Global Agricultural Testing Market Size, Share, Trends & Growth Forecast Report, Segmented By Contaminants (Toxins, Chemical Residues, Pathogens, And Others), Sample Type (Soil, Water, Seed, Bio-Solids, Manures And Others), And Region (North America, Europe, Asia-Pacific, Middle East & Africa, Latin America), Industry Analysis From 2026 To 2034

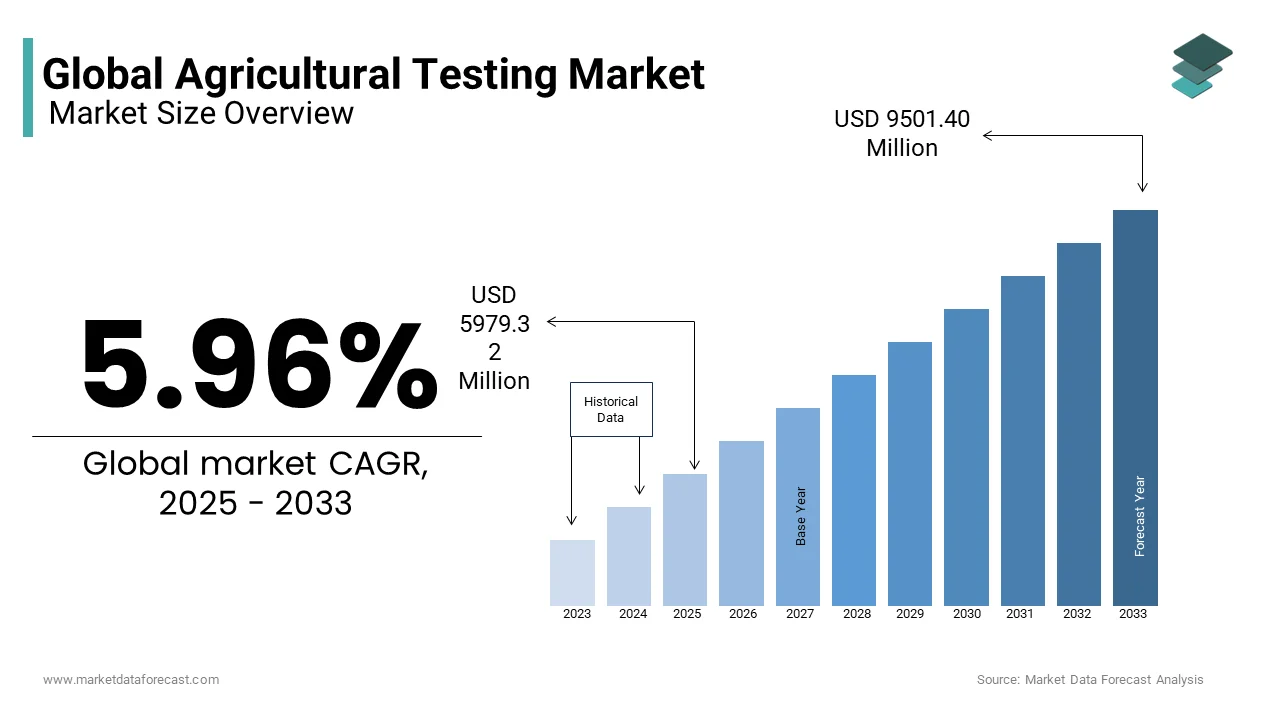

Market Size, 2025

$5979 MnMarket Estimate, 2026

$6160 MnMarket Forecast, 2034

$7368 MnCAGR, 2026–2034

5.96%Global Agricultural Testing Market Size

The global agricultural testing market was valued at USD 5979.32 million in 2025 and is anticipated to reach USD 6160.493 million in 2026 from USD 7368.815 million by 2034, growing at a CAGR of 5.96% during the forecast period from 2026 to 2034.

