Global Endodontics Market Size, Share, Trends & Growth Forecast Report By Instruments, Consumables, End User and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Global Endodontics Market Report Summary

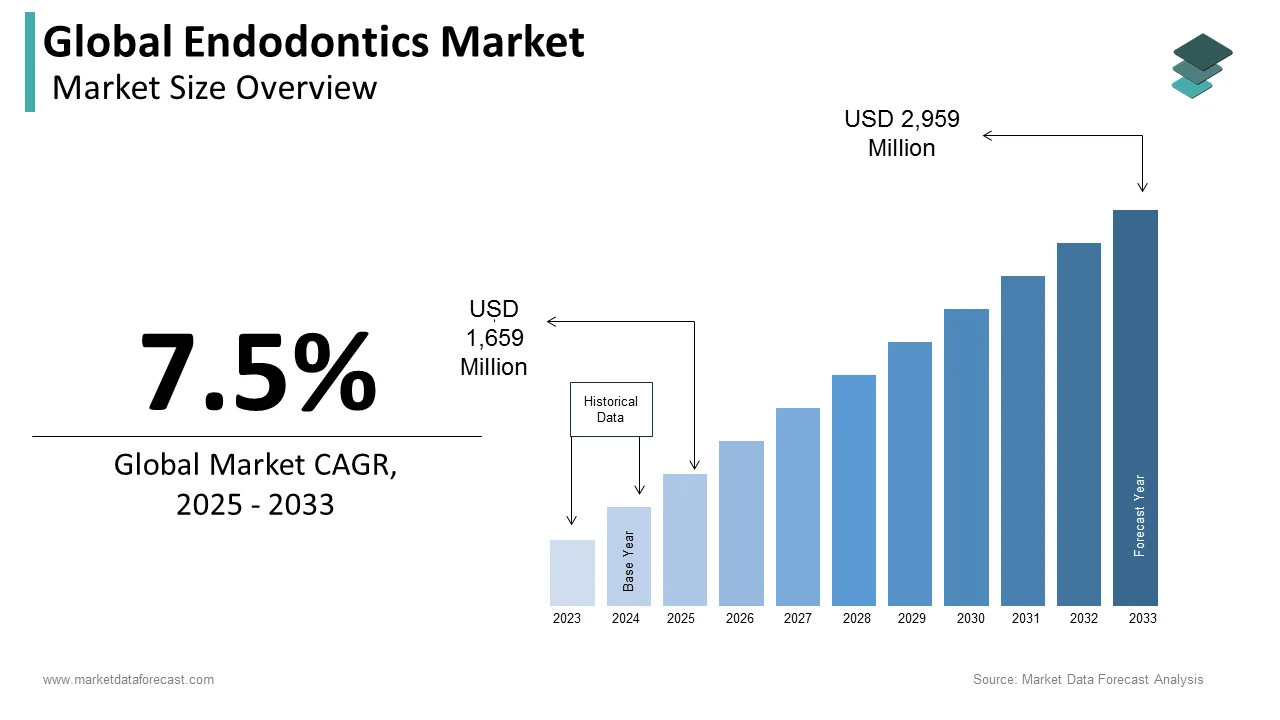

The global endodontics market was valued at USD 1,659 million in 2025, is estimated to reach USD 1,783.43 million in 2026, and is projected to reach USD 3,181 million by 2034, growing at a CAGR of 7.5% from 2026 to 2034. Market growth is driven by the increasing prevalence of dental disorders, rising demand for root canal treatments, and growing awareness of oral health. Technological advancements in endodontic instruments and materials, along with the expansion of dental clinics and cosmetic dentistry services, are further supporting market growth. Additionally, the rising adoption of minimally invasive dental procedures and improved treatment outcomes are contributing to market expansion globally.

Key Market Trends

- Increasing prevalence of dental diseases and root canal procedures.

- Growing demand for minimally invasive dental treatments.

- Advancements in endodontic instruments and materials.

- Expansion of dental clinics and specialty care centers.

- Rising awareness of oral hygiene and preventive care.

Segmental Insights

- Based on instruments, the motors segment dominated the global endodontics market by capturing 36.3% share in 2025, driven by their critical role in precision procedures.

- Based on consumables, the endodontic files segment led the market with 44.9% share in 2025, supported by their widespread use in root canal treatments.

- Based on end user, the clinics segment held the largest share of 74.7% in 2025, due to high patient inflow and specialized dental services.

