diagnostic and interventional procedures is limiting the growth of the fluoroscopy market. According to the U.S. Food and Drug Administration (FDA), fluoroscopy can expose patients and medical personnel to radiation doses significantly higher than those of standard X-rays, which is increasing the long-term risk of radiation-induced cancers and tissue damage. Moreover, public awareness campaigns and legal actions against hospitals for excessive radiation incidents have heightened scrutiny over fluoroscopic device usage. As per the Joint Commission, several U.S. hospitals have been cited for failing to implement adequate radiation dose management strategies.

High Cost of Advanced Fluoroscopic Systems and Maintenance

The high acquisition and maintenance costs associated with advanced imaging systems is also to hamper the growth of the fluoroscopy market. As noted by the Healthcare Financial Management Association (HFMA), a single high-end fluoroscopy suite can cost between USD 500,000 and USD 1.5 million, depending on configuration and integration with digital health platforms. Additionally, ongoing expenses related to software upgrades, detector replacements, and service contracts further add to the financial burden for healthcare institutions. In resource-limited settings, budgetary constraints often result in outdated or poorly maintained fluoroscopic units, compromising image quality and patient safety. As per the World Health Organization (WHO), nearly 40% of medical imaging devices in sub-Saharan Africa are either obsolete or non-functional due to lack of funding for repairs and technical support.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Machine Learning in Fluoroscopic Imaging

The integration of artificial intelligence (AI) and machine learning (ML) into imaging workflows to enhance diagnostic accuracy, reduce radiation exposure, and optimize procedural efficiency, which is creating huge opportunities for the fluoroscopy market. According to the National Institutes of Health (NIH), AI-powered fluoroscopic systems are being developed to provide real-time image enhancement, automatic organ tracking, and intelligent dose modulation based on patient anatomy and movement patterns.

As per the Radiological Society of North America (RSNA), leading medical imaging vendors are incorporating deep learning algorithms that assist radiologists in identifying anomalies more efficiently, reducing human error, and improving overall procedural outcomes. AI-driven analytics also enable predictive modeling of anatomical changes during surgery by allowing for greater precision in interventional settings. Additionally, AI-enhanced fluoroscopic systems are expected to facilitate remote consultations and telemedicine applications, expanding access to expert-guided procedures in rural and underserved areas. As per the World Health Organization (WHO), digital health integration is becoming a priority in national healthcare strategies, particularly in developing economies aiming to strengthen diagnostic capabilities.

Increasing Adoption of Portable and Compact Fluoroscopy Devices

Another significant opportunity influencing the fluoroscopy market is the rising demand for portable and compact fluoroscopic devices, particularly in emergency medicine, ambulatory surgery centers, and field hospitals. According to the World Health Organization (WHO), the need for mobile diagnostic solutions has intensified following recent global health emergencies, which is prompting manufacturers to innovate in lightweight, battery-operated fluoroscopic systems.Furthermore, the shift toward decentralized healthcare models and the expansion of point-of-care diagnostics have created new use cases for compact fluoroscopic equipment.

MARKET CHALLENGES

Need for Skilled Technicians and Specialized Training

The requirement for skilled technicians and specialized training to operate advanced imaging systems safely and effectively is quietly challenging the growth of the fluoroscopy market. According to the World Health Organization (WHO), there is a global shortage of trained radiographers and imaging specialists, particularly in low- and middle-income countries. In Sub-Saharan Africa, for instance, the ratio of radiologic technologists per million population is significantly lower than the global average, limiting access to fluoroscopic services in many regions.

Additionally, the complexity of newer fluoroscopic systems equipped with AI-driven dose reduction, three-dimensional imaging, and motion analysis requires continuous professional development and certification. As per the European Society of Radiology (ESR), many hospitals face delays in deploying advanced fluoroscopic equipment due to the lack of adequately trained staff.

