Global Industry 4.0 Market Size, Share, Trends & Growth Forecast Report, Segmented By Technology (Internet of Things, Cloud Computing, Artificial Intelligence, Robotics, Augmented and Virtual Reality, Big Data and Analytics, Cyber Security, Machine Learning, and Others), Connectivity, End-user, & Region (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa), Industry Analysis 2026 to 2034

Global Industry 4.0 Market Size

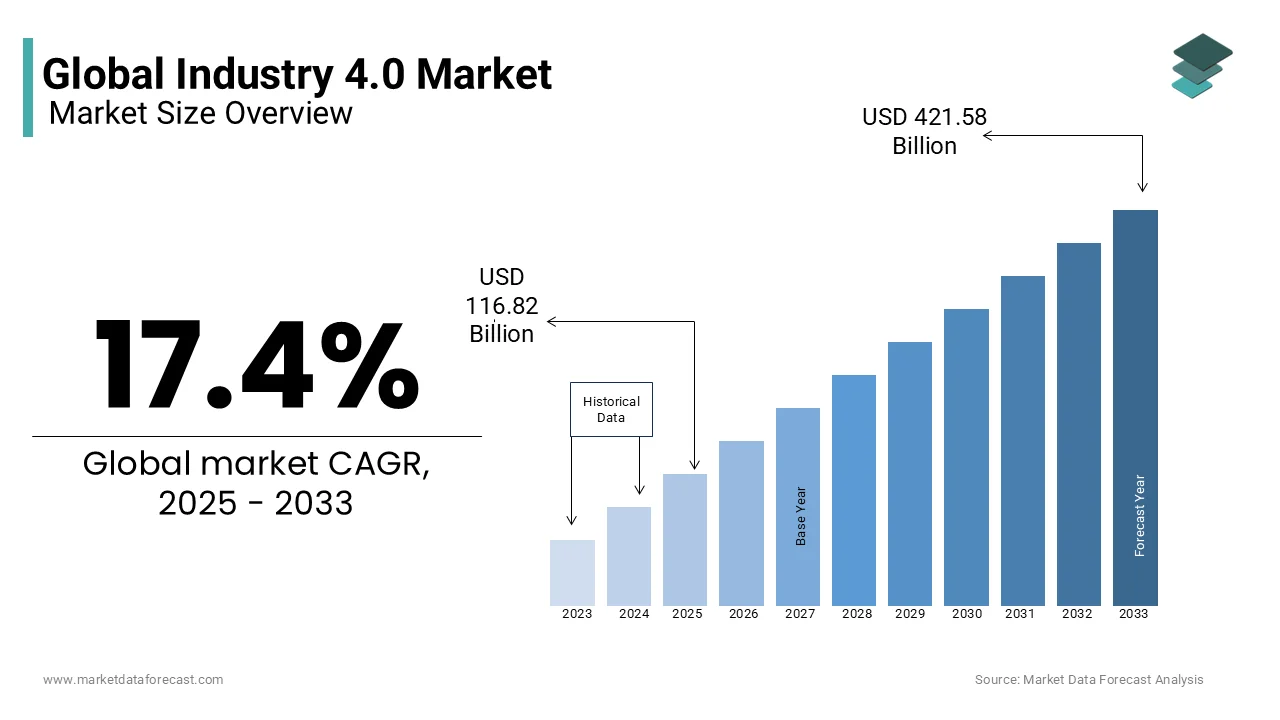

The global Industry 4.0 market size was valued at USD 116.82 billion in 2025 and is anticipated to reach USD 137.15 billion in 2026 and USD 494.91 billion by 2034, growing at a CAGR of 17.4% from 2026 to 2034.

