Global Soil Monitoring Market Size, Share, Trends & Growth Forecast Report, Segmented By System (Ground-Breaking Monitoring Systems, Sensing and Imagery Systems, and Others), Offering (Software, Hardware, and Services), Application (Agricultural and Non-agricultural), And Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Industry Analysis From 2025 to 2033

Global Soil Monitoring Market Size

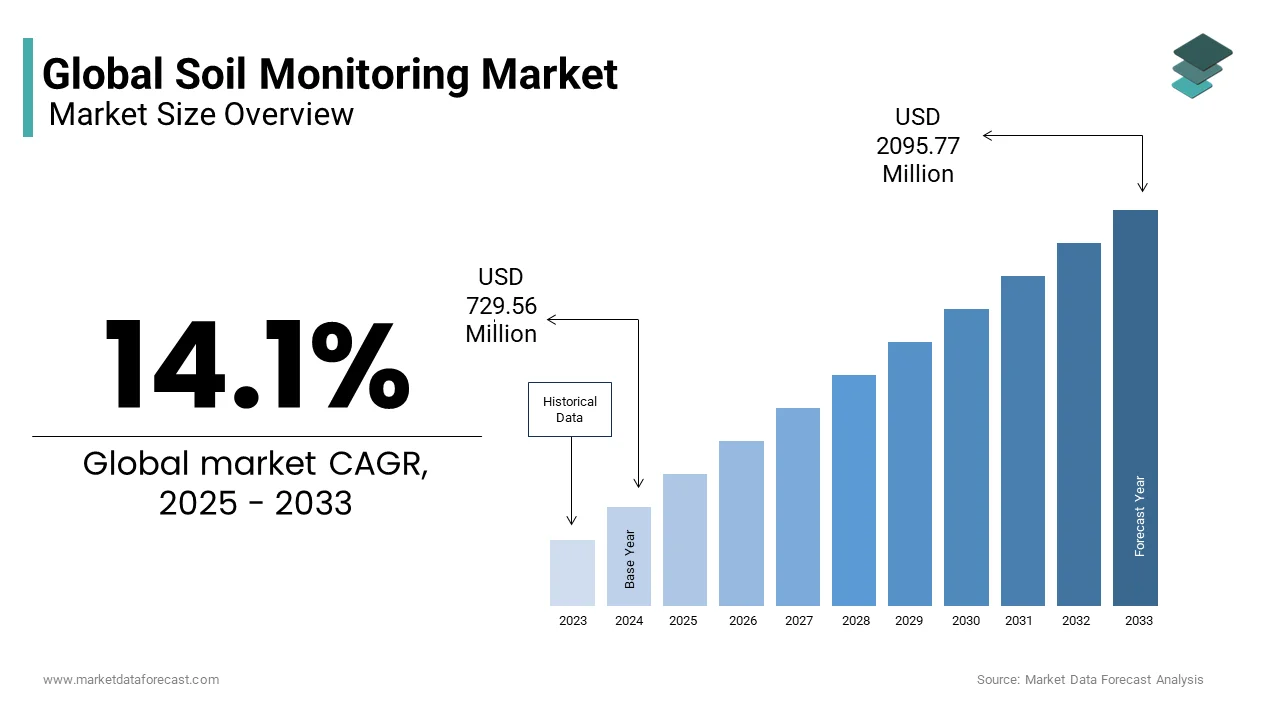

The global soil monitoring market was valued at USD 639.40 million in 2024 and is anticipated to reach USD 729.56 million by 2025 from USD 2095.77 million by 2033, growing at a CAGR of 14.1% from 2025 to 2033.

Soil monitoring refers to the systematic use of hardware, software, and services to measure and analyze soil properties over time and space to evaluate its condition for various uses, such as agriculture, environmental management, and construction. This market includes in situ sensors, remote sensing platforms, laboratory-based analytical tools, and integrated data analytics systems that measure parameters such as moisture content, pH, organic matter, salinity, ty and nutrient levels. Ensuring food security amid climate threats and rising demand depends heavily on robust soil intelligence. According to the Food and Agriculture Organization of the United Nations, approximately 33 percent of the world’s soil is moderately to highly degraded due to erosion,n nutrient depletion, and chemical pollution, which underscores the urgency for continuous soil health assessment. Apart from these, the Intergovernmental Technical Panel on Soils estimates that over 90 percent of ecosystem services are mediated by soil function,,s making systematic monitoring critical not only for farming but also for biodiversit,,water regulation,n and carbon sequestration. The convergence of digital agriculture and environmental sustainability imperatives is reshaping how stakeholders, from smallholder farmers to national governments, approach soil stewardship through data-driven insights.

