Europe Fluoroscopy Market Research Report By Type, Application, End-User and Country (United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, and Rest of Europe) - Industry Analysis, Size, Share, Growth, Trends and Forecast (2026 to 2034)

Market Size, 2025

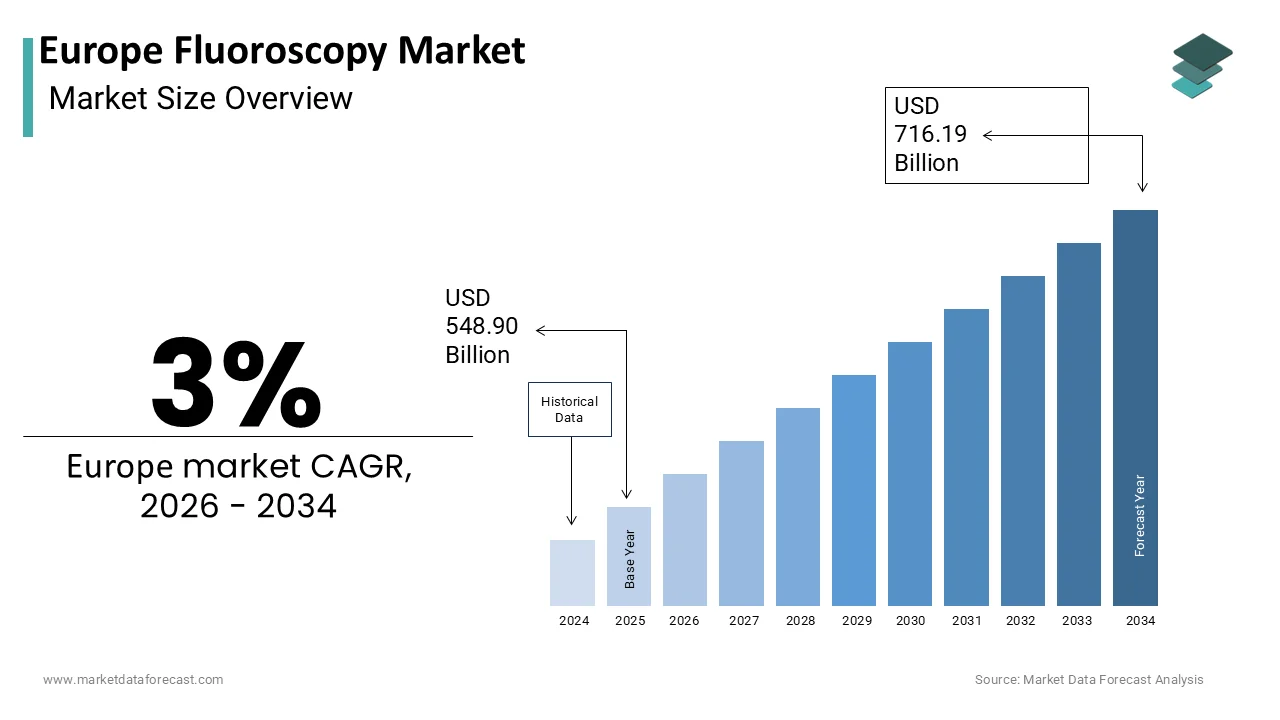

$548.90 MnMarket Estimate, 2026

$565.36 MnMarket Forecast, 2034

$716.19 MnCAGR, 2026–2034

3%Europe Fluoroscopy Market Summary

The Europe fluoroscopy market was valued at USD 532.91 million in 2024, is estimated to reach USD 548.90 million in 2025, and is projected to grow at a CAGR of 3.0% from 2025 to 2033, reaching USD 695.33 million by 2033, driven by rising cardiovascular and orthopedic intervention volumes, an aging population, and regulatory-driven modernization of imaging systems under EU radiation safety and medical device frameworks.

Key Market Insights

- 2024 Market Size: USD 532.91 million

- 2025 Estimate: USD 548.90 million

- 2033 Forecast: USD 695.33 million

- CAGR (2025–2033): 3.0%

Quick Growth Drivers

- Rising burden of cardiovascular diseases requiring image-guided interventions

- Growing adoption of minimally invasive orthopedic and spinal surgeries

- Rapid expansion of hybrid operating rooms in tertiary hospitals

- Aging European population increasing diagnostic and interventional imaging demand

- Regulatory push to replace legacy systems with low-dose digital fluoroscopy

Principal Restraints

- Stringent EU radiation protection and compliance requirements

- Extended procurement timelines and higher total cost of ownership

- Underutilization of systems due to staffing and regulatory constraints

- Budget limitations in smaller hospitals and regional clinics

High-Value Opportunities

- Expansion of fluoroscopy deployment in outpatient and ambulatory imaging centers

