Global Hot Water Bottle Market Size, Share, Trends, & Growth Forecast Report By Type (Chargeable and Non-chargeable), Application (Home Use and Medical Usage) and Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa) – Industry Analysis (2026 to 2034)

Global Hot Water Bottle Market Executive Summary

Market Size & Growth

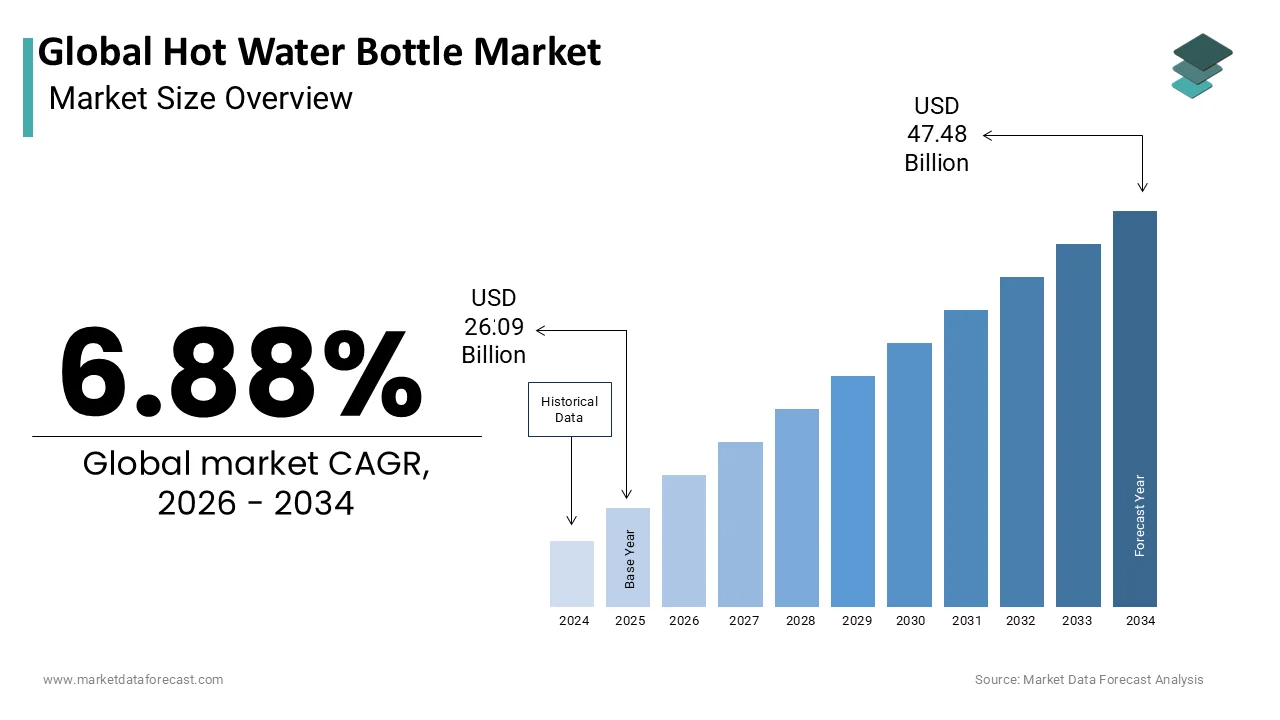

- The global hot water bottle market was valued at USD 26.09 billion in 2025.

- The market was valued at USD 27.88 billion in 2026 and is expected to reach USD 47.48 billion by 2034, growing at a CAGR of 6.88% from 2026 to 2034.

- Europe led the market with 29.7% of global share in 2025.

- The chargeable segment is the fastest-growing type, projected at a CAGR of 7.4% from 2026 to 2034.

- The medical application segment is projected to grow at a CAGR of 8.5% from 2026 to 2034.

Key Market Segments

- By Type: Chargeable, Non-chargeable (non-chargeable holds over 85% of heat therapy product sales)

- By Application: Home (dominant segment), Medical (fastest-growing segment)

- By Region: Europe leads; Asia Pacific is the fastest-growing region

Key Drivers

- Musculoskeletal conditions affect approximately 1.71 billion people globally (WHO), driving consistent demand for non-pharmacological pain relief solutions such as heat therapy.

