Global Maize Seed Market Size, Share, Trends and Growth Analysis Report, Segmented By Type (Conventional Seeds, GM seeds, Non-GM Seeds), Variety (Open Pollinated Varieties and Hybrids), Application (Food, Animal Feed, Industrial Applications, Others), and Region (North America, Europe, Asia-Pacific, Middle East & Africa, Latin America), Industry Analysis From (2026 to 2034)

Global Maize Seed Market Size

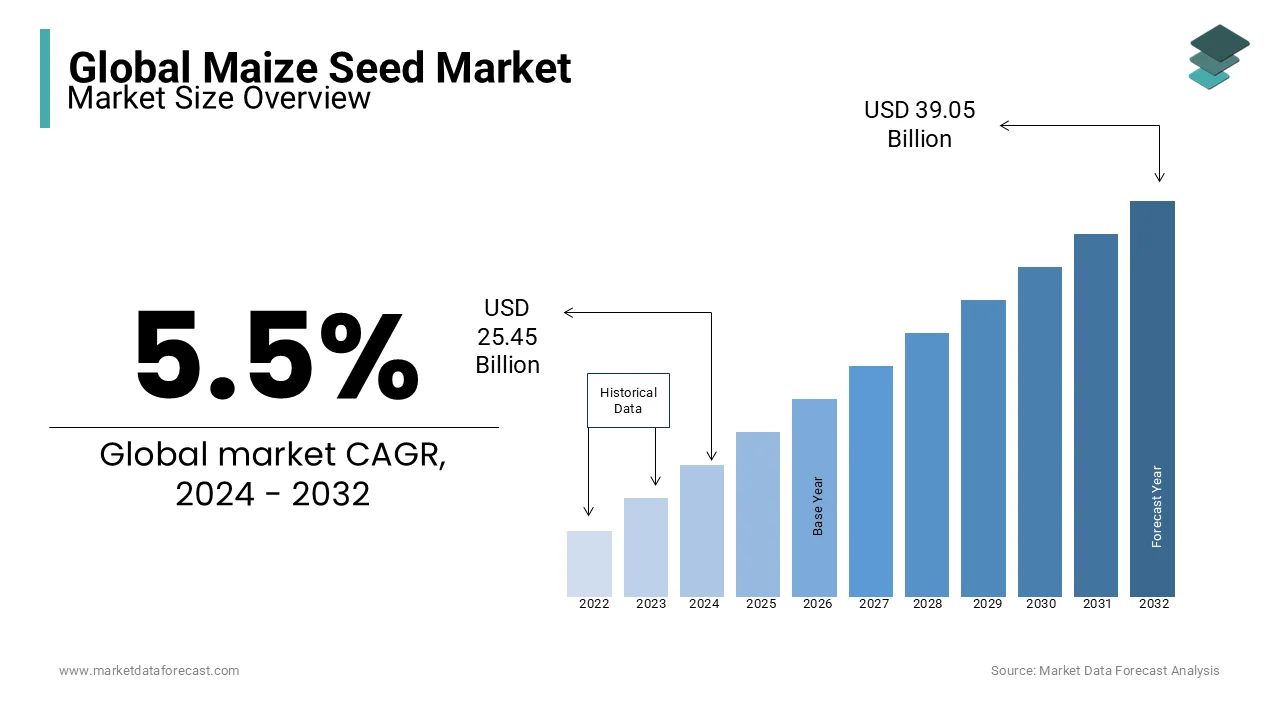

The global maize seed market size was valued at USD 26.85 billion in 2025 and is anticipated to reach USD 28.33 billion in 2026 from USD 43.47 billion by 2034, growing at a CAGR of 5.5% during the forecast period from 2026 to 2034.

A maize seed (or kernel) is the botanical fruit and reproductive unit of the maize plant (Zea mays), acting as a monocotyledonous grain that houses the embryo for a new plant, stored energy, and a protective outer layer. This sector is pivotal to global food security, as maize serves as a staple crop for human consumption, livestock feed, and industrial biofuel production. The market includes various seed types such as hybrid, open pollinated, and genetically modified varieties, each tailored to specific agronomic conditions and yield objectives. According to the Food and Agriculture Organization of the United Nations (FAO), maize is cultivated on roughly 195 to 200 million hectares globally; however, wheat remains the most widely grown cereal crop by land area, spanning over 220 million hectares worldwide. As per the United States Department of Agriculture, global maize production reached 1.2 billion metric tons in the 2023 harvest season, underscoring its critical role in the agricultural supply chain. The International Grains Council indicates that demand for maize as animal feed accounts for nearly 60 percent of total consumption, driven by rising meat production in emerging economies. Furthermore, the Renewable Fuels Association states that over 40 percent of the US maize crop is utilized for ethanol production, highlighting the crop's significance in the energy sector. Climate variability and soil degradation are prompting farmers to adopt high performance seeds with enhanced drought tolerance and disease resistance. The integration of precision agriculture technologies is also influencing seed selection, as farmers seek varieties that optimize input efficiency. This dynamic landscape requires continuous innovation in breeding techniques to address evolving environmental challenges and consumer preferences, ensuring sustainable productivity in the face of growing global population pressures.