Agricultural Testing Market Comprehensive Analysis

Agricultural testing encompasses a specialized suite of analytical services and diagnostic tools designed to evaluate the quality, safety, and composition of soil, water, crops, and agricultural inputs. This sector plays a critical role in modern agronomy by providing data-driven insights that optimize crop yield, ensure food safety, and promote environmental sustainability. The definition extends to the detection of contaminants such as pesticides, heavy metals, mycotoxins, and genetically modified organisms in food products. As per the Food and Agriculture Organization of the United Nations, approximately 13% of food is lost between harvest and retail, while an additional 19% is wasted at the retail and consumer levels, highlighting the need for rigorous quality control and testing throughout the supply chain. According to the World Health Organization, an estimated 600 million people fall ill each year after eating contaminated food, underscoring the public health imperative for robust agricultural testing protocols. The regulatory landscape is increasingly stringent, with governments implementing stricter maximum residue limits for agrochemicals to protect consumer health. Technological advancements in rapid testing methods and portable devices are transforming the industry, enabling real-time decision-making for farmers and processors. The market operates at the intersection of scientific innovation and regulatory compliance, addressing the dual challenge of feeding a growing global population while ensuring the safety and integrity of the food supply. This sector continues to evolve as stakeholders prioritize transparency and traceability in agricultural production systems.

MARKET DRIVERS

Stringent Food Safety Regulations and Compliance Requirements

The implementation of stringent food safety regulations and compliance requirements is a key factor fuelling the expansion of the global agricultural testing market. Governments and international bodies are enforcing stricter standards for pesticide residues, heavy metals, and microbial contaminants in food products to protect public health. As per the European Food Safety Authority, 96.3% of the samples analyzed in 2022 fell within legally permissible levels, demonstrating the effectiveness of regulatory frameworks. In the United States, the Food Safety Modernization Act mandates preventive controls and rigorous testing for agricultural products moving through the supply chain. According to the United States Department of Agriculture, the USDA's Pesticide Data Program found that over 99% of the samples tested had residues below the tolerances established by the EPA. Farmers and food processors must adhere to these standards to avoid legal penalties and maintain market access. The globalization of food trade further amplifies the need for standardized testing protocols to ensure consistency across borders. Importers and exporters face heightened scrutiny, requiring comprehensive certification and testing documentation. The increasing complexity of regulatory landscapes drives demand for accredited laboratories and advanced testing services. Companies invest in robust quality assurance systems to mitigate risks and build consumer trust. This regulatory pressure creates a structural demand for agricultural testing services, ensuring sustained market growth. The continuous evolution of safety standards necessitates ongoing adaptation and investment in testing capabilities.

Rising Consumer Awareness and Demand for Organic Products

The rising consumer awareness regarding food quality and the increasing demand for organic products are further contributing to the agricultural testing market expansion. Modern consumers are more informed and concerned about the origin, composition, and safety of their food, leading to a preference for transparent and verified supply chains. As per the Organic Trade Association, organic food sales in the United States hit a new record in 2023, totaling $63.8 billion. To validate organic claims and ensure authenticity, rigorous testing for pesticide residues and genetically modified organisms is essential. According to a 2024 consumer survey by McKinsey, approximately 60% of consumers report that they prioritize products with healthy or clean labels, often associated with organic and non-GMO certifications. This willingness drives producers to invest in third-party testing and certification to differentiate their products in a competitive market. The proliferation of private labels and specialty brands further intensifies the need for verification to maintain brand integrity. Social media and digital platforms amplify consumer voices, making reputation management critical for agribusinesses. Any failure in safety or labeling can lead to immediate backlash and loss of trust. Consequently, companies prioritize regular testing to demonstrate compliance and quality. This consumer-driven demand for transparency and purity ensures a consistent and growing need for agricultural testing services. The trend toward clean label products reinforces the importance of accurate and reliable testing protocols.

MARKET RESTRAINTS

High Costs of Advanced Testing Technologies

The high costs associated with advanced testing technologies and laboratory services are hampering the expansion of the agricultural testing market, particularly for small and medium-sized enterprises. Sophisticated equipment, such as mass spectrometers and chromatography systems, requires substantial capital investment and specialized maintenance. As per the World Bank, over 80% of the world's food is produced by family farms, many of whom lack the financial resources to access high-end testing facilities. According to a report by the International Food Policy Research Institute, the high cost of compliance and laboratory certification can represent up to 10% of the total production cost for small-scale exporters in developing nations. The expense of hiring qualified personnel and maintaining accredited laboratories further adds to the operational burden. Many smaller entities rely on basic or outdated testing methods, which may not meet current regulatory standards. This financial barrier limits the widespread adoption of comprehensive testing protocols. The lack of affordable testing options forces some producers to bypass necessary checks, increasing the risk of contamination and non-compliance. Government subsidies and support programs are often insufficient to cover the full cost of advanced testing. The economic disparity between large agribusinesses and smaller operators creates an uneven playing field. Until cost-effective solutions become widely available, the high expense will remain a persistent hurdle. This financial constraint restricts market penetration and limits the overall impact of agricultural testing on food safety.