MARKET DRIVERS

Escalating Soil Degradation Drives Demand for Continuous Monitoring Systems

Soil degradation has emerged as a pivotal driver of the soil monitoring market. As per the Food and Agriculture Organization of the United Nations, around 24 billion tons of fertile soil are lost annually due to erosion alone, which equates to roughly 3.4 tons per person globally. This alarming rate of deterioration directly compromises agricultural output and food securityparticularly in regions like Sub-Saharan Africa and South Asia, a small-scale farming dominates. Continuous monitoring enables early detection of declining soil health, allowing timely interventions such as cover cropping or reduced tillage. In the European Union, A considerable portion of agricultural land across the European Union is showing signs of compaction, which is a form of soil degradation that impacts productivity. Furthermore, the United Nations Convention to Combat Desertification notes that land degradation affects 3.2 billion people worldwide, de reinforcing the need for scalable diagnostic tools. Governments are implementing soil health initiatives, such as the United States Department of Agriculture actively supports and promotes the monitoring of soil health across millions of acres of American farmland to encourage sustainable management. These environmental policy-driven pressures create a sustained impetus for deploying sensor-based monitoring networks across diverse agroecosystems.

Integration of Digital Agriculture Platforms Amplifies Sensor Utilization

The proliferation of digital agriculture ecosystems has significantly accelerated the expansion of the soil monitoring market. These advanced soil monitoring technologies are now embedded within broader farm management workflows. Precision farming platforms integrate soil sensor data with satellite imagery, weather forecasts, and machinery telemetry to generate actionable agronomic recommendations. There is a recognized trend, emphasized by institutions, where smallholder farmers in developing regions stand to gain significantly from adopting effective digital agricultural advisory services. The Indian government's Digital Agriculture Mission is actively working to establish a comprehensive digital infrastructure, including detailed soil mapping and digital farmer identities, to provide data-driven services to a vast number of the nation's farmers. This convergence transforms soil sensors from standalone instruments into essential nodes within interconnected agricultural data infrastructures. Cloud analytics and mobile tech are now enabling small-scale farmers to access the precise soil data that was once the exclusive domain of large agribusinesses. Consequently, the functional value of soil monitoring is no longer confined to measurement but extends to predictive modeling and automated decision support, driving deeper market penetration.

MARKET RESTRAINTS

High Initial Investment and Operational Complexity Limit Adoption Among Smallholders

The substantial upfront costs and technical complexity associated with soil monitoring systems remain significant barriers, particularly for small-scale resource-limited farmers, which in turn hampers the growth of the soil monitoring market. According to sources, the high cost of comprehensive sensor networks presents a significant barrier to their adoption by the world's hundreds of millions of small farms. In regions with predominantly small farms, such as Sub-Saharan Africa, perceived uncertainty regarding the return on investment for agricultural technology is compounded by challenges like fragmented land tenure and limited access to credit. Moreover, the operational burden of maintaining calibration data security and software updates requires digital literacy that many rural communities lack. As per studies, a significant digital divide exists, with a minority of the population in the developed countries having internet access. Even in developed economies such as smaller farms are less likely to adopt digital soil monitoring technology compared to their larger counterparts. These structural and socioeconomic constraints create a pronounced adoption gap that hinders market scalability and reinforces inequities in access to soil health intelligence.

Data Interoperability and Standardization Deficits Impede System Integration

The absence of universal data standards and interoperability protocols across soil monitoring platforms severely restricts seamless integration with existing agricultural and environmental management systems, and thereby impedes the expansion of the soil monitoring market. A significant number of soil sensor manufacturers operate globally, often utilizing diverse, non-standardized data formats and communication protocols, which creates challenges for data sharing and integration, as per research. This fragmentation complicates data aggregation andOSS-platformm analysis, which are essential for regional soil health assessments. For instance, inconsistent soil data formats among different regions and organizations present a challenge to the timely and efficient implementation of large-scale environmental regulations, such as the EU Soil Health Law. Similarly, A notable challenge in data management is that many publicly available soil datasets do not adhere to common data standards, which limits their interoperability and broader use. In precision agriculture, this lack of harmonization forces farmers to rely on a single vendor ecosystem,,s reducing flexibility and increasing long-term costs. The Food and Agriculture Organization of the United Nations emphasizes that without standardized metadata and measurement units, global soil monitoring initiatives such as the Global Soil Partnership cannot achieve their full analytical potential. Reliable and scalable soil monitoring requires universal data structure and transmission protocols, as the current lack of standardization inhibits progress.