Industry 4.0 refers to the systematic integration of networked automation systems, advanced machine intelligence, and continuous data exchange into modern manufacturing and industrial operations. This paradigm shifts traditional production environments into interconnected ecosystems where equipment communicates autonomously, optimizes workflows, and adapts to dynamic operational requirements. The foundation relies on seamless convergence between operational technology and information technology, enabling immediate visibility across entire value chains. According to industrial studies monitored by the World Economic Forum, while 85% of manufacturing leaders view digital transformation as a strategic requirement, real-world 4IR deployment is led by a specialized network of advanced "Lighthouse" facilities mapping out global operational resilience. Research indicates that total global IoT active endpoints across all sectors hover around 17 billion to 20 billion, driving substantial net increases in corporate data generation. Additionally, frameworks managed by the United Nations Industrial Development Organization (UNIDO) confirm that integrating AI-driven optimization and real-time monitoring helps smart facilities reduce energy consumption by 10% to 30%, acting as a central component of global industrial decarbonisation. Workforce dynamics are also evolving rapidly. Also, workforce studies tracked by the International Labour Organization (ILO) highlight that the fourth industrial revolution is aggressively reshaping manufacturing jobs, with technological literacy ranking as a top global skill priority as employers restructure operations around system monitoring and predictive diagnostics. These structural changes indicate a fundamental reconfiguration of how industrial assets are managed, maintained, and optimized. The transition extends beyond mere technological adoption and encompasses comprehensive process reengineering, standardized data architectures, and continuous learning frameworks that empower organizations to sustain competitive advantage.

MARKET DRIVERS

Accelerated adoption of predictive maintenance frameworks drives substantial industrial modernization across global manufacturing sectors, which are among the major accelerators of the industry 4.0 market. Manufacturing operators increasingly demand continuous equipment monitoring to eliminate unplanned downtime and extend asset lifecycles. Traditional reactive maintenance protocols generate significant operational disruptions, whereas sensor equipped diagnostic systems analyze vibration patterns, thermal fluctuations, and acoustic signatures to forecast component degradation before failure occurs. : Research published across industrial engineering journals shows that integrating automated condition-driven monitoring strategies allows modern facilities to reduce overall maintenance costs by 30% to 50% and significantly eliminate unplanned factory floor downtime. The demand for these intelligent diagnostic architectures stems from stringent regulatory requirements surrounding workplace safety and environmental compliance, which compel enterprises to maintain transparent operational logs. Furthermore, according to industrial optimization guidelines monitored by the International Energy Agency (IEA), capturing lost energy through waste heat recovery and scaling smart, real-time Energy Management Systems (EMS) helps manufacturers reduce systemic production energy waste by 10% to 30%. Supply chain resilience remains a critical motivator, as organizations recognize that localized equipment failures cascade into broader logistical bottlenecks. Consequently, industrial managers prioritize investments in machine learning algorithms and localized computing infrastructure to process diagnostic data rapidly and execute corrective interventions without relying on centralized cloud networks. This operational shift fundamentally transforms maintenance from a cost center into a strategic efficiency catalyst.

Integrating digital twin simulations for process optimization accelerates industrial capability advancement, and thereby propels the global industry 4.0 market forward. This is achieved by enabling the virtual replication of physical assets and production environments. Enterprises demand precise operational forecasting to minimize material waste, streamline workflow sequencing, and validate engineering modifications before physical implementation. These virtual replicas continuously synchronize with live machinery through embedded telemetry networks, allowing engineers to test parameter adjustments in secure digital environments. Utilizing standardized simulation architectures supported by the National Institute of Standards and Technology (NIST) helps operations seamlessly map out production changes, identifying layout bottlenecks and optimizing cycle times before physical machinery is deployed. The demand originates from intensifying competitive pressures that require rapid product iteration while maintaining stringent quality benchmarks. Industrial leaders recognize that digital simulations provide unprecedented visibility into bottleneck formation, energy distribution patterns, and labor allocation inefficiencies. Consequently, organizations deploy advanced computational modeling to simulate stress scenarios, optimize throughput capacities, and validate control logic modifications without disrupting active manufacturing schedules. This capability transforms engineering validation from an empirical trial process into a deterministic analytical discipline that consistently enhances operational precision.

MARKET RESTRAINTS

A persistent shortage of specialized technical personnel constrains the widespread deployment of advanced industrial automation across manufacturing facilities, which restricts the growth of the global Industry 4.0 market. Enterprises encounter substantial difficulties in recruiting professionals capable of managing interconnected cyber infrastructure, programming autonomous control systems, and interpreting complex analytical outputs. Traditional educational frameworks frequently lag behind technological evolution, leaving graduates insufficiently prepared for roles requiring multidisciplinary expertise in data science, industrial networking, and machine diagnostics. According to employment studies tracked by the OECD, advanced manufacturing sectors face a persistent structural skills gap, driven by a mismatch between traditional engineering certifications and the multi-disciplinary skills required to operate automated networks. Research from the International Labour Organization (ILO) emphasizes that technical and vocational education and training systems must dynamically adapt to automation shifts, as the rapid evolution of digital factory systems renders rigid, static industrial training curricula obsolete. This skills gap directly impedes system integration timelines and forces organizations to operate advanced technologies below optimal capacity. Consequently, production managers frequently rely on external consultants for routine system calibration, which increases operational expenditures and reduces internal knowledge retention. The absence of standardized certification pathways for industrial data architecture further complicates workforce development initiatives. Enterprises must therefore invest heavily in continuous upskilling programs and collaborative academic partnerships to cultivate internal expertise capable of sustaining complex digital ecosystems without excessive reliance on external specialists.