Lack of Standardized Testing Protocols and Infrastructure

The lack of standardized testing protocols and adequate infrastructure are further hindering the agricultural testing market growth. Variations in testing methods and accreditation standards across different regions create challenges for international trade and data comparability. As per the International Organization for Standardization, there are currently over 1,600 standards specifically dedicated to food products to help harmonize global safety requirements. According to the United Nations Industrial Development Organization, many developing countries face a significant "quality gap" due to the lack of internationally accredited laboratories and metrology institutes. The absence of unified standards leads to discrepancies in results, causing disputes between exporters and importers. Inconsistent enforcement of regulations further complicates compliance efforts for multinational companies. The fragmentation of the testing landscape increases the complexity and cost of ensuring global supply chain safety. Small laboratories may struggle to achieve international accreditation, limiting their credibility and market access. The lack of interoperability between different testing systems hinders data sharing and collaboration. This infrastructural gap prevents the seamless integration of testing results into broader quality assurance frameworks. Without standardized protocols, the reliability of testing data is compromised, affecting decision-making and risk management. Addressing these inconsistencies requires significant investment in capacity building and regulatory harmonization. Until a unified framework is established, the lack of standardization will continue to hinder market efficiency and growth.

MARKET OPPORTUNITIES

Integration of Rapid and Point of Care Testing Solutions

The integration of rapid and point of care testing solutions is a lucrative opportunity for the agricultural testing market. These technologies enable real-time analysis of soil, water, and crop samples directly in the field, reducing the need for centralized laboratory testing. As per the Global System for Mobile Communications Association, there are now over 600 digital agriculture services globally, reaching over 30 million smallholder farmers. Rapid tests using biosensors and lateral flow assays provide immediate results, allowing farmers to make timely decisions regarding irrigation, fertilization, and pest management. According to a report by Deloitte, the adoption of precision agriculture tools can lead to an 18% increase in productivity and a 15% reduction in fertilizer use. The ability to detect contaminants and nutrient levels instantly enhances operational efficiency and reduces crop loss. Manufacturers are developing user-friendly devices that require minimal training, making them accessible to a broader range of users. The integration of these devices with mobile applications allows for data logging and remote monitoring. This technological advancement appeals to modern farmers aiming for data-driven management. The potential for cost savings and improved productivity drives the adoption of rapid testing solutions. By embracing these innovations, companies can capture a new segment of the market and enhance customer engagement. This convergence of technology and agriculture opens new avenues for service-based business models.

Expansion into Emerging Markets with Growing Agricultural Sectors

The expansion into emerging markets with growing agricultural sectors offers significant opportunities for the agricultural testing market. Countries in Asia-Pacific, Latin America, and Africa are experiencing rapid agricultural modernization driven by population growth and urbanization. As per the United Nations Conference on Trade and Development, developing countries' share of global agricultural exports increased to approximately 40% in recent years. Governments in countries like India, Brazil, and Kenya are investing in laboratory infrastructure and regulatory frameworks to meet international standards. According to a report by the Brookings Institution, the global middle class is expected to reach 4.8 billion by 2030, with the vast majority of that growth occurring in Asia. This shift creates a need for comprehensive testing services to verify product safety and quality. International testing companies can establish local partnerships and facilities to serve these expanding markets. The growing awareness of food safety issues among local producers further stimulates demand. The potential for long-term growth in these regions is substantial as agricultural practices become more sophisticated. By entering these markets early, companies can establish brand recognition and capture market share. The alignment with national development goals ensures supportive policy environments. This geographic expansion diversifies revenue streams and reduces dependence on mature markets. The untapped potential in emerging economies supports sustained industry growth.

MARKET CHALLENGES

Complexity of Sample Matrix and Interference Issues

The complexity of sample matrices and interference issues is a significant challenge to the agricultural testing market growth. Agricultural samples, such as soil, plant tissue, and food products, contain diverse and variable components that can interfere with analytical measurements. As per the American Chemical Society, the use of high-resolution mass spectrometry has become essential to distinguish target analytes from complex background interferences in environmental samples. According to a study published in the journal Analytical and Bioanalytical Chemistry, matrix effects can cause signal suppression or enhancement of up to 50% in multi-residue pesticide analysis. Food matrices with high fat, protein, or sugar content pose similar challenges for pesticide and mycotoxin analysis. These interferences require sophisticated sample preparation and extraction techniques, which increase the time and cost of testing. The variability of samples across different seasons and regions further complicates method validation. Laboratories must constantly update and refine their protocols to address new matrix challenges. The lack of universal reference materials for complex matrices hinders standardization and quality control. Analysts require extensive training and expertise to navigate these complexities effectively. Failure to account for matrix effects can lead to inaccurate data and poor decision-making. This technical challenge requires continuous research and development to improve method robustness. Addressing matrix interference is crucial for ensuring the credibility and utility of agricultural testing services.