Stringent Regulatory Requirements and Compliance Pressures

The imposition of stringent regulatory requirements aimed at ensuring patient safety, radiation protection, and device performance standards is also to degrade the growth of the fluoroscopy market. According to the U.S. Food and Drug Administration (FDA), fluoroscopic devices must undergo rigorous pre-market approval processes, including clinical validation, electromagnetic compatibility testing, and radiation output verification before commercialization.

As per the International Electrotechnical Commission (IEC), regulatory frameworks such as IEC 60601-2-65 and IEC 61217 govern the safety and functionality of medical imaging equipment, adding layers of compliance complexity for manufacturers. The European Union’s Medical Device Regulation (MDR) further mandates enhanced clinical evidence and post-market surveillance, increasing the administrative and financial burden on companies seeking market entry. Moreover, evolving guidelines on radiation exposure limits and mandatory reporting of adverse events have raised operational costs for healthcare providers. As noted by the Health Physics Society (HPS), many hospitals now invest in dosimetry tracking systems and staff training programs to comply with federal regulations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.30% |

| Segments Covered | By Surgery Type, End User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | GE Healthcare., Orthoscan Inc., Hologic Inc., Shimadzu Corporation |

SEGMENTAL ANALYSIS

By Surgery Type Insights

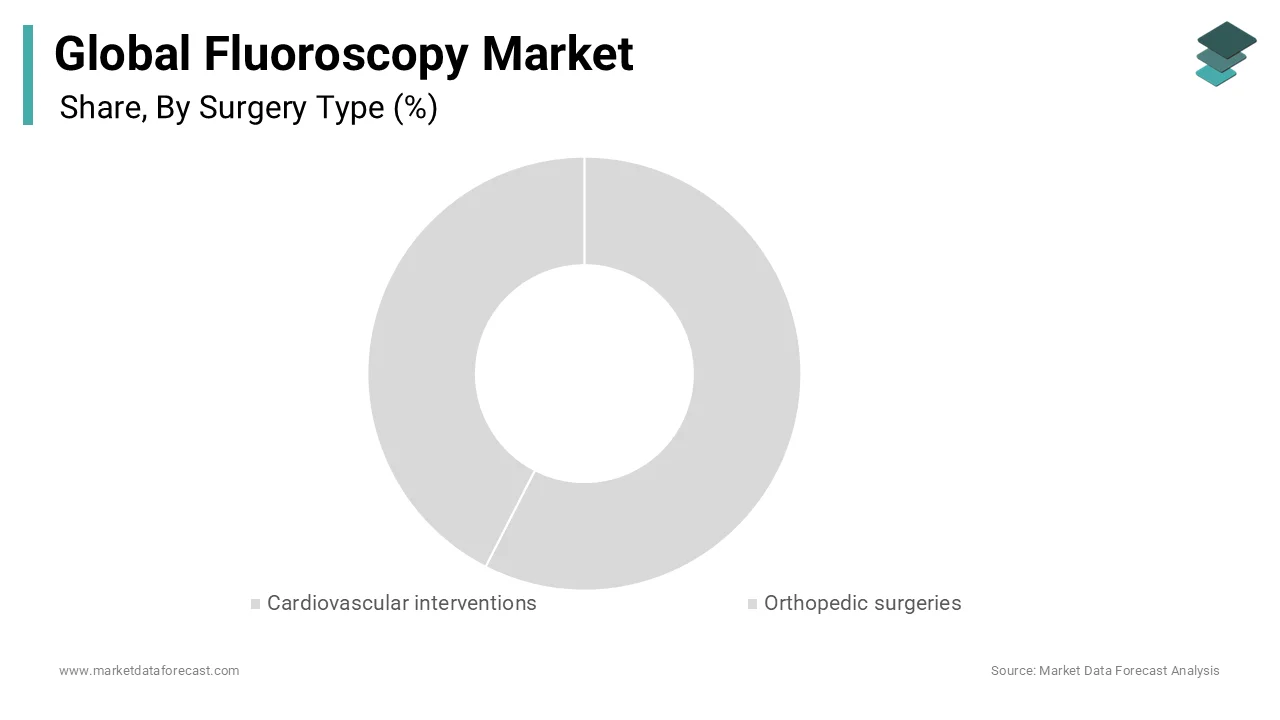

The cardiovascular interventions segment was the largest by accounting for 38.3% of share in 2024. According to the World Health Organization (WHO), cardiovascular diseases remain the leading cause of death globally, with an estimated 17.9 million deaths recorded annually. As reported by the American Heart Association (AHA), over 4 million interventional cardiology procedures were performed in the U.S. alone in 2022, all of which required fluoroscopic guidance for precision and safety. The increasing prevalence of coronary artery disease, coupled with an aging population, has further intensified demand for minimally invasive cardiac interventions. Additionally, advancements in hybrid operating rooms equipped with integrated imaging systems have expanded the use of fluoroscopy in complex cardiac surgeries. As per the European Society of Cardiology (ESC), more than 60% of cardiac catheterization labs now utilize advanced fluoroscopic systems capable of three-dimensional reconstruction and radiation dose optimization.

