Latin America Data Center Colocation Market Size, Share, Trends & Growth Forecast Report By Data Center Size (Large, Massive, Medium, Mega, Small), Tier Type, Absorption Status, And Country (Brazil, Mexico, Argentina, Chile, Rest Of Latin America), Industry Analysis From 2025 To 2033

Latin America Data Center Colocation Market Size

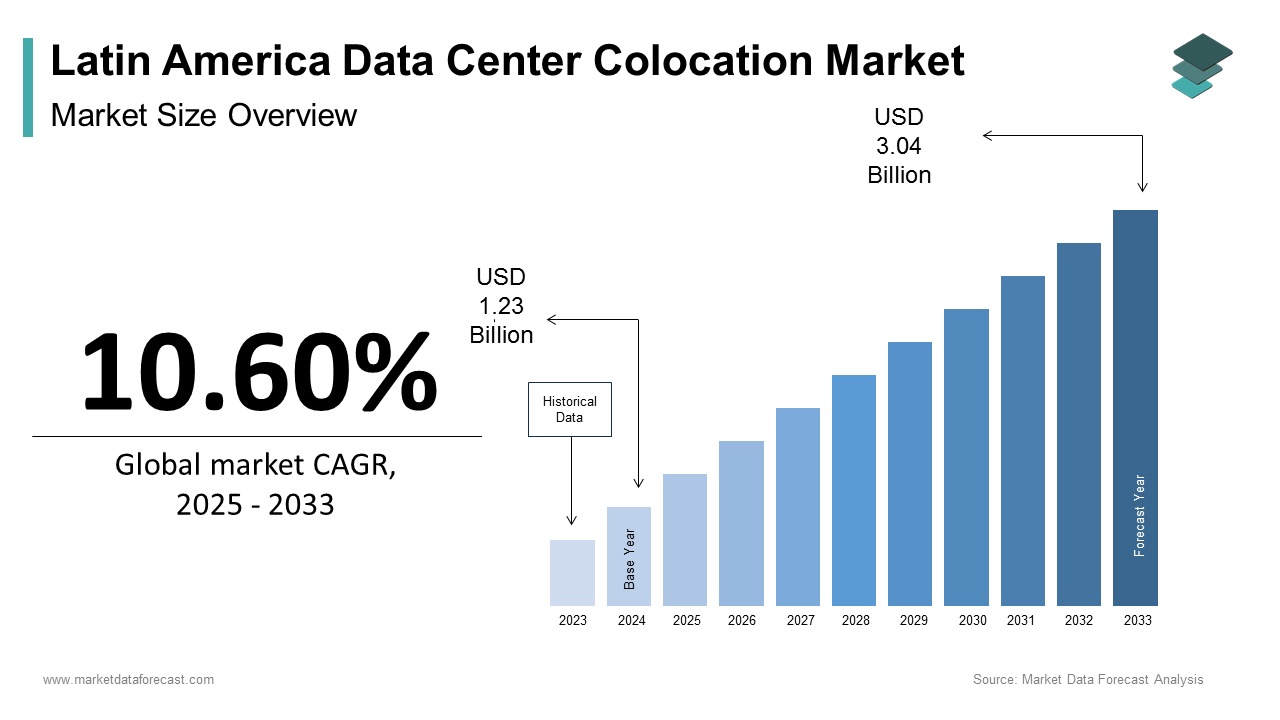

The Latin America Data Center Colocation Market Size is estimated to grow from USD 1.23 billion in 2024 to USD 3.04 billion in 2033, representing a CAGR of 10.60% during the forecast period.

Data center colocation is are third-party data center facilities that offer space, power, cooling, and security for businesses to host their IT infrastructure. This model has gained traction as enterprises seek scalable and cost-effective alternatives to building and maintaining in-house data centers. The region’s increasing digitalization, expansion of cloud services, and rising demand for low-latency connectivity have driven investment in colocation facilities across key economic hubs such as São Paulo, Mexico City, and Bogotá. In Brazil, government initiatives like the National Broadband Plan (Plano Nacional de Banda Larga) have played a pivotal role in expanding high-speed internet access, which in turn supports colocation growth. Moreover, growing concerns around cybersecurity and data sovereignty have influenced regional policies, shaping how data is stored and processed within national borders.

