Global Graphic Processing Unit (GPU) Market Size, Share, Trends & Growth Forecast Report – Segmented By Type (Dedicated or Discrete, Integrated, Hybrid), Application, Industry and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis From 2025 to 2033

Global Graphic Processing Unit (GPU) Market Summary

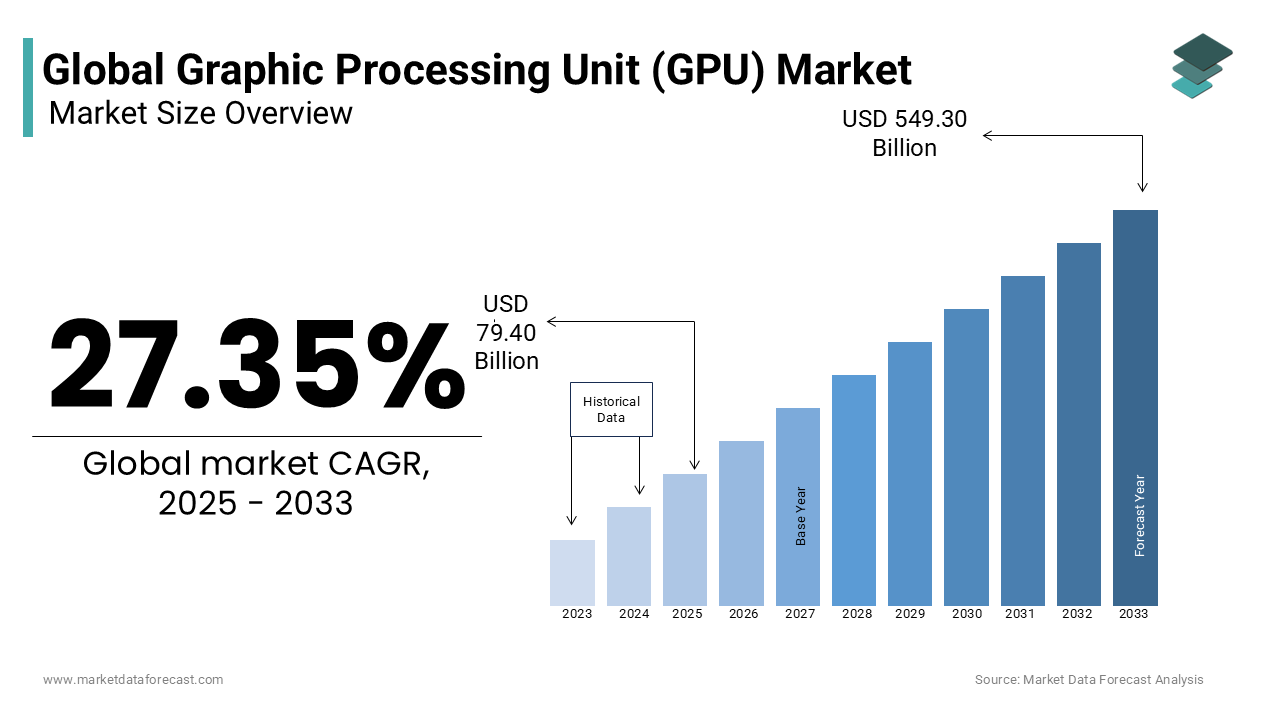

The global graphic processing unit (GPU) market was valued at USD 62.35 billion in 2024, is projected to reach USD 79.40 billion in 2025, and is expected to surge to USD 549.30 billion by 2033, expanding at a CAGR of 27.35% from 2025 to 2033. The rapid market expansion is fueled by the widespread adoption of artificial intelligence (AI), machine learning (ML), high-performance computing (HPC), and gaming applications, alongside the growing demand for GPUs in data centers and edge devices.

Key Market Trends

- Rising deployment of GPUs in AI/ML and deep learning workloads.

- Expansion of cloud gaming and AR/VR applications driving demand for advanced GPUs.

- Growth in autonomous vehicles and robotics, requiring real-time parallel processing.

- Increased use of GPUs in blockchain and cryptocurrency mining.

Segmental Insights

- Based on type, the dedicated (discrete) GPU segment dominated the market in 2024, driven by high demand from gaming, data centers, and professional visualization applications.

- Based on application, the machine learning and artificial intelligence (AI/ML) segment held a prominent share in 2024, reflecting the rising integration of GPUs in AI model training and inference.