MARKET OPPORTUNITIES

Expansion of Regenerative Agriculture Policies Creates New Monitoring Mandates

Government-backed regenerative agriculture programs are creating new opportunities for the growth of the soil monitoring market. This generates structured demand for soil monitoring by linking financial incentives to verifiable soil health metrics. Initiatives are emerging to support projects that incorporate soil organic carbon measurements using approved monitoring protocols. Programs are being established that require participating farms to demonstrate improvements in soil carbon stocks through verified data, which can involve continuous monitoring infrastructure. A growing number of countries are incorporating soil carbon sequestration targets into their climate commitments, fostering an expanding market for measurement, verification, and reporting systems. Strategies are in place within some regions to develop soil monitoring networks, with provisions for data collection across various sites. These regulatory and subsidy frameworks transform soil monitoring from a discretionary agronomic tool into a compliance necessity. "Accurate soil carbon quantification is an economic necessity for mature and growing carbon credit markets. Consequently, public policy is not only stimulating adoption but also shaping technical specifications and data validation standards within the monitoring ecosystem.

Emergence of Low-Cost Sensor Networks Enables Scalable Deployment in Developing Regions

Technological innovation in microelectronics and wireless communication has drastically reduced the cost and power requirements of soil sensors, which is setting up fresh possibilities for the expansion of the soil monitoring market. This enables large-scale deployment even in remote low-income agricultural settings. Recent developments indicate a substantial reduction in the unit cost of basic soil moisture and temperature sensors. The availability of lower-cost sensors is becoming more widespread. Solar-powered soil sensors have been distributed to small-scale agricultural users through mobile-based leasing arrangements in a specific region. The use of these sensors may improve the efficiency of water usage in agriculture. Efforts have led to the development of locally produced, cost-effective sensor nodes. These sensor nodes utilize low-power wide-area networks for data transmission over significant distances. Connectivity for these types of low-cost devices is facilitated by broad network coverage across many areas of the world. When combined with open-source analytics platforms democratizes access to soil intelligence. This cost-driven accessibility not only expands market reach but also generates high-resolution soil datasets from previously unmonitored region , enhancing both locadecision-making and global environmental models.

MARKET CHALLENGES

Persistent Calibration Drift Undermines Long-Term Data Reliability

Soil sensors are prone to calibration drift over time, which ultimately hinders the growth of the soil monitoring market. This is due to environmental stressors such as temperature fluctuations, chemical exposure, and biofouling, all of which compromise the accuracy of longitudinal soil health assessments. Unattended capacitance-based moisture sensors may show noticeable measurement errors after continuous use in certain soil conditions. Soil pH and electrical conductivity probes can experience a decline in initial accuracy over a growing season if they are not recalibrated. This degradation is particularly acute in tropical climates where high humidity and microbial activity accelerate sensor corrosion. As per sources, many commercial farms that use soil sensors do not perform regular calibration checks. Consequently, data collected from drifting sensors may misinform irrigation or fertilization decisions, leading to yield loss or environmental harm. The reliability of long-term soil monitoring programs will remain compromised by instrumental error until self-calibrating or drift-resistant sensor technologies are widely adopted.