MARKET DRIVERS

Rising Global Demand for Livestock Feed and Biofuel Production

The escalating global demand for livestock feed and biofuel production is driving the growth of the Maize Seed Market. This fundamentally shapes planting decisions and seed adoption rates. Rising incomes in developing nations are shifting diets toward higher protein consumption, driving significant growth in the meat and dairy sectors. This expansion relies heavily on maize as the primary energy source for livestock. The United States Department of Agriculture reports that approximately 60 percent of the world’s maize harvest is allocated to animal feed, creating a consistent and robust demand baseline for seed manufacturers. Simultaneously, government mandates for renewable energy have intensified the use of maize for ethanol production. The Renewable Fuels Association indicates that the US alone consumes over 5 billion bushels of corn annually for ethanol, representing a substantial portion of domestic production. This dual demand from the agricultural and energy sectors incentivizes farmers to maximize yields through advanced hybrid seeds. Consequently, seed companies are focusing on developing varieties with higher starch content and biomass potential to meet these specific industrial requirements, thereby propelling market expansion.

Adoption of High Yielding Hybrid and Genetically Modified Seeds

The widespread adoption of high yielding hybrid and genetically modified (GM) seeds is a critical factor accelerating growth in the Maize Seed Market. Farmers are increasingly transitioning from traditional open pollinated varieties to advanced hybrids that offer superior resistance to pests, diseases, and adverse weather conditions. These GM traits, such as Bt technology for insect resistance and herbicide tolerance, significantly reduce crop losses and lower input costs for pesticides and labor. The Food and Agriculture Organization of the United Nations states that hybrid maize varieties can yield up to 20 percent more than conventional seeds under optimal management practices. In regions like Latin America and Asia, where land availability is limited, maximizing output per hectare is essential for profitability. The Brazilian Ministry of Agriculture reports that over 90 percent of maize planted in the country utilizes hybrid or GM seeds, driven by the need for competitive export volumes. Furthermore, advancements in breeding technologies, including marker assisted selection and gene editing, are enabling the development of seeds with enhanced nutritional profiles and stress tolerance. The reliability and productivity offered by modern seed technologies are becoming indispensable as climate change intensifies pressure on agricultural systems. Consequently, this is driving continuous investment and adoption across major producing regions.

MARKET RESTRAINTS

Stringent Regulatory Frameworks for Genetically Modified Organisms

Stringent regulatory frameworks governing genetically modified organisms (GMOs) are a significant restraint to the maize seed market. This is particularly true in regions with cautious public sentiment towards biotechnology. Many countries impose rigorous approval processes for the commercialization of GM seeds, involving extensive safety assessments and environmental impact studies that can delay market entry by several years. According to the European Commission, the cultivation of GM crops remains highly restricted in the European Union, with only one variety currently approved for growth, limiting the market potential for advanced seed technologies in the region. The Cartagena Protocol on Biosafety, ratified by over 170 countries, establishes strict guidelines for the transboundary movement of living modified organisms, creating logistical and legal hurdles for international seed trade. In Africa, despite the potential benefits of GM maize for food security, many nations maintain moratoriums or complex registration requirements. The African Union notes that only a handful of countries have fully embraced commercial GM maize production, citing concerns over biodiversity and long term health effects. These regulatory barriers increase compliance costs for seed developers and discourage investment in certain markets. Furthermore, labeling requirements and traceability mandates add operational complexity to the supply chain. As a result, seed companies often hesitate to introduce their latest innovations in regulated markets. This hesitancy slows the overall pace of technological adoption and restricts market growth in key agricultural economies.

Climate Change Induced Weather Volatility and Crop Failure Risks

Climate change induced weather volatility and the associated risks of crop failure are hampering the expansion of the Maize Seed Market. This undermines farmer confidence and investment capacity. Maize is particularly sensitive to temperature fluctuations and water stress during critical growth stages, making it vulnerable to extreme weather events such as droughts, floods, and heatwaves. The United States Department of Agriculture reports that severe drought conditions in key producing states have led to significant yield reductions in recent years, forcing farmers to reconsider planting decisions. In sub Saharan Africa, the World Bank indicates that erratic rainfall patterns have resulted in frequent crop failures, exacerbating food insecurity and reducing the ability of smallholder farmers to purchase premium seeds. These unpredictable conditions increase the financial risk associated with agriculture, leading some farmers to revert to lower cost, traditional seeds rather than investing in expensive hybrids that may not perform well under stress. Additionally, the emergence of new pest and disease strains due to changing climates further complicates seed performance. The Food and Agriculture Organization of the United Nations highlights that climate related shocks can wipe out entire harvests, discouraging long term commitments to specific seed brands. More resilient varieties are not yet widely available and affordable. Therefore, weather uncertainty remains a persistent barrier to market expansion.

