- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

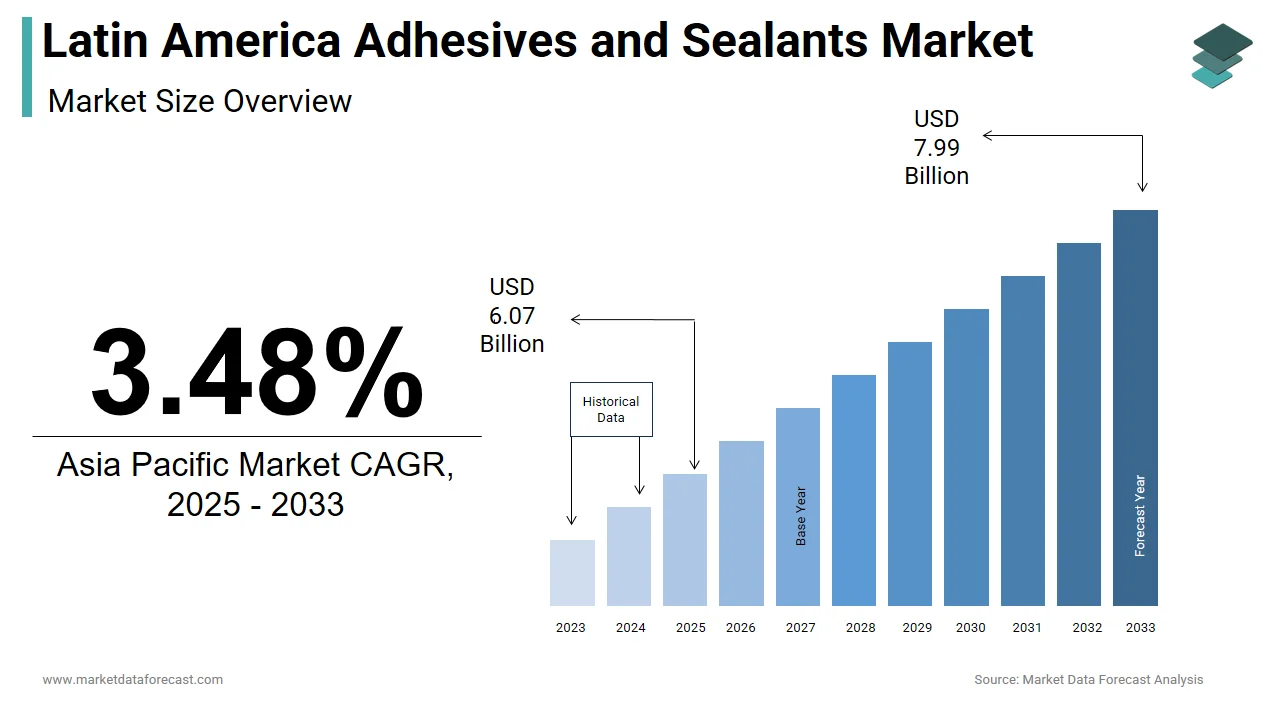

Market Size, 2025

$6.07 BnMarket Estimate, 2026

$6.28 BnMarket Forecast, 2034

$8.26 BnCAGR, 2026–2034

3.48%Latin America Adhesives and Sealants Market Summary

The Latin America adhesives and sealants market size was estimated at USD 6.28 billion in 2026 and is projected to reach USD 8.26 billion by 2034, growing at a CAGR of 3.48% from 2026 to 2034. Industrial growth, urban infrastructure development, and packaging expansion are boosting demand across construction, automotive, and consumer sectors.

Key Market Trends & Insights

- Brazil accounted for the largest share of 36.1% in 2024.

- Based on adhesive technology, the water-based adhesives led with 42.8% of total consumption in 2024.

- Based on adhesive technology, the reactive adhesives are the fastest-growing segment, expanding at a CAGR of 6.4%.

- Based on sealant resin type, silicone sealants dominated with a 35.7% share, while polyurethane sealants grew fastest at a 5.9% CAGR.

