Global Greenhouse Soil Market Size, Share, Trends & Growth Forecast Report, Segmented By Type (potting Mix, Garden Soil, Mulch, Topsoil, Other), Application (indoor Gardening, Greenhouse, Lawn & Landscaping, Other) And By Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034

Global Greenhouse Soil Market Size

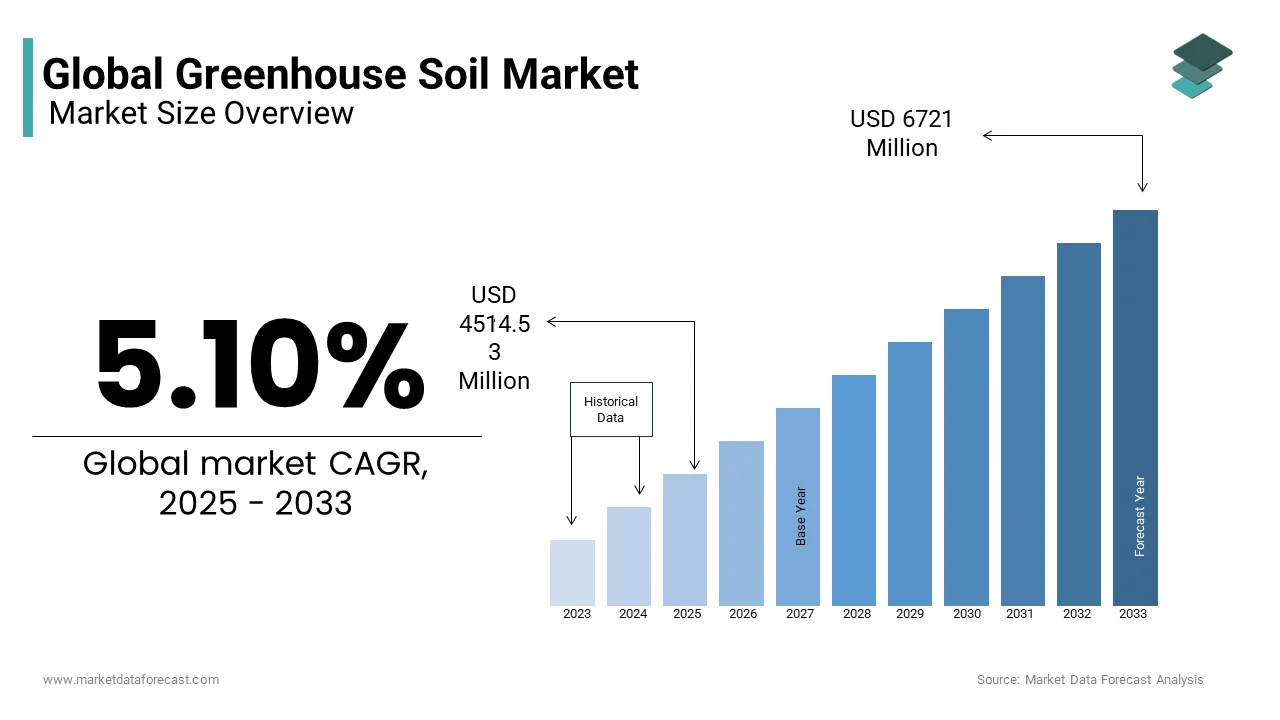

The global greenhouse soil market size was valued at USD 4514.53 million in 2025 and is anticipated to reach USD 4744.77 million in 2026 to reach USD 7063.78 million by 2034, growing at a CAGR of 5.10% during the forecast period from 2026 to 2034.

Greenhouse soil is a specialized category of engineered growing media designed specifically for controlled environment agriculture where natural topsoil is either absent or unsuitable for intensive cultivation. These substrates typically consist of formulated blends including peat moss coconut coir perlite vermiculite and composted organic matter optimized for water retention aeration and nutrient delivery in enclosed structures. The World Vegetable Center indicate that protected cultivation accounts for up to 45% of global vegetable production value, driven heavily by high-value crops like tomatoes, peppers, and cucumbers. This aligns with FAO global frameworks emphasizing that controlled environments optimize plant performance, extend regional growing seasons, and maximize yield quality. According to agricultural structure data managed by Eurostat and the European Commission, southern and western European nations exhibit the highest densities of protected agriculture. Substrate-based and plastic-bound cultivation dominates vast hubs like Almería, Spain, and the Westland region of the Netherlands, where commercial growers utilize soilless mediums to prevent catastrophic soil-borne disease pressures and optimize crop rotation. Modern greenhouse soils must meet stringent phytosanitary standards to prevent pathogen introduction while maintaining structural integrity over multiple cropping cycles. Wageningen University & Research (WUR) demonstrates that growing vegetables in a closed hydroponic system inside a high-tech greenhouse can reduce product water use down to just 4 liters of water per kilogram of fresh tomatoes, compared to roughly 60 to 300 liters required in traditional open-field farming. This drastic reduction represents a water-saving potential exceeding 90%, which is vital for commercial operations facing localized water scarcity. The composition of these media continues to evolve as growers seek sustainable alternatives to peat due to environmental concerns regarding bog degradation. Regulatory frameworks such as the EU Peatland Strategy influence material sourcing prompting innovation in renewable components like wood fiber and rice husks. This transition requires precise calibration of physical and chemical properties to ensure consistent crop performance and economic viability for commercial producers operating within tight margin constraints.

