Global Hernia Mesh Devices Market Size, Share, Trends & Growth Forecast Report By Hernia Type, Product Type and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Market Size, 2025

$4.21 BnMarket Estimate, 2026

$4.34 BnMarket Forecast, 2034

$5.54 BnCAGR, 2026–2034

3.1%Global Hernia Mesh Devices Market Report Summary

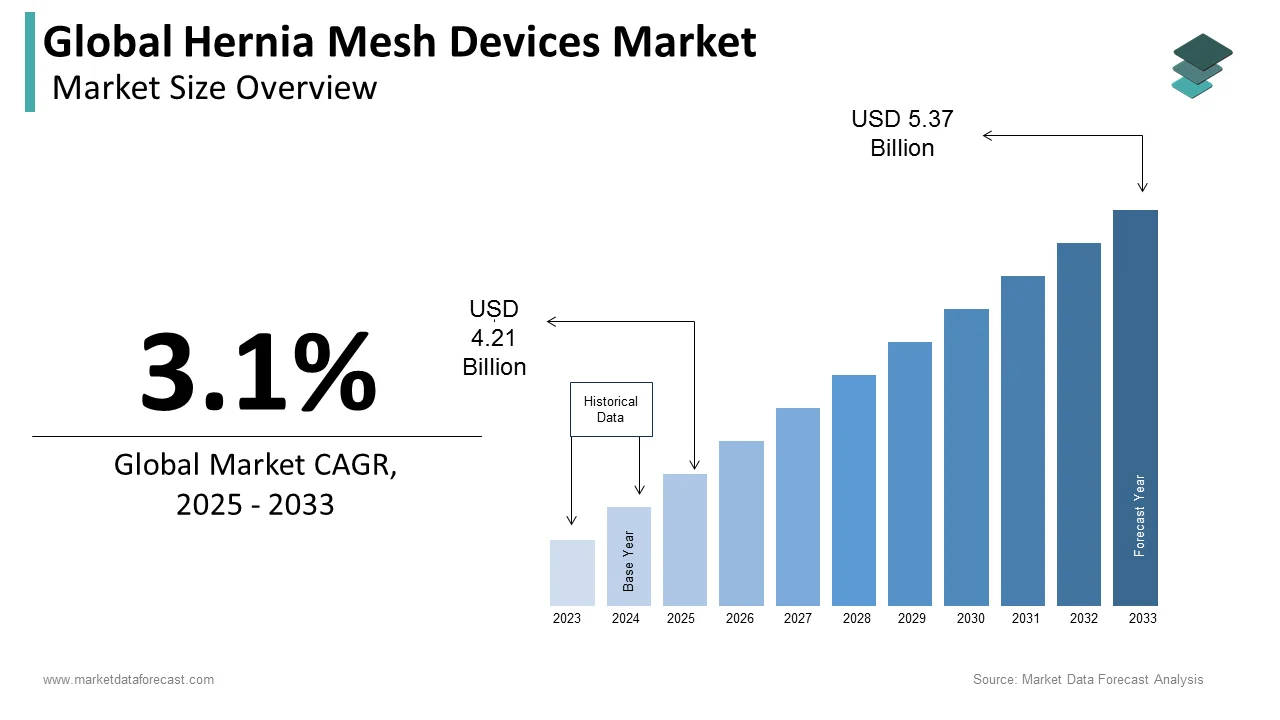

The global hernia mesh devices market was valued at USD 4.21 billion in 2025, is estimated to reach USD 4.34 billion in 2026, and is projected to reach USD 5.54 billion by 2034, growing at a CAGR of 3.1% from 2026 to 2034. Market growth is driven by the increasing prevalence of hernia conditions, the rising number of surgical procedures, and the growing preference for mesh-based repair techniques over traditional suturing methods. Hernia mesh devices enhance surgical outcomes by reducing recurrence rates and improving recovery times. The aging global population, advancements in surgical materials, and increasing adoption of minimally invasive procedures are further supporting market growth.

Key Market Trends

- Increasing adoption of mesh-based hernia repair procedures.

- Rising demand for minimally invasive and laparoscopic surgeries.

- Growing prevalence of inguinal and abdominal hernias.

- Advancements in biocompatible and lightweight mesh materials.