Fragmented data standardization across industrial networks hampers seamless interoperability between disparate manufacturing equipment and enterprise software platforms, which further slows down the expansion of the industry 4.0 market. Diverse machinery manufacturers implement proprietary communication protocols that prevent unified data aggregation and complicate information exchange across systems. Production environments frequently contain vintage control units operating alongside modern intelligent sensors, creating compatibility conflicts that hinder comprehensive operational visibility. As per documentation from the International Society of Automation (ISA), facilities face severe structural hurdles trying to achieve interoperability between legacy field machinery and modern cloud systems, highlighting the critical need for open data exchange frameworks like OPC UA to bypass communication silos. Academic research published through the IEEE confirms that industrial protocol incompatibility creates severe operational friction, requiring extensive human middleware development and custom configuration mapping to successfully bridge disparate networks. This lack of universal data architecture forces engineering teams to develop custom translation solutions that introduce additional latency points and potential security vulnerabilities. Consequently, organizations experience delayed analytics implementation and reduced accuracy in predictive modeling outputs. The absence of harmonized communication frameworks also complicates supply chain synchronization, as external partners cannot reliably exchange production status indicators or inventory metrics. Manufacturers must therefore prioritize adoption of open industrial communication standards to establish consistent data formatting and enable frictionless information flow across entire operational networks.

MARKET OPPORTUNITIES

Expansion of edge computing infrastructure for immediate analytics paves the way for enhanced operational responsiveness and localized decision protocols across distributed manufacturing facilities, which is anticipated to drive the growth of the Industry 4.0 market. Processing data directly at equipment endpoints eliminates network latency and enables instantaneous adjustment of production parameters without relying on centralized cloud architecture. Industrial operators increasingly recognize that localized computational capacity improves system reliability during network outages and reduces bandwidth consumption associated with continuous telemetry transmission. Research highlight that edge infrastructure is growing rapidly because it enables near-zero latency processing and drastically cuts cloud bandwidth fees by screening and handling production data right on the shop floor. Case profiles from the World Economic Forum Global Lighthouse Network show that smart factories deploying localized machine learning models at individual workstations drastically decrease escape defect rates and boost production quality by catching quality deviations instantly. This architectural shift empowers production managers to implement autonomous quality control mechanisms that respond to deviations within milliseconds rather than minutes. Consequently, organizations can execute dynamic workflow adjustments, optimize resource allocation, and maintain consistent output standards even under fluctuating operational conditions. The proliferation of compact processing modules and specialized industrial microprocessors continues to lower deployment barriers, allowing midsize manufacturers to implement sophisticated analytical capabilities previously restricted to major operations with substantial technology budgets.

Development of collaborative robotics for flexible assembly operations generates significant opportunities for workforce augmentation, which is expected to boost the expansion of the industry 4.0% market. Furthermore, it enables adaptive manufacturing configurations across diverse production environments. Unlike conventional automated systems that require isolated safety enclosures, modern collaborative platforms operate alongside human technicians and adjust movement trajectories in response to live environmental inputs. Manufacturing enterprises increasingly deploy these adaptable machines to execute repetitive positioning tasks while reserving skilled labor for complex quality inspection and engineering validation activities. Annual data from the International Federation of Robotics (IFR) shows that collaborative robots maintain a steady 10% share of all new global industrial robot deployments, acting as a high-growth sector for flexible assembly environments. Operational guidelines from the VDMA show that deploying flexible, software-driven robotic arms allows manufacturers to reconfigure assembly steps on the fly, while simultaneously lowering workforce physical strains by offloading heavy, repetitive material handling tasks. This operational model enables facilities to transition rapidly between product variants without extensive mechanical recalibration, thereby supporting customized production mandates and shorter delivery cycles. Additionally, integrated force sensing capabilities and advanced vision systems allow collaborative platforms to detect environmental anomalies and execute safe operational pauses, minimizing workplace incidents. Consequently, manufacturers achieve higher throughput consistency while maintaining adaptable production layouts that respond efficiently to evolving market demands.

