Global High-Altitude Pseudo Satellites Market Size, Share, Trends, & Growth Forecast Report Segmented, By Platform (Unmanned Aerial Vehicles (UAVs), Airships, Balloon Systems), Payload (Communication Systems, Imaging Systems, Surveillance & Reconnaissance, Weather And Environmental Sensors, Navigation And Positioning Systems), Application (Defense, Civilian government, Commercial, Others), Deployment (Land-Based Operations, Maritime Operations, Polar Regions, Disaster-Prone Areas), And Region (North America, Europe, Asia-Pacific, Latin America, Middle East And Africa), Industry Forecast From 2026 to 2034

Global High-altitude Pseudo-Satellite (HAPS) Market Size

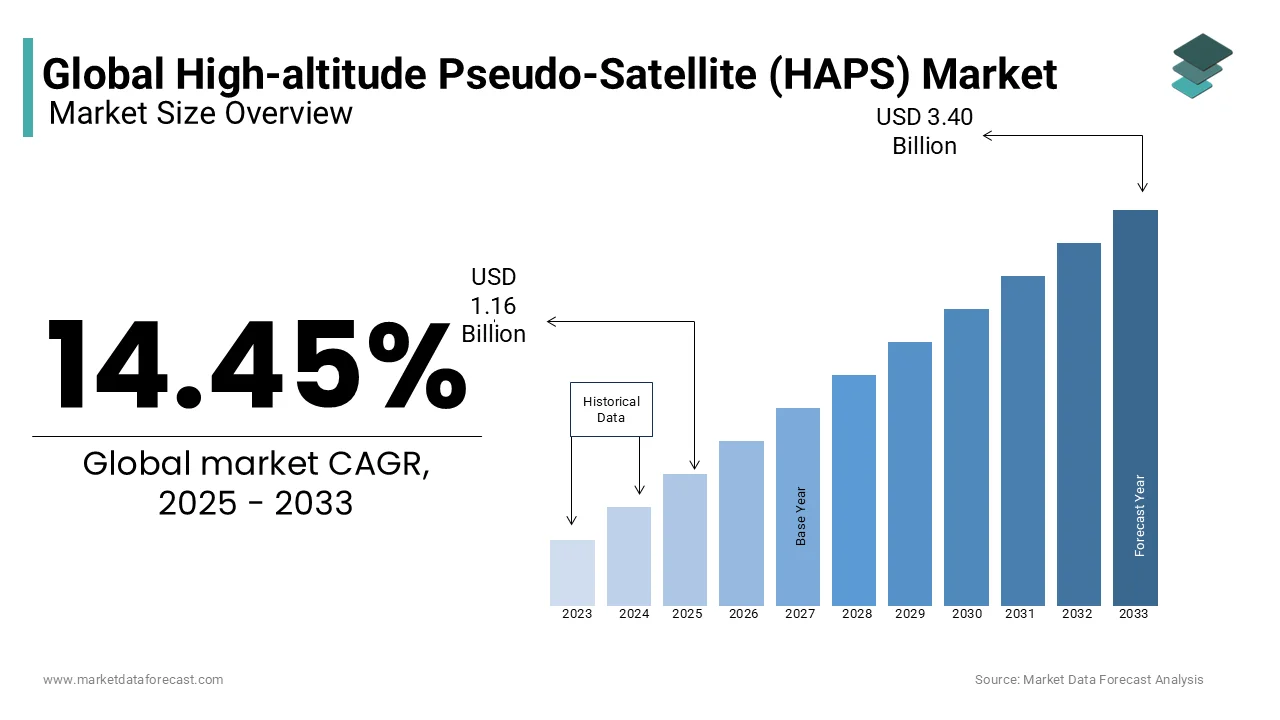

The global high-altitude pseudo-satellite (HAPS) market was valued at USD 1.16 billion in 2025 and is anticipated to reach USD 1.16 billion by 2026 from USD 3.40 billion in 2034, growing at a CAGR of 14.45% during the forecast period from 2026 to 2034.

High Altitude Pseudo Satellites (HAPS) are solar-powered Unmanned Aerial Vehicles (UAVs), airships, or balloons that fly in the stratosphere (about 18-20 km above the Earth). These systems function as stationary relay nodes that bridge operational gaps between terrestrial infrastructure and conventional orbital satellites. The stratospheric environment delivers minimal atmospheric turbulence and negligible commercial air traffic, enabling prolonged station keeping without frequent propulsion adjustments. As per the International Telecommunication Union, radio regulations and spectrum allocations are increasingly expanded and harmonized during World Radiocommunication Conferences to accommodate emerging aerial communication nodes and non-terrestrial network (NTN) configurations. Atmospheric science data confirms that solar irradiance levels at 20,000 meters exceed maximum surface exposure by approximately 30% to 35%, climbing close to the space-based constant of 1361WIM2, which significantly enhances photovoltaic energy harvesting efficiency for solar-powered stratospheric platforms. Regulatory frameworks established by the European Union Aviation Safety Agency for higher airspace operations utilize risk-based safety assessments and customized flight simulation validation tailored to the platform's design before granting operational stratospheric clearance. Furthermore, atmospheric density at these elevations drops to roughly 7 percent of sea level values, requiring specialized aerodynamic configurations and lightweight composite materials to maintain structural integrity during sustained flights. These physical and regulatory parameters establish the foundational operating environment for next generation aerial networks and dictate the engineering thresholds required for successful commercial deployment.