- Increasing focus on reducing post-surgical complications and recurrence rates.

Segmental Insights

- Based on hernia type, the inguinal hernia segment dominated the global hernia mesh devices market in 2025 due to its high prevalence.

- Based on product type, the synthetic mesh segment held the largest share, accounting for approximately 85–90% of total revenue, driven by durability, cost-effectiveness, and widespread clinical adoption.

Regional Insights

The global hernia mesh devices market is witnessing steady growth across major regions due to increasing surgical volumes and healthcare advancements.

- North America led the market in 2025 with 40.3% share, supported by advanced healthcare infrastructure and high adoption of surgical technologies.

- Europe followed with 28.3% share in 2025, driven by established healthcare systems and rising aging population.

- Asia-Pacific is expected to grow steadily due to improving healthcare infrastructure and increasing adoption of mesh-based surgical techniques.

Competitive Landscape

The global hernia mesh devices market is moderately competitive, with the presence of leading medical device manufacturers focusing on innovation and product development. Companies are investing in advanced materials, improving product safety, and expanding their global footprint. Strategic partnerships and regulatory approvals are shaping competitive dynamics across the market.

Prominent companies operating in the global hernia mesh devices market include Medtronic, Ethicon, Inc., C.R. Bard, Inc., Johnson & Johnson, Becton Dickinson and Company, Atrium, W.L. Gore & Associates, Lifecell Corporation, and B. Braun Melsungen AG.

Global Hernia Mesh Devices Market Size

The size of the global hernia mesh devices market was worth USD 4.21 billion in 2025. The global market is anticipated to grow at a CAGR of 3.1% from 2026 to 2034 and be worth USD 5.54 billion by 2034 from USD 4.34 billion in 2026.

Hernia mesh devices constitute a specialized category of surgical implants engineered to reinforce compromised tissue walls during hernia repair operations. These devices function as a permanent or temporary scaffold that facilitates tissue ingrowth and distributes tension across the repair site, significantly lowering the probability of recurrence compared to traditional suture techniques. The clinical imperative for these devices stems from the high prevalence of hernias, which are protrusions of internal organs through weak points in the abdominal wall. Globally, hernias represent one of the most common surgical conditions, with inguinal hernias alone affecting approximately 27% of men and 3% of women during their lifetimes. As per data from the European Hernia Society, over 20 million hernia repair procedures are performed annually worldwide, establishing a massive baseline volume for device consumption.

MARKET DRIVERS

Demographic Shifts and Rising Disease Incidence

The inexorable rise in hernia incidence, fueled by global demographic aging and escalating obesity rates, is certainly a primary factor boosting the growth of the hernia mesh devices market. Hernias are predominantly age-related conditions where the weakening of muscle and connective tissue allows internal organs to protrude, a process that accelerates significantly after the age of 50. Data from the United Nations Department of Economic and Social Affairs projects that the global population aged 65 years and older will surge from 761 million in 2021 to 1.6 billion by 2050, effectively doubling the high-risk demographic within a single generation. This trend is particularly acute in developed nations where life expectancy continues to extend, thereby lengthening the window of vulnerability for hernia development. Concurrently, the global obesity crisis acts as a potent multiplier for hernia risk. Excess adipose tissue increases intra-abdominal pressure, placing chronic strain on the abdominal wall and precipitating hernia formation. According to the World Health Organization, worldwide obesity has nearly tripled since 1975, and in 2022, 16% of the global adult population was classified as obese. In Europe, the European Commission reports that one in two adults is now overweight, creating a vast addressable patient population.

Technological Innovation and Surgical Evolution

The rapid evolution of mesh biomaterials, coupled with the widespread adoption of minimally invasive surgical techniques, is also propelling the growth of the hernia mesh devices market. The simple polypropylene sheets are used to develop sophisticated composite meshes featuring absorbable barriers, anti-adhesive coatings, and lightweight macroporous structures designed to minimize foreign body reactions and chronic pain. Simultaneously, the surgical procedure is shifting decisively toward laparoscopic and robotic-assisted repairs, which require specialized mesh formulations capable of being rolled or folded for insertion through small trocars. The American College of Surgeons indicates that minimally invasive techniques are in full swing, driven by benefits such as reduced hospital stays and lower infection rates. This procedural shift creates a distinct demand segment for high-value, procedure-specific mesh devices that command premium pricing. Furthermore, the integration of 3D printing and patient-specific implant designs is beginning to emerge, offering tailored solutions for complex ventral hernias.