The Orthopedic Surgeries segment is likely to grow with an expected CAGR of 7.2% in the next coming years with the rising musculoskeletal disorders, increasing joint replacement procedures, and the growing adoption of image-guided surgical techniques. According to the World Health Organization (WHO), musculoskeletal conditions affect more than 1.7 billion people globally, making them one of the most common causes of chronic pain and disability. As per the Global Burden of Disease Study, the number of hip and knee replacements performed worldwide has surged due to an aging population and increased incidence of osteoarthritis and trauma-related injuries. As per the Journal of Bone and Joint Surgery, nearly 85% of spinal fusion and trauma fixation procedures now incorporate fluoroscopic imaging to enhance accuracy and reduce revision rates. Furthermore, the expansion of outpatient orthopedic centers and the development of mobile C-arm systems tailored for orthopedic applications are contributing to increased adoption.

By End User Insights

The hospitals segment was accounted in holding a dominant share of the fluoroscopy market in 2024 with the widespread integration of fluoroscopic imaging in hospital-based diagnostic and interventional departments, including radiology, cardiology, gastroenterology, and emergency medicine.

According to the World Bank, there are over 43,000 hospitals across OECD countries alone, many of which are equipped with advanced imaging suites to support a wide range of fluoroscopically guided procedures. As reported by the American Hospital Association (AHA), U.S. hospitals perform millions of fluoroscopic exams annually, ranging from gastrointestinal tract evaluations to vascular interventions and intraoperative monitoring. Moreover, government funding initiatives aimed at upgrading medical imaging capabilities in public hospitals have reinforced this segment’s position. As per the World Health Organization (WHO), national health programs in several emerging economies have prioritized the installation of digital fluoroscopy units in regional hospitals to improve access to essential diagnostic services.

The diagnostic centers segment is lucratively growing with an expected CAGR of 8.3% in the netx omcing years with the increasing shift toward outpatient diagnostic imaging and the proliferation of independent imaging facilities offering cost-effective alternatives to hospital-based services.

According to the U.S. Centers for Medicare & Medicaid Services (CMS), outpatient diagnostic imaging utilization has grown by more than 20% in the past five years, driven by favorable reimbursement policies and patient preference for shorter wait times and lower costs. As noted by the Radiological Society of North America (RSNA), diagnostic imaging centers now account for nearly 30% of all fluoroscopic procedures in the U.S. for gastrointestinal and urological assessments. Another major factor driving this trend is the rise in preventive healthcare screening programs, especially in developed nations where early detection of conditions like osteoporosis and gastrointestinal disorders is emphasized.