MARKET DRIVERS

Increasing Digital Transformation Across Industries

The accelerating pace of digital transformation across industries such as banking, healthcare, retail, and government is one of the primary drivers of the Latin America data center colocation market. Enterprises are increasingly shifting from legacy systems to cloud-enabled, data-intensive applications, necessitating secure and scalable hosting environments.

In Brazil, financial institutions are leveraging colocation services to deploy real-time transaction processing and AI-based fraud detection systems. Moreover, public sector agencies are also embracing colocation to modernize administrative functions and enhance citizen services. As per the Ministry of Science, Technology, and Innovation (MCTI), Brazil’s federal government migrated over 30% of its digital services to colocation centers in 2023, improving data resilience and disaster recovery capabilities.

Surge in Cloud Adoption and Hybrid IT Strategies

The rapid adoption of cloud computing and hybrid IT strategies among enterprises seeking greater flexibility and scalability is another significant driver of the Latin America data center colocation market. As companies move away from traditional on-premises data centers, they are increasingly relying on colocation providers to house mission-critical infrastructure while integrating with public and private cloud platforms. According to Gartner, nearly 50% of Latin American enterprises had adopted a hybrid cloud strategy by the end of 2023, up from 28% in 2021. In Brazil, multinational firms and local startups alike are leveraging colocation to facilitate direct interconnection with cloud service providers like AWS, Microsoft Azure, and Google Cloud. Furthermore, the rise of edge computing is reinforcing the need for distributed colocation sites closer to end-users. These trends show the growing interdependence between cloud ecosystems and colocation infrastructure in supporting digital evolution across the region.

MARKET RESTRAINTS

High Capital Investment and Operational Costs

The high capital investment and ongoing operational costs associated with developing and maintaining Tier III and Tier IV-standard facilities are a major restraint affecting the Latin American data center colocation market. Unlike North America or Europe, where mature markets benefit from economies of scale and standardized infrastructure, Latin America faces higher construction, energy, and maintenance expenses due to inconsistent utility availability and regulatory inefficiencies. In Argentina, despite growing demand for digital infrastructure, high inflation and currency volatility have made long-term investments in data centers financially risky. Moreover, labor costs and import duties on critical components such as uninterruptible power supplies (UPS) and cooling systems further inflate development budgets. These financial barriers hinder market expansion and slow down the pace of technological advancement in several key countries.

Regulatory Fragmentation and Data Sovereignty Concerns

Regulatory fragmentation and data sovereignty concerns present a significant challenge to the Latin America data center colocation market. Each country in the region has distinct legal frameworks governing data localization, cybersecurity, and cross-border data transfers, complicating compliance for multinational firms and service providers. In Brazil, the implementation of the General Data Protection Law (LGPD) in 2020 introduced stricter requirements for data handling and storage, prompting companies to invest in localized colocation solutions. As per Deloitte, compliance-related expenditures accounted for nearly 15% of total IT budgets for foreign firms operating in Brazil in 2023, slowing down adoption rates. Meanwhile, in Mexico, recent amendments to the Federal Law on the Protection of Personal Data Held by Private Parties imposed additional consent and encryption mandates, affecting how colocation providers manage customer data. Also, political instability in certain countries introduces unpredictability in policy enforcement.

MARKET OPPORTUNITIES

Expansion of Edge Computing and 5G Infrastructure

The expansion of edge computing and 5G infrastructure, which is driving demand for decentralized, low-latency data processing capabilities, is a significant opportunity emerging in the Latin America data center colocation market. With the rollout of 5G networks gaining momentum across Brazil, Mexico, and Colombia, enterprises are seeking proximity-based colocation facilities to support real-time applications such as IoT, autonomous vehicles, and industrial automation. In Brazil, telecommunications operators are partnering with colocation providers to deploy micro data centers in urban and semi-urban areas, reducing latency and improving service reliability. As per the Anatel (Brazilian Communications Agency), telecom firms invested over USD 2 billion in 5G network expansion in 2023, directly influencing colocation demand. Moreover, industrial sectors such as logistics and manufacturing are increasingly adopting edge-based analytics to optimize supply chain operations and production efficiency. These advancements position edge colocation as a transformative force in the region's digital infrastructure landscape.

