Global Blood Flow Measurement Devices Market Size, Share, Trends & Growth Analysis Report By Product, Application and Region - Industry Forecast (2026 to 2034)

Blood Flow Measurement Devices Market Summary

Market Size & Growth

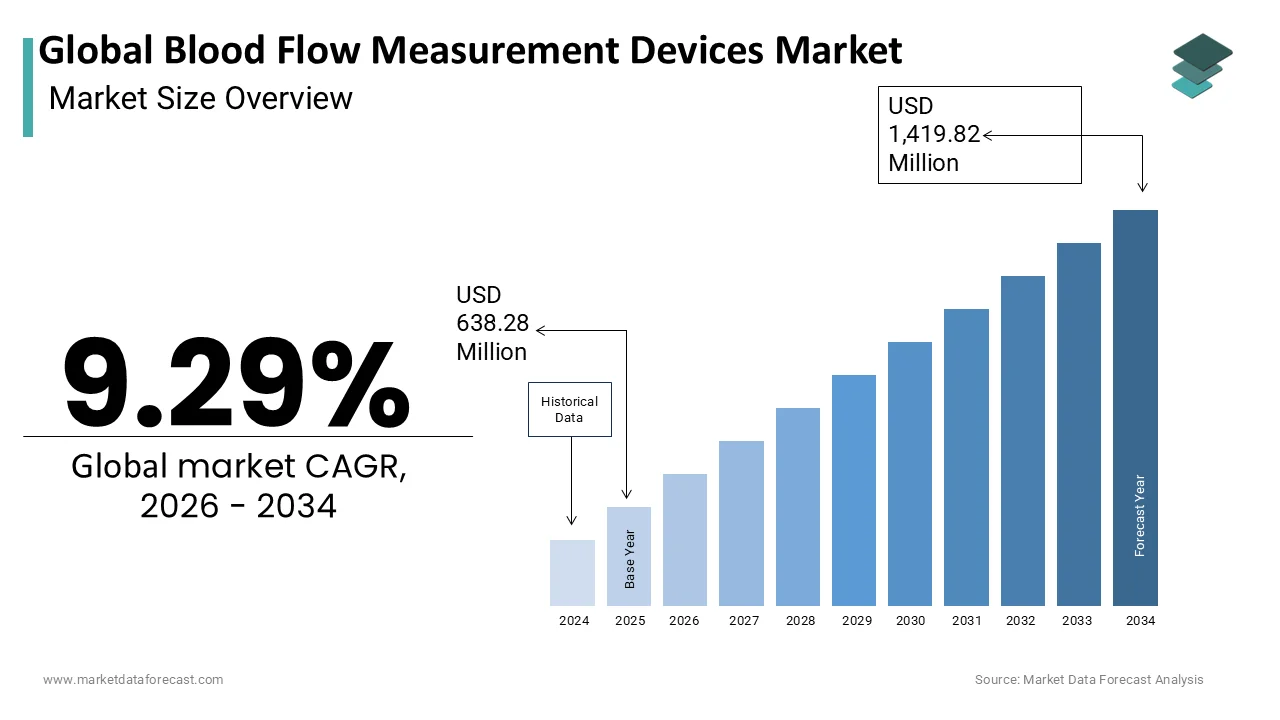

- The global blood flow measurement devices market was valued at USD 638.28 million in 2025.

- Expected to reach USD 1,419.82 million by 2034, growing at a CAGR of 9.29% from 2026 to 2034.

- North America held the largest regional share at 38.1% in 2025; Asia Pacific is the fastest-growing region.

Key Market Segments

- By Product: Ultrasound Doppler (dominant share in 2025), Transit-Time Flow Meters, Laser Doppler (fastest-growing at CAGR of 9.2%, 2026–2034)

- By Application: Cardiovascular Disease (largest segment in 2025), Tumour Monitoring (fastest-growing at CAGR of 8.7%, 2026–2034), Diabetes, Gastroenterology, CABG, Microvascular Surgery

- By Region: North America leads (38.1%); Europe second (30.3%); Asia Pacific highest growth rate

Key Drivers

- Cardiovascular disease affects over 60 million people in the European Union, driving sustained diagnostic demand (European Heart Network, 2025)

- WHO reports cardiovascular diseases cause approximately 19.8 million deaths annually, representing 32% of all global deaths

- Laser Doppler adoption accelerated by the 530 million+ diabetes patients worldwide requiring microvascular monitoring (WHO)

- AI integration enabling automated flow quantification and real-time hemodynamic analysis is expanding device utility

- Growth of telemedicine and remote patient monitoring driving demand for portable, Bluetooth-enabled Doppler units

Key Players

GE Healthcare, Siemens Healthineers, Philips, Cook Medical Inc., BIOPAC Systems Inc., Atys Medical, SONOTEC Ultraschallsensorik Halle GmbH, Moor Instruments Ltd., Transonic Systems Inc., Perimed AB, Medistim ASA, Deltex Medical Group plc, Compumedics Limited, ADInstruments Pty Ltd.