REGIONAL ANALYSIS

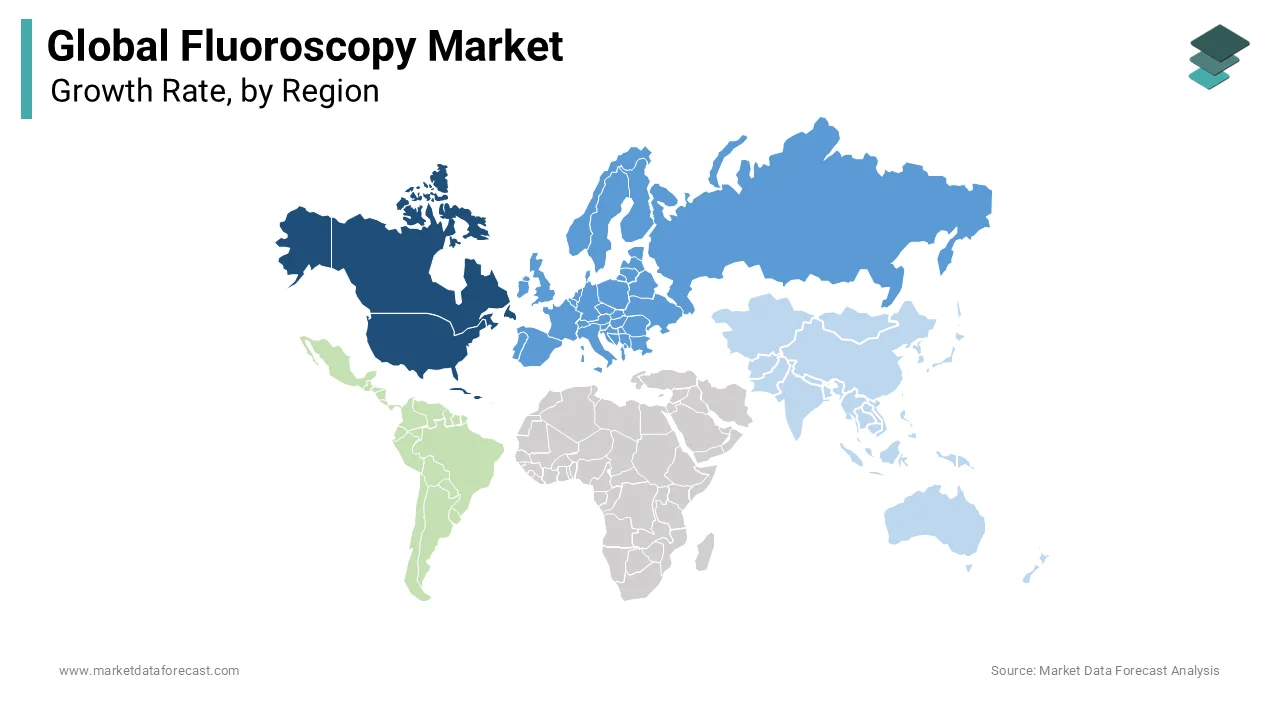

North America was the top performer in the global fluoroscopy market by occupying 35.3% of share in 2024. The growth of the market in this region is attributed to its well-established healthcare infrastructure, high prevalence of chronic diseases, and widespread adoption of advanced medical imaging technologies.

According to the U.S. Food and Drug Administration (FDA), there are over 10,000 active fluoroscopic imaging systems in the United States, supporting a broad spectrum of diagnostic and interventional procedures. As reported by the American College of Radiology (ACR), the U.S. performs millions of fluoroscopy-guided interventions annually, particularly in cardiology, gastroenterology, and orthopedics. Furthermore, the presence of leading manufacturers such as GE Healthcare, Siemens Healthineers, and Philips Healthcare has fostered continuous innovation and competitive product development.

Europe was positioned second with 25.3% of the global fluoroscopy market by maintaining a strong presence due to its well-developed healthcare systems, robust research environment, and emphasis on regulatory compliance. Countries such as Germany, the United Kingdom, and France are among the leading contributors, which is benefiting from extensive use of fluoroscopy in both public and private healthcare settings. According to the European Society of Radiology (ESR), Europe performs over 40 million diagnostic imaging procedures annually, with fluoroscopy playing a crucial role in interventional radiology and surgical applications. Another major growth driver is the increasing prevalence of cardiovascular and musculoskeletal disorders. As per the World Health Organization (WHO), cardiovascular diseases account for nearly 45% of all deaths in the European region, reinforcing the need for image-guided interventions. Additionally, the aging population and rising demand for joint replacement surgeries have further boosted fluoroscopy usage in orthopedic applications. oreover, the region is witnessing growing investment in digital health solutions, including AI-enhanced fluoroscopic imaging platforms.