MARKET RESTRAINTS

Litigation Risks and Safety Concerns

The pervasive atmosphere of safety concerns and the resulting wave of product liability litigation are restricting the growth of the hernia mesh devices market. Over the past decade, thousands of patients have reported severe complications following mesh implantation, including chronic pain, mesh migration, erosion into visceral organs, and persistent infections. These adverse events have triggered extensive legal actions against major manufacturers, resulting in billions of dollars in settlements and verdicts. Some leading device companies have faced tens of thousands of lawsuits alleging defective design and failure to provide adequate warnings regarding long-term risks. In several high-profile instances, specific mesh products were recalled from the global market, causing significant reputational damage and eroding confidence among both surgeons and patients. The US Food and Drug Administration has issued multiple safety communications highlighting these complications, which further amplify public scrutiny and caution. This litigious environment forces companies to allocate substantial resources to legal defense rather than research and development, while also causing some surgeons to hesitate in recommending mesh repairs for borderline cases to avoid potential liability. The shadow of litigation stifles innovation as manufacturers may delay the launch of novel materials until exhaustive long-term clinical data is available, slowing the pace of technological advancement.

Regulatory Hurdles and Reimbursement Constraints

The substantial headwinds from increasingly rigorous regulatory frameworks and tightening reimbursement policies that constrain commercial velocity is also impeding the growth of the hernia mesh devices market. Following high-profile device failures, regulatory bodies such as the European Medicines Agency and the US Food and Drug Administration have implemented stricter premarket approval requirements, mandating extensive clinical trials to demonstrate long-term safety and efficacy. In Europe, the full implementation of the Medical Device Regulation has introduced more demanding clinical evidence standards and rigorous post-market surveillance obligations, placing a heavy administrative burden on manufacturers. Simultaneously, healthcare payers are intensifying their focus on cost containment, scrutinizing the price-to-performance ratio of high-cost mesh implants. Hospitals and insurance providers are increasingly favoring lower-cost alternatives or generic mesh options to manage budgets. In many European countries, diagnosis-related group payment systems cap the reimbursement amount for hernia repair procedures, forcing hospitals to negotiate steep discounts with suppliers. This pricing pressure squeezes profit margins for device manufacturers, limiting their ability to invest in next-generation research and development.

MARKET OPPORTUNITIES

Emergence of Bioresorbable and Biologic Solutions

The developing sector of bioresorbable and biologically derived mesh products, aiming to overcome the limitations of permanent synthetic implants, is substantially to create new opportunities for the growth of the hernia mesh devices market. Traditional synthetic meshes remain in the body indefinitely, which can lead to long-term complications such as chronic inflammation, stiffness, and foreign body sensations. In contrast, bioresorbable meshes are engineered to provide temporary mechanical support during the critical healing phase and then gradually degrade, leaving behind only the patient's natural reinforced tissue. This approach aligns with the growing clinical preference for physiological restoration over permanent foreign body implantation. As per recent clinical studies, interest in biologic meshes derived from porcine, bovine, or human cadaveric tissue is rising sharply, particularly for contaminated surgical fields where the risk of infection precludes the use of synthetics. Companies investing in proprietary decellularization technologies and synthetic bioresorbable polymers stand to capture substantial market share by addressing unmet clinical needs. Furthermore, the integration of regenerative medicine principles, such as seeding meshes with stem cells or growth factors to accelerate tissue regeneration, offers a frontier for product differentiation.

Expansion of Ambulatory Surgical Centers

The strategic migration of hernia repair procedures from inpatient hospitals to ambulatory surgical centers and outpatient settings is also expected to expand the growth of the hernia mesh devices market in the coming years. Healthcare systems globally are prioritizing cost efficiency and patient convenience, driving the transition of surgical procedures to lower-cost outpatient facilities. Hernia repair is ideally suited for this model due to its minimally invasive nature and rapid recovery profile, allowing patients to return home on the same day. In Europe, national health services are actively promoting day-case surgery policies to reduce hospital bed occupancy and lower overall treatment costs. This trend necessitates hernia mesh devices that are specifically optimized for quick handling, ease of insertion, and minimal postoperative care requirements. Additionally, the faster turnover rates in outpatient centers drive higher procedural volumes, directly increasing the consumption of mesh devices.

