Global High-Density Polyethylene (HDPE) Market Size, Share, Trends, & Growth Forecast Report Segmented By Application (Pipes and Tubes, Sheets and Films, Rigid Articles, and Other), Resin Grade, End-User Industry, and Region (Latin America, North America, Asia Pacific, Europe, Middle East and Africa), Industry Analysis from 2025 to 2033

Global High-Density Polyethylene (HDPE) Market Size

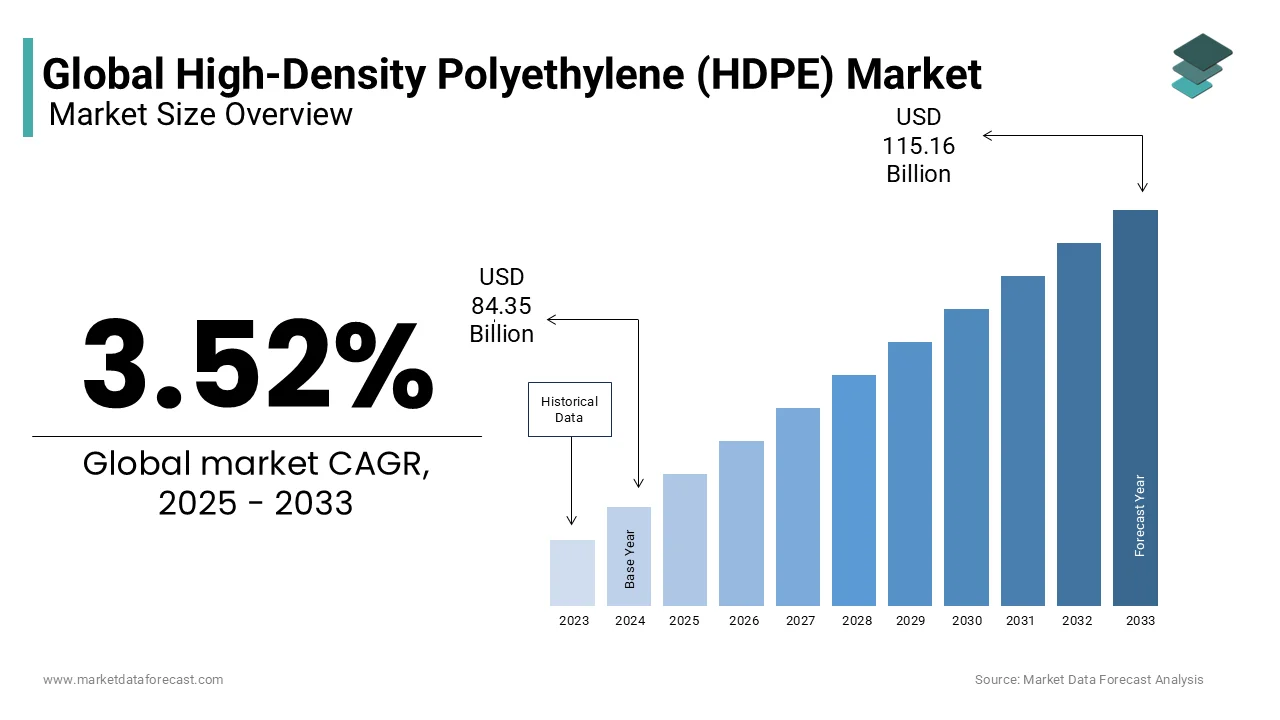

The global high-density polyethylene (HDPE) market size was valued at USD 84.35 billion in 2024 and is expected to reach USD 115.16 billion by 2033 from USD 87.32 billion in 2025. The market is projected to grow at a CAGR of 3.52%.

High-density polyethylene (HDPE) is a thermoplastic polymer derived from ethylene monomers, distinguished by its high strength-to-density ratio, chemical resistance, and durability under extreme temperatures. It is widely employed in applications requiring robustness and longevity, including pressure piping, blow-molded containers, geomembranes, and consumer packaging. Unlike low-density variants, HDPE exhibits a linear molecular structure with minimal branching, resulting in tighter polymer packing and enhanced mechanical properties. According to the research, millions of metric tons of HDPE were processed annually, reflecting its foundational role in industrial and municipal infrastructure. As per the study, HDPE accounts for a notable share of all polyethylene used in Europe, underscoring its dominance in rigid packaging and utility sectors. Its recyclability through established mechanical processes further supports its integration into circular economy frameworks, particularly in water management and food-safe packaging systems.