- AI-enabled dose optimization and workflow automation

- Compact and mobile C-arm systems for decentralized care models

- Cloud-integrated image management and reporting platforms

- Replacement demand for image-intensifier–based legacy systems

Key Market Challenges

- Shortage of trained radiologists and radiologic technologists

- Fragmented reimbursement policies across EU member states

- Rising cybersecurity risks in network-connected imaging equipment

- High compliance costs linked to EU MDR and GDPR requirements

Fastest-Growing Segments

- Orthopedic Surgeries: 6.8% CAGR — minimally invasive spine and joint procedures

- Diagnostic Centers: 7.1% CAGR — ambulatory care and outsourced imaging

- Cardiovascular Interventions: Largest segment (~42% share in 2024)

Regional Leadership & Dynamics

- Germany (22%) — high procedural volume, strong device manufacturing base

- France (16%) — centralized reimbursement, strict radiation safety enforcement

- United Kingdom (14%) — rapid growth of independent diagnostic centers

- Italy (11%) — high disease burden, EU-funded equipment modernization

- Spain (9%) — outpatient expansion and mobile C-arm adoption

What Wins Commercially

- Advanced dose-reduction and AI-driven imaging technologies

- Strong service, training, and post-installation support networks

- Flexible mobile and outpatient-optimized fluoroscopy platforms

- Proven compliance with EU MDR and radiation safety directives

- Long-term partnerships with hospitals and academic centers

Top Strategic Ask for Executives

- Accelerate AI integration for dose efficiency and workflow optimization

- Target outpatient and diagnostic center expansion aggressively

- Strengthen cybersecurity and software lifecycle management

- Align product roadmaps with EU radiation and device regulations

- Invest in clinical training and user education programs

Leading Players

Some of the companies that are playing a dominating role in the Europe fluoroscopy market include:

- Philips Healthcare

- GE Healthcare

- Siemens Medical Solutions

- Shimadzu Medical Systems

- Shanghai Bojin Medical Instrument Co., Ltd.

- Toshiba Medical Systems Corp.

Europe Fluoroscopy Market Size

The Europe Fluoroscopy Market is projected to grow from USD 548.90 million in 2025 to USD 565.36 million in 2026 and reach USD 716.19 million by 2034, registering a CAGR of 3% from 2026 to 2034.

Fluoroscopy is a medical imaging modality that enables real-time visualization of internal anatomical structures through continuous X-ray beams. In Europe, this technology plays a pivotal role across diverse clinical settings, including orthopedic surgery, cardiology, gastroenterology, and urology. The clinical utility of fluoroscopy has expanded significantly due to its capacity to guide minimally invasive interventions with precision. As per Eurostat, the proportion of the European Union population aged sixty-five and above reached 21.3% in 2023, reflecting a steadily aging demographic that drives demand for diagnostic and interventional imaging. Furthermore, the European Society of Radiology notes that over 800 million medical imaging procedures are conducted annually across the European Union, with fluoroscopy accounting for a substantial subset, particularly in hospital-based settings. Regulatory alignment under the European Union Medical Device Regulation has also intensified equipment modernization, compelling healthcare providers to adopt newer fluoroscopic systems compliant with radiation safety and image quality standards. These systems increasingly integrate digital flat panel detectors and dose optimization algorithms, aligning with the European Commission’s emphasis on patient safety and radiation protection as articulated in the 2013 Council Directive on medical exposure. The technological evolution and demographic pressure collectively shape a complex yet responsive market landscape unique to Europe.

MAKRET DRIVERS

Rising Prevalence of Chronic Cardiovascular Disorders Demands Advanced Imaging Guidance

Cardiovascular diseases remain the leading cause of mortality in Europe, exerting sustained pressure on diagnostic and interventional cardiology infrastructure. According to the European Heart Network, cardiovascular conditions accounted for 36% of all deaths in the European Union in 2023, with over 12 million people living with ischemic heart disease. This epidemiological burden has catalyzed a steep rise in image-guided procedures such as percutaneous coronary interventions, electrophysiology studies, and transcatheter aortic valve replacements, all of which rely on fluoroscopic visualization. The European Society of Cardiology reports that more than 2.3 million percutaneous coronary interventions were performed across Europe in 2022, a figure that continues to grow due to improved access and procedural success rates. Each of these interventions necessitates real-time fluoroscopic imaging for catheter navigation, stent deployment, and anatomical verification. Moreover, the increasing adoption of hybrid operating rooms, equipped with advanced fixed C-arm fluoroscopy systems, further elevates procedural accuracy and workflow efficiency. As national healthcare systems prioritize reducing hospital stays and postoperative complications, minimally invasive cardiac interventions supported by fluoroscopy gain strategic importance. The convergence of clinical necessity, procedural volume, and technological integration ensures that cardiovascular applications remain a primary catalyst for fluoroscopy system adoption across European hospitals and specialized cardiac centers.