Asia-Pacific fluoroscopy market is likely to gain huge growth opportunities with rapid expansion driven by growing healthcare expenditure, increasing chronic disease burden, and government-led modernization of medical infrastructure. China, Japan, and India are among the leading markets, which is supported by rising investments in hospital upgrades and diagnostic center networks. According to the World Bank, healthcare spending in Asia-Pacific has increased by more than 6% annually over the past decade, with governments focusing on improving access to advanced imaging technologies. In India, the Ministry of Health and Family Welfare has launched multiple initiatives to strengthen radiology services under the Ayushman Bharat scheme, facilitating broader access to fluoroscopy-based diagnostics. Additionally, Japan’s aging population and high prevalence of osteoporosis and cardiovascular diseases have led to increased use of fluoroscopy in geriatric care. As per the Japanese Ministry of Health, Labour and Welfare, over 2 million fluoroscopic procedures are conducted annually in Japan, particularly for gastrointestinal and orthopedic applications.

Latin America fluoroscopy market growth is likely to grow with Brazil and Mexico serving as primary contributors. According to the Pan American Health Organization (PAHO), Latin America has seen a steady increase in cardiovascular and metabolic diseases, prompting greater reliance on fluoroscopic imaging for diagnostic and therapeutic applications. In Mexico, the Secretariat of Health has implemented reforms to enhance medical equipment procurement and training for interventional radiologists, leading to improved fluoroscopy utilization in both public and private hospitals.

Middle East and Africa fluoroscopy market is set to grow with notable variations in adoption levels across different sub-regions. Saudi Arabia, the United Arab Emirates, and South Africa are among the leading contributors, benefiting from government-backed healthcare modernization programs and strategic investments in medical imaging infrastructure. According to the World Health Organization (WHO), the Middle East and Africa face a rising burden of non-communicable diseases, including cardiovascular and gastrointestinal disorders, necessitating increased access to diagnostic imaging. As noted by the Dubai Health Authority (DHA), the UAE has made substantial progress in equipping hospitals with state-of-the-art fluoroscopic systems, particularly in cardiac and interventional radiology departments. Meanwhile, in Sub-Saharan Africa, efforts by organizations such as the African Union and Gavi, the Vaccine Alliance, are gradually extending access to basic imaging services.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies leading the global fluoroscopy market profiled in the report are GE Healthcare., Orthoscan Inc., Hologic Inc., Shimadzu Corporation, Siemens Medical Solutions, Philips N.V., Hitachi Ltd., Toshiba Medical Systems Corporation, Ziehm Imaging GmbH, and Amico X-ray innovations.

The competition in the fluoroscopy market is characterized by a mix of established multinational corporations and emerging regional players striving to capture market share through technological differentiation and strategic expansion. Global leaders such as GE Healthcare, Siemens Healthineers, and Philips Healthcare dominate due to their extensive product portfolios, robust R&D capabilities, and strong brand recognition in both developed and emerging economies.

These companies benefit from long-standing relationships with hospitals, academic institutions, and government health programs, ensuring consistent procurement and service contracts. Their ability to integrate artificial intelligence, machine learning, and cloud-based imaging analytics into fluoroscopic platforms gives them a competitive edge over smaller firms.

However, mid-tier and independent manufacturers are gaining traction by offering cost-effective alternatives tailored to budget-conscious healthcare providers, particularly in Asia-Pacific and Latin America. These firms focus on modular design, ease of maintenance, and affordability without compromising core performance metrics.

Additionally, regulatory compliance and radiation safety standards play a crucial role in shaping market dynamics. Companies that successfully navigate evolving guidelines while maintaining innovation pipelines are better positioned to sustain dominance in this highly specialized and technically demanding sector.

