Global Industrial Filtration Market Size, Share, Trends & Growth Forecast Report By Type (Air Filtration, Liquid Filtration), By Application (Food & Beverages, Power Generation, Semiconductors & Electronics, Chemicals & Petrochemicals, Pharmaceutical Manufacturing, Metals & Mining, Paper & Paints, Others), and By Region (North America, Europe, Asia-Pacific, Middle East & Africa, Latin America) – Industry Analysis, 2026 to 2034

Global Industrial Filtration Market Size

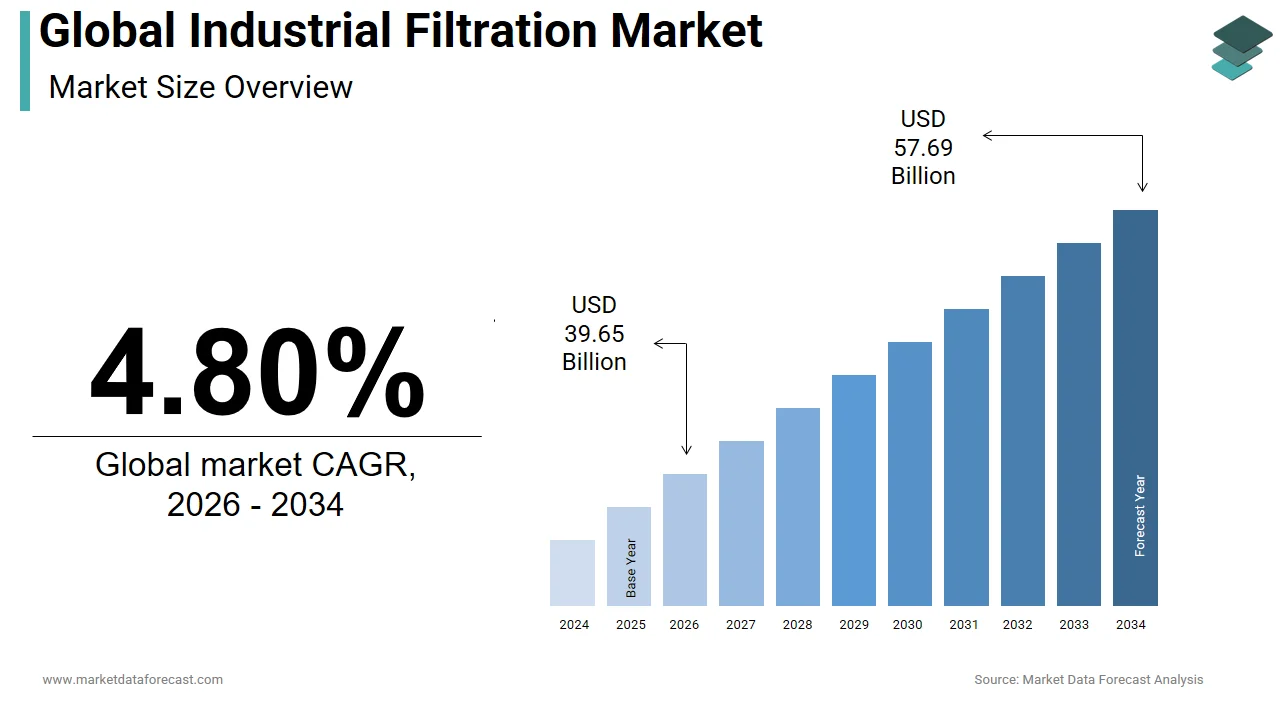

The global industrial filtration market was valued at USD 37.83 billion in 2025, is estimated to reach USD 39.65 billion in 2026, and is projected to reach USD 57.69 billion by 2034, growing at a CAGR of 4.80% from 2026 to 2034.

