Global Immunoprecipitation Market Size, Share, Trends & Growth Forecast Report – Segmented By Product (Kits, Reagents (Antibodies, Beads and Others), Type (Individual Protein, Protein Complex, Chromatin, Ribonucleoprotein and Tagged Proteins), End-User & Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) – Industry Analysis From 2025 to 2033

Global Immunoprecipitation Market Report Summary

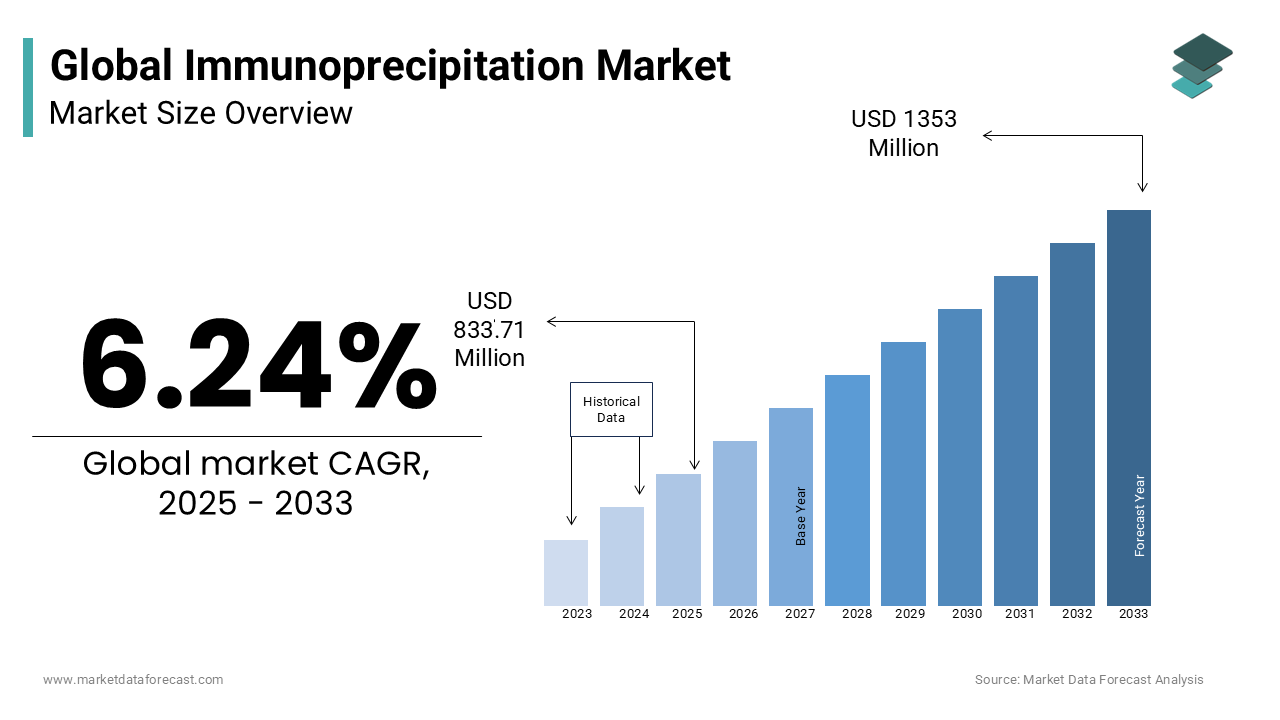

The global immunoprecipitation market was valued at USD 784.74 million in 2024, is estimated to reach USD 833.71 million in 2025, and is projected to reach USD 1353.07 million by 2033, growing at a CAGR of 6.24% during the forecast period from 2025 to 2033. The growth of the global immunoprecipitation market is driven by rising demand for proteomics research, expanding applications in biomarker discovery and personalized medicine, and rapid technological advancements in automation and high-throughput platforms. Increasing adoption of magnetic bead–based immunoprecipitation kits, AI-assisted workflow optimization, and multiplexing capabilities is further accelerating market expansion. Moreover, growing investments in precision diagnostics, increasing cancer and neurodegenerative disease research, and strengthening collaborations between pharmaceutical companies and academic institutions continue to broaden the global user base for immunoprecipitation tools.