Global Blood Flow Measurement Devices Market Size

The Global Blood Flow Measurement Devices Market is projected to grow from USD 638.28 million in 2025 to USD 697.57 million in 2026 and reach USD 1,419.82 million by 2034, registering a CAGR of 9.29% during the forecast period from 2026 to 2034.

Blood flow measurement devices are specialized medical and clinical instruments used to measure the velocity, volume rate, and distribution of blood circulating through arteries, veins, or tissues. These technologies include Doppler ultrasound systems, laser Doppler flowmetry units, and advanced magnetic resonance imaging modalities that provide critical insights into vascular health and tissue perfusion. The clinical significance of these devices extends across cardiology, neurology, and peripheral vascular disease management where precise assessment of blood velocity and volume is indispensable for accurate diagnosis and treatment planning. According to the World Health Organization (WHO), cardiovascular diseases are the leading cause of death globally, claiming an estimated 19.8 million lives annually, which accounts for roughly 32% of all global deaths. This staggering burden underscores the imperative for reliable diagnostic tools capable of early detection and continuous monitoring. The European Society of Cardiology (ESC) reports that an estimated 121 million people are living with cardiovascular disease across its member nations, signaling a massive population requiring continuous clinical management. Technological advancements have enabled noninvasive measurement techniques that reduce patient discomfort while maintaining diagnostic accuracy. Healthcare providers increasingly rely on quantitative flow data to guide surgical interventions and assess therapeutic efficacy in conditions such as arterial stenosis and venous insufficiency. The integration of artificial intelligence algorithms with imaging platforms further enhances the precision of flow quantification enabling clinicians to detect subtle abnormalities that might otherwise go unnoticed during conventional examinations.

MARKET DRIVERS

Rising Prevalence of Cardiovascular Disorders Drives Demand for Blood Flow Measurement Devices

The escalating incidence of cardiovascular diseases fuels the growth of the blood flow measurement devices market. Eurostat indicates that diseases of the circulatory system represent the leading cause of mortality in the European Union, accounting for approximately 33% of all recorded deaths. According to the European Heart Network (EHN), structural demographic shifts mean that over 60 million people in the European Union live with cardiovascular disease, maintaining a high volume of necessary diagnostic procedures. Peripheral artery disease affects nearly 12 percent of adults aged 65 years and older in developed nations as stated by the Journal of Vascular Surgery requiring regular monitoring through Doppler ultrasound and other flow measurement techniques. Stroke remains another critical concern with the European Stroke Organisation indicating that 1.1 million new stroke cases occur annually in Europe necessitating immediate cerebral blood flow assessment to determine appropriate intervention strategies. Data supported by the European Wound Management Association (EWMA) shows that poor systemic circulation leaves millions of European patients experiencing chronic wounds, driving a distinct medical niche for microcirculation flow testing devices. The aging demographic profile exacerbates this trend with the United Nations projecting that by 2050 nearly 30 percent of the European population will be aged 60 years or older a group particularly susceptible to vascular complications. Healthcare systems are consequently investing in advanced diagnostic infrastructure to manage this growing patient load effectively. Hospitals and specialized clinics are expanding their cardiovascular departments and purchasing state of the art flow measurement equipment to meet the rising diagnostic requirements. The correlation between disease prevalence and device utilization creates a sustained growth trajectory for manufacturers operating in this sector.

Technological Advancements in Noninvasive Diagnostic Methods Accelerate Market Expansion

Continuous innovation in noninvasive blood flow measurement technologies significantly propels the expansion of the global market. This offers superior diagnostic capabilities without compromising patient safety. The development of high resolution Doppler ultrasound systems with enhanced signal processing algorithms has revolutionized vascular diagnostics allowing clinicians to visualize blood flow patterns with unprecedented clarity. According to the European Federation of Societies for Ultrasound in Medicine and Biology modern ultrasound devices can detect flow velocities as low as 1 centimeter per second enabling early identification of vascular abnormalities before they progress to critical stages. Clinical research highlighted in the British Journal of Dermatology confirms that laser Doppler flowmetry offers a highly reliable, noninvasive method for evaluating skin microcirculation and predicting localized tissue healing outcomes. Magnetic resonance angiography techniques have evolved to provide three dimensional visualization of complex vascular networks without exposing patients to ionizing radiation as confirmed by the European Society of Radiology. The integration of artificial intelligence into these platforms enables automated flow quantification reducing operator dependency and minimizing interobserver variability. Strategic healthcare modernization frameworks backed by the European Commission encourage the integration of portable point-of-care ultrasound systems into community medicine to optimize initial patient triaging. Wireless connectivity features allow seamless data transfer to electronic health records facilitating comprehensive patient management. These technological improvements not only enhance diagnostic accuracy but also improve workflow efficiency making blood flow measurement more accessible across diverse healthcare settings. The continuous refinement of sensor technology and software algorithms ensures that these devices remain at the forefront of cardiovascular diagnostics.