Shortage of Skilled Personnel and Technical Expertise

The shortage of skilled personnel and technical expertise is further challenging the expansion of the agricultural testing market. Accurate testing requires highly trained analysts, scientists, and technicians who can operate complex instruments and interpret data correctly. As per the United Nations Educational, Scientific and Cultural Organization, women still represent only 33% of researchers globally, indicating a persistent gender gap and a broader untapped talent pool in STEM fields. According to a survey by the International Laboratory Accreditation Cooperation, 45% of accredited laboratories identify the recruitment of technically competent staff as a major operational challenge. The turnover rate in technical roles is high, leading to inconsistencies in service quality and increased training costs. The rapid evolution of testing technologies requires continuous professional development, which many organizations fail to provide adequately. In developing regions, the scarcity of educational institutions offering specialized training exacerbates the problem. The lack of experienced personnel hinders the adoption of advanced testing methods and limits innovation. Laboratories face delays in processing samples and generating reports due to staffing shortages. This bottleneck affects the timely delivery of results, which is critical for agricultural decision-making. Addressing this skills gap requires investment in education and training programs. Without a competent workforce, the industry cannot meet the growing demand for high-quality testing services.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.96% |

| Segments Covered | By Type of Sample, Contaminants, and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | SGS SA, Eurofins Scientific, Intertek Group plc, Bureau Veritas, ALS Limited, Agilent Technologies, Thermo Fisher Scientific, Mérieux NutriSciences, TUV Nord Group, AsureQuality Limited, RJ Hill Laboratories Ltd., SCIO Analytical, Cropnuts, Eurofins BioDiagnostics, A&L Canada Laboratories Inc., Waters Corporation, R J Hill Laboratories Ltd., SCS Global Services, Invivo Labs. |

SEGMENTAL ANALYSIS

By Contaminants Insights

The chemical residues segment dominated the market by holding the highest share of the global market in 2025. The growth of the chemical residues segment in the global market can be credited to the implementation of stringent regulatory limits on pesticide residues in food and agricultural products globally. Governments and international bodies have established maximum residue limits to protect public health from the adverse effects of agrochemical exposure. As per the European Food Safety Authority, the 2022 report showed that 96.3% of the 110,829 samples analyzed were within legal limits. In the United States, the Environmental Protection Agency regularly updates tolerance levels for pesticides, necessitating rigorous testing by producers and exporters. According to the United States Department of Agriculture, the Pesticide Data Program tested 10,127 samples in its latest cycle, with over 99% of products having residues below EPA tolerances. The global nature of food trade means that exporters must meet the standards of multiple jurisdictions, each with varying limits, creating a complex testing landscape. This regulatory pressure drives consistent demand for advanced analytical techniques, such as gas chromatography and mass spectrometry. The need to avoid trade rejections and legal penalties ensures that chemical residue testing remains a priority for agribusinesses. The continuous introduction of new pesticides and the revision of existing limits further sustain the high volume of testing activities in this segment.

However, the pathogens segment is projected to showcase a CAGR of 8.2% during the forecast period in the global market owing to the increasing incidence of foodborne illnesses and the need for rapid detection of microbial contaminants. The rapid growth of the pathogens segment is largely attributed to the rising incidence of foodborne illnesses caused by bacteria, viruses, and parasites in agricultural products. Outbreaks linked to contaminated fresh produce, meat, and dairy products have heightened awareness of the need for robust microbial testing. As per the World Health Organization, an estimated 600 million people fall ill and 420,000 die every year from eating contaminated food. In response, regulatory agencies, such as the Centers for Disease Control and Prevention, have intensified surveillance and reporting requirements for pathogens like Salmonella, E. coli, and Listeria. According to the CDC, roughly 48 million people in the U.S. get sick from foodborne diseases annually. The frequency of product recalls due to microbial contamination has increased, prompting food producers to enhance their testing protocols. The globalization of food supply chains increases the risk of cross-border transmission of pathogens, necessitating rigorous testing at multiple points. The adoption of preventive controls under frameworks like the Food Safety Modernization Act mandates regular environmental and product testing for pathogens. This regulatory and health-driven imperative drives the adoption of advanced rapid testing methods. The ability to detect low levels of pathogens quickly is crucial for preventing outbreaks. This urgent need for safety ensures that pathogen testing continues to grow at a faster rate than other contaminant segments.