Key Market Trends

- Rising demand for protein interaction, modification, and complex analysis in proteomics and precision medicine.

- Growing adoption of automated and high-throughput immunoprecipitation systems to improve speed, accuracy, and scalability.

- Increased emphasis on low-abundance protein detection supported by advanced magnetic bead–based platforms.

- Expansion of immunoprecipitation applications in oncology, epigenetics, and biomarker validation.

- Strengthening collaborations between pharmaceutical companies, academic institutes, and biotech firms to enhance reproducibility and protocol standardization.

Segmental Insights

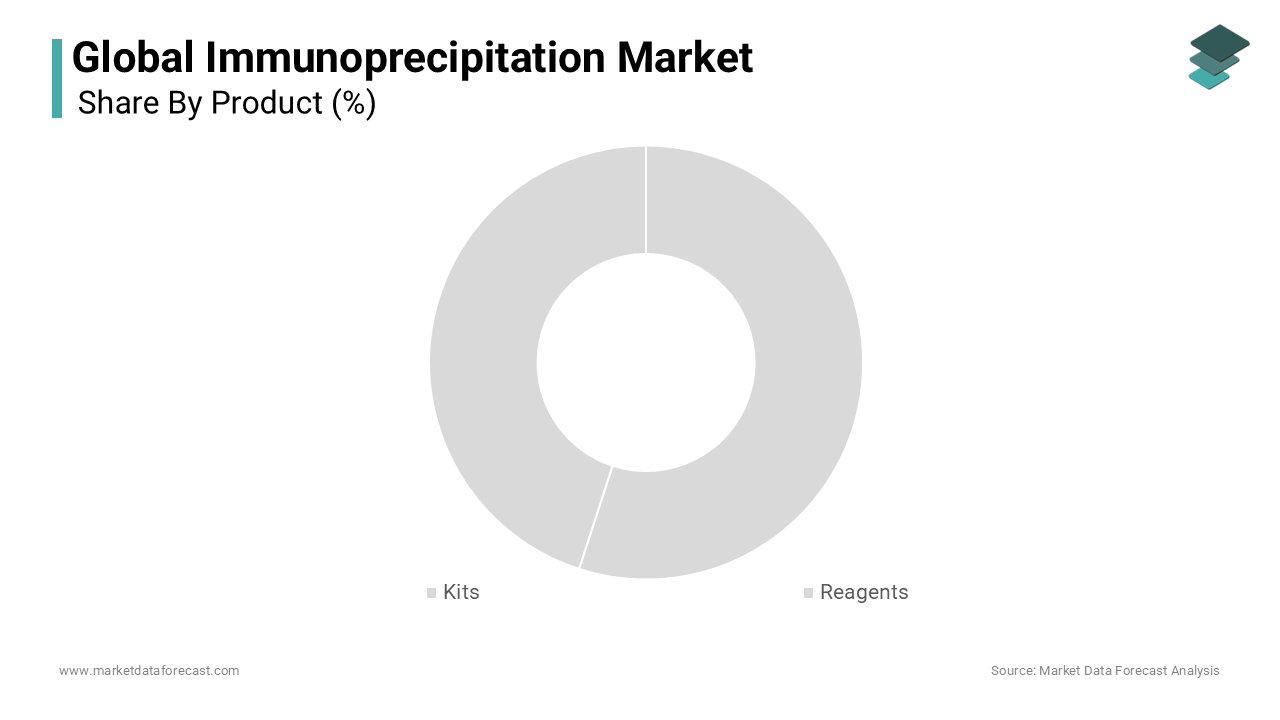

- Based on product,the kits segment was the largest and held 59.8% of the global immunoprecipitation market share in 2024, driven by convenience, pre-optimized protocols, and high reproducibility, making them ideal for both beginner and advanced research settings. The shift toward automation and magnetic bead–based kits further reinforces segment dominance.