Fragmented Regulatory Oversight Hinders Market Standardization and Consumer Trust

A regulatory vacuum, where no globally harmonized certification framework exists to validate the accuracy,yppperformanceata security of commercial soil sensors, is a major challenge to the soil monitoring market. Unlike medical or industrial instrumentation, which undergoes rigorous third-party testing, the majority of agricultural soil sensors are marketed without independent verification of their specifications. European standards bodies are currently working on guidelines for soil sensors, but these are not yet in force across member states. In the United States, official certification for agricultural sensors by a national body is not a current practice, meaning performance claims are determined by the manufacturers. Industry analysis indicates that a significant number of commonly used nutrient sensors may not meet their advertised performance parameters under typical use conditions. This lack of oversight erodes trust among end users, particularly institutional buyers such as government agencies and agribusinesses that require auditable data. Furthermore, inconsistent data privacy regulations, such as the absence of clear rules governing farm data ownership under the United States’ patchwork state laws, discourage data sharing and platform integration. Coordinated regulatory action is essential; without minimum performance benchmarks and data governance norms, market fragmentation and reputational damage could stifle the innovation and adoption of new technologies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2023 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024 to 2032 |

| CAGR | 14.1% |

| Segments Covered | By System, Offering, Application, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Stevens Water Monitoring Systems, Inc., Elementtt Materials Technology, SGS Group, Aquamonix, Campbell Scientific, The Toro Company, Meter Group, Sentek Technologies, CropX Technologies, and Spectrum Technologies. |

SEGMENT ANALYSIS

By System Insights

The ground-breaking monitoring systems segment was the largest in the soil monitoring market by capturing a 51.8% share in 2024. The leading position of the ground-breaking monitoring systems segment is credited to its unmatched ability to deliver continuous high-fidelity in situ measurements that form the bedrock of precision agronomy and environmental compliance. Ground-breaking monitoring Systems provide direct physical contact with soil, enabling precise quantification of moisture, re, semperature, and nutrient concentrations that remote methods cannot reliably replicate. Capacitance and tensiometer-based sensors can achieve high measurement accuracy for soil moisture. In regions where water efficiency is critical, farms using buried moisture sensors have significantly reduced irrigation needs while sustaining yields. Ground-based nitrate ion-selective electrodes offer reliable results that enable effective real-time nitrogen management in agricultural settings. This empirical reliability makes such systems indispensable for regulated applications, including food safety traceability and carbon credit verification, n where data defensibility is non-negotiable. Consequently, institutional buyers from cooperatives to government agencies prioritize ground systems despite higher installation costs. The operational synergy between ground sensors and mechanized input delivery systems cements their market dominance. The closed-loop automation not only conserves resources but also minimizes labor dependency, a critical advantage as rural workforce shortages intensify.

The sensing and imagery systems segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 15.2% from 2025 to 2033. The expansion of the sensing and imagery systems segment is propelled by technological convergence that transforms aerial platforms into scalable diagnostic tools. Recent breakthroughs in semiconductor manufacturing have enabled hyperspectral imagers to shrink in size and cost while increasing spectral resolution, making them viable for drone deployment. The cost of drone-mounted hyperspectral cameras has generally decreased, which facilitates wider commercial use. Hyperspectral data collected from drones can indicate soil organic matter content across various soil types. There is a trend of increased adoption and integration of agricultural drones equipped with advanced sensors, supported by various initiatives. These systems detect subtle reflectance signatures linked to soil properties such as iron oxide content and compaction that are invisible to conventional RGB or multispectral cameras. As machine learning models trained on global soil spectral libraries mature, the diagnostic power of aerial imagery approaches that of physical sampling without the spatial and temporal limitations. Sensing and Imagery Systems excel in scenarios requiring frequent monitoring of vast or inaccessible terrain where ground sensor deployment is impractical. This macro-scale perspective complements ground data by identifying spatial anomalies that warrant targeted in situ investigation. Integrating aerial and ground monitoring reduces total assessment costs while doubling spatial coverage, a value proposition driving rapid adoption among government agencies and large agribusinesses managing geographically dispersed assets.

By Offering Insights

The hardware segment held the leading share of 54.7% of the soil monitoring market in 2024. The supremacy of the hardware segment is attributed to the irreplaceable role of physical instrumentation in generating primary soil data. All soil monitoring workflows, whether for precision farming, environmental compliance o or or, or research, begin with hardware that captures raw physical or chemical signals from the soil matrix. The deployments emphasize that hardware is not merely a product but foundational infrastructure. The upfront nature of hardware investment concentrates revenue recognition in this segment as organizations budget for physical assets before subscribing to software or services. This capital intensity ensures hardware maintains revenue leadership even as the industry shifts toward service models because every subscription ultimately depends on a physical data source. The durability of these assets, typically seven to ten years for industrial sensors, also creates replacement cycles that sustain long-term demand independent of software updates or service renewals.