By Sample Insights

The soil segment led the market with the largest share of the global market in 2025. The growth of soil segment in the global market is driven by its critical role in precision agriculture and optimized nutrient management, which are essential for maximizing crop yields and minimizing input costs. Soil tests provide detailed information on nutrient levels, pH, and organic matter content, allowing farmers to apply fertilizers more efficiently. As per the United States Department of Agriculture, precision agriculture technologies are now used on over 50% of the acreage for major U.S. crops like corn and soybeans. According to a study by the American Society of Agronomy, grid soil sampling and variable rate fertilization can increase net returns by up to $15 per acre compared to uniform application. This economic benefit drives widespread adoption of soil testing among commercial growers. The increasing cost of fertilizers further incentivizes farmers to avoid over-application and ensure that nutrients are available in the right proportions. Soil testing also helps identify deficiencies and toxicities early, allowing for timely corrections. The integration of soil data with geographic information systems enables variable rate application technologies, which optimize input distribution across fields. This data-driven approach enhances sustainability by reducing nutrient runoff and environmental impact. The foundational importance of soil health in agricultural productivity ensures that soil testing remains the most frequently conducted analysis. The continuous emphasis on sustainable intensification supports the sustained leadership of this segment.

On the other hand, the water segment is expected to expand at a CAGR of 9.5% during the forecast period in the global market due to the increasing water scarcity and growing concerns about the quality of water sources used for irrigation and livestock. Climate change and over-extraction have reduced the availability of fresh water, forcing farmers to rely on alternative sources, such as recycled wastewater and groundwater, which may contain contaminants. As per the Food and Agriculture Organization of the United Nations, agriculture currently accounts for 70% of all freshwater withdrawals globally. According to a report by the World Bank, poor water quality can reduce economic growth in downstream areas by up to one third. The presence of salts, nitrates, and pathogens in irrigation water can adversely affect crop health and yield. Testing for these parameters is essential to prevent soil salinization and plant diseases. The reuse of treated wastewater in agriculture is gaining traction but requires rigorous monitoring to ensure it meets safety standards. Regulatory frameworks in many regions are tightening requirements for water quality in agricultural settings. The need to protect livestock from waterborne diseases also drives testing for microbial contaminants. The economic impact of poor water quality on crop productivity encourages proactive monitoring. This combination of scarcity and quality issues ensures that water testing continues to grow rapidly. The focus on sustainable water management supports the expansion of this segment.