Accelerated Integration of Minimally Invasive Orthopedic and Spinal Surgeries

The transformation of orthopedic care through image-guided minimally invasive techniques has become a cornerstone of surgical innovation in Europe. According to the European Federation of National Associations of Orthopaedics and Traumatology, over 2 million spinal fusion and joint replacement procedures are conducted annually in the European Union, with a measurable shift toward fluoroscopy-assisted approaches. For instance, percutaneous vertebroplasty and kyphoplasty, which treat osteoporotic vertebral fractures, depend entirely on real-time fluoroscopic imaging to ensure cement placement accuracy and avoid neural complications. Similarly, minimally invasive total hip and knee arthroplasties increasingly utilize intraoperative fluoroscopy to verify implant alignment and leg length discrepancy, thereby reducing revision rates. Germany alone performed more than 220 000 primary hip replacements in 2022, as per the German Arthroplasty Register, with a growing segment incorporating fluoroscopic verification. Additionally, trauma surgery for complex fractures, especially in the pelvis and spine, demands precise hardware placement that is unattainable without fluoroscopic guidance. National initiatives promoting outpatient surgical care and rapid patient mobilization further incentivize adoption of these techniques. The reliance on fluoroscopy in orthopedics is not merely procedural but foundational to achieving clinical outcomes that meet European quality benchmarks, thus reinforcing steady equipment utilization and replacement cycles across surgical theaters.

MARKET RESTRAINTS

Stringent Radiation Safety Regulations Constrain Equipment Utilization and Procurement

The European Union enforces some of the world’s most rigorous radiation protection standards, which significantly influence fluoroscopy system deployment and usage patterns. As per the Council Directive 2013 59 EURATOM, all medical exposures involving ionizing radiation must adhere to the principles of justification, optimization, and dose limitation. This directive mandates that healthcare facilities implement dose monitoring systems, conduct regular staff training, and ensure equipment compliance with diagnostic reference levels. The European Commission’s 2022 report on medical radiation exposure highlighted that approximately 40% of fluoroscopy procedures in Europe exceed national diagnostic reference levels, prompting intensified scrutiny from national radiation safety authorities. Consequently, hospitals face operational complexities such as delayed procurement approvals, mandatory audits, and increased documentation burdens. In countries like France and the Netherlands, regulatory bodies require pre-procurement assessments demonstrating that new fluoroscopy systems incorporate the latest dose reduction technologies such as pulsed fluoroscopy, automatic brightness control, and spectral filtering. These requirements not only extend procurement timelines but also elevate the total cost of ownership. Moreover, smaller clinics often lack resources to maintain compliance infrastructure, leading to equipment underutilization or reliance on outdated systems. Thus, while patient safety remains paramount, the regulatory ecosystem inadvertently dampens market fluidity and constrains the pace of technology refresh across diverse care settings.

Persistent Shortage of Trained Radiological Personnel Limits Procedural Throughput

Despite technological advancements, the European fluoroscopy market contends with a critical human resource gap that directly affects imaging service delivery. According to the European Society of Radiology, the average radiologist-to-population ratio in the European Union stands at one to 12 000, with significant disparities between Western and Eastern member states. Countries such as Romania and Bulgaria report ratios as high as one to 25 000, whereas Germany maintains one to 8 000. This uneven distribution restricts the availability of qualified professionals capable of operating fluoroscopy systems, particularly in rural and underserved regions. The European Federation of Radiographer Societies further notes that nearly 30% of European radiography departments operate below optimal staffing levels, leading to procedure backlogs and extended wait times. Fluoroscopy demands specialized skillsets for real-time image interpretation, radiation dose management, and patient positioning, all of which require formal training beyond general radiography certification. The European Commission’s 2023 workforce analysis indicated that over 45 000 additional radiological technologists are needed across the Union to meet current demand thresholds. Without adequate staffing, even the most advanced fluoroscopy systems remain underutilized, thereby diminishing return on investment for healthcare institutions. This human capital deficit not only curtails procedural volumes but also hinders the adoption of complex image-guided interventions that depend on seamless team coordination and technical expertise.