- Based on type, the individual protein immunoprecipitation segment held the largest share (45.3%) in 2024, owing to its widespread use in biomarker discovery, drug development, and disease diagnostics. Increasing use of high-specificity monoclonal antibodies continues to strengthen segment leadership.

- Based on end user, Academic and research institutes dominated the market with 50.4% share in 2024, supported by their essential role in proteomics, biomarker discovery, and disease mechanism studies, along with strong government and institutional funding.

Regional Insights

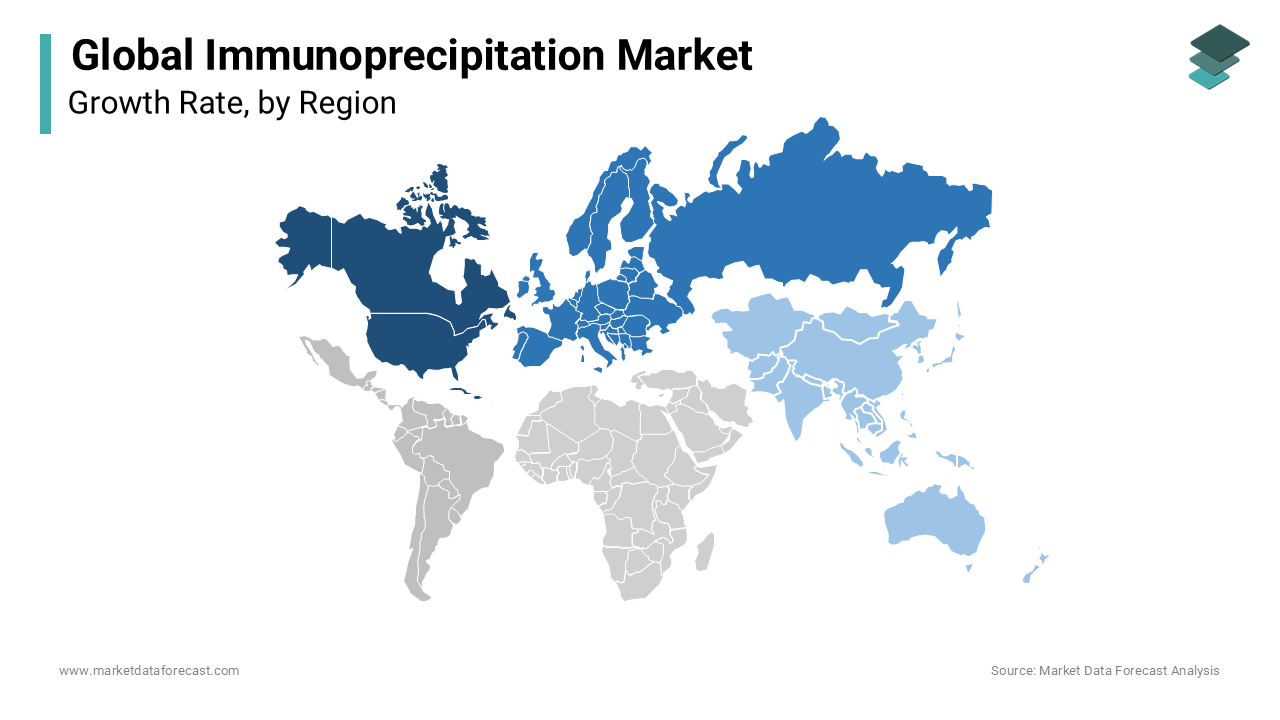

The global immunoprecipitation market demonstrates strong regional performance driven by research funding, biotechnology innovation, and expanding diagnostic applications.

- North America was the largest contributor with 40.5% share in 2024, supported by advanced research infrastructure, substantial NIH funding, and high adoption of cutting-edge proteomics technologies.

- Europe accounted for 25.4% of the global market, with Germany, the UK, and France leading adoption driven by precision medicine initiatives, stringent quality standards, and rising automation in research labs.

- Asia-Pacific is expected to witness the fastest growth, propelled by expanding biotech investment, government-sponsored programs in India and China, and increasing emphasis on personalized medicine.