Market Size & Forecast

- 2025 Market Size: USD 6.07 Billion

- 2034 Projected Market Size: USD 8.26 Billion

- CAGR (2026 to 2034): 3.48%

- Brazil: Largest market in 2024

- Mexico: Key emerging market

Latin America Adhesives and Sealants Market Size

The size of the Latin America adhesives and sealants market was valued at USD 6.07 billion in 2025. This market is expected to grow at a CAGR of 3.48% from 2026 to 2034 and be worth USD 8.26 billion by 2034 from USD 6.28 billion in 2026.

The Latin America adhesives and sealants market covers a wide array of chemical formulations used for bonding, sealing, and protecting materials across diverse industries such as construction, automotive, packaging, and consumer goods. As industrialization accelerates and urban development expands, demand for high-performance adhesives and sealants has grown significantly. The construction sector remains a key consumer, with Brazil, Mexico, and Colombia investing heavily in residential and commercial infrastructure projects. As per the Inter-American Development Bank (IDB), a substantial smount was allocated for housing and non-residential construction across Latin America in 2023, directly influencing the need for durable sealants and structural adhesives. Besides, the rise in packaged goods production driven by domestic consumption and export demands has further boosted adhesive usage, particularly in flexible packaging applications.

MARKET DRIVERS

Growth in the Construction Industry

One of the primary drivers fueling the Latin America adhesives and sealants market is the sustained expansion of the construction industry. Governments across the region have prioritized infrastructure development, leading to increased demand for building materials, including high-performance adhesives and sealants. According to the study, construction activity in Brazil grew by 6.8% in 2023 compared to the previous year, supported by public investments under the "Casa Verde e Amarela" housing program. Adhesives are extensively used in flooring, tile installation, and panel bonding, while sealants play a crucial role in waterproofing and insulation. Colombia’s Fourth Generation Road Concessions Program also contributed to rising demand, with over USD 6.8 billion invested in infrastructure between 2021 and 2023.

Expansion of the Packaging Industry

The rapid expansion of the packaging industry is another significant driver of the Latin America adhesives and sealants market. With rising consumer spending and increasing exports of food, beverages, and pharmaceuticals, demand for flexible and rigid packaging solutions has surged. According to the Latin American Packaging Association (ALPA), the region's packaging industry grew by 5.4% in 2023, fueled by increased production in countries like Brazil, Mexico, and Argentina. Adhesives are essential in laminating films, carton sealing, and pouch manufacturing, particularly in flexible packaging where lightweight materials require strong bonding without compromising integrity. In Brazil alone, the Brazilian Association of Packaging (EMBRAPAQ) noted that flexible packaging production rose by 7% in 2023, with water-based adhesives gaining preference due to their lower environmental impact. Similarly, in Mexico, the National Association of the Packaging Industry (ANIQ) reported that corrugated box production expanded by 8% during the same period, requiring high-strength adhesives for board lamination.

MARKET RESTRAINTS

Volatility in Raw Material Prices

A major restraint affecting the Latin America adhesives and sealants market is the volatility in raw material prices, particularly petrochemical derivatives such as acrylics, polyurethanes, and epoxies. These feedstocks are essential for producing synthetic adhesives and high-performance sealants, yet their costs fluctuate based on global crude oil prices and supply chain disruptions. In Brazil, the Brazilian Chemical Industry Association (ABIQUIM) reported that resin prices rose by up to 18% in 2023, forcing formulators to adjust pricing strategies and absorb part of the cost burden. Mexico faced similar challenges, with importers noting a 15% increase in polyurethane raw material costs due to supply shortages from Asian suppliers. Additionally, Argentina experienced inflationary pressures exceeding 90% in 2023, according to the International Monetary Fund (IMF), which further complicated procurement and inventory management for local adhesive producers.

Regulatory Compliance and Environmental Pressures

Environmental regulations and compliance requirements pose a significant challenge to the Latin America adhesives and sealants market. Governments in the region are increasingly implementing restrictions on volatile organic compound (VOC) emissions and promoting the use of eco-friendly alternatives. In 2023, Chile introduced stricter air quality standards under the Ministry of Environment, mandating a reduction in solvent-based adhesive usage in industrial applications. Similarly, Brazil’s National Environmental Council (CONAMA) updated Resolution No. 498 to impose tighter emission limits for adhesive manufacturing facilities, compelling companies to invest in cleaner technologies. These regulatory shifts increase production costs and necessitate reformulations, posing financial and technical barriers for smaller manufacturers.