MARKET RESTRAINTS

High Acquisition and Maintenance Costs Restrict Market Penetration in Resource Limited Settings

The substantial financial burden associated with purchasing and maintaining advanced devices is a major barrier to the blood flow measurement devices market. This trend is particularly visible in economically constrained healthcare environments. High end Doppler ultrasound systems equipped with sophisticated flow analysis capabilities typically cost between 50000 and 150000 euros according to pricing data from major medical equipment suppliers in Europe. This initial investment poses considerable challenges for smaller hospitals and outpatient clinics operating under tight budgetary constraints. Macroeconomic reviews compiled across Southern and Eastern European healthcare structures highlight that restrictive state reimbursement models and ongoing fiscal deficits regularly constrain hospitals from modernizing their specialized diagnostic imaging infrastructure. Maintenance contracts for these sophisticated devices often amount to 10 percent of the purchase price annually adding to the total cost of ownership over the device lifecycle. Operating sophisticated Doppler diagnostic equipment demands specialized personnel certifications, with professional masterclasses and vascular assessment modules hosted by organizations like the European Society for Vascular Surgery (ESVS) accumulating significant educational expenses per technician. Budget allocations for diagnostic imaging in many public healthcare systems have remained stagnant despite increasing patient volumes forcing administrators to prioritize essential services over advanced diagnostic tools. The economic downturn experienced by several European nations has exacerbated these financial constraints limiting the ability of healthcare providers to invest in cutting edge flow measurement technologies. Smaller private practices face similar challenges as they lack the economies of scale enjoyed by larger hospital networks. This financial barrier disproportionately affects rural and underserved communities where access to advanced vascular diagnostics remains limited. Consequently a significant portion of the potential patient population cannot benefit from timely and accurate blood flow assessments hindering early disease detection and optimal treatment outcomes.

Stringent Regulatory Compliance Requirements Delay Product Launches and Increase Development Expenses

Navigating the complex regulatory landscape for medical devices imposes substantial time and financial burdens on manufacturers seeking to introduce new technologies in the blood flow measurement devices market. The implementation of the Medical Device Regulation by the European Union has introduced more rigorous conformity assessment procedures requiring extensive clinical evidence and postmarket surveillance capabilities. According to the European Commission the average approval timeline for Class IIa and IIb medical devices has extended to 18 to 24 months compared to 12 months under the previous directive framework. This prolonged review process delays market entry and reduces the window for manufacturers to recoup their research and development investments. The heightened clinical evidentiary requirements imposed by modern European regulations can push the development and validation costs of novel diagnostic technologies into the multi-million euro range, straining smaller medical tech firms. The requirement for notified body involvement in the certification process has created bottlenecks due to limited capacity among designated authorities. A study highlights systemic capacity constraints and extensive review queues among European Notified Bodies, compounding delays for manufacturers seeking device certifications. Manufacturers must also maintain comprehensive technical documentation and quality management systems compliant with ISO 13485 standards which demands dedicated regulatory affairs personnel and ongoing compliance audits. Smaller companies with limited resources find these requirements particularly challenging as they lack the infrastructure to manage complex regulatory submissions efficiently. The uncertainty surrounding regulatory interpretations adds another layer of complexity forcing companies to engage multiple consultants and legal experts. These regulatory hurdles ultimately translate into higher product prices and reduced innovation incentives potentially limiting the diversity of available solutions in the market.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Machine Learning Creates New Diagnostic Possibilities

The convergence of artificial intelligence with blood flow measurement technologies opens unprecedented avenues for enhancing diagnostic precision and clinical decision making. This paves the way for the growth of the global blood flow measurement devices market. Machine learning algorithms can analyze vast quantities of hemodynamic data to identify subtle patterns indicative of early stage vascular disease that might escape human observation. The European Heart Journal ecosystem validates that integrating machine learning models with cardiac imaging enhances diagnostic sensitivity, boosting detection capabilities for advanced coronary conditions well beyond conventional manual interpretation. Deep learning models trained on extensive databases of vascular images can automatically segment blood vessels and calculate flow parameters with remarkable consistency reducing interoperator variability. The European Society of Cardiology shows that AI powered platforms can process ultrasound data in real time providing instantaneous feedback during examinations which streamlines workflow and improves patient throughput. Predictive analytics capabilities enable risk stratification by correlating flow measurements with patient history and genetic markers allowing for personalized treatment planning. Cloud based solutions facilitate collaborative diagnostics where specialists from different institutions can review and annotate flow studies remotely enhancing knowledge sharing and standardization of care. Under programs backed by the European Institute of Innovation and Technology (EIT Health), dozens of regional digital health startups are securing funding to develop AI-driven vascular and hemodynamic tracking systems. These innovations extend beyond traditional imaging to include wearable sensors that continuously monitor peripheral blood flow providing longitudinal data for chronic disease management. The integration of natural language processing enables automated report generation reducing administrative burden on clinicians. As computational power increases and algorithms become more sophisticated, the potential for AI to transform vascular diagnostics continues to expand. This offers new opportunities for manufacturers to differentiate their products through intelligent features.