Regional Insights

The global endodontics market is witnessing steady growth across major regions due to increasing dental care awareness and infrastructure.

- North America led the market in 2025 with 36.6% share, supported by advanced dental care systems and high treatment adoption.

- Europe holds a significant share, driven by strong healthcare systems and growing dental care awareness.

- Asia-Pacific is expected to grow at a notable rate due to rising dental healthcare infrastructure and increasing awareness in emerging economies.

Competitive Landscape

The global endodontics market is competitive, with leading dental product manufacturers focusing on innovation, product development, and expanding their global presence. Companies are investing in advanced materials, digital dentistry solutions, and ergonomic instruments to improve treatment efficiency and patient outcomes.

Prominent companies operating in the global endodontics market include Dentsply Sirona, Danaher Corporation, Ivoclar Vivadent, Ultradent Products, Septodont Holding, FKG Dentaire, Brasseler USA, MICRO-MEGA, DiaDent Group International, MANI, Coltene Holding, and VOCO.

Global Endodontics Market Size

The size of the global endodontics market was worth USD 1,659 million in 2025. The global market is anticipated to grow at a CAGR of 7.5% from 2026 to 2034 and be worth USD 3,181 million by 2034 from USD 1,783.43 million in 2026.

Endodontics encompasses a specialized sector of dentistry dedicated to the diagnosis, prevention, and treatment of diseases affecting the dental pulp and periapical tissues, primarily through root canal therapy and associated surgical procedures. This domain utilizes a sophisticated array of instruments, including rotary files, obturation systems, apex locators, and operating microscopes, to preserve natural dentition that would otherwise require extraction. The clinical imperative for these technologies stems from the high global prevalence of dental caries and pulpitis, which, if left untreated, lead to severe pain and systemic infection. According to the World Health Organization, dental caries remains the most common health condition globally, with untreated decay in permanent teeth representing a major burden. As per the Global Burden of Disease Study, oral diseases affect billions of individuals worldwide, which is creating a massive baseline demand for restorative interventions. In Europe, the European Commission notes that a majority of adults have experienced dental decay, driving the need for advanced endodontic solutions to save compromised teeth. As per the data from the American Dental Association, endodontists perform millions of root canal treatments annually in the United States, underscoring the procedure's centrality in modern oral healthcare. As the preference for tooth preservation over extraction grows among patients and clinicians, the reliance on precision endodontic technologies becomes increasingly critical for maintaining oral function and quality of life.

MARKET DRIVERS

Rising Global Prevalence of Dental Caries and Pulpal Diseases

The escalating global burden of dental caries and subsequent pulpal infections that need immediate therapeutic intervention to prevent tooth loss is one of the major factors propelling the growth of the global endodontics market. As sugar consumption increases and oral hygiene practices remain inconsistent in many populations, the incidence of deep cavities reaching the dental pulp has surged, which is making root canal therapy the standard of care for saving affected teeth. As per the World Health Organization, severe periodontal disease and untreated dental caries result in tooth loss for millions of people each year, with caries being the most prevalent noncommunicable disease worldwide. As per the National Institute of Dental and Craniofacial Research, a majority of adults in the United States have experienced cavities, and a significant portion progress to pulpitis requiring endodontic treatment. According to the data from the International Association for Dental Research, apical periodontitis affects a considerable share of the population in certain demographics, which is driving demand for both primary and retreatment procedures. Furthermore, the aging global population retains more natural teeth than previous generations, increasing the cumulative risk of pulp exposure due to wear, cracks, and recurrent decay. This demographic shift ensures a sustained and growing volume of cases where endodontic intervention is the only viable option to maintain dentition, thereby fuelling continuous demand for files, irrigants and sealing materials across all geographic regions.

Technological Advancements in Microscopic and Rotary Instrumentation

The rapid evolution of endodontic technology, specifically the widespread adoption of dental operating microscopes and nickel titanium rotary file systems that have revolutionized procedural success rates and efficiency is further contributing to the global endodontics market expansion. These innovations allow clinicians to visualize complex canal anatomies with magnification and illumination while navigating curved roots with flexible instruments that minimize the risk of file separation or canal transportation. As per the American Association of Endodontists, the use of dental operating microscopes has become the standard of care for specialists, enabling the detection of hidden canals and micro fractures that were previously undetectable. As per the Journal of Endodontics, studies demonstrate significantly higher treatment success rates when rotary instrumentation and microscopic visualization are employed compared to traditional manual techniques. As per the data from the European Society of Endodontology, cone beam computed tomography provides three dimensional imaging that allows for precise diagnosis and treatment planning, reducing procedural errors and enhancing patient outcomes. Furthermore, the development of heat treated nickel titanium alloys has improved the fatigue resistance of files, allowing for safer preparation of severely curved canals. These technological strides not only improve clinical efficacy but also reduce chair time and patient discomfort, making endodontic therapy a more attractive option for both practitioners and patients and thus accelerating market growth.