MARKET OPPORTUNITIES

Expansion into Emerging Markets in Asia and Africa

The expansion into emerging markets in Asia and Africa creates a significant opportunity for the Maize Seed Market. This is driven by increasing population growth, urbanization, and government initiatives to enhance food security. These regions are experiencing a shift towards commercial agriculture, with smallholder farmers increasingly adopting improved seed varieties to boost productivity. In India, the Ministry of Agriculture and Farmers Welfare reports that maize acreage has expanded by 15 percent in recent years, supported by policies promoting diversified cropping systems. Governments in countries like Kenya and Nigeria are actively subsidizing certified seeds to reduce reliance on imports and improve local yields. The Alliance for a Green Revolution in Africa states that access to high quality hybrid seeds can double maize yields for smallholder farmers, creating a vast untapped market potential. Furthermore, the rising middle class in Asia is driving demand for poultry and dairy products, indirectly boosting the need for feed maize. Seed companies are responding by developing locally adapted varieties that withstand regional climatic conditions and pest pressures. Firms can capture significant market share in these high-growth regions by establishing strong distribution networks and providing agronomic support. This strategy drives long-term revenue expansion.

Advancements in Precision Breeding and Digital Agriculture Integration

Advancements in precision breeding technologies and the integration of digital agriculture solutions open the door for innovation and differentiation in the Maize Seed Market. Techniques such as CRISPR Cas9 gene editing allow for the rapid development of seeds with specific traits, such as drought tolerance and nitrogen use efficiency, without the regulatory burdens associated with traditional GMOs. According to the National Academies of Sciences Engineering and Medicine, gene edited crops can be developed in half the time required for conventional breeding, accelerating the pipeline for new product launches. Simultaneously, the rise of digital farming platforms enables seed companies to provide data driven recommendations to farmers, optimizing seed selection based on soil health and weather forecasts. Companies are increasingly offering bundled services that combine premium seeds with agronomic advice and insurance products, enhancing customer loyalty. The Global System for Mobile Communications Association notes that increased connectivity in rural areas is facilitating the adoption of these digital solutions. Seed manufacturers can address specific farmer challenges by leveraging biotechnology and data analytics to create high-value propositions. Doing so opens new revenue streams and strengthens competitive advantage in a rapidly evolving market.

MARKET CHALLENGES

Proliferation of Counterfeit and Spurious Seeds

The proliferation of counterfeit and spurious seeds is a major challenge to the Maize Seed Market. This undermines farmer trust and causes significant economic losses. In many developing regions, informal seed markets dominate, where unregulated and low quality seeds are sold at lower prices, often mislabeled as premium hybrids. The Food and Agriculture Organization of the United Nations reports that farmers using fake seeds can experience yield reductions of up to 50 percent, leading to financial distress and reduced willingness to invest in certified products in subsequent seasons. This issue is exacerbated by weak intellectual property enforcement and limited regulatory oversight in rural areas. Seed companies face high costs in combating counterfeiting through legal actions and brand protection measures, which erode profit margins. Furthermore, the presence of inferior seeds distorts market data and hampers the adoption of genuine high performance varieties. The World Bank emphasizes that strengthening seed certification systems and raising farmer awareness are critical but resource intensive tasks. The prevalence of counterfeit seeds continues to hinder market growth and compromise food security efforts in key agricultural regions. This issue will persist until effective mechanisms are in place to eliminate illicit trade.

Consolidation of the Seed Industry and Antitrust Concerns

The ongoing consolidation of the seed industry and resulting antitrust concerns are serious impediments to the Maize Seed Market. This affects competition and innovation dynamics. Over the past decade, a series of mega mergers among major agrochemical and seed corporations has led to a highly concentrated market structure. The United States Department of Justice has launched investigations into these consolidations, citing potential negative impacts on seed prices and research diversity. Critics argue that reduced competition stifles innovation, as dominant players may prioritize profitable traits over diverse agronomic needs. The European Commission has imposed strict conditions on mergers to preserve market competition, requiring divestitures of certain seed assets. This regulatory scrutiny creates uncertainty for industry players and may slow down strategic investments. Furthermore, small and medium sized seed breeders struggle to compete with the vast resources of multinational conglomerates, limiting the diversity of genetic material available in the market. The Organisation for Economic Co operation and Development warns that excessive concentration could lead to higher prices for farmers and reduced resilience in the food system. Balancing economies of scale with competitive fairness remains a complex challenge for policymakers and industry stakeholders alike.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.5% |

| Segments Covered | By Type, Variety, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Syngenta, DuPont, Bayer, CropScience AG, Monsanto Company, Dow AgroSciences, BASSO, Longping High-tech, Limagrain, Shandong Seeds, Nuziveedu Seeds, DLF Trifolium, ShanDongDenghai Seeds, CP Seed, China National Seed, Hefei Fengbao Dekalb, Genetics Pacific Seeds, Jiangsu Dahua |

SEGMENTAL ANALYSIS

By Type Insights

GM Seeds

The genetically modified seeds segment was the largest by occupying a 58.5% of the Maize Seed Market in 2025. This supremacy of the segment was supported by its superior agronomic traits that significantly enhance yield potential and crop resilience. These seeds are engineered to possess specific characteristics such as insect resistance and herbicide tolerance, which directly address major production challenges faced by farmers. The United States Department of Agriculture reports that farms utilizing Bt corn varieties have experienced yield increases of up to 10 percent compared to non GM counterparts, primarily due to reduced damage from pests like the European corn borer. Furthermore, herbicide tolerant varieties allow for more efficient weed management, reducing labor costs and improving overall field hygiene. The Food and Agriculture Organization of the United Nations highlights that in regions with high pest pressure, such as parts of Latin America, GM maize adoption has led to a 25 percent reduction in pesticide applications. This efficiency not only lowers input costs but also minimizes environmental impact, aligning with sustainable farming goals. The consistent performance of GM seeds under varying climatic conditions provides farmers with a reliable return on investment, driving their dominance in commercial agriculture. As global food demand rises, the ability of GM seeds to maximize output per hectare ensures their continued leadership in the market.