- Based on industry, the IT & telecommunication sector led the market with a 45.3% share in 2024, supported by rising cloud computing workloads and 5G expansion.

Regional Insights

- North America led the global GPU market, accounting for 46.2% of the share in 2024, driven by strong AI adoption, gaming culture, and major GPU manufacturers.

- Asia-Pacific is projected to witness rapid growth, supported by large-scale electronics manufacturing, booming gaming industries, and government-backed AI initiatives.

- Europe is experiencing steady demand, particularly in automotive, AI research, and industrial automation.

- Latin America is gradually adopting GPUs with the rise of eSports and digital transformation initiatives.

- Middle East & Africa are emerging markets, driven by investments in smart city projects and advanced IT infrastructure.

Competitive Landscape

Key players in the global GPU market include NVIDIA, AMD, Intel, Qualcomm, ARM, Imagination Technologies, Samsung Electronics, Apple, ZOTAC, and Sapphire. These companies are focusing on next-generation GPU architectures, strategic partnerships with cloud service providers, and AI-optimized chip designs to strengthen their market presence.

Global Graphic Processing Unit (GPU) Market Size

The global graphic processing unit (GPU) market size was valued at USD 62.35 billion in 2024 and is estimated to reach USD 79.40 billion in 2025 from USD 549.30 billion by 2033, growing at a CAGR of 27.35% from 2025 to 2033.

The graphic processing unit (GPU) is a specialized electronic circuits designed to accelerate the rendering of images, video, and 3D graphics, while increasingly serving as a computational engine for non-graphics workloads. Originally developed for gaming and visualization, modern GPUs now underpin artificial intelligence training, scientific simulations, and data analytics due to their parallel processing architecture.

MARKET DRIVERS

The escalating demand for AI and machine learning across industries, which relies heavily on parallel computation capabilities intrinsic to GPU architecture, is driving the growth of the GPU market. Training deep neural networks involves processing vast matrices simultaneously, a task at which GPUs outperform CPUs by orders of magnitude. As per a 2023 Stanford AI Index report, global AI adoption has increased by 28% year-on-year, with 70% of enterprises deploying machine learning models in production environments, predominantly using GPU-accelerated frameworks like TensorFlow and PyTorch.

The rapid expansion of real-time 3D content creation in entertainment, design, and simulation, which demands high-performance GPU processing is additionally enhancing the growth of the GPU market. Industries such as film, architecture, and automotive design are increasingly adopting real-time rendering engines like Unreal Engine and Unity, which require powerful GPUs to deliver photorealistic visuals with minimal latency. According to Epic Games, over 70% of AAA video titles in 2023 were built using Unreal Engine, necessitating advanced GPU support for both development and end-user experiences. In virtual production, studios like Industrial Light & Magic utilize GPU-powered LED stages to render dynamic backgrounds in real time, reducing post-production costs by up to 40%, as cited in a 2023 Society of Motion Picture and Television Engineers case study.

MARKET RESTRAINTS

The persistent shortage of advanced semiconductor packaging and fabrication capacity for cutting-edge nodes below 5 nanometers is restricting the growth of GPU market. GPU production depends on foundries like TSMC and Samsung, which face bottlenecks due to geopolitical constraints, supply chain fragmentation, and capital-intensive infrastructure requirements. According to the Semiconductor Industry Association, global wafer fabrication capacity grew by only 4.1% in 2023 despite a 29% increase in demand for logic chips, leading to extended lead times. This scarcity has led to allocation prioritization, where data centers receive preferential access over consumer markets.

The escalating power consumption and thermal output of high-performance GPUs, which pose operational and environmental challenges is also hindering the growth of GPU market. Modern data centers housing thousands of GPU units face immense energy demands; a single NVIDIA H100 GPU can consume up to 700 watts under full load, as disclosed in its technical specifications. According to the International Energy Agency, data centers accounted for approximately 2% of global electricity demand in 2023, with AI-driven GPU workloads contributing disproportionately to this figure. Cooling such systems requires advanced liquid or immersion solutions, increasing capital and operational expenses.

MARKET OPPORTUNITIES

The integration of GPUs within edge computing architectures, where low-latency processing is essential for autonomous systems, robotics, and smart infrastructure is gearing up with new opportunities for the growth of GPU market. Unlike centralized data centers, edge environments require compact, energy-efficient GPUs capable of real-time inference without cloud dependency. NVIDIA’s Jetson platform, for instance, powers over 2.5 billion edge AI devices globally, including drones, warehouse robots, and medical imaging systems, as reported in its 2023 sustainability disclosure. According to ABI Research, the number of AI-capable edge devices will surpass 1.3 billion by 2027, creating a robust demand channel for embedded GPUs.