Expansion of Telemedicine and Remote Patient Monitoring Drives Demand for Portable Devices

The rapid growth of telemedicine services and remote patient monitoring programs creates substantial opportunities for manufacturers of portable devices within the blood flow measurement devices market. The World Health Organization (WHO) Europe indicates that digital health and telemedicine consultations saw exponential growth in recent years, permanently embedding virtual triaging into regional medical systems. This transformation necessitates compact and user friendly diagnostic tools that patients or community healthcare workers can operate outside traditional clinical settings. The Lancet Digital Health literature confirms that pocket-sized, lightweight handheld Doppler systems allow for reliable point-of-care or home-monitored vascular evaluations when operated under proper training protocols. Remote monitoring programs for patients with chronic venous insufficiency and peripheral artery disease require regular flow measurements to track disease progression and treatment response. The European Telemedicine Association (EUTA) highlights that millions of Europeans are actively managed via remote health networks, creating a massive, receptive market for portable diagnostic hardware. Reimbursement policies in several European countries now cover remote monitoring services encouraging healthcare providers to invest in connected devices that transmit data directly to electronic health records. Bluetooth enabled flow meters allow seamless integration with smartphone applications providing patients with visual feedback and educational content about their vascular health. The convenience of home based testing reduces hospital visits and associated healthcare costs while empowering patients to take active roles in managing their conditions. Manufacturers are responding by developing intuitive interfaces and automated calibration features that minimize the technical expertise required for accurate measurements. This trend toward decentralized care delivery positions portable blood flow measurement devices as essential components of modern healthcare infrastructure.

MARKET CHALLENGES

Shortage of Trained Professionals Limits Effective Utilization of Advanced Devices

The scarcity of adequately trained healthcare professionals capable of operating sophisticated equipment is a persistent challenge to the blood flow measurement devices market. This shortage hinders optimal device utilization. Vascular sonography requires specialized skills and extensive experience to obtain accurate readings and interpret complex flow patterns correctly. The European Federation of Societies for Ultrasound in Medicine and Biology (EFSUMB) highlight that a persistent shortage of specialized sonography professionals across Europe continues to create operational bottlenecks for advanced diagnostic departments. Training programs for Doppler ultrasound and other flow measurement techniques typically require 12 to 18 months of supervised practice before practitioners achieve competency levels sufficient for independent operation. Research shows that structural shortages frequently force non-specialized clinical personnel to manage basic hemodynamic examinations, underscoring the value of highly automated diagnostic systems. This skills gap results in suboptimal image quality and inconsistent measurements compromising diagnostic reliability. Rural and underserved areas face acute shortages as qualified professionals prefer urban centers with better career prospects and resources. Long-term personnel assessments across European medical networks indicate that a substantial segment of the specialized health workforce is approaching retirement age, threatening to worsen existing clinical skill gaps. Educational institutions struggle to expand training capacities due to limited faculty and clinical placement opportunities. Healthcare organizations incur additional costs recruiting and retaining skilled personnel in a competitive labor market. Without adequate staffing advanced devices remain underutilized or produce unreliable results undermining their clinical value and return on investment. Addressing this workforce challenge requires coordinated efforts among educational institutions professional societies and healthcare providers to develop standardized training pathways and attract new entrants to the field.

Interoperability Issues Hinder Seamless Integration with Existing Healthcare Information Systems

The lack of standardized data formats and communication protocols creates significant interoperability issues when integrating these devices with hospital information systems and electronic health records, which in turn limits the expansion of the blood flow measurement devices market. Different manufacturers employ proprietary software architectures that do not readily communicate with each other or with broader healthcare IT infrastructure. EHTEL demonstrate that siloed legacy informatics platforms create data-sharing challenges, often requiring manual workarounds that lower operational speed. The absence of universal standards for hemodynamic data representation means that flow measurements obtained from one device may not be comparable with results from another system even when measuring the same physiological parameter. This inconsistency complicates longitudinal patient monitoring and multi center research initiatives where data harmonization is essential. Healthcare providers investing in digital transformation initiatives face unexpected costs customizing interfaces and developing middleware solutions to bridge compatibility gaps. The European Commission has identified interoperability as a key barrier to achieving a connected health ecosystem with estimates suggesting that incompatible systems reduce operational efficiency by up to 30 percent in diagnostic departments. Legacy equipment installed in many hospitals lacks modern connectivity features further compounding integration challenges. Upgrading these outdated systems requires substantial capital expenditure that many institutions cannot afford amidst competing priorities. The fragmentation of the technology landscape discourages adoption of advanced analytics and artificial intelligence tools that depend on aggregated data from multiple sources. Industry stakeholders recognize the need for standardized application programming interfaces and data exchange protocols but progress toward universal adoption remains slow due to competitive interests and technical complexities. Resolving these interoperability barriers is crucial for realizing the full potential of digital health innovations in vascular diagnostics.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Analysed | By Product, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Analysed | North America, Europe, Asia Pacific, Latin America, Middle East, and Africa |

| Market Leaders Profiled | Cook Medical, Inc., BIOPAC Systems, Inc., Atys Medical |