- Latin America shows steady expansion, supported by improving healthcare infrastructure, scientific collaborations, and localized manufacturing initiatives.

- Middle East & Africa is emerging with growing adoption in Egypt, South Africa, and GCC nations driven by modernization of research capabilities and chronic disease monitoring initiatives.

Competitive Landscape

The global immunoprecipitation market is characterized by strong competition among established biotechnology leaders and innovative emerging companies. Market players focus on developing advanced magnetic bead–based kits, automation-ready platforms, and high-specificity reagents to address accuracy and reproducibility challenges. Strategic collaborations, acquisitions, and geographic expansion are key competitive themes as companies aim to strengthen distribution networks and enhance product portfolios. Sustainability initiatives and cost-reduction strategies are also shaping market dynamics. Prominent companies in the global immunoprecipitation market include Merck KGaA, Thermo Fisher Scientific, Abcam, Bio-Rad Laboratories, Cell Signaling Technology, BioLegend, Takara Bio, GenScript Biotech, Rockland Immunochemicals, Abbkine Scientific, and Geno Technology.

Global Immunoprecipitation Market Size

The global immunoprecipitation market size was valued at USD 784.74 million in 2024. The size of the market is predicted to grow at a CAGR of 6.24% from 2025 to 2033 and be worth USD 1353.07 million by 2033 from USD 833.71 million in 2025.

MARKET DRIVERS

Rising Demand for Proteomics Research

One of the primary drivers of the immunoprecipitation market is the escalating demand for proteomics research, which seeks to understand protein interactions, functions, and modifications. Proteomics studies are essential for identifying biomarkers, understanding disease mechanisms, and developing targeted therapies. For example, a study published in Nature Biotechnology revealed that immunoprecipitation-based assays achieve a 95% success rate in isolating low-abundance proteins by making them indispensable for cancer and neurodegenerative disease research. Additionally, the rise of personalized medicine has increased the need for precise protein analysis tools, which is driving adoption in academic and industrial labs.

Advancements in Automation and High-Throughput Technologies

Advancements in automation and high-throughput technologies represent another key driver propelling the immunoprecipitation market forward. For instance, robotic platforms reduce manual errors by 30%, which is appealing to large-scale research facilities. Emerging trends in multiplexing further accelerate adoption. For example, magnetic bead-based immunoprecipitation kits allow simultaneous analysis of multiple proteins by reducing processing times by 40%. Similarly, collaborations between biotech firms and AI developers optimize workflows by addressing scalability challenges effectively. These innovations position automation as a transformative force in the immunoprecipitation market.

MARKET RESTRAINTS

High Costs of Advanced Kits and Reagents

A significant restraint facing the immunoprecipitation market is the high cost associated with advanced kits and reagents for small research labs and institutions in developing regions. According to the World Bank, the average cost of a single immunoprecipitation kit exceeds $500, making it inaccessible for many researchers in low-income countries. This financial barrier limits adoption in regions where funding for scientific research is scarce. Additionally, the lack of reimbursement policies for research tools further exacerbates affordability challenges. According to a report by the International Finance Corporation, over 60% of academic labs in sub-Saharan Africa rely on outdated techniques due to budget constraints.

Technical Challenges in Protein Isolation

Technical challenges in protein isolation pose another major restraint, which is impacting both accuracy and reproducibility in immunoprecipitation experiments. According to a study published in the Proteomics Journal, over 30% of immunoprecipitation assays fail due to nonspecific binding or low target protein recovery, which leads to wasted resources and unreliable data. While advanced kits improve outcomes, their complexity creates a steep learning curve for new users. For instance, a survey conducted by the American Society for Biochemistry and Molecular Biology reveals that only 40% of researchers feel confident in optimizing immunoprecipitation protocols by leaving others dependent on external expertise. Additionally, improper storage conditions can degrade antibodies, further complicating results.

