Global Healthcare Staffing Market Size, Share, Trends & Growth Forecast Report By Services Type and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Market Size, 2025

$39.53 BnMarket Estimate, 2026

$42 BnMarket Forecast, 2034

$68.16 BnCAGR, 2026–2034

6.24%Global Healthcare Staffing Market Report Summary

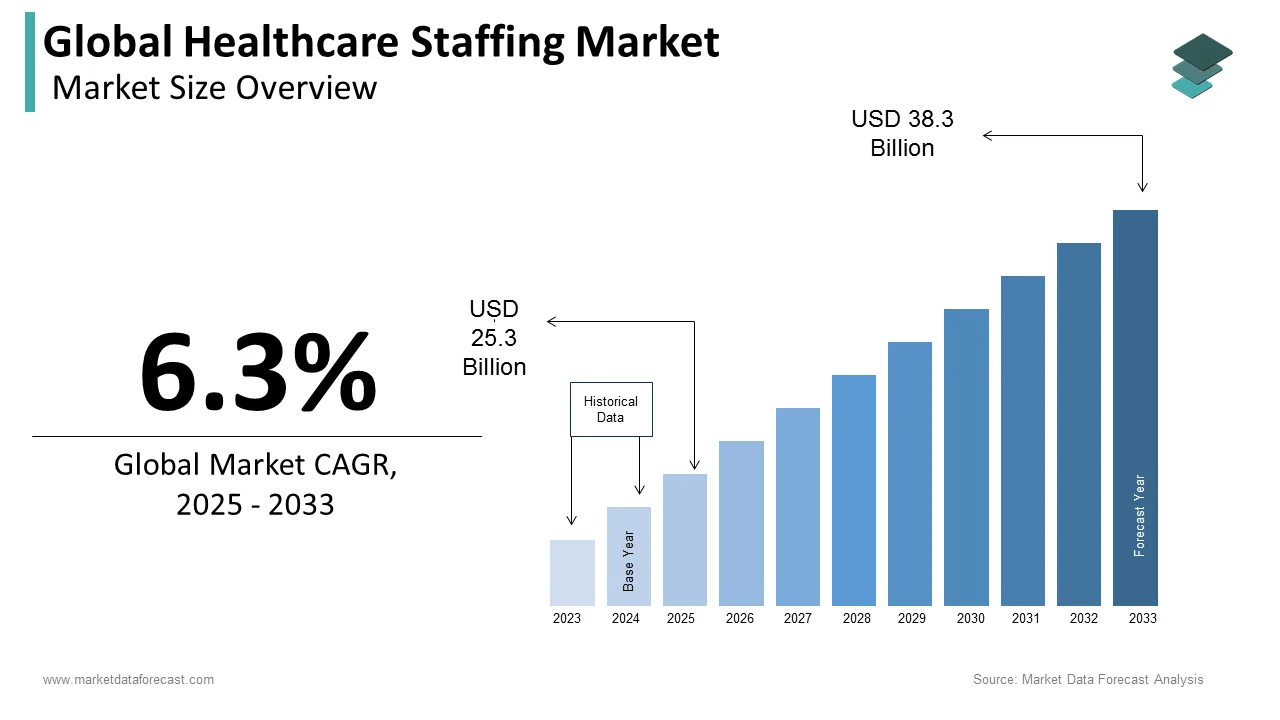

The global healthcare staffing market was valued at USD 39.53 billion in 2025 and is projected to grow from USD 42 billion in 2026 to USD 68.16 billion by 2034, registering a CAGR of 6.24% from 2026 to 2034. Market growth is driven by rising healthcare workforce shortages, increasing demand for flexible staffing solutions, and growing patient volumes across hospitals and healthcare facilities. The expansion of aging populations, increasing prevalence of chronic diseases, and rising pressure on healthcare systems are accelerating demand for temporary and contract healthcare professionals. Additionally, the growing adoption of outsourced staffing models and digital workforce management platforms is further supporting market expansion globally.

Key Market Trends

- Rising demand for temporary and flexible healthcare workforce solutions.

- Increasing adoption of travel nurse staffing and locum tenens services.

- Growing integration of digital staffing platforms and workforce management technologies.

- Expansion of outsourced healthcare staffing models across hospitals and clinics.

- Increasing healthcare workforce shortages due to aging populations and rising chronic disease burden.

Segmental Insights

- Based on service type, the travel nurse staffing segment dominated the global healthcare staffing market in 2025 by accounting for 43.4% market share, driven by rising nursing shortages, increasing patient admissions, and growing demand for flexible staffing support across healthcare facilities.

Regional Insights

The global healthcare staffing market is witnessing steady growth across major regions, supported by increasing healthcare expenditure, workforce shortages, and expanding healthcare infrastructure.