MARKET RESTRAINTS

High Cost of Advanced Endodontic Procedures and Limited Reimbursement

The substantial out of pocket cost associated with sophisticated procedures and the inconsistent coverage provided by insurance plans globally is one of the major impediments to the global endodontics market growth. Root canal therapy, especially when performed by specialists using microscopes and advanced imaging, commands a premium price that many patients cannot afford without adequate financial support. As per the Kaiser Family Foundation, dental insurance coverage often includes annual maximums that are insufficient to cover the full cost of complex endodontic work combined with necessary crown restoration, which is forcing patients to opt for extraction instead. As per the World Health Organization, oral health services in many low and middle income countries are largely paid for out of pocket, with a majority of the global population lacking access to essential dental care due to financial barriers. According to the data from the American Dental Association, the average cost of a molar root canal followed by a crown can be prohibitive for uninsured or underinsured individuals. Furthermore, public health systems in Europe and other regions frequently prioritize emergency extractions over costly restorative endodontics due to budget constraints, which is limiting the addressable market for high end devices. This economic disparity forces a significant number of patients to choose tooth extraction as a cheaper alternative, directly suppressing the demand for endodontic consumables and equipment despite the clear long term benefits of tooth preservation.

Shortage of Specialized Endodontists and Technical Expertise

The acute scarcity of trained endodontic specialists and the steep learning curve associated with mastering advanced endodontic techniques is a significant bottleneck to market expansion. While general dentists perform a large volume of root canals, complex cases involving calcified canals, resorption, or retreatment require the specialized skills of an endodontist, whose numbers are insufficient to meet global demand. As per the American Association of Endodontists, there are only a limited number of board certified endodontists in the United States, leaving vast geographic areas underserved. The European Society of Endodontology reports similar disparities across Europe, where specialists are concentrated in urban centers, leaving rural populations with limited access to high quality care. As per the World Health Organization, the training required to proficiently use operating microscopes and rotary systems is extensive, and many general practitioners lack the confidence or resources to invest in such advanced training and equipment. Furthermore, the physical demands of endodontic procedures contribute to practitioner burnout and early retirement, further exacerbating the workforce shortage. Without a sufficient cadre of skilled professionals to perform these intricate procedures, the utilization of advanced endodontic products remains capped, restricting market growth to regions with adequate specialist density and limiting the overall penetration of sophisticated technologies in broader dental practice.

MARKET OPPORTUNITIES

Integration of Regenerative Endodontics and Biologic Therapies

The emergence of regenerative endodontics offers a promising opportunity in the endodontics market. This innovative approach utilizes biologic scaffolds, growth factors, and stem cells to regenerate the pulp dentin complex, offering potential cures for conditions that previously had limited options. As per the National Institute of Dental and Craniofacial Research, regenerative procedures have shown promising results in restoring root development and vitality in young patients with open apices. The American Association of Endodontists has established guidelines for regenerative procedures, which is signalling a shift in clinical paradigms that will drive demand for specialized biologics and delivery systems. Data from the Journal of Endodontics indicates that clinical trials have demonstrated successful revascularization in a majority of treated cases, encouraging wider adoption among pediatric dentists and endodontists. Furthermore, the growing interest in stem cell therapy for adult teeth suggests a future market for bioactive materials that can stimulate healing and reverse pulpitis before necrosis occurs. As research advances and regulatory approvals expand, the endodontics market will see new revenue streams driven by regenerative kits and therapies that offer superior biological outcomes compared to conventional inert filling materials.