The services segment is expected to exhibit a noteworthy CAGR of 17.3% during the forecast period due to the market’s evolution from selling tools to delivering verified outcomes. The emergence of soil carbon markets has created demand for accredited third-party verification services that command premium pricing due to stringent methodological requirements. The Verified Carbon Standard mandates that soil carbon measurements be conducted by trained personnel using standardized protocols with data audited by independent validators. Agricultural carbon programs are providing financial opportunities to farmers through monitoring, verification, and registry services. The issuance of soil carbon credits in various regions often involves service provider attestations to ensure quality and credibility. The market for soil carbon verification services is projected to expand significantly, driven by a growing number of corporate pledges to achieve net-zero emissions. The integrity and credibility of carbon offset programs are a key focus to ensure they lead to real and permanent emission reductions. This regulatory complexity transforms soil monitoring from a technical exercise into a compliance service with recurring revenue and high barriers to entry based on accreditation and audit trail integrity. Agricultural enterprises are increasingly outsourcing the entire soil monitoring workflow to service providers who handle deployment, maintenance, data interpretation, and agronomic recommendations. Financial institutions are reinforcing this trend. This outcome-based model aligns provider incentives with farm performance, creating sticky customer relationships and predictable revenue streams that fuel service segment growth.

By Application Insights

The agricultural application segment dominated the soil monitoring market by occupying a substantial share in 2024. The dominance of the agricultural application segment is driven by soil’s central role in crop productivity and resource stewardship. Contemporary agriculture relies on soil data to optimize the application of water, fertilizers, and amendments, minimizing waste while maximizing yield. Variable-rate nitrogen application guided by real-time soil sensors may help in reducing nitrogen overuse. The use of soil moisture data can inform irrigation scheduling, which could lead to water savings. A scheme involving soil health guidance appears to be integrating sensor validation, potentially leading to increased crop yields among participants. Soil monitoring practices might help farmers optimize the use of inputs, potentially reducing application costs through precise targeting of soil conditions. These economic benefits create self-reinforcing adoption cycles where input savings fund further technology investments,,t, making oil monitoring a core component of farm financial viability. Governments worldwide are linking farm subsidies and market access to demonstrable soil stewardship verified through monitoring. This policy architecture transforms monitoring from a discretionary tool into a compliance requirement, ensuring structural demand that persists regardless of commodity price fluctuations.

The non-agricultural applications segment is predicted to witness the highest CAGR of 19.1% over the forecast period. The swift acceleration of the non-agricultural applications segment is fuelled by regulatory mandates and infrastructure resilience imperatives. Industrial facilities and municipalities face increasing legal obligations to monitor soil conditions during and after remediation to prevent liability exposure. Regulatory requirements in the United States emphasize continuous monitoring of soil vapor and moisture at remediation sites. The European Union maintains strict regulations concerning long-term soil monitoring recordkeeping for industrial installations after they are closed. Redevelopment projects for previously used commercial or industrial land in Japan commonly incorporate permanent soil monitoring infrastructure as a standard practice.ce These regulatory requirements generate high-value contracts for environmental consulting firms that bundle sensor deployment, data management, and regulatory reporting into turnkey services. Civil engineering projects increasingly embed soil sensors to detect early signs of subsidence, erosion,, moisture-induced instability that could compromise structural safety. The risk mitigation value justifies premium pricing for specialized monitoring services, particularly in energy transportation and urban development sectors, where public safety and asset longevity are paramount.

REGIONAL ANALYSIS

North America Market Analysis

North America outperformed other regions in the global soil monitoring market by capturing a 35.5% share in 2024. The region’s dominance is attributed to advanced technological adoption, robust policy support, and extensive research infrastructure. There is a significant public soil monitoring network providing data used in both public policy and private innovation. Government programs continue to allocate substantial funds to support on-farm conservation methods, including technology for soil data collection. Soil health monitoring initiatives operate across a wide area in Canada, focusing on measurements related to environmental benefits like carbon storage. Widespread rural high-speed internet access across the region facilitates efficient data transmission for various technologies. Private investment in agricultural technology is robust, supporting ongoing advancements in soil monitoring for commercial agriculture.