- North America led the global market in 2025 with 44.9% share, driven by strong demand for temporary healthcare professionals, advanced healthcare infrastructure, and high healthcare spending.

- Europe followed with 24.6% share in 2025, supported by aging populations, workforce shortages, and increasing reliance on outsourced staffing services.

- Asia-Pacific remains a significant and rapidly expanding regional market, driven by healthcare infrastructure development, rising chronic disease prevalence, and growing adoption of outsourced healthcare staffing models.

Competitive Landscape

The global healthcare staffing market is characterized by strong competition among staffing agencies, workforce management companies, and healthcare outsourcing providers, focusing on talent acquisition, workforce flexibility, and digital staffing solutions. Market players are emphasizing the expansion of specialized staffing services, integration of AI-driven recruitment technologies, and the strengthening of healthcare workforce networks to enhance market positioning. Strategic acquisitions, partnerships, and investments in workforce management platforms are shaping competitive dynamics across the market.

Prominent companies operating in the global healthcare staffing market include Adecco, AMN Healthcare, CHG Management, Syneos Health, TeamHealth (Blackstone), Accountable Healthcare Staffing, Aya Healthcare, InGenesis, Medical Solutions, Supplemental Health Care, EmCare, Almost Family, Cross Country Healthcare, Maxim Healthcare Services, Jackson Healthcare, Aureus Medical Group (C&A Industries), Favorite Healthcare Staffing, Healthcare Staffing Services, and Trustaff.

Global Healthcare Staffing Market Size

The global healthcare staffing market was worth US$ 39.53 billion in 2025 and is anticipated to reach a valuation of US$ 68.16 billion by 2034 from US$ 42 billion in 2026, and it is predicted to register a CAGR of 6.24% during the forecast period 2026 to 2034.

Healthcare staffing is the process of recruiting, evaluating, and placing qualified medical professionals, such as doctors, nurses, technicians, and administrative staff, into healthcare facilities. This ecosystem addresses the operational necessity of aligning specialized personnel with fluctuating patient volumes and evolving care delivery models. The sector operates at the intersection of human capital management and clinical service continuity, ensuring that hospitals, outpatient centers, and extended duration care institutions maintain adequate staffing ratios without compromising care quality. Demographic shifts and epidemiological transitions heavily influence the structural demand for medical personnel. According to the World Health Organization, the global population of people aged 60 and older reached 1.1 billion individuals in 2023. The global population of individuals over 60 is actually projected to reach 1.4 billion by the year 2030, and will double to 2.1 billion by 2050. The Centers for Disease Control and Prevention states that 6 in 10 adults in the United States currently manage at least 1 chronic condition, which increases the frequency of clinical interventions and diagnostic monitoring. These macro level indicators establish a foundational necessity for agile workforce deployment mechanisms that transcend traditional employment frameworks. Healthcare organizations now rely on external staffing networks to mitigate operational disruptions and sustain clinical throughput.

MARKET DRIVERS

Elevated prevalence of age-associated pathologies amplifies clinical personnel requirements

The progressive demographic transition toward older populations fundamentally alters care delivery paradigms and creates sustained demand for specialized medical professionals, thereby driving growth in the healthcare staffing market. Elderly patients typically require extended monitoring, polypharmacy management, and rehabilitative interventions that exceed the capacity of standard clinical teams. According to the World Health Organization, the global population of individuals aged 60 and older reached 1.1 billion in 2023 and is projected to reach 1.4 billion by 2030. The population aged 65 and older is projected by the UN to reach 16% of the global population by 2050. United Nations and WHO records confirm that global life expectancy at birth grew from 67 years in 2000 to 73.3 years in 2024, which marks an increase of 6.3 years. While certain high-risk developing sub-regions experienced a 9.4-year jump during malaria and HIV mitigation windows. Hospitals face structural capacity pressures due to an aging demographic, with case studies shared by the International Hospital Federation highlighting that senior patients drive a disproportionate share of acute-care bed utilization and average length of stay compared to younger patient demographics. This utilization pattern forces healthcare administrators to recruit supplementary nursing staff, respiratory therapists, and physical rehabilitation specialists to maintain acceptable patient-provider ratios. Temporary staffing agencies fulfill this demand by maintaining ready pools of credentialed professionals who can be deployed during seasonal surges or unexpected admission spikes. The reliance on flexible workforce models enables medical facilities to scale clinical capacity without incurring fixed employment costs, thereby aligning human resource allocation with actual patient care requirements. Consequently, the demand for adaptable clinical talent remains inelastic despite economic fluctuations, as patient volumes dictate immediate staffing interventions rather than extended hiring cycles.