Industrial filtration is used to remove contaminants from liquids and gases across manufacturing, energy, pharmaceuticals, food and beverage, and chemical processing sectors. These systems ensure product purity, regulatory compliance, equipment protection, and environmental safety. According to the International Energy Agency, industrial processes account for nearly 37% of global final energy consumption, much of which involves fluid-intensive operations requiring filtration to maintain efficiency and reduce emissions. As per the study, a portion of chemical manufacturing facilities utilize some form of liquid or gas filtration to meet Clean Air and Clean Water Act standards.

MARKET DRIVERS

Stringent Environmental Regulations Driving Filtration System Adoption

The escalating stringency of environmental regulations governing industrial emissions and wastewater discharge is accelerating the growth of the industrial filtration market. The European Union’s Industrial Emissions Directive requires that large combustion plants and chemical processing units install high-efficiency particulate air (HEPA) and liquid filtration systems to limit pollutants. As per the research, a portion of industrial facilities in the EU underwent filtration system upgrades to comply with revised emission thresholds. In China, it enforced stricter wastewater discharge standards, requiring pharmaceutical and chemical plants to adopt membrane filtration technologies.

Rising Demand for High-Purity Filtration in Semiconductor and Pharma Manufacturing

Expansion of high-purity manufacturing in the semiconductor and pharmaceutical industries, where even microscopic contaminants can compromise product integrity, is expected to further enhance the growth of the industrial filtration market. According to the research, the global semiconductor fabrication capacity is expected to grow, with new fabs under construction, each requiring advanced liquid and gas filtration systems. Ultrapure water (UPW) systems, which rely on multi-stage filtration, consume significant gallons per day in a single fab, as per the study. Many injectable drugs produced globally require such filtration, which is driving demand for single-use and integrity-tested filter cartridges.

MARKET RESTRAINTS

High Total Cost of Ownership Limiting Filtration System Adoption

The high total cost of ownership associated with advanced filtration systems is restraining the growth of the industrial filtration market. While initial equipment costs are substantial, ongoing expenses related to membrane replacement, energy consumption, and maintenance further strain operational budgets. The reverse osmosis systems in industrial water treatment can incur notable operating costs per cubic meter, with membrane replacement accounting for a portion of lifecycle expenses. In India, a study found that many small and medium-sized enterprises (SMEs) in the textile and dyeing sector delayed filtration upgrades due to capital constraints, despite facing regulatory penalties.

Filtration Media Performance Degradation Under Extreme Conditions

Performance degradation of filtration media under extreme industrial conditions is also a factor affecting the growth of the industrial filtration market. For example, high temperature, pressure, or chemical exposure. Polymeric membranes used in solvent filtration, for example, often degrade when exposed to aggressive organic compounds, reducing lifespan and filtration efficiency. As per the research, polyethersulfone (PES) membranes lose a portion of their flux capacity after long hours of continuous exposure to aromatic solvents at 80°C. Similarly, in cement and metal processing, particulate-laden exhaust gases can blind baghouse filters within weeks, necessitating frequent replacements.

MARKET OPPORTUNITIES

Smart Sensors & Predictive Maintenance Integration

Integration of smart sensors and predictive maintenance technologies is ascribed to promote new opportunities for the industrial filtration market expansion. The adoption of Internet of Things (IoT)-enabled pressure differential monitors and flow sensors allows real-time tracking of filter performance, enabling proactive replacement before failure. According to a study, predictive maintenance in industrial filtration can reduce unplanned downtime and extend filter life. Companies like Pall Corporation and Sartorius have launched self-diagnosing filter housings equipped with RFID tags that transmit usage data to cloud-based platforms. Furthermore, the Industrial Internet of Things (IIoT) trade in manufacturing is projected to increase notably, as per the study, creating a robust ecosystem for intelligent filtration integration. This shift enhances operational transparency and reduces lifecycle costs, which makes advanced systems more attractive to cost-conscious operators.