Europe Market Analysis

Europe was the second largest region in the global soil monitoring market and held a 27.1% share in 2024 because of harmonized environmental regulations and coordinated policy frameworks that mandate soil health assessment. The European Union has adopted its first-ever soil legislation, the Soil Monitoring Law, which requires member states to establish national soil monitoring systems using a common EU methodology to assess physical, chemical, and biological conditions, with an aspirational goal of achieving healthy soils by 2050. European countries are involved in research and innovation to support a transition to more sustainable farming practices, often leveraging digital tools and data to inform better soil management and reduce environmental impact. The integration of soil monitoring into mainstream agricultural practice is both deep and institutionally reinforced.

Asia Pacific Market Analysis

Asia Pacific is an attractive region in the soil monitoring market due to massive government-led digital agriculture initiatives aimed at food security and resource efficiency. Soil monitoring infrastructure is being developed in a large number of agricultural regions. Efforts are underway to expand soil data collection to a greater number of individual agricultural holdings using both physical testing and digital methods. There is an investment in national soil monitoring programs, which includes a focus on measuring soil components like carbon. The region faces acute pressure from land degradation. This environmental urgency, combined with rapidly improving rural connectivity, creates fertile ground for scalable monitoring solutions tailored to smallholder realities.

Latin America Market Analysis

Latin America expanded steadily in the global soil monitoring market, with large-scale commodity production systems where soil monitoring directly enhances export competitiveness. Brazil leads the region. Its agricultural initiatives include programs designed to support low-carbon technology adoption, which incorporates methods for monitoring soil carbon. Argentina has developed a system that integrates different data types, including satellite information, to facilitate its domestic carbon market. Chile's fruit export industry has implemented a requirement for producers to monitor soil moisture as part of its general certification standards, promoting efficient water management. The region generally offers environmental conditions that are suitable for the functionality and longevity of sensor technology in key agricultural zones. The implementation of monitoring technologies varies considerably, with a marked difference between their use on small farms compared to larger operations. This disparity indicates a potential area for expansion and development as various approaches to funding and adoption continue to emerge.

Middle East And Africa Market Analysis

The Middle East and Africa region is predicted to grow notably in the soil monitoring market over the forecast period. Despite its modest share, the region exhibits high strategic importance due to extreme water scarcity and land degradation pressures. Government initiatives in one nation encourage soil moisture monitoring as part of agricultural water management. In another region, the integration of precision agriculture, including the use of soil sensors, is a widespread practice on irrigated farms to enhance water use efficiency. Across parts of a major continent, there are projects involving the deployment of cost-effective sensors to aid in the development of drought early warning capabilities. Environmental reports indicate that a significant portion of the continent's agricultural land is experiencing degradation, highlighting the need for monitoring to support restoration efforts. The region's market potential is considerable thanks to better satellite coverage and mobile money-supported pay-as-you-go sensor leasing, though infrastructure remains a challenge.

COMPETITIVE LANDSCAPE

The soil monitoring market features a dynamic competitive landscape characterized by a mix of specialized sensor manufacturers, diversified agritech corporations, and emerging startups. Competition centers on technological differentiation, ion, data accuraeaseeasese of integration, nd service reliability rather than price alone. Established players leverage decades of agronomic research and global distribution networks, while newer entrants focus on disruptive business models such as sensor as a service or carbon credit linkage. The absence of universal technical standards intensifies product differentiation as companies develop proprietary calibration methods and communication protocols. Strategic alliances with equipmentOEMsplatformssms environmental certifiers are critical for scaling. Regulatory developments, particularly around soil carbon and water use, are reshaping competitive priorities with firms racing to align offerings with verification requirements. This environment fosters continuous innovation but also creates fragmentation that challenges interoperability and customer adoption.

KEY MARKET PLAYERS

These are some of the market players that dominate the global soil monitoring market.

- Stevens Water Monitoring Systems, Inc

- Element Materials Technology

- SGS Group

- Aquamonix

- Campbell Scientific

- The Toro Company

- Meter Group

- Sentek Technologies

- CropX Technologies

- Spectrum Technologies.