- Household electricity prices in Europe increased by 14% and gas prices by 21% in 2024 (IEA), accelerating the adoption of energy-efficient personal heating alternatives.

- Chronic pain affects approximately 20.9% of American adults (CDC), sustaining demand for accessible, drug-free therapeutic tools, including heat therapy devices.

Key Players

KSK GmbH (Germany), Narang Medical Limited (India), Hicks Thermometers India Ltd. (India), Sun Labtek Equipment (I) Pvt. Ltd. (India), Sanger GmbH (Germany), Fashy GmbH, Reliance Brands Limited, Kaz Europe Sarl.

Global Hot Water Bottle Market Size

The global hot water bottle market was valued at USD 26.09 billion in 2025, is expected to have a 6.88% CAGR from 2026 to 2034, and be worth USD 47.48 billion by 2034 from USD 27.88 billion in 2026.

Hot water bottles are portable containers designed to hold heated water for therapeutic warmth and comfort. These products typically consist of rubber or thermoplastic bladders encased in decorative fabric covers, serving as a non-electric alternative for pain relief and thermal regulation. The market is deeply rooted in traditional home care practices, particularly in regions with cold climates where central heating may be insufficient or costly. As per the World Health Organization (WHO), musculoskeletal conditions affect approximately 1.71 billion people globally, driving consistent demand for non-pharmacological pain management solutions such as heat therapy. The aging population further amplifies this need, with Eurostat data indicating that 21.1% of the European Union population was aged 65 or older in 2024, a demographic prone to chronic joint pain and circulation issues. Additionally, rising energy costs have prompted consumers to seek localized heating methods to reduce reliance on whole-house heating systems. According to the International Energy Agency (IEA), household electricity prices in Europe increased by an average of 14% and gas prices by 21% in 2024, encouraging the adoption of energy-efficient personal warming devices. Manufacturers are responding with innovations in sustainable materials and ergonomic designs to meet evolving consumer preferences. Safety standards remain a critical focus, with regulatory bodies enforcing strict testing protocols to prevent leaks and burns. This combination of health benefits, economic incentives, and technological refinement sustains the relevance of hot water bottles in modern wellness routines.

MARKET DRIVERS

Rising Prevalence of Chronic Pain Conditions Drives Therapeutic Demand

The increasing global burden of chronic pain conditions is fuelling the growth of the global hot water bottles market. Musculoskeletal disorders, arthritis, and menstrual cramps are among the most common ailments alleviated by heat therapy, which improves blood flow and relaxes tense muscles. According to the Global Burden of Disease Study, lower back pain remains the leading cause of disability worldwide, affecting over 619 million individuals globally. This widespread prevalence creates a vast target audience for non-invasive therapeutic devices. Hot water bottles offer a drug-free alternative that avoids the side effects associated with long-term medication use, appealing to health-conscious consumers and those managing multiple comorbidities. Medical professionals frequently recommend heat therapy as part of multimodal pain management strategies, lending clinical credibility to the product. The simplicity of use allows elderly individuals and those with limited mobility to manage discomfort independently at home. Furthermore, the growing awareness of self-care practices has normalized the regular use of heat therapy for minor aches and stresses. Retail pharmacies and online health stores prominently feature hot water bottles alongside other wellness products, enhancing visibility and accessibility. The low cost of entry compared to electronic heating pads makes them an attractive option for budget-constrained patients seeking immediate relief. This enduring medical necessity ensures stable demand regardless of broader economic fluctuations.