MARKET DRIVERS

Escalating Demand For Uninterrupted Broadband Connectivity In Remote Geographies

The deployment of aerial communication nodes directly addresses the persistent connectivity gap affecting isolated regions across developing economies, which drives the growth of the high altitude pseudo satellite market. Traditional terrestrial infrastructure requires extensive ground excavation and substantial capital allocation, which remains economically unfeasible for sparsely populated territories. Stratospheric platforms bypass these geographical constraints by broadcasting signals across diameters exceeding 300 kilometers from a single elevated position. According to the World Bank, approximately 2.6 billion individuals worldwide still lack access to reliable internet services, with 70 percent of these populations residing in topographically complex zones where fiber optic deployment proves prohibitively expensive. The International Telecommunication Union emphasizes that expanding mobile broadband penetration by 10% could increase gross domestic product per capita growth by up to 2.5% in emerging African markets. Furthermore, maritime shipping corridors and transcontinental aviation routes experience consistent signal degradation beyond coastal coverage boundaries, creating a persistent demand for elevated relay systems that guarantee continuous data transmission. This operational necessity compels telecommunications providers and government agencies to prioritize aerial network integration as a viable solution for universal digital inclusion and economic stabilization in underserved territories.

Rising Requirement For Persistent Border Surveillance And Environmental Monitoring

National security agencies and ecological research institutions increasingly rely on continuous aerial observation to monitor expansive territories without the operational limitations of conventional aircraft, which further propels the expansion of the high altitude pseudo satellites market. Traditional satellite orbits introduce temporal gaps in data collection due to fixed revisit cycles, whereas stratospheric platforms maintain stationary positioning over critical zones for months at a time. As per the European Space Agency, environmental monitoring programs utilize resolutions ranging from 10 to 60 meters via the Copernicus Sentinel network to monitor macro-deforestation rates, coastal changes, and regional agricultural water usage across millions of hectares. A single surveillance node can capture 10 terabytes of high definition sensor data daily while operating continuously for 90 days without ground intervention. Border control authorities utilize these capabilities to detect unauthorized crossings, track illicit trafficking routes, and coordinate rapid response units across 2000 kilometer perimeters. Tactical multi-agency reports confirm that incorporating persistent aerial observation platforms significantly compresses interception and response timelines during transnational border security incidents by delivering continuous, real-time geolocated threat streams. Additionally, meteorological agencies deploy stratospheric sensors to measure atmospheric composition changes at precise altitudes, generating continuous, real-time datasets that refine micro-climatic models and improve short-term weather forecasting fidelity. This sustained observational capacity transforms how governments manage territorial security and environmental stewardship.

MARKET RESTRAINTS

Stringent Airspace Integration Regulations And Spectrum Allocation Constraints

The operational deployment of stratospheric platforms faces extensive regulatory hurdles due to overlapping jurisdictional requirements and limited radio frequency availability, which restrains the growth of the high altitude pseudo satellites market. Civil aviation authorities mandate strict separation protocols to prevent interference with commercial aircraft cruising at lower altitudes, which complicates flight path approvals across international boundaries. According to the Federal Aviation Administration, integrating unmanned aerial systems into controlled airspace relies on a structured five-phase type certification process, with individual evaluation timelines varying substantially based on the platform's specific risk classification. Spectrum congestion presents an additional complication, as telecommunications regulators allocate narrow bandwidth segments for non terrestrial applications to prevent signal overlap with existing satellite constellations. The International Telecommunication Union designates specific regional and global millimeter-wave (mmWave) and fixed frequency bands for High-Altitude Platform Stations (HAPS), allocating broad spectrum blocks to enable high-throughput connectivity while preventing interference. These regulatory limitations force developers to conduct extensive coordination with 15 different national aviation authorities before initiating cross border missions. Furthermore, frequency licensing demands comprehensive electromagnetic compatibility testing under standardized aerospace guidelines like DO-160G, which increases engineering compliance workloads and extends commercial deployment schedules. These structural barriers significantly slow the transition from experimental testing to widespread commercial utilization.