Rise of Green and Sustainable Data Centers

The growing emphasis on sustainability presents a major opportunity for the Latin American data center colocation market, particularly through the development of green data centers powered by renewable energy sources. Governments and private sector players are increasingly prioritizing environmentally responsible infrastructure, aligning with global ESG (Environmental, Social, and Governance) goals.

In Chile, abundant solar and wind energy resources have enabled colocation providers to adopt clean energy-powered facilities, attracting international cloud providers looking to reduce their carbon footprint. As per the Chilean Ministry of Energy, over 70% of electricity generated in northern Chile came from renewable sources in 2023, making it an attractive location for sustainable data center investments. Similarly, in Brazil, the government introduced tax incentives for companies utilizing hydroelectric power in their colocation facilities, encouraging eco-friendly expansion. Colombia has also seen rising interest from investors focused on green colocation, with Medellín and Bogotá emerging as key locations for LEED-certified data centers. These developments indicate a strong trajectory for green colocation in Latin America.

MARKET CHALLENGES

Limited Availability of Skilled Workforce and Technical Expertise

The limited availability of skilled professionals and technical expertise required to design, operate, and maintain advanced data center infrastructure is a major challenge facing the Latin America data center colocation market. Despite the growing demand for colocation services, there remains a significant gap in trained personnel capable of managing complex IT ecosystems, cybersecurity protocols, and high-density server environments. This shortage is even more pronounced in smaller economies like Ecuador and Paraguay, where training programs and certifications remain underdeveloped. Moreover, competition for skilled workers is intensifying as global tech firms expand their presence in the region. Without targeted investments in education and professional training, the region may struggle to keep pace with global colocation market advancements.

Unreliable Power Supply and Grid Instability

Unreliable power supply and grid instability pose a persistent challenge to the Latin America data center colocation market, particularly in countries with aging electrical infrastructure and intermittent energy distribution. Unlike developed regions with consistent power grids, several Latin American nations experience frequent blackouts, voltage fluctuations, and delays in utility expansion, making continuous data center operations difficult without substantial backup systems. To mitigate these risks, colocation providers are investing heavily in redundant power systems, including diesel generators, battery backups, and microgrids. However, these additional measures increase operational costs and complexity.

Rising Competition from Hyperscalers Building Own Facilities

An emerging challenge for the Latin American data center colocation market is the increasing tendency of hyperscale cloud providers to build and operate their dedicated data centers rather than rely on third-party colocation providers. Companies like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud are expanding their regional footprints, establishing owned facilities that offer enhanced control over performance, security, and compliance. In Brazil, AWS opened a new availability zone in São Paulo in early 2023, while Google Cloud expanded its South America region with additional computing capacity. This movement limits revenue opportunities for traditional colocation firms, especially those lacking the ability to offer premium-tier services such as ultra-low latency interconnection and multi-cloud integration. As per Gartner, enterprises previously reliant on colocation for cloud adjacency are now opting for hyperscaler-owned facilities that provide built-in cloud integration, further intensifying market competition.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 10.60% |

| Segments Covered | By Data Center Size, Tier Type, Absorption Status, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | Brazil, Mexico, Argentina, Chile and Rest Of Latin America |

| Market Leaders Profiled | Equinix, Ascenty, ODATA, KIO Networks, Axtel, Telefónica, CenturyLink, Nabiax, Scala Data Centers, Lumen Technologies |

SEGMENTAL ANALYSIS

By Data Center Size Insights

The Medium-sized data centers segment dominated the market by accounting for 35.5% in 2024. This dominance of the medium-sized data centers segment is primarily attributed to the growing demand from mid-sized enterprises that require scalable infrastructure without the high costs associated with large or mega facilities. These facilities often serve as entry points for businesses transitioning from on-premises servers to outsourced IT infrastructure. Also, in Mexico, medium-sized colocation centers are favored by telecom operators and cloud service resellers seeking localized presence without committing to massive investments. Moreover, these facilities offer a balanced mix of performance, redundancy, and affordability, making them ideal for hybrid IT strategies.