MARKET DRIVERS

Expansion of Controlled Environment Agriculture for Food Security

The accelerating adoption of controlled environment agriculture technologies is a key factor accelerating the growth of the greenhouse soil market. This growth is driven by urgent global food security imperatives and urbanization trends. Demographics published by the United Nations Department of Economic and Social Affairs project that 68% of the global population will reside in urban areas by 2050. This ongoing demographic shift drastically alters urban supply networks, prompting agri-tech developers to build near-market controlled environment systems to safeguard inner-city food channels. Greenhouse facilities enable year round cultivation independent of external climatic conditions ensuring stable food availability in densely populated regions. Whitepapers from the World Bank advocate for aggressive investment in climate-smart agriculture to bypass open-field environmental volatility. Commercial operations are expanding vertical farming and automated greenhouse footprint models to stabilize regional yield metrics and reduce crop risk. Substrate based cultivation is essential for these systems since it provides sterile customizable root zones free from soil borne pathogens that plague continuous monoculture operations. Studies indicate that raw media requirements depend entirely on design matrix variables, ranging from low-volume plug cells in vertical racks to high-capacity trough systems for long-term vine crops. Commercial facilities optimize substrate density to regulate root aeration and ensure ideal moisture retention. The rise of leafy greens and berry production in indoor facilities further amplifies demand since these high value crops require precise pH and electrical conductivity management only achievable through engineered soils. Administered under the European Union's Common Agricultural Policy (CAP) and innovative Horizon Europe grants, funding streams support sustainable, regionalized agricultural infrastructure. These strategic financial injections help European growers transition to eco-certified facilities and procure high-performance alternative growing media. This structural shift toward localized intensive cultivation ensures sustained growth in greenhouse soil consumption as producers seek to maximize yield per unit area while minimizing resource inputs.

Regulatory Push for Sustainable and Peat Free Substrates

Stringent environmental regulations targeting peat extraction are propelling the greenhouse soil market. This shift mandates a transition toward renewable, circular economy-compliant growing media. The European Commission Biodiversity Strategy for 2030 strictly prioritizes the restoration of degraded wetlands and peatland ecosystems to protect natural carbon sinks. This intensive focus on preservation puts long-term supply pressures on commercial growers, accelerating research into alternative, organic materials for growing media. This regulatory pressure compels substrate manufacturers to innovate with alternative materials such as coconut coir wood fiber and composted green waste which offer comparable physical properties without ecological damage. Outlined by the German Federal Ministry for the Environment (BMUV), Germany's national environmental roadmap aims to eliminate peat in the hobby gardening sector by 2026 and achieve a major reduction in commercial cultivation by 2030. This regulatory trajectory forces potting soil manufacturers to heavily increase their usage of wood fiber, compost, and coir substitutes. Agricultural research institutions like the James Hutton Institute confirms that alternative mediums, such as coconut coir, possess strong natural re-wetting properties after drying out. Unlike traditional peat, which can become hydrophobic when completely dry, processed coir absorbs water evenly under automated drip irrigation schedules. Growers are increasingly adopting blended formulations that incorporate biochar and recycled organic matter to enhance nutrient retention and reduce fertilizer leaching. The transition creates substantial opportunities for suppliers of innovative sustainable components who can provide consistent quality at competitive prices. Certification schemes such as RHP Standard in the Netherlands verify substrate safety and performance ensuring market confidence in non peat alternatives.

MARKET RESTRAINTS

Volatility in Raw Material Supply Chains

Instability in the availability and pricing of key raw materials such as coconut coir, perlite, and high-quality compost creates significant operational limitations for manufacturers within the greenhouse soil market. The Food and Agriculture Organization (FAO) highlights that severe weather anomalies, monoculture pest pressures, and changing rainfall patterns in top-tier producing nations like India, Indonesia, and Sri Lanka introduce logistical volatility into the global coconut trade, directly impacting the steady upstream availability of raw husk byproducts. International potting soil associations confirm that international maritime freight spikes and surging multi-regional demand have added notable pricing premiums to processed coir pith. This volatility forces substrate producers to optimize local distribution nodes to absorb shipping shocks. Perlite another critical component for aeration relies on mining operations concentrated in Turkey Greece and the United States which are susceptible to energy cost fluctuations and regulatory permitting delays. Composted organic matter quality varies significantly based on source material consistency leading to batch to batch variability that complicates formulation standardization. The European Compost Network (ECN) emphasize that utilizing organic municipal bio-waste for professional horticulture requires highly specialized processing. Stringent physical and chemical purity criteria dictate that green compost must undergo verified heat-sterilization cycles to eliminate weed seeds and human or plant pathogens before it can be safely used in substrate blends. Transportation costs for bulky low density materials further exacerbate margin pressures particularly for landlocked facilities distant from ports or processing centers. Manufacturers struggle to maintain stable pricing contracts with growers when input costs fluctuate unpredictably forcing frequent formula adjustments that may impact crop performance consistency.