MARKET OPPORTUNITIES

Expansion of Outpatient Imaging Centers Presents a Viable Growth Corridor

The structural shift toward ambulatory care models across Europe is forging new deployment pathways for fluoroscopy systems beyond traditional hospital confines. As per the Organisation for Economic Co-operation and Development, outpatient visits in European healthcare systems grew by an average of 3.2% annually between 2018 and 2023, reflecting policy-driven efforts to contain costs and improve access. Within this context, standalone imaging centers and specialty clinics increasingly incorporate fluoroscopy for procedures such as hysterosalpingography, barium studies, and pain management injections. The United Kingdom’s National Health Service, for example, has actively outsourced over 15% of its diagnostic imaging workload to accredited independent providers, as reported by NHS England in 2025. These facilities prioritize compact, mobile, and low-dose fluoroscopy units that align with space constraints and regulatory requirements for non-hospital settings. Manufacturers are responding with purpose-built systems featuring integrated dose monitoring, ergonomic mobility, and cloud-based image management. Germany and France alone host more than 1 200 accredited outpatient radiology centers, according to national health agency registries, many of which have added or upgraded fluoroscopy capabilities in the past three years. This decentralization trend not only diversifies the customer base but also accelerates equipment turnover cycles, creating a resilient demand channel insulated from hospital budget fluctuations and procurement delays.

Advancements in Artificial Intelligence Enhance Clinical Workflow and Dose Efficiency

The integration of artificial intelligence into fluoroscopy systems is emerging as a transformative opportunity across European clinical environments. As per the European Society of Medical Imaging Informatics, over 60% of new fluoroscopy installations in Western Europe in 2025 included AI-enabled features for real time image enhancement and procedural guidance. These algorithms automatically adjust exposure parameters based on patient morphology, reduce image noise without compromising diagnostic clarity, and assist in anatomical landmark recognition during interventions. For example, AI-driven motion correction can mitigate artifacts during gastrointestinal studies, while predictive tracking tools improve catheter navigation accuracy in cardiac electrophysiology. The European Commission’s Horizon Europe program has allocated more than 120 million euros since 2021 to projects focused on AI in medical imaging, accelerating validation and regulatory approval pathways. Furthermore, AI facilitates compliance with dose optimization mandates by generating automated exposure reports and benchmarking against regional diagnostic reference levels. Hospitals in Sweden and the Netherlands have already piloted AI-integrated fluoroscopy platforms that demonstrate up to 35% reduction in mean dose area product per procedure, as documented in peer-reviewed clinical evaluations. As reimbursement frameworks begin to recognize AI as a value-added component, adoption incentives will intensify. This convergence of regulatory alignment, clinical validation, and funding support positions AI not as a peripheral enhancement but as a central driver of next-generation fluoroscopy deployment across Europe.

MARKET CHALLENGES

Fragmented Reimbursement Frameworks Across Member States Impede Uniform Market Growth

The absence of a harmonized reimbursement policy for fluoroscopy-guided procedures across European Union member states creates significant market unpredictability. Each country operates under distinct health technology assessment methodologies and payment codes, leading to substantial variation in procedure coverage, allowable fees, and equipment investment justification. As per the European Observatory on Health Systems and Policies, only 14 of the 27 EU member states have established specific reimbursement tariffs for advanced fluoroscopy-assisted interventions, such as percutaneous valve replacements or spinal fusion. In countries like Italy and Spain, delayed updates to national procedure catalogs result in underpayment for newer techniques, discouraging hospitals from acquiring high-end systems. Conversely, Germany and the Netherlands maintain robust innovation reimbursement pathways, enabling faster technology uptake. This fragmentation forces manufacturers to navigate a mosaic of pricing expectations and clinical evidence requirements, increasing go-to-market complexity and time. The European Commission’s 2023 assessment of cross-border health technology adoption noted that reimbursement disparities account for up to 40% of the variance in medical imaging equipment utilization rates across the Union. Consequently, healthcare providers in lower reimbursement environments often defer equipment upgrades or limit procedural scope, constraining market potential and distorting competitive dynamics across the region.

Escalating Cybersecurity Vulnerabilities in Connected Imaging Systems Introduce Operational and Compliance Risks

The digitization of fluoroscopy systems and their integration into hospital networks have exposed critical vulnerabilities to cybersecurity threats. As per the European Union Agency for Cybersecurity, the healthcare sector experienced a 38% increase in reported cyber incidents in 2023, with medical imaging devices among the most frequently targeted assets. Modern fluoroscopy platforms, equipped with network connectivity for image transfer and remote diagnostics, operate on software architectures that may lack real-time patching capabilities, creating exploitable entry points. A 2025 investigation by the German Federal Office for Information Security revealed that over 30% of installed fluoroscopy units in German hospitals ran outdated firmware with known security flaws, some of which could enable unauthorized access to patient data or device manipulation. Compliance with the EU’s General Data Protection Regulation and the Medical Device Regulation mandates stringent data protection protocols, yet many legacy systems were not designed with these requirements in mind. Hospitals now face costly retrofits, operational disruptions during security audits, and potential liability in case of breaches. Manufacturers, in turn, must invest heavily in secure software development lifecycles and post-market surveillance, which increases device costs and delays product launches. This emerging risk dimension not only affects procurement decisions but also necessitates a paradigm shift in how imaging infrastructure is maintained, monitored, and secured across Europe’s diverse healthcare ecosystems.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Surgery Type, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Philips Healthcare, GE Healthcare, Siemens Medical Solutions, Shimadzu Medical Systems, Shanghai Bojin Medical Instrument Co., Ltd, and Toshiba Medical Systems Corp. |