Furthermore, the widespread regulatory acceptance of genetically modified seeds in major maize producing nations further cements their dominance in the market. Countries such as the United States, Brazil, and Argentina have established robust regulatory frameworks that facilitate the approval and commercialization of GM crops, encouraging widespread adoption. According to the Brazilian Ministry of Agriculture, over 90 percent of the maize planted in Brazil is genetically modified, driven by favorable government policies and strong support from agricultural research institutions. In the United States, the Department of Agriculture has approved numerous GM maize traits, allowing farmers to stack multiple benefits such as drought tolerance and insect resistance in a single seed. The International Grains Council notes that these regulatory environments have enabled rapid technology diffusion, with GM maize accounting for more than 80 percent of total planting in key exporting countries. This broad acceptance creates a large and stable market base for seed companies, incentivizing continuous innovation and investment in new traits. Additionally, trade agreements between these nations often recognize each other’s safety assessments, facilitating the export of GM maize and reinforcing the economic viability of these seeds. The confidence provided by clear regulatory pathways encourages farmers to adopt GM technologies without fear of market rejection or legal hurdles, sustaining the segment's leading position globally.

Non-GM Seeds

On the other hand, the non-GM seeds segment is predicted to witness the highest CAGR of 8.1% from 2026 to 2034 due to rising consumer preference for natural and organic food products. Increasing health consciousness and concerns about the long term effects of genetic modification have prompted consumers in developed and emerging markets to seek out non GMO labels. The European Union has implemented strict labeling laws for GMOs, which has spurred demand for non GM maize imports to meet domestic consumption needs. Furthermore, major food corporations are committing to sourcing non GMO ingredients to align with brand values and consumer expectations. The Non GMO Project verifies thousands of products, creating a premium market for certified non GM maize. This trend is expanding beyond niche markets into mainstream retail, driving farmers to switch to non GM varieties to capture higher prices. The demand for non-GM maize is expected to accelerate, making it the fastest-growing segment. This trend is driven by awareness spreading through digital media and educational campaigns.

In addition, the potential for premium pricing and access to export markets with strict GMO regulations significantly accelerates the growth of the Non-GM seeds segment. Farmers who cultivate non GM maize can command higher prices due to the specialized nature of the supply chain and the scarcity of verified non GMO supplies. According to the United States Grains Council, non GM maize often trades at a premium of 10 to 15 percent over conventional GM maize in international markets, particularly in Europe and Asia. Japan, a major importer of maize, has stringent labeling requirements that favor non GMO supplies for human consumption, creating a lucrative export channel for producers. The Japanese Ministry of Agriculture Forestry and Fisheries states that over 80 percent of maize imported for direct human use is non GMO, driving dedicated production contracts in exporting countries. Additionally, identity preservation systems are becoming more efficient, allowing suppliers to guarantee the purity of non GM batches, which reduces risk for buyers. The Global Food Safety Initiative emphasizes the importance of traceability in maintaining consumer trust, further supporting the infrastructure for non GM trade. As more countries adopt precautionary principles regarding GMOs, the market for non GM maize expands, offering attractive financial incentives for growers. This economic advantage, combined with growing global demand for transparent food sources, propels the rapid expansion of the non GM seed segment.

By Variety Insights

Hybrids

The hybrid maize seeds segment dominated the global market and accounted for a substantial share in 2025. This dominance of the segment was driven by its significantly higher yield potential and uniformity, which are critical for commercial farming operations. Hybrid varieties are produced by crossing two genetically distinct parent lines, resulting in offspring that exhibit heterosis or hybrid vigor, leading to superior growth and productivity. This yield advantage translates directly into higher profitability for farmers, making hybrids the preferred choice for large scale production. The Food and Agriculture Organization of the United Nations reports that the adoption of hybrid seeds has been a primary driver of global maize production growth over the past five decades. Furthermore, hybrid seeds offer greater uniformity in plant height and maturity, which facilitates mechanized harvesting and reduces post harvest losses. This consistency is essential for industrial users who require standardized raw materials for processing. The reliability of hybrid performance across diverse environmental conditions ensures steady demand, solidifying their position as the leading variety in the global maize seed market.