MARKET DRIVERS

Expansion of Water and Wastewater Infrastructure in Urbanizing Regions

The global push for resilient water infrastructure is a primary catalyst for HDPE demand, particularly in rapidly urbanizing economies. HDPE pipes are preferred for potable water and sewage networks due to their corrosion resistance, leak-proof joints, and service life exceeding 50 years. According to the World Bank, over 2 billion people live in countries experiencing high water stress, prompting large-scale investments in pipeline networks. India’s Jal Jeevan Mission aims to provide functional household tap connections to all rural households by 2024, necessitating kilometers of HDPE piping annually, as per the research. Similarly, in Africa, substantial amount per year is needed to close the water infrastructure gap, with HDPE increasingly replacing aging metal pipes. The U.S. Environmental Protection Agency notes that HDPE reduces water loss compared to traditional materials, making it a strategic choice for sustainable water management.

Rising Adoption in Food and Beverage Packaging for Shelf-Life Extension

HDPE’s impermeability to moisture and resistance to microbial contamination make it a critical material in food-grade packaging, particularly for milk, juice, and dairy products. Its use in blow-molded bottles and containers ensures product safety and extends shelf life without refrigeration in certain conditions. According to the Food and Agriculture Organization, global food waste amounts to 1.3 billion tonnes annually, driving demand for packaging that enhances preservation. In the U.S., notable sharevof milk is packaged in HDPE containers. Additionally, the European Food Safety Authority confirms HDPE as compliant with stringent migration limits for direct food contact. With e-commerce grocery sales growing annually, the need for durable, lightweight, and recyclable packaging has elevated HDPE’s role in modern supply chains.

MARKET RESTRAINTS

Volatility in Crude Oil and Natural Gas Feedstock Prices

HDPE production is heavily dependent on ethylene, which is primarily derived from naphtha cracking or ethane feedstocks linked to oil and natural gas markets. Price fluctuations in these commodities directly impact manufacturing costs and profit margins. According to the research, ethane prices in the Gulf Coast surged due to supply constraints and export demand. These volatilities disrupt long-term planning for manufacturers and deter investment in capacity expansion. The International Energy Agency warns that geopolitical instability and energy transition policies may prolong price unpredictability, challenging the economic stability of HDPE supply chains reliant on fossil-based inputs.

Regulatory Pressure on Single-Use Plastics in Consumer Applications

Increasing legislative scrutiny on disposable plastic packaging is constraining HDPE demand in certain end-use segments. The European Union’s Single-Use Plastics Directive bans specific HDPE-containing items such as lightweight plastic bags and mandates a 90% collection target for plastic bottles by 2029. As per the European Commission, member states must ensure that PET and HDPE bottles contain at least 30% recycled content by 2030. The United Nations Environment Programme reports that several countries have implemented some form of plastic restriction, affecting packaging design and material selection. While HDPE remains exempt from outright bans in many regions due to its recyclability, brand owners are reformulating packaging to reduce virgin plastic use, slowing volume growth in consumer-facing applications.

MARKET OPPORTUNITIES

Integration into Renewable Energy Infrastructure Projects

HDPE is emerging as a critical material in solar and wind energy installations, particularly for cable insulation and conduit systems. Its dielectric properties and resistance to UV degradation make it ideal for protecting electrical wiring in photovoltaic farms and offshore wind turbines. According to the International Renewable Energy Agency, global solar capacity increased and is expected to exceed further by 2030, necessitating millions of kilometers of HDPE-insulated cabling. Additionally, HDPE is used in geothermal loop systems for heat exchange, with study estimating that a large number of geothermal installations annually utilize HDPE piping. These applications position HDPE as an enabler of clean energy deployment, opening new demand corridors beyond traditional sectors.