SEGMENTAL ANALYSIS

By Surgery Type Insights

Cardiovascular interventions represent the largest segment in the European fluoroscopy market, accounting for approximately 42% of total procedural volume in 2025. This dominance stems from the high burden of cardiovascular disease across the region and the indispensable role of real-time imaging in guiding catheter-based procedures. According to the European Society of Cardiology, over 2.4 million percutaneous coronary interventions were performed in Europe in 2023, a figure that has grown steadily due to expanded indications and improved outcomes. Fluoroscopy provides essential visualization for stent placement, valve deployment, and electrophysiological mapping, making it irreplaceable in interventional cardiology suites. Furthermore, the European Heart Network states that ischemic heart disease affects more than 15 million adults in the European Union, creating continuous demand for minimally invasive therapies. National health systems increasingly favor these image-guided techniques to reduce hospital length of stay and postoperative complications. Hybrid operating rooms equipped with advanced fixed C-arm fluoroscopy systems are now standard in tertiary cardiac centers across Germany, France, and the United Kingdom. The integration of dose-optimized imaging protocols and digital detector technology further reinforces fluoroscopy’s centrality in cardiovascular care, ensuring sustained procedural reliance and equipment utilization.

Orthopedic surgeries are the fastest-growing segment within the European fluoroscopy market, projected to expand at a compound annual growth rate of 6.8% between 2025 and 2030. This acceleration is driven by the rising volume of image-guided spinal and joint procedures that require intraoperative fluoroscopic verification. According to the European Federation of National Associations of Orthopaedics and Traumatology, over 1.8 million fluoroscopy-assisted orthopedic interventions were conducted in Europe in 2023, with minimally invasive spine surgeries showing the highest year on year increase. Germany’s national arthroplasty registry reported that more than 225 000 primary hip replacements in 2023 incorporated fluoroscopic alignment checks, a practice now considered standard of care. The shift toward outpatient orthopedic centers also fuels demand for mobile C-arm systems that offer portability without compromising image quality. Additionally, an aging population contributes significantly, as Eurostat data confirms that 29.5% of Europeans aged seventy five and above suffer from osteoarthritis, necessitating joint reconstruction. National policies promoting same-day discharge and rapid rehabilitation further incentivize the adoption of precision-guided techniques. These converging clinical, demographic, and operational factors position orthopedic fluoroscopy as the most dynamic procedural segment in the European landscape.

By End User Insights

Hospitals command the largest share of the European fluoroscopy market, representing approximately 78% of total system installations in 2025. This dominance is rooted in the concentration of complex surgical and interventional services within acute care settings, where fluoroscopy is essential for real-time procedural guidance. As per the European Hospital and Healthcare Employers’ Association, over 90% of image-guided cardiovascular, neurovascular, and orthopedic interventions in Europe occur in hospital operating rooms or catheterization labs. Hospitals also benefit from centralized procurement budgets, regulatory compliance infrastructure, and access to specialized radiological staff, all of which facilitate the adoption of high-end fluoroscopy systems. The European Commission’s 2023 report on medical device utilization noted that tertiary hospitals in Western Europe operate an average of 3.2 fluoroscopy units per facility, compared to 0.4 in outpatient settings. Furthermore, the mandatory alignment with the EU Medical Device Regulation has prompted large hospitals to replace legacy equipment with modern systems featuring dose monitoring and digital imaging capabilities. Given that hospitals manage the majority of emergency and high acuity cases, such as trauma, stroke, and acute cardiac events, their reliance on fluoroscopy remains structurally entrenched and operationally non-negotiable.

Diagnostic centers are the fastest-growing end-user segment in the European fluoroscopy market, anticipated to register a compound annual growth rate of 7.1% from 2025 to 2030. This expansion is propelled by the European healthcare sector’s strategic pivot toward ambulatory care to alleviate hospital congestion and control costs. According to the Organisation for Economic Co-operation and Development, outpatient imaging now accounts for nearly 35% of all diagnostic radiology services in high-income European countries, with fluoroscopy playing a key role in gastrointestinal, urological, and gynecological studies. The United Kingdom alone accredited over 320 independent diagnostic centers for fluoroscopy procedures in 2023, as reported by NHS England, reflecting a deliberate policy to shift low-risk imaging out of acute hospitals. These centers favor compact, low-dose, and mobile fluoroscopy units that comply with stringent radiation safety standards while fitting into limited physical footprints. Additionally, the European Commission’s Cross-Border Healthcare Directive has enabled patients to access private imaging services across member states, further stimulating private diagnostic center growth in countries like Spain and the Netherlands. As reimbursement mechanisms increasingly support decentralized care, diagnostic centers are becoming a high-velocity channel for next-generation fluoroscopy adoption.