Moreover, the broad adaptability and enhanced disease resistance features of hybrid maize seeds further drive their domination in the market. Breeders develop hybrids specifically tailored to withstand local stressors such as drought, salinity, and prevalent diseases, ensuring stable production even in challenging environments. According to the International Maize and Wheat Improvement Center, modern hybrid varieties have been engineered to resist major pathogens like northern corn leaf blight and gray leaf spot, which can cause significant yield losses if unchecked. The ability of hybrids to perform well across a wide range of soil types and climatic zones makes them versatile solutions for diverse agricultural landscapes. In India, the Indian Council of Agricultural Research highlights that region specific hybrids have helped stabilize maize production despite erratic monsoon patterns. Additionally, the continuous improvement of hybrid genetics through advanced breeding techniques ensures that new varieties remain effective against evolving pest and disease threats. This ongoing innovation cycle maintains the relevance and effectiveness of hybrid seeds, encouraging farmers to regularly update their seed stock and sustaining the segment's market leadership.

Open Pollinated Varieties

But the open pollinated varieties (OPVs) segment is anticipated to witness the fastest CAGR of 6.6% during the forecast period. This popularity stems from their cost-effectiveness and seed-saving capabilities. They are particularly popular among smallholder farmers in developing regions.Unlike hybrids, OPVs allow farmers to save seeds from one harvest to replant in the next season without significant loss of genetic integrity, reducing annual input costs. The World Bank highlights that for resource constrained farmers, the ability to recycle seeds is a crucial risk management strategy that enhances food security. In remote areas of Asia and Latin America, where distribution networks for commercial hybrid seeds are weak, OPVs remain the most accessible option. The International Fund for Agricultural Development notes that programs promoting improved OPVs have led to yield increases compared to traditional landraces, offering a viable middle ground for farmers unable to afford hybrids. As governments and NGOs focus on inclusive agricultural development, the promotion of high quality OPVs is gaining momentum. This targeted support, combined with the inherent economic advantages for low income farmers, drives the growth of the OPV segment in specific geographic and socioeconomic contexts.

Furthermore, the demand for specific local traits and culinary preferences associated with open pollinated varieties contributes to their growth in specialized market segments. Many traditional maize varieties possess unique flavors, colors, and textures that are highly valued in local cuisines and cultural practices, which hybrid seeds often lack. According to the Native Seeds SEARCH organization, there is a resurgence in the cultivation of heirloom and indigenous maize varieties in North America and Latin America, driven by consumer interest in authentic and diverse food experiences. In Mexico, the Commission for Environmental Cooperation reports that native OPVs are essential for preparing traditional dishes like tortillas and tamales, maintaining cultural heritage and biodiversity. The Slow Food movement and other culinary initiatives are promoting the conservation and use of these varieties, creating niche markets with premium pricing. Furthermore, OPVs are often better adapted to very specific microclimates and low input farming systems, making them resilient choices for organic and agroecological farmers. The Rodale Institute highlights that OPVs can perform well in organic systems where synthetic inputs are restricted, aligning with sustainable agriculture trends. The market for specialized open-pollinated maize is expanding as consumers increasingly value diversity and tradition in their food choices. This segment is experiencing growth despite the overall dominance of hybrids.

By Application Insights

Animal Feed

In 2025, the animal feed segment led the Maize Seed Market by capturing a 64.2% share because of the rapid expansion of global livestock and poultry industries. Maize is a primary energy source in animal diets due to its high starch content and digestibility, making it indispensable for meat, milk, and egg production. The United States Department of Agriculture reports that approximately 60 percent of the world’s maize harvest is used for animal feed, highlighting its critical role in the supply chain. In China, the Ministry of Agriculture and Rural Affairs indicates that the growing middle class is driving a surge in pork and poultry consumption, leading to increased demand for high quality feed maize. Similarly, in Brazil, the Brazilian Association of Animal Protein states that the country’s status as a top exporter of chicken and beef relies heavily on abundant and affordable maize supplies. The intensification of farming practices, where animals are raised in confined operations, further amplifies the need for consistent and nutritious feed formulations. The demand for animal protein continues to climb as populations grow and incomes rise. Consequently, the animal feed segment remains the largest global consumer of maize seeds.

In addition, the shift towards industrial scale feed production and the requirement for high efficiency in animal growth rates further reinforce the dominance of the animal feed segment. Large scale feed mills require consistent quality and volume of maize to formulate balanced rations that optimize animal performance. The National Corn Growers Association states that modern hybrid maize varieties are bred specifically for high starch content and energy density, which are crucial for rapid weight gain in livestock. In Europe, the European Compound Feed Manufacturers Federation highlights that efficiency in feed conversion ratios is a key priority for producers, driving the selection of high performance maize seeds. The reliability of supply chains and the ability to store maize for extended periods without significant quality degradation make it an ideal commodity for industrial feed operations. Furthermore, the integration of maize with other ingredients like soybean meal allows for precise nutritional balancing, supporting healthy and productive animals. The demand for convenient and affordable animal protein is growing due to increasing global population and accelerating urbanization. Consequently, maize continues to play a central role in the animal feed sector.]

Industrial Applications

On the contrary, the industrial applications segment is likely to experience the fastest CAGR of 7.5% over the forecast period. This quick surge of the segment is propelled by the escalating demand for biofuel and ethanol production. Governments worldwide are implementing mandates to blend renewable fuels with gasoline to reduce greenhouse gas emissions and dependence on fossil fuels. According to the Renewable Fuels Association, the United States produces over 15 billion gallons of ethanol annually, consuming more than 5 billion bushels of corn, which accounts for roughly 40 percent of the domestic crop. This sustained demand encourages farmers to allocate more land to maize cultivation, specifically selecting varieties with high starch content suitable for fermentation. The United States Department of Energy highlights that advancements in enzyme technology have improved the efficiency of converting maize starch to ethanol, making it a more competitive fuel source. As climate change mitigation efforts intensify, the role of maize in the energy sector is expected to expand, driving rapid growth in the industrial application segment.

