Europe Contrast Injector Market Research Report By Product, Application & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) - Industry Analysis, Size, Share, Growth, Trends, & Forecasts (2026 to 2034)

Market Size, 2025

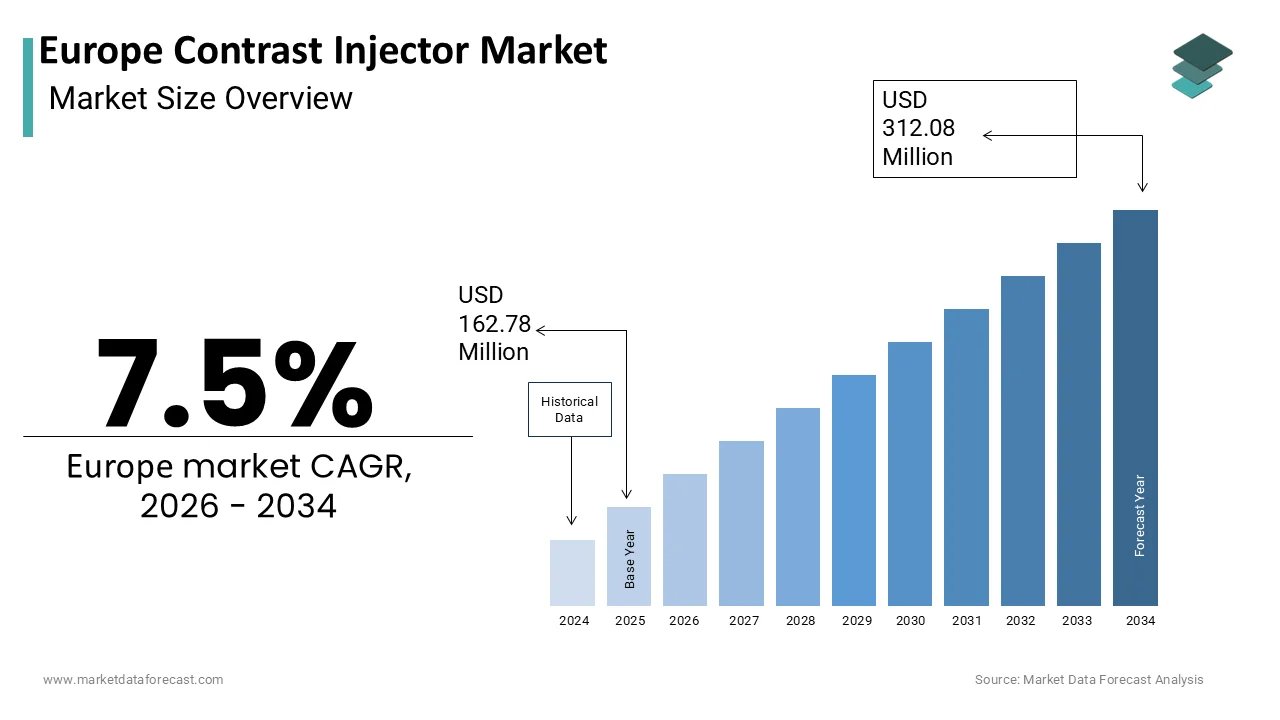

$162.78 MnMarket Estimate, 2026

$174.98 MnMarket Forecast, 2034

$312.08 MnCAGR, 2026–2034

7.5%Europe Contrast Injector Market Executive Summary

The Europe Contrast Injector Market was valued at USD 151.42 million in 2024, is projected to reach USD 162.78 million in 2025, and is expected to grow steadily to USD 290.31 million by 2033, registering a CAGR of 7.5% (2025–2033). Market expansion is driven by rising diagnostic imaging volumes, rapid integration of digital radiology workflows, technological upgrades under EU MDR, and increased adoption of power injectors in CT, MRI, and interventional radiology suites.