MARKET CHALLENGES

Management of Chronic Post-Surgical Complications

The complex clinical management of chronic post-surgical pain and other serious complications associated with mesh implantation is specifically a challenge for the growth of the hernia mesh devices market. Despite the overall high success rate of mesh repairs, a significant subset of patients experiences debilitating chronic pain that persists long after the surgery, severely impacting their quality of life. As per longitudinal studies published in surgical literature, the etiology of this pain is multifactorial, involving nerve entrapment, mesh shrinkage, and inflammatory responses to the foreign material. Addressing these issues often requires complex revision surgeries, which are technically demanding, carry higher risks than primary repairs, and frequently yield less predictable outcomes. The existence of these complications creates a clinical dichotomy where the device intended to cure the hernia becomes a source of new pathology. This reality complicates the decision-making process for both surgeons and patients, leading to hesitation in adopting mesh techniques for certain demographics or hernia types. Furthermore, the lack of standardized protocols for managing mesh-related complications results in varied patient outcomes and inconsistent clinical data. Manufacturers face the difficult task of engineering meshes that balance strength with flexibility to minimize nerve irritation while maintaining repair integrity.

Competitive Intensity and Pricing Pressure

The intense competitive pressure and aggressive pricing erosion in advanced healthcare facilities are likely to limit the growth of the hernia mesh devices market. Numerous established medical device corporations, along with emerging players, compete fiercely for market share, leading to the commoditization of standard mesh products. In regions such as North America and Western Europe, the presence of multiple vendors offering similar synthetic mesh solutions has triggered price wars that compress profit margins significantly. Hospitals leveraging their substantial buying power often dictate steep discounts, forcing manufacturers to compete primarily on price rather than innovation. This environment makes it difficult for companies to recoup the high research and development investments required to bring novel technologies to market. Smaller firms with limited financial resources struggle to survive in this cutthroat landscape, leading to market consolidation where only the largest entities can sustain operations. The pressure to lower costs may also compromise quality control or limit the availability of premium products in cost-sensitive public health systems. threatens the long-term profitability and sustainability of the hernia mesh devices sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Hernia Type, Product Type, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Medtronic (U.S.), Ethicon, Inc. (U.S.), C.R. Bard, Inc. (U.S.), Atrium (Sweden), W.L. Gore & Associates (Germany), Becton Dickinson and Company, Johnson & Johnson, Lifecell Corporation (U.S.), and B. Braun Melsungen AG (Germany). |

SEGMENTAL ANALYSIS

By Hernia Type Insights

The inguinal hernia segment was the largest by holding a significant share of the global hernia mesh devices market in 2025, owing to the disproportionately high incidence of inguinal hernias, particularly among men. Anatomical factors related to the descent of the testes create a natural weakness in the inguinal canal by making this area highly susceptible to herniation. This gender disparity creates a massive and consistent patient pool that drives procedural volume year after year. Furthermore, the condition is not limited to the elderly, where it affects individuals across a wide age range, including young adults and children, although repair rates peak in older demographics. The World Health Organization indicates that inguinal hernias account for roughly three-quarters of all abdominal wall hernias globally.

The incisional hernia segment is projected to be the fastest-growing category within the hernia mesh devices market, anticipated to expand at a Compound Annual Growth Rate of approximately 8.5% during the forecast period. This accelerated growth trajectory is fueled by the rising rates of abdominal surgeries that predispose patients to incisional hernias and the increasing complexity of repairs requiring advanced mesh solutions.