Expansion of Digital Dentistry and AI Driven Diagnostic Tools

The rapid integration of digital dentistry workflows and artificial intelligence into endodontic practice offers substantial growth potential by enhancing diagnostic accuracy, treatment planning, and procedural precision. Digital tools such as AI enhanced radiographic analysis and dynamic navigation systems allow clinicians to detect pathology earlier and navigate complex root canal systems with unprecedented accuracy. As per the American Dental Association, adoption of digital imaging and computer aided design technologies in dentistry is growing at strong rates, with endodontics being a key beneficiary. The International Journal of Computerized Dentistry reports that AI algorithms can now identify periapical lesions and calculate canal curvature with accuracy comparable to human experts, facilitating earlier intervention and better case selection. Industry data suggests that the global market for digital dentistry is projected to expand significantly, driven by demand for streamlined workflows and improved patient communication. Furthermore, the integration of cone beam computed tomography with intraoral scanners enables creation of surgical guides for microsurgery, reducing operative time and improving predictability. By leveraging these digital capabilities, practitioners can offer higher value services, attract tech savvy patients, and optimize clinical efficiency, which is creating robust demand for software, sensors, and connected endodontic devices.

MARKET CHALLENGES

Complexity of Canal Anatomy and Risk of Procedural Failure

The inherent complexity of root canal anatomy that varies significantly between individuals and teeth, which is leading to risks of missed canals, instrument separation, and treatment failure is one of the major challenges to the growth of the global market. Human dentition presents intricate variations such as C shaped canals, lateral canals, and apical deltas that are difficult to clean and shape thoroughly, even with advanced technology. As per the Journal of Endodontics, studies indicate that a considerable proportion of root canal treated teeth may harbour untreated canals or residual bacteria, which can lead to persistent infection and eventual failure. The European Society of Endodontology highlights that the risk of file fracture increases in severely curved or calcified canals, potentially complicating the procedure and necessitating surgical intervention or extraction. Data from clinical audits shows that retreatment rates remain significant, with a notable percentage of therapies requiring revision due to inadequate initial cleaning or sealing. Furthermore, the inability to completely eliminate biofilm from complex isthmus areas of the root canal system poses a continuous microbiological challenge that limits long term success. This anatomical unpredictability demands constant innovation in instrument design and irrigation techniques, yet the risk of complications remains a deterrent for some practitioners and a source of liability, which is hindering universal acceptance of endodontic therapy as a foolproof solution.

Infection Control Concerns and Sterilization Protocols

The stringent requirements for infection control and the complexities associated with sterilizing reusable endodontic instruments are also challenging the expansion of the endodontics market. Endodontic files and reamers possess intricate geometries that are difficult to clean thoroughly, raising concerns about cross contamination and pathogen transmission. As per the Centers for Disease Control and Prevention, dental settings must adhere to rigorous sterilization protocols, yet studies have shown that residual organic debris can persist on reused nickel titanium files even after autoclaving. The World Health Organization emphasizes the importance of preventing prion disease transmission, which has led some health authorities to recommend single use policies for certain instruments, thereby increasing operational costs for clinics. For instance, validating sterilization processes for complex dental instruments requires specialized equipment and monitoring, which is adding to overhead expenses. Furthermore, the environmental impact of disposing of large volumes of single use metal instruments is becoming a growing concern, creating a dilemma between safety and sustainability. Balancing the need for absolute sterility with economic feasibility and environmental responsibility remains a complex challenge that influences purchasing decisions and protocol adherence across the global endodontics market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Instruments, Consumables, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | DENTSPLY SIRONA (US), Danaher Corporation (US), Ivoclar Vivadent (Liechtenstein), Ultradent Products (US), Septodont Holding (France), FKG Dentaire (Switzerland), Brasseler USA (US), MICRO-MEGA (France), DiaDent Group International (Canada), MANI (Japan), COLTENE Holding (Switzerland), and VOCO (Germany). |

SEGMENTAL ANALYSIS

By Instruments Insights

The motors segment dominated the market by commanding for 36.3% of the global market share in 2025. The dominance of motors segment in this market is attributed to the necessity of electric or air-driven motors to power rotary and reciprocating file systems, which have become the standard of care for efficient root canal preparation worldwide. The complete shift in clinical practice from manual hand filing to mechanized rotary instrumentation that require a dedicated motor unit for every operatory performing endodontics is further contributing to the expansion of the motors segment in the global market. Manual preparation is increasingly viewed as obsolete due to its time-consuming nature and higher risk of procedural errors. As per the American Association of Endodontists, a majority of specialists and general dentists now utilize nickel titanium rotary files that require torque-controlled motors to operate safely. The European Society of Endodontology emphasizes that modern dental curricula mandate training on rotary systems, ensuring new graduates enter the workforce requiring a motor. Data from the Journal of Endodontics indicates that rotary preparation reduces chair time significantly compared to manual techniques, a critical efficiency metric for high-volume practices. Furthermore, the longevity of these devices means they are replaced less frequently than consumables, but the sheer volume of installations across millions of clinics worldwide creates a massive installed base. As the global number of practicing dentists increases, demand for motors scales linearly, solidifying this segment as the financial backbone of the instruments category.