Europe Contrast Injector Market Highlights

- Market Value in 2024: USD 151.42 million

- Market Value in 2025: USD 162.78 million

- Market Forecast for 2033: USD 290.31 million

- Growth Rate (2025–2033): 7.5% CAGR

Europe Contrast Injector Market Data Book

2024 Market Size: USD 151.42 million

2025 Market Size: USD 162.78 million

2033 Market Forecast: USD 290.31 million

CAGR (2025–2033): 7.5%

Largest Product (2024): Consumables – 63.6% share

Fastest-Growing Product: Injector Systems – 8.08% CAGR

Largest Application (2024): Radiology

Fastest-Growing Application: Interventional Radiology – 10.4% CAGR

Largest Country (2024): Germany – 26.6%

Key Segment Insights

- Leading Product Segment (2024):

Consumables — 63.6% share driven by recurring, single-use demand.

- Fastest-Growing Product Segment:

Injector Systems — 8.08% CAGR as hospitals replace aging equipment to meet MDR traceability standards.

- Leading Application Segment (2024):

Radiology — highest usage due to large CT & MRI procedure volumes.

- Fastest-Growing Application Segment:

Interventional Radiology — 10.4% CAGR with growing demand for minimally invasive procedures.

Country-Level Insights

- Germany leads with a 26.6% share due to high imaging volumes, stringent compliance, and advanced hospital infrastructure.

- France, UK, Italy, and Sweden show strong adoption driven by screening programs, hybrid OR expansion, and digital radiology upgrades.

Major Market Participants in Europe

Bracco Imaging S.p.A., Bayer HealthCare, Guerbet Group, Medtron AG, Ulrich GmbH & Co. KG, GE Healthcare, AngioDynamics, Nemoto Kyorindo, Sino Medical-Device Technology, VIVID IMAGING, Apollo RT.

Europe Contrast Injector Market Size

The Europe Contrast Injector Market is projected to grow from USD 162.78 million in 2025 to USD 174.98 million in 2026 and reach USD 312.08 million by 2034, registering a CAGR of 7.5% during the forecast period from 2026 to 2034.

A contrast injector is an electromechanical or pneumatic device designed to deliver precise volumes of iodinated or gadolinium-based contrast media during diagnostic imaging procedures such as computed tomography, magnetic resonance imaging, and angiography. These systems enhance image clarity by ensuring consistent injection rates, timing and bolus formation, thereby improving diagnostic accuracy and procedural efficiency. According to Eurostat, the European Union recorded over 132 million CT and MRI procedures in 2025, which reflects robust imaging utilisation across public and private healthcare settings. As per the European Society of Radiology, 78% of EU hospitals with more than 200 beds have adopted power injectors in at least one imaging suite. Regulatory frameworks under the EU Medical Device Regulation 2017/745 mandate stricter conformity assessments for contrast delivery systems, which are driving innovation in safety and interoperability. Concurrently, the European Commission’s 2023 Beating Cancer Plan allocated €240 million to expand early detection imaging capacity, indirectly stimulating injector procurement. These clinical, regulatory and policy dynamics shape a technologically sophisticated and compliance-driven market landscape.

MARKET DRIVERS

Rising Volume of Diagnostic Imaging Procedures Across EU Healthcare Systems

The steady increase in diagnostic imaging demand is one of the key factors driving the growth of the European contrast injector market. According to Eurostat, CT and MRI utilisation continues to rise across the European Union, which reflects robust imaging demand in both public and private healthcare settings. Many EU hospitals with more than 200 beds have adopted power injectors in at least one imaging suite to support advanced diagnostic workflows. Regulatory frameworks under the EU Medical Device Regulation 2017/745 mandate stricter conformity assessments for contrast delivery systems, driving innovation in safety and interoperability. The European Commission’s Beating Cancer Plan includes substantial funding initiatives aimed at expanding early detection imaging capacity, which is indirectly stimulating injector procurement. These clinical, regulatory and policy dynamics shape a technologically sophisticated and compliance‑driven market landscape.