Advancement in Recycled and Circular HDPE Technologies

Innovations in mechanical and chemical recycling are unlocking new growth avenues for post-consumer HDPE. Companies are investing in advanced sorting and decontamination technologies to produce food-grade recycled HDPE (rHDPE), reducing reliance on virgin resin. According to the research, North American rHDPE production capacity increased by I recent years. In Europe, the study points out that HDPE bottle recycling rates have surged. Unilever and Nestlé have committed to using 25% rHDPE in their packaging by 2025, as per their sustainability disclosures. Also, scaling rHDPE could reduce the sector’s carbon footprint millions of tonnes of CO₂ equivalent annually by 2030, aligning with global net-zero goals and enhancing brand compliance.

MARKET CHALLENGES

Contamination in Recycling Streams Affecting rHDPE Quality

Contamination from mixed plastics, labels, adhesives, and residual contents in post-consumer waste is a major obstacle to the circularity of HDPE. Even a small contamination with polyvinyl chloride (PVC) can degrade the entire batch during reprocessing, as noted by the Society of Plastics Engineers. According to study, a portion of collected HDPE containers in developing economies are contaminated with non-recyclable materials due to inadequate segregation. In the U.S., the Environmental Protection Agency acknowledges that only a portion of HDPE containers were recycled in 2022, with the remainder lost to landfill or incineration. Advanced sorting technologies like near-infrared (NIR) spectroscopy are improving purity, but adoption remains limited. The lack of standardized labeling and consumer awareness further exacerbates the issue, undermining the viability of high-quality rHDPE for premium applications.

Geographic Disparities in Waste Collection and Recycling Infrastructure

The effectiveness of HDPE recycling is heavily dependent on regional waste management systems, which vary significantly across geographies. In Southeast Asia, rapid urbanization has outpaced waste infrastructure development; Indonesia generates significant tonnes of plastic waste annually, yet only small share is formally collected, as per the study. This imbalance disrupts the supply of clean post-consumer feedstock needed for rHDPE production. Additionally, informal waste pickers, while crucial, lack integration into formal recycling value chains, reducing efficiency. These disparities hinder global efforts to scale circular HDPE models and increase production costs in regions reliant on imported recycled resin.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.52% |

| Segments Covered | By Application, Resin Grade, End-User Industry, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Mitsui Chemicals Inc. (Japan), Chevron Phillips Chemical Company (US), Exxon Mobil Corporation (US), DowDuPont (US), LyondellBasell Industries Holdings B.V. (The Netherlands), Reliance Industries Limited (India), INEOS Group Holdings SA (UK), SABIC (Saudi Arabia), Petronas Chemicals Group Berhad (Malaysia), and China Petrochemical Corporation, and others |

SEGMENTAL ANALYSIS

By Application Insights

The pipes and tubes segment dominated the HDPE application landscape by capturing 32.7% of global demand in 2024. This position is anchored in HDPE’s exceptional durability, flexibility, and resistance to corrosion, making it ideal for water supply, gas distribution, and sewer systems. According to the U.S. Environmental Protection Agency, miles of HDPE piping have been installed in municipal water networks across the United States, reducing leakage rates compared to traditional ductile iron. In India, the Jal Jeevan Mission also uses HDPE for rural water supply projects, with large kilometers deployed annually, as per the study. Additionally, HDPE’s ability to withstand seismic activity, demonstrated during Japan’s 2011 earthquake where HDPE lines remained intact, has made it a preferred material in seismically active regions, further solidifying its dominance in infrastructure development.

The sheets and films segment is expanding at the fastest rate and is projected to grow at a CAGR of 6.7% from 2025 to 2033. This acceleration is driven by rising demand for agricultural mulch films, geomembranes in mining, and protective liners in landfills. HDPE films are increasingly used in large-scale farming to retain soil moisture and suppress weeds, improving crop yields, as per the Food and Agriculture Organization. Additionally, the mining sector relies on HDPE geomembranes for tailings containment; most of new mine projects in Latin America now use HDPE liners to prevent groundwater contamination. With increasing investments in waste containment and sustainable agriculture, the segment is poised for sustained expansion.