Persistent workforce attrition drives reliance on external staffing networks

Clinical professionals face intense operational pressures that frequently exceed sustainable workloads, prompting many to leave permanent positions or reduce their clinical hours, which fuels the expansion of the healthcare staffing market. The American Medical Association documents that while physician burnout reached historic highs post-pandemic, recent data shows the share of physicians reporting at least one burnout symptom has declined to roughly 42%, though administrative burdens continue to threaten institutional retention. The International Council of Nurses reports that widespread exhaustion and inadequate recovery periods have severely strained the global workforce, with local surveys indicating a substantial portion of registered nurses intend to leave their current positions or the profession entirely. These attrition metrics create immediate vacancy gaps that disrupt patient care continuity and strain remaining staff members. Healthcare administrators utilize contingent staffing solutions to bridge these operational voids while permanent recruitment pipelines remain active. Travel nurse placements, locum tenens physicians, and contract allied health professionals provide immediate clinical coverage without compromising accreditation standards. According to the Bureau of Labor Statistics, the healthcare and social assistance sector consistently faces millions of unfilled job openings, maintaining a high job-opening rate that requires rapid, adaptive recruitment mechanisms that traditional human resource departments struggle to sustain. Flexible staffing arrangements allow facilities to maintain regulatory compliance and service delivery benchmarks while permanent recruitment processes address extended workforce stabilization. The structural dependency on temporary personnel has therefore evolved from a reactive measure to a core operational strategy for sustaining clinical throughput. This dynamic ensures that patient safety protocols remain intact during transitional employment phases.

MARKET RESTRAINTS

Stringent credential verification protocols extend deployment timelines

Healthcare facilities operate within heavily regulated environments, which inhibits the growth of the healthcare staffing market. These mandates ensure comprehensive background validation, license authentication, and clinical competency assessments before any external professional begins patient care. The Joint Commission requires healthcare organizations to execute primary source verification for all clinical credentials, a meticulous process that routinely extends temporary clinician onboarding timelines by 3 to 6 weeks before deployment authorization. The National Council of State Boards of Nursing (NCSBN) indicates that 41 U.S. states have enacted the Nurse Licensure Compact (NLC), allowing multi-state licensees to bypass traditional state-by-state registration delays and deploy rapidly during localized staffing shortages. These administrative bottlenecks restrict rapid workforce mobilization and reduce the operational flexibility that healthcare staffing solutions are designed to provide. Facilities frequently experience extended vacancy periods during critical staffing shortages because compliance procedures cannot be expedited without violating accreditation standards. The American Hospital Association highlights that persistent clinical labor shortages and complex onboarding requirements leave hospital human resource infrastructures severely strained, creating operational bottlenecks for external staffing onboarding. This friction between regulatory requirements and urgent staffing needs forces healthcare administrators to maintain larger internal buffer teams, which increases fixed labor expenditures and diminishes the cost efficiency of contingent workforce models. Consequently, staffing agencies must invest heavily in compliance infrastructure to navigate these procedural constraints while preserving service delivery timelines. The administrative burden ultimately constrains market agility and limits rapid response capabilities during acute clinical demand surges.

Public reimbursement limitations constrain flexible staffing expenditures

Publicly funded healthcare systems and publicly insured patient populations operate under fixed payment structures that restrict the financial capacity to absorb premium contract labor costs, and thereby hamper the expansion of the global healthcare staffing market. According to data reviewed by the American Hospital Association, Medicare underpayments routinely leave acute care reimbursement rates more than 11% below actual clinical delivery expenses, forcing hospitals to restrict operational labor budgets. The Organisation for Economic Co-operation and Development notes that while European public health systems face severe budgetary constraints, diverse localized fiscal regulations and national health frameworks govern the exact limits placed on temporary labor compensation. Financial administrators frequently prioritize permanent hiring over contingent arrangements to stabilize operational expenditures, even when temporary solutions offer superior immediate adaptability. Reports from the American Hospital Association indicate that severe financial pressures have left over 50% of rural hospitals with negative operating margins, limiting their financial capacity to absorb premium contract staffing costs. These fiscal boundaries compel healthcare networks to rely on overtime distributions among existing staff rather than engaging external workforce partners, which inadvertently elevates burnout risks and compromises scheduling flexibility. The resulting financial compression restricts the expansion of healthcare staffing enterprises within publicly financed medical ecosystems and forces agencies to recalibrate pricing models to align with constrained institutional budgets. This economic pressure necessitates strategic workforce planning that balances fiscal responsibility with clinical coverage requirements.