Integration with Advanced Imaging Modalities and Digital Radiology Workflows

Modern contrast injectors are increasingly embedded within integrated diagnostic ecosystems, acting as critical nodes in digital radiology workflows, which is further boosting the European contrast injector market expansion. As per the European Coordination Committee of the Radiological Electromedical and Healthcare IT Industry, many new injector installations now feature bidirectional communication with PACS and RIS systems, which is enabling automatic protocol recall and dose documentation. This interoperability is essential under the EU Medical Device Regulation, which requires full traceability of contrast media administration. The rise of multiparametric imaging demands millisecond‑level synchronisation between injector and scanner, which is a capability only offered by next‑generation systems from vendors like Bayer and Guerbet. Several European radiology networks increasingly emphasise DICOM‑compliant injector integration to facilitate centralised dose monitoring. Additionally, AI‑driven platforms such as GE Healthcare’s Edison use injector data to predict optimal contrast timing based on patient physiology. This convergence of hardware precision, software intelligence and regulatory compliance transforms injectors from standalone tools into indispensable components of precision diagnostics.

MARKET RESTRAINTS

Stringent Regulatory Requirements Under the EU Medical Device Regulation

The EU Medical Device Regulation 2017/745 imposes significant compliance burdens that constrain market entry and product iteration for contrast injector manufacturers, which is one of the key restraints to the European market growth. Unlike the previous Medical Devices Directive, the MDR requires robust clinical evaluation reports, post-market surveillance plans and unique device identification for all Class IIa and higher devices, including power injectors. According to the European Commission’s 2025 implementation review, the average certification timeline for new injector systems has lengthened significantly, which is delaying commercialisation. Additionally, notified bodies remain limited in capacity; as of late 2023, 41 organisations were designated under the MDR, which is creating bottlenecks for high‑risk device assessments. Legacy devices approved under the old regime must undergo re‑certification by May 2027, which is forcing manufacturers to allocate substantial R&D budgets toward compliance rather than innovation. Small and mid‑tier companies face disproportionate challenges, with industry surveys indicating that many SMEs have delayed European launches due to rising MDR‑related costs. These regulatory complexities elevate barriers to entry and slow technology refresh cycles across the continent.

High Cost of Acquisition and Limited Reimbursement for Advanced Injector Systems

Despite clinical benefits, the substantial upfront investment required for modern contrast injectors limits adoption, particularly in publicly funded healthcare systems with constrained capital budgets, which further hinders the growth of the European market. Dual‑head CT injectors with RFID‑enabled syringes and integrated safety sensors are typically priced at a premium, which reflects their advanced automation and safety capabilities. Reimbursement mechanisms rarely cover the device itself. Instead, contrast administration is bundled into the imaging procedure code, which offers minimal margin for capital recovery. Many EU member states provide limited or inconsistent capital‑equipment funding for radiology, and allocation cycles can be delayed by one to two years. In several Southern and Eastern European countries, which is a significant share of imaging departments continue to operate injector systems older than eight years, lacking features like extravasation detection or dose tracking. Hospitals in Italy and Spain report postponing injector upgrades due to competing priorities such as staffing and bed capacity. Without dedicated reimbursement pathways or leasing options, cost remains a persistent barrier to technology diffusion.

MARKET OPPORTUNITIES

Expansion of Interventional Radiology and Hybrid Operating Rooms

The proliferation of hybrid operating rooms and image-guided interventions presents a high-value opportunity for the European contrast injector market. According to the Cardiovascular and Interventional Radiological Society of Europe, hybrid suites continue to expand across the EU, which is supporting complex endovascular and oncological procedures requiring real‑time contrast visualisation. These environments demand injectors compatible with sterile fields, C‑arm fluoroscopy and intraoperative CT, which are capabilities addressed by mobile and ceiling‑mounted systems from Guerbet and Bracco. The European Commission’s Horizon Europe programme includes funding initiatives aimed at advancing integrated platforms for minimally invasive therapy, which is further accelerating adoption. Procedures such as transarterial chemoembolisation and uterine fibroid embolisation rely on precise contrast bolusing to delineate vascular anatomy, increasing injector utilisation per case. Interventional radiology volumes in major EU markets such as France and Germany have shown steady year‑on‑year growth, which is outpacing diagnostic imaging. Manufacturers responding with radiation‑resistant designs and foot‑pedal controls for sterile operation are capturing this specialised yet rapidly expanding niche.