REGIONAL ANALYSIS

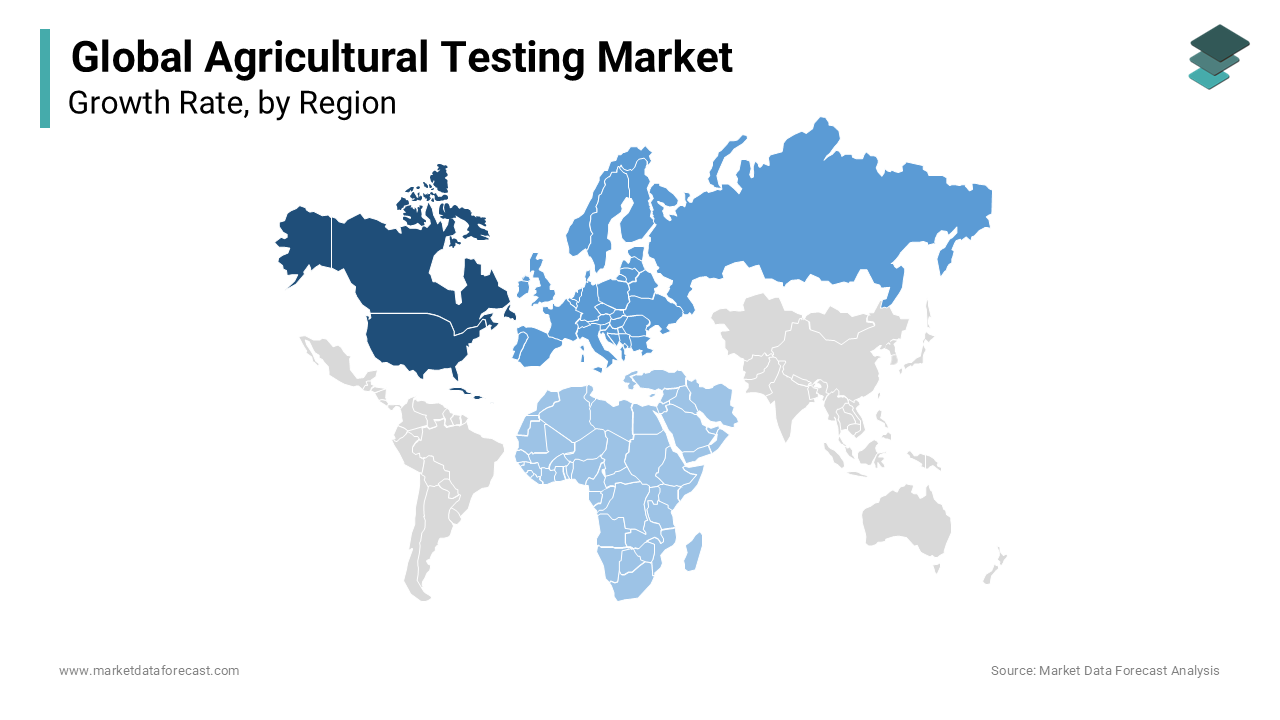

North America Market Analysis

North America held the dominant position in the global agricultural testing market by accounting for 33.8% of the global market share in 2025. The North America market is fundamentally driven by a robust regulatory framework and high levels of technological innovation in agricultural practices. As per the United States Department of Agriculture and the Canadian Food Inspection Agency, strict regulations govern pesticide residues, genetically modified organisms, and microbial contaminants in food products. These agencies mandate comprehensive testing protocols to ensure food safety and facilitate international trade. According to a 2023 USDA report, nearly 90% of U.S. corn, cotton, and soybean acreage is planted with genetically engineered seeds, necessitating continuous GMO testing and monitoring. The widespread adoption of precision agriculture technologies in the United States and Canada drives demand for detailed soil and water testing. The presence of leading testing laboratories and research institutions fosters innovation in rapid detection methods. The high level of consumer awareness regarding food safety and organic certification further stimulates market growth. The integration of digital tools and data analytics in farming operations enhances the efficiency and accuracy of testing processes. The strong intellectual property protection encourages investment in new testing technologies. This combination of regulatory rigor and technological advancement ensures that North America remains the largest and most sophisticated market for agricultural testing. The continuous evolution of safety standards and farming practices sustains high demand for testing services.

Europe Market Analysis

The European Union is likely to see an increase in specialized testing for biodiversity and soil carbon sequestration over the coming years as it implements the next phase of its comprehensive Green Deal. The stringent environmental regulations and a strong focus on sustainable agriculture are further driving the growth of the European market. The Europe market is fundamentally driven by strict environmental regulations and ambitious sustainability goals aimed at reducing the ecological footprint of agriculture. As per the European Union, the Farm to Fork Strategy aims to reduce the use of chemical pesticides by 50% and ensure at least 25% of agricultural land is under organic farming by 2030. According to the European Food Safety Authority, the 2022 pesticide residue report involved the analysis of over 110,000 food samples. The requirement for comprehensive traceability and certification drives regular testing across the supply chain. The high prevalence of organic farming in countries like Germany, France, and Italy necessitates rigorous testing to verify compliance with organic standards. The focus on soil health and biodiversity conservation also drives demand for soil and water quality assessments. The harmonization of testing standards across member states facilitates trade and ensures consistency. The strong consumer preference for safe and sustainable food products reinforces the importance of testing. This regulatory and cultural environment ensures steady market growth. The commitment to environmental protection sustains demand for advanced testing solutions.

Asia Pacific Market Analysis

Asia-Pacific holds a rapidly growing position in the global agricultural testing market. China, India, and Southeast Asian nations are projected to undergo a massive expansion of laboratory infrastructure and digital testing services in the next few years to match their rapid agricultural industrialization. The rising food safety concerns and the ongoing modernization of agricultural practices in countries like China, India, and Japan are fuelling the regional market growth. As per the Food and Agriculture Organization of the United Nations, the Asia-Pacific region is home to 60% of the world's population, making food security and safety a critical regional priority. According to a report by the Asian Development Bank, the region requires an estimated $800 billion in incremental investment by 2030 to build a sustainable and secure food system. Countries are strengthening regulatory frameworks and investing in laboratory capabilities to ensure food safety for domestic consumption and export. The growing middle class and increasing demand for high quality and safe food products drive the adoption of testing services. The expansion of export-oriented agriculture requires compliance with international standards, prompting producers to invest in rigorous testing. The adoption of modern farming techniques and precision agriculture is increasing the demand for soil and water testing. The presence of numerous smallholder farmers presents challenges, but also opportunities for scaling testing services through mobile and rapid testing solutions. The government initiatives to improve food security and safety support market growth. This dynamic environment ensures rapid expansion of the agricultural testing market in the region.