The fastest-growing segment in the Latin America data center colocation market is the Mega Data Centers category, which is projected to expand at a CAGR of 19.2%. This rapid expansion is fueled by increasing demand from hyperscalers, multinational corporations, and government-led digital infrastructure programs requiring high-capacity, ultra-reliable hosting environments. In Brazil, hyperscale providers like AWS, Google Cloud, and Microsoft Azure have been expanding their presence through mega data center partnerships. Mexico has also seen a surge in mega data center development, with América Móvil and Oracle investing heavily in next-generation facilities to support AI-driven applications and edge computing. Also, government-backed digital transformation projects have spurred mega data center investments. These developments show the pivotal role of mega facilities in shaping the future of Latin America's digital infrastructure ecosystem.

By Tier Type Insights

The Tier 3 segment held the largest share of the Latin America data center colocation market by contributing 52.3% in 2023. This lead position is due to its balance between reliability, uptime, and cost-efficiency, making it the preferred choice for enterprises requiring high availability without the exorbitant costs of Tier 4 facilities. In Brazil, Tier 3 data centers have become the standard for financial institutions, cloud service providers, and e-commerce platforms seeking resilient infrastructure.

The Tier 4 segment is the fastest-growing tier classification in the Latin America data center colocation market and is projected to expand at a CAGR of 17.8%. The increasing demand for ultra-high-availability infrastructure from hyperscalers, government agencies, and mission-critical financial institutions that cannot tolerate any downtime is one of the factors driving the Tier 4 segment. Also, Mexico has also witnessed rising interest in Tier 4 infrastructure, particularly from U.S.-based enterprises establishing secondary data centers in the country for disaster recovery and business continuity planning. Furthermore, Chile has emerged as a Tier 4 investment hotspot due to its stable political environment and abundant renewable energy resources.

By Absorption Status Insights

The utilized segment commanded the market by capturing 68.5% of available colocation space in 2024. This high absorption rate reflects strong demand from enterprises seeking immediate access to secure, scalable infrastructure, particularly in urban centers where colocation capacity is limited and highly competitive. Also, in Mexico, the occupancy of colocation facilities in Mexico City and Monterrey surpassed 70% in 2023, as per AMIPCI (Mexican Internet Association). The rise of digital banking, e-commerce, and remote work has intensified demand for hosted infrastructure, pushing utilization rates beyond initial projections.

The Non-Utilized Space segment is the fastest-growing segment in the Latin America data center colocation market and is projected to expand at a CAGR of 15.4%. While currently underutilized, this segment represents significant potential for future deployment, particularly in emerging markets and second-tier cities where digital infrastructure is still evolving. The developments suggest that non-utilized space will play a critical role in shaping the region’s colocation landscape as enterprise adoption accelerates.

REGIONAL ANALYSIS

Brazil Data Center Colocation Market Insights

Brazil held the largest share of the Latin American data center colocation market, accounting for 33.8% in 2024. As the most digitally advanced economy in the region, Brazil benefits from high internet penetration, strong regulatory frameworks, and a rapidly expanding tech ecosystem that drives continuous demand for reliable and scalable data hosting solutions. The country’s financial institutions have increasingly adopted colocation to comply with LGPD (General Data Protection Law) and support real-time transaction processing, as noted by the Central Bank of Brazil. Telecom operators have also played a crucial role in market expansion. In addition, São Paulo has become a key interconnection point for global cloud providers, with AWS, Microsoft Azure, and Google Cloud establishing direct links to local colocation facilities, reinforcing Brazil’s leadership in the regional colocation landscape.

Mexico Data Center Colocation Market Insights

Mexico has experienced rapid colocation adoption driven by proximity to North American markets, growing cloud dependency, and increasing digital transformation across multiple industries. The country’s strategic location makes it an attractive destination for U.S.-based enterprises seeking cross-border data residency compliance while maintaining low-latency access to Latin American customers. Telecom operators and hyperscalers have played a central role in driving colocation growth. Moreover, the Mexican government has introduced regulatory sandboxes and tax incentives to encourage further colocation investment, strengthening the country’s position as a key player in the regional colocation ecosystem.