MARKET OPPORTUNITIES

Expansion into Personalized Medicine

One promising opportunity lies in expanding immunoprecipitation applications into personalized medicine, where tailored therapies rely on precise protein analysis. Synergies with immunoprecipitation tools are designed for biomarker discovery and validation. Techniques like chromatin immunoprecipitation (ChIP) enable researchers to identify genetic and epigenetic markers, which are enhancing treatment efficacy. For example, partnerships between pharmaceutical companies and research institutions enhance accessibility for oncology applications.

Growth in Emerging Markets

Another lucrative opportunity exists in supporting emerging markets, where rising investments in life sciences and healthcare infrastructure create immense demand for immunoprecipitation tools. According to the Asian Development Bank, Asia-Pacific accounts for over 35% of global biotech funding, with India and China leading adoption. Government initiatives like India’s Biotechnology Industry Research Assistance Council (BIRAC) promote innovation by fostering growth. For instance, collaborations with international organizations ensure mass production of affordable kits, particularly for low-income regions. Additionally, advancements in portable systems appeal to field researchers, fostering inclusivity. These trends position emerging markets as a transformative growth driver within the immunoprecipitation market.

MARKET CHALLENGES

Regulatory Hurdles and Compliance Issues

The regulatory hurdles and compliance issues represent a significant challenge for small-scale manufacturers entering the immunoprecipitation market. According to the Food and Drug Administration (FDA), stringent regulations mandate extensive validation and quality assurance processes, which are delaying approvals by up to 3 years. For example, antibody-based kits must meet ISO standards, requiring substantial R&D investments. This complexity increases operational costs and limits market entry for startups. According to a report by Deloitte, over 70% of new entrants struggle to navigate regulatory frameworks, which is hindering innovation. Additionally, varying requirements across regions create logistical barriers, affecting global distribution.

Environmental Impact of Disposal Practices

The environmental impact of disposal practices poses another major challenge as plastic waste from laboratory consumables continues to rise. According to the World Health Organization (WHO), over 12 billion lab consumables are improperly discarded annually, contributing to pollution and health hazards. Improper disposal of immunoprecipitation kits not only harms ecosystems but also exposes communities to contamination risks. For example, a study in Environmental Pollution reveals that plastic tubes and pipette tips take hundreds of years to degrade, which is exacerbating landfill burdens. Additionally, recycling initiatives face resistance due to contamination risks and a lack of standardized protocols. These challenges hinder efforts to balance market growth with environmental responsibility without sustainable alternatives or robust waste management systems.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product, Type, End-User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape. Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key Market Players | Merck KGaA, Thermo Fisher Scientific, Abcam, Bio-Rad Laboratories, Abbkine Scientific Co. Ltd., Cell Signaling Technology, Rockland Immunochemicals, BioLegend, Takara Bio, GenScript Biotech Corporation, and Geno Technology |

SEGMENTAL ANALYSIS

By Product Insights

The kits segment was the largest and held 59.8% of the immunoprecipitation market share in 2024, with their convenience, pre-optimized protocols, and ability to deliver consistent results, which makes them ideal for both novice and experienced researchers. According to a survey conducted by the American Society for Biochemistry and Molecular Biology, over 75% of academic labs prefer ready-to-use kits for protein isolation due to their time-saving benefits.

A key factor propelling this dominance is the growing trend toward automation and high-throughput research. For instance, magnetic bead-based kits reduce processing times by 40% by appealing to large-scale proteomics studies. Additionally, collaborations between manufacturers and research institutions ensure robust validation, addressing reproducibility challenges effectively. These dynamics ensure that kits remain the preferred choice for diverse applications globally.

The reagents are likely to register a CAGR of 9.8% in the coming years. This growth is fueled by increasing demand for customizable solutions tailored to specific research needs. According to a study published in the Proteomics Journal, reagents achieve a 95% success rate in isolating low-abundance proteins by making them indispensable for niche applications like epigenetic studies. Emerging trends in multiplexing further accelerate adoption. For example, partnerships between biotech firms and AI developers optimize reagent formulations by enhancing specificity and sensitivity. Additionally, localized manufacturing reduces costs by 20%, which is fostering affordability in emerging markets.