MARKET OPPORTUNITIES

Rising Demand for Sustainable and Bio-Based Adhesives

The increasing demand for sustainable and bio-based adhesives presents a substantial opportunity for the Latin America adhesives and sealants market. In Brazil, Embrapa launched new adhesive formulations derived from sugarcane ethanol, offering a viable alternative to petroleum-based products. Apart from these, multinational adhesive suppliers such as Henkel and BASF have expanded their presence in Latin America by introducing eco-friendly product lines tailored to regional markets.

Growth in Automotive and Transportation Manufacturing

The expansion of the automotive and transportation manufacturing sector offers a significant growth avenue for the Latin America adhesives and sealants market. As vehicle production increases and electric mobility gains traction, demand for advanced bonding and sealing solutions rises correspondingly. According to the Brazilian Automobile Manufacturers Association (ANFAVEA), automotive production in Brazil grew by 10.4% in 2023, with over 2.7 million units manufactured domestically. Adhesives play a crucial role in modern vehicle assembly, replacing traditional mechanical fasteners to reduce weight and improve structural integrity. Additionally, the rise in electric vehicle (EV) production has spurred demand for thermally conductive adhesives used in battery assembly and electronic component integration. As per the International Energy Agency (IEA), EV sales in Latin America increased by 25% in 2023, with Chile and Colombia leading adoption efforts. Furthermore, in Argentina, YPF partnered with local automotive firms to develop lightweight adhesive solutions aimed at improving fuel efficiency and reducing carbon emissions.

MARKET CHALLENGES

Supply Chain Disruptions and Logistics Constraints

Supply chain inefficiencies and logistical bottlenecks present a persistent challenge for the Latin America adhesives and sealants market. According to the World Bank Logistics Performance Index (LPI), several Latin American countries rank below global averages in terms of customs efficiency and infrastructure reliability. These constraints not only inflate operational expenses but also create inconsistencies in supply, making it difficult for manufacturers and distributors to maintain steady inventory levels and meet customer demand efficiently.

Regulatory Uncertainty and Policy Instability

Regulatory uncertainty and policy instability pose ongoing challenges for the Latin America adhesives and sealants market, as inconsistent government directives and shifting taxation policies disrupt investment planning and production activities. For instance, in Argentina, the Central Bank imposed multiple foreign exchange controls in 2023, complicating raw material imports and causing periodic shortages of specialty adhesives. According to the International Trade Centre (ITC), Argentina’s import licensing system for chemical products underwent three major revisions between 2021 and 2023, adding administrative complexity. Similarly, in Mexico, recent amendments to environmental legislation have affected adhesive manufacturers, particularly those using solvent-based formulations. In addition, political transitions in countries like Peru and Chile have resulted in abrupt shifts in industrial policies, delaying approvals for new adhesive production facilities.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Adhesive Technology, Sealant Resin Type, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | Brazil, Mexico, Argentina, Chile, Rest of Latin America |

| Market Leaders Profiled | Henkel AG & Co. KGaA, H.B. Fuller Company, Sika AG, Arkema (Bostik), and 3M. |

SEGMENTAL ANALYSIS

By Adhesive Technology Insights

The water-based adhesives segment dominated the Latin America adhesives and sealants market by capturing a 42.8% of total consumption in 2024. This is primarily driven by increasing environmental awareness and regulatory pressure to reduce volatile organic compound (VOC) emissions. Countries such as Brazil and Mexico have implemented stricter air quality standards, encouraging manufacturers and end-users to shift away from solvent-based alternatives. Apart from these, the packaging industry, particularly flexible packaging, has been a major consumer of water-based adhesives due to their compatibility with food-safe materials and ease of application.

Reactive adhesives are emerging as the fastest-growing segment in the Latin America adhesives and sealants market, projected to expand at a CAGR of approximately 6.4%. This is fueled by increasing demand from high-performance sectors such as automotive, electronics, and construction, where strong bonding, durability, and resistance to extreme conditions are essential. According to the Brazilian Automobile Manufacturers Association (ANFAVEA), automotive production in Brazil increased by 10.4% in 2023, with structural adhesives replacing traditional fasteners to reduce vehicle weight and improve fuel efficiency. The International Energy Agency (IEA) reported a significant year-on-year increase in EV sales across Latin America in 2023, reinforcing this trend.