Middle East and Africa Market Analysis

Middle East and Africa holds a emerging position in the global agricultural testing market due to the efforts to improve food security and manage water resources. Countries across the Middle East and Africa are expected to prioritize desalination quality testing and desert-soil enrichment diagnostics over the next few years to bolster their domestic food sovereignty. As per the World Bank, agriculture accounts for about 15% of GDP in Sub-Saharan Africa and is the primary source of livelihood for many. According to a report by the African Union, only about 5% of agricultural land in Africa is currently irrigated, highlighting a massive potential for growth in water-related testing as infrastructure expands. The reliance on irrigation and the use of treated wastewater necessitate regular water quality testing to prevent soil salinization and crop damage. The expansion of commercial farming and export crops in countries like South Africa, Kenya, and Egypt drives demand for residue and contaminant testing. Government initiatives to enhance agricultural productivity and ensure food safety are supporting the establishment of testing laboratories. The increasing awareness of foodborne illnesses and the need for compliance with export standards further stimulate market growth. The challenges of limited infrastructure and technical expertise are being addressed through international collaborations and capacity building programs. This focus on sustainable agriculture and food safety ensures gradual but steady market expansion. The strategic importance of agriculture drives continued investment in testing services.

Latin America Market Analysis

Latin America holds a notable position in the global agricultural testing market owing to a strong export-oriented agricultural sector and increasing regulatory oversight. Brazil, Argentina, and Chile are likely to expand their adoption of satellite-integrated soil testing and biological residue monitoring over the next few years to maintain their competitive edge in global commodity exports. As per the Inter-American Institute for Cooperation on Agriculture, Latin America and the Caribbean account for approximately 14% of global agricultural and fisheries production. According to the World Trade Organization, the region provides about 25% of global exports in agricultural and fisheries products. Countries like Brazil, Argentina, and Chile are major exporters of soybeans, fruits, and meat, requiring comprehensive residue and contaminant testing. Compliance with regulations in importing countries, such as the United States and European Union, drives the demand for accredited testing services. The increasing domestic awareness of food safety and environmental protection is leading to stronger regulatory frameworks and enforcement. The adoption of modern agricultural practices and precision farming techniques is increasing the need for soil and water testing. The presence of multinational testing companies and local laboratories supports market growth. The focus on sustainable agriculture and certification schemes further stimulates demand for testing. This export-driven dynamic ensures consistent market activity. The continuous improvement in regulatory standards supports the expansion of the agricultural testing market in the region.

COMPETITIVE LANDSCAPE

The competitive landscape of the Agricultural Testing Market is characterized by the presence of large multinational corporations and specialized regional laboratories who compete on accuracy speed and service quality. Incumbent players leverage extensive networks and accredited facilities to maintain dominance while smaller firms differentiate through niche expertise and localized service. Competition is driven by the need for rapid and reliable results to ensure food safety and regulatory compliance. Price sensitivity varies by segment with large agribusinesses prioritizing quality and smallholders focusing on cost. Innovation in rapid detection technologies and digital integration serves as a key differentiator. Regulatory harmonization efforts influence market entry strategies and operational standards. Strategic mergers and acquisitions are common as companies seek to expand capabilities and geographic reach. The rise of private label testing services adds pressure on established brands. Overall the market favors entities that can balance technological sophistication with accessibility and customer trust while navigating complex regulatory environments.

KEY MARKET PLAYERS

They are playing a dominant role in the agricultural testing market.