By Resin Grade Insights

The PE-100 resin grade held the largest share of the HDPE resin market at 52.5% of total consumption in 2025. This dominance is due to its superior pressure resistance, slow crack growth performance, and suitability for high-stress applications such as gas and water pipelines. PE-100 can withstand operating pressures of up to 10 bar at 20°C for 50 years, meeting ISO 4427 standards for potable water systems. In the Middle East, where extreme temperatures challenge pipeline integrity, PE-100’s thermal stability has made it the material of choice for desalinated water transmission, with Saudi Arabia’s National Water Company deploying kilometers of PE-100 piping in its distribution network.

The PE-100-RC (resistant to crack) grade is the fastest-growing and is anticipated to expand at a CAGR of 8.2% through 2033. This rapid growth is fueled by its enhanced resistance to slow crack growth and rapid crack propagation, critical in high-risk environments such as gas transmission and offshore applications. PE-100-RC can withstand higher stress concentrations than standard PE-100, according to the research, making it ideal for trenchless installation methods like horizontal directional drilling. With increasing regulatory emphasis on pipeline safety and lifecycle performance, this advanced grade is becoming the benchmark for next-generation utility networks.

By End-User Industry Insights

The packaging industry was the leading end-user of HDPE, representing about 41% of global consumption in 2023, as stated by the American Chemistry Council. This dominance is driven by HDPE’s widespread use in blow-molded bottles for milk, detergents, shampoos, and pharmaceuticals, where its rigidity, chemical resistance, and recyclability are highly valued. Also, HDPE bottle collection rates in the EU surged, supporting circular economy goals. Additionally, e-commerce growth has increased demand for durable shipping containers and protective packaging, with Amazon and other logistics firms adopting HDPE-based reusable totes. The material’s compatibility with food-grade standards and established recycling streams ensures its continued leadership in rigid packaging applications.

The building and construction sector is emerging as the fastest-growing end-user and is projected to expand at a CAGR of 6.9% from 2025 to 2033. This growth is fueled by the increasing use of HDPE in plumbing, insulation, and structural protection systems. HDPE is now widely used in radiant floor heating systems, where its flexibility and thermal efficiency reduce energy consumption, as per the study. In high-rise construction, HDPE conduit systems protect electrical wiring from moisture and fire, with the National Fire Protection Association confirming their compliance with NEC standards. Additionally, HDPE is being integrated into modular and prefabricated buildings due to its lightweight nature and ease of installation. In Southeast Asia, countries like Vietnam and Indonesia are adopting HDPE piping in affordable housing projects, supported by government infrastructure programs, accelerating its penetration in urban development.

REGIONAL ANALYSIS

Asia Pacific High-Density Polyethylene Market Insights

Asia Pacific led the global HDPE market by holding a 44.5% of total demand in 2024. As the world’s most populous region, it is a hub for manufacturing, urbanization, and infrastructure development, all of which drive polymer consumption. China alone accounts for a notable share of global HDPE demand. India’s Smart Cities Mission and Jal Jeevan Mission are accelerating HDPE pipe deployment, while Southeast Asian nations like Indonesia and the Philippines are expanding plastic processing capacities. Japan and South Korea maintain high per-capita HDPE usage in electronics and automotive applications. With many new ethylene cracker projects underway, the region is not only a major consumer but also a growing producer, reshaping global supply dynamics.

North America High-Density Polyethylene Market Insights

North America is another key player by capturing 23.1% of the global HDPE market. The region benefits from abundant shale gas feedstock, which has lowered ethylene production costs and strengthened domestic HDPE manufacturing. The U.S. produces significant tonnes of HDPE annually, with Texas and Louisiana serving as primary production hubs. According to the rearch, many HDPE in North America is used in packaging and construction, supported by strict building codes favoring durable materials. Canada’s investment in water infrastructure, including Indigenous community water systems, has increased HDPE pipe demand. Additionally, the EPA’s emphasis on reducing water loss has driven municipalities to replace aging metal pipes with HDPE. With strong recycling initiatives in states like California, the region is also advancing circular HDPE models, enhancing long-term sustainability.