By Sealant Resin Type Insights

Silicone sealants held the largest share of the Latin America sealants market by accounting for a 35.7% of total consumption in 2024. Their dominance is due to widespread use in construction, automotive, and electronics industries due to superior properties such as temperature resistance, flexibility, and long-term durability. Brazil’s road freight transport accounts for a notable share of all cargo movement, necessitating durable infrastructure components. Chile also encouraged the use of silicone sealants in earthquake-prone areas due to their ability to absorb structural movement without cracking.

The polyurethane sealants are witnessing the highest growth within the Latin America sealants market, expanding at a CAGR of approximately 5.9% from 2025 to 2033. This quick development is attributed to their increasing use in construction, automotive assembly, and industrial applications where elasticity and chemical resistance are critical. Like, polyurethane-based sealants are now standard for joint sealing in newly constructed highways due to their superior load-bearing capacity and long service life. The Organization for Economic Co-operation and Development (OECD) highlighted that Latin American countries are investing heavily in energy infrastructure, supporting demand for corrosion-resistant sealants. Chile also endorsed their use in public transit vehicles for vibration damping and noise reduction.

COUNTRY-LEVEL ANALYSIS

Brazil had the dominant position in the Latin America adhesives and sealants market by contributing a 36.1% of total regional consumption in 2024. As the continent’s largest economy and most populous nation, Brazil's extensive industrial base and growing construction sector drive significant demand for adhesives and sealants. The country’s packaging industry alone expanded, with flexible packaging increasingly relying on water-based and reactive adhesive technologies. Despite supply chain challenges and fluctuating raw material prices, Brazil remains the core market for adhesives and sealants in Latin America, supported by continuous investment in infrastructure and manufacturing.

Mexico capturing a notable share of total regional consumption. The country benefits from a strong industrial foundation, particularly in automotive, electronics, and packaging sectors that drive consistent demand for advanced adhesive and sealant solutions. The Mexican Automotive Industry Association (AMIA) reported that light vehicle production exceeded 3.1 million units in 2023, reinforcing the need for structural adhesives in assembly processes. Although import dependency and regulatory changes pose challenges, Mexico’s strategic location and manufacturing prowess ensure sustained growth in the adhesives and sealants market.

Argentina driven by steady investments in construction, transportation, and consumer goods manufacturing. YPF, the country's leading energy firm, has also engaged in developing environmentally adapted adhesive products tailored for green infrastructure initiatives. Despite economic volatility, Argentina maintains a stable presence in the Latin American adhesives and sealants market, supported by government-backed infrastructure programs and growing industrial activity.

Chile is propelled by structured infrastructure planning and increasing adoption of high-performance bonding and sealing solutions. The Santiago Metropolitan Region executed over 1,200 kilometers of road maintenance projects between 2021 and 2023, requiring more than 400,000 tons of specialized sealants for pavement joints and expansion gaps. Additionally, the Chilean Copper Commission (COCHILCO) emphasized the importance of corrosion-resistant sealants in mining equipment, where exposure to extreme conditions necessitates durable protective coatings.

The remaining Latin American countries collectively account for a considerable share of regional adhesives and sealants consumption, with Colombia, Peru, Ecuador, and Central American nations playing pivotal roles in shaping demand patterns. Peru has intensified road development efforts, particularly along the Southern and Northern Interoceanic Highways, which require high-grade sealants resistant to varying climatic conditions. Collectively, these nations contribute significantly to the broader Latin American adhesives and sealants landscape.

COMPETITIVE LANDSCAPE

The Latin America adhesives and sealants market exhibits a competitive structure characterized by the coexistence of multinational corporations and regional players, each vying for a stronger foothold through differentiated offerings and strategic initiatives. Global leaders such as Henkel, Sika, and 3M dominate due to their extensive product portfolios, technological expertise, and established distribution networks. However, regional manufacturers and specialty formulators are gaining traction by offering cost-effective solutions tailored to local industry needs. The competition intensifies in countries like Brazil and Mexico, where industrial activity and infrastructure development drive consistent demand. Product innovation remains a key battleground, with companies striving to develop sustainable and high-performance formulations that align with environmental regulations and evolving end-user expectations. Additionally, pricing strategies, supply chain resilience, and after-sales technical support play crucial roles in differentiating market participants. As demand diversifies across construction, automotive, packaging, and electronics sectors, companies must continuously adapt to shifting dynamics, ensuring agility in product development, customer engagement, and operational efficiency to maintain and expand their market presence.