Growing Adoption of Single-Use Filtration Technologies in Biopharma

The growing adoption of single-use filtration technologies in biopharmaceutical manufacturing is an emerging opportunity for the growth of the industrial filtration market with the rise of personalized medicine and mRNA-based therapeutics. Unlike traditional stainless-steel systems, single-use filters and capsule filters eliminate cross-contamination risks and reduce cleaning validation requirements. As per the research, many new biologics facilities constructed since 2020 have adopted single-use filtration trains for upstream and downstream processing. This modularity supports agile and decentralized production, which positions single-use systems as a cornerstone of next-generation biomanufacturing.

MARKET CHALLENGES

Lack of Sustainable End-of-Life Management for Used Filtration Media

The scarcity of sustainable end-of-life management for used filtration media is a challenging factor for the growth of the Industrial market. Millions of tons of spent filters, including non-biodegradable membranes and contaminated cartridges, end up in landfills annually. As per the study, significant amounts of industrial filter waste were disposed of in hazardous landfills, with a lesser share being recycled. Polymeric filter elements, particularly those made from PVDF and PTFE, resist natural degradation and require specialized thermal or chemical recycling processes. While some manufacturers like Donaldson Company have introduced take-back programs, scalability remains limited.

Compatibility Issues of Advanced Filtration Systems with Legacy Industrial Infrastructure

The mismatch between filtration technology development and the operational realities of legacy industrial plants also challenges the growth of the industrial filtration market. Many existing facilities, particularly in the petrochemical and power sectors, were designed before modern filtration standards and lack the spatial or hydraulic compatibility for retrofitting advanced systems. According to the research, a portion of coal-fired power plants in operation globally are significantly old, with limited capacity to integrate baghouse upgrades or flue gas desulfurization filters. Retrofitting often requires extensive downtime and structural modifications, which can cost more than the price of the filtration unit itself, as per the study. In Eastern Europe and Southeast Asia, where aging infrastructure predominates, this barrier delays compliance with emissions norms.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Market Leaders Profiled | 3M Company, Alfa Laval Inc., Donaldson Company Inc., Filtration Group, Freudenberg Filtration Technologies SE & Co. KG, Mann + Hummel, Pall Corporation, Parker Hannifin Corp., Ahlstrom-Munksjö, Hollingsworth & Vose Company, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