By Type Insights

The individual protein immunoprecipitation segment was the largest by occupying 45.3% of the immunoprecipitation market share in 2024, owing to its widespread use in biomarker discovery, drug development, and disease diagnostics. According to the National Institutes of Health (NIH), over $10 billion is invested annually in studies targeting individual proteins with a critical need for precise isolation tools. A major factor propelling this dominance is advancements in antibody engineering. For instance, monoclonal antibodies achieve a 90% success rate in targeting specific proteins by reducing nonspecific binding. Additionally, collaborations between pharmaceutical companies and research labs enhance accessibility by addressing scalability challenges effectively.

The chromatin immunoprecipitation (ChIP) segment is likely to register a CAGR of 11.3% in the coming years. This growth is fueled by rising demand for epigenetic studies in cancer and neurodegenerative disease research. A study published in Nature Genetics reveals that ChIP assays identify genetic and epigenetic markers with 95% accuracy by appealing to precision medicine initiatives. Emerging trends in automation further accelerate adoption. For example, robotic platforms reduce manual errors by 30% by enhancing reproducibility. Additionally, government funding for epigenetic research fosters innovation, addressing unmet needs effectively. These innovations position chromatin immunoprecipitation as a transformative force in the immunoprecipitation market.

By End-User Insights

The academic and research institutes segment dominated the immunoprecipitation market by capturing 50.4% of the total share in 2024, which is driven by their central role in advancing proteomics research, biomarker discovery, and disease diagnostics. A key factor propelling this dominance is the rise of collaborative research initiatives. For instance, partnerships between universities and biotech firms enhance accessibility for large-scale studies. Additionally, government grants ensure steady funding, addressing logistical challenges effectively. These dynamics ensure that academic and research institutes remain the primary users of immunoprecipitation technologies globally.

The contract Research Organizations (CROs) segment is projected to register a CAGR of 10.5% throughout the forecast period. This growth is fueled by increasing outsourcing trends among pharmaceutical and biotechnology companies seeking cost-effective solutions. Emerging trends in personalized medicine further accelerate adoption. For example, collaborations between CROs and AI developers optimize workflows by enhancing efficiency and reproducibility. Additionally, regulatory support fosters innovation by addressing unmet needs effectively.

REGIONAL ANALYSIS

North America was the top performer in the global immunoprecipitation market by holding 40.5% of the share in 2024. The region’s dominance is driven by its advanced R&D infrastructure and high adoption of cutting-edge biotechnological tools. According to the National Institutes of Health (NIH), over $45 billion is invested annually in proteomics research in the U.S. by creating immense demand for immunoprecipitation solutions. A key factor propelling this dominance is the presence of leading pharmaceutical companies and academic institutions. For instance, collaborations between Harvard University and biotech firms enhance accessibility for large-scale studies. Additionally, government grants ensure steady funding by addressing logistical challenges effectively.

Europe was positioned second by holding 25.4% of the global immunoprecipitation market share in 2024, with Germany, the UK, and France emerging as key contributors. According to Eurostat, Europe’s aging population and rising prevalence of chronic diseases drive demand for protein analysis tools. The European Medicines Agency (EMA) mandates rigorous validation processes to ensure safety and efficacy. A major driver is the integration of automation technologies. For example, robotic platforms reduce manual errors by 30%, which is appealing to large-scale research facilities. Additionally, government initiatives promoting precision medicine are likely to fuel the growth of the market.

Asia-Pacific immunoprecipitation market is likely to have the fastest growth opportunities in the coming years. India and China lead adoption by rising investments in life sciences and growing awareness about personalized medicine. Technological advancements further boost growth. For instance, partnerships between multinational pharma companies and local healthcare providers enhance affordability and distribution. Additionally, government initiatives like India’s Biotechnology Industry Research Assistance Council (BIRAC) improve awareness and access to care.

Latin American immunoprecipitation market is expected to grow in the coming years, with Brazil and Mexico as primary contributors. The rising investments in healthcare infrastructure and increasing focus on disease diagnostics drive adoption. Government programs promoting scientific research address logistical challenges effectively. Key drivers include collaborations with international organizations and localized manufacturing. For example, partnerships with global firms ensure mass production of affordable kits for low-income regions.