Europe High-Density Polyethylene Market Insights

Europe accounts for a significant share of the global HDPE market. The region maintains a mature but evolving HDPE landscape, shaped by stringent environmental regulations and circular economy mandates. The European Green Deal requires all plastic packaging to be reusable or recyclable by 2030, prompting brands to increase rHDPE content. The Netherlands and France are key players in HDPE pipe adoption for gas and water networks, particularly PE-100-RC for enhanced safety. Additionally, the EU’s Construction Products Regulation is driving demand for long-life, low-maintenance materials in building projects. Despite slower growth, Europe remains a technology leader in advanced HDPE grades and recycling innovation, influencing global standards.

Middle East and Africa High-Density Polyethylene Market Insights

Middle East and Africa collectively represent 9% of the global HDPE market, as reported by OPEC’s Annual Statistical Bulletin. The Gulf Cooperation Council (GCC) countries are major producers due to access to low-cost ethane feedstock, with Saudi Arabia and Iran operating some of the world’s largest ethylene complexes. SABIC is a top global HDPE producer with several million tonnes of production capacity and extensive exports. According to the study, regional HDPE capacity is expected to grow by 2027. In Africa, rising urbanization in Nigeria, Kenya, and South Africa is increasing demand for water pipes and packaging.

Latin America High-Density Polyethylene Market Insights

Latin America holds smaller share of the global HDPE market. The region is witnessing steady growth, led by Brazil, Mexico, and Chile, where industrialization and infrastructure development are accelerating polymer demand. Brazil consumes tonnes of HDPE annually, primarily for packaging and agriculture, according to the study. Mexico’s proximity to the U.S. enables integration into North American supply chains, with maquiladora plants using HDPE in electronics and automotive components. Chile is adopting HDPE in mining operations for slurry transport and containment. Additionally, Colombia’s National Infrastructure Agency is deploying HDPE pipes in rural water projects. With expanding petrochemical capacity in Argentina and Ecuador, Latin America is gradually reducing import dependence, positioning itself as a self-sufficient HDPE market in the long term.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

The key players in the high-density polyethylene market are Mitsui Chemicals Inc. (Japan), Chevron Phillips Chemical Company (US), Exxon Mobil Corporation (US), DowDuPont (US), LyondellBasell Industries Holdings B.V. (The Netherlands), Reliance Industries Limited (India), INEOS Group Holdings SA (UK), SABIC (Saudi Arabia), Petronas Chemicals Group Berhad (Malaysia), and China Petrochemical Corporation.

The high-density polyethylene market is characterized by intense competition shaped by feedstock access, technological innovation, and compliance with evolving environmental regulations. While global producers dominate through scale and R&D capabilities, regional players are gaining ground by offering cost-competitive resins tailored to local infrastructure and packaging needs. Differentiation is increasingly achieved through advanced resin grades such as PE-100-RC and recycled HDPE, rather than price alone. The rise of circular economy mandates in Asia and Europe has intensified competition in sustainable product development, with companies racing to commercialize food-grade recycled content. Strategic alliances with waste management firms and brand owners are becoming critical to securing feedstock and offtake agreements. The competitive landscape is further influenced by energy costs, with shale-based producers in North America and gas-rich regions in the Middle East maintaining cost advantages, while Asian converters focus on value-added applications to offset import dependency.

TOP PLAYERS IN THE MARKET

SABIC

SABIC has established a formidable presence in the Asia Pacific HDPE market through strategic investments in advanced resin development and regional partnerships. The company operates a major production hub in Singapore and supplies tailored HDPE grades for pipe, film, and packaging applications across Southeast Asia. It collaborated with Thai Union Group to develop recyclable HDPE packaging for seafood products, aligning with ASEAN’s plastics circularity roadmap. Additionally, SABIC partnered with Japan’s Mitsui Chemicals to co-develop high-performance PE-100-RC resins for gas and water infrastructure. These initiatives underscore SABIC’s focus on innovation, sustainability, and localized solutions to meet the region’s evolving regulatory and industrial demands.