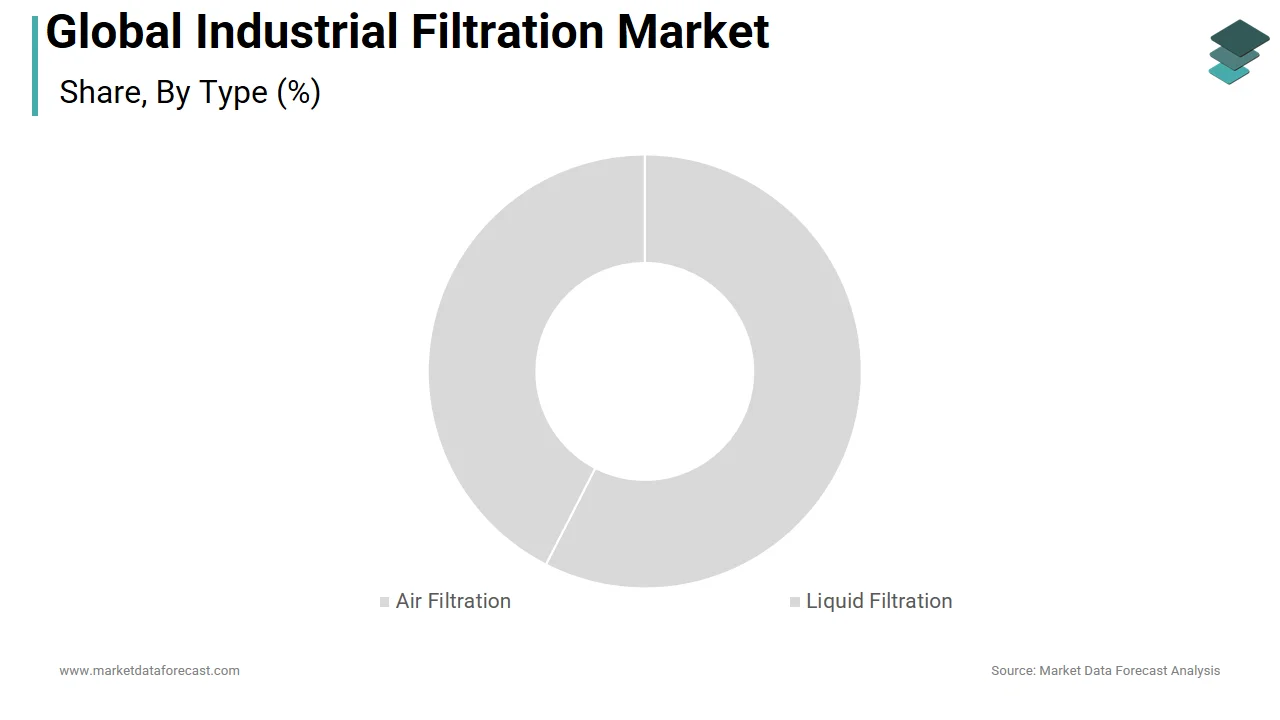

The liquid filtration segment dominated the industrial filtration market by capturing a 58.4% share in 2024 with its widespread integration across industries where purity and process efficiency are non-negotiable. For instance, the U.S. Food and Drug Administration requires that pharmaceutical manufacturers use sterile filtration processes, driving demand for advanced liquid filters. Apart from these, the wastewater treatment business worldwide heavily depends on liquid filtration technologies, further reinforcing its dominance.

The air filtration segment is predicted to witness a CAGR of 7.2% from 2026 to 2034 due to escalating concerns over industrial air pollution and worker safety. A significant number of workers die annually from work-related diseases and injuries, many linked to poor air quality in industrial environments. The regulatory bodies, such as OSHA in the United States and the European Agency for Safety and Health at Work, have tightened permissible exposure limits for particulates and hazardous fumes. Industries like metalworking, cement, and power generation are investing heavily in high-efficiency particulate air (HEPA) and electrostatic precipitator systems. Furthermore, the global push for cleaner manufacturing, which is exemplified by the EU’s Industrial Emissions Directive, accelerates adoption.

By Application Insights

The chemicals and petrochemicals segment led the industrial filtration market by accounting for 30.8% share in 2024. The growth of the chemicals and petrochemicals segment is attributed to the sector’s complex and contaminant-sensitive production processes. Filtration is essential in refining crude oil, purifying solvents, and protecting catalysts in reactors, where even minor particulate presence can degrade performance or cause costly downtime. Moreover, with global ethylene production increasing, the scale of operations demands robust filtration infrastructure. Environmental regulations, such as the U.S. Clean Air Act and REACH in Europe, further compel operators to adopt advanced filtration to minimize emissions and effluent discharge, which makes it a non-negotiable component of modern petrochemical operations.

The pharmaceutical manufacturing segment is estimated to register the fastest CAGR of 8.1% during the forecast period. The growth of the pharmaceutical manufacturing segment can be due to the industry’s stringent purity requirements and the global surge in biopharmaceutical production. With biologics accounting for a portion of new drug approvals in the U.S., as per the research, the demand for ultra-pure water (WFI) and viral filtration systems has skyrocketed. Single-use filtration technologies, which reduce cross-contamination risks, are gaining traction.