The primary catalyst for the rapid expansion of the incisional hernia segment is the escalating global volume of abdominal surgeries, particularly laparotomies and bariatric procedures, which are the main precursors to incisional hernia formation. An incisional hernia occurs at the site of a previous surgical scar, and the risk increases significantly with factors such as obesity, infection, and poor wound healing. As per statistics from the Centers for Disease Control and Prevention, the number of abdominal surgeries performed annually in the United States alone exceeds 4 million, creating a vast population at risk for subsequent hernia development. The correlation with obesity is particularly strong; the World Health Organization states that obesity increases the risk of incisional hernia by up to 4 times due to increased intra-abdominal pressure and compromised tissue quality. With global obesity rates continuing to climb, the incidence of post-surgical hernias is rising in tandem. Furthermore, the increase in survival rates for complex abdominal conditions means more patients are living long enough to develop and seek repair for these late complications. This expanding at risk population directly translates into a higher volume of incisional hernia repairs, driving demand for specialized mesh devices designed to handle the larger defects and higher tension associated with this hernia type.

The second major factor propelling the growth of the incisional segment is the increasing reliance on sophisticated mesh technologies to manage the complexity of ventral and incisional hernia repairs. Unlike simple inguinal hernias, incisional hernias often involve large defects, loss of domain, and contaminated fields, necessitating the use of premium mesh products such as composite meshes, biologic meshes, and reinforced synthetic options. As per clinical data published in the Annals of Surgery, the use of advanced composite meshes with anti-adhesive barriers has become the standard of care for intraperitoneal onlay mesh placement, significantly reducing adhesion formation and bowel obstruction risks. The market for these high-value devices is expanding as surgeons increasingly opt for durable solutions that minimize the high recurrence rates historically associated with incisional hernia repairs, which can exceed 20% with traditional methods. Additionally, the rise of component separation techniques combined with mesh reinforcement is driving the need for larger and more specialized mesh sizes. Manufacturers are responding by launching innovative products specifically tailored for complex abdominal wall reconstruction, which command higher price points and contribute to revenue growth. This shift toward premiumization and the technical necessity of advanced materials in complex cases ensure that the incisional segment grows at a faster pace than the mature inguinal market.

By Product Type Insights

The synthetic mesh segment holds the largest share of the global hernia mesh devices market, accounting for an estimated 85 to 90% of total revenue. This dominance is underpinned by the cost-effectiveness of synthetic materials, their proven long-term durability, and their status as the first line of treatment for the vast majority of clean and contaminated hernia repairs.

The foremost driver of the synthetic mesh segment's dominance is its superior cost-effectiveness compared to biologic alternatives, making it the preferred choice for healthcare systems and payers globally. Synthetic meshes, primarily composed of polypropylene, polyester, or polytetrafluoroethylene, are manufactured using scalable industrial processes that keep unit costs low, often ranging from a fraction of the price of biologic meshes. As per health economic analyses conducted by various national health services, the use of synthetic mesh in routine hernia repairs results in significant cost savings without compromising clinical outcomes in standard cases. This economic advantage is critical in both developed markets facing budget constraints and emerging markets, where affordability is a primary determinant of access. The World Bank notes that in many low and middle-income countries, the high cost of biologic meshes restricts their use to only the most complex contaminated cases, leaving synthetic mesh as the only viable option for the majority of patients. Furthermore, the extensive history of clinical use spanning several decades has established a deep comfort level among surgeons with synthetic materials. The availability of a wide range of synthetic products from numerous manufacturers ensures a consistent supply and competitive pricing. This combination of affordability, availability, and established clinical trust ensures that synthetic mesh remains the workhorse of hernia repair, securing its overwhelming market share.

The second pivotal factor sustaining the leadership of synthetic meshes is their unparalleled mechanical strength and proven long-term durability in providing permanent reinforcement. Hernia repair requires a scaffold that can withstand significant intra-abdominal pressures over the lifetime of the patient, and synthetic polymers excel in maintaining tensile strength without degrading. According to long-term follow-up studies published in major surgical journals, synthetic meshes demonstrate excellent stability with minimal loss of strength over 10 to 20 year periods, resulting in consistently low recurrence rates. This permanence is particularly valued in inguinal and ventral hernia repairs where the structural integrity of the abdominal wall must be permanently restored. The American Hernia Society highlights that synthetic meshes provide the necessary support for tissue ingrowth while maintaining their structural role, unlike resorbable materials that may lose strength before tissue remodeling is complete. Advances in manufacturing have also allowed for the creation of lightweight synthetic meshes that reduce foreign body sensation and chronic pain while retaining sufficient strength for most applications. This balance of durability and improved biocompatibility has solidified the position of synthetic mesh as the standard of care.