Surging Energy Costs Promote Adoption of Localized Heating Solutions

Escalating household energy expenses have significantly influenced consumer behavior, which is driving a shift toward cost-effective and energy-efficient personal heating methods, such as hot water bottles,s and further boosting the global market expansion. As global energy markets face volatility due to geopolitical tensions and supply chain disruptions, families are actively seeking ways to reduce their carbon footprint and utility bills. According to the IEA, residential energy prices in many developed nations rose significantly during the recent energy crisis, with some European countries seeing retail electricity prices surge by over 20%, which is prompting a re-evaluation of heating habits. Using a hot water bottle requires minimal energy, typically just the cost of boiling a kettle, whereas maintaining ambient room temperature through central heating consumes substantially more resources. This economic incentive is particularly strong in older housing stocks with poor insulation, common in parts of Europe and North America, where retaining heat is challenging. Consumers perceive hot water bottles as a practical supplement to lower thermostat settings, allowing for comfortable warmth without excessive expenditure. Environmental consciousness also plays a role, as individuals aim to reduce their household emissions in line with climate goals. The portability of hot water bottles enables users to direct heat exactly where needed, maximizing efficiency. Retailers report increased sales during winter months correlated with energy price announcements, highlighting the product’s role as a financial coping mechanism. This trend reinforces the hot water bottle’s position not just as a health aid but as an essential tool for economical living.

MARKET RESTRAINTS

Safety Concerns and Risk of Burns Restrict Consumer Confidence

Persistent safety concerns regarding potential leaks, bursts, and scalding injuries constitute a significant restraint on the hot water bottle market, deterring some consumers from purchasing or using these products. Despite improvements in manufacturing standards, incidents involving faulty rubber degradation or improper filling continue to occur, leading to negative perceptions and liability fears. According to the United States Consumer Product Safety Commission (CPSC), thousands of emergency room visits annually are attributed to burns from hot water bottles and similar heating devices, primarily affecting children and the elderly. These statistics highlight the inherent risks associated with handling boiling water and maintaining aging rubber components. Media coverage of severe burn cases can trigger public alarm, causing temporary dips in sales and increased scrutiny from regulators. Manufacturers must invest heavily in quality control and clear labeling to mitigate these risks, which adds to production costs. Some consumers opt for electric heating pads or microwaveable wraps, ps perceived as safer alternatives, despite their higher price points and dependency on electricity. The need for regular replacement every two to three years to ensure material integrity is often overlooked by users, increasing the likelihood of failure. Regulatory bodies enforce strict testing protocols, but enforcement varies globally, creating uneven safety standards. This lingering apprehension limits market expansion among risk-averse demographics and necessitates continuous education efforts to promote safe usage practices.

Availability of Advanced Electric Alternatives Limits Market Growth

The proliferation of sophisticated electric heating devices poses a substantial competitive threat to the traditional hot water bottle market by offering convenience and consistent temperature control. Electric heating pads, wearable heat wraps, and smart thermostatic blankets provide uninterrupted warmth without the need for refilling or waiting for water to boil. As per market data, sales of personal electric heating devices have grown significantly, reflecting consumer preference for hassle-free solutions. These modern alternatives often feature adjustable heat settings, auto shut-off timers, and washable covers, addressing many of the inconveniences associated with traditional hot water bottles. The integration of technology into wellness products appeals to younger demographics accustomed to digital convenience and instant gratification. Electric devices eliminate the physical effort of carrying heavy water-filled bottles and the risk of spills, making them more attractive for use in offices or while traveling. Although they require a higher initial investment and ongoing electricity costs, the perceived value of ease and safety drives adoption. Marketing campaigns for electric alternatives emphasize their advanced features and medical-grade reliability, positioning them as superior upgrades. This competitive pressure forces hot water bottle manufacturers to innovate aggressively or risk losing market share to technologically enhanced substitutes that better align with modern lifestyles.

MARKET OPPORTUNITIES

Expansion into Eco-Friendly and Sustainable Material Innovations

The growing consumer demand for environmentally responsible products is a significant opportunity for manufacturers to innovate with sustainable materials in hot water bottle production. Traditional rubber and synthetic plastics face scrutiny due to their environmental impact and non-biodegradable nature, prompting a shift toward natural and recyclable alternatives. Companies are developing hot water bottles made from natural rubber sourced from sustainably managed plantations, as well as biodegradable thermoplastics that reduce landfill waste. For instance, a major shift in consumer sentiment reveals that over 60% of consumers now look for products with eco-friendly credentials when making purchases. Fabric covers made from organic cotton, bamboo, or recycled polyester further enhance the sustainability profile of these items. Brands that transparently communicate their supply chain ethics and carbon reduction efforts gain a competitive edge in the conscientious consumer segment. Certification from organizations like the Forest Stewardship Council (FSC) or Global Organic Textile Standard (GOTS) validates these claims and builds trust. Innovation in packaging, such as plastic-free wrapping, aligns with broader retail trends toward zero waste. This strategic pivot not only addresses environmental concerns but also opens new market niches among younger buyers who prioritize sustainability. By leading the transition to green manufacturing, companies can differentiate themselves and command premium pricing while contributing to global ecological goals.