MARKET CHALLENGES

Escalating cybersecurity vulnerabilities in connected industrial ecosystems present critical operational risks, which constrain the growth of the Industry 4.0 market. These threats jeopardize both production continuity and intellectual property integrity across modern manufacturing networks. As enterprises expand digital interconnectivity, previously isolated operational technology environments become accessible through enterprise information networks, creating additional attack surfaces for malicious actors. Vintage control systems frequently lack modern encryption protocols and continuous monitoring capabilities, rendering them susceptible to unauthorized command execution and data manipulation. Cyber intelligence trends monitored alongside IEC 62443 cybersecurity frameworks confirm that modern factories face escalating threats, as the convergence of IT and OT networks expands the attack surface, making outdated device firmware and weak credential management top entry vectors for industrial hackers. Threat reports highlighted by the National Cyber Security Centre (NCSC) show that ransomware is the most acute cyber threat facing global manufacturing, with attackers aggressively targeting supervisory control and data acquisition (SCADA) systems to force immediate financial payouts by halting production lines. These security breaches frequently trigger extended production halts, equipment malfunctions, and significant financial losses associated with system recovery and regulatory penalties. Furthermore, the interconnected nature of supply chain networks enables threat propagation across multiple vendor ecosystems, amplifying disruption potential beyond individual facility boundaries. Organizations must therefore implement comprehensive verification architectures, continuous vulnerability assessments, and segmented network topologies to isolate critical operational functions and mitigate systemic exposure to increasingly sophisticated digital threats.

Complex capital allocation for legacy system modernization restricts the pace of technological transformation across established manufacturing enterprises with aging operational infrastructure, and therefore impedes the expansion of the industry 4.0 market. Production facilities frequently operate with vintage control equipment that lacks native compatibility with contemporary data acquisition platforms and requires extensive retrofitting to support modern connectivity standards. Engineering teams must navigate intricate upgrade pathways that involve simultaneous replacement of mechanical components, electrical distribution networks, and software management interfaces while maintaining continuous production output. Digital scaling assessments from the McKinsey Global Institute point out that a vast majority of advanced manufacturing initiatives struggle to move beyond "pilot purgatory" due to the steep financial and operational friction of scaling software solutions across diverse, unaligned factory environments. Economic metrics from the World Bank indicate that small and medium-sized enterprises (SMEs) face disproportionate financing barriers globally, heavily limiting their ability to fund large-scale technology upgrades or transition to high-cost automated infrastructure. These incremental upgrade approaches frequently generate fragmented system architectures that complicate data synchronization and increase maintenance overhead. Additionally, uncertain return on investment calculations deter executive leadership from approving extensive transformation initiatives, particularly when traditional production metrics remain stable. Consequently, enterprises must develop phased implementation roadmaps, secure specialized financing mechanisms, and establish clear performance benchmarking protocols to justify sustained investment in comprehensive operational modernization programs.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 17.4% |

| Segments Covered | By Technology, Connectivity, End-Use, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Mitsubishi, General Electric, Microsoft, Google, Intel, HP, Siemens, ABB Ltd, Schneider Electric SE, Qualcomm Inc. |

SEGMENTAL ANALYSIS

By Technology Insights

The Internet of Things segment dominated the industry 4.0 market and accounted for a 28.5% share in 2025. Factors such as the foundational role of connected sensors and devices in enabling real time data exchange across production environments drive the dominance of this segment. Industrial operators increasingly deploy IoT endpoints to monitor equipment performance, track material flow, and coordinate autonomous workflows without manual intervention. Commercial tech trackers show that total global IoT active endpoints hover around 17 billion to 20 billion, providing data visibility across interconnected supply chains. Factory profiles from the World Economic Forum Global Lighthouse Network show that smart facilities incorporating digital monitoring and predictive loops significantly minimize equipment failures and maximize overall equipment effectiveness (OEE) across their operations. Manufacturing leaders recognize that seamless device interconnectivity forms the backbone for advanced analytics, predictive maintenance, and adaptive control systems. Consequently, enterprises prioritize investments in robust communication protocols, edge compatible sensors, and secure data pipelines to ensure reliable information flow across distributed assets. This technological foundation empowers organizations to transition from reactive operations to proactive optimization strategies that enhance productivity and resource efficiency.