- SGS SA

- Eurofins Scientific

- Intertek Group plc

- Bureau Veritas

- ALS Limited

- Agilent Technologies

- Thermo Fisher Scientific

- Mérieux NutriSciences

- TUV Nord Group

- AsureQuality Limited

- RJ Hill Laboratories Ltd

- SCIO Analytical

- Cropnuts

- Eurofins BioDiagnostics

- A&L Canada Laboratories Inc

- Waters Corporation

- R J Hill Laboratories Ltd

- SCS Global Services

- Invivo Labs

Top Players In The Market

- Eurofins Scientific SE is a global leader in bioanalytical testing services with a significant presence in the agricultural testing sector. The company provides comprehensive solutions for food safety soil analysis and environmental monitoring. Recent strategic initiatives include expanding its laboratory network in key agricultural regions to enhance local service capabilities. Eurofins has invested heavily in digital platforms to streamline sample tracking and result delivery for clients. The corporation focuses on acquiring specialized niche laboratories to broaden its technical expertise and geographic reach. By leveraging advanced analytical technologies Eurofins ensures high accuracy and rapid turnaround times. These efforts aim to solidify its position as a trusted partner for agribusinesses seeking reliable and compliant testing services while supporting sustainable agricultural practices globally.

- SGS SA contributes significantly to the market through its extensive network of inspection verification and testing facilities worldwide. The company offers robust agricultural testing services including pesticide residue analysis and soil health assessments. Recent actions involve strengthening its sustainability credentials by offering certified organic and non GMO testing services. SGS has enhanced its digital capabilities to provide real time data access and integrated supply chain solutions. The organization focuses on collaborating with governments and industry bodies to develop standardized testing protocols. By emphasizing quality and integrity SGS builds strong relationships with producers and exporters. These strategies enable the company to maintain its reputation for excellence and drive growth in the evolving agricultural testing landscape.

- Bureau Veritas SA plays a pivotal role in the agricultural testing market with its diverse portfolio of certification and testing services. The company specializes in ensuring compliance with international food safety standards and environmental regulations. Recent strategic moves include expanding its agricultural testing laboratories in emerging markets to meet growing demand. Bureau Veritas has invested in research and development to improve detection methods for contaminants and pathogens. The organization emphasizes customer centric solutions by providing tailored testing packages for specific crop types. By leveraging its global expertise Bureau Veritas positions itself as a key enabler of safe and sustainable agriculture. These initiatives help the company differentiate itself in a competitive market and build long term partnerships with stakeholders.

Top Strategies Used By Key Market Participants

Key players in the Agricultural Testing Market primarily employ expansion and technological innovation strategies to sustain growth. Companies are increasingly investing in advanced analytical technologies such as mass spectrometry and rapid testing kits to enhance accuracy and efficiency. This approach allows them to offer faster turnaround times and broader testing capabilities. Another major strategy involves expanding geographic presence through acquisitions and partnerships in emerging markets. Manufacturers focus on developing digital platforms for seamless data management and client engagement. Strategic collaborations with regulatory bodies help shape industry standards and ensure compliance. By balancing technological advancement with global reach key participants strengthen their market positions and adapt to evolving regulatory and consumer demands effectively.

MARKET SEGMENTATION

This research report on the global agricultural testing market is segmented and sub-segmented based on the type of sample, contaminants, and region.

By Type Of Sample

- Water

- Seed

- Bio-solids

- Manures

- Soil

- Others

By Contaminants

- Toxins

- Chemical residues

- Pathogens

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the agricultural testing market?

The agricultural testing market includes soil, water, seed, and crop testing services used to assess quality, safety, and productivity in farming.

What is driving the growth of the agricultural testing market?

Rising food safety regulations, soil health awareness, precision farming adoption, and demand for higher crop yields are key growth drivers.

Which type of testing dominates the agricultural testing market?

Soil testing dominates due to its critical role in nutrient management, fertilizer optimization, and sustainable farming practices.

Why is soil testing important in agriculture?

Soil testing helps determine nutrient levels, pH balance, and contamination, enabling efficient fertilizer use and improved crop productivity.

How does precision agriculture support market growth?

Precision agriculture relies on accurate testing data to optimize inputs, reduce costs, and improve yield predictability.

Which regions are leading the agricultural testing market?

North America and Europe lead due to strict regulatory frameworks, while Asia-Pacific shows rapid growth from expanding agriculture activities.

What role do government regulations play in this market?

Regulations mandate soil, water, and residue testing to ensure food safety, environmental protection, and export compliance.

What are the key challenges in the agricultural testing market?

High testing costs, lack of awareness among small farmers, and limited laboratory infrastructure in developing regions are major challenges.

How is technology transforming agricultural testing?

Advancements like digital soil sensors, AI-based analytics, and rapid diagnostic kits are improving accuracy and turnaround times.

What is the future outlook of the agricultural testing market?

The market is expected to grow steadily due to sustainable farming initiatives, climate-smart agriculture, and increasing global food demand.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com