REGIONAL ANALYSIS

Asia-Pacific Industrial Filtration Market Insights

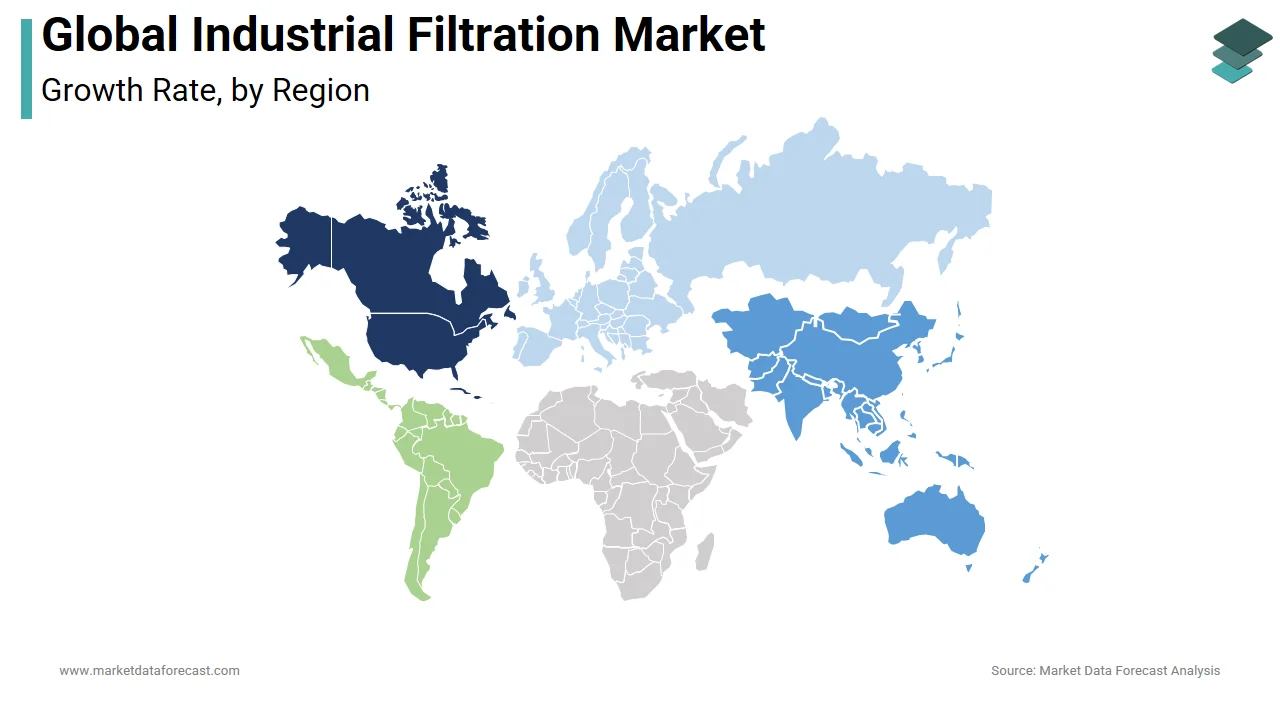

Asia-Pacific was the top performer in the global industrial filtration market in 2024 and accounted for 37.2% of the market share in 2024. Moreover, the Asia Pacific is also the fastest-growing region in the global market. The domination of the APAC market is primarily driven by the rapid industrialization, urbanization, and government-led environmental reforms across China, India, and Southeast Asia. China alone accounts for a notable share of global industrial output, as per the study, creating massive demand for process filtration in steel, chemicals, and power sectors. India aims to reduce particulate matter in cities, driving the deployment of industrial air filters. Apart from these, the region hosts a portion of the world’s new power plant constructions, mostly coal and gas-based, as per the study, all requiring advanced filtration systems.

North America Industrial Filtration Market Insights

North America was the second-largest in the global industrial filtration market due to its mature industrial base and regulatory rigor. The region’s strength lies in its advanced manufacturing infrastructure and strict compliance standards enforced by agencies like the Environmental Protection Agency and OSHA. The U.S. industrial sector spends a significant amount annually on pollution control equipment, including filtration systems. The shale gas boom has also increased demand for liquid filtration in natural gas processing, with a number of active oil and gas wells in the U.S. requiring continuous filtration, as per the research. Furthermore, the rise of biomanufacturing hubs in Massachusetts and North Carolina is boosting demand for sterile filtration in pharmaceuticals. North America remains a leader in R&D; companies like Pall Corporation and 3M are pioneering smart, modular filtration systems integrated with AI for predictive maintenance.