SEGMENTAL ANALYSIS

By Product Insights

In 2025, the ultrasound doppler technology segment held the majority share of the blood flow measurement devices market mainly because of its widespread clinical acceptance and noninvasive nature. The modality serves as the first line diagnostic tool for assessing vascular health across cardiology neurology and peripheral vascular departments. Clinical guidance from the European Society of Cardiology (ESC) positions Doppler ultrasound as a primary, frontline noninvasive imaging tool due to its real-time workflow efficiency and complete absence of ionizing radiation. The cost effectiveness of these systems compared to magnetic resonance imaging or computed tomography angiography makes them accessible to a broader range of healthcare facilities including outpatient clinics and primary care centers. Supported by clinical protocols from organizations like the American Institute of Ultrasound in Medicine (AIUM), noninvasive vascular ultrasound testing represents a massive procedural segment in the United States, driving high yearly device consumption. Technological advancements such as color flow mapping and power Doppler have enhanced the sensitivity of these devices allowing detection of low velocity flows in small vessels which is critical for early diagnosis of conditions like deep vein thrombosis. The portability of modern handheld Doppler units has further expanded their utility enabling point of care testing in emergency rooms and intensive care units. Training programs for sonographers are well established globally ensuring a steady supply of qualified operators which sustains high utilization rates. Reimbursement policies in major markets favor ultrasound based diagnostics due to their proven clinical value and lower procedural costs compared to invasive alternatives. This combination of clinical efficacy affordability and operational convenience solidifies the dominant position of Ultrasound Doppler in the global market landscape.

On the other hand, the laser doppler flowmetry segment is predicted to witness the highest CAGR of 9.2% over the forecast period. This accelerated growth of the segment is propelled by increasing applications in microcirculation assessment which is vital for managing chronic wounds burns and peripheral neuropathy. The World Health Organization (WHO) highlights that diabetes impacts more than 530 million people worldwide, severely expanding the patient population vulnerable to microvascular issues, tissue perfusion deficiencies, and subsequent limb amputations. Laser Doppler technology offers unique capabilities to measure blood flow in capillaries and small arterioles where conventional ultrasound cannot penetrate effectively. Research highlights that noninvasive microvascular blood flow assessments using laser Doppler imaging allow for early, objective evaluation of localized tissue perfusion and ulcer healing trajectories. The rising prevalence of cosmetic and reconstructive surgeries drives demand for intraoperative perfusion monitoring to ensure flap viability and reduce postoperative complications. The International Society of Aesthetic Plastic Surgery (ISAPS) track over 34 million cosmetic and reconstructive procedures annually, expanding clinical niches where microcirculatory monitoring tools ensure graft and flap viability. Advancements in laser source stability and signal processing algorithms have improved the reliability of these devices making them suitable for routine clinical use. Pharmaceutical companies also employ laser Doppler in clinical trials to evaluate the efficacy of vasoactive drugs creating additional demand. The ability to provide quantitative and continuous measurements of microvascular blood flow positions this technology as an indispensable tool in specialized medical fields driving its rapid adoption.

By Application Insights

The cardiovascular disease applications segment was the largest in the blood flow measurement devices market and occupied a significant share in 2025. This prominence of the segment was supported by the overwhelming prevalence of heart and vascular conditions worldwide. The massive disease burden necessitates extensive diagnostic infrastructure capable of detecting arterial stenosis valvular defects and heart failure with high precision. In addition, the European Heart Network (EHN) calculates that cardiovascular diseases impose an annual burden of €282 billion on European economies, reinforcing the priority for early diagnostic intervention tools. The Global Burden of Disease Study demonstrate that ischemic heart disease affects more than 240 million individuals worldwide, cementing blood flow analysis as a standard step in chronic cardiac evaluation. Doppler echocardiography remains the gold standard for assessing cardiac output and valve function providing critical data for surgical planning and medication management. The American Heart Association (AHA) notes that nearly half of all adults in the United States live with a cardiovascular condition, creating a massive demand for long-term diagnostic tracking and checkups. Aging populations in developed nations further amplify this demand as the risk of vascular disorders increases significantly after age 65. Guidelines from major cardiology societies mandate routine hemodynamic assessment for patients with hypertension diabetes and hyperlipidemia ensuring consistent utilization of flow measurement devices. The integration of these tools into standard care pathways for stroke prevention and heart failure management reinforces their central role in cardiovascular medicine. Healthcare systems prioritize procurement of advanced flow measurement equipment to meet screening targets and improve patient outcomes in this high priority therapeutic area.