Technical Limitations In Energy Storage And Propulsion Endurance At Stratospheric Levels

Sustaining continuous flight operations within the upper atmosphere requires overcoming severe energy density constraints and temperature induced material degradation, which hinder the expansion of the high altitude pseudo satellites market. Solar powered aerial platforms depend on photovoltaic arrays to generate daytime electricity while relying on battery systems to maintain propulsion during extended nighttime cycles. National research benchmarks indicate that current lithium-ion configurations deliver specific energies near 250 Wh/kg, which introduces severe structural weight penalties for stratospheric platforms requiring continuous power during extended nocturnal operations. Stratospheric temperatures routinely drop to 55 degrees below zero and colder, causing severe electrochemical performance degradation or total operational failure within unprotected energy storage units. These thermal extremes necessitate specialized thermal management and heating mechanisms, introducing a continuous parasitic power draw that diminishes the platform's overall operational endurance. Aerodynamic research confirms that low fluid density at atmospheric pressures below 50 millibars drastically reduces propeller thrust and lift generation, forcing aerospace engineers to utilize ultra-high-aspect-ratio wing structures to maintain flight. This structural weight penalty from battery systems tightly restricts maximum payload capacities, limiting the weight and power budget available for advanced communication arrays and heavy sensor equipment. Consequently, developers must prioritize incremental battery chemistry improvements before achieving multi month station keeping capabilities.

MARKET OPPORTUNITIES

Expansion Of Fifth Generation Mobile Networks And Complementary Infrastructure Deployment

The rapid rollout of advanced mobile telecommunications architectures creates substantial integration pathways for aerial communication platforms to serve as dynamic network nodes, which is anticipated to fuel the growth of the high altitude pseudo satellites market. Telecommunications operators require dense infrastructure deployment to achieve ultra low latency and gigabit data throughput, particularly in urban corridors where ground level base stations face physical space limitations. Stratospheric platforms offer a cost effective alternative by projecting signals across 300 kilometer diameters while consuming 75 percent less energy than equivalent terrestrial tower clusters. The deployment of aerial relays reduces infrastructure deployment timelines by 8 months compared to conventional construction methods. Mobile network providers utilize these elevated nodes to backhaul traffic from hundreds of remote rural cell sites simultaneously, effectively eliminating the requirement for laying physical fiber-optic cabling across mountainous regions. Furthermore, the integration of software defined networking architectures enables dynamic bandwidth allocation, allowing platforms to redirect 15 gigabits per second toward emergency response zones during crisis events. This infrastructure synergy accelerates network modernization while reducing capital expenditure requirements.

Integration Of Artificial Intelligence For Autonomous Flight Navigation And Real Time Data Processing

Advanced computational algorithms enable stratospheric platforms to execute complex flight maneuvers and process massive information streams without continuous ground intervention, which offers major opportunities for the expansion of the high altitude pseudo satellites market. Machine learning architectures analyze atmospheric pressure variations, wind shear patterns, and solar irradiance fluctuations to optimize station keeping trajectories with sub meter precision. Engineering models demonstrate that artificial intelligence-driven navigation systems substantially reduce trajectory drift errors through autonomous deep-learning correction loops, lowering the necessity for continuous manual ground control supervision. Autonomous data processing capabilities allow onboard systems to filter 90 percent of redundant imagery before transmission, preserving valuable bandwidth for critical intelligence dissemination. Furthermore, predictive maintenance algorithms monitor propulsion motor vibrations and structural stress points, forecasting component failures 200 hours in advance with 92 percent accuracy. This technological convergence enables operators to deploy single pilot command centers managing 12 simultaneous aerial platforms, dramatically reducing operational overhead. The integration of neural network architectures transforms passive observation systems into intelligent decision making assets capable of executing autonomous mission parameters.

MARKET CHALLENGES

Vulnerability To Extreme Stratospheric Weather Patterns And Solar Radiation Degradation

Vulnerability to erratic stratospheric climate dynamics and solar radiation photodegradation challenges the growth of the high altitude pseudo satellites market. Operating continuously at altitudes exceeding 18000 meters exposes aerial platforms to severe atmospheric disturbances and intense ultraviolet exposure that accelerate material degradation. Sudden jet stream fluctuations generate wind velocities surpassing 250 kilometers per hour, creating structural stress that compromises wing integrity and disrupts station keeping trajectories. According to the National Aeronautics and Space Administration, uncrewed platforms operating in the stratosphere are exposed to intense ultraviolet radiation and up to 35% higher solar irradiance than ground systems, requiring specialized protective encapsulants to limit long-term photovoltaic cell degradation to baseline levels. Thermal cycling between 80 degrees above zero during daylight operations and 60 degrees below zero at night generates micro fractures in composite materials after 500 flight cycles. These environmental factors necessitate ultra-thin, lightweight protective coatings engineered at microscopic scales to shield the airframe from severe UV degradation without adding prohibitive structural weight. Operators must develop advanced shielding methodologies to extend platform lifespans.