The 3D mesh segment is swiftly growing at a fastest CAGR of 9.2% in the coming years, with the rapid growth of the 3D mesh segment is the global shift toward minimally invasive hernia repair techniques, specifically laparoscopic and robotic-assisted surgeries, which heavily favor the use of preformed 3D devices. Traditional flat meshes require manual cutting and shaping by the surgeon during laparoscopic procedures, which can be time-consuming and prone to sizing errors. In contrast, 3D meshes are pre-shaped to conform to specific anatomical spaces such as the preperitoneal space in inguinal repairs, allowing for faster and more precise deployment. As per data from the Society of American Gastrointestinal and Endoscopic Surgeons, the utilization of laparoscopic inguinal hernia repair has grown steadily, now accounting for a significant portion of all inguinal repairs in major markets. These procedures inherently benefit from 3D mesh designs that can be easily inserted through trocars and self-expand to cover the myopectineal orifice adequately. The efficiency gains in the operating room translate to reduced anesthesia time and lower overall procedural costs, making 3D meshes attractive to hospital administrators. Furthermore, the ergonomic advantages for surgeons reduce the learning curve associated with minimally invasive techniques, encouraging broader adoption.

REGIONAL ANALYSIS

North America Hernia Mesh Devices Market Analysis

North America was the top performer in the global hernia mesh devices market by holding 40.3% of the market share in 2025. The United States, which boasts the highest volume of hernia repair procedures globally, serves as the primary hub for medical device innovation and adoption. The exceptionally high prevalence of obesity and an aging population, which directly correlates with increased hernia incidence, is also to propel the growth of the market. As per data from the Centers for Disease Control and Prevention, the prevalence of obesity in the United States reached 41.9% in recent years, creating a massive cohort of patients at risk for both inguinal and ventral hernias. Furthermore, the region leads in the adoption of minimally invasive surgical techniques, with a significant proportion of repairs performed laparoscopically or robotically, driving demand for specialized 3D and composite meshes. The presence of major market players and robust research and development activities further solidifies the region's position. High healthcare expenditure per capita ensures that patients have access to the latest mesh technologies, while favorable reimbursement policies from private insurers and Medicare support the utilization of high-cost devices.

Europe Hernia Mesh Devices Market Analysis

Europe hernia mesh devices market was ranked second by holding 28.3% of the market share in 2025, with a diverse mix of highly developed healthcare systems in Western Europe and emerging countries in Eastern Europe, all contributing to steady demand. The expanding aging population, which significantly elevates the risk of hernia development. According to Eurostat, individuals aged 65 and older comprised over 21% of the European Union population in 2024, a figure that continues to rise, thereby expanding the patient pool for hernia repairs. Additionally, the region has seen a concerted push toward standardizing hernia care guidelines, with the European Hernia Society actively promoting mesh-based repairs as the gold standard, leading to high penetration rates. The implementation of the Medical Device Regulation has raised quality standards, fostering trust in approved mesh products. Furthermore, increasing obesity rates across the continent, with the World Health Organization reporting that more than 50% of adults in the WHO European Region are overweight, are contributing to a higher incidence of ventral and incisional hernias. The growing adoption of day case surgery policies in countries like Germany, France, and the UK is also boosting procedural volumes in ambulatory settings by creating new avenues for mesh device consumption and sustaining the region's robust market position.

Asia-Pacific Hernia Mesh Devices Market Analysis

The Asia-Pacific region hernia mesh devices market growth is likely to grow with a rapid transition from traditional suture repairs to mesh-based techniques, driven by improving healthcare infrastructure and rising medical awareness. As per reports from the World Health Organization, obesity rates in Asia are rising alarmingly, particularly in countries like China and India, leading to a surge in hernia cases. Additionally, significant investments in healthcare infrastructure by governments in the region are expanding access to surgical services for millions of previously underserved individuals. The growing medical tourism industry in countries like Thailand and Singapore is also contributing to market expansion, attracting international patients for high-quality hernia repairs. Furthermore, the increasing number of trained surgeons and the adoption of international clinical guidelines are accelerating the shift toward mesh usage.