The Digital Twin segment is expected to exhibit a noteworthy CAGR of 25.1% from 2026 to 2034. This accelerated expansion is propelled by rising demand for virtual replication of physical assets to validate engineering modifications before physical implementation. Manufacturing enterprises utilize digital simulations to test production line configurations, optimize workflow sequencing, and predict maintenance requirements without disrupting active operations. Utilizing standardized simulation architectures supported by the National Institute of Standards and Technology (NIST) helps engineering teams successfully test product workflows and predict layout bottlenecks before deploying physical machinery on the shop floor. Industrial leaders recognize that digital replicas provide unprecedented visibility into bottleneck formation, energy distribution patterns, and labor allocation inefficiencies. Consequently, organizations deploy advanced computational modeling to simulate stress scenarios, optimize throughput capacities, and validate control logic modifications without disrupting active manufacturing schedules. This capability transforms engineering validation from an empirical trial process into a deterministic analytical discipline that consistently enhances operational precision.

By Connectivity Insights

The wired connectivity segment maintained the lead in the Industry 4.0 market and captured a 58.3% share in 2025 because of its reliability for time critical industrial communications. Production environments require deterministic data transmission with minimal latency to coordinate synchronized machine operations and safety interlock systems. Industrial operators prioritize physical cabling for core production networks because it eliminates radio frequency interference risks and provides consistent performance under electromagnetic noise conditions common in manufacturing facilities. Consequently, engineering teams deploy structured cabling architectures with redundant pathways to maintain operational continuity during component failures or maintenance activities. This foundational connectivity layer enables seamless integration of programmable logic controllers, human machine interfaces, and supervisory systems that form the backbone of modern automated production environments.

On the other hand, the Wireless connectivity segment is predicted to witness the highest CAGR of 24.3% from 2026 to 2034 owing to increasing adoption of flexible deployment scenarios where physical cabling proves impractical or cost prohibitive. Manufacturing facilities leverage wireless protocols to connect mobile robots, handheld diagnostic tools, and temporary sensor arrays that require rapid reconfiguration during product changeovers. Technical frameworks mapped out by the International Telecommunication Union (ITU) establish rigid performance metrics for latency and connection availability, enabling manufacturers to confidently deploy specialized industrial wireless networks to scale up real-time environmental monitoring. Global asset profiles monitored by the World Economic Forum confirm that scaling up IoT-driven logistics and wireless asset tracking provides unprecedented operational visibility, allowing managers to optimize supply routes and mitigate component losses across large campuses. Industrial managers recognize that modern wireless standards provide sufficient reliability for non safety critical applications while offering significant advantages in deployment speed and maintenance accessibility. Consequently, organizations implement hybrid network architectures that combine wired backbone infrastructure with wireless edge extensions to balance performance requirements with operational flexibility. This approach enables comprehensive connectivity coverage while preserving deterministic performance for critical control functions.

By End User Analysis

The Manufacturing segment held the majority share of 31.4% of the Industry 4.0 market in 2025. This supremacy of the segment was supported by the sector's early adoption of automation technologies and continuous pressure to enhance productivity amid rising labor costs and supply chain volatility. Production facilities deploy integrated digital platforms to coordinate material flow, optimize machine utilization, and ensure consistent quality across high volume assembly operations. Technical efficiency blueprints overseen by the United Nations Industrial Development Organization (UNIDO) indicate that deploying digital twins and automated climate loops helps optimized factories reduce net unit energy waste by 10% to 30% to meet corporate net-zero requirements. Labor transition guidelines from the International Labour Organization (ILO) stress that technical vocational institutions must comprehensively modernize training formats, as automated systems increasingly shift factory floor roles toward continuous network monitoring and digital predictive troubleshooting. Manufacturing leaders recognize that comprehensive digital transformation enables rapid response to changing customer specifications while maintaining stringent regulatory compliance across global operations. Consequently, enterprises invest in unified data architectures that synchronize engineering design, production execution, and quality assurance workflows to eliminate information silos. This holistic approach transforms traditional production management into an adaptive ecosystem that continuously optimizes resource allocation and operational performance.