Top Players In The Market

- Sentek Technologies is a globally recognized innovator in soil monitoring solutions, specializing in capacitive-based sensor systems that deliver high-accuracy moisture and salinity data. The company serves agricultural research institutions, commercial far, and environmental agencies across multiple countries. In recent years, Sentek has enhanced its product portfolio by integrating wireless telemetry and cloud-based analytics, enabling real-time remote access to soil conditions. Its EnviroSCAN and Drill and Drop probe systems are widely adopted for their durability and precision in diverse soil types. Sentek’s strategic collaborations with irrigation equipment manufacturers and digital agronomy platforms have expanded its ecosystem integration, reinforcing its relevance in precision farming and sustainable land management initiatives worldwide.

- METER Group delivers advanced soil monitoring instrumentation combining decades of scientific expertise with robust engineering for field and laboratory applications. Known for its TEROS sensor line, the company provides reliable measurements of water content,,nt water potential,, temperatur,,e and electrical conductivity. METER actively supports global research networks, including those coordinated by the United Nations and national agricultural departments. METER's emphasis on scientific validity and user-centric design has solidified its standing among agronomists, hydrologists, and environmental scientists who need reliable data for decision-making in both commercial and regulatory environments.

- Teralytic leverages Internet of Things technology to offer real-time nitrogen, moisture, and temperature monitoring through wireless probe networks tailored for modern agronomic practices. The company’s platform integrates seamlessly with major farm management software, enabling actionable insights for nutrient optimization and emissions reduction. Teralytic has focused on sustainability-driven markets, particularly in North America and Europe, where regulatory pressure and carbon credit programs incentivize precise soil management. This strategic alignment with climate-smart agriculture trends has positioned Teralytic as a key enabler of data-driven environmental compliance and input efficiency for progressive farming operations.

Top Strategies Used By The Key Market Participants

Key players in the soil monitoring market employ several core strategies to reinforce their competitive stance. Product innovation remains central with companies continuously enhancing sensor accuracy, battery life, and connectivity features. Strategic partnerships with agritech platforms, irrigation system providers, and government agencies enable deeper market penetration and ecosystem integration. Geographic expansion, particularly into emerging economies with high agricultural activity, allows access to new customer bases. Investment in cloud-based analytics and mobile applications improves user experience and data utility. Companies also prioritize compliance with international environmental and data standards to qualify for public sector contracts and carbon market participation. Additionally m,, many firms adopt subscription-based service models to generate recurring revenue and strengthen customer retention through ongoing support and insights.

MARKET SEGMENTATION

This market research report on the global soil monitoring market has been segmented and sub-segmented based on system, offering, application,,n and region.

By System

- Ground-based Monitoring Systems

- Sensing and Imagery Systems

- Others (Telematics Systems and Robotics)

By Offering

- Software

- Hardware

- Services

By Application

- Non-Agricultural

- Agricultural

By Country

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the global soil monitoring market about?

It includes tools and digital systems that help farmers and land managers understand soil conditions — such as moisture levels, nutrient balance, and overall soil health — so they can make smarter decisions.

Why is soil monitoring becoming important worldwide?

Because climate uncertainty, water scarcity, and rising food demand make it essential to manage soil more intelligently rather than relying on guesswork.

What is driving the growth of soil monitoring solutions?

A shift toward precision farming, pressure to use fertilizer more responsibly, and the need to boost yields without harming ecosystems are major drivers.

Who uses soil monitoring technologies the most?

Crop growers, greenhouse operators, orchard managers, research institutions, and even environmental agencies rely on soil data to guide their activities.

What types of soil monitoring methods are commonly used?

On-field sensors, remote sensing tools, satellite data, handheld probes, and software platforms that turn field readings into actionable recommendations.

Why do farmers adopt soil monitoring?

Having real-time information helps them irrigate efficiently, detect nutrient gaps early, and improve plant quality which saves money and protects soil health.

What challenges slow adoption globally?

Cost of equipment, limited awareness in rural areas, variable soil conditions across regions, and the need for training to interpret collected data.

How is technology changing soil monitoring?

Devices are becoming more wireless, automated, and connected — turning soil monitoring into a system that works continuously rather than through occasional testing.

Which regions show strong interest in soil monitoring?

Areas with water scarcity, high-value crops, or advanced farming systems — for example, regions growing fruits, vegetables, nuts, or greenhouse produce — tend to adopt these tools faster.

What is the future outlook for the soil monitoring market?

As food systems shift toward sustainability and digital farming becomes mainstream, soil monitoring is likely to move from a “nice-to-have” tool to a normal part of global agricultural practice.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com