Integration of Ergonomic Designs and Multifunctional Features

The evolution of hot water bottle designs to include ergonomic shapes and multifunctional capabilities offers a promising avenue for market expansion. Modern consumers seek versatility and comfort, driving demand for bottles that conform to body contours and serve dual purposes beyond simple heat application. Manufacturers are introducing elongated shapes for back support, contoured designs for neck relief, and smaller sizes for targeted hand or foot warming. For instance, products with enhanced usability features see 25% higher engagement rates than standard rectangular models. Some innovative designs incorporate removable covers that double as eye masks or neck pillows, adding value and convenience. The use of soft-touch materials and hypoallergenic fabrics improves user experience, particularly for individuals with sensitive skin. Customization options, such as personalized embroidery or interchangeable cover patterns, appeal to gift buyers and fashion-conscious consumers. Collaborations with healthcare providers to develop medically optimized shapes for specific conditions like sciatica or arthritis further validate product efficacy. These design enhancements transform the hot water bottle from a basic utility item into a lifestyle accessory, broadening its appeal. By focusing on user-centric innovation, manufacturers can revitalize interest in the category and attract new customer segments that previously overlooked traditional offerings.

MARKET CHALLENGES

Regulatory Compliance and Standardization Variations across Regions

Navigating the complex landscape of international safety regulations and quality standards presents a persistent challenge for hot water bottle manufacturers operating in global markets. Different countries enforce varying requirements for material composition, burst pressure testing, and labeling, complicating production and distribution processes. For instance, the European Standard EN 71 mandates rigorous testing for chemical safety and physical durability, while other regions may have less stringent or entirely different criteria. According to the International Organization for Standardization (ISO), harmonizing these diverse regulations remains an ongoing effort, leaving manufacturers to manage multiple compliance frameworks simultaneously. Failure to meet specific regional standards can result in product recalls, legal penalties, and reputational damage. Small and medium-sized enterprises (SMEs) often lack the resources to conduct extensive testing and certification for every target market, limiting their export potential. Continuous updates to safety guidelines require constant vigilance and adaptation of manufacturing processes, increasing operational costs. Counterfeit products that bypass these regulations flood online marketplaces, undermining legitimate brands and posing safety risks to consumers. Ensuring consistent quality across supply chains while adhering to disparate legal requirements demands robust quality assurance systems. This regulatory fragmentation creates barriers to entry and slows down the introduction of new products, challenging companies to balance compliance costs with competitive pricing strategies.

Supply Chain Volatility Affecting Raw Material Availability

Fluctuations in the availability and cost of raw materials such as natural rubber and synthetic polymers pose a significant challenge to the expansion of the hot water bottle market. Natural rubber prices are highly sensitive to weather conditions, disease outbreaks in plantations, and geopolitical factors in major producing countries like Thailand and Indonesia. As per the Food and Agriculture Organization (FAO) of the United Nations, global natural rubber production faced a decline of approximately 5% in recent years due to adverse weather patterns and labor shortages, leading to price spikes. Synthetic alternatives derived from petroleum are equally vulnerable to oil price volatility and supply chain disruptions. These instabilities make it difficult for manufacturers to maintain consistent pricing and profit margins. Long lead times for raw material procurement exacerbate inventory management challenges, forcing companies to hold larger stockpiles or risk production delays. The transition to sustainable materials, while desirable, often involves newer supply chains that are less established and more prone to disruption. Smaller manufacturers struggle to negotiate favorable terms with suppliers, putting them at a disadvantage compared to larger competitors. Any interruption in the flow of key inputs can halt production lines, affecting the ability to meet seasonal demand peaks. This uncertainty necessitates flexible sourcing strategies and strong supplier relationships, yet remains a critical vulnerability in the industry’s operational framework.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | Based on Type, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | KSK (Germany), Narang Medical (India), Hicks (India), Sun Labtek (India), and Sanger (Germany) |