High Capital Expenditure For Specialized Materials And Ground Station Network Establishment

Manufacturing stratospheric platforms requires precision-engineered components and ultra-lightweight composite structures that demand substantial financial investment and specialized production facilities, which holds back the expansion of the high-altitude pseudo-satellites market. Advanced carbon-fiber reinforced polymers constitute a critical core structural component of these vehicles, with labor-intensive automated layup, autoclave processing, and non-destructive testing representing the largest components of total manufacturing expenditures. Industrial project blueprints demonstrate that establishing a dedicated manufacturing center for high-altitude platform stations requires specialized clean-room assembly environments, computerized carbon-fiber automated layup setups, and vacuum infusion equipment to ensure structural uniformity. Ground infrastructure deployment requires strategically located launch and recovery sites equipped with phased-array antennas, while long-range mission trajectories are managed continuously via centralized, cloud-linked command applications. Each ground facility demands 1200 square meters of operational space and consumes 800 kilowatts of continuous electrical power to maintain signal transmission capabilities. The procurement of encrypted communication hardware and redundant backup systems increases total network establishment costs. These substantial financial barriers restrict market participation to well capitalized aerospace corporations and government entities, limiting competitive innovation and delaying commercial scalability initiatives.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 14.45% |

| Segments Covered | By Platform, Payload, Application, Deployment, Technology, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | AUGUR-RosAeroSystems, Prismatic Ltd, Airbus SE, Astigan Ltd, Thales Group, Lockheed Martin Corporation, AeroVironment Inc, and Loon LLC (Alphabet Inc.) |

SEGMENTAL ANALYSIS

By Platform Insights

The unmanned Aerial Vehicles segment was the top performer in the high altitude pseudo satellites market and accounted for a 50.5% share in 2025. Factors such as superior aerodynamic efficiency and extended endurance capabilities drive the dominance of this segment. The integration of ultra-lightweight carbon fiber composite structures minimizes structural dead-weight, allowing long-endurance solar-powered HAPS platforms to carry payloads ranging from 15 to 45 kilograms depending on airframe scaling, while maintaining station-keeping capabilities at altitudes of approximately 20,000 meters. As per the European Space Agency's higher airspace studies, UAV-based HAPS platforms offer highly flexible deployment advantages, though their seasonal operational availability remains deeply constrained by wind velocities, cloud cover during launch, and localized solar irradiance variations. The integration of autonomous flight management systems reduces ground control intervention requirements, lowering operational expenditures for commercial deployments. Defense agencies prioritize UAV platforms for intelligence gathering missions because these systems provide persistent surveillance coverage across 300 kilometer diameters with sub meter spatial resolution imaging capabilities. The scalability of unmanned aerial vehicle architectures allows manufacturers to customize configurations for specific mission profiles, accelerating adoption across telecommunications and environmental monitoring sectors.

But the balloon systems segment is likely to experience the fastest CAGR of 24.5% from 2026 to 2034 due to minimal infrastructure requirements and rapid deployment capabilities. The buoyancy driven flight mechanics eliminate propulsion energy demands during daytime operations, extending mission endurance to 180 consecutive days under optimal atmospheric conditions. Aerospace flight tracking shows that balloon-based HAPS systems utilize advanced ballast and gas management algorithms to navigate changing wind vectors at varying stratospheric layers, enabling sustained regional loitering and persistence over targeted geographic areas. The modular payload integration architecture supports simultaneous deployment of communication relays, imaging sensors, and atmospheric sampling instruments without compromising flight performance. Commercial operators leverage balloon platforms for temporary connectivity solutions during major events or disaster recovery scenarios because these systems provide 15 gigabits per second throughput across remote territories. The reduced manufacturing complexity lowers unit costs relative to unmanned aerial vehicles, enabling broader market accessibility for emerging economy applications.

By Payload Insights

The communication payloads segment held the majority share of 35.7% of the high altitude pseudo satellites market in 2025. This supremacy of the segment was credited to escalating global demand for ubiquitous broadband connectivity. As per the International Telecommunication Union, frequency allocation frameworks now support dedicated spectrum bands for non terrestrial communication systems, enabling interference free operations across multiple platforms. The integration of software defined radio architectures allows dynamic bandwidth allocation, optimizing spectral efficiency during peak usage periods. Defense organizations utilize secure communication payloads for beyond line of sight data transmission, ensuring resilient command and control networks during contested electromagnetic environments. The convergence of satellite and aerial network technologies creates hybrid architectures that enhance service reliability while reducing capital expenditure requirements for next generation telecommunications infrastructure.