MARKET OPPORTUNITIES

Virtual care delivery models generate unprecedented demand for remote clinical personnel

The rapid integration of digital health platforms has transformed traditional patient-provider interactions and created new operational requirements for geographically dispersed medical teams, which offer significant opportunities for the healthcare staffing market. The American Telemedicine Association highlights that the permanent integration of hybrid healthcare requires organizations to reconfigure existing labor pipelines, utilizing virtual nursing to alleviate bedside burdens rather than creating independent staffing units. The World Health Organization notes that digital health interventions and remote patient monitoring are essential for strengthening primary healthcare frameworks, expanding care access, and optimizing global workforce distribution. Healthcare staffing agencies capitalize on this transition by curating talent pools specifically trained in digital communication protocols, electronic documentation standards, and remote patient engagement techniques. The expansion of residential care networks further amplifies the requirement for mobile clinical professionals who can operate independently while maintaining digital connectivity with centralized medical command centers. National health tracking reports indicate that while peak pandemic surges have receded, virtual medical encounters have stabilized at roughly 5% to 11% of overall outpatient visits, cementing a permanent baseline demand for remote care coordinators. This structural shift enables staffing enterprises to develop niche service offerings that address digital care delivery requirements, thereby diversifying revenue streams and reducing dependency on traditional hospital placement models. The integration of virtual care into standard clinical pathways establishes a sustainable foundation for distributed workforce deployment.

Predictive analytics platforms enable proactive workforce alignment strategies

Advanced computational systems now analyze historical admission patterns, seasonal disease prevalence, and live patient flow metrics to forecast clinical personnel requirements with unprecedented accuracy, which is anticipated to amplify the expansion of the healthcare staffing market. The Healthcare Information and Management Systems Society notes that advanced digital health platforms allow medical networks to automate core scheduling operations, mitigating workforce supply gaps by predicting localized patient surges. The National Academy of Medicine emphasizes that deploying predictive workforce analytics can mitigate systemic administrative burdens, helping to prevent the operational friction that accelerates clinician burnout. Healthcare staffing agencies leverage these analytical frameworks to predeploy qualified professionals before anticipated demand surges occur, thereby transforming reactive deployment into strategic workforce planning. Algorithmic matching systems evaluate clinician competencies against specific departmental requirements, which minimizes skill mismatches and accelerates credential verification processes. Economic analysis from the Brookings Institution underscores that the widespread adoption of predictive labor technologies allows healthcare employers to optimize recruitment pipelines and respond rapidly to localized clinical shortages. This technological advancement allows staffing enterprises to operate with enhanced precision, optimize resource allocation, and establish extended partnerships with healthcare institutions that prioritize information-based workforce management. Consequently, market participants who adopt these analytical tools secure competitive advantages through superior service reliability and optimized placement efficiency. The convergence of artificial intelligence and human capital deployment represents a transformative pathway for sustainable clinical operations.

MARKET CHALLENGES

Clinical competency gaps restrict the immediate deployment of specialized personnel

Modern clinical institutions are continuously seeking personnel with highly specialized diagnostic skills and advanced procedural mastery that go beyond traditional medical curricula, which challenges the growth of the healthcare staffing market. The Association of American Medical Colleges documents a severe structural gap in the physician pipeline, projecting a national shortage of up to 86,000 doctors by 2036, with acute shortfalls concentrated heavily within surgical subspecialties, critical care, and anesthesia. Industry workforce data highlights that a significant portion of newly deployed or contract nurses require robust on-site orientation and clinical competency validation to safely navigate advanced medical equipment and high-acuity patient environments. Staffing agencies frequently encounter placement delays when candidate skill profiles do not align with precise clinical requirements, forcing facilities to either extend onboarding periods or compromise on expertise levels. National residency and fellowship match data indicate that limited training capacities and rigid institutional funding caps consistently prevent hundreds of qualified applicants from securing positions, constraining the pipeline of highly specialized clinicians. This educational bottleneck forces healthcare networks to invest heavily in continuous professional development while relying on temporary staff for routine clinical coverage. The resulting competency misalignment complicates workforce matching processes and increases operational friction for staffing enterprises attempting to fulfill highly specific institutional requirements. Addressing these training deficiencies requires expanded simulation programs and accelerated certification pathways.