The adoption of GPUs in scientific research and high-performance computing (HPC) in climate modeling, genomics, and fusion energy simulation is expected to fuel the growth of GPU market. These domains require massive parallel computation to process complex datasets and run predictive models. According to the U.S. National Science Foundation, 85% of federally funded supercomputing projects in 2023 utilized GPU-accelerated systems, citing performance gains of up to 20x over CPU-only configurations. In climate science, the European Centre for Medium-Range Weather Forecasts reported in 2023 that GPU-accelerated models improved forecast accuracy by 15% while reducing computational time by 70%.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Type, Application, Industry, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Key Market Players | NVIDIA, AMD, Intel, Qualcomm, ARM, Imagination Technologies, Samsung Electronics, Apple, ZOTAC, Sapphire |

SEGMENTAL ANALYSIS

By Type Insights

The dedicated (discrete) GPU segment dominated the global graphic processing unit market by capturing a significant share in 2024 with its superior computational throughput and memory bandwidth, essential for high-intensity workloads in gaming, AI, and professional visualization. Unlike integrated GPUs, discrete units operate independently of the CPU by enabling higher clock speeds and advanced cooling mechanisms.

The integrated GPU segment is projected to expand at a CAGR of 16.8% from 2025 to 2033 with the widespread adoption of energy-efficient, compact computing devices such as ultrabooks, tablets, and embedded systems where power consumption and space constraints are important. Integrated GPUs, embedded within the CPU die, offer cost-effective graphics performance for everyday computing and light creative tasks. As per the U.S. International Trade Commission, over 230 billion laptops with integrated graphics were imported into the U.S. in 2023, reflecting strong consumer and enterprise demand.

By Application Insights

The Machine Learning and Artificial Intelligence (AI/ML) segment was accounted for a prominent share of the GPU market in 2024. The growth of the segment is attributed with the architectural suitability of GPUs for parallel matrix operations essential in deep learning. Training large neural networks requires processing petabytes of data across thousands of cores tasks where GPUs outperform CPUs by up to 50x in efficiency. According to a 2023 MIT Technology Review analysis, over 90% of AI training in enterprise and research environments is conducted on GPU-accelerated platforms, primarily using NVIDIA’s A100 and H100 chips. Cloud providers have responded aggressively Google Cloud deployed over 100,000 GPU instances in 2023 alone for AI model development. Furthermore, the number of AI startups globally surpassed 15,000 in 2023, as reported by Stanford’s AI Index, nearly all of which rely on GPU infrastructure. This entrenched dependency on GPUs for AI scalability ensures the segment’s continued leadership.

The scientific computing segment is likely to grow with an expected CAGR of 20.4% in the coming years with the increasing reliance on GPU-accelerated simulations in fields such as climate modeling, genomics, and particle physics. The U.S. Department of Energy’s Exascale Computing Project relies entirely on GPU-powered supercomputers like Frontier and Aurora to conduct high-fidelity simulations of nuclear fusion and atmospheric dynamics. According to Oak Ridge National Laboratory, GPU-accelerated codes run up to 30 times faster than CPU equivalents in molecular dynamics simulations. In genomics, the Broad Institute reported in 2023 that GPU-based alignment tools reduced whole-genome processing time from hours to under 15 minutes.

By Industry Insights

The IT & Telecommunication sector held 45.3% of the GPU market share in 2024 with the sector’s role as the primary enabler of cloud computing, data centers, and network virtualization all of which rely heavily on GPU acceleration. Hyperscale data centers operated by Amazon Web Services, Microsoft Azure, and Google Cloud have deployed billions of GPU instances to support AI inference, video transcoding, and real-time analytics.

The Defense & Intelligence sector is swiftly emerging with an expected CAGR of 19.7% in the coming years with the integration of AI and real-time image processing in surveillance, drone operations, and battlefield decision systems. Modern reconnaissance satellites and UAVs generate terabytes of visual data daily, requiring onboard GPU processing for immediate threat detection. According to the U.S. Defense Advanced Research Projects Agency (DARPA), over 70% of new defense platforms now incorporate AI-accelerated vision systems powered by GPUs. The U.S. Air Force’s Skyborg autonomous drone program relies on NVIDIA’s Jetson AGX for real-time navigation and target identification.