On the other hand, the weather and environmental sensor payloads segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 26.8% over the forecast period owing to intensifying climate monitoring requirements. According to environmental remote sensing frameworks, stratospheric platforms equipped with advanced hyperspectral imaging instruments can detect trace gas concentration anomalies and track greenhouse gas emission plumes over vast regional grids, enhancing the fidelity of climate monitoring systems. The deployment of experimental miniaturized lidar payloads enables high-resolution three-dimensional wind field mapping, providing localized atmospheric data that refines numerical weather prediction models and improves storm trajectory forecasting. As per meteorological observation frameworks, HAPS-based environmental sensors can fill critical observation gaps between low Earth orbit satellites and ground-based stations, providing persistent data streams that enhance early warning systems for localized extreme weather events. The integration of artificial intelligence driven data processing algorithms enables real time anomaly detection, accelerating emergency response coordination during natural disasters. Research institutions leverage these payloads for atmospheric chemistry studies because stratospheric platforms operate above cloud interference while maintaining proximity to target measurement zones. The growing regulatory emphasis on climate accountability drives government investments in persistent environmental monitoring capabilities, establishing sustainable revenue pathways for sensor payload manufacturers.

By Application Insights

The defense applications segment led the High Altitude Pseudo Satellites Market and captured a 46.7% share in 2025 because of strategic requirements for persistent intelligence and surveillance capabilities. A single defense-oriented HAPS system can monitor vast geographic perimeters continuously, significantly lowering the necessity for continuous ground patrols while enhancing situational awareness through multi-spectral sensor fusion. As per the United States Department of Defense, stratospheric platforms provide resilient communication backbones that maintain operational connectivity during contested electromagnetic environments where satellite links face vulnerability. The integration of electronic intelligence payloads enables signals interception across 1500 kilometer ranges, supporting strategic decision making with real time threat assessment data. Defense contractors prioritize HAPS deployments because these systems offer cost effective alternatives to manned reconnaissance aircraft, reducing mission expenditures by 70 percent per flight hour. The growing complexity of asymmetric warfare scenarios accelerates adoption of persistent aerial observation platforms that deliver actionable intelligence with minimal logistical footprint.

On the contrary, the telecommunications services segment is expected to exhibit a noteworthy CAGR of 28.3% during the forecast period. This swift expansion of the segment is propelled by urgent requirements for universal broadband access. A single stratospheric communication node can deliver 15 gigabits per second throughput across 300 kilometer coverage areas, eliminating the need for extensive terrestrial tower deployment in topographically challenging regions. Econometric models highlighted by international telecom frameworks indicate that expanding mobile broadband penetration by 10% could increase gross domestic product per capita growth by up to 2.5% in emerging markets. The integration of network slicing technologies enables telecommunications providers to allocate dedicated bandwidth segments for emergency services, industrial automation, and consumer applications simultaneously. Commercial operators leverage HAPS platforms for temporary connectivity during major events or infrastructure maintenance because these systems provide rapid deployment capabilities with 99.99 percent service availability. The convergence of satellite and aerial network architectures creates resilient hybrid infrastructures that enhance service continuity while reducing capital expenditure requirements for next generation telecommunications ecosystems.

By Deployment Insights

The land based operations segment dominated the global market and accounted for a 58.2% share in 2025. This dominance of the segment is fuelled by established ground infrastructure and favorable regulatory environments. The proximity to population centers enables efficient payload data transmission through existing fiber optic backhaul networks, reducing latency compared to maritime deployment scenarios. As per civil aviation guidelines, land-based HAPS operations must navigate structured airspace coordination procedures to ensure safe, localized segregation from commercial air traffic during launch and ascent phases. The integration of automated launch systems allows daily sortie generation with minimal personnel requirements, optimizing operational efficiency for commercial service providers. Defense organizations prioritize land based deployments because these configurations support secure facility access and rapid payload reconfiguration between missions. The growing availability of dedicated HAPS operating zones within national airspace frameworks reduces regulatory uncertainty, encouraging private sector investments in persistent aerial service platforms.

However, the disaster prone areas segment is estimated to register the fastest CAGR of 31.2% from 2026 to 2034. This quick surge of the segment is driven by escalating requirements for resilient emergency communication and situational awareness capabilities. According to the United Nations Office for Disaster Risk Reduction, climate related catastrophes increased by 83 percent over the past two decades, creating urgent demand for rapidly deployable aerial platforms that restore connectivity within 72 hours of event onset. HAPS systems operating in disaster affected territories can provide 10 gigabits per second emergency communication bandwidth across 250 kilometer coverage areas, supporting coordination among 50000 first responders simultaneously. As per humanitarian relief frameworks, stratospheric platforms substantially accelerate emergency response coordination by delivering real-time damage assessment imagery and autonomous survivor location mapping directly to rescue crews. The modular payload architecture enables rapid reconfiguration between communication relay, thermal imaging, and atmospheric monitoring functions based on evolving mission requirements. Humanitarian organizations leverage HAPS deployments because these systems maintain operational continuity during ground infrastructure destruction, ensuring persistent service delivery when conventional networks fail. The growing frequency of extreme weather events accelerates government investments in pre positioned aerial assets that guarantee rapid response capabilities during crisis scenarios.