Regional workforce concentration imbalances impede equitable clinical access

Geographical disparities in the distribution of healthcare professionals severely restrict equitable access to medical care, which negatively impacts the expansion of the healthcare staffing market. Clinical professionals predominantly concentrate within metropolitan healthcare ecosystems due to superior compensation structures, advanced facility infrastructure, and expanded career development pathways. The World Health Organization highlights a severe global maldistribution of healthcare workers, noting that while roughly half of the world's population resides in rural areas, they are served by less than 25% of the global physician workforce. The National Rural Health Association confirms that systemic staffing shortages plague rural health networks, leaving a vast majority of remote medical centers vulnerable to critical personnel deficits and operational instability. Healthcare staffing agencies encounter substantial logistical barriers when attempting to deploy qualified professionals to geographically isolated regions due to housing limitations, transportation constraints, and professional isolation concerns. Federal economic data indicate that rural hospitals experience disproportionately higher vacancy and turnover rates than urban facilities, forcing rural administrations to rely heavily on premium travel staffing contracts that strain institutional budgets. Geographic distribution challenges complicate workforce planning and require specialized incentive frameworks to attract clinical talent to underserved locations. The persistent spatial mismatch between professional concentration and population distribution creates structural inefficiencies that restrict market penetration and limit the scalability of staffing solutions across decentralized healthcare networks. Addressing these spatial disparities requires coordinated policy interventions and targeted recruitment strategies that align professional incentives with community healthcare requirements.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Service Type and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Market Leaders Profiled | Adecco, AMN Healthcare, CHG Management, Syneos Health, TeamHealth (Blackstone), Accountable Healthcare Staffing, Aya Healthcare, InGenesis, Medical Solutions, Supplemental Health Care, EmCare, Almost Family, Cross Country Healthcare, Maxim Healthcare Services, Jackson Healthcare, Aureus Medical Group (C&A Industries), Favorite Healthcare Staffing, Healthcare Staffing Services, and Trustaff., and Others. |

SEGMENTAL ANALYSIS

By Service Type Insights

The travel nurse staffing segment dominated the healthcare staffing market, accounting for a 43.4% share in 2025. This segment’s dominance was driven by its unique capacity to address acute clinical shortages while providing healthcare facilities with operational agility during demand fluctuations. Travel nurse staffing enables healthcare organizations to rapidly mobilize credentialed professionals across geographic regions without long-term employment commitments. The Association of American Medical Colleges projects a systemic national physician shortfall reaching up to 86,000 doctors by 2036, structurally intensifying institutional reliance on temporary clinical talent. Hospitals frequently navigate predictable seasonal admission surges that outpace permanent floor-staffing capacity, necessitating immediate partnerships with travel nursing agencies capable of rapid, short-term workforce deployment. The Bureau of Labor Statistics forecasts an average of 194,500 annual registered nurse job openings through 2033, driven by retirements and workforce transitions that domestic academic pipelines struggle to satisfy entirely. Travel nurses bring specialized competencies in critical care, emergency medicine, and perioperative services that are scarce in rural and underserved markets. This segment also benefits from competitive compensation structures that attract experienced clinicians seeking schedule autonomy and geographic diversity. Healthcare administrators strategically utilize contingent staffing to alleviate chronic internal staff burnout and curb compounding internal overtime expenses, while safely maintaining mandate-compliant nurse-to-patient ratios. The integration of modern mobile credentialing and digital wallet platforms significantly accelerates onboarding timelines, allowing travel clinicians to clear background checks and begin clinical assignments much faster than legacy human resource pipelines allow. Consequently, this segment sustains market leadership through superior responsiveness to dynamic clinical workforce requirements.

Moreover, financial rewards and professional development opportunities significantly influence nurse participation in travel staffing programs. Travel nurses earn higher hourly compensation compared to permanent staff, according to the National Council of State Boards of Nursing, which motivates experienced clinicians to pursue contract-based roles. Healthcare facilities benefit from reduced benefit liabilities since travel staff typically receive stipends rather than comprehensive employment packages. This cost structure enables hospitals to allocate resources toward capital investments and technology upgrades while maintaining clinical service levels. Additionally, travel assignments provide clinicians with exposure to diverse electronic health record systems and care protocols, enhancing their marketability for future permanent roles. The rise of digital staffing platforms has simplified application processes, allowing nurses to secure assignments in under 48 hours through mobile interfaces. These economic and technological enablers reinforce travel nurse staffing as the predominant service model within the healthcare staffing ecosystem.

On the other hand, the locum tenens staffing segment is anticipated to witness the fastest CAGR of 7.6% from 2026 to 2034 due to structural shifts in physician practice patterns and evolving healthcare delivery models that prioritize flexible clinical coverage. According to the American Medical Association, more than 45% of practicing physicians in the United States are over the age of 55, positioning a significant portion of the workforce near retirement age and prompting facilities to plan for long-term clinical replacement. Locum tenens arrangements enable healthcare systems to maintain service continuity while recruiting permanent replacements, a process that typically requires 6 to 9 months for specialized roles. The Association of American Medical Colleges projects a national shortage of up to 86,000 physicians by 2036 across primary care and specialized surgical categories, straining hospital capabilities to maintain regular procedural volumes. Rural hospitals experience the most acute gaps. The National Rural Health Association emphasizes that rural health systems face disproportionate recruitment obstacles, with a medical specialist shortage nearly eight times more severe than in urban areas, leading to acute care gaps. Locum tenens physicians fill these voids while bringing diverse clinical perspectives that enhance care quality metrics. Additionally, physician assistants and nurse practitioners are increasingly utilized in locum capacities. This expansion of eligible provider types broadens the addressable market for locum services and supports sustained segment growth across multiple clinical disciplines.