Adoption of Artificial Intelligence for Personalised Contrast Protocols

Artificial intelligence is unlocking new potential in contrast delivery by enabling patient-specific injection regimens that optimise image quality while minimising contrast volume and nephrotoxic risk, which is another major opportunity for the European contrast injector market. AI algorithms analysing patient‑specific parameters such as weight, cardiac output and renal function have been shown in multiple studies to reduce contrast media usage in abdominal CT without compromising diagnostic confidence. Companies like Bayer have embedded such predictive models into their injector platforms, which allows automatic protocol adjustment at the point of care. According to the European Society of Urogenital Radiology, the value of adaptive contrast‑management systems is noted in its recent contrast safety guidance, which notes their potential to support safer dosing practices. Furthermore, EU‑funded research initiatives are developing federated learning networks that refine injection protocols across hospitals while preserving data privacy. As AI becomes integral to radiology decision support, injectors evolve from mechanical dispensers to intelligent diagnostic partners, which is opening a pathway for premium pricing and clinical differentiation in a value‑based care environment.

MARKET CHALLENGES

Shortage of Trained Radiology Technologists and Workflow Disruptions

A critical yet often overlooked challenge in the European contrast injector market is the persistent shortage of skilled radiology personnel capable of operating advanced injection systems. According to the European Federation of Radiographer Societies, the EU continues to face a significant radiographer shortage, with several countries reporting persistent double‑digit vacancy rates. This staffing gap leads to inconsistent injector utilisation. For instance, many technologists skip advanced features like test bolus or multiphase programming due to time pressure or insufficient training. Misuse increases risks of extravasation and suboptimal imaging, which undermines the value proposition of high‑end injectors. Moreover, frequent staff turnover in public hospitals disrupts protocol standardisation, forcing departments to rely on basic manual modes. Without parallel investment in workforce development and simplified user interfaces, even the most sophisticated injectors may underperform in real‑world settings, which limits clinical ROI and procurement justification.

Environmental and Safety Concerns Regarding Gadolinium and Iodinated Contrast Agents

Growing awareness of the environmental persistence and biological risks of contrast media is indirectly challenging injector utilisation patterns in Europe, which is further challenging the growth of the regional market. According to the European Medicines Agency, linear gadolinium‑based agents have been restricted due to concerns about gadolinium retention in the brain, which is prompting a shift toward safer macrocyclic alternatives. Iodinated contrast is classified as hazardous waste under the EU Waste Framework Directive, and disposal requirements have become increasingly stringent in recent years. Hospitals in Sweden and the Netherlands now implement contrast‑minimisation protocols, favouring low‑volume or non‑contrast techniques where feasible. This trend pressures injector manufacturers to demonstrate dose‑reduction capabilities, not just delivery precision. Regulatory scrutiny is intensifying. As per the European Commission’s Strategic Approach to Pharmaceuticals in the Environment, contrast media in its monitoring list, which potentially leads to tighter oversight. As sustainability becomes a pillar of radiology governance, injectors must evolve to support ultra‑low‑dose regimens or risk declining procedural relevance.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Bracco Imaging S.p.A. (Italy), Bayer HealthCare (Germany), Guerbet Group (France), Medtron AG (Germany), Ulrich GmbH & Co. KG (Germany), GE Healthcare (U.S.), AngioDynamics (U.S.), Nemoto Kyorindo Co., Ltd. (Japan), Sino Medical-Device Technology Co., Ltd. (China), VIVID IMAGING (China), Apollo RT Co., Ltd. (China) |