However, the tumour monitoring applications segment is estimated to register the fastest CAGR of 8.7% between 2026 and 2034 owing to advancements in oncology and the need for precise treatment response assessment. Angiogenesis or the formation of new blood vessels is a hallmark of cancer progression making blood flow measurement a critical biomarker for tumor characterization and therapy evaluation. The International Agency for Research on Cancer projects that global cancer cases will rise to 29.9 million by 2040 increasing the demand for diagnostic tools that can monitor tumor vascularity noninvasively. Dynamic contrast enhanced magnetic resonance imaging and Doppler ultrasound are increasingly used to quantify tumor perfusion providing insights into treatment efficacy before anatomical changes become visible. The rise of personalized medicine necessitates detailed physiological data to tailor interventions to individual patient profiles enhancing the utility of flow measurement technologies. Pharmaceutical companies incorporate perfusion metrics into clinical trial endpoints accelerating regulatory approval for novel anticancer drugs. The European Society for Medical Oncology emphasizes the importance of functional imaging in monitoring metastatic disease where blood flow patterns indicate active tumor sites. Advances in software algorithms enable automated segmentation and quantification of tumor vasculature reducing observer variability and improving reproducibility. As immunotherapy and targeted therapies become more prevalent, the need for sensitive biomarkers like blood flow intensifies. Consequently, this drives the adoption of specialized measurement devices in oncology departments worldwide.

COUNTRY LEVEL ANALYSIS

North America Blood Flow Measurement Devices Market Analysis

North America led the global blood flow measurement devices market and held a 38.1% share in 2025. Its robust healthcare infrastructure and high adoption of advanced diagnostic technologies have contributed to the region's leading position. The region benefits from massive healthcare expenditure, with official data from the Centers for Medicare & Medicaid Services (CMS) showing that annual U.S. national health spending has surpassed $5.3 trillion, driving substantial procurement of advanced medical technologies. The presence of major market players such as GE Healthcare Siemens Healthineers and Philips headquartered in the region fosters innovation and rapid commercialization of new products. Joint clinical guidance from the American College of Cardiology (ACC) and American Heart Association (AHA) establishes noninvasive Doppler ultrasound as a gold-standard diagnostic tool for patients displaying symptoms of or possessing high-risk profiles for peripheral vascular disorders. High prevalence of lifestyle related diseases including obesity and diabetes contributes to elevated rates of cardiovascular complications requiring frequent hemodynamic assessment. The Food and Drug Administration maintains a streamlined regulatory pathway for medical devices encouraging manufacturers to introduce innovative solutions quickly. Reimbursement policies under private insurance and government programs provide financial coverage for diagnostic procedures ensuring accessibility for patients. Academic medical centers in the United States and Canada conduct extensive research on vascular diagnostics contributing to evidence based practices that support device utilization. The aging baby boomer population creates a growing demographic of patients susceptible to peripheral artery disease and stroke further sustaining market growth. Technological literacy among healthcare providers facilitates adoption of AI enhanced flow measurement systems positioning North America at the forefront of diagnostic innovation.

Europe Blood Flow Measurement Devices Market Analysis

Europe followed closely behind in the global blood flow measurement devices market and occupied a share of 30.3% in 2025. This growth of the European market was supported by universal healthcare systems and a rapidly aging demographic profile. The European Union mandates high standards for medical device safety and performance through the Medical Device Regulation ensuring quality and reliability of diagnostic equipment across member states. Countries such as Germany France and the United Kingdom invest heavily in public healthcare infrastructure enabling widespread access to diagnostic services including blood flow measurement. The aging population presents a significant driver as individuals over 65 years constitute more than 20 percent of the European population according to Eurostat data increasing the incidence of age related vascular disorders. National health services in many European countries cover comprehensive cardiovascular screening programs promoting early detection and management of conditions like abdominal aortic aneurysm. Collaborative research initiatives funded by the European Commission foster development of next generation flow measurement technologies enhancing regional competitiveness. The prevalence of smoking and sedentary lifestyles in certain Eastern European countries contributes to higher rates of peripheral artery disease driving demand for diagnostic tools in these emerging markets. Standardized training programs for vascular technologists ensure consistent quality of care across the region. Government initiatives to reduce healthcare disparities between urban and rural areas are expanding access to advanced diagnostic equipment in underserved communities.

Asia Pacific Blood Flow Measurement Devices Market Analysis

The Asia Pacific region is experiencing the highest growth rate in the blood flow measurement devices market, driven by rapid economic development expanding healthcare infrastructure and increasing awareness of cardiovascular health. Fueled by their massive populations and rising disposable incomes, China and India stand as the primary regional growth engines, anchoring the vast majority of medical service and diagnostic device demand across Asia-Pacific healthcare sectors. The American College of Cardiology (ACC) reveals that over half of all global cardiovascular disease deaths now occur in Asian nations, putting immense pressure on regional healthcare providers to upgrade diagnostic workflows. Governments in countries such as Japan South Korea and Australia are implementing national health insurance schemes that cover diagnostic procedures including vascular ultrasound enhancing patient access. The Chinese government has allocated substantial funds under its Healthy China 2030 initiative to upgrade hospital equipment and expand primary care facilities driving procurement of blood flow measurement devices. Rising prevalence of diabetes and hypertension in Southeast Asian nations creates urgent demand for early detection tools to prevent complications. Local manufacturing hubs in China and India are producing cost effective diagnostic equipment making these technologies more affordable for smaller clinics and rural health centers. The increasing number of medical tourism destinations in Thailand and Singapore attracts international patients seeking advanced vascular care boosting demand for state of the art flow measurement systems. Educational initiatives by professional societies are training more sonographers and technicians addressing the workforce shortage. Urbanization and lifestyle changes contribute to higher incidence of metabolic syndrome further fueling market expansion. Strategic partnerships between global manufacturers and local distributors facilitate market entry and penetration in diverse Asian markets.