In addition, policy adjustments and digital health adoption have removed traditional barriers to locum tenens utilization across state and institutional boundaries. Telehealth platforms enable locum providers to deliver remote consultations, expanding their reach beyond physical facility constraints. Healthcare systems increasingly integrate locum providers into hybrid care models that combine in-person and virtual services, optimizing resource allocation across patient populations. These regulatory and technological enablers position locum tenens staffing for accelerated adoption as healthcare delivery continues to evolve toward flexible, distributed care models.

REGIONAL ANALYSIS

North America Healthcare Staffing Market Analysis

North America led the global healthcare staffing market and captured a 44.9% share in 2025. This leading position of the North American market was attributed to advanced healthcare infrastructure, persistent workforce shortages, and robust adoption of flexible staffing solutions across the United States and Canada. The United States accounts for the majority of regional revenue, driven by high healthcare expenditure, an aging population, and regulatory mandates requiring specific nurse-patient ratios. According to the Bureau of Labor Statistics, the healthcare and social assistance sector is projected to add approximately 2.6 million new jobs through 2033, intensifying competition for qualified clinical talent. The American Hospital Association reports that contract labor expenses have surged by over 250% since 2019, reflecting a sustained, critical reliance on external staffing agencies to address vacancy gaps. Canada contributes through its publicly funded system, where temporary staffing addresses regional disparities in rural and northern communities. Government initiatives, including immigration reforms for healthcare workers and funding for workforce retention programs, further support market expansion. Digital staffing platforms have achieved widespread adoption, with over 60 percent of US facilities using algorithmic matching tools to optimize candidate placement according to the Healthcare Information and Management Systems Society. These structural advantages position North America to retain its market leadership through the forecast period while driving innovation in workforce management technologies.

Europe Healthcare Staffing Market Analysis

Europe followed closely behind in the healthcare staffing market and occupied a share of 24.6% in 2025. Regional growth is propelled by healthcare system reforms, demographic aging, and cross-border workforce mobility initiatives within the European Union. Germany, the United Kingdom, and France represent the largest national markets due to substantial public healthcare budgets and persistent nursing shortages. The World Health Organization estimates that the European Region will face a deficit of nearly 1.2 million healthcare workers by 2030, necessitating robust retention strategies and reliance on agency-supplied clinical staff. The European Commission has implemented standardized credentialing frameworks that facilitate professional mobility across member states, expanding the available talent pool for staffing agencies. According to the Organisation for Economic Co-operation and Development, many European nations face critical retention challenges, with nurse vacancy rates in countries like the United Kingdom exceeding 9%, driving demand for temporary cross-border solutions. The United Kingdom experiences additional pressure from post Brexit workforce adjustments, with the National Health Service increasingly partnering with private staffing firms to maintain service levels. Digital transformation initiatives, including electronic credential verification and AI-driven candidate matching, are gaining traction across European markets, improving placement efficiency. These factors collectively support Europe's significant market position while creating opportunities for staffing enterprises that can navigate diverse regulatory environments and deliver compliant workforce solutions.

Asia Pacific Healthcare Staffing Market Analysis

Asia Pacific continues to be a significant regional market. This region shows the highest growth potential driven by rapid healthcare infrastructure expansion, rising chronic disease prevalence, and increasing adoption of outsourced staffing models. China and India lead regional demand due to large populations, government healthcare investments, and growing private hospital networks. According to the United Nations and WHO, the Asia Pacific region is home to 60% of the global population, with a rapidly aging demographic that will see one in four individuals aged over 60 by 2050, creating unprecedented demand for geriatric clinical services. The Chinese government's Healthy China 2030 initiative allocates substantial funding toward hospital construction and workforce development, stimulating demand for both permanent and temporary clinical staff. India faces acute nursing shortages, with rural health centers experiencing vacancy rates as high as 27% for clinical posts, while urban tertiary care centers struggle to maintain optimal nurse-to-patient ratios. Japan and South Korea contribute through aging demographics that increase geriatric care requirements and drive demand for specialized nursing and rehabilitation professionals. Digital health adoption is accelerating across the region, with telehealth platforms enabling remote staffing solutions for underserved rural communities. These macroeconomic and demographic trends position Asia Pacific for accelerated market share gains in the coming decade.