Top Players in the Market

GE Healthcare is a leading global provider of fluoroscopic imaging systems, known for its innovative and high-performance diagnostic and interventional solutions. The company offers a broad portfolio of fluoroscopy equipment designed to support cardiovascular, gastrointestinal, orthopedic, and urological applications. GE Healthcare plays a critical role in advancing imaging technology through continuous R&D investments and digital integration strategies.

Siemens Healthineers is a key player in the fluoroscopy market, offering cutting-edge imaging platforms that combine superior image quality with radiation dose optimization. The company’s commitment to integrating artificial intelligence and machine learning into fluoroscopic workflows has positioned it as a leader in next-generation medical imaging technologies.

Philips Healthcare contributes significantly to the global fluoroscopy market by delivering advanced, patient-centric imaging solutions tailored for complex interventional procedures. Philips focuses on smart connectivity, AI-assisted diagnostics, and compact system designs that cater to both hospital and outpatient settings, which is reinforcing its strong presence across diverse healthcare environments.

Top Strategies Used by Key Market Participants

One of the primary strategies employed by key players in the fluoroscopy market is continuous innovation and product development by focusing on AI-integrated imaging systems, low-dose radiation technologies, and portable fluoroscopic devices that enhance clinical outcomes while improving operational efficiency.

Another major approach involves expanding geographic reach through strategic partnerships, acquisitions, and localized distribution networks, which is enabling companies to strengthen their foothold in emerging markets where demand for cost-effective and accessible imaging solutions is growing rapidly.

Companies are increasingly prioritizing digital transformation and integration with telemedicine platforms , allowing remote diagnostics, real-time collaboration between specialists, and enhanced workflow automation to meet evolving healthcare delivery models and improve access to fluoroscopic imaging worldwide.

RECENT HAPPENINGS IN THE MARKET

In January 2023, GE Healthcare launched an AI-enhanced fluoroscopic imaging platform featuring real-time dose modulation and automated organ tracking, which is aiming to improve procedural accuracy and reduce radiation exposure during interventional surgeries.

In August 2023, Siemens Healthineers expanded its manufacturing facility in Germany to increase production capacity for next-generation hybrid operating room fluoroscopy systems by supporting rising demand from cardiac and vascular surgery centers across Europe and North America.

In March 2024, Philips Healthcare introduced a new line of compact mobile C-arm fluoroscopy units designed for use in ambulatory surgical centers and field hospitals, which is enhancing accessibility and flexibility in point-of-care diagnostics.

In November 2024, Canon Electron Tubes & Devices partnered with a U.S.-based software firm to develop AI-driven fluoroscopic image enhancement tools, aimed at improving visualization and reducing manual interpretation errors during minimally invasive procedures.

In May 2025, Shimadzu Corporation launched a radiation-reduction module for existing fluoroscopy systems, allowing retrofitting of older units with advanced dose management features, which is addressing growing concerns around patient and staff safety in clinical settings.

MARKET SEGMENTATION

This research report on the global fluoroscopy market segmented and sub-segmented into the following categories.

By Surgery Type

- Cardiovascular interventions

- Orthopedic surgeries

By End User

- Hospitals

- Diagnostic centers

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What are the companies playing a major share in the global fluoroscopy market?

GE Healthcare., Orthoscan Inc., Hologic Inc., Shimadzu Corporation, Siemens Medical Solutions, Philips N.V., Hitachi Ltd., Toshiba Medical Systems Corporation, Ziehm Imaging GmbH and Amico X-ray innovations are some of the notable companies in the fluoroscopy market.

What was the size of the fluoroscopy market worldwide in 2024?

The worldwide fluoroscopy market size was valued at USD 2186.81 million in 2024.

Which segment by type had the major share of the global fluoroscopy market in 2025?

Based on type, the cardiovascular intervention segment had the leading share of the global market in 2025.

Which region is expected to grow the fastest in the worldwide fluoroscopy market in the coming years?

The Asia-Pacific is predicted to grow the fastest in the worldwide market during the forecast period.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com