By Technology Insights

The unmanned Aerial Vehicle technology segment held the majority share of 52.7% of the global market in 2025 because of superior flight control precision and payload integration flexibility. According to UAV based HAPS platforms achieve positional stability within 100 meter tolerances through advanced autopilot systems that compensate for stratospheric wind shear effects in real time. The integration of distributed electric propulsion architectures enhances aerodynamic efficiency compared to conventional single motor configurations, extending mission endurance to 120 consecutive days. As per the European Union Aviation Safety Agency, unmanned aerial vehicle (UAV) designs leverage established Specific Operations Risk Assessment (SORA) pathways, though a unified regulatory framework for all higher airspace operations (HAO) remains under active, coordinated development to address emerging airship and balloon designs safely. The modular airframe designs support rapid payload reconfiguration between communication, imaging, and electronic intelligence functions without compromising flight performance characteristics. Defense contractors prioritize UAV technology because these platforms provide scalable architectures that accommodate evolving mission requirements while maintaining interoperability with existing command and control networks. The growing availability of commercial off the shelf components reduces manufacturing costs, enabling broader market accessibility for emerging economy applications.

On the contrary, the stratospheric balloon technology segment is anticipated to witness the fastest CAGR of 27.4% during the forecast period due to minimal energy requirements and simplified operational procedures. The passive altitude control mechanisms maintain station keeping within 800 meter tolerances using ballast management systems that compensate for thermal expansion effects without active propulsion intervention. As per the National Aeronautics and Space Administration, stratospheric balloons provide stable observation platforms for scientific instruments because these systems experience minimal vibration and acoustic interference compared to powered flight configurations. The rapid deployment capabilities enable mission initiation within 24 hours of authorization, supporting time sensitive applications such as disaster response and temporary event connectivity. Commercial operators leverage balloon technology for atmospheric research because these platforms offer extended endurance at reduced operational complexity, enabling continuous data collection across seasonal cycles. The growing emphasis on sustainable aviation technologies accelerates adoption of buoyancy based flight systems that minimize carbon emissions while delivering persistent aerial services.

REGION ANALYSIS

North America Market Analysis

North America was the top performer in the global High Altitude Pseudo Satellites Market and accounted for a 38.6% share in 2025. The demand for these satellites was attributed to robust defense investments and advanced aerospace innovation ecosystems. The presence of established aerospace manufacturers enables rapid technology maturation cycles that reduce development timelines compared to emerging market regions. As per the Federal Aviation Administration, streamlined regulatory frameworks accelerate operational approval processes for experimental stratospheric flights, encouraging private sector investments in commercial service offerings. The integration of HAPS platforms with existing satellite and terrestrial networks creates hybrid architectures that enhance service reliability while reducing infrastructure deployment costs. Defense contractors prioritize North American deployments because these regions provide secure testing environments and skilled technical workforces that support complex system integration activities. The growing emphasis on resilient communication infrastructure accelerates adoption of stratospheric platforms that guarantee service continuity during terrestrial network disruptions or contested electromagnetic environments.

Europe Market Analysis

Europe was the next prominent regional player in the High Altitude Pseudo Satellites market and captured a 27.5% share in 2025. This growth of the European market was supported by collaborative research initiatives and environmental monitoring priorities. According to the European Space Agency, member states heavily prioritize and fund optional and mandatory Earth observation and telecommunication programs, utilizing public-private co-funding to drive innovation in climate monitoring and satellite-complementary connectivity solutions. The integration of solar powered propulsion systems aligns with European Union sustainability mandates, reducing operational carbon emissions compared to conventional aviation alternatives. As per the European Aviation Safety Agency, harmonized regulatory frameworks enable cross border HAPS operations that optimize airspace utilization across continental territories. The presence of leading aerospace manufacturers facilitates technology transfer and knowledge sharing that accelerates innovation cycles for next generation stratospheric platforms. Commercial operators leverage European HAPS deployments because these regions provide stable regulatory environments and skilled technical workforces that support complex system integration activities. The growing emphasis on digital inclusion accelerates adoption of aerial connectivity solutions that bridge broadband access gaps across rural and remote territories.