Argentina has demonstrated steady progress in digital infrastructure development, supported by growing demand from financial institutions, startups, and government agencies. The Argentine government has taken steps to attract foreign investment in digital infrastructure. Moreover, academic institutions like Universidad de Buenos Aires have partnered with private providers to develop research-driven data hosting solutions, indicating broader institutional support for market expansion.

Chile Data Center Colocation Market Insights

Chile has become an attractive destination for colocation investments, particularly in Santiago, which serves as a regional technology and financial services hub. The financial sector has been a major contributor, with banks such as BancoEstado and Itaú Chileno leveraging colocation for enhanced data security and disaster recovery capabilities. In addition, Chile’s renewable energy advantage has made it an appealing location for sustainable data center operations.

Rest of Latin America Data Center Colocation Market Insights

The rest of Latin America encompasses countries such as Colombia, Peru, Ecuador, and Central American nations. While individually these markets are smaller, they are experiencing notable growth driven by increasing internet penetration, government-led digital infrastructure projects, and expanding cloud adoption among SMEs. Colombia has emerged as a key growth engine in the Andean region, with Bogotá and Medellín serving as digital infrastructure hotspots. Peru has also demonstrated strong momentum, with Lima becoming a regional data center hub. Furthermore, Central American countries such as Costa Rica and Panama are attracting colocation investments due to their favorable business climates and strategic positioning within North-South digital corridors.

LEADING PLAYERS IN THE LATIN AMERICA DATA CENTER COLOCATION MARKET

One of the leading players in the Latin American data center colocation market is Digital Realty, a U.S.-based global provider with a strong presence in Brazil and Mexico. Digital Realty offers carrier-neutral facilities equipped with high-density power, scalable infrastructure, and direct interconnections to major cloud providers. Its contribution to the global market includes pioneering multi-tenant data center ecosystems and promoting hybrid IT strategies that bridge enterprise and cloud environments.

Another major player is Equinix, which has significantly expanded its footprint in Latin America, particularly in São Paulo and Mexico City. Equinix provides high-performance colocation services tailored for multinational enterprises, financial institutions, and cloud providers. Its global reach and extensive interconnection capabilities make it a key enabler of digital transformation in the region, facilitating seamless integration with global networks and cloud ecosystems.

Telehouse South America, part of the KDDI group, plays a vital role in the Latin American colocation landscape. With a focus on enterprise-grade infrastructure and managed colocation services, Telehouse supports data-intensive industries such as finance, healthcare, and manufacturing. Its contributions to the global market include advancing carrier-neutral peering environments and enhancing data sovereignty through localized hosting solutions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

A primary strategy employed by key players in the Latin America data center colocation market is expanding regional footprints through strategic acquisitions and greenfield developments, particularly in high-growth urban centers such as São Paulo, Mexico City, and Bogotá. Companies are investing in new facilities and upgrading existing ones to cater to the rising demand for cloud adjacency and low-latency interconnection.

Another critical tactic is enhancing interconnectivity and cloud integration capabilities, allowing enterprises to deploy hybrid IT architectures seamlessly. Leading colocation providers are forming direct peering agreements with major cloud providers like AWS, Microsoft Azure, and Google Cloud to offer optimized data pathways and improved network performance for enterprise clients.

Lastly, adopting sustainability-driven data center designs and renewable energy sourcing has become essential for maintaining long-term competitiveness. Market leaders are integrating green building certifications, energy-efficient cooling systems, and carbon offset programs to align with global ESG goals and attract environmentally conscious enterprises seeking responsible digital infrastructure partners.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players of the Latin America Data Center colocation Market include Equinix, Ascenty, ODATA, KIO Networks, Axtel, Telefónica, CenturyLink, Nabiax, Scala Data Centers, Lumen Technologies

The Latin America data center colocation market is characterized by intense competition between global colocation giants, regional operators, and local providers vying for market share. International players such as Digital Realty, Equinix, and NTT Global Data Centers coexist with regional firms like Ascenty, TerraNova, and Teclógica, all competing through differentiated service offerings, geographic expansion, and specialized infrastructure capabilities.