SEGMENTAL ANALYSIS

By Type Insights

The non-chargeable segment dominated the market by holding the major share of the global market in 2025. The dominance of the non-chargeable segment in the global market is attributed to its affordability, simplicity, and widespread availability across diverse retail channels. These traditional rubber or thermoplastic bladders require no electricity or complex mechanisms, making them accessible to consumers of all income levels and particularly appealing in regions with unreliable power infrastructure. According to the CPSC, non-electric heating devices account for over 85% of all heat therapy product sales, which reflects their entrenched position in household wellness routines. The low manufacturing cost allows retailers to offer these products at competitive price points, often under ten dollars, which drives high volume sales during seasonal peaks. Consumers appreciate the immediate usability of non-chargeable bottles, which only require boiling water, eliminating the wait times associated with electric alternatives. The durability of modern natural rubber and PVC materials ensures a long product lifespan, providing excellent value for money. Furthermore, the absence of electronic components reduces the risk of mechanical failure and simplifies disposal processes. Traditional consumer habits in Europe and North America strongly favor these classic designs, which are often perceived as more reliable and safer than battery-operated counterparts. The extensive distribution network spanning pharmacies, supermarkets, and online platforms ensures constant visibility and availability. This combination of economic accessibility, operational simplicity, and cultural familiarity cements the dominance of non-chargeable hot water bottles in the global market.

On the other hand, the chargeable segment is the fastest-growing segment and is predicted to record a CAGR of 7.4% during the forecast period, owing to the increasing consumer demand for convenience and enhanced safety features. These electrically heated devices eliminate the need to boil water, reducing the risk of scalding accidents and offering consistent temperature control through built-in thermostats. As per data from major electronics retailers, sales of rechargeable personal heating devices have increased by 15% annually as consumers seek hassle-free wellness solutions. The integration of automatic shut-off mechanisms addresses primary safety concerns associated with traditional bottles, appealing to elderly users and parents of young children. Modern chargeable models feature rapid heating capabilities, reaching optimal temperatures within a minute, which aligns with the fast-paced lifestyles of urban professionals. Advancements in battery technology have improved portability and usage duration, allowing users to enjoy warmth without being tethered to power outlets. The sleek and modern design of many chargeable bottles appeals to younger demographics that prioritize aesthetics and technological integration in their home goods. Marketing campaigns emphasizing ease of use and injury prevention further accelerate adoption. Although the initial cost is higher, the perceived value of convenience and safety justifies the investment for many consumers. This shift toward smart, user-friendly heating solutions positions the chargeable segment for sustained rapid growth in the coming decade.

By Application Insights

The home segment accounted for the dominant share of the global market in 2025 due to the widespread use of these products for personal comfort, relaxation, and supplemental heating in residential settings. Consumers utilize hot water bottles to warm beds, soothe muscles after daily activities, and reduce reliance on central heating systems during colder months. According to the IEA, household energy consumption for space heating accounts for approximately 40% of total residential energy use in Europe, prompting many individuals to adopt localized heating methods to lower utility bills. The practice of using hot water bottles as a cost-effective alternative to raising thermostat settings has gained significant traction amidst rising energy prices. Additionally, the cultural tradition of using hot water bottles for comfort and sleep aid remains strong in many Western countries, ensuring consistent demand. The versatility of home use extends to leisure activities such as reading or watching television, where portable warmth enhances relaxation. Retailers capitalize on this by offering decorative covers and varied sizes that blend with home decor, transforming functional items into lifestyle accessories. The ease of storage and maintenance makes them ideal for occasional use in guest rooms or vacation homes. This broad acceptance and multifaceted utility in domestic environments sustain the leadership of the home application segment.