Latin America Blood Flow Measurement Devices Market Analysis

Latin America shows moderate growth in the blood flow measurement devices market due to economic volatility and uneven healthcare access across countries. Brazil and Mexico dominate the regional market due to their larger economies and more developed healthcare systems compared to neighboring nations. The Pan American Health Organization reports that cardiovascular diseases are the leading cause of death in Latin America accounting for nearly 30 percent of all fatalities which drives baseline demand for diagnostic tools. Public healthcare systems in many countries face budget constraints limiting their ability to purchase advanced equipment while private hospitals in urban centers adopt newer technologies to attract affluent patients. Brazil's foundational Family Health Strategy primary care framework continuously strengthens preventive clinical screenings, channeling rising patient volumes into public diagnostic pathways for specialized vascular evaluations. Economic instability and currency fluctuations pose challenges for importing high end diagnostic equipment leading some healthcare providers to opt for refurbished or locally assembled units. Increasing awareness campaigns about stroke and heart attack symptoms are encouraging individuals to seek preventive checkups boosting outpatient diagnostic volumes. Private insurance penetration is growing in middle income segments enabling more patients to afford comprehensive vascular assessments. Manufacturers are adapting by offering flexible financing options and tiered product portfolios to accommodate varying purchasing powers. Regulatory harmonization efforts through regional bodies aim to streamline approval processes facilitating faster market entry for new devices. Despite challenges the underlying disease burden ensures steady demand for essential blood flow measurement technologies.

Middle East and Africa Blood Flow Measurement Devices Market Analysis

The Middle East and Africa region is expected to expand gradually in the global market from 2026 to 2034. It exhibits a fragmented market landscape with significant disparities between wealthy Gulf nations and lower income African countries. Countries such as Saudi Arabia the United Arab Emirates and Qatar drive demand in the Middle East through substantial healthcare investments and medical tourism initiatives. Driven by widespread national transformation frameworks, healthcare spending across the Gulf Cooperation Council (GCC) member states is projected to climb toward $159 billion, enabling aggressive procurement of state-of-the-art diagnostic and imaging systems. These nations aim to achieve world class healthcare standards attracting international patients and retaining local talent which necessitates state of the art infrastructure. In contrast many African nations struggle with limited healthcare resources and inadequate infrastructure restricting access to sophisticated diagnostic tools. The World Bank indicates that less than 50 percent of the population in sub Saharan Africa has access to essential health services limiting the market for advanced devices. However initiatives by international organizations and NGOs are improving diagnostic capabilities in select African hospitals focusing on maternal health and infectious disease complications that require blood flow assessment. South Africa and Egypt serve as regional hubs with more developed private healthcare sectors adopting modern technologies. Government visions such as Saudi Vision 2030 prioritize healthcare transformation driving digitalization and adoption of innovative diagnostic solutions. The prevalence of diabetes and hypertension in the Middle East creates a specific need for vascular monitoring tools. Manufacturers focus on premium segments in the Gulf while exploring affordable solutions for emerging African markets through public private partnerships.

COMPETITIVE LANDSCAPE

The competition in the blood flow measurement devices market is characterized by intense rivalry among established multinational corporations and emerging niche players who strive to differentiate through technological innovation and service excellence. Major competitors leverage their extensive research and development resources to introduce advanced features such as artificial intelligence driven analytics and portable designs that cater to diverse clinical environments. The market sees frequent product launches aimed at enhancing diagnostic accuracy and improving user experience which forces companies to continuously upgrade their offerings. Strategic alliances and partnerships are common as firms seek to combine expertise in imaging software hardware and data management to create integrated solutions. Price competition remains significant particularly in price sensitive regions prompting manufacturers to optimize production costs while maintaining quality standards. Regulatory hurdles and the need for clinical validation create barriers to entry yet also encourage higher quality standards across the industry. Customer loyalty is often determined by after sales support training programs and interoperability with existing hospital systems. As demand for noninvasive diagnostics grows companies must balance innovation with affordability to capture market share in both developed and developing economies ensuring sustained competitive positioning.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Global Blood Flow Measurement Devices Market include

- Cook Medical, Inc.

- BIOPAC Systems, Inc.

- Atys Medical

- SONOTEC Ultraschallsensorik Halle GmbH

- Moor Instruments Ltd.

- ADInstruments Pty Ltd.

- Deltex Medical Group plc

- Compumedics Limited

- Transonic Systems Inc.