SEGMENTAL ANALYSIS

By Product Insights

The consumables segment dominated the market by holding 63.6% of the regional market share in 2025. The domination of the consumables segment is driven by their recurring nature and regulatory-mandated single-use requirements. Syringe tubing sets and RRFID-enabled contrast containers must be replaced with every patient procedure under the EU Medical Device Regulation to prevent cross-contamination and ensure dosing accuracy. Contrast‑enhanced imaging procedures represent a substantial share of diagnostic activity across EU hospitals, with each requiring at least one consumable kit. This procedural volume translates into sustained demand irrespective of capital equipment cycles. Manufacturers such as Bayer and Guerbet have embedded proprietary RFID chips in their consumables that communicate with injector systems to verify contrast type, volume and expiry, which is preventing off‑label use and enabling automatic billing. Many accredited imaging departments in countries such as Germany, France and the Netherlands now use closed‑system consumables to comply with safety protocols. This integration locks in recurring revenue and minimises substitution risk, making consumables the financial backbone of the injector ecosystem.

The injector systems segment is the fastest-growing product segment in the European contrast injector market and is predicted to grow at a CAGR of 8.08% over the forecast period due to the replacement of legacy manual and semi-automated devices with next-generation electromechanical platforms featuring AI integration and interoperability. A significant share of EU hospitals operating imaging suites built before 2015 still use first‑ or second‑generation injectors lacking dose tracking or extravasation detection. The EU Medical Device Regulation’s requirement for full contrast traceability has rendered these systems non‑compliant, which is triggering upgrade cycles. Germany’s Hospital Future Fund includes dedicated allocations for diagnostic equipment modernisation, supporting the replacement of outdated contrast delivery systems. Moreover, the rise of multiphase and perfusion imaging demands precise bolus timing only achievable with dual‑head CT injectors. Companies like Bracco have responded with ceiling‑mounted systems that reduce floor clutter in hybrid rooms. This convergence of regulatory obsolescence, clinical need and funding availability fuels systemic hardware renewal across the continent.

By Application Insights

The radiology segment occupied the most significant share of the European contrast injector market in 2025. The growth of the radiology segment in the European market is attributed to its central role in diagnostic imaging across oncology, neurology and emergency medicine. Computed tomography remains the primary modality across the EU, with Eurostat data confirming consistently high CT utilisation levels. Hospitals rely on injector systems to standardise bolus delivery across high‑volume departments, as major university hospitals in Europe routinely perform large numbers of contrast‑enhanced CT scans each day. Standardisation is further reinforced by clinical guidelines from the European Society of Radiology, which mandate power injection for all vascular and oncological protocols to ensure diagnostic reproducibility. Additionally, national screening initiatives have institutionalised contrast use in preventive care. The integration of injectors with RIS and PACS enables automatic protocol selection based on referral diagnosis, which streamlines workflow in busy radiology units. This entrenched procedural dependency ensures radiology remains the dominant application for contrast delivery.

The interventional radiology segment is the fastest-expanding application segment for contrast injectors in Europe and is projected to witness a CAGR of 10.4% over the forecast period due to the shift toward minimally invasive image-guided therapies for conditions such as liver cancer, peripheral artery disease, and uterine fibroids. Interventional radiology procedures continue to grow across the EU, supported by expanding clinical adoption and increasing procedural complexity. These interventions require real‑time contrast visualisation during catheter navigation, which is demanding mobile or ceiling‑mounted injectors compatible with sterile fields and C‑arm fluoroscopy. The European Commission’s Beating Cancer Plan has prioritised access to locoregional therapies, contributing to the expansion of interventional radiology infrastructure across Southern and Eastern Europe. Manufacturers have responded with radiation‑hardened injectors featuring foot‑pedal control and low‑profile designs to avoid obstructing surgical access. In France and Sweden, national reimbursement codes now explicitly cover contrast delivery during embolisation procedures, improving hospital economics. This clinical momentum, regulatory support and procedural complexity position interventional radiology as the highest‑growth application frontier.