Moreover, the development of biodegradable plastics and industrial starches derived from maize is another key factor accelerating growth in the industrial applications segment. Concerns over plastic pollution are prompting industries to seek sustainable alternatives, with maize based polylactic acid (PLA) emerging as a viable biodegradable material. According to the European Bioplastics Association, the global production capacity for bioplastics is expected to double in the next five years, with maize starch being a primary feedstock. In the packaging industry, major corporations are committing to using compostable materials, driving demand for maize derived polymers. The United States Department of Agriculture reports that industrial uses of maize, including starches for adhesives, textiles, and paper, are diversifying and expanding. In Asia, the Chinese Ministry of Industry and Information Technology supports the development of bio based materials as part of its green manufacturing initiatives. The versatility of maize starch allows it to be used in a wide range of industrial processes, from pharmaceuticals to construction materials. As technology advances and costs decrease, the adoption of maize based industrial products is becoming more widespread. This diversification away from traditional food and feed uses opens new revenue streams for maize producers, fueling the fastest growth in the industrial application segment.

REGIONAL ANALYSIS

North America Market Analysis

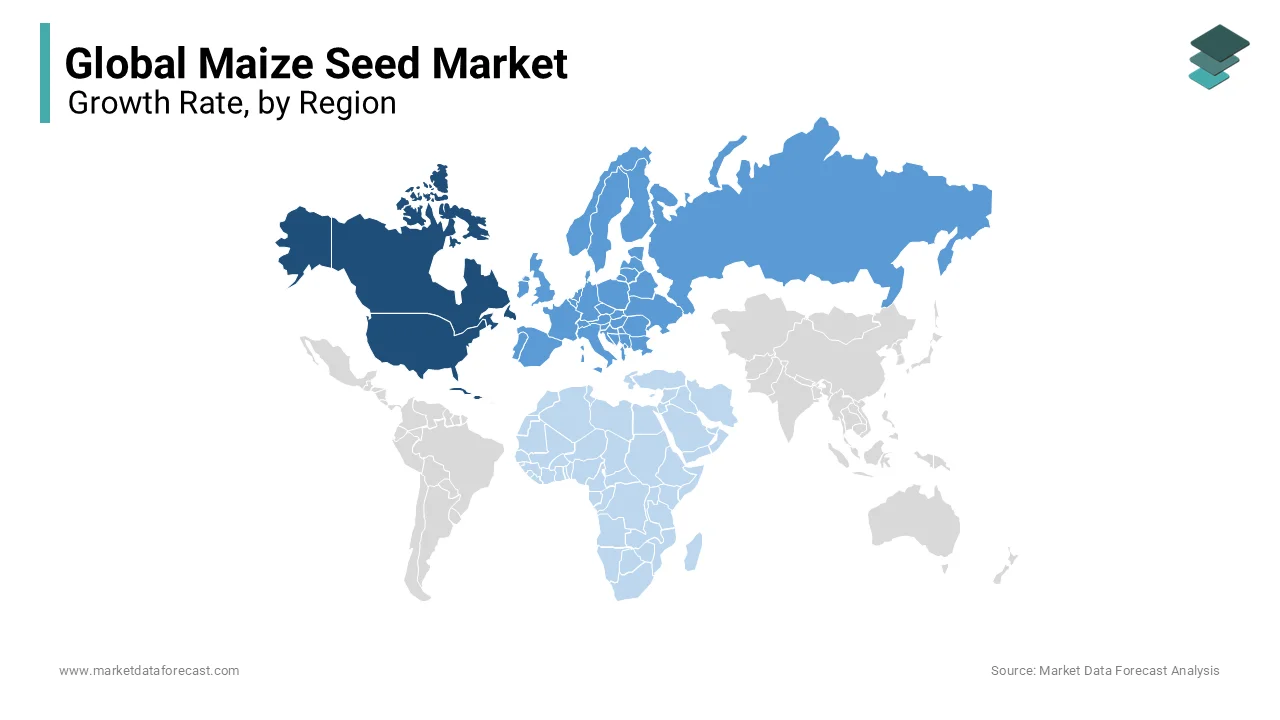

North America was the top performer in the global Maize Seed Market and accounted for a 49.6% share in 2025. This position of the region was driven by advanced agricultural practices, high adoption of genetically modified seeds, and robust infrastructure. The United States is the world’s largest producer and exporter of maize, driven by strong demand from the animal feed and ethanol industries. The presence of leading seed companies such as Corteva Agriscience and Bayer fosters continuous innovation and product development. The Renewable Fuels Association states that the US ethanol industry consumes a significant portion of the maize crop, providing a stable market for growers. Canada also contributes to the regional market, with a focus on high quality feed maize for its livestock sector. The Canadian Grain Commission reports that maize production in Ontario and Quebec has increased due to favorable weather conditions and improved seed varieties. Government subsidies and crop insurance programs further support farmer investment in premium seeds. The region’s emphasis on precision agriculture and data driven farming enhances seed performance and yield efficiency. North America leads in biotechnology and agricultural productivity, driving its dominant position in the global maize seed market. This position is further solidified by strong domestic consumption and export capabilities.