But the healthcare segment is estimated to register the fastest CAGR of 21.9% during the forecast. This swift expansion is fuelled by rising demand for precision manufacturing of medical devices, pharmaceuticals, and diagnostic equipment that require stringent process validation and traceability. Production facilities in this sector deploy connected monitoring systems to ensure compliance with regulatory standards while maintaining batch consistency across complex formulation processes. Training standards managed by the World Health Organization (WHO) stress that implementing strict continuous process analysis and routine Product Quality Reviews (PQRs) is critical to preventing downstream batch rejections and keeping medicine production lines consistent. Engineering guidelines published by the International Society for Pharmaceutical Engineering (ISPE) document that shifting from batch processing to continuous manufacturing helps facilities eliminate intermediate storage steps, improve quality assurance, and reduce material waste. Healthcare manufacturers recognize that integrated digital ecosystems enable rapid adaptation to evolving clinical requirements while maintaining comprehensive audit trails for regulatory submissions. Consequently, organizations invest in specialized control systems that synchronize formulation, filling, and packaging operations with quality management protocols to ensure patient safety. This capability transforms medical production from batch oriented processes into continuous validation frameworks that consistently enhance therapeutic outcomes.

REGIONAL MARKET ANALYSIS

North Market Analysis

North America was the top performer in the Industry 4.0 market and accounted for a 32.4% share in 2025. The region benefits from robust technological infrastructure, substantial research and development investments, and strong policy support for advanced manufacturing initiatives. United States based enterprises leverage federal programs such as the National Network for Manufacturing Innovation to accelerate digital transformation across automotive, aerospace, and pharmaceutical sectors. Standards and reference models deployed by the National Institute of Standards and Technology (NIST) assist American manufacturing firms in implementing interoperable systems that eliminate communication friction and optimize automated shop floor data flows. Canadian industrial operators similarly prioritize connectivity upgrades to enhance supply chain resilience and support export oriented production strategies. Regional leadership stems from early adoption of cloud based analytics, collaborative robotics, and predictive maintenance frameworks that enable rapid response to market fluctuations. Consequently, North American organizations continue to allocate significant capital toward intelligent infrastructure that sustains competitive advantage in global markets. This commitment to technological advancement ensures the region remains a primary catalyst for Industry 4.0 innovation and deployment worldwide.

Europe Market Analysis

Europe was positioned second in the Industry 4.0 market and occupied a share of 35.8% in 2025. The region benefits from coordinated policy frameworks such as the European Commission's Digital Europe Programme that incentivize cross border adoption of smart manufacturing technologies. German industrial enterprises lead continental efforts through initiatives like Industry 4.0 Plattform that standardize communication protocols and data architectures across supply networks. Operational guidelines published by the VDMA show that integrating software-driven automation and real-time monitoring allows European facilities to optimize machine workloads and track precise carbon footprints to meet strict regional sustainability laws. French and Italian manufacturers similarly prioritize automation investments to address demographic challenges and maintain export competitiveness in precision engineering sectors. Regional growth stems from strong collaboration between academic institutions, technology providers, and industrial users that accelerates practical deployment of emerging capabilities. Consequently, European organizations continue to pioneer interoperable solutions that enable seamless integration of legacy equipment with modern analytics platforms. This collaborative approach ensures the region remains a global benchmark for sustainable and efficient industrial modernization.

Asia Pacific Market Analysis

Asia Pacific holds a significant share of the Industry 4.0 market due to rapid industrialization, expanding middle class consumption, and aggressive government support for technological advancement across manufacturing sectors. Chinese enterprises leverage national strategies such as Made in China 2025 to accelerate adoption of robotics, artificial intelligence, and industrial internet platforms. The China Academy of Information and Communications Technology (CAICT) emphasize that deploying private 5G networks and fully integrated industrial software platforms is driving high-speed, data-connected automation across manufacturing corridors. Japanese and South Korean manufacturers similarly prioritize precision automation to maintain leadership in electronics, automotive, and semiconductor production. Regional growth stems from substantial investments in digital infrastructure, workforce development, and cross border technology transfer that enable scalable deployment of smart manufacturing solutions. Consequently, Asia Pacific organizations continue to expand adoption of connected systems that enhance productivity while addressing rising labor costs and environmental regulations. This momentum ensures the region remains a primary growth engine for global Industry 4.0 expansion.

Latin America Market Analysis

Latin America is growing steadily in the Industry 4.0 market, with increasing adoption driven by resource optimization mandates and export competitiveness requirements. Brazilian and Mexican industrial operators prioritize automation investments to enhance productivity in automotive, aerospace, and agribusiness sectors that serve global supply chains. Development initiatives funded by the Inter-American Development Bank (IDB) indicate that introducing basic digital management software helps regional manufacturing enterprises boost overall productivity and integrate more smoothly into global value chains. Regional growth stems from growing collaboration between multinational technology providers and local integrators that enable cost effective deployment of connected solutions. Consequently, Latin American organizations continue to adopt modular automation platforms that support incremental modernization without disrupting existing production workflows. This pragmatic approach ensures sustainable advancement toward intelligent manufacturing capabilities that enhance regional competitiveness in international markets.