The Middle East and Africa are deemed to have steady growth in the global immunoprecipitation market. Egypt performs over 500,000 proteomics studies annually through government initiatives to modernize healthcare. Meanwhile, South Africa’s focus on precision medicine addresses unmet needs effectively.

A major driver is the rise of public health campaigns targeting chronic diseases. For example, awareness programs reduce diagnostic delays by 15% in targeted regions. Additionally, collaborations with international organizations enhance local expertise by ensuring compliance with quality standards.

COMPETITIVE LANDSCAPE

The immunoprecipitation market is highly competitive, with established giants and emerging players vying for dominance. Companies like Thermo Fisher Scientific, Merck KGaA, and Abcam plc leverage their expertise in manufacturing, R&D, and distribution to differentiate themselves. Consolidation through mergers and acquisitions is common, enabling firms to expand geographically and diversify product portfolios. For instance, Thermo Fisher’s acquisition of a biotech startup strengthened its pipeline for advanced immunoprecipitation tools.

Meanwhile, startups disrupt traditional dynamics by introducing innovative materials and automated systems, appealing to health-conscious consumers. Regional players also pose a threat, capitalizing on localized expertise to challenge global leaders. This competitive landscape drives continuous innovation, benefiting end-users through improved product quality, affordability, and sustainability.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global immunoprecipitation market include

- Merck KGaA

- Thermo Fisher Scientific

- Abcam

- Bio-Rad Laboratories

- Abbkine Scientific Co., Ltd.

- Cell Signaling Technology

- Rockland Immunochemicals

- BioLegend

- Takara Bio

- GenScript Biotech Corporation

- Geno Technology

Top Players in the Immunoprecipitation Market

Thermo Fisher Scientific

Thermo Fisher Scientific is a global leader in the immunoprecipitation market, known for its innovative solutions tailored to diverse research needs. The company specializes in magnetic bead-based kits and reagents, serving over 50 countries. Thermo Fisher prioritizes R&D, investing heavily in advanced technologies like automation and high-throughput systems. Its commitment to quality ensures consistent sterility and precision by making it a trusted partner for researchers worldwide.

Merck KGaA

Merck KGaA excels in developing high-quality immunoprecipitation tools, including individual protein and chromatin assays. The company offers a wide range of products, addressing diverse customer preferences. Merck collaborates with academic institutions globally to develop customized solutions, enhancing reproducibility and accuracy. Its focus on ergonomic designs positions it as a key innovator in the immunoprecipitation market.

Abcam plc

Abcam plc is a pioneer in antibody-based immunoprecipitation tools, known for its high-specificity reagents and kits. The company supplies products for both academic and industrial applications, catering to diverse markets globally. Abcam invests heavily in training programs, equipping researchers with hands-on expertise. With a strong emphasis on accessibility, Abcam continues to expand its footprint in emerging economies by ensuring broader adoption.

Top Strategies Used by Key Market Participants

Product Innovation

Key players prioritize product innovation to stay ahead in the competitive immunoprecipitation market. For example, Thermo Fisher Scientific introduced magnetic bead-based kits that achieve a 95% success rate in isolating low-abundance proteins, appealing to researchers seeking reliable solutions. These innovations not only enhance reproducibility but also address unmet needs effectively by fostering customer loyalty and market growth.

Strategic Partnerships

Strategic partnerships are another major strategy used by industry leaders to enhance scalability. In April 2024, Merck KGaA partnered with AI firms to optimize workflows for high-throughput assays, improving efficiency by 25%. Such collaborations streamline operations and foster knowledge sharing by addressing regional challenges while expanding market reach.

Geographic Expansion

Expanding into emerging markets strengthens market presence and operational efficiency. In June 2024, Abcam plc launched new distribution centers in sub-Saharan Africa, targeting underserved populations.

RECENT HAPPENINGS IN THIS MARKET

- In 2019, Merck announced plans to open a new life science center to focus on immunology, cancer, and immuno-oncology.