COUNTRY LEVEL ANALYSIS

Germany Contrast Injector Market Analysis

Germany dominated the contrast injector market in Europe in 2025 by accounting for 26.6% of the regional market share. The dominance of Germany in the European market is attributed to its dense network of high-volume radiology centres and early adoption of regulatory compliance infrastructure. Germany performs a high volume of contrast‑enhanced imaging procedures annually, which is supported by a large installed base of CT and MRI units across public hospitals. The Hospital Future A,ct passed in 2023, allocated €3.5 billion for digital health upgrades, including injector system modernisation to meet EU MDR traceability requirements. University hospitals in Berlin, Munich and Heidelberg have implemented fully integrated injector–PACS workflows enabling automatic contrast documentation for every scan. Additionally, Germany hosts the headquarters of several key medtech players, including Siemens Healthineers, which is fostering close collaboration on system interoperability. Strict enforcement of single‑use consumable mandates by the Federal Institute for Drugs and Medical Devices ensures consistent replacement demand. This combination of procedural scale, regulatory rigour and technological sophistication solidifies Germany’s position as Europe’s most advanced and highest‑value contrast injector market.

France Contrast Injector Market Analysis

France held a substantial share of the European contrast injector market in 2025. The growth of France in the European market is driven by its centralised healthcare planning and strong emphasis on interventional radiology expansion. The French National Authority for Health mandated in 2023 that all regional cancer centres integrate contrast injectors into their diagnostic and therapeutic pathways, directly linking equipment procurement to the national oncology strategy. Santé Publique France has highlighted the growing use of contrast agents nationwide, which reflects rising imaging and interventional procedure volumes across the healthcare system. The government’s “Ma Santé 2022” digital health roadmap requires injector systems to transmit usage data to the national health data hub for real‑time monitoring of contrast safety. Public hospitals in Paris, Lyon and Marseille have adopted AI‑enabled injectors that adjust flow rates based on estimated glomerular filtration rate to reduce nephrotoxicity risk. Furthermore, France’s strict ban on reusable contrast tubing since 2022 has accelerated consumable turnover. This top‑down policy integration ensures sustained and predictable demand across both diagnostic and therapeutic domains.

United Kingdom Contrast Injector Market Analysis

The United Kingdom is anticipated to command a prominent share of the European contrast injector market during the forecast period due to its national cancer screening programmes and NHS infrastructure investment. The NHS Long Term Plan committed to diagnosing 75% of cancers at stages one or two by 2028, spurring a nationwide rollout of contrast‑enhanced CT and MRI. NHS England reports consistently high imaging activity with a substantial share of diagnostic appointments involving contrast administration each year. Lung cancer screening programmes continue to expand, which is generating significant additional demand for injector‑supported procedures. The National Institute for Health and Care Excellence has updated its contrast guidance to support wider standardisation of power‑injection practices across trusts. The NHS Supply Chain has established framework agreements with major vendors, ensuring rapid deployment of compliant systems. Additionally, the UK’s Medicines and Healthcare products Regulatory Agency enforces rigorous post‑market surveillance, compelling hospitals to use injectors with full audit trails. Despite fiscal constraints, this policy‑driven diagnostic surge sustains robust demand for both systems and consumables across England, Scotland and Wales.

Italy Contrast Injector Market Analysis

Italy is estimated to exhibit a healthy CAGR in the European contrast injector market in 2025, owing to the regional disparities in equipment modernisation and a strong focus on cardiac imaging. Northern regions such as Lombardy and Emilia Romagna operate injector systems comparable to German standards, while Southern facilities often rely on older manual devices. A substantial volume of contrast procedures is performed annually in Italy, with interventional cardiology representing one of the highest‑utilisation segments in Europe. The National Recovery and Resilience Plan allocated significant funding in 2025 to upgrade radiology infrastructure in public hospitals, including injector system procurement. Italian cardiology societies have championed the use of dual‑syringe injectors for coronary CT angiography to achieve optimal arterial opacification. Moreover, Italy’s strict adherence to EU MDR has accelerated the phase‑out of non‑traceable consumables, particularly in accredited centres. This blend of clinical specialisation, policy funding and regulatory compliance creates a dynamic yet uneven growth landscape where modernisation is both urgent and regionally prioritised.