Latin America Healthcare Staffing Market Analysis

Latin America occupies a noteworthy position in the global healthcare staffing market with emerging growth opportunities concentrated in Brazil, Mexico, and Argentina. Regional expansion is supported by increasing healthcare access initiatives, rising middle-class populations, and growing private hospital investments. Brazil leads regional adoption due to its large population, universal healthcare system, and expanding private insurance coverage that increases utilization of clinical services. Mexico benefits from proximity to the United States, enabling cross-border staffing arrangements and knowledge transfer of best practices in workforce management. Argentina experiences economic volatility that complicates healthcare financing but also drives cost-conscious adoption of flexible staffing models to manage labor expenditures. Digital infrastructure improvements are enabling mobile-based recruitment platforms that connect clinical talent with facilities in remote regions. Regulatory harmonization efforts within regional trade blocs are beginning to facilitate professional mobility, though progress remains slower than in Europe or North America. These factors position Latin America for steady but measured growth in healthcare staffing adoption over the forecast period.

Middle East and Africa Healthcare Staffing Market Analysis

The Middle East and Africa region is anticipated to grow within the healthcare staffing market from 2026 to 2034. Emerging prospects there are mostly focused in South Africa and the Gulf Cooperation Council nations. Market development is driven by healthcare infrastructure investments, medical tourism expansion, and government initiatives to improve population health outcomes. Gulf states, including Saudi Arabia and the United Arab Emirates, invest heavily in hospital construction and specialist recruitment to support growing populations and medical tourism sectors. South Africa leads sub-Saharan adoption through its mixed public-private healthcare system and relatively advanced regulatory frameworks for clinical staffing. Expatriate recruitment remains prevalent due to domestic training pipeline limitations, though regional governments are implementing policies to develop local workforce capacity. Digital health adoption is accelerating with mobile-based telehealth platforms enabling remote clinical coverage for rural communities. These structural dynamics position the Middle East and Africa for gradual market development with significant long-term growth potential as healthcare systems mature and workforce planning capabilities advance.

COMPETITIVE LANDSCAPE

The healthcare staffing market exhibits moderate fragmentation with several large national players competing alongside numerous regional and specialty-focused enterprises. Market leaders differentiate through scale advantages, proprietary technology platforms, and comprehensive service portfolios that span multiple clinical disciplines and staffing models. Competitive intensity remains elevated as participants invest in digital recruitment tools, predictive analytics, and mobile applications to improve candidate engagement and placement efficiency. Mergers and acquisitions activity continues as firms seek to consolidate market share, expand geographic coverage, and acquire specialized capabilities in high-growth segments such as locum tenens and allied health staffing. Price competition exists particularly in commoditized service categories, though leading firms emphasize value-based differentiation through compliance expertise, clinical quality metrics, and workforce planning support. Regulatory complexity creates barriers to entry that favor established participants with robust credentialing infrastructure and compliance management systems. The emergence of platform-based staffing models introduces new competitive dynamics as technology-enabled entrants challenge traditional agency approaches through improved user experience and algorithmic matching capabilities. Overall, the competitive environment rewards participants that combine clinical expertise, technological innovation, and operational excellence to deliver reliable workforce solutions across diverse healthcare settings and evolving delivery models.

KEY MARKET PLAYERS

Some of the notable companies operating in the global healthcare staffing market are

- Adecco

- AMN Healthcare

- CHG Management

- Syneos Health

- TeamHealth (Blackstone)

- Accountable Healthcare Staffing

- Aya Healthcare

- InGenesis

- Medical Solutions

- Supplemental Health Care

- EmCare

- Almost Family

- Cross Country Healthcare

- Maxim Healthcare Services

- Jackson Healthcare

- Aureus Medical Group (C&A Industries)

- Favorite Healthcare Staffing

- Healthcare Staffing Services

- Trustaff

TOP PLAYERS IN THE MARKET

- AMN Healthcare operates as a comprehensive workforce solutions provider delivering clinical and nonclinical staffing services across the United States. The company maintains extensive networks of travel nurses, locum tenens physicians, and allied health professionals deployed through proprietary digital platforms. AMN has also integrated artificial intelligence-driven matching algorithms to optimize candidate facility alignment and reduce time to placement. The company invests in telehealth-enabled staffing models that support remote clinical delivery and hybrid care arrangements. AMN's vendor-neutral managed service programs help health systems streamline contingent labor procurement while ensuring compliance with regulatory standards. These initiatives reinforce AMN's position as a technology-enabled workforce partner capable of addressing complex clinical staffing requirements across diverse care settings.