COUNTRY LEVEL ANALYSIS

Germany Fluoroscopy Market Analysis

Germany holds the largest share of the European fluoroscopy market at approximately 22% in 2025, driven by its advanced healthcare infrastructure, high procedural volume, and robust medical device manufacturing base. The country performs over 650 000 fluoroscopy guided interventions annually, with cardiology and orthopedics accounting for nearly 70% of usage, according to the German Federal Statistical Office. Germany’s statutory health insurance system covers a comprehensive range of image-guided procedures, ensuring consistent demand across public and private hospitals. The nation is also home to leading medical technology firms such as Siemens Healthineers, which accelerates domestic adoption of cutting-edge fluoroscopy platforms featuring AI integration and dose reduction algorithms. The German Radiological Society mandates continuous professional training for fluoroscopy operators, enhancing procedural safety and equipment utilization. Furthermore, the country’s aging population,n where 22.1% of citizens are aged sixty-five or older, er as per Destatis 2023 data,ata exerts sustained pressure on diagnostic and interventional imaging services. These structural, demographic, and industrial advantages solidify Germany’s position as Europe’s foremost fluoroscopy market.

France Fluoroscopy Market Analysis

France ranks second in the European fluoroscopy market with a 16% share in 2025, underpinned by a centralized public healthcare system that prioritizes equitable access to advanced imaging. The French National Authority for Health reported that over 520 000 fluoroscopy assisted procedures were conducted in public hospitals in 2023, with cardiovascular interventions representing the largest application. France’s national health insurance covers nearly all fluoroscopy-guided diagnostic and therapeutic services, minimizing out-of-pocket barriers for patients. The country also enforces some of the strictest radiation protection protocols in Europe, requiring all fluoroscopy systems to undergo biannual calibration and dose auditing, as mandated by the French Nuclear Safety Authority. This regulatory rigor has spurred the replacement of older image intensifier units with modern flat panel detector systems, particularly in university hospitals in Paris, Lyon, and Marseille. Additionally, France’s commitment to reducing surgical wait t,imes evidenced by a 12% increase in same-day orthopedic interventions since 2020, which has intensified reliance on intraoperative fluoroscopy. These systemic and operational factors ensure France maintains a high and stable fluoroscopy utilization rate.

United Kingdom Fluoroscopy Market Analysis

The United Kingdom commands a 14% share of the European fluoroscopy market in 2025, distinguished by its hybrid public-private delivery model and growing reliance on independent imaging providers. As per NHS England, the National Health Service outsourced 18% of its diagnostic imaging workload to accredited private facilities in 2023, including a significant portion of fluoroscopy procedures such as barium studies and pain management injections. This strategic shift alleviates pressure on overstretched hospital radiology departments, where average wait times for non-urgent imaging exceeded 14 weeks in early 2025. The UK also leads in adopting mobile C-arm systems for outpatient orthopedic and pain clinics, with over 210 private diagnostic centers now equipped for fluoroscopy, according to the Care Quality Commission registry. Despite post Brexit regulatory realignment, the Medicines and Healthcare products Regulatory Agency has maintained stringent device safety standards, ensuring only modern, low-dose systems enter clinical use. The Office for National Statistics confirms that 19.3% of the UK population is aged sixty five or above, sustaining demand for joint and spine interventions. These dynamics position the UK as a responsive and increasingly decentralized fluoroscopy market.

Italy Fluoroscopy Market Analysis

Italy holds an 11% share of the European fluoroscopy market in 2025, characterized by high clinical need amid fiscal constraints within regional healthcare systems. According to the Italian National Institute of Statistics, cardiovascular diseases cause over 230 000 deaths annually, necessitating frequent fluoroscopy-guided interventions such as angioplasty and pacemaker implantation. The Italian Association of Medical Physics reports that over 380 000 fluoroscopy procedures were performed in public hospitals in 2023, with significant concentration in northern regions like Lombardy and Emilia Romagna. However, budget limitations in southern regions have delayed equipment upgrades, resulting in a mixed fleet of image intensifier and flat panel systems. Recent reforms under the National Recovery and Resilience Plan have allocated 1.2 billion euros for medical device modernization, with fluoroscopy listed as a priority for catheterization labs and operating theaters. Additionally, Italy’s aging population, with 24.1% aged sixty-five or older, fuels demand for orthopedic and gastrointestinal fluoroscopy. Despite procurement challenges, the sheer volume of chronic disease ensures Italy remains a top-tier market in terms of procedural throughput and clinical relevance.