On the other hand, the laser segment is a promising segment and is estimated to witness a CAGR of 10.5% over the forecast period in the global market owing to the increasing adoption of laser-assisted disinfection protocols that address the challenge of eliminating bacteria from complex root canal systems where traditional irrigation cannot reach. The proven efficacy of laser energy in eradicating biofilms and bacteria from lateral canals, isthmuses, and dentinal tubules is further contributing to the expansion of the laser segment in the global market. As per the Journal of Endodontics, studies using erbium-doped yttrium aluminum garnet lasers demonstrate significantly higher bacterial reduction compared to standard irrigation techniques. The American Association of Endodontists notes that laser activation of irrigants enhances cleaning power through acoustic streaming and cavitation effects, improving success rates in retreatment cases. Data from the European Society of Endodontology highlights that lasers have moved from experimental to mainstream, with clinical guidelines increasingly recognizing their value in managing resistant infections. Furthermore, lasers can seal dentinal tubules immediately after cleaning, reducing post-operative sensitivity and improving patient comfort. As evidence mounts regarding superior microbiological outcomes, more clinics are investing in these systems to differentiate services and improve long-term treatment predictability.

By Consumables Insights

The endodontic files segment held the dominant position in the global market by holding 44.9% of the worldwide market share in 2025. The growth of the endodontic files segment in the global market is attributed to the fact that files are the primary working instruments used in every root canal procedure and are predominantly designed for single use to ensure safety and efficacy. The universal adoption of single-use protocols mandated by infection control guidelines and manufacturer recommendations is further aiding the dominance of endodontic files segment in the global market. Nickel titanium files undergo significant stress during canal shaping, making reuse dangerous due to fracture risks. As per the Centers for Disease Control and Prevention, strict sterilization guidelines and the difficulty of cleaning complex file geometries have led dental associations to recommend disposable usage. The American Dental Association notes that millions of root canal treatments are performed annually in the United States, each requiring multiple files, creating massive recurring demand. Data from the European Centre for Disease Prevention and Control reinforces that reusing rotary files is a liability risk, prompting clinics to adhere to one-patient-one-file policies. With rising prevalence of dental caries and increasing dentist numbers globally, procedure volumes continue to climb, multiplying file consumption. Since files cannot be economized through reuse without compromising outcomes, they represent the highest volume consumable item in endodontics, which is securing their leadership.

However, the obturation segment is anticipated to witness the fastest growth and register a CAGR of 9.7% over the forecast period owing to the shift toward warm vertical compaction techniques and the development of bioactive sealing materials that offer superior hermetic seals and biological compatibility. The widespread transition from cold lateral condensation to warm vertical compaction methods is further fuelling the expansion of the obturation segment in the global market. These techniques require specialized consumables such as heated gutta-percha carriers, injectable thermoplasticized gutta-percha, and bioceramic sealers. Warm techniques provide a more homogeneous fill of the root canal system, adapting better to complex anatomies and reducing voids. As per the American Association of Endodontists, warm vertical compaction is now considered the gold standard, with adoption rates among specialists exceeding 80%. According to the European Society of Endodontology, clinical studies show lower leakage rates with warm obturation compared to cold techniques, driving general practitioners to adopt advanced kits. As per the data from the Journal of Endodontics, carrier-based gutta-percha systems have seen rapid growth as clinicians seek faster and more predictable filling methods. Furthermore, integration of obturation guns and heating devices into routine practice necessitates constant supply of compatible refills, creating a recurring revenue model. As training programs increasingly emphasize these advanced techniques, demand for specific consumables surges and propelling this segment to the forefront of market growth.

By End User Insights

The clinics segment led the market by capturing the highest share of 74.7% of the global market in 2025 due to the fact that the vast majority of root canal treatments are performed in private dental practices and specialized endodontic offices rather than hospital settings, due to the outpatient nature of the procedure. The overwhelming preference for performing endodontic therapy in an outpatient setting, which is more cost-effective, convenient for patients, and logistically simpler than hospital admission is further supporting the dominance of clinics segment in the global market. Root canal treatment is typically a chairside procedure that does not require general anesthesia or overnight monitoring, making private clinics the ideal environment for delivery. As per the American Dental Association, the majority of endodontic procedures in the United States are conducted in private practices, ranging from general dentist offices to specialized endodontic clinics. The European Commission reports similar trends across Europe, where national health systems encourage community-based dental care to reduce the burden on hospital emergency departments. According to the data from the World Health Organization indicates that decentralization of oral health services is a global priority, with governments investing in primary care dental facilities to improve access. Furthermore, the rise of corporate dental chains and group practices has consolidated purchasing power, leading to bulk procurement of endodontic supplies that further entrenches the clinic sector’s dominance. The ability of clinics to offer flexible scheduling and personalized care attracts the majority of patients, ensuring that the volume of procedures remains heavily skewed toward this setting.