Latin America Hernia Mesh Devices Market Analysis

Latin America hernia mesh devices market is likely to grow with a blend of developing healthcare systems and pockets of advanced medical care. The market status is evolving, with a gradual shift from public sector-dominated low-cost procedures to increased utilization of advanced mesh technologies in private healthcare facilities. According to the Pan American Health Organization, obesity rates in Latin America have doubled in the last two decades, with countries like Mexico and Brazil reporting some of the highest rates in the world, directly fueling the demand for hernia repairs. Additionally, the expansion of private health insurance coverage in urban centers is enabling more patients to access elective hernia surgeries using modern mesh devices. Government initiatives aimed at reducing surgical backlogs in public hospitals are also increasing procedural volumes. The presence of multinational device companies establishing local distribution networks is improving product availability and surgeon training. Furthermore, the growing trend of medical tourism within the region, particularly to Brazil and Costa Rica, is stimulating demand for high-quality surgical implants.

Middle East and Africa Hernia Mesh Devices Market Analysis

The Middle East and Africa hernia mesh devices market growth is likely to grow with Gulf Cooperation Council countries boasting advanced healthcare facilities comparable to Western nations, while many African nations face infrastructure challenges. As per data from the International Diabetes Federation, the Middle East and North Africa region has the highest prevalence of diabetes globally, a condition closely linked to obesity and increased hernia risk. Governments in countries like Saudi Arabia and the United Arab Emirates are investing heavily in healthcare infrastructure and the localization of medical device manufacturing, which is enhancing access to advanced mesh products. In Africa, the market is driven by gradual improvements in healthcare access and the increasing adoption of mesh repairs over traditional methods in urban centers. The growing medical tourism sector in destinations like Dubai and Turkey further supports market activity.

COMPETITIVE LANDSCAPE

The competition within the hernia mesh devices market is characterized by intense rivalry among established multinational corporations and agile niche players striving for dominance. Major competitors differentiate themselves through continuous technological advancements aimed at reducing postoperative complications such as chronic pain and mesh infection. This features a constant race to develop superior biomaterials, including lightweight synthetics and advanced biologics that offer better tissue integration. Companies frequently engage in strategic acquisitions to broaden their product offerings and gain access to innovative manufacturing processes. Litigation history regarding mesh safety has forced all participants to adhere to rigorous quality standards and transparency which shapes competitive dynamics. Pricing pressure from group purchasing organizations and government tenders compels firms to optimize cost structures while maintaining high quality. The shift toward minimally invasive surgeries has further intensified competition as manufacturers vie to produce meshes specifically designed for laparoscopic and robotic applications.

KEY MARKET PLAYERS

Companies playing a prominent role in the global hernia mesh devices market include

- Medtronic (U.S.)

- Ethicon, Inc. (U.S.)

- R. Bard, Inc. (U.S.)

- Johnson & Johnson

- Becton Dickinson and Company

- Atrium (Sweden)

- L. Gore & Associates (Germany)

- Lifecell Corporation (U.S.)

- Braun Melsungen AG (Germany)

TOP PLAYERS IN THE MARKET

- Medtronic plc stands as a preeminent force in the global hernia mesh devices landscape due to its extensive portfolio of synthetic and biologic solutions. The company leverages its vast distribution network to ensure widespread availability of its products across diverse healthcare settings worldwide. Medtronic consistently invests in research and development to introduce advanced mesh technologies that minimize complications such as chronic pain and infection. Recent actions include the launch of next-generation lightweight composite meshes designed specifically for laparoscopic procedures, which enhance surgeon handling and patient recovery times. The firm actively engages in strategic partnerships with surgical societies to promote best practices in hernia repair. By focusing on innovation and clinical education, Medtronic reinforces its leadership position and drives the adoption of superior mesh-based repair techniques globally without relying on static market metrics.

- Becton Dickinson and Company maintains a robust presence in the hernia mesh devices sector through its specialized Davol brand, which offers a comprehensive range of ventral and inguinal mesh products. The company is deeply involved in advancing surgical outcomes by developing meshes with unique macroscopic structures that facilitate optimal tissue integration. Recent initiatives have focused on expanding their biologic mesh portfolio to address complex contaminated surgical fields where synthetic options carry higher risks. Becton Dickinson has also strengthened its market position by acquiring niche technology firms to integrate smart materials into their product lines. The organization prioritizes surgeon training programs to ensure proper utilization of their devices, which fosters loyalty and clinical confidence. Through continuous product refinement and a commitment to solving complex abdominal wall challenges, Becton Dickinson solidifies its role as a critical contributor to the global hernia care ecosystem.