Technical Complexity of Substrate Formulation and Quality Control

Achieving consistent physical and chemical properties in greenhouse soil blends requires sophisticated technical expertise and rigorous quality control protocols that pose barriers to entry and operational efficiency in the global market. Research confirms that predictable root zone management relies entirely on balancing a substrate’s air-filled porosity, water-holding capacity, and cation exchange capacity. Because alternative raw materials display broad batch-to-batch structural variance, raw material suppliers use strict laboratory screening to maintain mechanical uniformity. Agronomic trials published by agricultural extensions prove that substantial deviations in particle size distribution alter the vital air-to-water ratio within a growing medium. If a substrate contains an excess of fine dust or lack of coarse aggregates, it can suffer from compaction and waterlogging, increasing the risk of root rot in sensitive crops like strawberries. Studies emphasize that managing substrate pH stability is vital for optimal nutrient uptake, as most high-value greenhouse crops require a root-zone window of 5.5 to 6.5. Consequently, manufacturing alternative substrates like coconut coir or wood fiber requires precise pre-treatment washings and calcium-magnesium buffering to avoid premature nutrient lockout. Manufacturing facilities must invest in advanced laboratory equipment for regular testing of electrical conductivity nutrient content and pathogen presence which increases capital expenditure requirements. Small and medium sized producers often lack resources for comprehensive quality assurance programs resulting in product variability that undermines brand reputation. Additionally the biological activity within organic components continues to evolve post production potentially altering nutrient availability during storage and transport. This dynamic nature necessitates rapid inventory turnover and careful monitoring throughout the supply chain adding complexity to logistics and distribution management.

MARKET OPPORTUNITIES

Integration of Smart Sensors and Precision Irrigation Compatibility

The convergence of digital agriculture technologies with substrate science offers major opportunities for the global greenhouse soil market. This paves the way for developing smart greenhouse soils compatible with precision irrigation and monitoring systems. Innovation frameworks backed by the European Union CAP Network (EIP-AGRI) actively fund pilot programs to accelerate the deployment of smart agritech. These initiatives demonstrate that incorporating real-time substrate moisture sensors enables commercial indoor growers to transition away from timer-based watering, synchronizing nutrient delivery directly with a crop's current transpiration demands. Substrate manufacturers can capitalize on this trend by engineering media with uniform hydraulic conductivity and predictable wetting patterns that enhance sensor accuracy and system reliability. Operational guides published by greenhouse automation leaders like Priva highlight that pairing digital climate computers with advanced substrate monitoring tools maximizes crop uniformity. Automating the irrigation feedback loop based on volumetric water content data allows commercial facilities to maintain predictable root-zone conditions without relying on manual labor. Development of substrates with embedded conductive materials or standardized dielectric properties enables seamless compatibility with emerging IoT platforms facilitating data driven decision making for growers. This technological alignment supports the broader Industry 4.0 transformation in agriculture where predictive analytics optimize resource use and maximize yield potential. Manufacturers collaborating with technology providers to validate substrate performance under automated conditions can differentiate their offerings and command premium pricing. The growing adoption of closed loop irrigation systems further drives demand for substrates that minimize leaching and maintain stable nutrient balances over extended cropping cycles enhancing sustainability credentials.

Development of Circular Economy Certified Reusable Substrates

Emerging circular economy principles create significant opportunities for providers in the greenhouse soil market. These providers must develop reusable, sterilizable, and recyclable growing media solutions. Research featured across circular economy frameworks estimates that transitioning to circular business models represents a $4.5 trillion global economic opportunity by 2030. This systemic shift heavily incentivizes agricultural suppliers to design out waste and invest in regenerative, reusable material loops to reduce reliance on finite raw commodities. Substrate manufacturers are innovating with durable materials such as rockwool and rigid foam structures that can be steam sterilized and reused for multiple cropping cycles without degradation of physical properties. Research shows that the commercial lifecycle of inert substrates can be integrated into a closed loop through structured recycling programs. Instead of reusing spent growing media on-site, which risks disease carryover, used slabs are collected, processed, and upcycled into raw inputs for building insulation and industrial brick manufacturing. Composting programs for spent organic substrates convert waste into valuable soil amendments for open field agriculture closing the nutrient loop and reducing landfill disposal costs. The European Committee for Standardization is developing certification protocols for circular substrates ensuring safety and performance benchmarks that facilitate market acceptance. Growers benefit from reduced material procurement expenses and lower environmental compliance burdens while manufacturers gain competitive advantage through sustainability leadership. Partnerships with waste management firms and agricultural cooperatives enable efficient collection and processing networks that support scalable circular operations. This model aligns with corporate sustainability goals and consumer preferences for environmentally responsible production methods enhancing brand value and market access.