- In 2018, Thermo Fisher Scientific built a new bioprocess design center in Shanghai to interact with biologic developers and collaborate on developing efficient bioprocessing solutions.

- In 2019, Merck & Co. Inc. opened a new life science facility focusing on research and development activities in oncology, immunology, and immuno-oncology.

- Genscript USA, Inc. acquired FDA Emergency Use Authorization for its cPass SARS-CoV-2 Neutralizing Antibody Detection Kit in November 2020.

- In Bio-Protocol, 2020, chromatin immunoprecipitation was utilized in conjunction with quantitative PCR (Chip-qPCR) to identify DNA-binding protein binding sites and detect histone modification in locus-specific regions of the genome.

RECENT MARKET DEVELOPMENTS

- In April 2024, Thermo Fisher Scientific acquired a biotech startup specializing in magnetic bead technologies. This move expanded its product portfolio and promoted its dominant advanced immunoprecipitation solutions.

- In June 2024, Merck KGaA launched a new line of automated kits designed for high-throughput proteomics studies. This initiative diversified its offerings and addressed shifting consumer preferences.

- In August 2024, Abcam plc partnered with a telemedicine provider to enhance accessibility for researchers in remote regions. This collaboration reduced costs by 20% by aligning with affordability goals.

- In October 2024, Thermo Fisher announced a $1 billion investment in long-term clinical trials for immunoprecipitation tools, improving safety and efficacy data. This reinforced its commitment to innovation.

- In December 2024, Merck KGaA signed a distribution agreement with Amazon, enabling direct-to-consumer sales of its immunoprecipitation products. This partnership expanded accessibility and tapped into the booming e-commerce segment.

MARKET SEGMENTATION

This research report on the global immunoprecipitation market has been segmented and sub-segmented based on product, type, end-user, and region.

By Product

- Kits

- Reagents

- Antibodies

- Beads

- Others

By Type

- Individual protein

- Protein complex

- Chromatin

- Ribonucleoprotein

- Tagged proteins

By End-User

- Academic & Research Institutes

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the Global Immunoprecipitation Market?

The Global Immunoprecipitation Market focuses on techniques that use antibodies to isolate specific antigens from biological samples. It is widely used in protein interaction studies, epigenetics, and disease research.

What drives the growth of the immunoprecipitation market?

Growing demand for targeted protein analysis, increased adoption of personalized medicine, and advancements in antibody technology are major drivers

What are the main types of immunoprecipitation techniques?

The key types include chromatin immunoprecipitation (ChIP), co-immunoprecipitation (Co-IP), RNA immunoprecipitation (RIP), and traditional IP. Each method serves a unique purpose in studying protein interactions and gene regulation.

Which regions dominate the global market?

North America leads due to strong research infrastructure and high R&D spending. Europe and Asia-Pacific are rapidly growing because of increased investment in genomics and proteomics.

Who are the key end users?

Major end users include academic research institutions, pharmaceutical companies, biotechnology firms, and CROs. These organizations use immunoprecipitation in drug discovery and mechanistic studies.

What industries commonly use immunoprecipitation?

It is widely used in life sciences research, oncology, immunology, and neurology. Its role in identifying protein pathways makes it valuable for disease diagnostics and therapeutic development.

What challenges are limiting the market?

High costs of antibodies, technical variability, and requirement for skilled personnel limit adoption. Additionally, reproducibility issues in complex assays can affect results.

What technological innovations are shaping the market?

Automation, high-throughput IP platforms, magnetic bead-based systems, and next-generation antibody engineering are transforming the workflow. Integration with mass spectrometry is also expanding research capabilities.

What are the major applications of immunoprecipitation?

Applications include studying protein interactions, mapping epigenetic modifications, analyzing RNA-binding proteins, and isolating antigens for immunological studies.

Who are the major players in the Global Immunoprecipitation Market?

Key players include Thermo Fisher Scientific, Merck KGaA, Abcam, Cell Signaling Technology, Bio-Rad Laboratories, Proteintech, Takara Bio, GenScript, and Rockland Immunochemicals. These companies offer a wide portfolio of IP kits, antibodies, and reagents.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com