REGIONAL ANALYSIS

North America Graphic Processing Unit (GPU) Market Analysis

North America was accounted in holding 46.2% of the global GPU market share in 2024. The region’s dominance is anchored in the presence of leading semiconductor designers, hyperscale data centers, and federal investments in AI and defense technologies. The United States alone accounts for over 80% of global AI research funding, according to the National Science Foundation, much of which is directed toward GPU-accelerated systems. NVIDIA, based in California, supplies over 90% of AI training GPUs used in U.S. research institutions. Additionally, the Department of Energy has commissioned five exascale supercomputers, all GPU-powered, to advance energy and national security research.

Europe Graphic Processing Unit (GPU) Market Analysis

Europe was positioned second with 23.3% of the GPU market share in 2024 with its strong industrial base and growing emphasis on digital sovereignty. The region has prioritized GPU adoption in scientific research and autonomous systems, with initiatives like the EuroHPC Joint Undertaking deploying GPU-powered supercomputers across member states. Germany leads in industrial automation, where Siemens integrates GPUs into digital twin simulations for manufacturing. These strategic investments are positioning Europe as a key player in high-performance computing despite reliance on foreign chipmakers.

Asia-Pacific Graphic Processing Unit (GPU) Market Analysis

Asia Pacific GPU market is projected to grow with a significant CAGR throughout the forecast period due to rising tech manufacturing, AI adoption, and government-backed digitalization. China, Japan, and South Korea are major consumers, with China alone accounting for over 35% of global AI investment, as reported by the China Academy of Information and Communications Technology. The country has developed indigenous GPU capabilities through firms like Huawei (Ascend series) and Moore Threads to reduce dependency on U.S. suppliers. Japan’s Society 5.0 initiative integrates GPUs into smart cities and robotics, while South Korea’s LG and Samsung use GPU clusters for OLED and semiconductor R&D. Additionally, India’s National Supercomputing Mission has deployed over 70 GPU-accelerated systems in academic and research institutions.

Latin America Graphic Processing Unit (GPU) Market Analysis

Latin America GPU market growth is likely to be driven by digital transformation in Brazil and Mexico. The region’s growth is fueled by expanding cloud infrastructure and rising demand for AI in financial services and agriculture. Brazil’s Itaú Unibanco, one of Latin America’s largest banks, deployed GPU-powered fraud detection systems that reduced false positives by 40%, as disclosed in its 2023 sustainability report. Chile and Colombia are leveraging GPU computing for seismic analysis in mining and energy exploration. According to the Inter-American Development Bank, data center investments in the region grew by 28% in 2023, with AWS and Google Cloud expanding GPU instance availability.

Middle East and Africa Graphic Processing Unit (GPU) Market Analysis

The Middle East & Africa GPU market is growing, with a strategic interest in GPU technologies for smart governance and energy optimization. The UAE leads the region with its AI-driven government services, including Dubai’s smart traffic system, which uses GPU-accelerated video analytics to reduce congestion by 22%, as reported by the Dubai Roads and Transport Authority. Saudi Arabia’s NEOM project employs GPU-powered simulations for urban planning and autonomous mobility.

COMPETITIVE LANDSCAPE

Key Market Participants

Companies playing a leading role in the global GPU market include

- NVIDIA

- AMD

- Intel

- Qualcomm

- ARM

- Imagination Technologies

- Samsung Electronics

- Apple

- ZOTAC

- Sapphire

The graphic processing unit market is marked by intense technological rivalry, where leadership hinges on architectural innovation, software ecosystem maturity, and strategic positioning in AI and high-performance computing. NVIDIA maintains a strong foothold due to its early dominance in CUDA and deep integration with AI frameworks, but faces growing pressure from AMD and Intel, which are leveraging open standards and competitive pricing to gain enterprise traction. The rise of domain-specific accelerators and in-house chip development by hyperscalers like Google and Amazon introduces further disruption.

Top Players in the Graphic Processing Unit Market

NVIDIA is a top most player with its influence in the Asia Pacific GPU market through deep integration with cloud providers, research institutions, and AI startups. The company has established AI innovation centers in Tokyo, Seoul, and Bangalore to support local enterprises in developing GPU-accelerated applications. In 2023, NVIDIA partnered with Australia’s CSIRO to deploy GPU-powered climate modeling systems for environmental forecasting. It also collaborated with Taiwan’s TSMC to optimize chip design workflows using AI-driven simulation on its own GPUs. In India, NVIDIA launched the Inception program for AI startups, providing access to its DGX Cloud platform. The company introduced its H100 Tensor Core GPUs through Alibaba Cloud and Tencent Cloud, ensuring broad availability across APAC data centers. These strategic alliances and localized infrastructure investments have positioned NVIDIA as a foundational technology enabler across the region’s digital transformation initiatives.