Sweden Contrast Injector Market Analysis

Sweden is a notable regional segment for contrasinjectors in Europe. The leadership of Spain in sustainable radiology and digital health integration are propelling the contrast injector market growth in Spain. The Swedish Radiation Safety Authority requires all contrast injector systems to log dose data in the national quality registry, enabling population-level monitoring of contrast safety. A large share of public imaging departments in Sweden use RFID‑enabled closed‑system consumables to minimise waste and ensure traceability. The country performs a substantial volume of contrast procedures annually, with a strong emphasis on dose‑minimisation protocols supported by AI‑driven injectors. Karolinska University Hospital has implemented low‑volume injection approaches designed to reduce contrast usage without compromising image quality, influencing practice across Scandinavia. Sweden’s participation in the EU4Health‑funded “Green Radiology” initiative has further incentivised procurement of energy‑efficient and low‑waste injector systems. This forward‑looking combination of environmental stewardship, digital governance and clinical innovation positions Sweden as a high‑value Nordic hub for next‑generation contrast delivery.

COMPETITIVE LANDSCAPE

The European contrast injector market is characterised by concentrated competition among three vertically integrated multinational corporations that dominate both contrast media and delivery system segments. Bayer Guerbet and Bracco leverage their proprietary consumables to create closed ecosystems that ensure recurring revenue and limit third-party substitution. Competition is less about hardware pricing and more about clinical workflow integration, regulatory compliance, and service depth. New entrants face high barriers, including EU Medical Device Regulation certification cost,,s stringent hospital procurement requirements, and the need for extensive clinical validation. Differentiation arises through AI-driven protocol optimisation, interoperability with major imaging vendors, and sustainability features such as contrast minimisation. While small regional players exist in consumables, they lack the scale to offer full system solutions. The market remains innovation-intensive with continuous upgrades in safety, connectivity, and dose management, defining ng competitive advantage in this highly specialised medical technology domain.

KEY MARKET PLAYERS

Key players operating in the europe contrast injector market profiled in this report are

- Bracco Imaging S.p.A. (Italy)

- Bayer HealthCare (Germany)

- Guerbet Group (France)

- Medtron AG (Germany)

- Ulrich GmbH & Co. KG (Germany)

- GE Healthcare (U.S.)

- AngioDynamics (U.S.)

- Nemoto Kyorindo Co., Ltd. (Japan)

- Sino Medical-Device Technology Co., Ltd. (China)

- VIVID IMAGING (China)

- Apollo RT Co., Ltd. (China)

TOP LEADING PLAYERS IN THE MARKET

- Bayer AG is a global leader in contrast media and delivery systems with deep integration across the radiology value chain. Through its Radiology division, Bayer develops and commercialises the Medrad family of injector systems, including the Stellant and Spectris platforms, widely used in European hospitals. The company supplies both iodinated gadolinium-based contrast agents alongside RFID-enabled consumables, ensuring end-to-end protocol control. In 2025, Bayer launched its Calantic Digital Solutions platform in Europe, which integrates injector data with AI-driven image analysis to optimise contrast timing. It also expanded its collaboration with Siemens Healthineers to embed protocol harmonisation directly into CT and MRI consoles. These initiatives reinforce Bayer’s position as a solutions-oriented partner advancing precision diagnostics across Europe and globally.