However, the medical segment is estimated to showcase a CAGR of 8.5% during the forecast period in the global market, owing to the increasing recognition of heat therapy as an effective non-pharmacological intervention for pain management. Healthcare providers frequently recommend hot water bottles for alleviating symptoms of arthritis, menstrual cramps, back pain, and muscle spasms, integrating them into comprehensive treatment plans. As per the WHO, musculoskeletal conditions affect over 1.71 billion people globally, creating a vast patient population seeking accessible relief options. The rise in chronic pain prevalence among aging populations further fuels demand for medical-grade hot water bottles that offer consistent and safe heat delivery. Hospitals and physiotherapy clinics utilize these devices for post-operative care and rehabilitation, valuing their simplicity and low risk profile compared to electrical heating pads. Innovations in ergonomic designs tailored for specific body parts, such as contoured neck wraps or elongated back supports, enhance therapeutic efficacy and patient compliance. Insurance coverage for durable medical equipment in some regions also supports adoption. The shift toward preventive healthcare and self-management empowers patients to incorporate heat therapy into their daily routines. Clinical studies validating the benefits of moist heat for tissue healing further reinforce professional recommendations. This growing endorsement from the medical community and the expanding base of pain sufferers drive the rapid expansion of the medical application segment.

COUNTRY LEVEL ANALYSIS

Europe Hot Water Bottle Market Analysis

Europe led the market by capturing 29.7% of the global market share in 2025 and is anticipated to experience robust growth over the next few years as consumers continue to navigate volatile energy landscapes and prioritize personal wellness solutions. Europe holds the commanding position in the global hot water bottle market due to deep-rooted cultural traditions and recent economic pressures related to energy costs. The use of hot water bottles is a longstanding habit in countries like the United Kingdom, Germany, and France, where cold winters make supplemental heating essential. According to Eurostat, household energy prices in the European Union rose substantially during the recent energy crisis, with electricity climbing 14% and gas 21% in 2024, significantly boosting demand for cost-effective warming solutions. Consumers increasingly view hot water bottles as a practical tool to reduce central heating usage, aligning with both financial savings and environmental sustainability goals. The region benefits from strict safety standards enforced by the European Committee for Standardization (CEN), which ensures high product quality and consumer trust. Major manufacturers based in Europe focus on premium designs and eco-friendly materials, catering to discerning buyers who value aesthetics and sustainability. The aging population in Europe, with over 21.1% aged 65 or older, drives consistent demand for pain relief products. Retail pharmacies and department stores maintain extensive selections, ensuring high visibility and accessibility. Government initiatives promoting energy efficiency further encourage the adoption of localized heating methods. This combination of cultural heritage, economic necessity, and regulatory support sustains Europe’s dominance in the global market.

North America Hot Water Bottle Market Analysis

The North American market is projected to expand steadily over the next few years due to an increasing consumer preference for holistic wellness and drug-free pain relief strategies. North America occupies a significant share of the global hot water bottle market, characterized by a strong focus on wellness, self-care, and non-invasive pain management. The United States and Canada have seen a resurgence of interest in natural health remedies, with hot water bottles gaining popularity among younger demographics influenced by social media trends. As per the Centers for Disease Control and Prevention (CDC), chronic pain affects approximately 20.9% of American adults, driving demand for accessible therapeutic tools. The region benefits from a robust retail infrastructure, including online platforms that offer a wide variety and convenience. Consumers in North America prefer high-quality, durable products with stylish covers that fit modern home decor aesthetics. The growing awareness of the risks associated with long-term medication use encourages individuals to explore physical therapy alternatives like heat application. Winter sports and outdoor activities in northern states create seasonal spikes in demand for muscle recovery tools. Healthcare providers increasingly recommend heat therapy as part of multimodal pain management strategies, lending clinical credibility. The presence of major manufacturing and distribution hubs ensures efficient supply chains and competitive pricing. While electric alternatives are popular, the simplicity and reliability of traditional hot water bottles maintain a loyal customer base. This blend of health consciousness and lifestyle integration supports steady market growth in the region.