Spain Fluoroscopy Market Analysis

Spain accounts for 9% of the European fluoroscopy market in 2025, experiencing accelerated transformation through ambulatory care expansion and public hospital modernization. The Spanish Ministry of Health recorded over 310 000 fluoroscopy procedures in 2023, with notable growth in outpatient pain management and gastroenterology studies. Spain’s decentralized regional health system has enabled autonomous communities like Catalonia and Madrid to invest in next-generation mobile C-arms for day surgery centers, reducing reliance on fixed installations. According to the Spanish Society of Medical Radiology, over 65% of new fluoroscopy purchases in 2023 were mobile units, reflecting a strategic shift toward flexibility and cost efficiency. The country also benefits from EU structural funds, with the 2021 2027 Digital Spain Plan allocating 400 million euros for imaging infrastructure upgrades in public hospitals. Spain’s elderly ppopulationpulation 20.8% aged sixty-five or older, per the National Statistics Institute, continues to drive demand for joint and spinal interventions. Combined with progressive reimbursement for minimally invasive procedures, these factors position Spain as a high-potential market with evolving utilization patterns and strong growth momentum.

KEY MARKET PLAYERS

Key market participants dominating the europe fluoroscopy market profiled in this report are

- Philips Healthcare

- GE Healthcare

- Siemens Medical Solutions

- Shimadzu Medical Systems

- Shanghai Bojin Medical Instrument Co., Ltd.

- Toshiba Medical Systems Corp.

COMPETITIVE LANDSCAPE

The European fluoroscopy market features intense competition among a select group of multinational imaging companies that dominate through technological differentiation and deep clinical integration. These players continuously refine their systems to comply with the European Union Medical Device Regulation and radiation safety mandates while addressing the rising demand for minimally invasive procedures. Competition is not solely price-based but centers on image quality, dose efficiency, system versatility, and post sale support infrastructure. Regional variations in healthcare funding procurement cycles and clinical practices require companies to adopt localized strategies,ies especially between Western and Eastern Europe. Innovation in mobC-arm arm platforms, AI-driven workflows, and hybrid operating room compatibility further intensifies rivalry. Smaller firms struggle to compete due to high regulatory barriers and the capital intensity of R and D. As a result,t the market remains consolidated with leading players reinforcing their positions through strategic partnerships, product customization, ion and proactive engagement with European clinical and regulatory stakeholders.

TOP LEADING PLAYERS IN THE MARKET

- Siemens Healthineers is a pivotal contributor to the global fluoroscopy landscape with a strong footprint across Europe. The company specializes in advanced imaging systems that integrate real-time visualization with dose optimization technologies. Its Artis family of angiography and C arm systems is widely deployed in cardiovascular and hybrid operating rooms throughout Germany, France,e and the United Kingdom. Inrecent years, rs the company has focused on embedding artificial intelligence into its fluoroscopy platforms to enhance image clarity and automate procedural workflows. Siemens Healthineers also collaborates with European academic medical centers to validate new clinical applications and ensure regulatory alignment with the EU Medical DevicRegulation at, ion thereby reinforcing its technological leadership and clinical relevance in the region.

- GE Healthcare maintains a significant presence in the European fluoroscopy market through its Innova and OEC product lines, which serve both fixed and mobile imaging needs. The company actively supports hospitals and diagnostic centItaly Spain, Ital Spainin and the Nordic countries with systems designed for cardiology,ogy orthopedics, and interventional radiology. GE Healthcare has recently acceleratedsoftware-drivenn innovations, including low-dose imaging protocols and cloud-based image management tools tailored for European healthcare workflows. The company also participates in pan-European initiatives on radiation safety and has launched training programs for radiological staff in partnership with national health authorities. These efforts strengthen its role as a solutions-oriented partner rather than just an equipment supplier within the European clinical ecosystem.