Europe Market Analysis

Europe plays a key role in the global Maize Seed Market due to a mix of conventional and non GMO seed usage due to strict regulatory frameworks. Genetically modified maize cultivation is limited in the European Union. However, there is substantial demand for non-GMO maize for food and feed purposes. France and Romania are the largest maize producers within the EU, relying heavily on high performing hybrid seeds to maximize yields. The European Seed Association highlights that breeders are focusing on developing varieties with enhanced disease resistance and drought tolerance to cope with climate variability. The European Environment Agency notes that sustainable farming practices are influencing seed selection, with increasing interest in varieties that require fewer chemical inputs. In Eastern Europe, countries like Hungary and Poland are expanding maize acreage to support growing livestock sectors. The Common Agricultural Policy provides financial support for farmers adopting sustainable practices, indirectly influencing seed choices. The European market is shifting towards specialized hybrid and non-GMO seeds, driven by growing consumer preference and tightening environmental regulations. This trend creates niche opportunities for seed companies capable of navigating the complex regulatory landscape.

Asia Pacific Market Analysis

Asia Pacific was the second largest region as well as the fastest growing region in the global Maize Seed Market in 2025 because of rising population, increasing meat consumption, and government initiatives to boost agricultural productivity. China and India are the key markets, with China being the second largest maize producer globally. According to the Ministry of Agriculture and Rural Affairs of China, maize acreage has expanded significantly to meet demand from the livestock and industrial sectors, with a strong focus on hybrid seed adoption. In Southeast Asia, countries like Vietnam and Indonesia are increasing maize cultivation for animal feed, reducing reliance on imports. The Food and Agriculture Organization of the United Nations highlights that smallholder farmers in the region are gradually transitioning from open pollinated varieties to hybrids to improve incomes. Government subsidies for seeds and fertilizers in countries like Thailand and the Philippines are accelerating this transition. The rising middle class in the region is driving demand for poultry and pork, further boosting the need for feed maize. Agricultural infrastructure is improving and awareness of modern farming techniques is spreading across the Asia Pacific region. Thus, this presents substantial growth opportunities for the maize seed market, driven by both volume expansion and technology adoption.

Latin America Market Analysis

Latin America holds a major share of the global maize seed market, with Brazil and Argentina leading the region. These two nations are major exporters of maize and among the earliest adopters of genetically modified seeds. Brazil has become a powerhouse in maize production, with a significant portion of its crop grown in the safrinha or second season. According to the Brazilian Ministry of Agriculture, over 90 percent of maize planted in Brazil is genetically modified, utilizing advanced traits for insect resistance and herbicide tolerance. The Argentine Seed Chamber reports that Argentina also has high GM adoption rates, driven by the efficiency gains and export competitiveness they provide. The region’s favorable climate allows for multiple cropping cycles, maximizing land use efficiency. The Inter American Institute for Cooperation on Agriculture highlights that investment in research and development by multinational seed companies has introduced varieties tailored to local conditions, such as drought tolerance. In Mexico, while native maize varieties are culturally significant, commercial production for feed and industry increasingly relies on hybrid seeds. The United States Department of Agriculture notes that Latin American exports play a crucial role in global supply chains, particularly for Asian markets. Latin America continues to expand its agricultural frontier and adopt digital farming tools. Consequently, the region remains a critical driver of growth and innovation in the global maize seed market.

Middle East and Africa Market Analysis

The Middle East and Africa region is likely to expand notably in the global Maize Seed Market from 2026 to 2034 due to a mix of subsistence and emerging commercial farming. Sub Saharan Africa is a key focus area, where maize is a staple food for millions. According to the Food and Agriculture Organization of the United Nations, maize production in Africa is constrained by low yields, but initiatives to promote improved hybrid and open pollinated varieties are showing positive results. In South Africa, the largest producer in the region, commercial farmers widely adopt genetically modified hybrid seeds, contributing significantly to regional supply. In Kenya and Ethiopia, government programs are distributing drought tolerant varieties to combat climate change impacts. The World Bank reports that increasing urbanization is driving demand for processed maize products and animal feed, stimulating market growth. In the Middle East, countries like Egypt import significant quantities of maize for feed, influencing regional trade dynamics. As infrastructure improves and investment in agricultural research increases, the region is poised for gradual but steady growth in the maize seed market, driven by the need for food security and resilience against environmental challenges.