AMD has intensified its presence in the Asia Pacific GPU market by expanding its data center and gaming ecosystem partnerships. In 2023, AMD launched its Instinct MI300X accelerator, specifically targeting AI workloads, and secured adoption in Japan’s ABCI supercomputer, enhancing its credibility in high-performance computing. The company strengthened its collaboration with Lenovo and ASUS to integrate Radeon GPUs into workstations and servers across China and Southeast Asia. AMD also opened a new engineering hub in Hyderabad, India, focused on GPU software optimization for AI and machine learning. Additionally, it partnered with South Korea’s SK Telecom to deploy GPU-based AI inference solutions for 5G network optimization.

Intel has strategically repositioned itself in the Asia Pacific GPU landscape through its Ponte Vecchio and Gaudi accelerators, targeting AI and data center markets. In 2023, Intel collaborated with Japan’s RIKEN institute to integrate its GPUs into next-generation supercomputing initiatives, including upgrades to the Fugaku system. The company launched its Data Center GPU Max Series in Taiwan and South Korea, emphasizing support for AI training and scientific simulation. Intel also forged alliances with cloud providers like Naver Cloud and KT Corporation to offer GPU-as-a-Service solutions in Korea. In India, Intel partnered with the Centre for Development of Advanced Computing (C-DAC) to deploy GPU-accelerated systems for national AI research.

Top Strategies Used by Key Market Participants

Key players in the graphic processing unit market are deploying multifaceted strategies to consolidate their technological and commercial dominance. Vertical integration is a core focus, with companies like NVIDIA and Intel developing full-stack solutions encompassing hardware, software, and AI frameworks to enhance ecosystem lock-in. Strategic partnerships with cloud providers, telecom operators, and research institutions enable broader deployment and validation of GPU capabilities in real-world environments.

RECENT MARKET DEVELOPMENTS

- In February 2023, NVIDIA launched its AI Enterprise Suite on Alibaba Cloud, enabling enterprises across the Asia Pacific to deploy scalable, secure AI workloads using NVIDIA’s GPUs and optimized software stack.

- In June 2023, AMD announced a strategic collaboration with Japan’s National Institute of Advanced Industrial Science and Technology to deploy Instinct MI250X GPUs for large-scale AI research and industrial automation projects.

- In September 2023, Intel inaugurated a GPU software optimization lab in Bangalore, India, focused on enhancing ROCm compatibility and performance for AI and HPC applications in emerging markets.

- In January 2024, NVIDIA partnered with South Korea’s LG AI Research to integrate H100 GPUs into its AI development pipeline for robotics and smart home technologies.

- In March 2024, AMD introduced its Embedded Radeon PRO GPU series in Taiwan, targeting medical imaging, digital signage, and industrial automation systems with long-term reliability and support.

MARKET SEGMENTATION

The research report on the graphic processing unit (GPU) market has been segmented and sub-segmented based on categories.

By Type

- Dedicated or Discrete

- Integrated

- Hybrid

By Application

- Machine Learning and Artificial Intelligence

- Scientific Computing

- 3D Modeling and Rendering

- Video Editing and Rendering

- Cryptocurrency Mining

By Industry

- IT & Telecommunication

- Electronics

- Media & Entertainment

- Defense & Intelligence

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is driving the growth of the GPU market?

Major growth drivers include rising demand for gaming and eSports, AI and deep learning adoption, cloud computing expansion, and increasing use of GPUs in automotive and industrial automation.

Which regions dominate the GPU market?

North America, especially the U.S., leads due to strong demand from AI and gaming sectors, followed by Asia-Pacific with rapid growth from manufacturing hubs like China, Taiwan, and South Korea.

Who are the major players in the GPU market?

Leading players include NVIDIA, AMD, Intel, Qualcomm, ARM, Imagination Technologies, Samsung Electronics, and Apple.

What challenges does the GPU market face?

Challenges include high manufacturing costs, supply chain disruptions, global chip shortages, and strong competition among leading players.

What is the future outlook for the GPU market?

The market is expected to grow significantly with increasing demand for AI-driven applications, 5G adoption, virtual/augmented reality, and edge computing solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com