- Perimed AB

- Medistim ASA

TOP LEADING PLAYERS IN THE MARKET

- GE Healthcare stands as a pivotal force in the blood flow measurement sector by leveraging its extensive portfolio of advanced ultrasound and imaging technologies. The company continuously innovates its Voluson and Vivid series which integrate artificial intelligence to enhance diagnostic precision for vascular assessments. Recent strategic initiatives include launching cloud based platforms that facilitate remote collaboration among clinicians thereby improving workflow efficiency. GE Healthcare actively partners with academic institutions to validate new algorithms for automated flow quantification ensuring clinical reliability. Their commitment to sustainability is evident in the development of energy efficient devices that reduce operational costs for healthcare facilities. By focusing on user centric design and seamless integration with electronic health records the company strengthens its position as a preferred provider for hospitals seeking comprehensive cardiovascular solutions. These efforts underscore their dedication to transforming patient care through technological excellence and global accessibility.

- Siemens Healthineers contributes significantly to the market through its robust lineup of magnetic resonance imaging and computed tomography systems equipped with sophisticated flow measurement capabilities. The company emphasizes digital health integration by offering AI powered tools that automate vessel segmentation and hemodynamic analysis reducing manual effort for radiologists. Recent actions include expanding its teamplay digital health platform which enables secure data sharing and collaborative diagnostics across multiple sites. Siemens Healthineers invests heavily in research and development to enhance image resolution and speed allowing for more accurate detection of subtle vascular abnormalities. They also prioritize training programs for healthcare professionals to ensure optimal utilization of their advanced technologies. By fostering partnerships with healthcare providers and technology firms the company drives innovation in personalized medicine. Their focus on precision diagnostics and operational efficiency solidifies their reputation as a leader in delivering high quality vascular assessment solutions globally.

- Philips maintains a strong presence in the blood flow measurement market by combining its expertise in ultrasound technology with intelligent informatics solutions. The company offers a wide range of portable and cart based ultrasound systems designed for diverse clinical settings from emergency rooms to specialized vascular labs. Recent strategies involve enhancing their Epic suite with machine learning algorithms that assist in real time flow visualization and quantification. Philips actively engages in collaborations with healthcare organizations to develop standardized protocols for vascular screening improving consistency in diagnosis. They also focus on sustainable design principles creating devices with longer lifecycles and reduced environmental impact. By prioritizing patient centered care and interoperability Philips ensures their devices integrate seamlessly into existing hospital infrastructure. Their commitment to innovation and global health equity drives continuous improvement in diagnostic accuracy and accessibility making them a key contributor to advancements in vascular health management worldwide.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the blood flow measurement devices market primarily focus on strategic partnerships and collaborations to expand their technological capabilities and geographic reach. Companies frequently engage in mergers and acquisitions to integrate complementary technologies such as artificial intelligence and cloud computing into their existing product portfolios. This approach allows them to offer more comprehensive solutions that address evolving clinical needs. Investment in research and development remains a critical strategy enabling firms to innovate faster and introduce advanced features like automated flow quantification and enhanced image resolution. Manufacturers also prioritize regulatory compliance and quality assurance to maintain trust and meet stringent international standards. Expanding into emerging markets through localized manufacturing and distribution networks helps companies capture growth opportunities in regions with increasing healthcare spending. Additionally providing extensive training and support services ensures proper device utilization and strengthens customer loyalty. These multifaceted strategies collectively drive competitive advantage and sustain long term growth in the dynamic medical device landscape.

GLOBAL BLOOD FLOW MEASUREMENT DEVICES MARKET NEWS

-

On May 31, 2017, Deltex Medical Group Plc announced its new patent that has received acceptance, a leader in Oesophageal Doppler Monitoring. The device filling covers the usage of Doppler measurements of blood flow, and that is measured using the oesophageal that is in co-occurrence with blood pressure signals. The Cardiac-ODM is used in patients during surgery to monitor and measure the blood flow. The ODM permits the doctors to step in quickly to do the changes in circulating blood volume.

-

On July 8, 2015, Compumedics Ltd. made a public statement that the brain blood-flow Doppler ultrasonography division, where the importance and impact can have business and trade and economic.

- On January 22, 2016, Medistim introduced a new product called MiraQ for the intraoperative quality of cardiac, vascular, and transplant surgery. This product is the fourth-generation device of Medistim. This Mira integrates both the ultrasound imaging quality and blood flow measurement. The system is very malleable and accessible that allows customers for customer application.

MARKET SEGMENTATION

This research report on the global blood flow measurement devices market has been segmented and sub-segmented based on the product, application, and region.

By Product

- Ultrasound

- Ultrasound Doppler

- Transit-Time Flow Meters

- Laser Doppler

By Application

- Non-Invasive Applications

- Cardiovascular Disease

- Diabetes

- Gastroenterology

- Tumour Monitoring

- Other Non-Invasive Applications

- Invasive Applications

- CABG

- Microvascular Surgery

- Other Invasive Application

By Region

- North America

- The United States

- Canada

- Rest of North America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Rest of EU

- Asia Pacific

- India

- China

- Japan

- Australia

- New Zealand

- South Korea

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Argentina

- Chile

- Rest of Latin America

- The Middle East and Africa

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com