- Guerbet Group is a France-based multinational specialising in medical imaging with a comprehensive portfolio spanning contrast agents and injector systems under the OptiVantage and Acist brands. The company plays a pivotal role in advancing interventional radiology workflows by offering mobile and ceiling-mounted injectors compatible with hybrid operating rooms. Guerbet actively participates in EU-funded research initiatives, including the Horizon Europe Project, to develop adaptive contrast protocols. In early 20,25, Guerbet introduced a new generation of low-volume syringes, reducing contrast waste by 25% while maintaining bolus integrity. Its GESIO platform enables real-time dose tracking aligned with EU MDR requirements. These innovations strengthen Guerbet’s reputation as a sustainability-focused innovator in both European and global imaging markets.

- Bracco Imaging S.p.A. is a leading European player in diagnostic imaging with a vertically integrated strategy encompassing contrast media production and injector system development through its EZEM and Acist subsidiaries. The company offers the EmpowerCTA and EmpowerMR injectors designed for high-throughput diagnostic and interventional settings. Bracco actively supports radiology departments in meeting EU regulatory mandates by providing integrated consumables with QR-coded traceability and automatic expiry validation. In 2025, Bracco partnered with Philips to develop injector interfaces that auto-configure based on exam type and patient data. It also launched a training academy across Mila and Warsaw to certify technologists on advanced injection protocols. These educational and technological investments enhance clinical adoption and reinforce Bracco’s commitment to safety and workflow efficiency in Europe and beyond.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European contrast injector market are pursuing vertical integration by aligning contrast media formulation with delivery system design to ensure protocol fidelity. They invest in AI-enabled software platforms that synchronise injector parameters with imaging modalities for precision bolusing. Companies are embedding RFID and QR technologies in consumables to comply with the EU Medical Device Regulation traceability mandates. Strategic partnerships with imaging OEMs such as Siemens, Philips, and GE Healthcare facilitate native system integration. Expansion of training programmes for radiology staff ensures proper utilisation of advanced features. Additionally, ly firms are developing low-volume and low-waste injector systems to address environmental and nephrotoxicity concerns. These strategies collectively enhance clinical value, regulatorycompliancee and customer retention.

MARKET SEGMENTATION

This research report on the europe contrast injector market has been segmented and sub-segmented into the following categories.

By Product

- Injector Systems

- Consumables

By Application

- Radiology

- Interventional Cardiology

- Interventional Radiology

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the size of the Europe contrast injector market?

The market was valued at USD 151.42 million in 2024 and is projected to reach USD 290.31 million by 2033, growing at a CAGR of 7.5%.

2. What is driving the growth of contrast injectors in Europe?

Rising CT/MRI volumes, strict MDR regulations, and increased cancer-screening initiatives are significantly boosting injector adoption across hospitals.

3. How does MDR 2017/745 impact the contrast injector market?

The MDR imposes strict conformity assessments, longer certification timelines, and mandatory traceability, raising compliance costs but accelerating technological upgrades

4. Which product segment dominates the market?

Consumables lead with 63.6% share due to single-use requirements, RFID-enabled safety, and mandatory replacement for every contrast procedure.

5. .Which segment is growing the fastest?

Injector systems are growing the fastest (CAGR 8.08%), driven by upgrades from older devices to next-generation AI-enabled and interoperable platforms.

6. Which application contributes most to market demand?

Radiology is the largest application, owing to high volumes of CT/MRI scans and standardized power-injection protocols across EU hospitals.

7. Which application is expanding quickest?

Interventional radiology is growing the fastest (CAGR 10.4%) due to rising minimally invasive procedures and hybrid OR installations.

8. Which country leads the Europe contrast injector market?

Germany dominates with 26.6% share, supported by high imaging volumes, strict regulatory enforcement, and strong digital integration.

9. What major challenges slow market growth?

Stringent MDR compliance, high equipment costs, limited reimbursement, and skilled radiology workforce shortages hinder widespread adoption.

10. Who are the leading market players?

Key players include Bayer, Bracco, Guerbet, Medtron, ulrich GmbH, GE Healthcare, AngioDynamics, and Nemoto Kyorindo, dominating through integrated injectors, consumables, and AI platforms.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com