On the other side, the hospitals segment is projected to grow at the highest CAGR of 7.4% over the forecast period in the global market. The growing incidence of dental trauma emergencies, the rise of medically compromised patients requiring hospital-based care, and the expansion of public health dental programs in developing regions are driving the expansion of the hospitals segment in the global market. The increasing volume of dental trauma cases and acute infections that present as emergencies is further boosting the expansion of hospitals segment in the global market. Accidents, sports injuries, and severe facial trauma frequently result in tooth avulsion or fracture that necessitates urgent endodontic stabilization, which is often managed in hospital emergency departments or oral surgery units. As per the Centers for Disease Control and Prevention, dental trauma accounts for a significant portion of emergency room visits related to oral health globally. The World Health Organization highlights that in many low and middle-income countries, hospitals serve as the primary point of care for acute dental conditions due to the lack of widespread private clinic infrastructure. Data from the Journal of Endodontics indicates that complex cases involving maxillofacial fractures or patients with systemic comorbidities are increasingly being routed to hospitals for multidisciplinary management. Furthermore, the growing awareness of the link between oral infection and systemic health issues like sepsis drives hospitals to prioritize immediate endodontic intervention for severe abscesses. As emergency preparedness and trauma care capabilities expand globally, the role of hospitals in delivering urgent endodontic services grows, driving demand for hospital-grade endodontic supplies.

REGIONAL ANALYSIS

North America Endodontics Market Analysis

North America dominated the endodontics market in 2025 with 36.6% of the global market share. The dominance of North America in the global market is attributed to advanced healthcare infrastructure, a high density of endodontic specialists, and strong reimbursement frameworks that support premium technologies. The United States serves as the primary engine, driven by a culture of tooth preservation and high awareness of oral health aesthetics. As per the American Dental Association, there are hundreds of thousands of active dentists in the US, with a significant proportion specializing in or regularly performing endodontics using state-of-the-art microscopes and rotary systems. The presence of major market players and leading research institutions fosters innovation and rapid technology adoption. Data from the Centers for Medicare and Medicaid Services indicates that while dental coverage varies, high out-of-pocket spending capacity supports the use of advanced procedures. Stringent infection control regulations mandate single-use protocols, driving consumable volumes. Early adoption of digital dentistry and AI-driven diagnostics further solidifies North America’s position as the most mature and lucrative market globally.

Europe Endodontics Market Analysis

Europe occupied a promising share of the global endodontics market in 2025. Europe emphasizes standardized clinical guidelines and universal healthcare systems that ensure broad access to dental care. Western European countries such as Germany, France, and the UK lead in penetration rates, with national health services prioritizing restorative dentistry. As per the European Society of Endodontology, Europe has pioneered rigorous quality standards for training and practice, ensuring high success rates and consistent demand. The implementation of the Medical Device Regulation has harmonized safety standards across member states, boosting confidence in devices. Data from the European Commission highlights that an aging population retaining more natural teeth is driving demand for root canal treatments and retreatments. Europe also benefits from a strong manufacturing base for dental instruments, fostering local innovation and competitive pricing. Digital integration in dental practices across Scandinavia and Central Europe is improving efficiency and access to advanced care. Despite economic variations, the commitment to oral health sustains steady growth and scientific advancement.

Asia Pacific Endodontics Market Analysis

Asia Pacific is anticipated to account for a prominent share of the global market during the forecast period. The region is transitioning from extraction-based care to sophisticated tooth-preserving endodontics, driven by improving healthcare access, rising disposable incomes, and dental tourism. China and India are key contributors, with massive populations and rising urbanization leading to higher incidences of dental caries and demand for restorative solutions. As per the World Health Organization, untreated dental caries remain highly prevalent, creating a vast untapped market for interventions. Government initiatives in Japan, South Korea, and Australia are investing in dental infrastructure and insurance coverage, making treatment more affordable. Data from the Asian Development Bank highlights improvements in dental graduates and specialized training programs, addressing workforce shortages. Private dental chains and adoption of international quality standards are driving uptake of advanced rotary systems and bioceramic materials. Local manufacturing of cost-effective instruments balances imports with domestic production. These demographic, economic, and policy shifts position Asia Pacific as the next frontier for expansion.