- Philips is recognized for its integrated approach to image-guided therapy with a fluoroscopy portfolio centered on the Azurion platform. This system combines real-time imaging with advanced data analytics and is extensively used in electrophysiology and endovascular procedures across the Netherlands, Belgium,m and Sweden. Philips has emphasized sustainability and workflow efficiency in its recent European engagement, ts promoting compact system designs that reduce installation complexity and energy consumption. The company has also expanded its service network to offer predictive maintenance and remote diagnostics,ics ensuring minimal downtime high-volumelume centers. Through strategic collaborations with European healthcare providers, Philips continues to align its fluoroscopy innovations with regional priorities such as outpatient care expansion and AI-enabled clinical decision support.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European fluoroscopy market consistently prioritize technology integration through artificial intelligence and dose reduction algorithms to meet strict regulatory standards. They invest heavily in research and development to launch next-generation systems with enhanced image quality and workflow efficiency. Strategic collaborations with academic hospitals and national health agencies facilitate clinical validation and faster regulatory approvals. Companies also expand their service and support networks to offer predictive maintenance, remote diagnostics,s and staff training,n g which strengthens customer retention. Additionally,lly they tailor product portfolios for outpatient and ambulatory settings to align with Europe’s shift toward decentralized care. These strategies collectively enhance competitiveness and long-term market relevance across diverse European healthcare environments.

EUROPE FLUOROSCOPY MARKET NEWS

- In March 2025, Siemens Healthineers launched the Artis pheno Q withenhaAI-basedd image processing for European hybrid operating rooms, strengthening its portfolio for complex cardiovascular and neuro interventions.

- On May 20,24 GE Healthcare introduced a low-dose mobile C-arm system, OEC Mov,e specifically designed for outpatient orthopedic centers across France and Spain to align with the ambulatory care trendIn

- On February 2025, Philips expanded its Azurion service network in Italy and Sweden, offering predictive maintenance and remote diagnostics to reduce system downtimehigh-volumelume hospitals.

- In June 2025, GE Healthcare partnered with the Spanish Society of Radiology to launch a training program on radiation safety and fluoroscopy best practices for technologists across Southern Europe.

- In January 2025, Siemens Healthineers collaborated with a leading university hospital in the Netherlands to validate a new AI algorithm for real-time spine alignment during minimally invasive orthopedic surgeries.

MARKET SEGMENTATION

This research report on the europe fluoroscopy market has been segmented and sub-segmented into the following categories.

By Surgery Type

- Cardiovascular interventions

- Biopsy

- Orthopedic surgeries

By End User

- Hospitals

- Diagnostic Centers and Clinics

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands, and the rest of Europe

Frequently Asked Questions

1. Who are the major players in the Europe Fluoroscopy Market?

Major players in the Europe Fluoroscopy Market include Canon Medical Systems, Hitachi Medical Systems, Koninklijke Philips NV, Siemens Healthineers, and GE Healthcare. These companies compete through advanced systems and EU regulatory compliance, holding significant shares in Western Europe

2. What drives growth in the Europe Fluoroscopy Market?

Rising cardiovascular diseases, with over 5.4 million new cases by 2015, and demand for early diagnostics drive the Europe Fluoroscopy Market. Minimally invasive procedures and tech advancements like AI integration further boost adoption in interventional suites.

3. What are key applications in the Europe Fluoroscopy Market?

Cardiovascular procedures dominate the Europe Fluoroscopy Market, using fluoroscopy for catheterizations and blockages detection. Orthopedics and gastroenterology also key, supported by mobile C-arms for real-time guidance in surgeries.

4. How does Germany influence the Europe Fluoroscopy Market?

Germany leads the Europe Fluoroscopy Market with advanced healthcare infrastructure and high-volume interventional suites, demanding premium cone-beam CT systems. Its CAGR exceeds regional averages, driven by hospital procurements.

5. What challenges face the Europe Fluoroscopy Market?

Radiation exposure concerns and stringent EU MDR regulations challenge the Europe Fluoroscopy Market, pushing dose reduction innovations. High costs limit smaller clinics, though digital upgrades aid compliance.

6. What is the role of mobile systems in the Europe Fluoroscopy Market?

Mobile fluoroscopy systems gain traction in the Europe Fluoroscopy Market for portability in ORs and emergency use, especially in orthopedics. They offer flexibility amid rising ambulatory procedures.

7. How does cardiovascular demand impact the Europe Fluoroscopy Market?

Cardiovascular applications cover a large share of the Europe Fluoroscopy Market, aiding blood flow visualization in catheterizations amid increasing CVD cases. Early diagnosis tech drives sustained demand.

8. What future trends shape the Europe Fluoroscopy Market?

AI-powered imaging, robotic positioning, and low-dose tech trend in the Europe Fluoroscopy Market, enhancing precision and safety. Edge computing integration supports real-time analytics.

9. Which countries lead the Europe Fluoroscopy Market?

Germany, UK, France, Italy, and Spain lead the Europe Fluoroscopy Market, accounting for most demand due to robust healthcare and replacement cycles under EU MDR.

10. What is fixed vs mobile in the Europe Fluoroscopy Market

Fixed systems dominate hospital settings in the Europe Fluoroscopy Market for high-volume imaging, while mobiles excel in versatility for surgeries. Both evolve with digital enhancements.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com