- Johnson & Johnson operates as a major contributor to the hernia mesh devices market via its Ethicon subsidiary, which is renowned for pioneering innovations in surgical mesh technology. The company offers a wide array of solutions, including absorbable and non-absorbable meshes tailored for various surgical approaches ranging from open to robotic-assisted procedures. Recent efforts by Johnson & Johnson have centered on enhancing the biocompatibility of their mesh products to reduce foreign body reactions and improve long-term patient comfort. The firm has launched several new preformed three-dimensional meshes that simplify surgical workflow and ensure consistent anatomical coverage. Additionally, Johnson & Johnson actively collaborates with clinical researchers to generate real-world evidence supporting the safety and efficacy of their devices.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the hernia mesh devices market primarily employ strategies focused on continuous product innovation and strategic acquisitions to maintain a competitive advantage. Companies heavily invest in research and development to create next-generation meshes that offer improved biocompatibility and reduced complication rates. Mergers and acquisitions allow larger entities to absorb niche technologies and expand their product portfolios rapidly. Another prevalent strategy involves forming strategic partnerships with surgical centers and professional societies to drive clinical education and promote best practices. Manufacturers also focus on expanding their geographic footprint by entering emerging countries, where healthcare infrastructure is improving. Pricing strategies often involve bundling mesh devices with specialized delivery instruments to increase value perception. Furthermore, companies are increasingly adopting digital health tools to track patient outcomes and gather real-world data.

MARKET SEGMENTATION

This research report on the global hernia mesh devices market has been segmented and sub-segmented based on the hernia type, product type, and region.

By Hernia Type

- Inguinal

- Umbilical

- Hiatal

- Femoral

- Incisional

By Product Type

- Synthetic Mesh

- Flat Mesh

- 3D Mesh

- Biologic Mesh

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What is the global hernia mesh devices market?

The global hernia mesh devices market comprises surgical meshes used to repair hernias by reinforcing tissue, improving recovery, and reducing recurrence in orthopedic and general surgery worldwide

2. What drives growth in the global hernia mesh devices market?

Growth is fueled by increasing hernia prevalence, obesity rates, aging populations, innovation in mesh materials, and wide adoption of minimally invasive surgeries in the global hernia mesh devices market

3. Which regions lead the global hernia mesh devices market?

North America leads due to advanced healthcare and technology adoption, followed by Europe, with Asia Pacific growing rapidly from rising healthcare access and surgical capabilities in the global hernia mesh devices market

4. What are the main types of mesh in the global hernia mesh devices market?

Main types include synthetic mesh, biological mesh, and biosynthetic mesh, each offering varied biocompatibility and use cases in the global hernia mesh devices market

5. What are common applications in the global hernia mesh devices market?

Common applications include inguinal hernia repair, incisional hernia repair, femoral hernia repair, and other abdominal hernia surgeries in the global hernia mesh devices market

6. How do minimally invasive surgeries influence the global hernia mesh devices market?

Minimally invasive surgeries drive demand for advanced meshes designed for laparoscopic and robotic procedures, expanding the global hernia mesh devices market

7. What innovations are shaping the global hernia mesh devices market?

Innovations include lightweight mesh, self-fixating mesh, improved biocompatibility, and absorbable materials enhancing outcomes in the global hernia mesh devices market

8. What challenges affect the global hernia mesh devices market?

Challenges include post-surgical complications, regulatory hurdles, product recalls, patient safety concerns, and cost considerations in the global hernia mesh devices market

9. Who are the primary end-users of products in the global hernia mesh devices market?

Hospitals, ambulatory surgical centers, and specialized clinics are the primary recipients using products from the global hernia mesh devices market

10. How does obesity impact the global hernia mesh devices market?

Rising obesity increases hernia risk, boosting demand for mesh-based repairs, thereby expanding the global hernia mesh devices market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com