Europe Industrial Filtration Market Insights

Europe grew steadily in the global industrial filtration market with its commitment to environmental sustainability and industrial modernization. The European Green Deal, which targets a reduction in greenhouse gas emissions, has spurred investments in clean manufacturing technologies, including high-efficiency filtration. Germany, Europe’s largest industrial economy, operates a notable number of manufacturing firms that require filtration for precision engineering and chemical processes, as per the study. The REACH regulation requires filtration for chemical handling, while the Industrial Emissions Directive covers several installations across the EU, all requiring emission control systems. Apart from these, the pharmaceutical sector in Switzerland and Ireland relies on ultra-pure water systems, with the European Medicines Agency enforcing strict sterility standards.

Latin America Industrial Filtration Market Insights

Latin America grew steadily in the global industrial filtration market. It is a smaller but rapidly evolving segment. Brazil and Mexico are the key contributors to the growth of the Latin America market, which is driven by expanding mining, food processing, and energy sectors. Brazil is the world’s largest exporter of iron ore, with substantial metric tons produced, as per the research, necessitating extensive dust and liquid filtration in extraction and processing. Mexico’s proximity to the U.S. has boosted its role in nearshoring manufacturing, particularly in automotive and electronics, where cleanroom environments require advanced air filtration.

Middle East and Africa Industrial Filtration Market Insights

The Middle East and Africa are likely to grow in the global industrial filtration market during the forecast period. The Middle East dominates the regional market due to its energy-intensive industries. Saudi Arabia and the UAE are investing heavily in diversifying their economies under visions like Saudi Vision 2030, which includes expanding petrochemical and desalination capacity. The region operates a notable share of the world’s large-scale desalination plants, according to the study, all relying on advanced liquid filtration to treat seawater.

COMPETITION OVERVIEW

The industrial filtration market features intense competition shaped by technological innovation, regulatory demands, and regional industrial growth. While global players dominate with advanced R&D and extensive distribution networks, regional manufacturers are gaining ground by offering cost-effective, localized solutions. Differentiation is driven by product performance, customization, and integration with digital monitoring systems. Competition is particularly fierce in high-growth sectors like pharmaceuticals and semiconductors, where purity standards are extreme. Companies are investing in sustainable filtration media and modular systems to meet evolving environmental regulations. Strategic partnerships with engineering firms and industrial OEMs are common to embed filtration solutions into larger process systems. The rise of single-use and smart filtration technologies has intensified rivalry, especially in Asia-Pacific, where rapid industrialization and government policies are accelerating demand and encouraging new market entrants.

KEY MARKET PLAYERS

Some of the noteworthy companies in the global industrial filtration market profiled in this report are

- 3M Company

- Alfa Laval Inc.

- Donaldson Company, Inc.

- Filtration Group

- Freudenberg Filtration Technologies SE & Co. KG

- MANN+HUMMEL

- Pall Corporation

- Parker Hannifin Corporation

- Ahlstrom-Munksjö

- Hollingsworth & Vose Company

TOP LEADING PLAYERS IN THE MARKET

Pall Corporation (a Danaher Company)

Pall Corporation has been a cornerstone in advancing industrial filtration technologies across the Asia-Pacific region, particularly in life sciences and semiconductor manufacturing. The company has deepened its footprint by establishing regional innovation centers in Shanghai and Singapore by enabling localized R&D and rapid customer support. It has also expanded its service network in Japan and South Korea to support cleanroom and ultra-pure water systems. Pall enhances predictive maintenance capabilities for clients in high-tech industries by integrating digital monitoring tools into its filtration units.

Alfa Laval

Alfa Laval plays a pivotal role in the Asia-Pacific industrial filtration landscape, particularly in energy, marine, and food processing sectors. The company has strengthened its regional presence through strategic expansions in China and India, where it operates manufacturing facilities and application centers. The company has also partnered with local engineering firms in Indonesia and Vietnam to deliver integrated separation and filtration systems for palm oil and chemical processing. Alfa Laval’s focus on sustainability-driven innovation, such as energy-efficient filtration systems that reduce operational waste, has made it a preferred partner for industrial modernization projects across emerging Asian markets.