Middle East and Africa Market Analysis

The Middle East and Africa region is predicted to expand notably in the Industry 4.0 market from 2026 to 2034 due to economic diversification initiatives and infrastructure modernization programs. United Arab Emirates and Saudi Arabian enterprises prioritize smart manufacturing investments to support non oil economic development strategies and attract foreign direct investment. Strategic industrial blueprints published by the Gulf Organization for Industrial Consulting (GOIC) stress that implementing automated tech frameworks is critical to improving production efficiency and reducing dependence on foreign manual labor across GCC manufacturing markets. Regional growth stems from strategic partnerships between government entities, technology providers, and academic institutions that enable knowledge transfer and workforce development. Consequently, Middle Eastern and African organizations continue to adopt scalable digital solutions that support sustainable industrial growth while addressing unique operational challenges. This focused approach ensures the region gradually expands its adoption of Industry 4.0 capabilities that enhance long term economic resilience.

COMPETITIVE LANDSCAPE

Competition in the Industry 4.0 market intensifies as technology providers, industrial conglomerates, and specialized startups converge to deliver integrated digital transformation solutions. Established players leverage extensive industry expertise and global support networks to offer comprehensive platforms that address complex operational requirements across diverse manufacturing environments. Emerging entrants differentiate through innovative applications of artificial intelligence, edge computing, and modular architectures that enable rapid deployment and scalability. Market dynamics favor organizations that demonstrate tangible return on investment through measurable improvements in productivity, quality, and sustainability outcomes. Competitive advantage increasingly depends on ecosystem partnerships that ensure interoperability, cybersecurity, and continuous innovation across evolving technology landscapes. Companies that successfully balance technological sophistication with practical implementation support gain stronger customer loyalty and market share expansion. This environment drives continuous advancement in industrial automation capabilities while creating opportunities for specialized solutions that address niche operational challenges. Consequently, the Industry 4.0 competitive landscape remains highly dynamic with ongoing consolidation, collaboration, and innovation shaping long term market leadership.

KEY MARKET PLAYERS

Some of the major players in the global Industry 4.0 market are

- Mitsubishi

- General Electric

- Microsoft

- Intel

- HP

- Siemens

- ABB Ltd

- Schneider Electric SE

- Qualcomm Inc.

Top Players In The Market

- Siemens AG maintains a prominent position in the Industry 4.0 market through its comprehensive portfolio of industrial automation, digitalization, and electrification solutions. The company leverages its Siemens Xcelerator platform to provide an open digital ecosystem that enables rapid deployment of industrial artificial intelligence and edge computing capabilities. Recent initiatives include the launch of Industrial Copilot for Operations which integrates generative AI with industrial edge systems to enhance real time decision making and minimize production downtime. Siemens continues to strengthen its market position through strategic acquisitions such as Altair Engineering to expand simulation and high performance computing offerings. The company collaborates extensively with technology partners to ensure interoperability across diverse industrial environments while maintaining stringent cybersecurity standards. Siemens also invests heavily in research and development to advance digital twin technologies and predictive analytics that enable proactive operational optimization. These efforts empower manufacturing enterprises to achieve sustainable productivity gains while adapting to evolving market demands and regulatory requirements.

- ABB Ltd contributes significantly to the Industry 4.0 market through its integrated solutions spanning robotics, process automation, and electrification technologies. The company emphasizes boundless automation strategies that connect field devices, edge systems, and cloud platforms to enable seamless data flow across industrial operations. Recent actions include the acquisition of ASTI Mobile Robotics to expand autonomous mobile robot capabilities for flexible material handling applications. ABB also partners with technology leaders to integrate artificial intelligence into vision inspection and predictive maintenance systems that enhance quality control and equipment reliability. The company focuses on developing vendor agnostic control platforms that support interoperability across diverse equipment ecosystems while ensuring compliance with international safety standards. ABB continues to invest in digital services that enable remote monitoring and optimization of industrial assets to reduce operational costs and improve sustainability outcomes. These initiatives empower customers to achieve greater operational agility and resource efficiency in increasingly complex production environments.