Latin America Endodontics Market Analysis

Latin America represents a developing yet promising segment. The market in this region is characterized by advanced private clinics in urban centers and limited access in rural areas, though the gap is narrowing. Brazil and Mexico dominate, fueled by large populations and a strong culture of aesthetic dentistry that prioritizes saving natural teeth. As per the Pan American Health Organization, oral diseases are a public health priority, prompting ministries to strengthen dental networks. Rising prevalence of caries due to dietary changes is stimulating demand in both public and private sectors. Data from the Inter-American Development Bank indicates steady increases in healthcare spending, correlating with higher adoption of advanced technologies. Expansion of international dental chains and partnerships with global manufacturers is improving product availability and practitioner education. While cost sensitivity and fragmented systems remain challenges, the growing middle class and focus on oral health provide a foundation for steady growth.

Middle East and Africa Endodontics Market Analysis

The Middle East and Africa is representing a nascent but evolving landscape with untapped potential. Market activity is concentrated in Gulf Cooperation Council countries such as Saudi Arabia and the UAE, where high healthcare expenditure and government vision plans support device adoption. As per the World Health Organization, dental disease prevalence is high in the Middle East, driven by sugar consumption and limited preventive care. In Africa, access remains limited, but urbanization and private healthcare growth in nations like South Africa, Nigeria, and Kenya are opening new avenues. Data from the African Development Bank shows increasing investment in health infrastructure, improving distribution networks for dental supplies. Specialized dental centers and national oral health strategies are fostering market development. International aid and collaborations with global organizations are introducing affordable solutions and training programs in resource-limited settings. Although the overall share is small, rising disease burden, young demographics, and improving economic conditions suggest gradual but meaningful expansion in the coming years.

COMPETITIVE LANDSCAPE

The competition within the endodontics market is intense and characterized by the presence of several large multinational corporations alongside numerous specialized niche players striving for technological superiority. Major companies compete vigorously by leveraging their extensive research and development capabilities to introduce innovative file alloys and bioceramic sealers that offer superior flexibility and sealing ability. The landscape is further complicated by the critical importance of clinical evidence which forces manufacturers to conduct rigorous studies proving that their devices reduce procedure time and improve long term success rates. Brand loyalty plays a significant role as dentists prefer established vendors who provide reliable instruments and comprehensive training support to minimize procedural failures. Price competition exists but is often secondary to the value provided by proven clinical efficacy and robust after sales service agreements. The emergence of digital dentistry has introduced a new dimension to rivalry as firms race to develop platforms that integrate cone beam computed tomography with robotic assistance. Smaller entities often focus on specific applications such as regenerative endodontics or novel irrigation methods to carve out distinct market segments before potentially being acquired by larger conglomerates seeking to diversify their offerings. This dynamic environment necessitates continuous innovation and strategic agility to sustain long term success.

KEY MARKET PARTICIPANTS

Some of the notable companies operating in the global endodontics market profiled in the report are

- Dentsply Sirona (US)

- Danaher Corporation (US)

- Ivoclar Vivadent (Liechtenstein)

- Ultradent Products (US)

- Septodont Holding (France)

- FKG Dentaire (Switzerland)

- Brasseler USA (US)

- MICRO-MEGA (France)

- DiaDent Group International (Canada)

- MANI (Japan)

- Coltene Holding (Switzerland)

- VOCO (Germany)

TOP PLAYERS IN THE MARKET

- Dentsply Sirona Inc stands as a preeminent global leader in the endodontics sector offering a comprehensive portfolio that spans rotary files obturation systems and advanced imaging technologies. The company significantly contributes to the market by driving innovation through its WaveOne and ProTaper file systems which have set industry standards for efficiency and safety. Recent actions to strengthen its position include the integration of artificial intelligence into its imaging platforms to enhance diagnostic accuracy for root canal therapies. Dentsply Sirona has also expanded its educational initiatives globally to train dentists on the latest minimally invasive techniques. By focusing on digital workflow integration the firm ensures seamless connectivity between diagnosis and treatment. These strategic efforts reinforce its commitment to improving clinical outcomes and solidify its reputation as a trusted partner for dental professionals seeking cutting edge endodontic solutions worldwide.