Asia Pacific Market Analysis

Asia Pacific is also a key player in the High Altitude Pseudo Satellites Market due to large unconnected populations and expanding digital infrastructure requirements. The integration of HAPS platforms with fifth generation mobile networks enables cost effective broadband deployment across topographically complex territories where terrestrial infrastructure proves economically unfeasible. As per the International Telecommunication Union, Asia-Pacific nations actively prioritize aerial and non-terrestrial connectivity solutions to address the severe rural-urban digital divide, targeting isolated communities that form part of the world's 1.8 billion rural offline individuals. The presence of emerging aerospace manufacturers facilitates localized production capabilities that reduce procurement costs compared to imported alternatives. Commercial operators leverage Asia Pacific HAPS deployments because these regions provide growing consumer markets and supportive policy frameworks that encourage technology adoption. The escalating frequency of climate related disasters accelerates government investments in resilient communication platforms that guarantee service continuity during infrastructure disruptions.

Middle East and Africa Market Analysis

The Middle East and Africa region is an emerging player in the High Altitude Pseudo Satellites market owing to expanding connectivity requirements and resource monitoring priorities. The integration of multispectral imaging payloads enables precision agriculture initiatives that increase crop yields through data driven irrigation and fertilization strategies. The growing emphasis on natural resource management accelerates adoption of persistent observation platforms that monitor water reserves and mineral extraction activities. Commercial operators leverage Middle East and Africa HAPS deployments because these regions provide untapped market opportunities and supportive policy frameworks that encourage technology adoption. The escalating requirements for maritime domain awareness accelerate government investments in stratospheric platforms that enhance coastal surveillance capabilities across extensive territorial waters.

Latin America Market Analysis

Latin America is likely to expand in the High Altitude Pseudo Satellites market during the forecast period due to expanding telecommunications requirements and environmental conservation priorities. The integration of real time data transmission capabilities enables rapid emergency response coordination during natural disasters that affect millions of individuals annually across the region. In addition, the growing emphasis on sustainable development accelerates adoption of solar powered platforms that minimize environmental impact while delivering persistent aerial services. Commercial operators leverage Latin American HAPS deployments because these regions provide emerging market opportunities and supportive policy frameworks that encourage technology adoption. The escalating requirements for forest conservation monitoring accelerate government investments in stratospheric platforms that enhance deforestation detection capabilities across extensive tropical territories.

COMPETITIVE LANDSCAPE

The High Altitude Pseudo Satellites Market features intensifying competition among established aerospace manufacturers and emerging technology specialists pursuing strategic differentiation through innovation and partnership development. Market participants leverage proprietary aerodynamic configurations and energy management technologies to deliver platforms capable of extended stratospheric operations with minimal logistical support. Organizations pursue regulatory engagement initiatives that accelerate operational approval processes for commercial deployments across diverse geographical regions. Companies establish collaborative frameworks with telecommunications providers and government agencies to customize platform configurations that address specific mission requirements while maintaining interoperability with existing network infrastructures. Market leaders invest in artificial intelligence driven autonomy features that reduce ground control intervention requirements while enhancing operational efficiency through real time decision making capabilities. Organizations implement iterative flight testing programs that validate system reliability under diverse atmospheric conditions while gathering performance data for continuous improvement cycles. Companies develop modular architectures that enable rapid payload reconfiguration between communication imaging and electronic intelligence functions without compromising flight performance characteristics. Market participants prioritize sustainability initiatives that minimize environmental impact through solar powered propulsion and lightweight composite materials that reduce operational carbon emissions. Organizations expand global service networks that enable localized deployment and maintenance capabilities across diverse geographical regions while strengthening customer relationships through responsive support frameworks. The competitive landscape continues evolving as technological advancements and regulatory developments create new opportunities for market entrants and established players pursuing strategic growth initiatives.

KEY MARKET PLAYERS

These are some of the major players in the global high-altitude pseudo-satellite (HAPS) market.

- AUGUR-RosAeroSystems

- Prismatic Ltd

- Airbus SE

- Astigan Ltd

- Thales Group

- Lockheed Martin Corporation

- AeroVironment Inc

- Loon LLC (Alphabet Inc.)

Top Players In The Market

- Airbus SE maintains prominent positioning within the High Altitude Pseudo Satellites Market through its Zephyr platform development and commercialization initiatives. The company leverages extensive aerospace engineering expertise to deliver solar powered unmanned aerial systems capable of 90 day continuous stratospheric operations. The organization collaborates with telecommunications providers and defense agencies to customize payload configurations that address specific mission requirements across global territories. Airbus prioritizes technology maturation through iterative flight testing programs that validate system reliability under diverse atmospheric conditions. The company integrates artificial intelligence driven autonomy features that reduce ground control intervention requirements while enhancing operational efficiency. Airbus SE continues expanding manufacturing capabilities to support increased production volumes as commercial demand for stratospheric platforms accelerates across multiple application sectors.