This dynamic environment fosters continuous innovation, with companies launching new data center campuses, investing in edge computing-ready facilities, and offering tailored solutions for specific verticals such as finance, healthcare, and e-commerce. The increasing influence of hyperscalers and cloud service providers further intensifies competition, as colocation vendors strive to offer direct cloud interconnection, low-latency hosting, and compliance-aligned data residency options.

Additionally, government-backed digital transformation initiatives are reshaping the competitive landscape, prompting colocation providers to align with national broadband expansion plans and data localization mandates. As consumer and enterprise reliance on digital services grows, the ability to deliver high-uptime, scalable, and secure infrastructure will be a decisive factor in securing long-term success in this rapidly evolving market.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Digital Realty announced the expansion of its São Paulo campus with a new phase dedicated to hybrid cloud integration, aiming to enhance interconnection capabilities and support enterprise migration to multi-cloud environments.

- In August 2023, Equinix acquired a Tier 3 colocation facility in Mexico City, strengthening its presence in the country and providing a direct interconnection point for U.S.-based enterprises seeking regional expansion opportunities.

- In March 2024, Ascenty launched a new Tier 4 data center in Bogotá, Colombia, designed to support government and financial institutions requiring high-security, low-latency infrastructure for mission-critical operations.

- In November 2023, NTT Global Data Centers entered a strategic partnership with a Brazilian cloud service provider to offer integrated colocation and managed services, enhancing value propositions for enterprise clients seeking full-stack digital infrastructure.

- In May 2024, Telehouse South America expanded its interconnection offerings in Santiago, Chile, aligning with regional cloud adoption trends and supporting hyperscaler expansion into South America’s southern corridor.

MARKET SEGMENTATION

This research report on the Latin America Data Center Colocation Market has been segmented and sub-segmented based on data center size, tier type, absorption status, and region.

By Data Center Size

- Large

- Massive

- Medium

- Mega

- Small

By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

By Absorption Status

- Non-Utilized

- Utilized

By Region

- Brazil

- Mexico

- Argentina

- Chile

- Rest of Latin America

Frequently Asked Questions

1. What is driving the growth of the data center colocation market in Latin America?

Key growth drivers include Rising demand for cloud computing and digital services, increasing data consumption due to mobile and internet penetration, Government and enterprise digital transformation initiatives, and Cost-efficiency and scalability benefits of colocation

2. Which countries are leading the market in Latin America?

Top contributing countries include Brazil (the largest market), Mexico, Chile, and Colombia. These nations have better connectivity infrastructure and high enterprise IT adoption.

3. What are the major trends shaping the market?

Rise of hyperscale and edge data centers, Increased use of renewable energy and green data center initiatives, Growth of hybrid cloud deployments, and Partnerships and acquisitions between telecom and data center providers

4. What challenges does the Latin America colocation market face?

High energy costs and limited power availability in some regions, Security and regulatory compliance concerns, Infrastructure disparity between countries, and fluctuating political and economic conditions

5. What are the key services offered in colocation facilities?

Retail and wholesale colocation, Rack space leasing (shared or private cages), Power and cooling infrastructure, Physical and cybersecurity services, and Remote hands and managed services

6. Who are the leading players in the Latin America data center colocation market?

Major providers include Equinix, Ascenty, ODATA, KIO Networks, Axtel, Telefónica, CenturyLink, Nabiax, Scala Data Centers, Lumen Technologies

7. How is cloud computing influencing the colocation market?

The shift toward hybrid and multi-cloud strategies is increasing the need for carrier-neutral colocation facilities that offer direct cloud connectivity, especially for SaaS and fintech providers.

8. What industries are the top adopters of colocation services?

Key industries include Banking, Financial Services & Insurance (BFSI), Healthcare, E-commerce and Retail, Telecom and IT services, Media & Entertainment

9. What is the future outlook for the Latin America data center colocation market?

The market is projected to grow at a CAGR of over 8–10% through 2030, driven by 5G rollouts, IoT expansion, and increased data localization policies, with continued investment in green and modular data centers.

10. How is sustainability impacting the Latin America data center colocation market?

Sustainability is becoming a key focus, with colocation providers increasingly investing in energy-efficient infrastructure, green building certifications, and the use of renewable energy sources. This trend is driven by customer demand for eco-friendly operations, regulatory pressure, and global corporate ESG commitments.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com