Countries across the Asia-Pacific region are poised to witness exceptional market acceleration over the next few years, fueled by infrastructure developments and a massive demographic shift toward modern lifestyle accessories. The Asia-Pacific region is emerging as a dynamic growth engine in the hot water bottle market, driven by rapid urbanization, rising disposable incomes, and increasing awareness of wellness products. Countries such as China, Japan, and South Korea are experiencing growing demand for personal care items as middle-class populations expand. According to the World Bank, healthcare expenditure in East Asia has grown at a steady pace of roughly 5% to 6% annually in recent years, reflecting greater investment in preventive health and comfort. In regions with cold winters, such as Northern China and Japan, hot water bottles are becoming common household items for supplemental heating. The influence of Western wellness trends through digital media is accelerating adoption among younger urban consumers. Local manufacturers are introducing innovative designs and affordable options that cater to diverse consumer preferences. The e-commerce boom in the region facilitates easy access to a wide range of products, driving volume sales. The increasing prevalence of sedentary lifestyles and associated musculoskeletal issues further boosts demand for pain relief solutions. Government initiatives improving healthcare access and education promote self-care practices. While traditional methods like hot compresses remain popular, the convenience and safety of modern hot water bottles are gaining traction. This convergence of economic development, health awareness, and digital connectivity positions the Asia-Pacific for substantial future growth.

Latin American Hot Water Bottle Market Analysis

Latin American nations are set to exhibit progressive market improvements over the next few years as regional distribution networks expand and essential healthcare awareness increases among the general public. Latin America represents a smaller but developing segment of the hot water bottle market, as countries in the region strive to improve healthcare access and affordability. Brazil and Mexico are the primary markets driving demand, supported by growing awareness of non-pharmacological pain management options. As per the Pan American Health Organization (PAHO), chronic noncommunicable diseases account for a substantial and rising burden of illness in Latin America, creating a need for accessible therapeutic tools. Economic constraints often limit the ability of consumers to purchase expensive electric heating devices, making traditional hot water bottles an attractive low-cost alternative. Local production capabilities are expanding, reducing reliance on imports and lowering prices for end-users. Public health campaigns promoting self-care and home remedies contribute to gradual market penetration. The tropical climate in many parts of the region limits year-round demand, but cooler southern areas and high-altitude zones maintain consistent usage. Retail expansion in urban centers improves product availability and visibility. Cultural acceptance of natural remedies supports the integration of heat therapy into daily routines. While market maturity lags behind developed regions, the combination of demographic shifts and economic factors provides a foundation for steady growth. International brands are beginning to enter the market, introducing higher quality standards and diverse product ranges.

Middle East and Africa Hot Water Bottle Market Analysis

The Middle East and Africa region is expected to showcase specialized, localized growth over the next few years centered around evolving medical sectors and unique climate demands. In Gulf Cooperation Council (GCC) countries, the widespread use of air conditioning creates artificial cold environments that stimulate demand for personal warming devices. According to the WHO, ongoing structural developments to strengthen regional health systems are increasing awareness of therapeutic interventions, including heat therapy. Expatriates from Europe and North America bring familiar habits and preferences for hot water bottles, creating a specialized consumer base. In Africa, limited access to reliable electricity in rural areas makes non-electric heating solutions practical and necessary for basic comfort. Medical tourism in countries like Dubai and South Africa drives demand for high-quality wellness products in hospitals and rehabilitation centers. Local manufacturing is minimal, leading to reliance on imports from Europe and Asia. Rising health consciousness among urban populations is slowly expanding the market beyond traditional medical uses. However, high temperatures in many regions limit general household demand. Government investments in healthcare and improving living standards provide opportunities for gradual market expansion. International distributors are focusing on premium segments and medical supplies to establish a foothold. While currently small, the market shows potential for growth as healthcare access and economic conditions improve.