MARKET CHALLENGES

Pathogen Contamination Risks in Organic Components

Managing biological contamination risks in organic substrate components remains a persistent impediment to the greenhouse soil market. This threatens crop health and regulatory compliance in greenhouse operations. The European and Mediterranean Plant Protection Organization (EPPO) warn commercial growers that soil-borne pathogens like Pythium, Phytophthora, and Fusarium present continuous containment challenges. Because these persistent fungi easily propagate in closed, humid greenhouse systems, keeping organic raw components absolutely clean remains a top regulatory and operational priority. Organic materials like composted bark and green waste serve as potential vectors for these pathogens if not properly treated during processing. Steam pasteurization and chemical fumigation are common mitigation strategies but they increase production costs and may leave residual compounds affecting plant growth. Horticultural extensions, including those at the University of Florida Institute of Food and Agricultural Sciences (UF/IFAS), emphasize that raw organic materials used in alternative substrates must undergo verified sanitization or composting procedures. Failing to control processing temperatures can leave heat-tolerant microbial spores alive, leading to mold outbreaks or pathogen resurgence during transport and storage in humid regions. Biological control agents offer alternative protection but their efficacy varies depending on substrate composition and environmental conditions requiring complex integration protocols. Regulatory restrictions on chemical disinfectants such as methyl bromide have limited available treatment options forcing reliance on thermal methods that consume significant energy. The European Food Safety Authority mandates strict testing for human pathogens like E coli and Salmonella in substrates used for edible crops adding compliance burden. Outbreaks of contaminated substrates can trigger widespread recalls and reputational damage for manufacturers necessitating robust traceability systems. Balancing microbial diversity beneficial for plant health with pathogen suppression requires nuanced formulation expertise that many producers lack.

High Logistics and Transportation Costs for Bulky Materials

The inherent bulkiness and low density of greenhouse soil components result in disproportionately high logistics and transportation costs that constrain expansion and profitability of the global market. The International Transport Forum (ITF) emphasize that geopolitical fuel price volatility and shifting maritime container capacities create severe pricing pressures on global shipping networks. These logistics shocks hit low-density, high-volume agricultural products particularly hard, as shipping costs often outpace the intrinsic raw value of the material itself. Shipping air filled materials such as perlite and vermiculite over long distances is economically inefficient since volume rather than weight determines freight charges. A study shows that shipping and distribution constitute a massive portion of the final delivered price of commercial growing media. Because loose substrates are heavy and bulky, transport logistics can become the single largest expense for growers operating far from primary coastal processing plants or peat bog reserves. Local sourcing mitigates some costs but limits access to specialized high quality materials available only in specific geographic locations such as volcanic perlite deposits. Compression technologies reduce volume but require additional processing energy and may compromise substrate structure upon rehydration affecting performance. The carbon footprint associated with long distance transport contradicts sustainability goals prompting retailers and growers to prefer locally sourced alternatives even if quality is slightly inferior. Regional trade barriers and customs delays further complicate international shipments causing inventory shortages and production disruptions. Manufacturers must optimize packaging density and establish regional production hubs to remain competitive but these strategies require substantial capital investment. Fluctuating diesel prices and driver shortages in key markets exacerbate delivery uncertainties impacting just in time supply models prevalent in commercial greenhouse operations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.10% |

| Segments Covered | By Type, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Scotts Miracle-Gro, Sun Gro, Klasmann-Deilmann, Premier Tech, Compo, ASB Greenworld, Bord na Móna, Florentaise, Lambert, FoxFarm, Westland Horticulture, Matécsa Kft, Espoma, Hangzhou Jinhai, Michigan Peat, C&C Peat, Good Earth Horticulture, Free Peat, and Vermicrop Organic, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The potting mix segment held a 45.1% share of the greenhouse soil market because of its critical role in containerized cultivation and controlled environment agriculture. Moreover, the main driver for this market share is the widespread adoption of soilless culture systems in commercial greenhouses, which require sterile, lightweight, and nutrient-optimized media for high-value crops. The Food and Agriculture Organization (FAO) emphasize that substrate-based soilless cultivation is highly preferred in high-tech greenhouse operations. These specialized potting mediums provide optimized root aeration and uniform water retention, allowing commercial operations to maximize per-square-meter yields compared to open-field soil cultivation. The Dutch Potting Soil Association (VPN) shows that the Netherlands is a global cornerstone for growing media production, generating millions of cubic meters of specialized substrates annually. This robust infrastructure directly fuels the high-yield Dutch indoor agritech network, enabling massive exports of premium floriculture and fresh produce to global markets. Wageningen University & Research (WUR) demonstrates that transitioning crops from open-field soil to closed-loop greenhouse systems drastically cuts water consumption. Utilizing high-porosity alternative substrates like coconut coir allows growers to manage automated, precise drainage cycles, keeping root zone moisture levels uniform while eliminating run-off waste. The rise of urban vertical farming further amplifies demand since these facilities rely exclusively on engineered potting media to maximize yield per square meter in stacked growing systems. Industry standards such as RHP certification in Europe ensure consistent quality and phytosanitary safety driving professional growers to prefer branded potting mixes over unregulated alternatives. The versatility of potting mixes allows customization for specific crops including strawberries tomatoes and ornamental plants ensuring optimal pH and electrical conductivity levels for diverse agricultural needs.