- CHG Healthcare specializes in physician and advanced practitioner staffing with particular strength in locum tenens placements across rural and urban markets. This acquisition enhances CHG's ability to engage passive candidates through targeted content and virtual events. CHG operates dedicated divisions for travel nursing, allied health, and permanent placement services supported by a national network of recruitment consultants. The company has implemented mobile credentialing tools that accelerate onboarding timelines and improve candidate experience. CHG also partners with health systems to develop workforce analytics programs that forecast staffing needs and optimize resource allocation. These strategic investments position CHG to capture growing demand for flexible physician staffing while differentiating through technology-enabled service delivery and specialized clinical expertise.

- Aya Healthcare ranks among the largest healthcare staffing firms in the United States with comprehensive service offerings spanning travel nursing, allied health, and locum tenens placements. Aya has also invested in predictive analytics platforms that enable proactive workforce planning and real-time shift optimization for client facilities. The company's mobile application allows clinicians to manage assignments, submit documentation, and access support resources through a single interface. Aya emphasizes clinician experience through competitive compensation, housing assistance, and professional development programs that improve retention and satisfaction. These initiatives support Aya's growth strategy of combining scale with personalized service delivery while leveraging technology to enhance operational efficiency and candidate engagement across its national staffing network.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Leading participants in the healthcare staffing market prioritize strategic acquisitions to expand service capabilities and geographic reach. Technology integration represents a core focus area with investments in artificial intelligence-driven candidate matching, mobile credentialing platforms, and predictive workforce analytics. Companies develop vendor-neutral managed service programs that help health systems consolidate contingent labor procurement while ensuring regulatory compliance. Digital transformation initiatives include telehealth-enabled staffing models that support remote clinical delivery and hybrid care arrangements. Participant firms also emphasize clinician experience through competitive compensation structures, housing assistance, and professional development programs that improve retention and satisfaction. Strategic partnerships with academic institutions help address pipeline constraints by supporting nursing education and clinical training programs. These multifaceted strategies enable market leaders to differentiate through service quality, operational efficiency, and technology-enabled solutions that address evolving healthcare workforce requirements.

GLOBAL HEALTHCARE STAFFING MARKET NEWS

- In February 2025, CHG Healthcare acquired CareerMD, a physician career management platform, to expand digital recruitment capabilities and strengthen its Healthcare Staffing Market presence.

- In January 2024, Aya Healthcare acquired ID Medical, a United Kingdom-based staffing firm, to enhance international service offerings and strengthen its Healthcare Staffing Market presence.

- In November 2023, Aya Healthcare acquired Winnow, a technology-enabled staffing solutions provider, to enhance digital recruitment infrastructure and strengthen its Healthcare Staffing Market presence.

- In August 2024, Triage Staffing acquired RTG Medical to integrate travel nurse staffing capabilities and strengthen its Healthcare Staffing Market presence.

MARKET SEGMENTATION

This research report on the global healthcare staffing market has been segmented and sub-segmented based on service type and region.

By Service Type

- Travel Nurse Staffing

- Per Diem Nurse Staffing

- Locum Tenens Staffing

- Allied Healthcare Staffing

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What drives growth in the global healthcare staffing market?

Growth is driven by rising patient loads, aging populations, healthcare labor shortages, and increasing use of staffing agencies for flexible workforce solutions

2. Which staffing segment dominates the global healthcare staffing market?

Nurse staffing holds the largest share due to high demand across hospitals and care settings in the global healthcare staffing market

3. How important is allied health staffing in the global healthcare staffing market?

Allied health staffing is growing fast as specialized healthcare functions increase, adding significant value to the global healthcare staffing market

4. What role do locum tenens play in the global healthcare staffing market?

Locum tenens provide temporary, flexible physician coverage, helping healthcare providers manage shortages in the global healthcare staffing market

5. Which regions lead the global healthcare staffing market?

North America leads due to a robust healthcare infrastructure; Asia-Pacific is growing rapidly with increasing healthcare investments

6. How does telehealth affect the global healthcare staffing market?

Telehealth adoption increases demand for remote healthcare staffing and supports flexible patient care options in the global healthcare staffing market

7. What challenges does the global healthcare staffing market face?

Challenges include nurse shortages, high recruitment costs, regulatory complexity, and workforce burnout in the global healthcare staffing market

8. How does healthcare staffing technology impact the market?

Technology enhances recruitment, scheduling, and workforce management efficiency, driving growth in the global healthcare staffing market

9. Who are the key players in the global healthcare staffing market?

Leading companies include AMN Healthcare, Aya Healthcare, Cross Country Healthcare, and Maxim Healthcare Services

10. How does home healthcare staffing contribute to the market?

Home healthcare staffing grows with aging populations and increased preference for at-home medical services worldwide

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com