KEY MARKET PLAYERS

Noteworthy Companies dominating the Latin America Adhesives and sealants market profiled in the report are

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Sika AG

- Arkema (Bostik)

- 3M

TOP LEADING PLAYERS IN THE MARKET

Henkel is a leading global player with a strong presence in the Latin America adhesives and sealants market, offering a comprehensive portfolio across industrial, consumer, and automotive applications. The company leverages its well-established brand recognition and technological expertise to cater to diverse end-use sectors. In Latin America, Henkel focuses on innovation and sustainability, introducing eco-friendly formulations that align with regional regulatory trends. Its extensive distribution network and localized production facilities allow for efficient supply chain management. Through continuous investment in R&D and customer engagement, Henkel maintains a competitive edge in key markets such as Brazil and Mexico.

Sika plays a pivotal role in shaping the Latin America adhesives and sealants landscape by providing high-performance products tailored for construction, infrastructure, and transportation industries. The company has strategically expanded its footprint through acquisitions and greenfield investments in the region. Sika’s emphasis on product durability, energy efficiency, and compliance with environmental standards positions it as a preferred supplier in both public and private sector projects. With a strong technical support system and localized service centers, Sika enhances customer satisfaction and project execution quality. Its commitment to sustainable development supports long-term growth in emerging Latin American economies.

3M is a major contributor to the Latin America adhesives and sealants market, known for its innovative product lines used in electronics, healthcare, transportation, and general industrial applications. In Latin America, 3M emphasizes customization, adapting formulations to meet regional climatic conditions and industry-specific needs. Its robust brand reputation and long-standing partnerships with local distributors enhance market penetration. By focusing on application-specific innovation and customer collaboration, 3M strengthens its position as a technology-driven leader in the region.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the primary strategies adopted by leading players in the Latin America adhesives and sealants market is product innovation and formulation differentiation. Companies are investing heavily in research and development to create high-performance, environmentally friendly, and application-specific solutions that meet evolving industry demands and regulatory requirements. This approach allows them to cater to niche markets while maintaining a competitive edge.

Another critical strategy involves expanding production and distribution capabilities within the region. By establishing or expanding local manufacturing units and logistics networks, companies reduce dependency on imports, lower costs, and improve response times to customer needs. These localized operations also enable better alignment with regional supply chains and facilitate quicker adaptation to market fluctuations.

Lastly, firms are increasingly engaging in strategic partnerships, collaborations, and acquisitions to strengthen their market position. By partnering with regional players or acquiring smaller manufacturers, companies can access new customer bases, enhance technical expertise, and integrate complementary product portfolios, thereby reinforcing their presence in key Latin American markets.

RECENT MARKET DEVELOPMENTS

- In February 2023, Henkel launched a new line of bio-based adhesives specifically designed for flexible packaging applications in Latin America, responding to increasing demand for sustainable alternatives in the food and beverage industry.

- In August 2023, Sika opened a new technical center in São Paulo, Brazil, aimed at enhancing local R&D capabilities and supporting customers with customized adhesive and sealant solutions for construction and infrastructure projects.

- In November 2023, 3M partnered with a Brazilian industrial distributor to expand its reach in the automotive and electronics sectors, improving accessibility to specialized adhesive tapes and bonding solutions across South America.

- In March 2024, a leading European sealant manufacturer entered into a joint venture with a Mexican chemical firm to establish a regional production facility focused on silicone and polyurethane sealants for construction and transportation applications.

- In July 2024, an international adhesives supplier acquired a Chilean distributor specializing in industrial bonding solutions, aiming to strengthen its market presence and provide faster, more localized service across Andean markets.

MARKET SEGMENTATION

This Latin America adhesives and sealants market research report is segmented and sub-segmented into the following categories.

By Adhesive Technology

- Water-based

- Solvent-based

- Hot-melt

- Reactive

By Sealant Resin Type

- Silicone

- Polyurethane

- Plastisol

- Emulsion

- Polysulfide

- Butyl

By Country

- Brazil

- Mexico

- Argentina

- Chile

- Rest of Latin America