On the other hand, the mulch segment is expected to exhibit a noteworthy CAGR of 7.8% over the forecast period due to increasing emphasis on moisture conservation and weed suppression in sustainable agriculture. A key growth enabler is the regulatory push toward organic farming practices which prohibit synthetic herbicides and mandate natural weed control methods. The annual statistical report published by FiBL and IFOAM - Organics International documents a massive global expansion of certified organic agricultural land, now exceeding 96 million hectares. This rising adoption of organic standards pushes indoor and outdoor growers to source natural, organic-compliant mulches to satisfy stringent international chemical-free certification criteria. Biodegradable mulches made from straw wood chips and composted bark are gaining traction as they decompose into valuable soil amendments enhancing long term fertility. The USDA Natural Resources Conservation Service (NRCS) confirm that applying proper mulching materials significantly suppresses soil water evaporation. By acting as a physical barrier against solar radiation and wind, mulching preserves root-zone moisture, lowering overall irrigation frequencies in drought-prone regions like California. The University of California Division of Agriculture and Natural Resources (UC ANR) state that organic mulches act as a thermal buffer for the root zone. By shading the ground from direct sunlight during extreme summer heatwaves, a thick mulch layer prevents excessive soil temperature spikes, protecting delicate root systems from heat stress. The aesthetic appeal of decorative mulches also drives demand in ornamental greenhouse production where visual presentation influences consumer purchasing decisions. Market updates shared across professional nursery and landscape associations highlight a steady consumer demand for premium, dyed mulches. Residential and commercial landscaping projects rely heavily on these aesthetic options to enhance visual curb appeal while simultaneously providing baseline weed suppression and soil moisture retention benefits. Additionally mulch acts as a physical barrier against soil borne pathogens reducing disease incidence and lowering pesticide reliance aligning with integrated pest management strategies promoted by environmental agencies globally.

By Application Insights

The greenhouse application segment led the global market and captured a 55.9% share in 2025. This leading position of the segment was attributed to the superior productivity of greenhouse operations which can produce significantly more output per unit area than open field farming. Such market share is also propelled by the intensification of protected cultivation techniques to ensure year round food security and high crop yields. One of the major drivers is the increasing investment in high tech greenhouse infrastructure in regions with adverse climatic conditions such as the Middle East and Northern Europe. Eurostat and European Commission agricultural registries show that Mediterranean and Western European countries manage the highest densities of protected agriculture. Vast multi-hectare production hubs across Spain and Italy rely heavily on specialized growing media substrates to optimize continuous crop rotations and prevent soil-borne diseases. The Chinese Academy of Sciences (CAS) reveal that China produces more than one-third of its total vegetable crop inside protected facilities. This massive domestic infrastructure requires large quantities of cost-effective growing media and potting mixes to sustain urban fresh food supply chains year-round. The shift toward hydroponic and aeroponic systems within greenhouses further drives demand for inert substrates like rockwool and perlite based mixes that facilitate precise nutrient delivery. Commercial growers prioritize consistency and sterility in greenhouse soils to prevent crop loss from diseases such as Pythium and Fusarium which thrive in traditional soil environments. The economic viability of greenhouse farming relies on maximizing harvest cycles per year which requires rapid substrate turnover and efficient replanting protocols. Advanced climate control systems integrated with substrate monitoring sensors enable real time adjustments to irrigation and fertilization optimizing resource use and enhancing profitability for large scale operators.

However, the lawn and landscaping application segment is predicted to witness the highest CAGR of 6.5% from 2026 to 2034 owing to urbanization trends and rising disposable incomes driving demand for aesthetic outdoor spaces. The main force moving this segment is the expansion of residential housing developments and commercial real estate projects that incorporate extensive green areas requiring high quality topsoil and amendment products. Also, the U.S. Census Bureau and the Department of Housing and Urban Development (HUD) track the underlying pipeline of residential construction, which acts as a major catalyst for the green industry. New single-family housing completions trigger immediate, large-scale commercial demand for bulk topsoil, specialized lawn turf starters, and landscaping soils to establish initial turf and garden layers. Urban forestry and urban greening frameworks backed by the European Environment Agency (EEA) emphasize that expanding city parks, public green belts, and sustainable drainage zones requires significant investments in local soil management. These large-scale infrastructure projects necessitate massive volumes of premium organic composts and engineered topsoils to support long-term plant health and meet urban biodiversity targets. The UK Horticultural Trades Association (HTA) indicates that despite broader inflationary pressures and cost-of-living challenges, consumer interest in domestic garden maintenance remains resilient. Homeowners continue to allocate discretionary funds toward premium bagged potting soils, composts, and seasonal plants to upgrade private outdoor spaces. Municipalities are increasingly investing in green infrastructure to mitigate urban heat islands and manage stormwater runoff which necessitates the use of permeable and nutrient rich soil blends. The trend toward native plant landscaping requires specific soil compositions that mimic natural habitats supporting biodiversity and reducing maintenance costs. Professional landscaping firms prefer certified soil products that guarantee weed free and pathogen free conditions ensuring successful establishment of turf and ornamental plants. Regulatory requirements for soil quality in public spaces further drive adoption of standardized landscaping soils that meet strict environmental and safety criteria.