ExxonMobil

ExxonMobil plays a pivotal role in the Asia Pacific HDPE landscape by leveraging its proprietary catalyst technologies and integrated supply chain to deliver high-performance resins. The company’s Singapore refinery and petrochemical complex serve as a key export and formulation center for the region, supplying HDPE to packaging, construction, and automotive sectors. It also collaborated with Australian water authorities to promote the use of its HDPE pipe resins in drought-resilient water networks. Through technical service centers in Shanghai and Bangalore, ExxonMobil provides application engineering support to converters and municipal agencies. These efforts reflect its strategy to combine material science excellence with on-the-ground technical engagement to drive adoption in high-growth infrastructure and consumer markets.

LyondellBasell

LyondellBasell has deepened its engagement in the Asia Pacific HDPE market through technology licensing, joint development programs, and sustainability-focused product launches. The company supplies its Hostalen ACP technology to licensees in China, India, and Taiwan, enabling local producers to manufacture high-stiffness HDPE for blow molding and pipe applications. It partnered with Indonesia’s PT Chandra Asri to enhance recycling integration and expand circular product offerings. The company also established a customer innovation center in Shanghai to accelerate co-development of lightweight, durable packaging solutions. By combining proprietary process technology with a growing portfolio of circular polymers, LyondellBasell is positioning itself as a long-term enabler of sustainable industrial growth across the Asia Pacific region.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the high-density polyethylene market are deploying a combination of technological differentiation, vertical integration, and sustainability-driven innovation to consolidate their positions. Companies are investing in proprietary catalyst systems to produce resins with enhanced mechanical and processing properties, catering to specialized applications in piping and thin-film packaging. Strategic collaborations with converters, brand owners, and government agencies enable tailored product development and regulatory alignment. Expansion of circular polymer portfolios—using mechanical and advanced recycling—is a growing priority to meet environmental mandates. Firms are also enhancing regional production and technical support capabilities to reduce lead times and improve customer responsiveness. Additionally, participation in industry coalitions and standardization bodies helps shape policy and accelerate adoption of next-generation HDPE grades in infrastructure and consumer sectors.

MARKET SEGMENTATION

This research report on the global high-density polyethylene market has been segmented and sub-segmented based on application, resin grade, end-user industry, and region.

By Application

- Pipes and Tubes

- Sheets and Films

- Rigid Articles

- Other Applications

By Resin Grade

- PE-80

- PE-100

- PE-100-RC

- More

By End-User Industry

- Packaging

- Building and Construction

- Agriculture

- Transportation

- Electrical and Electronics

- More

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is HDPE?

High-Density Polyethylene (HDPE) is a thermoplastic polymer made from petroleum, known for its strength, durability, and chemical resistance.

2. What are the major applications of HDPE?

HDPE is widely used in pipes and tubes, sheets and films, rigid articles, packaging, construction materials, and agricultural products.

3. Which industries are the primary end-users of HDPE?

Key industries include packaging, building & construction, agriculture, transportation, and electrical & electronics.

4. What factors are driving the growth of the HDPE market?

Growth is driven by rising demand in packaging, infrastructure development, increasing use in pipes, and sustainability initiatives.

5. Which region dominates the global HDPE market?

Asia-Pacific leads the market due to rapid industrialization, urbanization, and large-scale manufacturing in countries like China and India.

6. What role does HDPE play in sustainable packaging?

HDPE is recyclable, lightweight, and durable, making it an eco-friendly option for bottles, containers, and other packaging solutions.

7. Who are the major players in the HDPE market?

Key players include ExxonMobil Corporation, LyondellBasell Industries, SABIC, Dow, Reliance Industries Limited, and INEOS.

8. What challenges does the HDPE market face?

Challenges include fluctuating crude oil prices, environmental concerns about plastic waste, and competition from alternative materials.

9. What opportunities exist in the HDPE market?

Opportunities lie in bio-based HDPE, demand for lightweight automotive components, and government initiatives for water infrastructure projects.

10. What is the future outlook of the HDPE market?

The market is expected to grow steadily due to rising demand in packaging, construction, and sustainable materials across global industries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com