COMPETITIVE LANDSCAPE

The global maize seed market features intense competition among multinational corporations and regional specialists who strive for technological superiority. Leading entities such as Bayer Corteva and Syngenta dominate the landscape through extensive research networks and broad distribution channels. These companies continuously launch new hybrid varieties with enhanced traits to meet the evolving demands of farmers worldwide. Competition drives significant investment in biotechnology and digital farming tools that provide integrated solutions for crop management. Regional players also contribute to the competitive dynamics by offering locally adapted seeds that cater to specific climatic conditions. Strategic alliances and acquisitions are common tactics used to consolidate market positions and access new territories. The focus on sustainability and climate resilience further intensifies rivalry as firms seek to differentiate their offerings. Innovation in seed treatment and precision agriculture technologies remains a key battleground for capturing farmer loyalty. This competitive environment fosters rapid advancements in seed genetics and agronomic practices globally. The market structure encourages constant improvement in yield potential and stress tolerance metrics. As a result, farmers benefit from a wide array of high performance options that support food security goals.

KEY MARKET PLAYERS

Some of the market players dominate the global market.

- Syngenta

- DuPont

- Bayer

- CropScience AG

- Corteva Agriscience

- Monsanto Company

- Dow AgroSciences

- BASSO

- Longping High-tech

- Limagrain

- Shandong Seeds

- Nuziveedu Seed

- DLF Trifolium

- ShanDongDenghai Seeds

- CP Seed

- China National Seed

- Hefei Fengbao Dekalb

- Genetics Pacific Seeds

- Jiangsu Dahua

Top Players In The Market

- Bayer CropScience stands as a leading entity in the global maize seed sector through its extensive Dekalb brand portfolio. The company focuses heavily on integrating advanced genetic traits with digital farming solutions to enhance crop yield and resilience. Recent actions include the opening of a new maize seed facility to boost local production capabilities. Bayer also launched its Maize Product Guide featuring advanced genetics and seed treatment technologies to protect young roots. These initiatives demonstrate a strong commitment to expanding regional access while improving product performance through continuous innovation. The company leverages its integrated crop science division to provide holistic solutions that address pest pressure and environmental stressors effectively. This strategic approach strengthens its position by offering farmers comprehensive tools for sustainable agriculture and improved productivity outcomes globally.

- Corteva Agriscience maintains a prominent role in the maize seed market via its renowned Pioneer brand and extensive research capabilities. The company prioritizes developing drought tolerant and high yielding hybrid varieties to meet diverse agricultural needs across different geographies. Corteva consistently publishes annual PACTS trial results to provide transparent performance data for growers and advisors. These efforts highlight its dedication to scientific excellence and customer centric innovation. Corteva reinforces trust among farmers and secures its competitive edge by focusing on localized solutions. Furthermore, they leverage robust field trial data in the evolving global seed landscape.

- Syngenta Group plays a critical part in the global maize seed industry through its strong presence in both developed and emerging markets. The company emphasizes breeding innovations and strategic acquisitions to expand its genetic portfolio and regional footprint. These moves illustrate a clear strategy to bolster supply chain efficiency and product availability. Syngenta combines advanced breeding techniques with expanded manufacturing capabilities. By doing so, the company ensures it remains a key provider of high-quality maize seeds worldwide.

Top Strategies Used By The Key Market Participants

Key players in the maize seed market primarily focus on intensive research and development to create superior hybrid varieties. Companies invest heavily in biotechnology to introduce traits such as drought tolerance and pest resistance. Strategic mergers and acquisitions allow firms to expand their geographic reach and diversify product portfolios significantly. Partnerships with local distributors and agricultural organizations help enhance market penetration in emerging regions. Digital agriculture integration is another major strategy where firms bundle seeds with data analytics platforms. These approaches enable companies to offer comprehensive solutions that improve farm productivity and sustainability. Continuous innovation in seed treatment technologies also serves as a vital strategy to protect crop health. Market leaders adopt these methods to maintain their competitive advantage. This approach also drives overall industry growth effectively.

MARKET SEGMENTATION

This research report on the global maize seed market is segmented and sub-segmented based on the Type, Variety, Application, and Region.

By Type

- Conventional Seeds

- GM seeds

- Non-GM Seeds

By Variety

- Open Pollinated

- Hybrid

By Application

- Food

- Animal Feed

- Biofuel

- Ethanol

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

What is the maize seed market?

The maize seed market covers the production and sale of hybrid, GM, and conventional seeds used for corn cultivation.

What is driving the growth of the maize seed market?

Rising demand for animal feed, biofuels, and high-yield crops is driving market growth.

Which type of maize seed is most commonly used?

Hybrid maize seeds dominate due to higher yield, disease resistance, and stress tolerance.

How does climate change affect the maize seed market?

Climate variability increases demand for drought- and heat-tolerant maize seed varieties.

What are the major applications of maize seeds?

Maize seeds are used for food, animal feed, ethanol production, and industrial starch.

Which regions lead the maize seed market?

North America and Asia-Pacific lead due to large cultivation areas and advanced farming practices.

What are the key challenges in the maize seed market?

High seed costs, regulatory restrictions on GM seeds, and climate risks are major challenges.

How do hybrid seeds benefit maize farmers?

They improve productivity, ensure uniform crops, and enhance resistance to pests and diseases.

Are non-GMO maize seeds in demand?

Yes, demand is growing in regions with strict GMO regulations and organic farming practices.

What is the future outlook of the maize seed market?

The market is expected to grow steadily with advancements in seed breeding and precision agriculture.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com