REGIONAL ANALYSIS

North America Market Analysis

North America dominated the global greenhouse soil market and accounted for a 30.7% share in 2025. Factors such as advanced agricultural technologies and strong consumer demand for fresh produce have contributed to the supremacy of the regional market. The United States dominates the regional market due to its extensive commercial greenhouse industry concentrated in states like California Florida and Michigan. In addition, the USDA National Agricultural Statistics Service shows that the market value of agricultural products sold within the Nursery, greenhouse, floriculture, and sod segment exceeds $15.2 billion. This substantial valuation underscores a continuous rise in capital-intensive controlled environment infrastructures across the United States. Canada contributes significantly through its large scale tomato and cucumber production in Ontario and Quebec where harsh winters necessitate year round indoor farming using specialized substrates. The North American Free Trade Agreement facilitates cross border trade of horticultural inputs ensuring steady supply of raw materials such as peat and perlite. Also, the Canadian Greenhouse Conference emphasize that commercial indoor cultivation is accelerating, with data from the RBC Climate Action Institute noting that Canadian fruit and vegetable greenhouse farm-gate value has climbed to $2.5 billion. This rapid industry growth forces a heavy operational reliance on high-efficiency, soilless substrate systems to mitigate soil-borne pathogens and maximize water reuse. Environmental regulations in both countries promote sustainable sourcing practices encouraging the use of renewable components like coconut coir and recycled wood fiber. The presence of major substrate manufacturers and distributors ensures wide availability of high quality products tailored to diverse crop requirements. Consumer preference for locally grown organic produce further supports market growth as retailers source from nearby greenhouse facilities that rely on premium potting mixes for consistent quality.

Europe Market Analysis

Europe was the next prominent region in the greenhouse soil market and occupied a share of 35.4% in 2025 because of stringent environmental regulations and advanced horticultural expertise. The Netherlands Spain and Italy are the primary contributors driven by their status as global hubs for flower and vegetable production. Eurostat state that the European Union harvests approximately 59.8 million tonnes of fresh vegetables annually, led by Spain and Italy. A significant portion of this high-yield, premium-grade produce relies on advanced greenhouse operations and specialized growing media substrates to ensure uncompromised quality. The European Green Deal and Biodiversity Strategy mandate reduction in peat usage prompting rapid innovation in alternative substrates such as wood fiber and composted green waste. Under the strategic framework outlined by the Dutch Potting Soil Association (VPN), the Netherlands' horticulture sector is bound by a sustainability covenant designed to systematically lower the footprint of substrates. The sector's roadmap targets shifting to 50% renewable raw materials by 2030 and 90% by 2050, which accelerates commercial adoption of innovative, circular substrate alternatives. Germany and France are key markets for ornamental plant production where high quality potting mixes are essential for meeting consumer expectations for healthy vibrant plants. The European Committee for Standardization enforces rigorous quality controls ensuring substrate safety and performance across member states. Research institutions like Wageningen University collaborate with industry stakeholders to develop next generation substrates that enhance resource efficiency and crop resilience. Political support for sustainable agriculture through subsidies and grants accelerates transition toward eco friendly soil alternatives. The mature market structure favors established brands with proven track records in reliability and technical support.

Asia-Pacific Market Analysis

Asia-Pacific is the fastest growing regional market due to rapid urbanization population growth and government initiatives to enhance food security. China India and Japan are the largest consumers due to expanding greenhouse infrastructure for vegetable and flower production. National agricultural land surveys spearheaded by the Chinese Academy of Sciences (CAS) prove that China's greenhouse footprint spans approximately 1.8 million hectares. Accounted for by satellite mapping as over 80% of the world's total protected cultivation surface area, this massive infrastructure requires millions of cubic meters of accessible, cost-effective growing media annually. Administered by the Ministry of Agriculture and Farmers Welfare, the Indian government's Mission for Integrated Development of Horticulture (MIDH) scheme actively funds a 50% credit-linked subsidy for private polyhouse and greenhouse construction. The Netherlands Agricultural Network in Japan outline that Japan is heavily prioritizing modern, industrialized agrotechnology to counter shrinking domestic labor pools and an aging farming demographic. Also, the implementation of high-tech, landless hydroponic installations serves to bolster long-term food security inside an economy reliant on imports for a large share of its food supply. Southeast Asian countries like Thailand and Vietnam are emerging markets driven by export oriented flower and fruit production requiring international quality standards for substrates. Limited local production of high quality peat and perlite leads to reliance on imports from Australia and Europe affecting pricing dynamics. Rising awareness of sustainable farming practices encourages adoption of organic amendments and biochar based mixes. Urban farming initiatives in megacities like Tokyo and Singapore drive demand for compact lightweight substrates suitable for rooftop and vertical gardens. Regional trade agreements facilitate technology transfer and investment in modern greenhouse facilities enhancing overall market potential.