Sartorius AG

Sartorius AG has emerged as a key enabler of advanced filtration in Asia-Pacific’s rapidly expanding biopharmaceutical sector. The company has invested heavily in regional infrastructure, including a state-of-the-art filtration membrane production facility, to meet rising demand for single-use technologies. It has expanded its technical service teams in South Korea and Singapore to support biotech firms adopting continuous manufacturing processes. The company also launched digital twin-enabled filtration systems that simulate performance under real-world conditions, improving process efficiency. Through collaborations with academic institutions in Australia and India, Sartorius is driving innovation in sterile filtration and process intensification which places itself at the forefront of next-generation bioprocessing in the region.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the industrial filtration market are deploying a mix of innovation-driven and geographically focused strategies to strengthen their positions. A primary approach is product differentiation through advanced materials, such as nanofiber membranes and pleated cartridge designs, enhancing efficiency and lifespan. Companies are increasingly integrating digital technologies, IoT sensors and cloud-based monitoring, into filtration systems to enable predictive maintenance and real-time performance tracking. Strategic expansions into high-growth regions like Asia-Pacific through local manufacturing and joint ventures are common. Mergers and acquisitions are also prevalent which allowes firms to broaden technology portfolios and customer reach.

MARKET SEGMENTATION

This global industrial filtration market research report is segmented and sub-segmented into the following categories.

By Type

- Air Filtration

- Liquid Filtration

By Application

- Food & Beverages

- Power Generation

- Semiconductors & Electronics

- Chemicals & Petrochemicals

- Pharmaceutical Manufacturing

- Metals & Mining

- Paper & Paints

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Middle East Africa

- Latin America

Frequently Asked Questions

1. What is the Industrial Filtration Market?

The Industrial Filtration Market involves the production and deployment of systems and technologies designed to remove particulate, liquid, and gaseous contaminants from industrial processes in sectors such as manufacturing, oil and gas, power generation, food and beverage, and pharmaceuticals

2. What are the main types of filtration in the Industrial Filtration Market?

Key types are air and gas filtration, liquid filtration, HEPA and ULPA filters, membrane-based solutions, and advanced media for removing pollutants and ensuring regulatory compliance

3. Which industries are the largest end users in the Industrial Filtration Market?

The market is driven by demand from power generation, oil and gas, chemicals, metal and mining, pharmaceuticals, food and beverage, and manufacturing sectors

4. Why is air and gas filtration dominant in the Industrial Filtration Market?

Air and gas filtration account for nearly 70% of market share due to stringent emission standards and the need to control particulate matter and toxic gases in heavy industries

5. How do regulations impact the Industrial Filtration Market?

Increasingly strict environmental and safety regulations for air and water emissions drive demand for higher-efficiency filtration systems across global industries

6. What are the regional trends in the Industrial Filtration Market?

Asia Pacific is the fastest-growing region due to rapid industrialization, while North America leads in share driven by regulatory enforcement and investment in advanced filtration

7. What are current technology trends in the Industrial Filtration Market?

Trends include HEPA-grade and membrane innovations, nanofiber filters, smart IoT-integrated systems, and energy-efficient filter designs for sustainability and operational cost savings

8. Who are the leading vendors in the Industrial Filtration Market?

Top vendors include Donaldson, Pall, Mann+Hummel, Parker Hannifin, and specialized technology providers in filtration and filter media

9. How does the Industrial Filtration Market address industrial wastewater?

Industrial filtration solutions ensure removal of solids and hazardous materials from wastewater streams before discharge, supporting regulatory compliance and water reuse

10. What are the benefits of adopting advanced industrial filtration systems?

Benefits include improved workplace safety, reduced emissions, efficient process optimization, compliance with international norms, and lower operational costs

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com