- Schneider Electric strengthens its Industry 4.0 market position through its EcoStruxure platform which delivers integrated energy management and automation solutions for industrial applications. The company emphasizes sustainable digital transformation by combining IoT connectivity, edge control, and analytics to optimize resource consumption and reduce environmental impact. Schneider Electric collaborates with cloud providers to enable hybrid deployment models that balance scalability with deterministic performance requirements for critical industrial processes. The company also invests in cybersecurity frameworks that protect operational technology networks from emerging digital threats while maintaining compliance with international standards. These efforts enable manufacturing enterprises to achieve significant energy savings and productivity improvements while advancing toward net zero operational footprints. Schneider Electric continues to expand its ecosystem partnerships to deliver comprehensive solutions that address evolving customer needs across diverse industrial sectors.

Top Strategies Used By Key Market Participants

Key players in the Industry 4.0 market prioritize platform based strategies that integrate hardware, software, and services to deliver comprehensive digital transformation solutions. Companies increasingly focus on developing open ecosystems that enable interoperability across diverse equipment and software environments while maintaining robust cybersecurity protections. Strategic acquisitions allow market leaders to rapidly expand capabilities in emerging areas such as artificial intelligence, digital twins, and autonomous systems. Partnerships with cloud providers facilitate scalable deployment models that balance edge processing requirements with centralized analytics capabilities. Investment in research and development ensures continuous innovation in predictive maintenance, quality optimization, and energy management applications. Companies also emphasize workforce enablement through intuitive human machine interfaces and collaborative robotics that enhance productivity while addressing skills gaps. These coordinated strategies enable market participants to deliver measurable operational improvements while adapting to evolving customer requirements and technological advancements.

RECENT MARKET NEWS

In April 2024, Dell, Hyundai, and Intel, technology and manufacturing leaders, collaborated to enhance Industry 4.0 AI capabilities by integrating NativeEdge and using edge AI and real time data to optimize production operations. This collaboration is anticipated to accelerate intelligent automation adoption and strengthen the Industry 4.0 Market presence.

MARKET SEGMENTATION

This research report on the global Industry 4.0 market has been segmented and sub-segmented based on technology, connectivity, end-user, and region.

By Technology

- Internet of Things

- Cloud Computing

- Artificial Intelligence

- Robotics

- Augmented and Virtual Reality

- Big Data and Analytics

- Cyber Security

- Machine Learning

- Others

By Connectivity

- Wired

- Wireless

- Mobile

- Others

By End-User

- Manufacturing

- Automotive

- Healthcare

- Aerospace

- Transportation

- Energy and Power

- Others

By Region

- North America

- The United States

- Canada

- Rest of North America

- Europe

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

- The Asia Pacific

- India

- Japan

- China

- Australia

- Singapore

- Malaysia

- South Korea

- New Zealand

- Southeast Asia

- Latin America

- Brazil

- Argentina

- Mexico

- Rest of LATAM

- The Middle East and Africa

- Saudi Arabia

- UAE

- Lebanon

- Jordan

- Cyprus

Frequently Asked Questions

What is the Industry 4.0 market?

The Industry 4.0 market comprises technologies and solutions that enable smart factories, automation, and real-time data exchange in manufacturing.

What technologies are included in Industry 4.0?

Key technologies include IoT, artificial intelligence (AI), robotics, digital twins, cloud computing, and industrial analytics.

What drives growth in the Industry 4.0 market?

Rising automation demand, digital transformation strategies, and the need for operational efficiency drive Industry 4.0 adoption.

How does Industry 4.0 benefit manufacturers?

It improves productivity, reduces downtime, enhances quality control, and enables predictive maintenance.

Which industries use Industry 4.0 solutions most?

Automotive, electronics, aerospace, consumer goods, and energy sectors are major adopters of Industry 4.0 technologies.

What role does IoT play in the Industry 4.0 market?

IoT connects machines, systems, and sensors to enable real-time monitoring and process optimization.

How does Industry 4.0 support predictive maintenance?

AI and sensor data analytics help forecast equipment failure and schedule maintenance before breakdowns occur.

Are small and medium enterprises (SMEs) adopting Industry 4.0?

Yes, SMEs are increasingly implementing scaled-down Industry 4.0 solutions to improve competitiveness.

What impact does Industry 4.0 have on the workforce?

It creates demand for digital skills while enabling human–machine collaboration and higher-value roles.

What challenges does the Industry 4.0 market face?

Data security concerns, high implementation costs, and skills gaps are significant market challenges.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com