- Coltene Holding AG operates as a vital force in the endodontics landscape leveraging its strong heritage in precision Swiss manufacturing to deliver high quality instruments and consumables. The company plays a crucial role in the global market by supplying reliable nickel titanium files and bioceramic sealers that cater to both specialists and general practitioners. Recent efforts to bolster its market stance involve the launch of next generation heat treated file systems designed to withstand extreme curvature without fracture. Coltene has also focused on expanding its distribution network in emerging markets to increase accessibility of its premium products. Furthermore the company actively engages in clinical research partnerships to validate the efficacy of its new biomaterials. By prioritizing product durability and clinical performance Coltene appeals to discerning clinicians who demand consistency. These initiatives demonstrate its dedication to advancing endodontic care through superior engineering and robust scientific validation across diverse international markets.

- Ultradent Products Inc is a key participant known for its innovative approach to endodontic disinfection and obturation materials including its renowned UltraCal and RealSeal product lines. The company contributes substantially to the global market by providing specialized solutions that address complex challenges such as biofilm removal and hermetic sealing. Recent actions to enhance its competitive position include the development of advanced activation devices that improve irrigant penetration into intricate canal anatomies. Ultradent has also strengthened its presence by launching comprehensive training centers dedicated to teaching modern endodontic protocols. Additionally the firm invests heavily in research to create bioactive materials that promote periapical healing. By focusing on solving specific clinical pain points Ultradent addresses the evolving needs of endodontists. These strategic developments underscore its commitment to elevating the standard of care through specialized products and extensive professional education programs globally.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the endodontics market primarily employ strategic acquisitions and product innovation to expand their portfolios and capture emerging opportunities. Companies frequently acquire niche startups specializing in bioceramic materials or digital imaging to integrate advanced technologies into their existing ecosystems rapidly. Another major strategy involves heavy investment in continuous education and training programs to ensure clinicians are proficient in using new rotary systems and microscopic techniques. Manufacturers also focus on developing single use disposable instruments to align with stringent infection control guidelines and reduce cross contamination risks. Expanding into high growth regions like Asia Pacific through localized distribution partnerships helps firms tap into rising demand for restorative dentistry. Additionally participants are increasingly adopting digital workflows that connect diagnostic imaging directly to treatment planning software. These combined approaches enable companies to maintain competitive advantages and drive sustained adoption of advanced endodontic solutions in a rapidly evolving industry landscape.

MARKET SEGMENTATION

This research report on the global endodontics market has been segmented and sub-segmented into the following categories and calculated market size and forecast for each segment until 2033.

By Instruments

-

Scalers

-

Apex Locator

-

Motors

-

Handpiece

-

Laser

By Consumables

-

Access Cavity Preparation

-

Endodontic Files

-

Burs

-

Drill

-

Lubricant

-

Obturation

By End User

-

Clinics

-

Hospitals

By Region

-

North America

-

Europe

-

Asia-Pacific

-

Latin America

-

The Middle East and Africa

Frequently Asked Questions

1. What drives growth in the global endodontics market?

Increasing dental caries, rising dental tourism, and advancements in rotary instruments drive growth in the global endodontics market

2. Which regions dominate the global endodontics market?

North America and Europe hold leading shares, while Asia Pacific presents rapid growth opportunities in the global endodontics market

3. What are key product types in the global endodontics market?

Instruments, consumables like sealers and irrigants, and bioceramic materials are vital segments in the global endodontics market

4. How do technological innovations impact the global endodontics market?

Advances in 3D imaging, rotary tools, and biocompatible materials improve treatment accuracy, boosting the global endodontics market

5. What role does dental tourism play in the global endodontics market?

Affordable and quality endodontic care attracts international patients, supporting growth in the global endodontics market

6. How do dental infections influence the global endodontics market?

High prevalence of dental infections and decay increases demand for root canal treatments in the global endodontics market

7. What are common end-user segments in the global endodontics market?

Dental hospitals, clinics, and specialty endodontic centers are primary end users in the global endodontics market

8. How important are bioceramic materials in the global endodontics market?

Bioceramics offer superior sealing and biocompatibility, enhancing endodontic treatment outcomes in the global endodontics market

9. What challenges exist in the global endodontics market?

High costs, lack of skilled practitioners, and stringent regulations challenge growth in the global endodontics market

10. How does aging population affect the global endodontics market?

An aging population increases dental issues requiring endodontic interventions, expanding the global endodontics market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com