- AeroVironment Inc demonstrates significant market contribution through its high altitude long endurance unmanned aircraft systems designed for defense and commercial applications. The company leverages proprietary aerodynamic configurations and energy management technologies to deliver platforms capable of extended stratospheric missions with minimal logistical support. The organization collaborates with government agencies to customize system architectures that address specific operational requirements while maintaining interoperability with existing command and control networks. AeroVironment prioritizes technology innovation through research partnerships that accelerate development of next generation propulsion and autonomy features. The company expands global service offerings through strategic alliances that enable localized deployment and maintenance capabilities across diverse geographical regions. AeroVironment Inc continues strengthening market positioning through iterative product enhancements that address evolving customer requirements for persistent aerial observation and connectivity solutions.

- Thales Group maintains influential market presence through its Stratobus airship development and EuroHAPS demonstration initiatives supported by European Commission funding. The company leverages extensive systems integration expertise to deliver stratospheric platforms capable of one year continuous operations with 250 kilogram payload capacities. The organization collaborates with aerospace partners to validate system performance through comprehensive flight testing programs that demonstrate operational readiness for commercial and defense applications. Thales prioritizes technology maturation through iterative development cycles that address regulatory requirements and customer specifications across multiple market segments. The company expands service offerings through strategic partnerships that enable integrated solutions combining HAPS platforms with terrestrial and satellite network infrastructures. Thales Group continues strengthening competitive positioning through innovation investments that address emerging requirements for resilient communication and persistent observation capabilities across global territories.

Top Strategies Used By Key Market Participants

Key market participants employ strategic approaches centered on technology innovation and partnership development to strengthen competitive positioning within the High Altitude Pseudo Satellites Market. Organizations prioritize research and development investments that advance solar energy harvesting efficiency and autonomous flight management capabilities. Companies establish collaborative frameworks with telecommunications providers and government agencies to customize platform configurations that address specific mission requirements. Market leaders pursue regulatory engagement initiatives that accelerate operational approval processes for commercial stratospheric deployments. Organizations leverage strategic acquisitions to expand payload integration expertise and manufacturing capabilities. Companies implement iterative flight testing programs that validate system reliability under diverse atmospheric conditions while gathering performance data for continuous improvement. Market participants develop modular architectures that enable rapid payload reconfiguration between communication imaging and electronic intelligence functions. Organizations prioritize sustainability initiatives that minimize environmental impact through solar powered propulsion and lightweight composite materials. Companies establish global service networks that enable localized deployment and maintenance capabilities across diverse geographical regions. Market leaders invest in artificial intelligence driven autonomy features that reduce ground control intervention requirements while enhancing operational efficiency.

MARKET SEGMENTATION

This research report on the global high-altitude pseudo-satellite (HAPS) market has been segmented and sub-segmented based on the following categories.

By Platform

- Unmanned Aerial Vehicles (UAVs)

- Airships

- Balloon systems

By Payload

- Communication systems

- Imaging systems

- Electro-optical/Infrared (EO/IR) Sensors

- Synthetic Aperture Radar (SAR)

- Surveillance & reconnaissance

- Electronic Intelligence (ELINT)

- Signal Intelligence (SIGINT)

- Weather and environmental sensors

- Navigation and positioning systems

By Application

- Defense

- Border surveillance

- Maritime surveillance

- Disaster management

- Military operations

- Civilian government

- Environmental monitoring

- Weather forecasting

- Emergency services

- Commercial

- Telecommunications

- Internet services

- Agriculture

- Media & broadcasting

- Others

- Scientific research

By Deployment

- Land-based operations

- Maritime operations

- Polar regions

- Disaster-prone areas

By Technology

- Stratospheric Balloons

- Airships

- UAVs

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What are High-Altitude Pseudo Satellites (HAPS)?

HAPS are unmanned aircraft or balloons that operate in the stratosphere to provide satellite-like communication, imaging, and surveillance services.

How high do HAPS platforms operate?

HAPS typically fly between 18 km and 25 km above the Earth, above commercial air traffic and weather systems.

What is driving the growth of the HAPS market?

Rising demand for low-latency connectivity, border surveillance, disaster response, and remote communication is fueling market growth.

How are HAPS different from satellites?

HAPS offer lower latency, lower deployment cost, faster repositioning, and easier maintenance compared to traditional satellites.

Which industries use HAPS the most?

Defense, telecommunications, emergency services, environmental monitoring, and agriculture are the primary users of HAPS systems.

What types of HAPS platforms exist?

Solar-powered fixed-wing aircraft, airships, balloons, and long-endurance UAVs are the main HAPS platform types.

What is the biggest advantage of HAPS technology?

They provide near-satellite coverage with aircraft-level flexibility and much lower operational cost.

Are HAPS environmentally friendly?

Most modern HAPS platforms use solar energy, making them low-emission and sustainable.

How long can HAPS stay in the air?

Advanced HAPS can remain airborne for weeks to several months without landing.

What role do HAPS play in 5G and 6G networks?

HAPS act as aerial base stations to extend mobile network coverage to remote and disaster-hit areas.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com