COMPETITIVE LANDSCAPE

The competitive landscape of the hot water bottle market features a mix of established manufacturers and emerging brands vying for consumer attention through quality innovation and price competitiveness. Major players differentiate themselves by emphasizing superior safety standards, durable materials, and aesthetically pleasing designs that appeal to modern home decor trends. Private label products from large retail chains exert pressure on branded manufacturers by offering lower-priced alternatives with comparable functionality. Innovation in eco-friendly materials serves as a key battleground where companies strive to meet growing environmental concerns and regulatory demands. Brand reputation built on reliability and trust plays a crucial role in retaining customers who prioritize safety over cost. Online retailers facilitate direct-to-consumer sales, allowing niche brands to reach specific demographics with specialized products. Seasonal demand fluctuations require efficient inventory management and agile supply chains to capitalize on winter peaks. Collaborations with health influencers and medical professionals enhance credibility and drive adoption among new user segments. This dynamic environment encourages continuous improvement in product quality and customer service to maintain market relevance.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Global Hot Water Bottle Market include

- KSK GmbH (Germany)

- Narang Medical Limited (India)

- Hicks Thermometers India Ltd. (India)

- Sun Labtek Equipment (I) Pvt. Ltd. (India)

- Sänger GmbH (Germany)

TOP LEADING PLAYERS IN THE MARKET

- Fashy GmbH stands as a premier manufacturer of high-quality hot water bottles, renowned for its commitment to safety and durability. The company utilizes advanced injection molding technology to produce seamless thermoplastic bottles that resist leaks and maintain heat efficiently. Recent initiatives include expanding its range of eco-friendly covers made from organic cotton and recycled materials to appeal to environmentally conscious consumers. Fashy actively collaborates with healthcare professionals to validate the therapeutic benefits of its products for pain management. Their rigorous testing protocols exceed international safety standards, ensuring consumer trust. By focusing on premium design and functional innovation,n Fashy strengthens its reputation as a leader in the global market while addressing the growing demand for sustainable and reliable home wellness solutions.

- Reliance Brands Limited operates as a significant player in the hot water bottle sector,r leveraging its extensive distribution network across Asia and emerging markets. The company focuses on producing affordable and accessible heating solutions that cater to diverse consumer segments,s including rural and urban populations. Recent actions include launching ergonomic designs tailored for specific body parts, such as necks and backs, to enhance therapeutic effectiveness. Reliance invests in modernizing manufacturing facilities to improve production efficiency and product consistency. Strategic partnerships with local retailers ensure wide availability during peak winter seasons. By prioritizing cost-effectiveness and functional versatility, Reliance Brands strengthens its market position and meets the essential warmth needs of millions of households while adapting to regional climate variations and economic conditions.

- Kaz Europe Sàrl contributes significantly to the global market through its portfolio of well-known brands that integrate traditional heating methods with modern safety features. The company emphasizes user-friendly designs, including easy fill funnels and secure stoppers to prevent accidents. Recent developments involve introducing smart temperature indicators that alert users when the water is at an optimal heat level. Kaz Europe expands its retail presence through online platforms and major pharmacy chains,s offering convenient access to consumers. They prioritize customer education on safe usage practices through detailed packaging and digital content. By combining trusted brand heritage with innovative safety enhancements, Kaz Europe strengthens its competitive edge and reinforces consumer confidence in using hot water bottles for daily comfort and pain relief.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the hot water bottle market primarily focus on product differentiation through innovative designs and enhanced safety features to attract health-conscious consumers. Companies invest in developing eco-friendly materials such as natural rubber and organic fabrics to align with sustainability trends and regulatory requirements. Strategic partnerships with healthcare providers help validate therapeutic claims and build credibility among medical professionals. Expanding distribution channels via e-commerce platforms ensures a broader reach and convenience for buyers seeking immediate relief. Marketing campaigns emphasize the cost-effectiveness and energy-saving benefits of hot water bottles compared to electric alternatives. Continuous improvement in manufacturing processes reduces defects and enhances durability, fostering long-term customer loyalty. Educational initiatives promote safe usage practices to mitigate injury risks and maintain positive brand perception in a competitive wellness landscape.

MARKET SEGMENTATION

This research report on the global hot water bottle market has been segmented and sub-segmented based on type, application, and region.

By Type

- Chargeable

- Non-chargeable.

By Application

- Home

- Medical

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the projected CAGR of the hot water bottle market during the forecast period 2023-2028?

The market is projected to grow at a 1.81 % CAGR during the forecast period.

What is the expected value of the market shares by 2028?

The hot water bottle market shares are expected to reach USD 225 million by the end of 2028.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com