Latin America Market Analysis

Latin America grew steadily in the global greenhouse soil market owing to expanding floriculture and vegetable exports particularly from Colombia Ecuador and Mexico. The region benefits from favorable climatic conditions that allow year round production with minimal heating requirements reducing operational costs. Asocolflores (Colombia) and Expoflores (Ecuador), the combined annual flower exports of these two nations exceed $3 billion, solidifying them as global floriculture leaders. This large-scale, high-value greenhouse infrastructure relies on imported and locally engineered substrate mixes to meet strict quality guidelines for premium international markets. Mexico serves as a major supplier of fresh vegetables to the United States under the USMCA agreement with greenhouse tomato and pepper production expanding rapidly in states like Sinaloa and Jalisco. The Mexican Association of Protected Agriculture (AMHPAC) details a long-term compound annual growth rate exceeding 20% for total protected agriculture acreage. This rapid technological shift helps commercial operations produce export-grade tomatoes, peppers, and cucumbers primarily destined for North American supply chains. Local manufacturing of substrates is developing but still faces challenges in consistency and quality control leading to preference for international brands among large exporters. Economic volatility and currency fluctuations impact purchasing power of small scale growers limiting market penetration in rural areas. Government programs supporting agricultural modernization provide opportunities for substrate suppliers to introduce innovative products. Increasing awareness of soil health and sustainability drives gradual shift toward organic and renewable substrate components.

Middle East and Africa Market Analysis

The Middle East and Africa region is likely to expand notably in the global greenhouse soil market due to food security initiatives and investments in controlled environment agriculture in Gulf Cooperation Council countries. Saudi Arabia the United Arab Emirates and Qatar are leading investors in high tech greenhouses to reduce reliance on food imports in arid climates. Official agricultural census updates from the Saudi Ministry of Environment, Water and Agriculture (MEWA) confirm that the kingdom's strategic focus has accelerated the agricultural sector's contribution to a $31.5 billion GDP footprint. Driven by Saudi Vision 2030, localized food infrastructure projects have successfully pushed self-sufficiency past 100% for dates and dairy, while using modern irrigation and specialized substrates to scale up indoor vegetable yields. Governed by the UAE Ministry of Climate Change and Environment, the National Food Security Strategy 2051 focuses on transforming local food production via technology-driven indoor farming systems. The African Development Bank and international logistics networks highlight that East and North Africa are global centers for protected agriculture. Egypt's massive government greenhouse complexes, alongside Kenya's dominant cut-flower export sector and South Africa's premium berry facilities, require large quantities of specialized substrates to maintain high-yield production for global markets. Water scarcity is the primary driver for adopting soilless systems that offer superior water use efficiency compared to traditional farming. High energy costs for cooling and desalination constrain widespread adoption but solar powered greenhouse projects are emerging as viable solutions. Local substrate production is minimal resulting in heavy dependence on imports from Europe and Asia. Political stability issues in some African nations hinder long term investment but stable Gulf economies continue to drive regional demand for premium greenhouse soils.

COMPETITIVE LANDSCAPE

The Greenhouse Soil Market exhibits a moderately consolidated competitive landscape characterized by established international leaders and numerous regional specialists. Major corporations leverage their extensive distribution networks and brand reputation to secure long term contracts with large commercial greenhouse operators. These entities compete primarily on product consistency technical support and sustainability credentials rather than price alone. Smaller niche players differentiate themselves through specialized formulations for unique crops or local raw material availability. Intense competition drives continuous innovation in substrate composition to improve water efficiency and nutrient retention capabilities. Regulatory compliance regarding peat extraction and waste management serves as a significant barrier to entry ensuring that only qualified manufacturers can participate in regulated markets. Mergers and acquisitions are common strategies employed by leading firms to expand geographic reach and acquire proprietary blending technologies. The market remains dynamic with participants constantly adapting to shifting environmental policies and evolving customer preferences for eco friendly growing media across diverse agricultural sectors globally.

KEY MARKET PLAYERS

The major players operating in the global greenhouse soil industry include

- Scotts Miracle-Gro

- Sun Gro

- Klasmann-Deilmann

- Premier Tech

- Compo

- ASB Greenworld

- Bord na Móna

- Florentaise

- Lambert

- FoxFarm

- Westland Horticulture

- Matécsa Kft

- Espoma

- Hangzhou Jinhai

- Michigan Peat

- C&C Peat

- Good Earth Horticulture

- Free Peat

- Vermicrop Organics.

Top Players In The Market

- Klasmann Deilmann operates as a leading international supplier of professional growing media and substrates for horticulture and agriculture. The company specializes in producing high quality peat based and peat free mixes tailored for greenhouse crops including vegetables flowers and soft fruits. Klasmann recently expanded its production facilities in Europe to increase capacity for sustainable wood fiber based substrates aligning with regulatory demands for reduced peat usage. The firm invests heavily in research and development to optimize substrate structures for improved water retention and root aeration. Strategic partnerships with global seed companies enable customized solutions that enhance germination rates and crop uniformity. Klasmann maintains rigorous quality control standards ensuring consistent product performance across diverse climatic conditions. Its commitment to sustainability includes responsible peat sourcing and carbon neutral production initiatives strengthening its reputation among environmentally conscious growers worldwide.

- Lambert Peat Moss is a prominent North American manufacturer of premium horticultural substrates serving commercial greenhouse operators and retail markets. The company focuses on delivering reliable and consistent growing media formulated with sphagnum peat moss perlite and vermiculite for optimal plant growth. Lambert recently launched a new line of organic certified potting mixes catering to the expanding demand for sustainable cultivation practices in the United States and Canada. The organization has upgraded its processing infrastructure to improve blending precision and reduce dust content enhancing worker safety and product quality. Lambert collaborates with agricultural universities to validate substrate performance under various cropping systems providing data driven recommendations to customers. Its extensive distribution network ensures timely delivery of bulk and packaged products to growers across the continent. The company emphasizes customer support through technical agronomy services helping clients optimize irrigation and nutrient management strategies for maximum yield.

- Premier Tech Horticulture is a global leader in innovative growing media solutions offering a diverse portfolio of substrates for professional and consumer markets. The company distinguishes itself through advanced formulation technologies that integrate renewable materials such as coconut coir and composted bark into high performance mixes. Premier Tech recently acquired several regional substrate manufacturers to expand its geographic footprint and enhance local supply chain resilience in Europe and Asia. The firm actively promotes circular economy principles by developing recyclable packaging and reusable substrate systems for commercial greenhouses. Premier Tech invests in digital tools that allow growers to monitor substrate moisture and nutrient levels in real time improving resource efficiency. Its strong brand presence is supported by comprehensive educational programs and technical workshops for horticultural professionals. The company continues to innovate with biochar enriched mixes that enhance soil health and carbon sequestration capabilities aligning with global sustainability goals.

Top Strategies Used By Key Market Participants

Key players in the Greenhouse Soil Market primarily focus on product innovation and sustainability to maintain competitive advantage. Companies invest heavily in research and development to create peat free alternatives using renewable materials like wood fiber and coconut coir. Strategic acquisitions of regional manufacturers enable firms to expand geographic reach and secure raw material supplies. Partnerships with agricultural research institutions help validate substrate performance and develop customized solutions for specific crops. Digital integration offers value added services such as remote monitoring and precision irrigation support enhancing customer loyalty. Manufacturers prioritize compliance with environmental regulations by adopting circular economy practices and reducing carbon footprints. Expansion into emerging markets through localized production facilities helps reduce logistics costs and improve service responsiveness. These strategies collectively drive market growth and address evolving consumer demands for sustainable and efficient horticultural solutions globally.

MARKET SEGMENTATION

This research report on the global greenhouse soil market is segmented and sub-segmented into the following categories.

By Type

- potting mix

- garden soil

- mulch

- topsoil

- Others

By Application

- Indoor gardening

- Greenhouse

- Lawn & Landscaping

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle-East & Africa

Frequently Asked Questions

Why is the greenhouse soil market becoming increasingly important for modern agriculture?

The market is growing due to the expansion of protected cultivation, increasing demand for high-yield crop production, and the need for optimized growing media in controlled-environment agriculture.

What is greenhouse soil and how does it differ from conventional agricultural soil?

Greenhouse soil is a specialized growing medium designed to provide optimal water retention, aeration, nutrient availability, and root development for crops grown in greenhouse environments.

Which crop types generate the highest demand for greenhouse soil products?

Vegetables, fruits, flowers, herbs, and ornamental plants generate the highest demand due to their extensive cultivation in greenhouse facilities.

How does greenhouse soil improve crop productivity and quality?

It supports healthy root growth, enhances nutrient uptake, improves moisture management, and creates a stable growing environment that boosts crop yields and quality.

What factors are driving the adoption of greenhouse cultivation worldwide?

Rising food demand, limited arable land, climate variability, year-round production requirements, and increasing focus on sustainable agriculture are key growth drivers.

Who are the primary users of greenhouse soil solutions?

Commercial greenhouse operators, horticulture growers, nursery producers, hydroponic farms, and agricultural research facilities are the primary users.

What trends are transforming the greenhouse soil market?

The adoption of organic growing media, peat alternatives, coco coir substrates, precision agriculture practices, and sustainable cultivation methods is transforming the market.

How are sustainable farming practices influencing greenhouse soil demand?

Growers are increasingly seeking environmentally friendly growing media that improve resource efficiency, reduce environmental impact, and support sustainable crop production.

What challenges could affect the growth of the greenhouse soil market?

Raw material availability, fluctuating production costs, environmental regulations, and competition from soilless cultivation systems could affect market growth.

Which regions are expected to lead the greenhouse soil market?

Europe remains a major market due to advanced greenhouse cultivation, while North America and Asia Pacific are experiencing strong growth driven by commercial horticulture expansion.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com